Esomeprazole Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Market Size (2026) | USD 2.13 Billion |

| Market Size (2031) | USD 2.87 Billion |

| Growth Rate (2026 - 2031) | 6.08% CAGR |

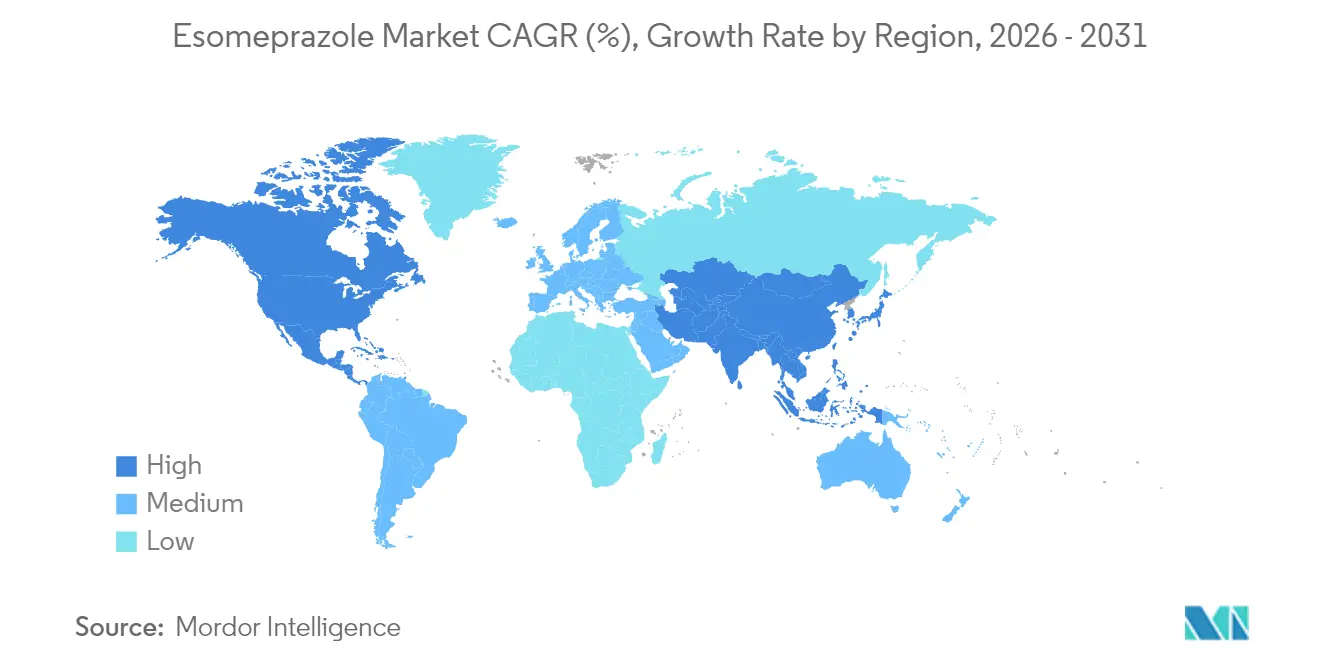

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Esomeprazole Market Analysis by Mordor Intelligence

The esomeprazole market size was valued at USD 2.01 billion in 2025 and estimated to grow from USD 2.13 billion in 2026 to reach USD 2.87 billion by 2031, at a CAGR of 6.08% during the forecast period (2026-2031). Steady demand arises from the continuing rise in gastroesophageal reflux disease (GERD) cases, which stand at 783.95 million worldwide, and from the therapeutic need for sustained acid suppression. Competitive pressure from potassium-competitive acid blockers (P-CABs) such as vonoprazan is intensifying, yet brand familiarity, broad clinical guidelines, and a large installed patient base support ongoing growth. North America leads with 40.44% revenue contribution, while Asia-Pacific posts the fastest 7.22% CAGR on the back of healthcare capacity expansion and rising GERD awareness. Tablets hold sway with a 46.77% revenue share, but capsules show the strongest 7.11% growth thanks to dual-release and nano-delivery innovations. Generic entries continue to expand, lowering prices and widening access, even as P-CAB alternatives challenge the traditional therapeutic paradigm.

Key Report Takeaways

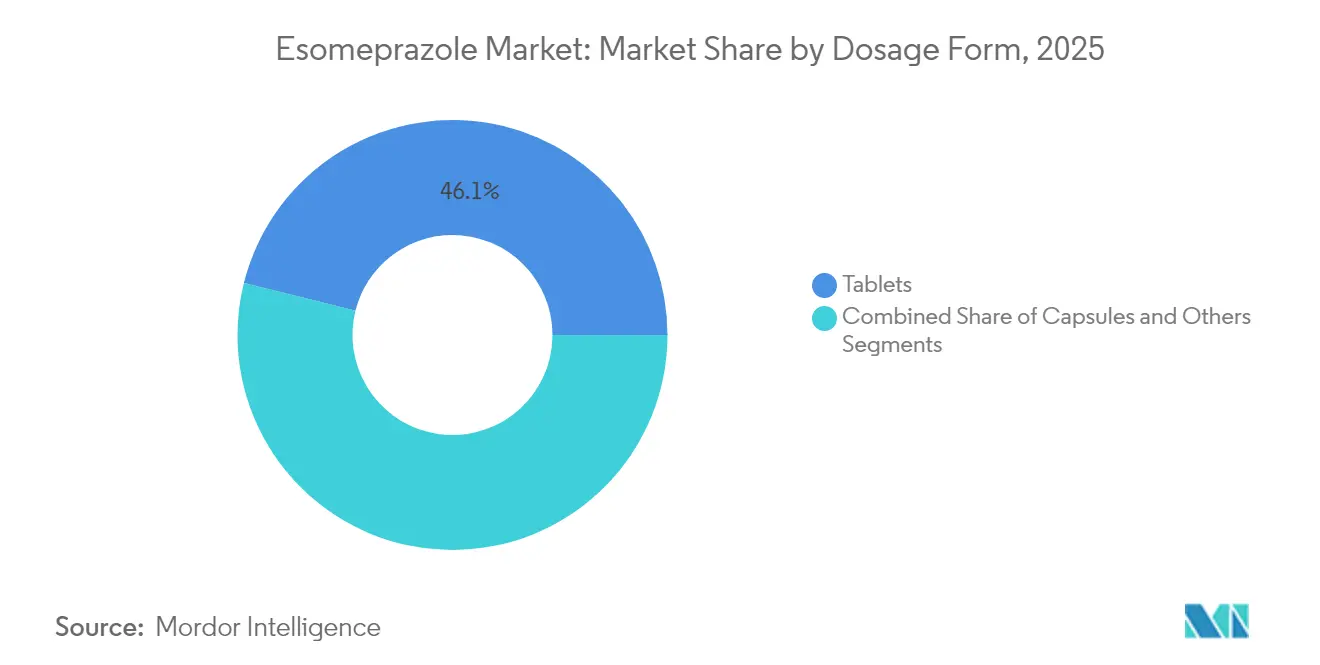

- By dosage form, tablets captured 46.12% of esomeprazole market share in 2025; capsules are projected to advance at a 6.98% CAGR through 2031.

- By strength, 20 mg held 64.72% share of the esomeprazole market size in 2025, while 40 mg strength is projected to expand at a 6.90% CAGR to 2031.

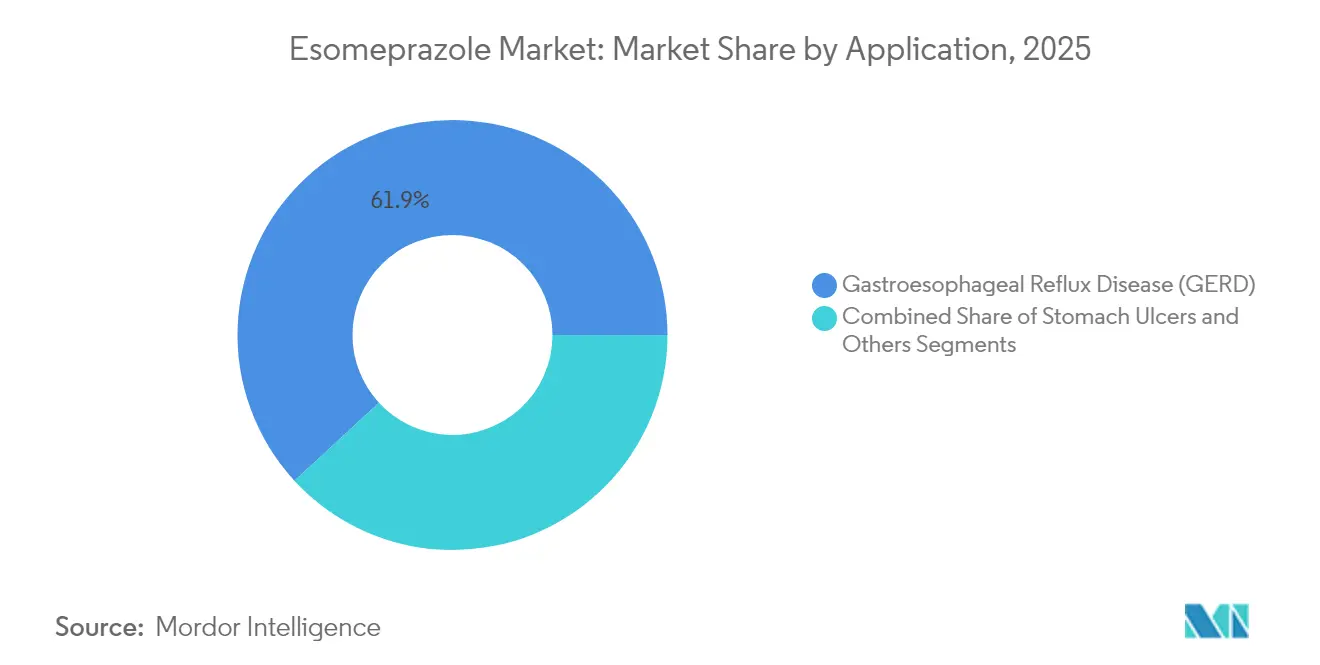

- By application, GERD accounted for 61.85% of the esomeprazole market size in 2025 and is forecast to grow at a 6.08% CAGR through 2031.

- By distribution channel, hospital pharmacies controlled 44.92% revenue share in 2025; online pharmacies are poised to record a 7.05% CAGR through 2031.

- By region, North America dominated with 40.12% revenue share in 2025, whereas Asia-Pacific is primed for a 7.08% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Esomeprazole Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing prevalence of GERD | +1.8% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) |

| Ageing population-linked gastric disorders | +1.2% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Rx-to-OTC switch momentum in key markets | +0.9% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Escalating demand for pediatric-approved PPIs | +0.7% | Global, with regulatory focus in US & EU | Medium term (2-4 years) |

| E-pharmacy penetration in emerging economies | +0.6% | Asia-Pacific, Latin America, MEA | Short term (≤ 2 years) |

| Nano- & dual-release formulation breakthroughs | +0.5% | Global, led by developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Prevalence of GERD

Rising global GERD incidence propels esomeprazole market demand as the disorder now affects up to one fifth of the global population. Direct medical spending in the United States alone reaches USD 9.3 billion annually. Turkey’s 23% prevalence mirrors rates in Western economies, while Asia-Pacific sees rising diagnosis given lifestyle shifts and better endoscopic access. Elderly patients face heightened risks of Barrett’s esophagus and adenocarcinoma, prompting longer treatment courses. Clinicians thus continue to rely on high-potency proton pump inhibitors, keeping the esomeprazole market on a firm growth footing.

Ageing Population-Linked Gastric Disorders

Demographic aging creates a deeper pool of chronic acid-related diseases that underpin esomeprazole market expansion. Lower esophageal sphincter pressure, reduced saliva flow, and impaired motility worsen reflux in older adults, even when symptoms feel milder. Polypharmacy and comorbidities compound gastric mucosal stress, leading physicians to prefer proven PPIs for long-term control. Payers in developed markets have adjusted formularies to accommodate chronic prescription use, reinforcing esomeprazole market prospects.

Rx-to-OTC Switch Momentum in Key Markets

Wider self-care access continues after Nexium 24HR and Japan’s Pariet S received switch approvals, showing regulators’ confidence in 14-day lower-dose regimens. Broader OTC availability lifts compliance and offers manufacturers a post-patent revenue extension strategy. Retail pharmacists now play a central educational role, guiding consumers on safe use. Momentum in Asia-Pacific and parts of Europe is set to widen the accessible patient base, providing a stable lift to the esomeprazole market.

Escalating Demand for Pediatric-Approved PPIs

Regulators have cleared weight-based pediatric dosing protocols that deliver 89% erosive esophagitis healing within eight weeks. Development of flavored granules and sprinkle-style capsules addresses swallowing challenges and drives incremental volume growth. Hospitals and specialists thus treat pediatric GERD more aggressively, enlarging the esomeprazole market’s total addressable patient group [1]U.S. Food and Drug Administration, "Clinical Pharmacology Review," fda.gov.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Generic price erosion & shrinking margins | -2.1% | Global, most severe in developed markets | Short term (≤ 2 years) |

| Long-term safety concerns | -0.8% | Global, regulatory focus in US & EU | Medium term (2-4 years) |

| Rapid uptake of P-CAB alternatives | -1.2% | Global, led by developed markets | Medium term (2-4 years) |

| API supply-chain volatility | -0.6% | Global, concentrated in Asia-Pacific sourcing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Generic Price Erosion & Shrinking Margins

Once key patents lapsed, a wave of approvals for capsules and suspensions drove list prices down by as much as 80%. Major generics players leverage low-cost active ingredient sourcing in India and China, intensifying price competition. Hospital formularies now favor the least-expensive bio-equivalent option, and direct-to-consumer platforms further compress margins, redirecting strategic focus toward volume rather than brand premium.

Long-Term Safety Concerns

Observational studies link extended PPI use to kidney dysfunction, bone fractures, and C. difficile infection, prompting guideline bodies to recommend periodic deprescribing. Regulatory agencies have increased pharmacovigilance requirements, nudging prescribers toward the lowest effective dose and shorter treatment duration. This headwind modestly tempers esomeprazole market growth, especially among older adults with polypharmacy profiles [2]Bijaya K. Padhi, "Adverse cardiovascular outcomes associated with proton pump inhibitor use after percutaneous coronary intervention: a systematic review and meta-analysis," BMC Cardiovascular Disorders, bmccardiovascdisord.biomedcentral.com.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Dosage Form: Tablets Lead Despite Capsule Innovation

Tablets controlled 46.12% of the esomeprazole market in 2025 as payers and prescribers gravitated toward the most budget-friendly solid oral form. Capsules, helped by dual-release and nano-delivery technologies, are expected to outpace with a 6.98% CAGR thanks to better nightly symptom control and patient adherence. The esomeprazole market size for tablets is poised to expand steadily, yet capsules will narrow the gap by 2031. Liquid suspensions and intravenous formulations fill specialized gaps in pediatrics and hospitalized acute care.

Capsule makers adopt enteric pellets that release drug in sequential pH zones, offering an immediate and sustained effect that improves mucosal healing rates. Tablet producers defend share with blister-pack redesigns and high-volume cost efficiencies . Hospital procurement committees weigh price ceilings against clinical differentiation, keeping competitive tension strong within the esomeprazole market.

By Strength: 20 mg Dominance Shifts Toward Higher Dosing

The 20 mg segment held 64.72% of esomeprazole market share in 2025 as it remains the guideline-recommended starting dose for typical GERD. High-dose 40 mg variants are projected to rise at a 6.90% CAGR, supported by clinician experience that dose escalation speeds mucosal healing in refractory cases. The esomeprazole market size for 40 mg is therefore widening faster than its lower-dose counterpart.

Ten-milligram sachets address pediatric weight-based regimens, while combination products such as esomeprazole-domperidone target motility disorders. Strength choice increasingly reflects personalized medicine trends as clinicians calibrate dosing to symptom severity, comorbidities, and nighttime breakthrough episodes.

By Application: GERD Applications Drive Core Demand

GERD contributed 61.85% of the esomeprazole market size in 2025, underscoring the chronicity of the disorder and its reliance on maintenance therapy. Stomach ulcers, supported by dual therapy with antibiotics for H. pylori eradication, are poised for a 6.94% CAGR by 2031. Zollinger-Ellison syndrome and other hypersecretory states provide niche demand for high-dose regimens, bolstering overall esomeprazole market resilience.

Guideline updates that favor early endoscopy in high-risk GERD cases support prescription renewals, while data showing 89% pediatric healing rates broaden the therapeutic base. Concomitant use after endoscopic submucosal dissection further embeds esomeprazole in varied clinical pathways.

By Distribution Channel: Hospital Pharmacies Face Online Disruption

Hospital pharmacies retained 44.92% revenue share in 2025 owing to integrated electronic prescribing and bundled procurement contracts. The esomeprazole market size flowing through online pharmacies is expected to climb at 7.05% CAGR as digital health adoption accelerates. Retail drugstores remain pivotal for OTC 20 mg packs, but rapid home delivery platforms are steadily capturing refill volumes.

Institutional buyers emphasize acquisition cost, creating a battleground for generics. Online models differentiate via transparent pricing and subscription refills, attracting chronic users who seek both convenience and savings. Hospital and retail incumbents respond with click-and-collect options to defend share in the esomeprazole market.

Geography Analysis

North America dominated with a 40.12% revenue share in 2025, anchored by GERD awareness programs, wide insurance coverage, and mature generic distribution. The esomeprazole market size in the region will remain substantial through 2031 as aging demographics heighten acid-related morbidity. Europe holds a balanced profile where strong generic uptake meets stringent pharmacovigilance, keeping volumes high but pricing tight.

Asia-Pacific is forecast to register a 7.08% CAGR, the fastest worldwide, driven by rising living standards, urban dietary shifts, and expanded endoscopic services. Local makers have introduced both PPIs and P-CABs, fostering price competition yet also elevating treatment penetration. Emerging regions in Latin America and the Middle East experience rising PPI use as public insurance schemes broaden formulary coverage, though currency volatility and distribution gaps temper upside. Europe maintains a significant market presence through established pharmaceutical manufacturing capabilities and comprehensive healthcare systems that support chronic disease management protocols. The region's regulatory environment promotes generic competition while maintaining quality standards, creating balanced market dynamics between innovation and affordability. Emerging markets in the Middle East and Africa, along with South America, represent growth opportunities driven by healthcare infrastructure development and increasing pharmaceutical access, though market penetration remains constrained by economic factors and regulatory complexities.

Competitive Landscape

The esomeprazole market features moderate concentration. AstraZeneca retains strong brand equity through legacy Nexium promotion, yet its share is diluted by robust generic competition from Teva, Aurobindo, and Sun Pharmaceutical. Players compete on cost efficiency, cGMP compliance, and supply reliability as hospital tenders favor lowest unit price.

Formulation innovation is a key differentiator. Dual-release, nano-encapsulated, and pediatrics-optimized versions draw clinician interest and command modest premium pricing. Market entrants must also navigate the P-CAB advance; Phathom’s vonoprazan approval underscores acid suppression paradigms shifting towards faster, more potent agents.

Strategic partnerships for localized manufacturing and OTC brand building remain central to defending share in the esomeprazole market.

Esomeprazole Industry Leaders

-

Teva Pharmaceutical Industries Ltd.

-

Amneal Pharmaceuticals LLC

-

Viatris Inc.

-

DAIICHI SANKYO COMPANY, LIMITED

-

Sun Pharmaceutical Industries Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: The National Drug Scheduling Advisory Committee recommended that esomeprazole OTC packs above 280 mg move to Schedule II in Canada.

- May 2025: FDA announced a recall of 1,584,780 single-dose esomeprazole suspension packs due to impurity deviations.

- April 2025: Aurobindo Pharma secured final FDA approval for 10 mg delayed-release oral suspension.

- June 2024: Glenmark Specialty gained FDA clearance to market 20 mg delayed-release OTC capsules in the United States.

Global Esomeprazole Market Report Scope

As per the scope of the report, esomeprazole is a type of proton pump inhibitor that is used for treating gastrointestinal diseases such as peptic ulcers, Zollinger-Ellison Syndrome, etc. It lowers the acidic level by decreasing its production in the stomach. The Esomeprazole Market is Segmented by Dosage Type (Tablets, Capsules, and Others), Application (Gastroesophageal Reflux Disease (GERD), Stomach Ulcers, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Tablets |

| Capsules |

| Others |

| 20 mg |

| 40 mg |

| Others |

| Gastroesophageal Reflux Disease (GERD) |

| Stomach Ulcers |

| Others |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Dosage Form | Tablets | |

| Capsules | ||

| Others | ||

| By Strength | 20 mg | |

| 40 mg | ||

| Others | ||

| By Application | Gastroesophageal Reflux Disease (GERD) | |

| Stomach Ulcers | ||

| Others | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current esomeprazole market size?

The esomeprazole market size stood at USD 2.13 billion in 2026 and is projected to reach USD 2.87 billion by 2031.

Which region leads esomeprazole revenue?

North America leads with a 40.12% share in 2025, buoyed by widespread GERD diagnosis and insurance coverage.

Why are capsules growing faster than tablets?

Capsules integrate dual-release and nano-delivery technologies that deliver longer acid suppression, driving a 6.98% CAGR through 2031.

How significant is generic competition?

Generic entries now sell at up to 80% lower prices than legacy brands, prompting hospitals and insurers to prioritize cost-efficient sourcing.

Are safety concerns limiting long-term use?

Regulators advise periodic review because chronic use may raise risks such as kidney issues and bone fractures, though therapeutic benefits often outweigh risks when managed appropriately.

Page last updated on: