EPA And DHA Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

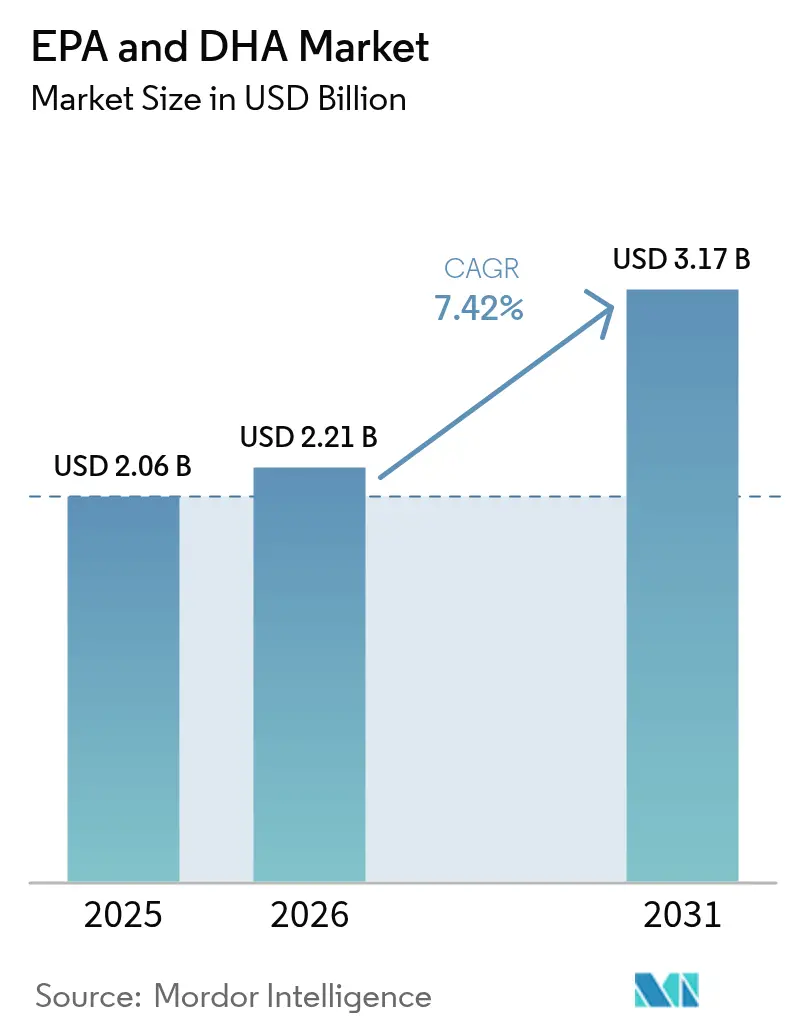

| Market Size (2026) | USD 2.21 Billion |

| Market Size (2031) | USD 3.17 Billion |

| Growth Rate (2026 - 2031) | 7.42% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

EPA And DHA Market Analysis by Mordor Intelligence

EPA and DHA market size in 2026 is estimated at USD 2.21 billion, growing from the 2025 value of USD 2.06 billion, with 2031 projections showing USD 3.17 billion, growing at 7.42% CAGR over 2026-2031. Strong clinical evidence, favorable regulatory frameworks, and the scaling of algae-based production drive the EPA and DHA market. Rapid adoption of prescriptions following the REDUCE-IT cardiovascular outcomes trial, coupled with real-time oxidation controls that extend shelf life, supports market growth. North America continues to lead due to robust healthcare reimbursement policies, while the Asia-Pacific region benefits from swift regulatory approvals and growing health awareness. Diversifying raw material sourcing toward algae reduces reliance on Peruvian anchovy quotas, mitigating supply volatility, while quality certifications enhance consumer confidence. Ongoing investments in sustainable algae cultivation and process innovation are expected to enhance cost efficiency and support long-term market expansion.

Key Report Takeaways

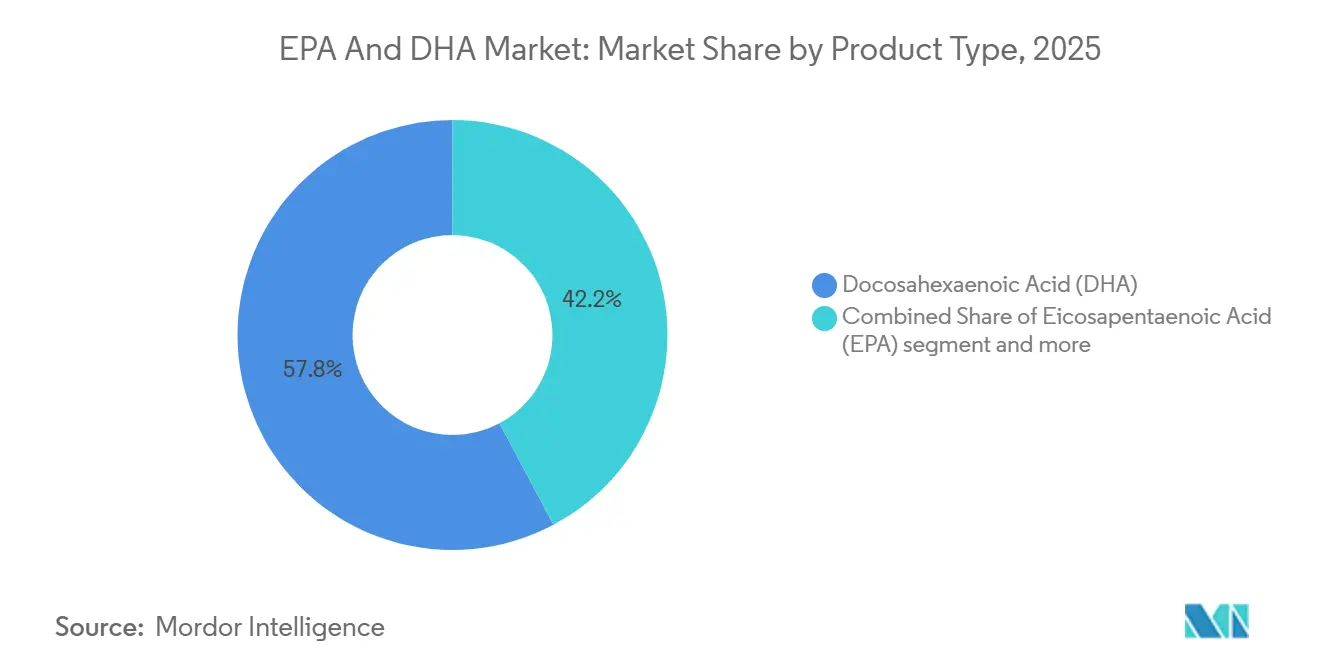

- By source, fish oil accounted for 60.92% of the EPA and DHA market share in 2025, whereas algae oil is projected to advance at an 8.63% CAGR through 2031.

- By product type, DHA captured 57.78% of the EPA and DHA market size in 2025, while EPA is forecast to post the fastest growth rate of 7.86% from 2025 to 2031.

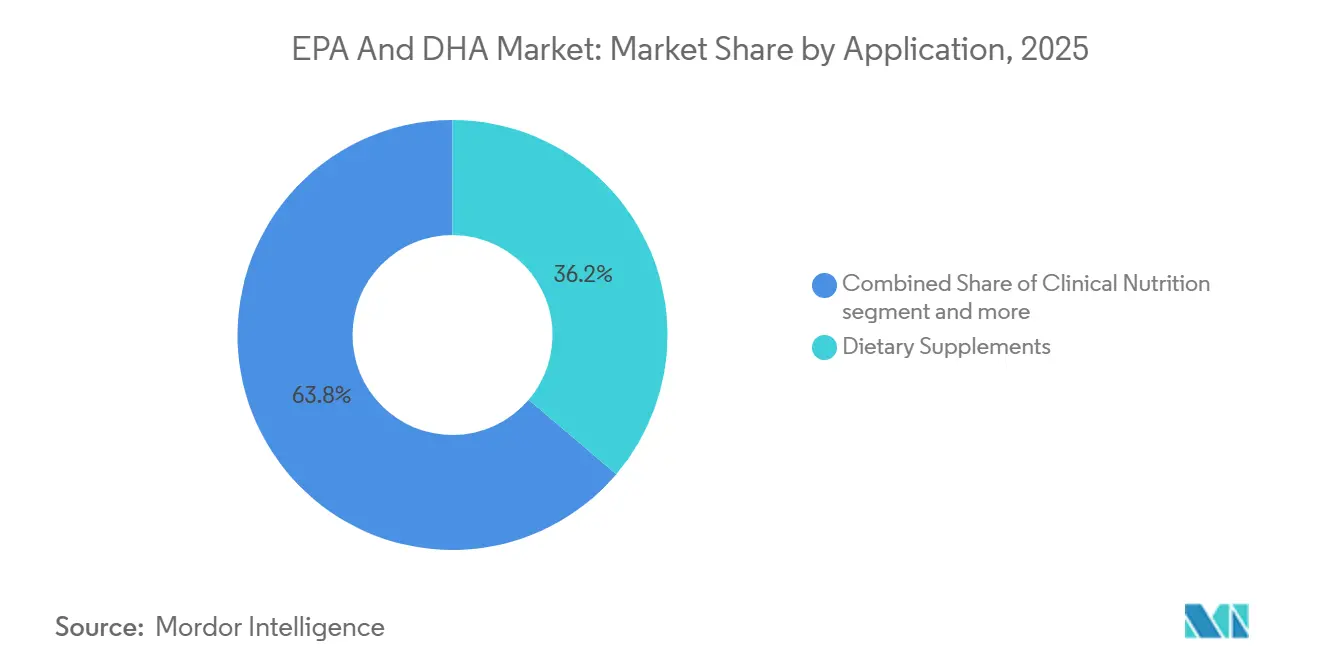

- By application, dietary supplements led with 36.21% revenue share in 2025; clinical nutrition and medical foods are expected to expand at a 8.72% CAGR to 2031.

- By geography, North America held 40.88% of the EPA and DHA market share in 2025, and the Asia Pacific is poised for the quickest 8.19% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global EPA And DHA Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Clinical evidence for high-dose EPA | +1.5% | North America and Europe | Medium term (2-4 years) |

| Uptake of >90% purity concentrates | +1.2% | North America and Europe, APAC | Short term (≤ 2 years) |

| Vegan demand lifting algae DHA | +0.8% | North America and Western Europe | Long term (≥ 4 years) |

| Regulatory and certification gains | +1.1% | North America and Europe, APAC | Medium term (2-4 years) |

| Prenatal DHA guidelines | +0.9% | APAC core, MEA, LATAM | Long term (≥ 4 years) |

| Real-time oxidation monitoring | +1.0% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Clinical evidence for high-dose EPA

Findings from the landmark REDUCE-IT trial, which highlighted a 25% reduction in major adverse cardiovascular events with icosapent ethyl, have led to significant shifts in global clinical practice guidelines and regulatory approvals. Following these findings, the FDA greenlit high-dose EPA formulations aimed at reducing cardiovascular risks in patients with elevated triglycerides [1]Source: U.S. Food and Drug Administration, “GRAS Notice Inventory,” fda.gov . This move has birthed a new prescription drug category, with projections soaring past USD 4 billion by 2030. Notably, an Asian subgroup analysis from REDUCE-IT revealed an even more pronounced benefit (HR 0.72) than the overall population. This insight has spurred regulatory submissions across APAC markets, especially given the region's escalating burden of cardiovascular diseases. The distinct mechanism of EPA, in contrast to combined EPA/DHA formulations, has led pharmaceutical firms to reformulate their products. This shift has resulted in supply chain premiums for high-purity EPA concentrates. Beyond prescriptions, nutraceutical companies are capitalizing on REDUCE-IT data for structure-function claims. However, regulatory bodies remain vigilant, drawing clear lines between therapeutic uses and dietary supplements. The ripple effect of this evidence has reached medical society guidelines. Both the American Heart Association and the European Society of Cardiology have integrated omega-3 recommendations, influencing clinical nutrition protocols.

Uptake of more than 90% purity concentrates

Pharmaceutical-grade omega-3 concentrates, boasting over 90% purity, have become staples in prescription formulations. This shift is largely due to their enhanced bioavailability and the resulting ease of patient compliance. A prime example of this trend is BASF's K85EE platform. It features 800-880 mg/g of total omega-3 ethyl esters, with an EPA content ranging from 430-495 mg/g, showcasing the technical prowess driving these prescription applications. Transitioning from 30-40% crude fish oil to over 90% concentrates demands cutting-edge molecular distillation and chromatographic separation technologies [2]Source: BASF, “K85EE Omega-3-Acid Ethyl Esters,” basf.com. Such advancements create entry barriers, favoring established players with the necessary processing capabilities. In medical nutrition, there's a growing emphasis on specific concentrate grades. This focus ensures therapeutic dosing fits within practical serving sizes, especially for conditions needing a daily intake of 2-4 grams of EPA/DHA. In a significant industry move, KD Pharma Group acquired DSM-Firmenich's marine lipids business in October 2024. This consolidation not only boosted concentrate production capacity but also crowned the combined entity as the globe's leading omega-3 manufacturer, granting it heightened pricing leverage in the pharmaceutical-grade market. The trend isn't limited to traditional sources; algae-based production is also in the spotlight. Companies like Corbion are pushing boundaries, achieving over 50% DHA concentrations in their AlgaPrime products, thanks to their unique fermentation and purification methods.

Vegan demand lifting algae DHA

Plant-based omega-3 alternatives have moved from niche markets to mainstream shelves. Algae-derived EPA and DHA now match fish oil prices in concentrated forms. In 2024, Veramaris boasted a 50% production surge, while Nature's Bounty rolled out algae-based products, eyeing the 79 million Americans on plant-based diets. The sustainability angle strikes a chord with younger consumers: algae farming spares marine ecosystems and offers omega-3s identical to those from fish. Regulatory bodies are catching up: Health Canada greenlit Nutriterra's plant-based omega-3 oil in December 2024, and EFSA recognized several algae-derived DHA products as novel foods. Thanks to tech leaps in fermentation and processing, production costs have plummeted by about 30% since 2022, making algae a cost-competitive alternative to fish oil. Moreover, the appeal of algae isn't just about being vegan; it sidesteps the heavy metals and pollutants often linked to marine ingredients.

Regulatory and certification gains

Major markets have harmonized their regulatory frameworks, simplifying compliance and broadening access to omega-3 ingredients and products. Starting February 2025, EFSA's updated guidance will streamline applications for algae-derived omega-3s, all while upholding stringent safety assessments. The International Fish Oil Standards (IFOS) program now certifies over 1,000 products worldwide, and GOED's lab recognition ensures consistent testing across regions. China's NMPA framework designates DHA as an approved nutrient supplement and classifies fish oil as a non-nutrient raw material, clarifying market entry strategies [3]Source: China National Medical Products Administration, “Health Food Raw Materials Catalogue,” nmpa.gov.cn. India's FSSAI regulations allow algal/fungal DHA in infant nutrition at 0.2-0.5% limits, unlocking significant opportunities in the world's most populous nation. This regulatory alignment fosters global product platforms but respects local compliance, slashing development costs and speeding up market entry for multinational omega-3 suppliers. As concerns over oxidation grow, quality standards have adapted, with real-time monitoring now a hallmark of premium products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile anchovy quotas tightening fish-oil supply | -0.7% | Global, with acute impact on Peru-dependent supply chains | Short term (≤ 2 years) |

| High cost of purification and advanced extraction | -0.5% | Global, with greater impact on emerging markets | Medium term (2-4 years) |

| Regional market fragmentation | -0.4% | Global, with highest impact in emerging markets and developing regulatory frameworks | Long term (≥ 4 years) |

| Heavy-metal and dioxin contamination concerns prompting stricter testing costs | -0.3% | Global, with emphasis on EU, North America, and premium market segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regional market fragmentation

Disparate regulatory frameworks across major markets complicate compliance and create barriers to entry, constraining global omega-3 trade flows and inflating operational costs for multinational suppliers. While EFSA's novel food approvals facilitate access to the European market, China's NMPA framework mandates distinct documentation and testing protocols, potentially extending product launch timelines by 12 to 18 months. This fragmentation poses challenges, especially for smaller companies that lack the regulatory expertise and resources to simultaneously navigate multiple approval processes. As a result, market concentration is increasingly favoring established players with global compliance capabilities. Labeling requirements differ markedly across jurisdictions; some markets allow structure-function claims, while others limit therapeutic positioning. This divergence compels companies to maintain multiple product variants and diverse marketing strategies. Furthermore, the regulatory landscape varies in terms of quality standards: while IFOS certification might be adequate for certain markets, others demand local testing and documentation. Such discrepancies not only escalate compliance costs but also complicate the supply chain. Additionally, trade barriers like import tariffs and registration fees further fragment the global market. Some regions adopt protectionist policies, bolstering domestic omega-3 suppliers at the expense of international competitors.

Heavy-metal and dioxin contamination concerns prompting stricter testing costs

Heightened regulatory scrutiny over persistent organic pollutants and heavy metals in marine-sourced omega-3 products has led to increased testing requirements and compliance costs throughout the supply chain. The European Union has set stringent maximum limits for dioxins, PCBs, and heavy metals. Meeting these standards demands sophisticated analytical methods, costing between USD 500 and 1,500 per batch. Some premium suppliers even conduct tests at multiple stages of production. As contamination concerns grow, consumers are increasingly turning to algae-based alternatives. This shift is largely because fermentation-based production methods sidestep the bioaccumulation risks tied to marine food chains. The complexity of testing has surged; modern analytical methods can now detect lower concentration thresholds. This advancement necessitates investments in cutting-edge laboratory equipment and specialized expertise, a challenge for smaller suppliers. With regulators tightening limits, there's a looming compliance risk. Historical contamination levels that once met standards might soon surpass future thresholds, compelling suppliers to either reformulate products or change sourcing. As consumers become more aware of contamination issues, brands are elevating quality assurance as a key marketing differentiator. Many are investing in third-party certifications and transparency initiatives. While these efforts bolster market credibility, they also inflate costs. Fish oil suppliers, especially those in areas plagued by industrial pollution or agricultural runoff, feel the weight of these testing burdens. This has inadvertently created a geographic advantage for production facilities nestled in pristine marine environments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: EPA Accelerates Despite DHA Dominance

In 2025, DHA holds a commanding 57.78% share of the market, underscoring its strong foothold in both infant formula applications and cognitive health supplements. Meanwhile, EPA is on a rapid ascent, boasting an 7.86% CAGR through 2031, fueled by the burgeoning expansion of cardiovascular prescription drugs. The pivotal outcomes from the REDUCE-IT trial have spurred a surge in EPA-centric product development. In response, pharmaceutical firms are reengineering their combination products, placing a heightened emphasis on EPA content, especially for cardiovascular uses, as sanctioned by the FDA. Blend formulations strike a balance, providing cost efficiency and a wide array of benefits, making them a favored choice for dietary supplement manufacturers in search of adaptable ingredient platforms.

EPA's upward momentum is in sync with the precision medicine movement, which leans towards targeted therapeutic uses. Clinical studies highlight EPA's unique mechanisms of action, setting it apart from DHA, which primarily serves structural membrane roles. This heightened focus on cardiovascular health has led to a surge in supply chain premiums for high-purity EPA concentrates. Notably, BASF's K85EE platform, utilizing cutting-edge molecular distillation, boasts an impressive EPA content ranging from 430-495 mg/g. While DHA continues to reign supreme, thanks in part to regulatory nods in major markets for infant nutrition, such as FSSAI's green light for algal/fungal DHA in Indian infant formulas, set at 0.2-0.5% limits. The segmentation by type is evolving, emphasizing application-specific optimizations over a one-size-fits-all omega-3 approach, thereby fueling product differentiation and premium pricing strategies.

By Source: Algae Oil Gains Momentum Amid Fish Oil Constraints

In 2025, fish oil commands a 60.92% market share. Meanwhile, algae oil surges at an 8.63% CAGR through 2031, buoyed by maturing production technologies and heightened sustainability mandates. Peru's anchovy quota recovery, surpassing 98% fulfillment in 2024, has stabilized fish oil availability post-El Niño disruptions. However, climate change forecasts hint at escalating volatility in marine supply chains. Krill oil carves out a premium niche, boasting phospholipid delivery benefits. Simultaneously, marine sources like squid and mussel emerge as diversification avenues for specialized applications.

Algae oil's rapid ascent is driven by technological strides in fermentation optimization and downstream processing, slashing production costs by about 30% since 2022. Veramaris celebrated a 50% production boost in 2024, while Corbion's AlgaPrime platform, through its unique algae cultivation techniques, achieved concentrations exceeding 50% DHA. The sustainability narrative strikes a chord with younger consumers and institutional buyers, who prioritize environmental, social, and governance criteria in their procurement choices. Regulatory bodies are quickening their pace: Health Canada greenlit Nutriterra's plant-based omega-3 oil in December 2024, and EFSA conferred novel food status to several algae-derived products. As omega-3 demand surges, outpacing the availability of traditional marine resources, the trend of source diversification underscores a strategic move in supply chain risk management.

By Application: Clinical Nutrition Emerges as Growth Driver

In 2025, dietary supplements dominate the market with a 36.21% share, bolstered by rising consumer self-care trends and aggressive direct-to-consumer marketing. Meanwhile, clinical nutrition and medical foods are on a growth trajectory, boasting a 8.72% CAGR through 2031, as healthcare systems increasingly adopt omega-3 protocols for managing chronic diseases. The infant formula segment remains stable and regulated, showcasing consistent demand. At the same time, fortified food and beverages are on the rise, thanks to technological advancements in oxidation control and sensory optimization. Pharmaceutical applications, especially those related to cardiovascular indications post-REDUCE-IT trial validation, command premium pricing following prescription drug approvals. The swift expansion of the clinical nutrition segment underscores a strategic shift in healthcare. There's a growing emphasis on preventive nutrition interventions, steering away from traditional reactive treatments.

Notably, esteemed medical societies, such as the American Heart Association and the European Society of Cardiology, have woven omega-3 recommendations into their clinical guidelines. This endorsement has spurred institutional demand for standardized therapeutic formulations. In a surprising twist, pet nutrition has emerged as a significant growth catalyst. This diversification in applications underscores omega-3's transformation from a mere commodity supplement to a sought-after therapeutic ingredient. This evolution not only allows for premium positioning but also facilitates margin expansion across diverse end markets. Furthermore, the FDA's GRAS determinations for pet food applications have ushered in greater regulatory clarity. Complementing this, third-party certifications from IFOS bolster quality assurance, reinforcing professional endorsements.

Geography Analysis

In 2025, North America commands a dominant 40.88% share of the EPA and DHA market, bolstered by the FDA's robust regulatory framework. This framework not only endorses dietary supplements but also prescription drug applications for omega-3 products. The region's well-established clinical research infrastructure substantiates therapeutic claims, and its strong healthcare reimbursement systems have spurred the adoption of prescription omega-3s, especially post the REDUCE-IT trial validation. In a nod to innovative and sustainable sourcing, Canada's Health Canada greenlit Nutriterra's plant-based omega-3 oil in December 2024. The mature supplement market in North America is increasingly prioritizing quality, with third-party certifications playing a pivotal role. Notably, IFOS-certified products are fetching premium prices, justifying investments in advanced processing. Meanwhile, Mexico's burgeoning middle class and modernizing healthcare present lucrative expansion avenues. Furthermore, the USMCA trade agreements are streamlining regulatory processes, bolstering cross-border trade in omega-3 products.

Asia Pacific is on track to be the fastest-growing region, boasting an 8.19% CAGR through 2031. This surge is fueled by demographic shifts, notably aging populations and urbanization, coupled with escalating healthcare expenditures. These factors are amplifying the demand for omega-3s across various therapeutic applications. China's NMPA framework is paving the way for international suppliers by clearly designating DHA as an approved nutrient supplement. Additionally, it recognizes fish oil as a permissible non-nutrient raw material. In India, the FSSAI has set concentration limits of 0.2-0.5% for algal and fungal DHA in infant nutrition. This move is particularly significant, given the potential market expansion for the 24 million infants born annually. Japan's regulatory landscape is equally advanced, listing omega-3 fatty acids in its Foods with Function Claims positive list. South Korea's MFDS is set to re-evaluate health functional ingredients in 2025. The region's rapid growth can be attributed to a regulatory modernization that adeptly balances consumer protection with a nod to innovation, fostering a thriving omega-3 market.

Europe's omega-3 market is witnessing steady growth, thanks in part to EFSA's stringent novel food approval process. This process has successfully granted regulatory status to several algae-derived omega-3 products, including the DHA 550 oil from Schizochytrium sp., a brainchild of Fermentalg. European consumers, increasingly leaning towards sustainability, are favoring algae-based alternatives and sustainably sourced fish oils. This trend is steering premium positioning strategies that highlight both environmental responsibility and health benefits. While Brexit introduced some regulatory hiccups, bilateral agreements have ensured that omega-3 products maintain their market access between the UK and the EU. Furthermore, regulatory harmonization among EU member states is simplifying compliance challenges, all while upholding stringent safety standards. This consistency is bolstering consumer trust in omega-3 products. The European market is also placing a premium on transparency and traceability, with stringent supply chain documentation favoring suppliers with robust quality systems. Emerging markets in South America, the Middle East, and Africa are showcasing promise, buoyed by evolving regulatory frameworks. Local production initiatives, such as Corbion's AlgaPrime facility in Brazil, underscore a strategic alignment with regional demand growth.

Competitive Landscape

The EPA and DHA market exhibits moderate concentration, indicating strategic consolidation opportunities as evidenced by KD Pharma Group's acquisition of DSM-Firmenich's marine lipids business in October 2024, positioning the combined entity as the world's largest omega-3 manufacturer. This move not only positions the newly formed entity as the world's leading omega-3 manufacturer but also highlights a trend in the industry: a shift towards vertical integration and scale advantages in producing pharmaceutical-grade concentrates. Meanwhile, smaller players are carving out niches, focusing on specialized applications and innovative sourcing methods.

Companies that boast diversified sourcing, cutting-edge processing technologies, and a deep understanding of regulatory landscapes across various jurisdictions are finding themselves at an advantage. These capabilities create formidable barriers to entry, favoring established entities with robust omega-3 platforms. Moreover, the deployment of advanced technologies has emerged as a key differentiator in the competitive arena. Firms are channeling investments into real-time oxidation monitoring, state-of-the-art purification techniques, and eco-friendly production methods, all in a bid to tap into premium market segments.

Aker BioMarine's recent strategic pivot, highlighted by its USD 590 million divestiture of the Feed Ingredients business to American Industrial Partners, underscores its commitment to prioritizing high-value human nutrition applications. Furthermore, the industry is eyeing white-space opportunities in precision nutrition, unique delivery formats, and burgeoning markets with fluid regulatory landscapes. The patent landscape is buzzing with innovation, spotlighting advancements in microencapsulation, boosting bioavailability, and refining algae cultivation methods. This trend underscores the industry's belief that technological prowess is paramount for a competitive edge. Meanwhile, GOED's initiative to recognize third-party laboratories has set a benchmark for quality testing, shifting the industry's focus from mere purity claims to the more nuanced aspects of sourcing sustainability and transparency in the supply chain.

EPA And DHA Industry Leaders

BASF SE

KD Pharma Group

Koninklijke DSM NV

Croda International PLC

Aker BioMarine ASA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Nuseed Nutritional selected Connoils as the exclusive partner to produce and distribute Nutriterra DHA Canola oil in powder formats through low-temperature electrostatic dehydration, enabling plant-based omega-3 applications in beverages and functional foods.

- April 2025: Epax launched Epax Evolve 05, the first commercially available very long chain polyunsaturated fatty acid concentrate containing 10x the VLC-PUFA content of crude fish oil, with EFSA novel food clearance and self-affirmed GRAS status in the United States.

- October 2024: KD Pharma Group completed the acquisition of DSM-Firmenich's marine lipids business, creating the world's largest omega-3 manufacturer with enhanced pharmaceutical-grade concentrate production capabilities and a global distribution network.

- October 2024: Aker BioMarine signed a strategic distribution partnership with Barentz International to expand krill oil product distribution across Italy, San Marino, Belgium, the Netherlands, and Luxembourg, strengthening European market presence.

Global EPA And DHA Market Report Scope

EPA (eicosapentaenoic acid) and DHA (docosahexaenoic acid) are long-chain omega-3 fatty acids from various vegetable and animal sources. The EPA and DHA Market Report is Segmented by Product Type (Eicosapentaenoic Acid, Docosahexaenoic Acid, Blends), Source (Fish Oil, Algae Oil, Krill Oil, Other Marine Sources), Application (Dietary Supplements, Infant Formula, Fortified Food and Beverages, Pharmaceuticals, and More), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Eicosapentaenoic Acid (EPA) |

| Docosahexaenoic Acid (DHA) |

| Blends |

| Fish Oil |

| Algae Oil |

| Krill Oil |

| Other Marine Sources |

| Dietary Supplements |

| Infant Formula |

| Fortified Food and Beverages |

| Pharmaceuticals |

| Clinical Nutrition and Medical Foods |

| Pet Nutrition |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Product Type | Eicosapentaenoic Acid (EPA) | |

| Docosahexaenoic Acid (DHA) | ||

| Blends | ||

| By Source | Fish Oil | |

| Algae Oil | ||

| Krill Oil | ||

| Other Marine Sources | ||

| By Application | Dietary Supplements | |

| Infant Formula | ||

| Fortified Food and Beverages | ||

| Pharmaceuticals | ||

| Clinical Nutrition and Medical Foods | ||

| Pet Nutrition | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the EPA and DHA market in 2026?

The EPA and DHA market size reached USD 2.21 billion in 2026 and is forecast to hit USD 3.17 billion by 2031 at a 7.42% CAGR.

Which region grows the fastest for EPA and DHA-based products?

Asia Pacific leads growth with an 8.19% CAGR thanks to regulatory modernization in China and India plus aging demographics.

Why is algae oil gaining share in omega-3 supply?

Advances in fermentation have cut production costs 30% since 2022, and algae avoids fish-stock volatility while meeting sustainability goals.

What drives prescription demand for EPA concentrates?

Cardiovascular guidelines now favor high-dose EPA after the REDUCE-IT trial showed a 25% risk reduction in major events.

How volatile are fish-oil supplies?

Peruvian anchovy quotas, impacted by climate cycles, trimmed fish-oil output 21% in 2023 and remain a supply risk despite a 2024 rebound.

Page last updated on: