1,3-Propanediol (PDO) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 435.12 Million |

| Market Size (2031) | USD 620.61 Million |

| Growth Rate (2026 - 2031) | 7.36% CAGR |

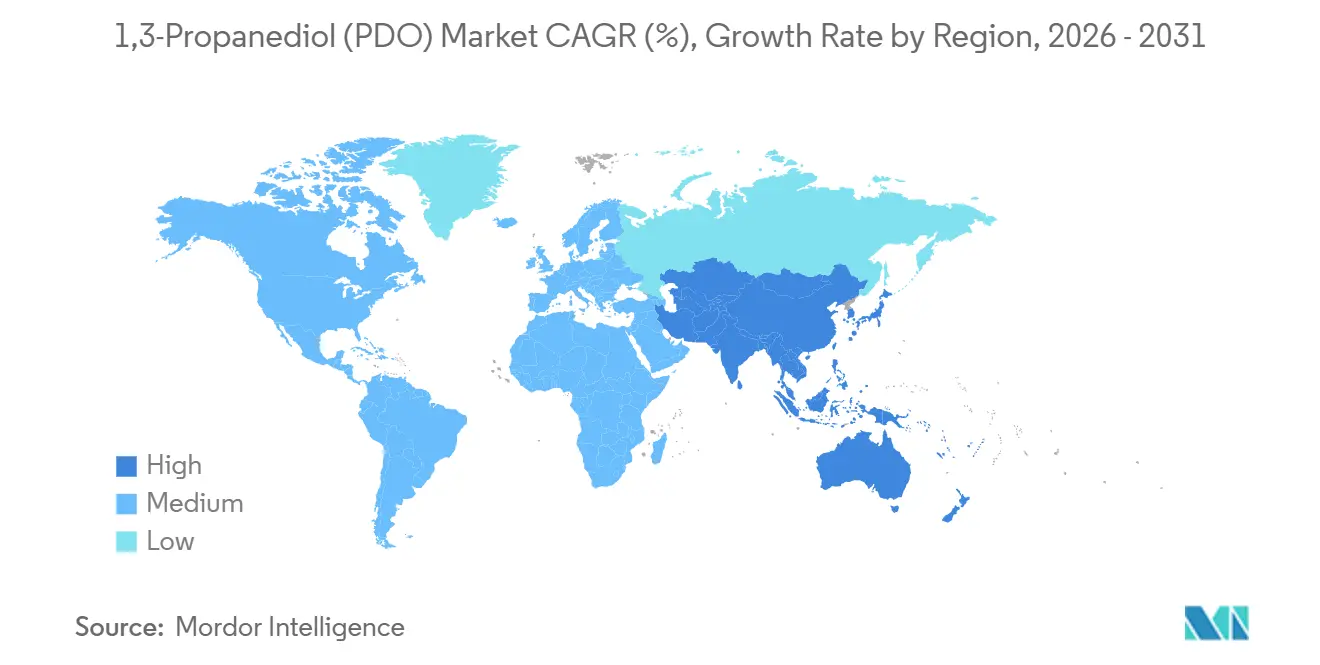

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

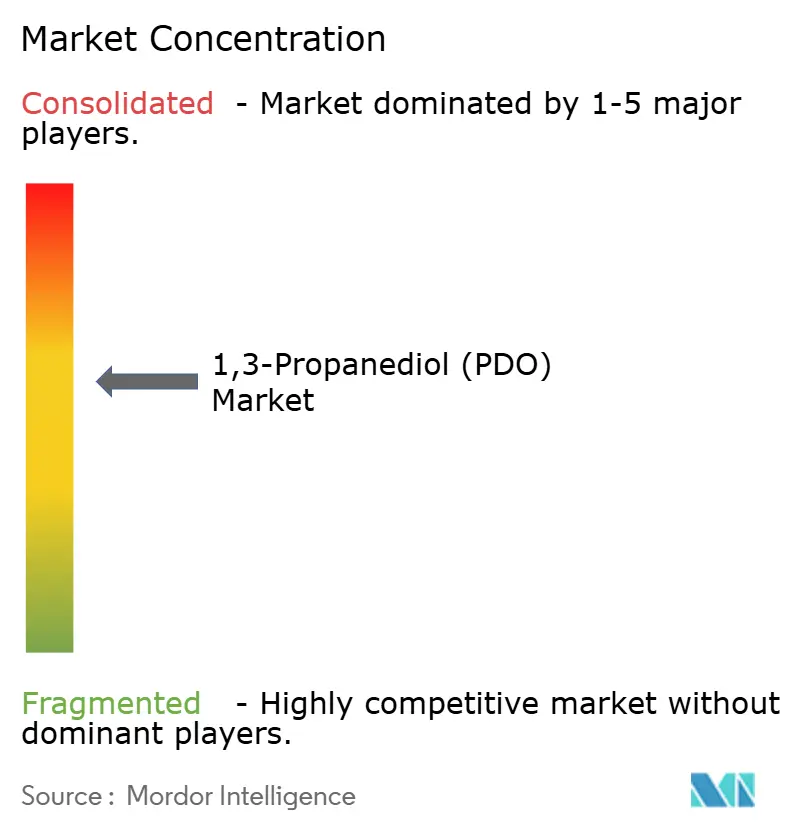

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

1,3-Propanediol (PDO) Market Analysis by Mordor Intelligence

The 1,3-Propanediol Market size is estimated at USD 435.12 million in 2026, and is expected to reach USD 620.61 million by 2031, at a CAGR of 7.36% during the forecast period (2026-2031). Rapid penetration of bio-based polymers, sustained premium pricing for high-purity grades, and automotive electrification are amplifying structural demand for specialty diols. Policy incentives in the United States, the European Union, and China are compressing the historical green premium, which fell from 25% in 2023 to nearly 15% by late-2025. Meanwhile, volatility in corn and crude-glycerol prices continues to test margins for fermentation players, although process optimizations are curbing feedstock intensity by 5%-8%. Competitive intensity is inching upward as Chinese glycerol-route producers undercut industrial-grade prices, prompting Western incumbents to sharpen their focus on cosmetic, pharmaceutical, and polymer applications that reward sustainability credentials. The 1,3-propanediol (PDO) market is therefore evolving into a two-tier ecosystem that pairs a volume-oriented industrial base with an insulated specialty tier.

Key Report Takeaways

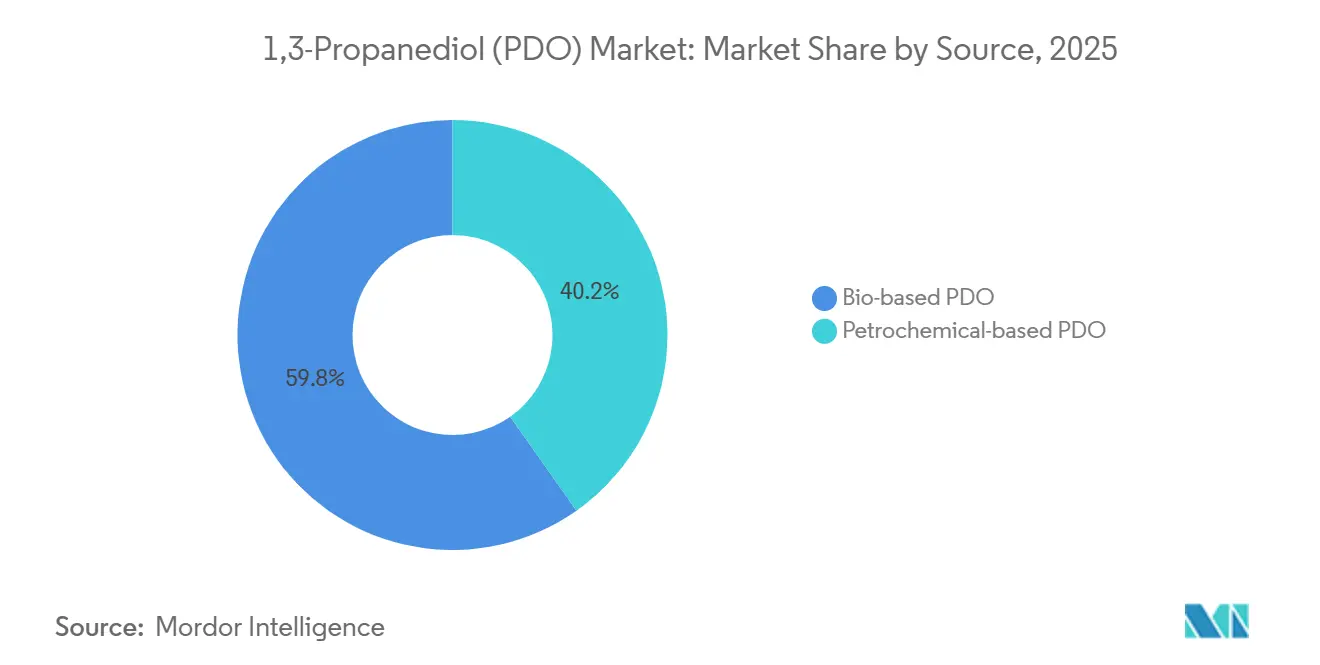

- By source, bio-based PDO captured 59.78% of revenue in 2025 and is anticipated to expand at an 8.93% CAGR through 2031.

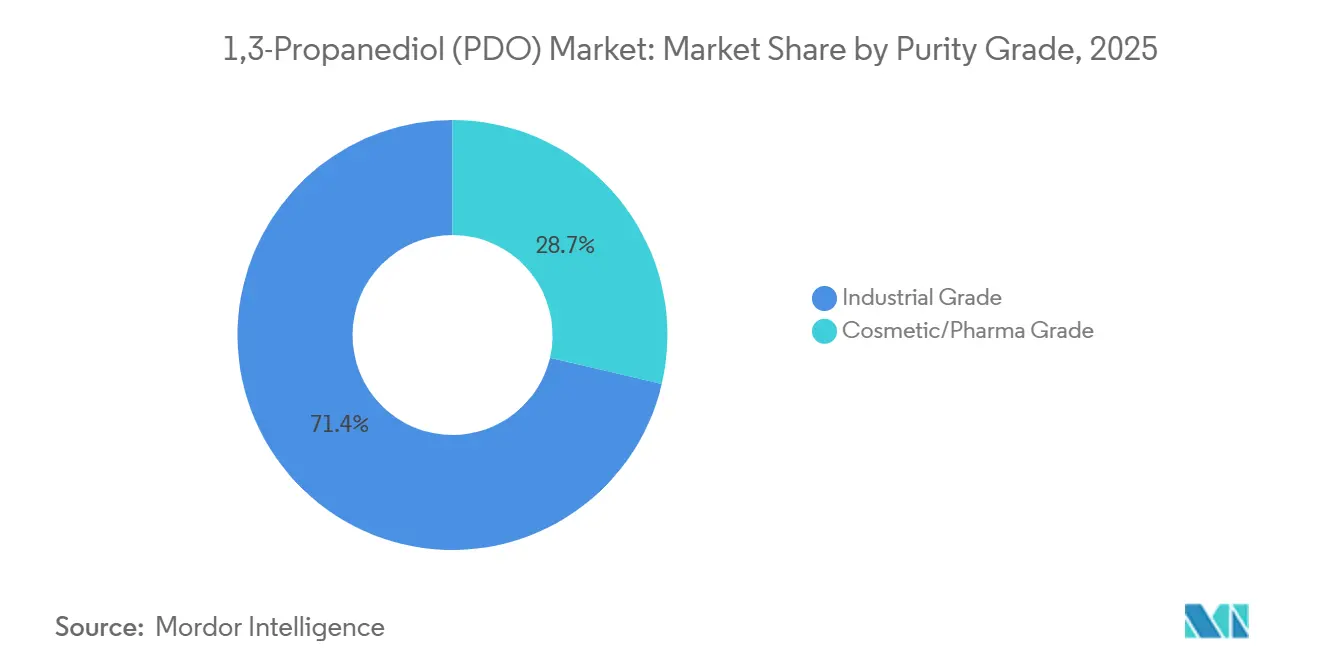

- By purity grade, industrial grade held 71.35% share in 2025 while cosmetic/pharma grade is projected to grow at a 9.88% CAGR through 2031.

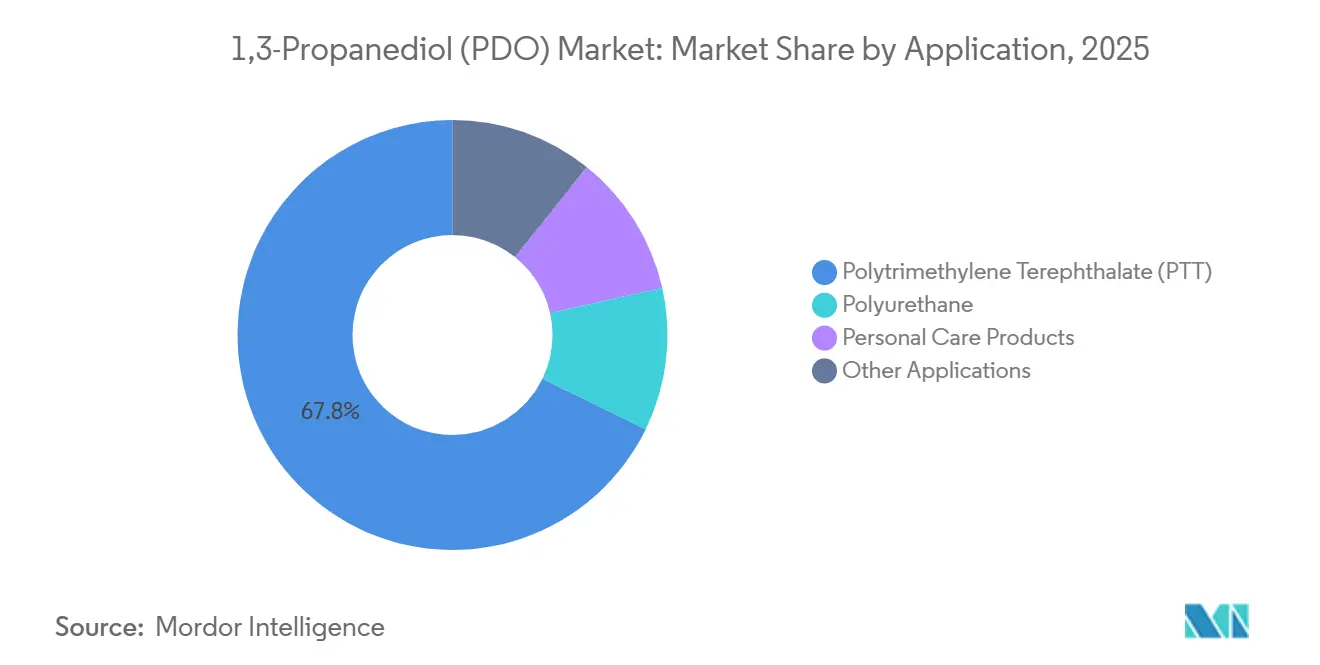

- By application, polytrimethylene terephthalate (PTT) led with 67.78% of 2025 demand and personal care products record the fastest 10.34% CAGR to 2031.

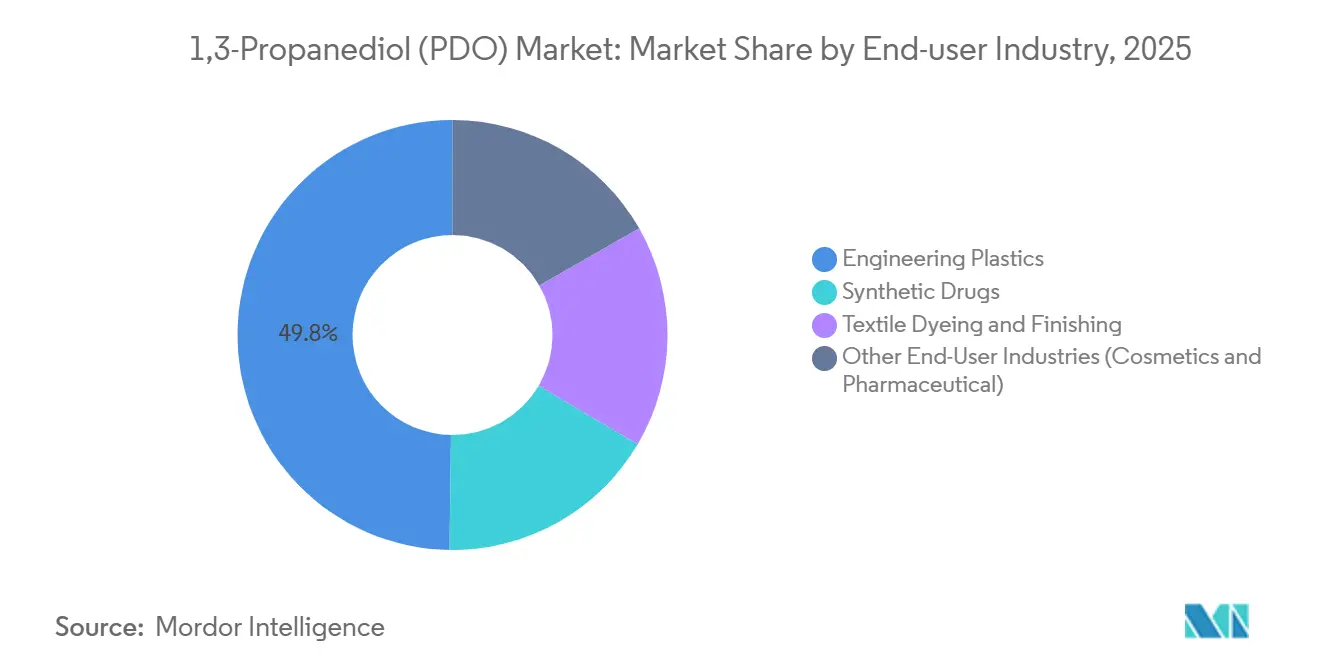

- By end-user industry, engineering plastics held 49.78% share of the 1,3-propanediol (PDO) market size in 2025 and textile dyeing and finishing is advancing at an 8.92% CAGR through 2031.

- By geography, North America commanded 34.89% share in 2025 and Asia-Pacific is forecast to deliver the highest 10.67% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of 1,3-Propanediol (PDO) Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Demand for Bio-Based Polymers | +2.1% | Global, with North America and EU leading adoption | Medium term (2-4 years) |

| Growing PTT Fiber Adoption in Automotive and Apparel | +1.8% | North America, Europe, APAC core markets | Medium term (2-4 years) |

| Expansion of Polyurethane Foams and Insulation | +1.3% | Global, particularly North America and Europe | Long term (≥ 4 years) |

| Government Incentives for Biomass-Based Chemicals | +1.5% | North America (US IRA), EU, China | Short term (≤ 2 years) |

| Shift Toward PDO-Based High-Purity Heat-Transfer Fluids | +0.7% | North America, Europe, emerging in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Bio-Based Polymers

Corporate decarbonization is pushing buyers toward renewable monomers that carry verified life-cycle savings. DuPont’s latest sustainability audit shows that Susterra PDO delivers a 61% greenhouse-gas reduction versus petrochemical routes. The European Commission’s 2024 bio-based products strategy prioritizes drop-in chemicals such as PDO that avoid downstream retooling. China’s 14th Five-Year Plan earmarked CNY 15 billion (USD 2.1 billion) for fermentation capacity with PDO listed among 12 platform chemicals. Scale economies and carbon-pricing schemes are narrowing the green premium to near single digits. As a result, the 1,3-propanediol (PDO) market is pivoting from early-adopter niches toward mainstream polymer applications where cost parity is within reach.

Growing PTT Fiber Adoption in Automotive and Apparel

Electric-vehicle lightweighting agendas are intensifying PTT fiber penetration into seating, headliners, and carpeting. Sorona fiber sales to automotive customers grew 22% year-over-year in 2025, with European OEMs responsible for 40% of incremental volume. PTT dyes at 100 °C versus 130 °C for polyester, trimming energy use by 30% and aligning with forthcoming EU eco-design rules[1]European Commission, “Ecodesign for Sustainable Products Regulation,” europa.eu . Athletic-apparel brands prize PTT’s elastic recovery, while premium home-textile suppliers tout the fiber’s softer hand. These performance advantages are translating into long-term supply contracts that lock in PDO offtake and buttress the 1,3-propanediol (PDO) market against price swings in commodity glycols.

Expansion of Polyurethane Foams and Insulation

North American and European building codes now impose higher R-value benchmarks that are spurring adoption of PDO-extended polyols. BASF’s technical data indicate that such polyols improve compressive strength by 12% compared with conventional EO-PO grades. The International Code Council increased mandated insulation performance by 15% in its 2024 energy code updates. Formulators value the inherent flame resistance of PDO-based foams that reach B-s1,d0 classification without halogenated additives restricted under REACH. This regulatory synergy continues to channel steady volume into the 1,3-propanediol (PDO) market.

Government Incentives for Biomass-Based Chemicals

The U.S. Inflation Reduction Act awards up to USD 1.75 per gasoline-equivalent gallon of avoided carbon for qualifying bio-chemicals, a measure that shaves 12-18 cents per kilogram from U.S. fermentation cash costs. Europe’s REPowerEU program allocates EUR 3 billion in loan guarantees and grants to derisk commercial-scale biorefineries. China’s 2024 VAT rebate on bio-based intermediates drops effective tax to near zero, further accelerating payback for new projects. These incentives are pulling several greenfield plants forward, uplifting near-term supply yet anchoring long-run competitiveness of the 1,3-propanediol (PDO) market.

Restraints Impact Analysis of 1,3-Propanediol (PDO) Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Feedstock (Corn/Glycerol) Price Volatility | -1.4% | Global, acute in North America (corn) and EU (glycerol) | Short term (≤ 2 years) |

| Cheaper Glycols as Functional Substitutes | -0.9% | Global, particularly in price-sensitive industrial applications | Medium term (2-4 years) |

| Biodiesel-Glycerol Supply Disruptions | -0.6% | North America and EU, spillover to APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Feedstock Price Volatility

Corn prices swung between USD 4.20-5.80 per bushel during 2024-2025, causing as much as USD 0.08 per kilogram variance in bio-PDO cash cost. Crude-glycerol values whipsawed between USD 150-320 per ton as renewable-diesel expansions diverted feedstock from biodiesel. Such swings deter long-term offtake agreements, particularly with automotive tier-ones that demand 12-18-month cost certainty. The 1,3-propanediol (PDO) market remains exposed, although integrated players with hedged grain contracts are cushioning volatility.

Cheaper Glycols as Functional Substitutes

Ethylene glycol averaged USD 0.85 per kilogram in Asia during 2025, roughly 20%-30% below bio-PDO spot quotes. Propylene glycol carries U.S. FDA GRAS status, easing regulatory barriers in food and pharma niches. BASF reported that bio-based BDO costs slipped below USD 1.50 per kilogram in 2024, eroding PDO’s differentiation edge in polyurethane and engineering-plastic segments. Unless sustainability premiums deepen, price-sensitive buyers may lean on these incumbents, limiting upside for the 1,3-propanediol (PDO) market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

1,3-Propanediol (PDO) Market Segment Analysis

By Source:

Fermentation Maturity Extends Bio-Based LeadBio-based PDO held 59.78% market share in 2025 and is projected to outpace overall growth at an 8.93% CAGR through 2031. The 1,3-propanediol (PDO) market benefits from DuPont’s corn-to-PDO pathway that now delivers titers of 135 g/L and yields above 0.51 g/g glucose. Genomatica’s four active Asian licensees add 80 kilotons of capacity by 2027, diversifying global supply. Petrochemical PDO remains price competitive when Brent trades near USD 70 per barrel, yet mounting carbon levies are squeezing its cost advantage, particularly in Europe. Shell permanently exited petro-PDO production in Singapore in 2024, underscoring structural headwinds for fossil routes.

Captive monomer pull from PTT polymerization allows integrated bio-players to hedge spot risk and capture higher margins. Conversely, glycerol-route producers in China thrive on feedstock arbitrage, supplying industrial grades at double-digit discounts. These dynamics signal that the 1,3-propanediol (PDO) market is settling into a bio-centric growth arc with fossil supply relegated to price-driven niches.

By Purity Grade:

Cosmetic and Pharma Specifications Accelerate Premium TierIndustrial grade accounted for 71.35% volume in 2025, yet cosmetic and pharmaceutical grades are expanding at 9.88% CAGR to 2031. Updated European Pharmacopoeia monographs cap residual water at 0.1% and individual impurities below 50 ppm. Meeting these targets adds USD 0.30-0.50 per kilogram but earns 40-60% price premiums. L’Oréal reformulated 120 SKUs with bio-PDO during 2025 to align with clean-beauty positioning. The U.S. FDA’s inactive-ingredient database now lists PDO for both parenteral and oral applications, lowering regulatory barriers.

Industrial demand still dominates because PTT and polyurethane segments absorb bulk tonnage. Even so, the specialty-grade niche is forecast to supply an outsized share of incremental value. Sustained brand-owner pull suggests that high-purity grades will continue to elevate the value mix of the 1,3-propanediol (PDO) market.

By Application:

PTT Retains Scale as Personal Care SurgesPolytrimethylene Terephthalate (PTT) captured 67.78% of 2025 demand, underpinning core volume for the 1,3-propanediol (PDO) market. PTT’s 95% elastic recovery and lower melt temperature cut processing energy by 8-12%, making it the polymer of choice for automotive carpet and performance apparel. Personal-care products, however, post the fastest 10.34% CAGR, buoyed by PDO’s 1.2-g/g water-binding capacity and lighter sensorial profile versus glycerin. Polyurethane foams are widening adoption due to PDO-based polyols that achieve flame-resistant ratings without halogens. Niche applications such as heat-transfer fluids and unsaturated polyester resins collectively remain below 10% share but offer differentiated margins.

The 1,3-propanediol (PDO) market size for PTT remains pivotal, yet faster-growing personal-care products are diversifying demand, trimming concentration risk and supporting value resilience.

By End-user Industry:

Engineering Plastics Dominate as Textiles AccelerateEngineering plastics held 49.78% share in 2025, leveraging PTT’s 80 J/m notched Izod impact strength and low thermal expansion to replace metal and nylon in automotive clips and consumer-appliance housings. Textile dyeing and finishing exhibits an 8.92% CAGR as PDO-based dispersants cut dyeing time by up to 20% and curb effluent volumes. Pharmaceutical formulators, meanwhile, rely on PDO to solubilize poorly water-soluble APIs, though volume remains modest.

Overall, the 1,3-propanediol (PDO) market share anchored in engineering plastics continues to fund R&D, while emerging end users expand the addressable base and hedge sectoral downturns.

Geography Analysis

North America 1,3-Propanediol (PDO) Market

North America accounted for 34.89% of 2025 revenue, a position underpinned by DuPont’s Tennessee biorefinery and favorable corn economics. Inflation Reduction Act credits shave production costs, reinforcing continental competitiveness[2]U.S. Department of Energy, “Bioenergy Technologies Office Update 2025,” energy.gov . Canadian producers are exploring a Saskatchewan project that leverages canola-derived glycerol feedstock. Mexico’s role remains downstream compounding. These factors ensure that the 1,3-propanediol (PDO) market retains a North American anchor even as growth moderates.

APAC 1,3-Propanediol (PDO) Market

Asia-Pacific is projected to post a 10.67% CAGR to 2031, the fastest regional expansion. China’s Sheng Hong Group commissioned 50 kilotons of bio-PDO in 2024, feeding its captive PTT lines and exporting to Southeast Asian mills. Indian pharmaceutical demand is scaling at 18% annually as injectable generics gain global share. Japan and South Korea remain premium importers focused on cosmetics and specialty polymers. Thailand and Vietnam are emerging textile-auxiliary markets as garment production migrates from China. Collectively, these trends enlarge the 1,3-propanediol (PDO) market footprint in Asia-Pacific.

EMEA and South America 1,3-Propanediol (PDO) Market

Europe represents a moderate share of demand, with Germany and France leading automotive and cosmetic demand. REPowerEU grants and REACH restrictions accelerate PDO adoption, especially in personal care where petrochemical glycols face tighter scrutiny. Scandinavia’s focus on circular materials further amplifies uptake. South America and the Middle East and Africa jointly represent a lower share, though Brazil’s sugarcane economy offers future optionality if fermentation costs fall. Overall, regional diversification supports stable global growth for the 1,3-propanediol (PDO) market.

Regulatory Landscape

In the European Union, 1,3-propanediol (propane-1,3-diol, EC 207-997-3) is a registered substance under REACH (Regulation (EC) No 1907/2006), so market access depends on dossier maintenance, supply-chain communication, and downstream safe-use documentation across polymer, personal-care, and industrial applications. In the United States, 1,3-propanediol is exempt from the requirement of a tolerance for pesticide inert ingredient residues under 40 CFR 180.910 and 40 CFR 180.940(a), supporting its use in formulations where pesticide-adjacent regulatory screens apply.

For bio-based PDO, procurement-linked sustainability requirements increasingly influence qualification alongside chemical compliance, with producers aligning to voluntary schemes such as the Roundtable on Sustainable Biomaterials (RSB) Principles and Criteria and biobased content standards used in claims substantiation. The USDA BioPreferred Program was updated in December 2024 through revisions to 7 CFR 4270, consolidating biobased product rules that can shape U.S. federal purchasing preferences for bio-based intermediates and finished goods embedding PDO.

Value Chain Analysis

The PDO value chain starts with feedstocks that split by route: corn-derived glucose (or other fermentable sugars) and crude glycerol for bio-based production, and petrochemical intermediates for chemocatalytic synthesis. Bio-based PDO production centers on fermentation using engineered microorganisms, followed by multi-step downstream purification (such as microfiltration, ion exchange, and distillation) to meet industrial versus cosmetic/pharma impurity and water specifications; purification intensity is a key cost and yield lever for premium grades.

PDO is distributed in bulk and packaged formats through direct producer-to-converter supply and chemical distributors, then consumed by polymer and formulation value chains, most notably PTT (as a monomer input) and polyurethane/polyol systems, along with personal care humectant uses and industrial fluids. Integration can tighten the chain where PDO is captive to PTT polymerization and fiber applications, while merchant volumes depend on consistent fermentation infrastructure, stable biomass inputs, and qualification packages (regulatory dossiers and sustainability documentation) that enable access to stricter downstream markets such as EU and U.S. personal care and selected pharma-adjacent uses.

Competitive Landscape

The market shows moderate concentration. DuPont, BASF, and Cargill control key fermentation IP and integrate downstream channels, giving them a pricing moat in premium grades. DuPont’s 63 kiloton facility runs near full rates and feeds its Sorona PTT line, insulating cash flow from spot swings. BASF pursues joint development with LG Chem to co-produce PDO-based polyols for automotive seating, leveraging BASF’s formulation expertise and LG’s regional reach. Cargill’s Primient brand targets cosmetic-grade demand under COSMOS certification.

Chinese challengers Zhangjiagang Glory and Sheng Hong compete on cost through glycerol routes and provincial subsidies. However, limited regulatory dossiers constrain their access to EU and U.S. personal-care markets. Genomatica’s licensing model democratizes access to optimized strains, enabling regional producers to bypass multi-year R&D cycles. Patent activity in 2024-2025 shows incumbent focus on PDO-based polyols and esters to expand into flame-retardant foams and biodegradable lubricants.

Heat-transfer fluids, pharma solubilizers, and specialty polyurethanes represent white-space opportunities. Rising Chinese capacity is compressing industrial-grade margins, pressuring Western incumbents to double down on sustainability certification and technical-service differentiation. The competitive equilibrium of the 1,3-propanediol (PDO) market therefore hinges on innovation pace and downstream integration depth.

1,3-Propanediol (PDO) Industry Leaders

Shell plc

Zhangjiagang Glory Biomaterial

Primient Covation LLC

Sheng Hong Group Holdings Limited

METabolic Explorer SA

- *Disclaimer: Major Players sorted in no particular order

1,3-Propanediol (PDO) Market Companies Covered in this Report

- BASF

- Cargill Inc.

- Connect Chemicals

- Dow Inc.

- DSM

- DuPont

- Eastman Chemical Company

- Genomatica

- LG Chem

- Merck KGaA

- METabolic Explorer SA

- MOJIABIO

- Primient Covation LLC

- Shell plc

- Sheng Hong Group Holdings Limited

- Sinopec

- Zhangjiagang Glory Biomaterial

Market Opportunities and Future Outlook

Opportunities are clearest where buyers pay for verified carbon accounting and traceable bio-content rather than competing purely on glycol price, particularly in cosmetic/pharma-grade humectants and specialty polymer systems. Primient has publicly framed bio-PDO carbon-footprint data as a procurement tool, including an 86% lower carbon footprint figure used in lifecycle assessment communications, which supports supplier differentiation in Scope 3 reporting workflows and can accelerate qualification for brand-owner reformulation programs.

On the supply and technology side, multiple levers are being pursued to widen margins and diversify feedstock optionality. Primient has confirmed 77,000 metric tons per year of capacity at its Loudon, Tennessee facility and initiated planning for a further 33,000 metric ton expansion, reflecting ongoing efforts to add scale in established production hubs. In parallel, research disclosed in May 2026 by KAIST and Hanwha Solutions Future Technology Research Institute demonstrated pilot-scale (300-liter) conversion of biodiesel-derived glycerol to 1,3-PDO using engineered Corynebacterium without antibiotic supplementation, and a February 2026 patent publication described microorganisms designed to co-produce 1,3-PDO and 3-hydroxypropionic acid (3-HP), pointing to process-intensification pathways that can change economics for glycerol-linked and multi-product biorefinery concepts.

Recent Industry Developments in 1,3-Propanediol (PDO) Market

- June 2026: Primient partnered with TrueNorth Collective to publish lifecycle assessment results for bio-based 1,3-propanediol, highlighting an 86% reduction in carbon footprint versus fossil-based PDO. The work strengthens carbon-accounting credentials that large polymer and personal-care buyers use for Scope 3 reporting, supporting qualification and premium-grade positioning.

- June 2026: YiDa Chemicals Co., Ltd. launched its Biebl series of bio-based 1,3-PDO, including a 100% palm-free (PF) version positioned around rapeseed oil fermentation sourcing. The product-line move targets sustainability-sensitive downstream formulators and adds competitive pressure on suppliers differentiating via feedstock traceability and claims substantiation.

- November 2025: Primient Covation LLC introduced new hair color formulations incorporating Zemea propanediol, positioned as a 100% plant-based 1,3-propanediol alternative to petroleum-derived diols. This application-led launch expands end-use pull in personal care and reinforces the shift toward bio-based humectants and solvents where formulation performance and sustainability claims are both decision drivers.

1,3-Propanediol (PDO) Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the market covers the value of 1,3-propanediol sold as a chemical intermediate, measured at the point it is supplied to downstream users across major regions, and reported in USD terms.

Scope exclusions: We exclude lab reagent grades, recycled streams, and captive consumption that never enters commercial trade channels.

Segments Covered in This Report

- By Source

- Bio-based PDO

- Petrochemical-based PDO

- By Purity Grade

- Industrial Grade

- Cosmetic/Pharma Grade

- By Application

- Polytrimethylene Terephthalate (PTT)

- Polyurethane

- Personal Care Products

- Other Applications

- By End-user Industry

- Engineering Plastics

- Synthetic Drugs

- Textile Dyeing and Finishing

- Other End-User Industries (Cosmetics and Pharmaceutical)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clean fact base around PDO supply, demand, and pricing, so later interview inputs can be tested against something observable. We mainly rely on public sources such as USGS chemical and minerals statistics, US Census Bureau trade data, Eurostat, UN Comtrade, and national environmental and chemical regulatory portals that flag permitted uses and handling requirements.

Next, we add context using company annual reports, investor presentations, press releases, association websites, and reputable industry news that discuss capacity changes, plant utilization, and downstream demand signals. In parallel, we use a paid subscription for company financials and another paid source for patent databases to track new process routes and commercialization timing. These examples are not exhaustive, and many other public references were used for collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test model assumptions that desk sources do not fully answer, such as regional price realization, route-wise output mix, and how much demand is tied to long-term supply agreements. We spoke with a mix of producers, distributors, and downstream formulators across APAC, EMEA, and the Americas, so the final numbers reflect real buying patterns and not only announced capacities.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 20% | APAC: 45% |

| Mid tier: 42% | Functional/Unit leaders: 24% | EMEA: 35% |

| Smaller Players: 21% | Managers: 56% | Americas: 20% |

Market-Sizing & Forecasting

The sizing starts with a top-down build where production, capacity, and trade data are used to reconstruct the addressable PDO supply pool by region, and then it is translated into value using observed price ranges. Once that is in place, we corroborate the totals with selective bottom-up checks, such as sampled supplier revenues, channel conversations on contract versus spot volumes, and simple volume times ASP sanity tests for key applications.

A few inputs that matter in this market include announced and operating capacity by production route (bio-based and petrochemical), utilization trends, import and export flows, feedstock-linked cost movement that influences selling prices, and demand indicators from PTT and personal care formulations. When data is missing in a country, proxies are used such as trade-based apparent consumption or region-level splits shared by interviewees, and the impact is then reviewed in sensitivity checks.

Forecasts are developed using scenario analysis supported by a light multivariate regression on demand drivers like textile and polymer activity, consumer products output, and expected capacity additions. The final curve is adjusted only after expert feedback confirms whether the assumed ramp-ups and price direction match what is being seen in contracting and procurement.

Data Validation & Update Cycle

Model outputs are checked against independent signals, including trade balances, capacity announcements, and implied regional consumption trends, so large jumps are flagged early. If an anomaly is found, the input series is rechecked, assumptions are reviewed by another analyst, and follow-up calls are triggered to confirm whether the change is real or a data artifact.

The report is refreshed annually, and interim updates are made when material events occur, such as major capacity starts, shutdowns, or policy shifts affecting bio-based production economics. Before delivery, we run a final update pass to ensure the market numbers and assumptions reflect the latest publicly available information and recent primary feedback.

Mordor Intelligence's 1 3 Propanediol Pdo Market Size Versus Other Published Estimates

It is normal to see different PDO market numbers in the public domain, because studies often count different product grades, choose different base years, and apply different pricing logic when converting volumes into USD. The gap also widens when forecast ramps for new capacity are assumed to be faster than what buyers say is achievable.

Some published figures appear to include broader chemical value pools, or they apply aggressive price and utilization progressions that are not anchored to observed trade and contracting patterns. In contrast, Mordor Intelligence counts only merchant-grade PDO that is commercially traded into downstream uses, and it keeps captive internal transfers and lab-grade material out of the value total, which narrows the market size for the same time point.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 435.12 M (2026) | |

| Industry Publisher A | USD 424.80 M (2023) | Uses an earlier base year and may reflect a different price environment, which can shift value even if volumes are similar. The scope description is less explicit on excluding captive usage, so totals can differ based on what is treated as market sales. |

| Market Publisher B | USD 594.47 M (2024) | Reports a higher base-year valuation that likely reflects broader inclusions and a faster assumed ramp in demand tied to downstream polymers and cosmetics. Limited clarity on how contract versus spot pricing and regional price spreads are applied can also inflate the USD conversion. |

Taken together, the spread mainly comes from what is counted as market sales and from how pricing and ramp-up assumptions are applied across regions and routes. By tying the value build to observable supply signals and then rechecking it with targeted interviews, we keep the estimate traceable to repeatable steps that users can challenge and re-run over time.

Key Questions Answered in the Report

What is the current value of the 1,3-propanediol (PDO) market?

The market is valued at USD 435.12 million in 2026 and is on track to reach USD 620.61 million by 2031.

Which segment is growing fastest within application?

Personal care products are expanding at a 10.34% CAGR due to demand for bio-based humectants.

Why is Asia-Pacific expected to lead future PDO growth?

New Chinese and Indian capacity, plus strong textile and pharmaceutical demand, drive a projected 10.67% regional CAGR.

How do government incentives influence PDO economics?

U.S., EU, and Chinese policies reduce production costs by up to 20 cents per kilogram, improving project paybacks and boosting capacity additions.

Page last updated on: