Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

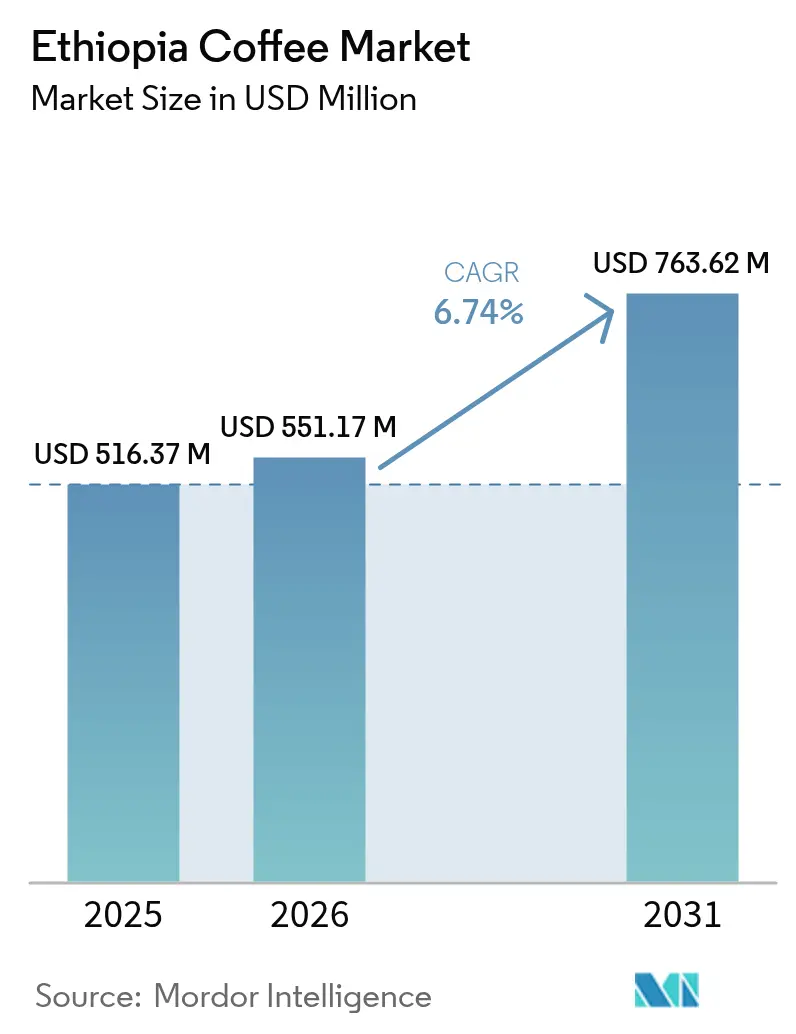

| Base Year Market Size (2025) | USD 516.37 Million |

| Market Size (2026) | USD 551.17 Million |

| Market Size (2031) | USD 763.62 Million |

| Growth Rate (2026 - 2031) | 6.74% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Ethiopia Coffee Market Analysis by Mordor Intelligence

The Ethiopia coffee market size is expected to grow from USD 516.37 million in 2025 to USD 551.17 million in 2026 and is forecast to reach USD 763.62 million by 2031 at 6.74% CAGR over 2026-2031. Momentum comes from the government’s January 2025 coffee strategy that shifts value creation from raw-bean exports to roasted and specialty offerings, an urban youth demographic embracing convenient formats, and regulatory openness that draws foreign investment into processing and retail. Coffee holds a significant place in Ethiopian culture and daily life. Traditional coffee ceremonies not only drive domestic demand but also enhance the global reputation of Ethiopian coffee brands. The expansion of e-commerce and modern retail channels, such as supermarkets and online platforms, enables Ethiopian brands and cooperatives to reach consumers both locally and internationally. Competitive intensity is high but fragmented, encouraging cooperatives and private processors to fast-track vertical integration. Ethiopia’s ambition to become the world’s second-largest coffee exporter by 2033 underpins sustained capital inflows into milling, roasting, and digital traceability systems.

Key Report Takeaways

- By product type, whole-bean coffee led with 41.12% of Ethiopia coffee market share in 2025, while instant coffee is advancing at a 7.78% CAGR through 2031.

- By flavor, plain coffee accounted for 70.55% share of the Ethiopia coffee market size in 2025, and flavored variants are expanding at a 7.7% CAGR to 2031.

- By category, conventional offerings captured a 66.44% share in 2025; specialty coffee is projected to grow at a 6.85% CAGR through 2031.

- By bean type, Arabica held 59.22% of the Ethiopia coffee market share in 2025, while Robusta production is rising at a 6.96% CAGR to 2031.

- By distribution channel, off-trade outlets controlled a 69.10% share in 2025; the segment is forecast to expand at an 8.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Ethiopia Coffee Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Booming RTD/cold-brew consumption | +1.2% | Urban Ethiopia | Short term (≤ 2 years) |

| Export of roasted coffee for value capture | +1.8% | National | Medium term (2-4 years) |

| Rising demand for specialty and premium coffee | +1.5% | Urban Ethiopia | Medium term (2-4 years) |

| Value-addition and processing innovations | +1.1% | National | Long term (≥ 4 years) |

| ECX traceability upgrade unlocking premiums | +0.9% | National | Short term (≤ 2 years) |

| Growing e-commerce and digital platforms | +0.8% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Booming RTD/cold-brew consumption

Urbanization and changing lifestyle preferences among Ethiopia's youth are driving a transformation in the domestic market, with ready-to-drink (RTD) coffee playing a central role. The Ethiopian Coffee and Tea Authority has highlighted RTD beverages as a major growth opportunity. In 2024, domestic coffee consumption in Ethiopia is anticipated to account for 50% of the nation's production, in contrast to other African countries that predominantly export raw coffee beans[1]Source: Ethiopian Coffee and Tea Authority, "Ethiopia: Continental Coordination for African Coffee Competitiveness", ethiocts.gov.et. Urban centers like Addis Ababa are seeing an increase in coffee shops and convenience stores offering cold-brew options. This expansion is supported by improvements in refrigeration and a modernized supply chain. USDA projects Ethiopia's coffee consumption to hit 3.7 million 60-kilogram bags by 2025, fueled by deep-rooted cultural ties, rising urbanization, and a surge in coffee shop openings[2]Source: United States Department of Agriculture, "Coffee Annual- Ethiopia", usda.gov. These trends align with global RTD coffee market dynamics, where convenience and portability are key factors for working professionals and students. By focusing on value addition, the government aims to position RTD coffee as a strategic initiative to secure higher profit margins from domestic production while reducing dependence on the volatile pricing of commodity exports.

Ethiopia moves to export more roasted coffee for value capture

Ethiopia's government is shifting from decades of dependence on raw coffee beans, now emphasizing processed coffee exports to secure higher prices. In February 2024, Ethiopia exported 200,000 bags (each weighing 60 kilograms) of coffee, according to the Information Commissioner's Office[3]Source: Information Commissioner's Office, "Exports of all forms of coffee by exporting countries to all destinations", ico.org. The Ethiopian Coffee and Tea Authority is focusing on expanding roasting capacities, with new facilities planned in the Jimma and Guji regions to strengthen export preparations. This transition is advancing through international partnerships, such as MIDROC Investment Group's significant coffee marketing agreement with Neumann Kaffee Gruppe in March 2025, which provides access to global roasted coffee markets. Technological advancements, including a 75% efficiency improvement at Coffee Processing and Warehouse Enterprise using Sortex solutions, highlight scalable opportunities for enhancing coffee quality.

Rising demand for specialty and premium coffee

Ethiopia's export portfolio is evolving, driven by the growing demand for specialty coffee. This growth highlights Ethiopia's effective quality improvement efforts and strategic market positioning. Urbanization is significantly boosting coffee consumption, particularly for specialty and premium brews. Cities like Addis Ababa are experiencing a rise in trendy cafés, coffee shops, and upscale restaurants that showcase single-origin brews and creative blends. Younger Ethiopians are increasingly drawn to quality, diverse flavors, and internationally-inspired coffee beverages. This shift is driving higher domestic consumption of specialty coffee. The expansion of specialty cafés and "third wave" coffee shops is further enhancing the demand for premium coffees. These establishments focus on tasting experiences, coffee origins, and sustainable sourcing stories, which are directly increasing the demand for high-quality beans within Ethiopia. By utilizing compelling narratives, prioritizing sustainability, and employing digital marketing, efforts are being made to engage younger audiences. This approach is embedding specialty coffee more deeply into the daily lives of Ethiopians.

Value addition and processing innovations

The adoption of processing technologies in Ethiopia's coffee value chain is advancing rapidly, driven by the integration of artificial intelligence and automation to improve quality control and operational efficiency. Debo Engineering provides its Coffee AI Innovation Solution, addressing key industry challenges such as disease detection, precise grading, and automated sorting. These solutions are being implemented in major coffee-producing regions, including Jimma, Sidama, Yirgacheffe, and Hararge. Additionally, innovative technologies like Covestro's polycarbonate solar dryers are transforming the drying process. These solar dryers enable faster and cleaner coffee bean drying while protecting against rain, pests, and mold. This improves cup quality, reduces spoilage, and increases the volume of coffee meeting specialty grade standards. Infrastructure investments are also expanding processing capacities. For instance, Henan Gold Key Machinery Technology has established a 10 tons per hour green coffee processing plant in Gelan, reflecting strong foreign investment confidence in Ethiopia's processing sector.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited domestic roasting capacity | -1.4% | National | Medium term (2-4 years) |

| Lack of efficient market structure | -1.1% | National, rural producers | Short term (≤ 2 years) |

| Traceability and compliance challenges | -0.8% | National | Short term (≤ 2 years) |

| Policy and governance issues | -0.6% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited domestic roasting capacity

Roasting infrastructure limitations are a major obstacle to Ethiopia's efforts to enhance value addition in its coffee sector. The current roasting capacity is inadequate to meet the government's objectives of increasing processed coffee production. Most roasting facilities in Ethiopia are located in urban areas, creating logistical difficulties for rural producers and limiting their access to value-added processing and retail distribution. To address this issue, the Ethiopian Coffee and Tea Authority has announced plans to build new coffee preparation facilities in the Jimma and Guji regions. However, these facilities are projected to become operational only by 2026. The infrastructure challenges are further intensified by unreliable energy supplies and transportation difficulties, particularly in remote coffee-producing regions where processing facilities could deliver the greatest economic benefits.

Lack of efficient market structure

Unreliable infrastructure and poor coordination among market participants result in unpredictable fluctuations in coffee prices. This volatility discourages farmers from enhancing quality or increasing production, thereby limiting the variety and consistency of coffee available to local consumers. Insufficient roads, storage, and processing facilities contribute to post-harvest losses and reduced quality. Consequently, the coffee reaching consumers often lacks the desired freshness and specialty attributes, which hampers the growth of premium and specialty coffee consumption domestically. The fragmented market and inefficient wholesale and retail structures create challenges for specialty coffee shops, modern retailers, and e-commerce platforms in reliably sourcing quality coffee at scale. These issues constrain the expansion of premium coffee consumption channels in Ethiopia. Moreover, inefficiencies in Ethiopia's coffee market hinder the development of consistent supply, quality assurance, and transparent pricing—critical factors for fostering and expanding domestic coffee consumption, particularly for specialty and premium products. Enhancing market linkages, infrastructure, and the flow of market information is crucial to promoting vibrant domestic coffee consumption that aligns with changing consumer preferences.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Instant Coffee Drives Processing Innovation

Instant coffee’s 7.78% CAGR illustrates how convenience reshapes the Ethiopia coffee market. Instant coffee, known for its convenience and simple preparation with just hot water or milk, is gaining popularity among busy urban consumers and young professionals in Ethiopia, where coffee culture is evolving. Whole-bean offerings nevertheless retained 41.12% Ethiopia coffee market share in 2025, supported by traditional brewing customs. Ground coffee holds mid-range demand, and pod systems gain relevance as supermarkets diversify appliance aisles. The Ethiopia coffee market size attached to instant formats is projected to swell as AI-enabled sorting boosts granule consistency and flavor retention.

Processors invest in spray-drying and freeze-drying lines to commercialize local beans domestically, a shift exemplified by Garden of Coffee’s urban boutique that now retails single-serve instant sachets. Imported RTD know-how merges with indigenous roasting techniques, blurring lines between specialty and soluble categories. New entrants leverage online channels to ship micro-lot instant coffee to consumers. Such dynamics signal that Ethiopia coffee market participants see soluble applications as vital to absorbing the climbing harvest volumes.

By Flavor: Plain Coffee Dominance Faces Flavored Segment Challenge

In 2025, plain profiles accounted for 70.55% of Ethiopia's coffee market share, reflecting the nation's culinary tradition that values unadulterated aromas. Ethiopia's rich coffee culture, deeply rooted in the traditional coffee ceremony, emphasizes plain, naturally brewed coffee. This cultural preference highlights the demand for unflavored, pure Arabica coffee, aligning with the country's longstanding taste and social practices. However, flavored variants, growing at a 7.7% CAGR, indicate evolving preferences among millennials seeking unique experiences. Cafés in Addis Ababa now offer chocolaty and spice-infused blends, often served with chilled milk to accommodate the warmer climate.

Producers utilize honey-processing and anaerobic fermentation methods to naturally enhance fruit notes while avoiding artificial additives, ensuring authenticity. Compliance with EU deforestation regulations is driving processors toward natural flavoring and traceable supply chains. This shift positions Ethiopian producers competitively against those relying on synthetic flavors. As discretionary incomes rise, flavored coffee lines are becoming premium options in Ethiopia's coffee market, reinforcing the trend of premiumization.

By Category Type: Specialty Coffee Gains Premium Market Position

In 2025, conventional coffee constitutes 66.44% of the market value. Its affordability and easy accessibility in local markets and homes—both rural and urban—drive mass consumption across various income groups. The urban café culture, along with rural household preferences, supports the traditional coffee experience, resulting in consistent, high-volume consumption. In Ethiopia, coffee is more than just a drink; it is an integral part of daily life, exemplified by traditional coffee ceremonies. These ceremonies primarily use plain, conventional coffee styles, maintaining strong demand across diverse demographics.

Although specialty labels currently form a smaller segment, they are expanding at a significant 6.85% CAGR (2026-2031), propelling the Ethiopian coffee market into higher-margin categories. Urbanization and the rise of a growing middle class, particularly younger consumers, are driving interest in premium experiences at specialty cafés and retail outlets. Increased awareness of sustainability, coffee origins, quality, and health benefits is enhancing the demand for organic and single-origin specialty coffees. While still niche, specialty coffee consumption is rapidly increasing among urban consumers with disposable income who seek diverse and premium options.

By Bean Type: Arabica Leadership Meets Robusta Diversification

In 2025, Arabica represented 59.22% of Ethiopia's coffee market share. As the origin of Arabica coffee, Ethiopia has integrated it into its culture and daily life for centuries. This strong connection drives a steady domestic preference for Arabica. Ethiopian coffee production primarily focuses on Arabica, aligning with local consumption trends. The premium taste profile of Arabica beans, highly valued in Ethiopian culture, reinforces their dominant consumption share.

Robusta acreage is expected to grow at a 6.96% CAGR from 2026 to 2031. As a more economical caffeine source, Robusta attracts an increasing number of price-sensitive consumers in urban and rural areas. Consumer awareness and acceptance of Robusta are rising, particularly for instant coffee production and blending, which is boosting its consumption growth. Although Robusta currently holds a smaller market share, its domestic consumption is increasing due to crop expansion and growing demand for instant and blended coffees.

By Distribution Channel: Off-Trade Dominance Reflects Domestic Focus

In 2025, off-trade formats—supermarkets, hypermarkets, and convenience stores- accounted for a significant 69.10% market share, demonstrating robust growth at an 8.05% CAGR. This expansion is largely attributed to the liberalization of the retail sector, which has facilitated the entry of foreign retail chains into the market. Consumers are increasingly drawn to the wide variety of products available in these formats, ranging from affordable coffee blends to premium single-origin micro-lots that cater to diverse preferences. Additionally, e-commerce has played a pivotal role in extending market reach by directly connecting rural coffee roasters with diaspora households. This connection is made seamless through the integration of mobile payment systems, which enhance accessibility and convenience for consumers.

On-trade growth is primarily driven by the rising popularity of café culture, where baristas are innovating with advanced brewing techniques such as pour-over and cold-drip methods. These methods not only enhance the sensory experience but also elevate the perceived quality of coffee among consumers. Furthermore, digital platforms are streamlining the procurement processes for hotels and offices, ensuring efficient inventory management and reducing the risk of stock-outs. Together, these on-trade and off-trade channels play a crucial role in strengthening domestic demand, which has become a key pillar of the Ethiopian coffee market.

Geography Analysis

In Ethiopia, traditional coffee-growing regions continue to dominate the market, but emerging areas are increasingly contributing to its expansion. Ethiopia is recognized for having one of the highest coffee consumption rates globally. Urban areas are experiencing a shift in consumer preferences, with growing interest in diverse coffee products, while rural regions maintain their strong adherence to traditional consumption patterns. The Sidama, Yirgacheffe, and Jimma regions are the primary hubs of coffee production, excelling in specialty coffee output. These regions consistently achieve premium pricing in both domestic and international markets due to the superior quality of their coffee.

Emerging coffee-producing regions, such as Guji, Bench Maji, and Nekemte, are playing a significant role in diversifying production and supporting market growth strategies. Across multiple regions, advancements in coffee processing are being implemented to enhance efficiency and quality. For instance, Debo Engineering's Coffee AI Innovation Solution has been deployed in Jimma, Sidama, Yirgacheffe, and Hararge. This technology addresses critical challenges, including disease detection and quality grading, thereby improving overall production standards. In rural areas, the steady demand for conventional coffee varieties is driven by cultural traditions, affordability, and the easy availability of locally grown coffee.

Addis Ababa, the capital city, serves as a key driver of domestic market growth and acts as a testing ground for innovative coffee products, such as ready-to-drink and flavored coffee variants. The retail sector liberalization introduced in April 2024 has opened the market to foreign investments, fostering increased competition among supermarket chains and convenience stores. This development has significantly enhanced the distribution network within the city. Additionally, regional export hubs are strengthening their logistics infrastructure to support the growing coffee trade. The Ethiopian Coffee and Tea Authority has implemented direct market linkages, eliminating the need for broker intermediaries. This initiative not only streamlines the supply chain but also ensures that farmers receive fairer compensation for their produce.

Regulatory Landscape

Ethiopia Coffee and Tea Authority (ECTA) is the primary regulator for coffee marketing, quality control, and export standards, working alongside the Ethiopian Commodity Exchange (ECX), which continues to handle most commercial coffee trading and requires compliance with its membership and quality standards for exports. Coffee exports are also governed by national legislation such as the Coffee Marketing and Quality Control Proclamation No. 1051/2017, with pre-export quality and safety testing (including pesticide residue and microbiological checks) conducted through the Ethiopian Conformity Assessment Enterprise (ECAE) or other approved laboratories.

Regulatory changes during 2024-2026 have focused on expanding participation while tightening compliance and traceability. In March 2024, the Ethiopian Investment Board issued Directive No. 1001/2024 that permits foreign investors to participate directly in raw coffee exports, subject to procurement and export-volume thresholds. ECTA further consolidated operational oversight in 2025 by moving export coffee contract registration responsibilities from the National Bank of Ethiopia to ECTA (effective May 2025) and issuing a comprehensive Coffee Marketing and Quality Control Directive in July 2025, while 2026 actions emphasized traceability and value addition, including ATI-led traceability consultations in June 2026 and ECTA guidelines enabling value-added (roasted and ground) coffee exports in foreign currency.

Competitive Landscape

In Ethiopia's coffee market, numerous cooperatives, private exporters, and processing companies engage in fragmented competition, with no single entity holding a dominant market share. Urban specialty cafes, retail outlets, and a growing number of online platforms showcase the strong presence of leading players like Belco Coffee, Nestlé SA, Hadero Coffee, Moyee Coffee Ethiopia, and Ya Coffee. These companies prioritize delivering high-quality products, emphasizing the distinct regional flavors of Ethiopian coffee, and actively engaging younger consumers through targeted marketing strategies. Meanwhile, global giants like Nestlé SA and Enjoy Better Coffee (Mokate) are expanding their footprint in Ethiopia by offering instant and ground coffee products specifically tailored to meet the preferences of local consumers. These multinational companies leverage their extensive distribution networks, ensuring product availability in supermarkets and convenience stores across the country.

Groups such as the Oromia Coffee Farmers Cooperative Union and Sidama Coffee Farmers Cooperative Union play a crucial role in maintaining quality standards and ensuring a consistent supply of coffee. They also actively support value addition initiatives aimed at boosting domestic consumption. The increasing presence of specialty cafés, modern retail grocery stores, convenience outlets, and e-commerce platforms is significantly influencing consumption patterns, providing consumers with a broader range of premium and convenient coffee options. To cater to the evolving preferences of consumers, market players are focusing on innovative packaging designs, promoting sustainable sourcing practices such as organic and fair trade certifications, and diversifying their product portfolios to include instant coffee, ready-to-drink (RTD) beverages, and single-origin varieties. The growing demand for specialty coffee is largely driven by urban youth, who are seeking premium coffee experiences both in cafes and through home brewing using branded products.

Ethiopia's domestic coffee consumption market is experiencing steady growth, fueled by increasing consumer interest in premium, convenient, and sustainably sourced coffee options. The competitive landscape is intensifying, with established local brands emphasizing quality and authenticity, while multinational companies leverage their economies of scale and focus on product innovation to capture market share. To attract and retain customers, key players are increasingly utilizing social media platforms, online marketing campaigns, and strategic product branding to enhance their visibility and appeal to a broader audience.

Ethiopia Coffee Industry Leaders

-

Nestle SA

-

Hadero Coffee

-

Ya Coffee

-

Moyee Coffee Ethiopia

-

Belco Coffee

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Expanding Ethiopia-based value addition is a near-term opportunity, particularly roasting, grinding, and industrial instant coffee, in line with the government push to shift earnings from green-bean exports toward processed formats. ECTA confirmed in January 2026 that new guidelines support value-added coffee exports, and the national coffee strategy highlighted in 2026 frames productivity and export-earnings targets that increase the incentive for investments across processing, packaging, and quality assurance. This direction also aligns with the segment momentum visible in Ethiopia, where convenience-led formats such as instant coffee and RTD/cold-brew are gaining traction in urban centers.

A second opportunity is traceability and quality infrastructure that supports higher-value channels and direct trade. With ECX still central to most trade, policy mechanisms allowing vertical integration and direct export in some cases create space for exporters and cooperatives to invest in farm-to-export data systems, segregation, and lab capacity that meet buyer requirements. Programs such as the EU-CAfE (EU Coffee Action for Ethiopia) project, which works on value-chain strengthening and database systems for EU Deforestation Regulation (EUDR) compliance, add practical demand for traceability tools, farm mapping, and post-harvest controls, reinforcing demand for digital platforms and service providers that can operationalize compliance at scale.

Recent Industry Developments

- July 2026: Ethiopian Coffee and Tea Authority (ECTA) reported historic coffee export earnings of USD 3 billion. The milestone reinforces the sector's foreign-exchange importance and keeps policy focus on upgrading quality control, traceability, and value-added exports.

- April 2025: Royal Coffee opened a new sourcing and logistics office in Addis Ababa, including a fully equipped cupping lab. The added in-country capability supports faster quality evaluation and tighter supplier engagement, helping specialty-oriented procurement and export logistics.

- October 2024: Belco invested in multiple Ethiopian processing stations, including the Sediloya coffee station in the Jimma zone, and launched agroforestry nursery projects. The investments expand processing throughput and support sustainability-linked sourcing narratives that are increasingly used in premium and specialty coffee channels.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Ethiopia coffee market is defined as the value of coffee products sold for consumption within Ethiopia, across retail and foodservice channels, captured in USD for the stated time period.

Scope exclusions: It does not count farmgate green coffee value meant only for export trade flows unless it is sold as a consumer coffee product in the country.

Segmentation Overview

-

By Product Type

- Whole-bean

- Ground Coffee

- Instant Coffee

- Coffee Pods and Capsules

- Ready-to-Drink (RTD)

-

By Flavor

- Plain

- Flavored

-

By Category Type

- Conventional

- Specialty (Organic/Single-Origin)

-

By Bean Type

- Arabica

- Robusta

- Others

-

By Distribution Channel

- On-trade

-

Off-trade

- Supermarkets/Hypermarkets

- Convenience Stores

- Specialty Stores

- Online Stores

- Other Off-trade Channels

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with building a fact base on Ethiopia coffee supply, local consumption patterns, and observed price movement, since these signals drive value even when volumes are seasonal. We relied on public sources such as FAOSTAT, UN Comtrade, the International Coffee Organization, and Ethiopian government publications from agriculture and trade bodies for production, export, and policy context.

To connect demand-side clues, we reviewed national statistics releases, customs updates, and notes from industry bodies, along with peer reviewed papers on coffee consumption and processing. Where available, we also checked company filings and investor presentations for processing and trade references. In parallel, we used paid database subscriptions for company financial intelligence and shipment level import and export checks to keep desk assumptions grounded. The sources listed here are illustrative and not exhaustive, since additional public materials were also used to collect data, validate inputs, and clarify research assumptions.

Primary Interviews and Surveys

Primary work was used to pressure test the desk model by speaking with growers and cooperatives, processors, traders, distributors, and on-trade buyers, followed by cross-checks with retail and foodservice focused participants. Inputs were validated across the main producing belts and major consumption centers, so pricing, product mix shifts, and channel dynamics could be understood consistently across Ethiopia.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 14% | APAC: 48% |

| Mid tier: 41% | Functional/Unit leaders: 28% | EMEA: 30% |

| Smaller Players: 20% | Managers: 58% | Americas: 22% |

Market-Sizing & Forecasting

Sizing was built using a top-down, Ethiopia-specific demand pool where production and trade statistics are used to reconstruct what stays in-country, then converted into value using observable consumer price ranges by product form and channel. The totals were corroborated with selective bottom-up approximations such as sampled retail shelf prices, on-trade menu pricing checks, and a roll-up of identified processors and branded suppliers, which helped adjust for underreported informal flows.

Key inputs used in the model included (illustratively) domestic coffee consumption share versus export share, green-to-roasted conversion factors, product mix across whole bean, ground, and instant, the on-trade versus off-trade split, and inflation-driven price progression that impacts realized selling prices. Forecasts were produced using scenario analysis, where volume and price paths were adjusted based on expert views on harvest variability, policy moves affecting trade and FX, and channel expansion in modern retail and cafes. When a bottom-up proxy had missing disclosure, gaps were filled using peer group ranges and then rechecked through follow-up calls before the final totals were locked.

Data Validation & Update Cycle

Model outputs were checked against independent signals such as export earnings trends, visible price movements in mainstream retail, and consistency between implied per-capita consumption and realistic household usage patterns. Any large variance by channel or product form was flagged, reviewed by a second analyst, and corrected only after the underlying assumption was explained and supported by evidence.

The report is refreshed annually, and an interim update is triggered when material events occur, such as sharp price shocks, major policy changes, or a clear shift in channel structure. Before delivery, a final pass is completed so clients receive the most current view available at that time.

Mordor Intelligence's Ethiopia Coffee Market Size Compared With Other Published Estimates

Published market values for Ethiopia coffee can look far apart because the scope being counted is not always the same, and the year and pricing basis can also differ. Some sources focus on export value or farmgate trade, while others try to count only consumer coffee sold inside the country.

Export and consumption signals, plus channel-level price checks, are the evidence used to keep Mordor Intelligence's estimate tied to in-country coffee product sales instead of blending in farmgate green coffee trade value. The remaining gaps usually come from how coffee pods and capsules or ready-to-drink forms are treated, how informal sales are approximated, and whether currency conversion uses spot rates or an averaged approach for the year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.52 B (2025) | |

| Industry Publisher A | USD 1.50 B (2024) | The scope appears to blend domestic consumption with export-led value pools, and the pricing basis is not clearly tied back to Ethiopia retail and on-trade selling prices. A different base year can also change the value when global coffee prices swing. |

| Market Tracker B | USD 3.36 B (2025) | The scope reads like it extends beyond Ethiopia-only consumption by using broad application and geography framing, which can pull in non-comparable demand. Without clear local channel calibration, value totals can scale quickly even if underlying in-country volumes are modest. |

Across the table, the biggest driver is scope, especially whether export value pools or non-Ethiopia demand are folded into the same market number. When the sizing is kept aligned to domestic product sales and cross-checked with trade, channel, and pricing signals, the result is easier to trace back to a few repeatable steps and inputs.

Key Questions Answered in the Report

How large is the Ethiopia coffee market in 2026?

The Ethiopia coffee market size stands at USD 551.17 million in 2026, with a 6.74% CAGR projected to 2031.

Which segment is expanding fastest within Ethiopian coffee?

Instant coffee leads growth, recording a 7.78% CAGR as urban consumers favor convenience.

What share of Ethiopian coffee is Arabica?

Arabica accounts for 59.22% of 2025 output, maintaining dominance despite Robusta expansion.

How will roasted-coffee exports change by 2031?

Government strategy and new roasting plants aim to raise roasted coffee exports well above the current sub-1% share, capturing higher margins.

Page last updated on: