Ethylene Carbonate Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

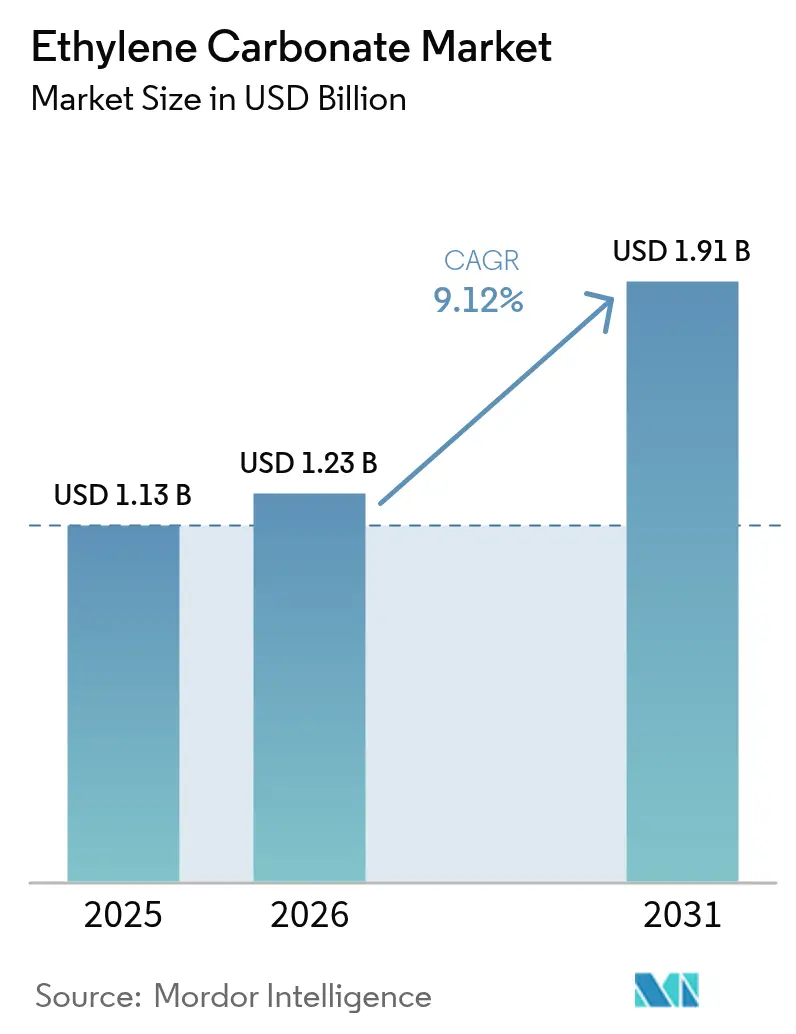

| Market Size (2026) | USD 1.23 Billion |

| Market Size (2031) | USD 1.91 Billion |

| Growth Rate (2026 - 2031) | 9.12% CAGR |

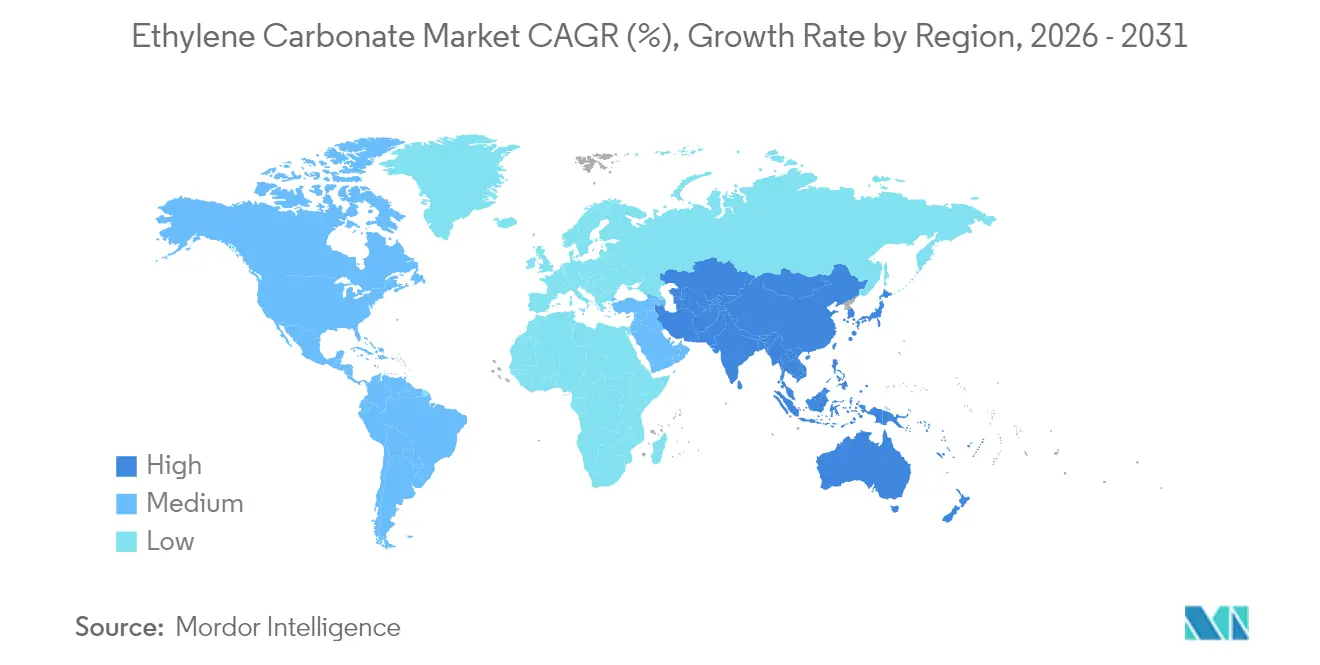

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ethylene Carbonate Market Analysis by Mordor Intelligence

The Ethylene Carbonate market size is expected to grow from USD 1.13 billion in 2025 to USD 1.23 billion in 2026 and is forecast to reach USD 1.91 billion by 2031 at 9.12% CAGR over 2026-2031. Demand is propelled by the compound’s irreplaceable role in lithium-ion battery electrolytes, where it promotes the solid-electrolyte interphase (SEI) that protects graphite anodes and enables higher energy densities. Asia-Pacific’s integrated petrochemical and battery ecosystems underpin both cost leadership and supply security, while North American and European producers compete on purity grades and regulatory compliance advantages. Integrated supply chains that span ethylene oxide feedstocks to ready-to-use electrolyte blends are becoming decisive competitive levers. At the same time, feedstock volatility and toxicity classifications inject cost and compliance risks that favor large, vertically integrated suppliers able to amortize safety and sustainability investments.

Key Report Takeaways

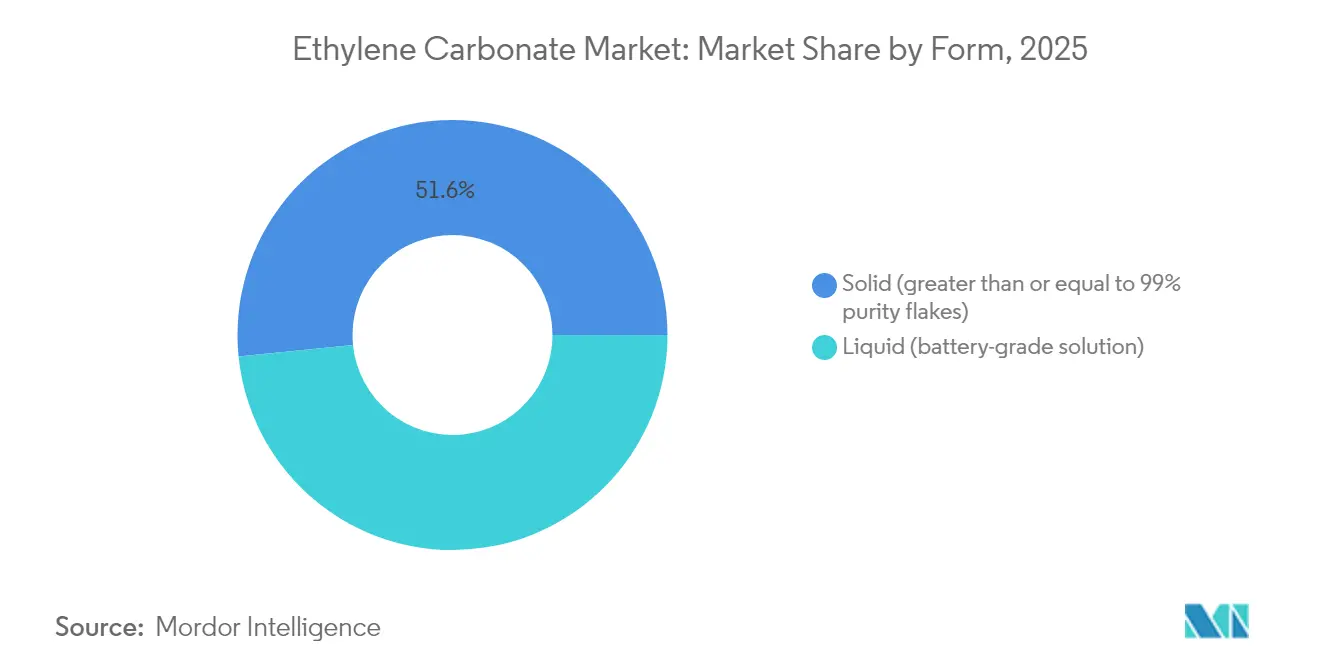

- By form, solid ethylene carbonate commanded 51.60% revenue in 2025, whereas liquid battery-grade solutions are tracking a 9.55% CAGR to 2031.

- By application, lithium-ion batteries accounted for 46.70% of the ethylene carbonate market share in 2025 and are projected to grow at an 11.22% CAGR through 2031.

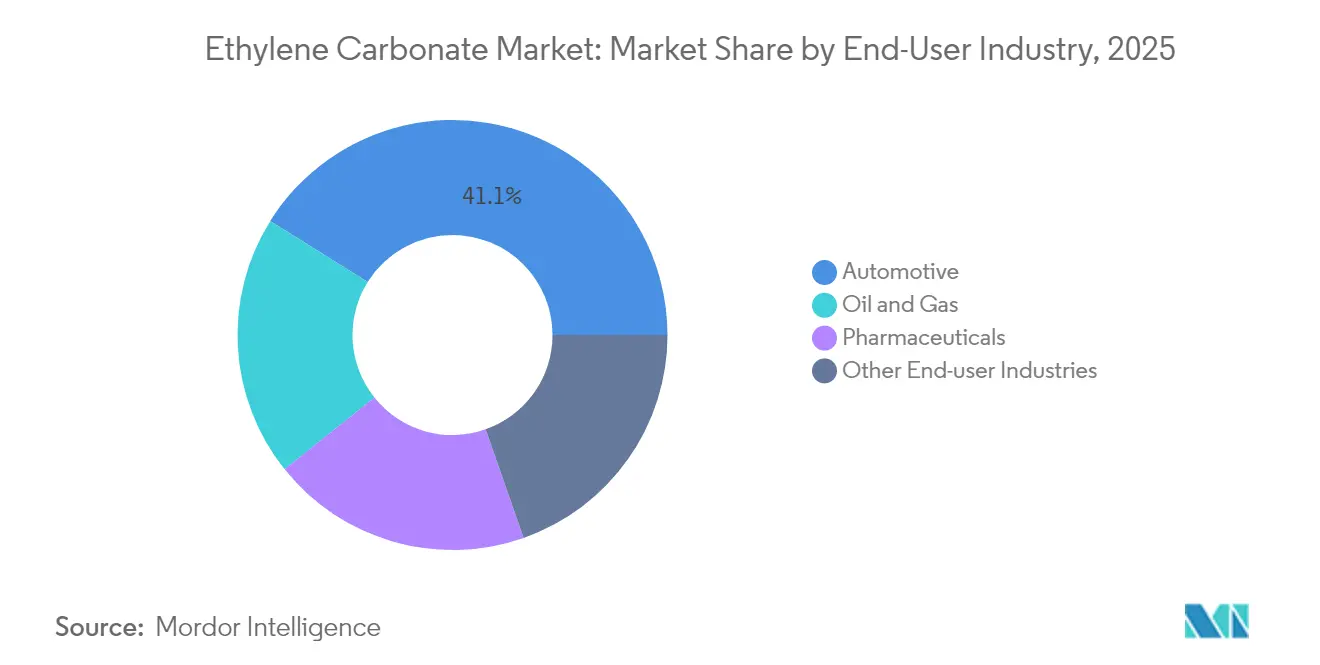

- By end-user industry, automotive led with 41.10% of 2025 demand, while its electrification push is set to expand at a 10.42% CAGR to 2031.

- By geography, Asia-Pacific controlled 54.05% of global revenues in 2025 and is earmarked for a 9.48% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ethylene Carbonate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for high-energy-density Li-ion batteries in EVs | +3.20% | Global, with APAC leading | Medium term (2-4 years) |

| Growth in premium industrial & automotive lubricants | +1.80% | North America & Europe primarily | Long term (≥ 4 years) |

| Expansion of Asian battery-manufacturing capacity | +2.70% | APAC core, spill-over to global supply chains | Short term (≤ 2 years) |

| Favourable regulations for safer electrolyte solvents | +1.10% | Europe & North America | Medium term (2-4 years) |

| Emergence of solid-state battery precursor requirements | +0.90% | Global, early adoption in Japan & South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for High-Energy-Density Li-ion Batteries in EVs

Global electric-vehicle rollouts require electrolyte systems that sustain cell voltages above 4.4 V while enabling fast-charge performance. Ethylene carbonate forms a stable SEI layer that protects graphite anodes from solvent co-intercalation, a property validated in Skoltech research showing markedly lower capacity fade versus propylene carbonate alternatives. Automakers and cell makers therefore embed long-term offtake clauses into supply contracts, shielding demand from short-term price swings. The cumulative effect adds 3.20 percentage points to the forecast CAGR as battery deployments scale across passenger cars, commercial fleets, and stationary storage.

Growth in Premium Industrial & Automotive Lubricants

High-performance lubricants in metal-working, engine oils, and wind-turbine gearboxes increasingly specify polar carbonate additives that maintain viscosity at temperatures above 200 °C. Laboratory data on oleochemical carbonates confirm that the short carbon chain of ethylene carbonate confers superior solubility and film-forming properties, enhancing extreme-pressure resistance[1]Robert O. Dunn et al., “Physical Properties of Oleochemical Carbonates,” Journal of the American Oil Chemists' Society, springer.com . OEM warranty extensions to 20,000 km oil-change intervals amplify additive loading per formulation, translating into steady, margin-accretive demand beyond the battery sector.

Expansion of Asian Battery-Manufacturing Capacity

China is slated to add 26 million tons of annual ethylene capacity by 2027, lowering feedstock costs for downstream carbonate producers. Regional makers leverage just-in-time deliveries to neighboring gigafactories, cutting logistics costs that erode the competitiveness of trans-Pacific shipments. Mitsubishi Chemical’s 2,000 t/year gamma-butyrolactone debottlenecking and BASF’s USD 10 billion Zhanjiang complex illustrate how incumbents co-locate upstream intermediates with battery-grade carbonate units[2]Mitsubishi Chemical Group, “Expansion of Gamma-Butyrolactone Production Capacity,” mcgc.com. Resulting supply-security premiums underpin 2.70 percentage points of incremental CAGR.

Emergence of Solid-State Battery Precursor Requirements

Next-generation solid-state cells deploy polymer electrolytes that incorporate ethylene carbonate derivatives to boost ionic conductivity and interfacial stability. Pilot-scale lines in Japan and South Korea already stipulate greater than or equal to 99.9% purity, favoring suppliers with advanced fractional-crystallization technology. Though volumes remain small to 2027, design-in cycles in consumer electronics foreshadow larger automotive uptake post-2028, adding 0.90 percentage points to the long-term growth curve.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health & environmental toxicity classification of EC | -1.40% | Global, stricter in Europe & North America | Medium term (2-4 years) |

| Volatility in ethylene-oxide feedstock prices | -2.10% | Global, particularly affecting integrated producers | Short term (≤ 2 years) |

| Substitution by dimethyl & propylene carbonate blends | -1.80% | Global, led by cost-sensitive applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Ethylene-Oxide Feedstock Prices

Feedstock costs constitute a significant portion of variable production costs for non-integrated manufacturers. A substantial share of global ethylene capacity is at risk of closure during the current market downturn, intensifying price volatility and reducing carbonate converters' profit margins. Producers with captive ethylene-oxide units hedge exposure, but merchants supplying smaller downstream players experience margin whiplash, dragging the sector CAGR by 2.10 percentage points.

Substitution by Dimethyl & Propylene Carbonate Blends

Dimethyl carbonate offers lower viscosity and a cleaner toxicological profile, prompting formulators in adhesives, coatings, and select lubricants to trial 20-30% substitution ratios[3]Ayoub O. G. Abdalla and Dong Liu, “Dimethyl Carbonate as a Promising Oxygenated Fuel,” MDPI Energies, mdpi.com . Propylene carbonate blends similarly cut overall solvent costs in large-volume industrial applications. Although high-energy battery chemistries still require ethylene carbonate, the loss of incremental demand in cost-sensitive niches subtracts 1.80 percentage points from the market CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Supply Chain Convenience Tilts Growth Toward Liquids

The solid segment retained leadership with 51.60% revenue in 2025, supported by a decades-old logistics network that ships greater than or equal to 99% purity flakes worldwide for on-site dissolution. Liquid battery-grade solutions, however, are expanding at a 9.55% CAGR to 2031 because they arrive moisture-controlled and filtered to less than 20 ppm water, eliminating in-plant handling steps that risk contamination. This structural pivot lets suppliers capture processing spreads while enabling automated filling in gigafactory electrolyte lines. Solid products will remain relevant for bulk industrial uses where drum or bag handling is not rate-limiting, preserving a sizeable, slow-growing base.

The performance gap between 99.0% technical-grade solids and 99.7% battery-grade liquids is narrowing as crystallization and ion-exchange polishing are embedded upstream, raising the addressable share of liquids in non-battery segments. US-based Huntsman’s recent investment in a Texan E-GRADE purification line exemplifies how Western suppliers defend market share with higher-purity, value-added volumes. Asian competitors counter with bulk ISO-tank shipments that cut freight costs by 10-12%, intensifying form-factor competition through 2031.

By Application: Battery-Led Dominance Anchors Future Revenue

Lithium-ion batteries contributed 46.70% of 2025 consumption and are forecast to expand at an 11.22% CAGR. The chemistry’s reliance on ethylene carbonate stems from its ability to form a high-impedance SEI at voltage plateaus above 4.4 V, a prerequisite for nickel-rich NCA and NCM cathodes used in long-range EV packs. Grid-scale energy storage projects are beginning to mirror this formulation, extending demand beyond mobility into peak-shaving and renewable integration.

Lubricant formulations represent a significant portion of ethylene carbonate volumes, due to their ability to dissolve anti-wear additives at high temperatures. Yet their mid-single-digit growth lags battery demand, constraining their influence on overall pricing. Specialty medical and pharmaceutical uses, while less than 5% of tonnage, command the highest gross margins due to stringent endotoxin and heavy-metal specifications. The dispersion of growth rates across applications underscores why producers allocate incremental capacity toward battery-grade purification modules that deliver faster payback periods.

By End-User Industry: Automotive Electrification Steers Volume Trajectory

Automotive OEMs, spanning passenger cars to light-duty delivery vans, absorbed 41.10% of global volume in 2025. Their aggregated offtake is on track for a 10.42% CAGR. Battery manufacturers in China, Europe, and the United States synchronize carbonate call-offs via vendor-managed inventory programs that penalize late deliveries, nudging suppliers toward regional buffer stock and localization of final filtration to ppm moisture.

Industrial equipment and renewable energy machinery represent a significant end-user segment, utilizing premium lubricants and coolants to increase component longevity under high mechanical stress. Pharma-grade ethylene carbonate retains its niche in controlled drug-release matrices and contrast-media stabilizers, posting low-to-mid-single-digit growth. The end-market portfolio provides diversification, but the dominance of automotive electrification means that any slowdown in EV adoption would ripple across supply-demand balances within one to two quarters.

Geography Analysis

Asia-Pacific’s integrated chemical-to-battery corridor yielded 54.05% of global revenues in 2025 and is expected to clock a 9.48% CAGR to 2031, buoyed by 26 million t of planned ethylene cracker capacity in mainland China that underpins cost leadership. Local carbonate producers typically site plants near gigafactories, shaving 2-3 days off transit times and embedding on-call quality-assurance labs that align with automotive traceability protocols. Japan’s ethylene output hit a 35-year low in 2024, reflecting a shift toward high-value specialty chemicals even as domestic battery projects grow, which widens China’s regional production advantage.

North America remains structurally short in battery-grade carbonate despite Huntsman’s position as the largest domestic supplier. The Inflation Reduction Act’s incentives for US cell factories have triggered multi-year offtake agreements that partially hedge trans-Pacific supply risks. Feedstock costs, however, are higher because shale-gas-advantaged ethane crackers prioritize polyethylene, requiring carbonate makers to secure ethylene oxide at index-linked premiums.

Europe’s stringent REACH environment raises compliance costs yet secures a premium for fully documented material. BASF’s pledge to power six US care-chemical sites entirely with renewable electricity underscores how sustainability credentials are being deployed globally as soft differentiators in mature markets. Meanwhile, Middle East & Africa and South America collectively account for smaller share of volume but present upside through petrochemical diversification programs and growing EV import penetration. Logistics flexibility—using ISO tanks and regional stocking hubs—remains the route to profitable share capture in these emerging destinations.

Competitive Landscape

Competitive intensity sits at a moderately consolidated level. The top five firms leverage vertical integration from ethylene oxide to solvent blends, enabling cost efficiencies and supply assurances that smaller formulators struggle to match. BASF’s USD 10 billion Zhanjiang project integrates ethylene, ethylene oxide, and carbonate units within a single coastal zone to trim inter-plant logistics. Huntsman’s newly commissioned Texan E-GRADE line delivers 99.9% purity liquids into North American EV programs, demonstrating how purity thresholds are being raised as cell chemistries push higher voltages.

Asian specialists such as Guangzhou Tinci expand capacity through tolling partnerships that minimize capital outlay and allow agile response to spot demand spikes. Patent filings covering non-aqueous electrolyte blends and solid-state precursors reveal strategic R&D investments aimed at locking in future royalties. Western incumbents counter with sustainability and circular-economy initiatives, for example Clariant’s cooperation with OMV to cut the carbon footprint of ethylene derivatives. While cost remains a gating factor in commodity-grade volumes, procurement teams increasingly weigh traceable, low-carbon credentials when awarding long-term contracts, slightly diluting pure price competition.

Over the next five years, competitive advantage will stem from (1) proximity to gigafactories, (2) ability to meet greater than or equal to 99.9% purity at scale, and (3) demonstrable reductions in Scope 1-3 emissions. Players that excel along all three vectors will capture the majority of incremental demand, whereas non-integrated converters face margin compression, particularly when feedstock volatility re-emerges. Consolidation through joint ventures and targeted acquisitions therefore remains a likely scenario, especially in Europe where REACH compliance costs strain smaller balance sheets.

Ethylene Carbonate Industry Leaders

BASF SE

Huntsman International LLC

Mitsubishi Chemical Group Corporation

OUCC

Shida Shenghua New Materials Group Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2024: Clariant and OMV have announced their strategic collaboration aimed at reducing the carbon footprint of ethylene and its derivatives, including ethylene oxide. The initiative is expected to drive market growth for ethylene carbonate, as this ethylene oxide derivative aligns with environmental sustainability requirements.

- May 2024: Asahi Kasei, Mitsui Chemicals, and Mitsubishi Chemical have initiated a joint study to achieve carbon neutrality in ethylene production in western Japan by 2050, focusing on biomass feedstock and low-carbon fuels. This effort is expected to enhance sustainability in the ethylene carbonate market, driving eco-friendly innovations and market growth.

Global Ethylene Carbonate Market Report Scope

Ethylene carbonate (C3H6O3) is an organic substance. It is a colorless, odorless, extremely polar solvent and chemical producer. Electrolyte additives like ethylene carbonate improve lithium-ion battery performance and stability. It also produces urethane plastics and cellulose derivatives as an intermediary. The ethylene carbonate market is segmented by application, end-user industry, and region. By application, the market is segmented into lithium batteries, lubricants, medical products, intermediates and agents, and other applications. By end-user industry, the market is segmented into automotive, pharmaceutical, oil and gas, and other end-user industries. The report also covers the size and forecasts for the ethylene carbonate market in 15 countries across major regions. The market sizing and forecasts for each segment are based on volume (kilotons) and revenue (USD million).

| Solid (greater than or equal to 99% purity flakes) |

| Liquid (battery-grade solution) |

| Lithium-ion Batteries |

| Lubricants |

| Medical Products |

| Intermediates and Agents |

| Other Applications |

| Automotive |

| Pharmaceuticals |

| Oil and Gas |

| Other End-user Industries |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Form | Solid (greater than or equal to 99% purity flakes) | |

| Liquid (battery-grade solution) | ||

| By Application | Lithium-ion Batteries | |

| Lubricants | ||

| Medical Products | ||

| Intermediates and Agents | ||

| Other Applications | ||

| By End-user Industry | Automotive | |

| Pharmaceuticals | ||

| Oil and Gas | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is driving the fastest growth in the ethylene carbonate market?

Demand from lithium-ion batteries, especially in electric vehicles, is expanding at an 11.22% CAGR and remains the single largest growth engine.

Which region dominates global consumption?

Asia-Pacific held 54.05% of 2025 revenues, benefiting from integrated ethylene-to-battery supply chains and new cracker capacity coming online through 2027.

How will solid-state batteries influence ethylene carbonate demand?

While volumes remain small to 2027, ultra-high-purity grades are already being specified as polymer-electrolyte precursors, adding long-term incremental demand.

What supply risks affect ethylene carbonate producers?

Ethylene-oxide feedstock volatility and potential substitution by dimethyl or propylene carbonate blends can pressure margins and erode share in cost-sensitive segments.

How consolidated is the competitive landscape?

The top five suppliers control roughly 51% of global volume, giving the market a moderately consolidated concentration.

Page last updated on: