Epitaxy Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

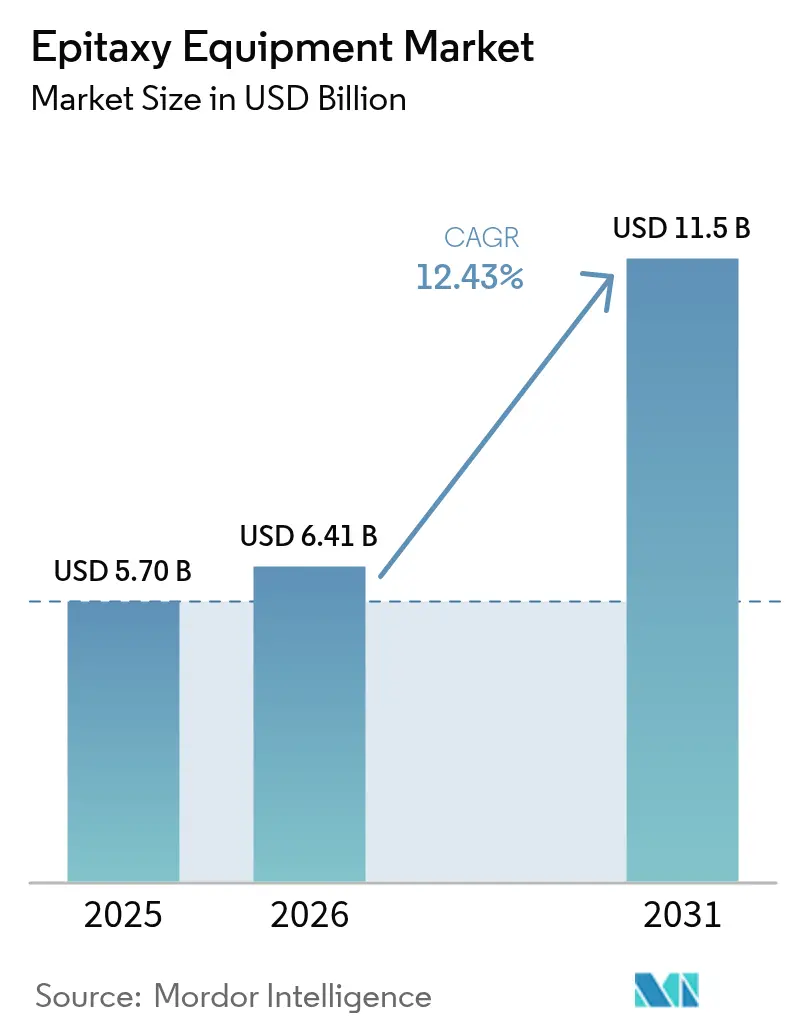

| Market Size (2026) | USD 6.41 Billion |

| Market Size (2031) | USD 11.5 Billion |

| Growth Rate (2026 - 2031) | 12.43% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Epitaxy Equipment Market Analysis by Mordor Intelligence

The epitaxy equipment market size was valued at USD 5.7 billion in 2025 and estimated to grow from USD 6.41 billion in 2026 to reach USD 11.5 billion by 2031, at a CAGR of 12.43% during the forecast period (2026-2031). Demand increases as compound semiconductor manufacturers scale capacity for electric-vehicle power modules, 5G base-station front-end chips, and high-brightness LED backlighting. Precision epitaxial layers on silicon-carbide and gallium-nitride substrates now dictate performance in high-power and high-frequency devices, encouraging integrated-device manufacturers to pivot capital budgets away from legacy silicon tools. U.S. CHIPS Act allocations exceeding USD 300 million dedicated to epitaxy lines confirm the process as a sovereignty priority. Equipment suppliers answer with larger-wafer reactors, tighter process-control software, and flexible multi-material chambers, preserving yield while lowering cost per die. However, lengthy tool-qualification cycles and precursor price swings continue to temper near-term shipment rhythms even as long-term growth fundamentals remain intact.

Key Report Takeaways

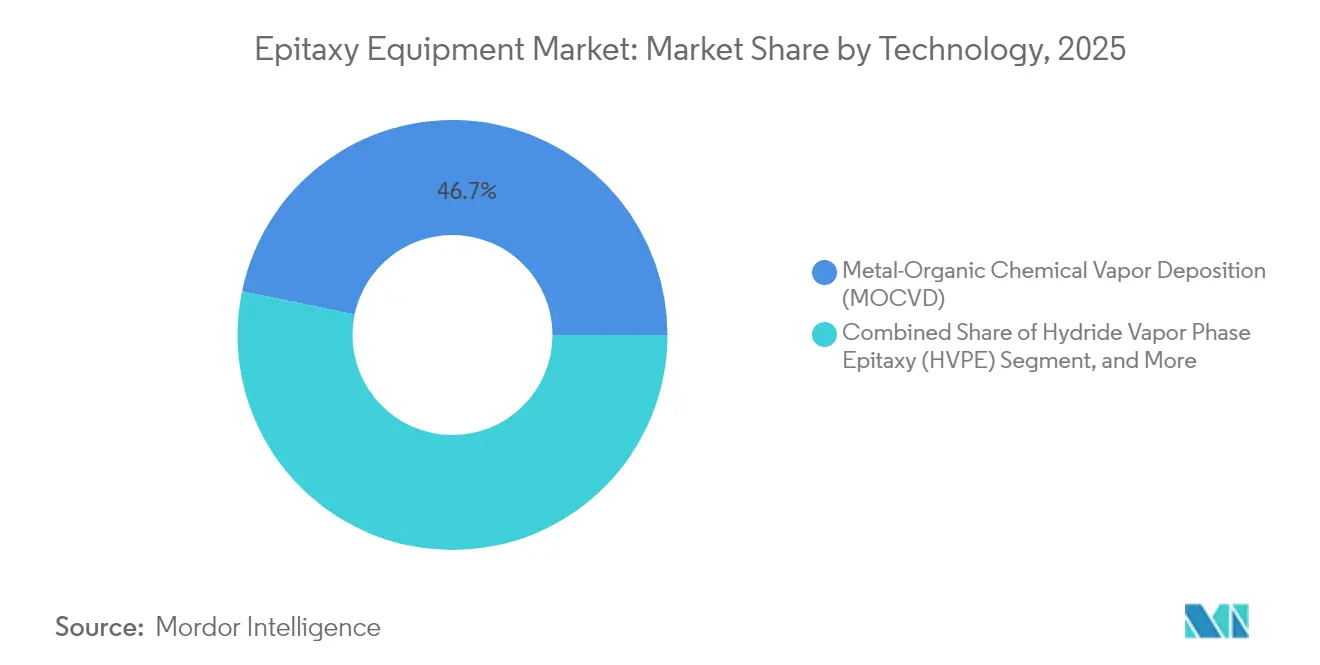

- By technology, metal-organic chemical vapor deposition held 46.73% of the epitaxy equipment market share in 2025.

- Remote-plasma CVD is forecast to expand at a 13.35% CAGR through 2031, the quickest among deposition technologies.

- By application, compound-semiconductor devices captured 52.10% revenue share in 2025; wide-bandgap materials are advancing at a 13.52% CAGR to 2031.

- By material, silicon carbide accounted for 71.05% of the epitaxy equipment market size in 2025, while gallium-nitride tools are growing at a 15.65% CAGR through 2031.

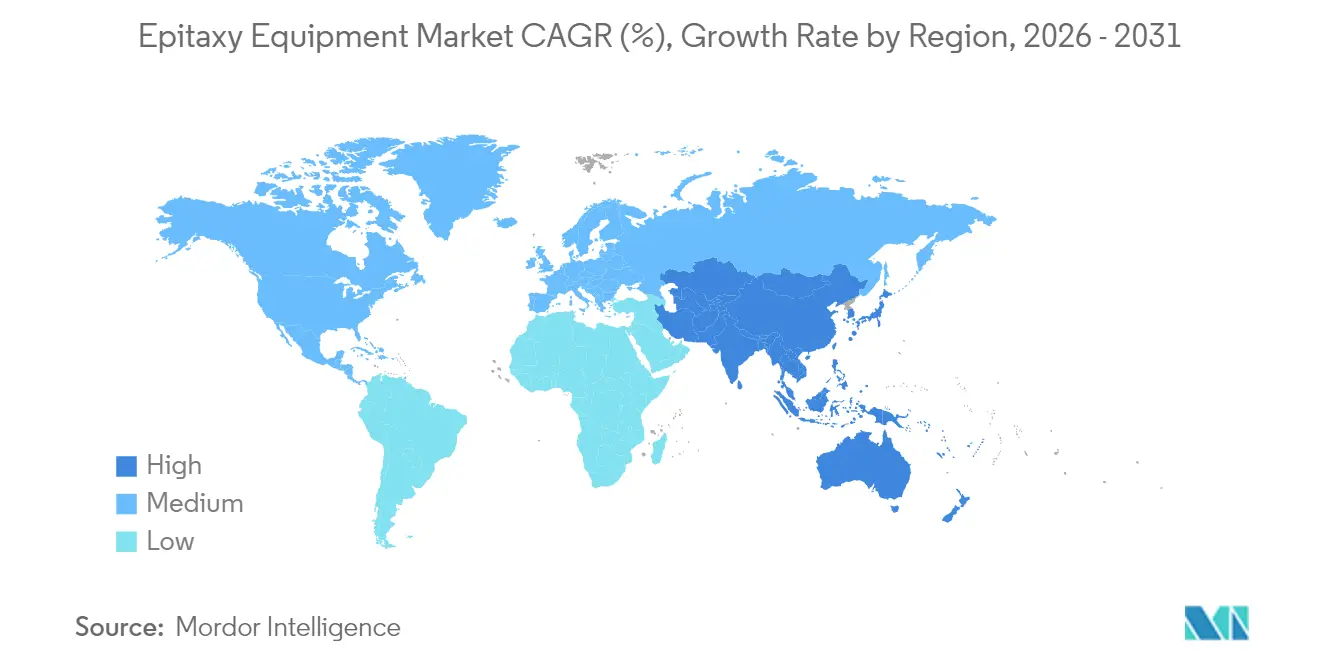

- By region, North America commanded 43.25% revenue in 2025; Asia-Pacific records the fastest CAGR of 15.22% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Epitaxy Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing demand for high-brightness LEDs | +2.10% | APAC core, spill-over to North America | Medium term (2-4 years) |

| Rapid electrification of powertrains in EVs | +2.80% | Global, with early gains in North America, Europe, China | Long term (≥ 4 years) |

| Expansion of 5G/6G compound-semiconductor front-end modules | +1.80% | Global, concentrated in APAC and North America | Medium term (2-4 years) |

| Government incentives for SiC/GaN capacity build-out | +2.20% | North America & EU, selective APAC markets | Short term (≤ 2 years) |

| Adoption of gallium-oxide (β-Ga₂O₃) devices | +0.80% | Global R&D centers, early commercial in Japan, US | Long term (≥ 4 years) |

| Transition to 8- and 12-inch GaN-on-Si epitaxy lines | +1.50% | Global, led by advanced fabs in Taiwan, Korea, US | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand for High-Brightness LEDs

MicroLED and mini-LED adoption in premium displays and automotive lighting causes LED makers such as San’an Optoelectronics to book multi-system MOCVD orders. Throughput upgrades must coincide with lower defect density across 6- and 8-inch wafers, keeping Veeco’s Lumina platform backlog elevated.[1]Compound Semiconductor Staff, “PlayNitride Selects Veeco MOCVD System,” compoundsemiconductor.net Automotive daytime-running lamps and adaptive-beam headlamps also require higher luminous flux, which in turn pushes epitaxy specifications for GaN layer uniformity. These combined forces translate into a predictable equipment-replacement cycle every three to four years, fortifying mid-term shipment trajectories.

Rapid Electrification of Powertrains in EVs

Automakers migrate to 800 V architectures, accelerating silicon-carbide MOSFET and diode uptake that demands epitaxial layers grown at ≥1,600 °C. Tokyo Electron’s high-temperature CVD tool bookings rose in tandem with Bosch securing USD 225 million in CHIPS Act grants for Alabama SiC lines.[2]U.S. Department of Commerce, “CHIPS Act Funding Announcements,” commerce.gov The move from 150 mm to 200 mm SiC substrates compels both new-tool investments and retrofit kits across global fabs. Because power-module yields are hypersensitive to micropipe density and doping drift, device makers award purchase orders only after months of process-recipe co-engineering, extending revenue recognition yet building an entrenched installed base.

Expansion of 5G/6G Compound-Semiconductor Front-End Modules

Gallium-nitride high-electron-mobility transistors outperform LDMOS in 3–8 GHz 5G bands, prompting base-station OEMs to expand GaN-on-SiC epitaxy lines. Research alliances led by Imec validate GaN and indium-phosphide scaling for 140 GHz 6G concepts, keeping university and pilot-fab tools active.[3]IEEE Authors, “MOCVD Reactor Optimization Research,” ieeexplore.ieee.org Mobile handset suppliers mirror infrastructure trends by qualifying GaN RF switches to curb heat and extend battery life. Combined, these infrastructure and consumer rollouts widen the demand funnel for premium-grade epitaxy systems over the medium term.

Government Incentives for SiC/GaN Capacity Build-Out

Public funding under the U.S. CHIPS Act and the European Chips Act covers a share of capex for domestic epitaxy and substrate plants. Coherent won USD 79 million to scale SiC epitaxy in Texas, while IntelliEPI received USD 10.3 million for military-grade MBE R&D.[4]U.S. Department of Commerce, “CHIPS Act Funding Announcements,” commerce.gov Subsidies mandate local supply commitments, tilting near-term orders toward home-region tool suppliers and accelerating lead times for qualifying new reactor designs. The incentive wave compresses a five-year capacity pipeline into a two-year window, creating backlog peaks but also heightening competition for skilled process engineers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complexities associated with reactor design | -1.90% | Global, affecting all major equipment suppliers | Medium term (2-4 years) |

| Volatile prices and supply of specialty precursors | -1.10% | Global, with acute impact in Asia-Pacific | Short term (≤ 2 years) |

| Lengthy tool qualification cycles at IDMs and foundries | -0.80% | Global, concentrated at tier-1 semiconductor fabs | Medium term (2-4 years) |

| High capex for next-gen high-temperature reactors | -0.60% | Global, affecting capacity expansion decisions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Complexities Associated With Reactor Design

As fabs request dual-material or 300 mm chambers, computational-fluid-dynamics models must reconcile laminar gas flow with sharp temperature gradients, lengthening R&D cycles. Suppliers therefore integrate multi-zone heaters, motorized injector plenums, and in-situ spectroscopic ellipsometry, driving up bill-of-materials and software validation costs. These engineering hurdles defer revenue and raise the entry barrier for latecomers.

Volatile Prices and Supply of Specialty Precursors

Metal-organic trimethylgallium and trichlorosilane depend on a handful of purification plants; any outage ripples through MOCVD throughput within a month. The high-purity precursor market grew with a high CAGR in 2024 but remains concentrated in fewer than ten global vendors. Supply shocks force LED fabs to idle reactors, cutting utilization and delaying new-tool ROI. To mitigate risk, device makers push for multi-source qualification, extending procurement cycles and inflating raw-material buffers, a cost that indirectly weighs on tool investments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: MOCVD Retains Scale Advantages While RPCVD Surges

Metal-organic chemical vapor deposition occupied 46.73% of the epitaxy equipment market share in 2025 on the back of its entrenched position in LED and GaN power devices. The segment’s scale enables incremental wafer-size increases without catastrophic redesign, sustaining repeat orders. Remote-plasma CVD, though, is projected to post a 13.35% CAGR as lower-temperature processing opens doors to fragile substrates and tighter interface control. The epitaxy equipment market size for RPCVD tools is expected to reach USD 1.59 billion by 2031. MBE and hydride vapor-phase epitaxy remain niche, favored for ultra-pure heterostructures and thick GaN substrates, respectively, while HT-CVD dominates SiC layers exceeding 20 µm thickness. Across all platforms, suppliers position multi-material flexibility as a hedge against future technology nodes.

A second competitive angle revolves around advanced process-control stacks. Tier-one fabs increasingly insist on closed-loop emissivity-corrected pyrometry and machine-learning fault detection, features most readily retrofitted to MOCVD and RPCVD architectures. Consequently, average selling prices rise faster than unit volumes, cushioning margins even as entry-level Chinese tools crowd the LED subsegment. Open-platform software ecosystems emerge as another differentiator, enabling fabs to port recipes across vendor hardware and thus shorten qualification cycles.

By Application: Compound Semiconductors Lead, Wide-Bandgap Demand Accelerates

Compound-semiconductor device manufacturing captured 52.10% of 2025 revenue, driven by RF amplifiers, LiDAR VCSELs, and photonics transceivers. Yet the fastest uplift stems from wide-bandgap materials used in electric-vehicle inverters and telecom power supplies, advancing 13.52% annually. The epitaxy equipment market size for wide-bandgap applications stood at USD 2.28 billion in 2025 and could surpass USD 4.88 billion by 2031. Photonics lines, especially indium-phosphide PICs, benefit from hyperscale data-center optics, evidenced by Coherent tripling InP output at its Texas site. MEMS foundries, though smaller, rely on custom epitaxial stacks for pressure sensors and RF filters, carving a steady yet specialized equipment niche.

The diversity of end-use cases forces equipment makers to supply modular reactors configurable between SiC, GaN, and InP within the same fab footprint. Such adaptability protects capex budgets from sudden demand shifts. Concurrently, partnerships between tool vendors and chemical suppliers aim to co-optimize precursor flow dynamics, improving film stoichiometry and unlocking new device architectures such as GaN vertical transistors.

By Wafer Size: Migration to 300 mm Gains Traction

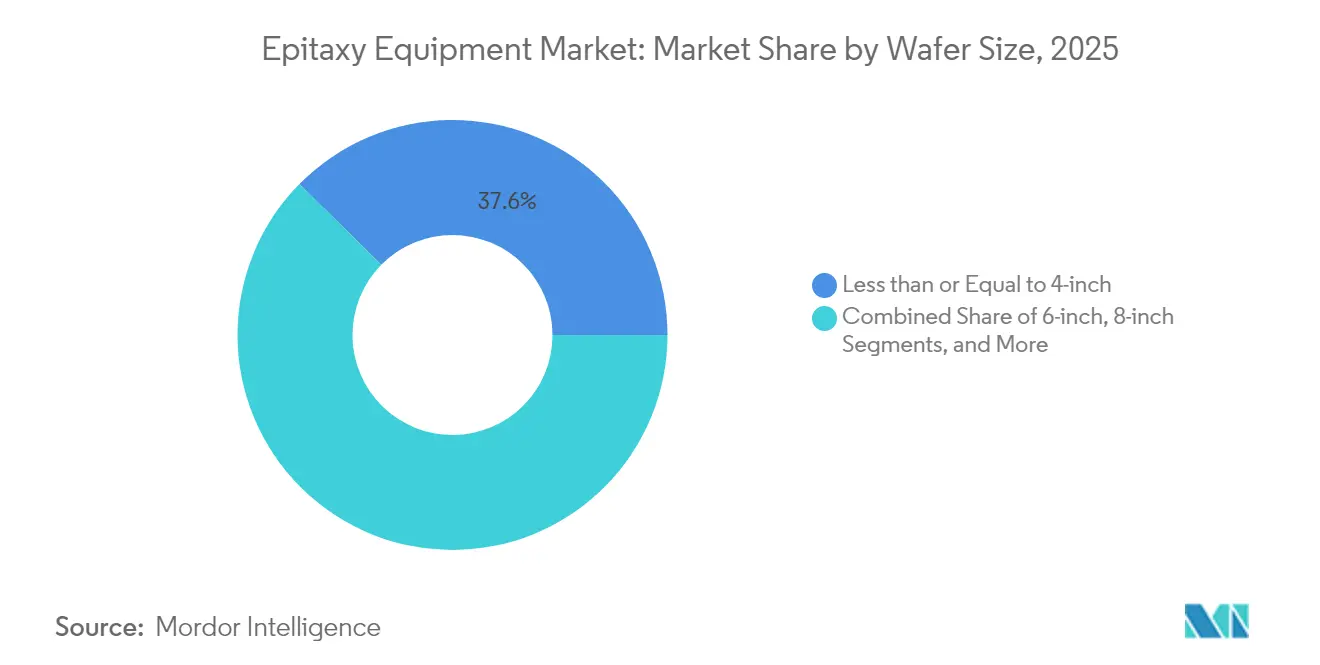

Wafers of Less than or Equal to 4-inch diameter still represent 37.62% of units because universities and pilot lines rely on small substrates for exotic compounds. Nevertheless, 12-inch systems exhibit the highest 14.92% CAGR, propelled by microLED, GaN power IC, and advanced RF programs. Line-item quotations show that a single 300 mm GaN MOCVD reactor can replace three 150 mm tools, cutting fab footprint by 30%. The epitaxy equipment market size allocated to 12-inch tools could top USD 3.22 billion by 2031. Intermediate 6- and 8-inch nodes serve as stepping-stones for SiC and InP, balancing yield risk with cost savings.

Engineering hurdles revolve around center-to-edge uniformity. Suppliers combat radial temperature drift with multi-zone susceptor heaters and rotating showerheads. Demand for in-situ metrology rises accordingly: real-time PL mapping and pyrometric feedback now ship standard on most 300 mm installations. Such features shorten recipe development, enhancing the value proposition despite higher list prices.

By Material: SiC Dominance Meets GaN Momentum

Silicon-carbide commanded 71.05% of revenue in 2025 thanks to automotive and renewable-energy inverters. Yet gallium-nitride tool revenue is growing 15.65% annually, poised to reshape shipment mix by 2031. The epitaxy equipment market share split will likely compress as GaN power ICs move from 650 V to 1,200 V classes, requiring thicker epitaxial layers and therefore more sophisticated reactors. III-V arsenides and phosphides remain essential for optoelectronics, while research into β-Ga₂O₃ attracts grant-funded prototype tools aimed at ≥3.3 kV devices. Process recipes diverge markedly: SiC favors hot-wall graphite reactors and high partial pressures of silane, whereas GaN leans on cold-wall metal-organic flow and ammonia overpressure, compelling OEMs to maintain distinct product lines.

Material-specific subsidy programs amplify the split. U.S. and German car OEMs invest directly in SiC lines to secure traction-inverter supply, whereas telecom players co-finance GaN RF capacity. As both camps scale, metrology packages fine-tune oxygen and carbon contamination levels to below 1×10¹⁵ cm⁻³, an imperative for defect-free drift zones.

Geography Analysis

North America preserved a 43.25% revenue share in 2025, supported by dense clusters in Texas, Arizona, and upstate New York. CHIPS Act disbursements flow to both greenfield fabs and brownfield upgrades, anchoring long-term demand for domestic epitaxy capacity. Coherent’s Sherman campus, for instance, tripled InP device output to meet AI optical-link demand. Local sourcing rules embedded in government contracts tilt procurement toward resident suppliers, bolstering order pipelines even as exchange-rate swings temper export competitiveness.

Asia-Pacific represents the fastest-growing theater with a 15.22% CAGR through 2031. Chinese LED houses such as HC SemiTek accumulate MOCVD install bases that already exceed 2,500 reactors, driving unit-volume leadership. Simultaneously, South Korean memory giants invest in compound-semiconductor roadmaps for CXL photonics and HBM power delivery, widening the regional addressable market. Tokyo Electron’s net sales climb to YEN 654.5 billion in Q1 2025 underscores the pull-through effect on upstream tool vendors.

Europe concentrates on automotive electrification and resilient aerospace supply chains. Programs under the European Chips Act channel subsidies to SiC epi fabs in Germany and Sweden, while French institutes pilot 200 mm GaN-on-Si lines for radar and satellite payloads. Local environmental regulations expedite adoption of low-global-warming-potential process gases, prompting European fabs to specify upgraded abatement modules. Although the region trails in unit volumes, it excels in high-margin specialty tools and research-grade MBE systems tailored for quantum-computing materials.

Competitive Landscape

Incumbent suppliers Tokyo Electron, Aixtron, and Applied Materials jointly delivered over half of 2024 shipment value, reflecting moderate concentration. Each differentiates via proprietary showerhead geometries, multi-zone heaters, and recipe-transfer software that lock customers into upgrade paths. Average selling price resilience offsets cyclical volume dips, preserving gross margins above 40%. Meanwhile, Veeco’s focus on 300 mm GaN platforms secures strategic wins at display and power startups, raising competitive intensity in the premium tier.

Emerging Chinese manufacturers leverage cost advantages to penetrate first-generation LED lines but struggle to match the uniformity specifications demanded by SiC and high-frequency GaN fabs. Some Western IDMs impose export-control vetting, effectively gating high-temperature reactor adoption outside OECD supply chains. Consequently, market entrants often pursue joint ventures with established brands to gain process IP and customer trust.

Technology roadmaps gravitate toward closed-loop machine learning analytics that predict particle excursions before yield hits occur. Aixtron and Applied Materials pilot edge AI modules that correlate real-time chemiluminescence signals with wafer-level defects, promising up to 3% yield uplift. Intellectual-property litigation occasionally surfaces around plasma-source designs, indicating intangible assets as a core battleground. Despite these skirmishes, supply-chain resilience efforts push customers to adopt multi-vendor strategies, sustaining healthy rivalry without triggering destructive price wars.

Epitaxy Equipment Industry Leaders

Aixtron SE

Applied Materials, Inc.

Tokyo Electron Limited

Veeco Instruments Inc.

LPE S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: PlayNitride qualified Veeco’s Lumina MOCVD system for microLED production and ordered two additional reactors for 2025 delivery.

- February 2025: Coherent reported a record USD 1.43 billion quarterly revenue, citing AI transceiver demand and tripled InP output.

- December 2024: Coherent received USD 33 million CHIPS Act funding to expand InP capacity.

- December 2024: II-VI completed its USD 7.01 billion acquisition of Coherent, consolidating laser and epitaxy portfolios.

Global Epitaxy Equipment Market Report Scope

Epitaxy is commonly done through chemical vapor deposition, which is basically a process that forms a non-volatile solid film on a substrate from reactions of the appropriate chemical vapors. The market has been segmented on the basis of application and geography.

| Metal-Organic Chemical Vapor Deposition (MOCVD) |

| Hydride Vapor Phase Epitaxy (HVPE) |

| High-Temperature Chemical Vapor Deposition (HT-CVD) |

| Molecular Beam Epitaxy (MBE) |

| Remote-Plasma CVD (RPCVD) |

| Photonics |

| Semiconductors |

| Wide-Bandgap Materials |

| Micro-Electro-Mechanical Systems (MEMS) |

| Others |

| Less than or Equal to 4-inch |

| 6-inch |

| 8-inch |

| 12-inch |

| Greater than 12-inch |

| III-V (GaAs, InP) |

| GaN |

| SiC |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Technology | Metal-Organic Chemical Vapor Deposition (MOCVD) | ||

| Hydride Vapor Phase Epitaxy (HVPE) | |||

| High-Temperature Chemical Vapor Deposition (HT-CVD) | |||

| Molecular Beam Epitaxy (MBE) | |||

| Remote-Plasma CVD (RPCVD) | |||

| By Application | Photonics | ||

| Semiconductors | |||

| Wide-Bandgap Materials | |||

| Micro-Electro-Mechanical Systems (MEMS) | |||

| Others | |||

| By Wafer Size | Less than or Equal to 4-inch | ||

| 6-inch | |||

| 8-inch | |||

| 12-inch | |||

| Greater than 12-inch | |||

| By Material | III-V (GaAs, InP) | ||

| GaN | |||

| SiC | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What revenue does the epitaxy equipment market generate in 2026?

The epitaxy equipment market size stands at USD 6.41 billion in 2026.

Which technology currently leads unit shipments?

Metal-organic chemical vapor deposition commands 46.73% shipment share because of its entrenched use in LED and GaN devices.

Why are SiC tools seeing strong demand from automakers?

Transition to 800 V electric-vehicle architectures requires low-defect SiC epitaxial layers for inverters and onboard chargers.

Which region is growing fastest for new reactor installations?

Asia-Pacific records a 15.22% CAGR through 2031, fueled by Chinese LED expansion and Korean memory investments.

How will 12-inch wafer tools impact cost structure?

A single 300 mm reactor can replace three 150 mm tools, reducing fab footprint by 30% and lowering cost per die.

What is the biggest supply-chain risk for epitaxy production?

Limited sources of high-purity metal-organic precursors create price volatility and potential reactor idle time.

Page last updated on: