Market Overview

| Study Period | 2019 - 2030 |

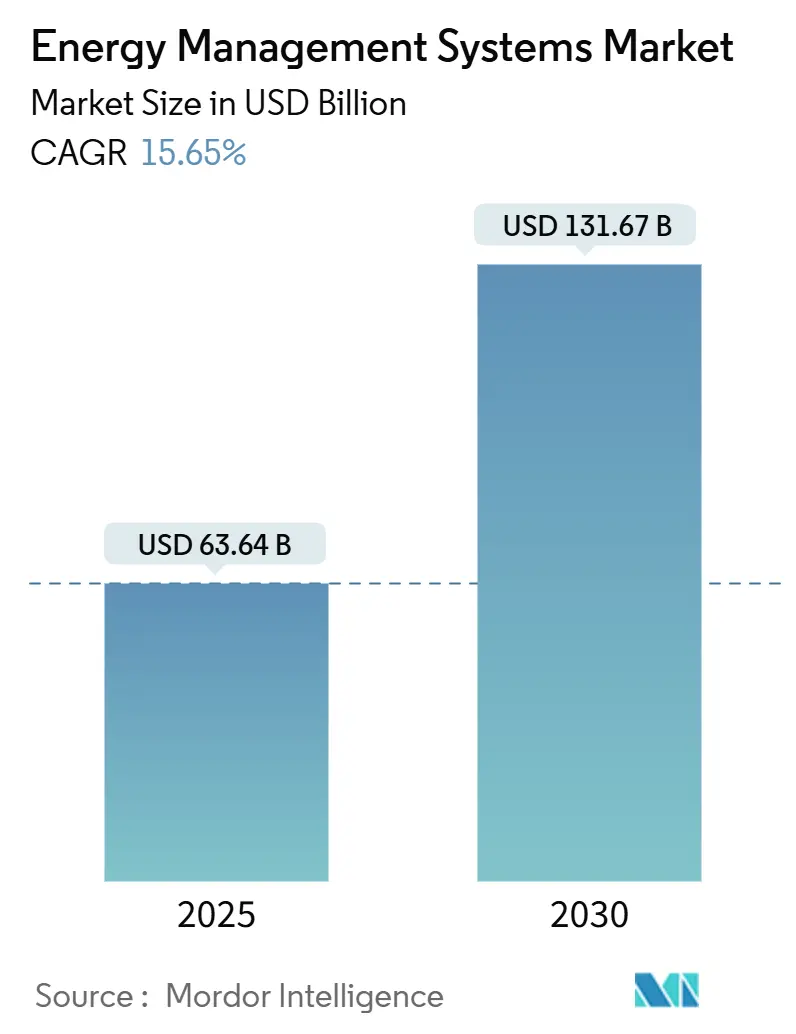

| Market Size (2025) | USD 63.64 Billion |

| Market Size (2030) | USD 131.67 Billion |

| Growth Rate (2025 - 2030) | 15.65% CAGR |

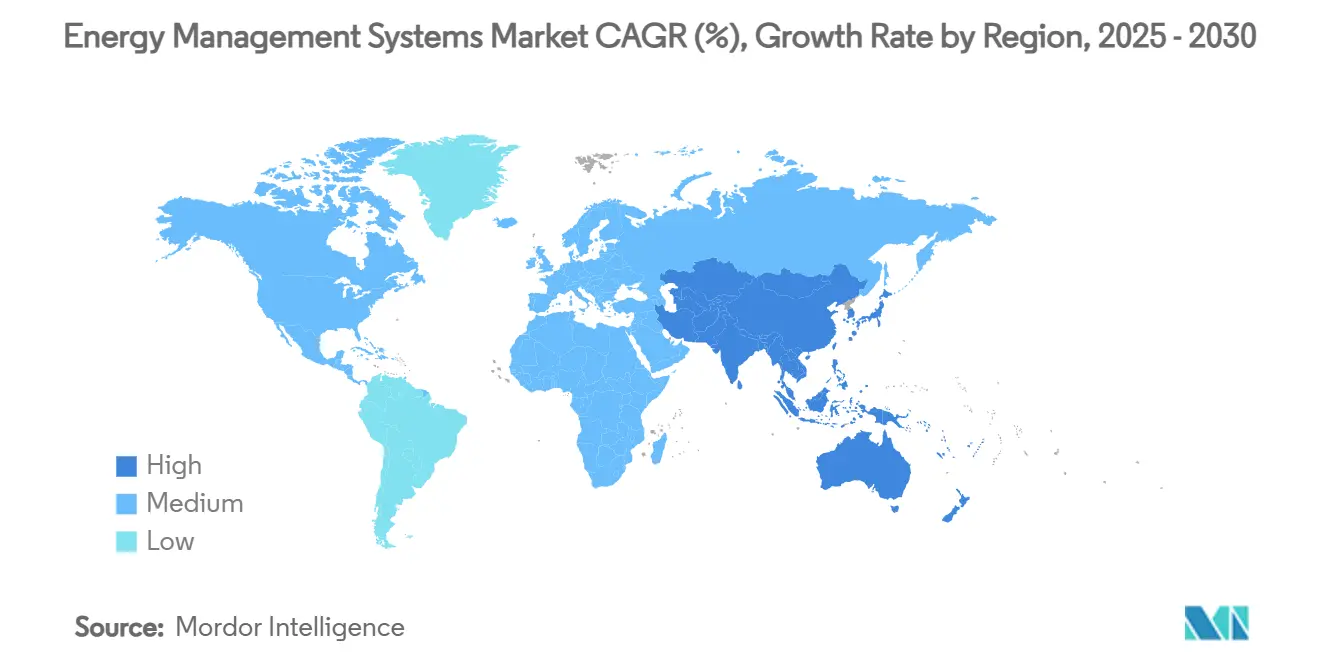

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

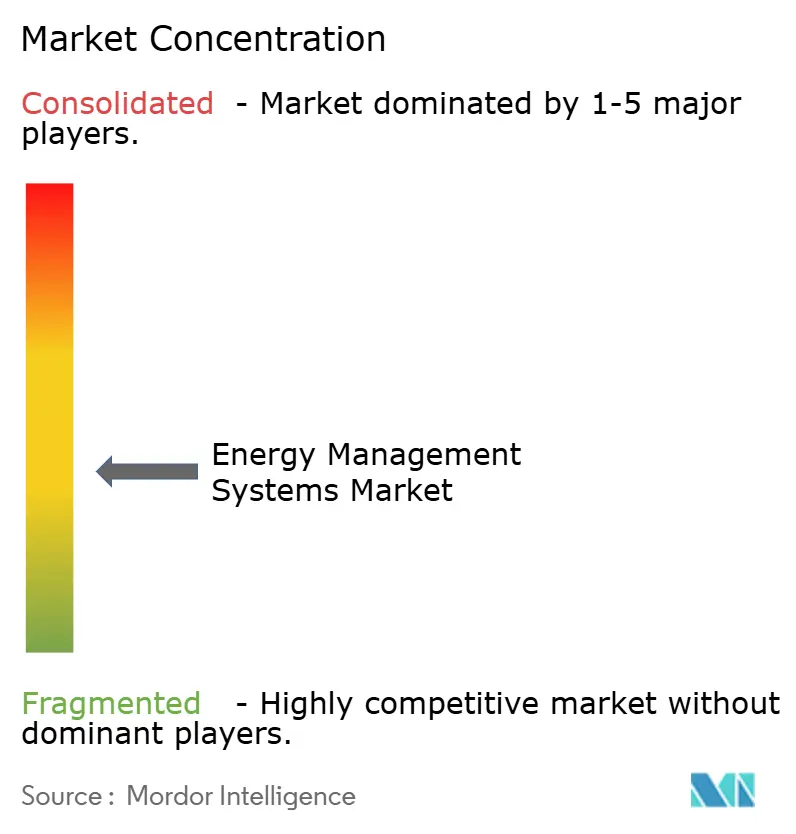

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Energy Management Systems Market Analysis by Mordor Intelligence

The Energy Management Systems market size reaches USD 63.64 billion in 2025 and is forecast to climb to USD 131.67 billion by 2030, advancing at a 15.65% CAGR. The surge reflects stricter decarbonization rules, rapid smart-grid deployment, and mounting corporate net-zero targets that elevate real-time energy optimization from optional to indispensable. Utilities are rolling out advanced metering infrastructure (AMI) at scale, giving operators the granular data they need to pair with AI-driven analytics for self-healing grid functions and lower operating costs. Commercial real-estate owners face mandatory net-zero building codes starting in 2026, driving a jump in demand for connected HVAC, lighting, and controls platforms. Meanwhile, firms signing large renewable power-purchase agreements require integrated systems capable of hourly tracking, certificate management, and carbon accounting. Beyond climate policy, volatile commodity prices and growing carbon costs sharpen the economic case for the Energy Management Systems market, as enterprises chase double-digit savings and resilience against supply-side shocks.

Key Report Takeaways

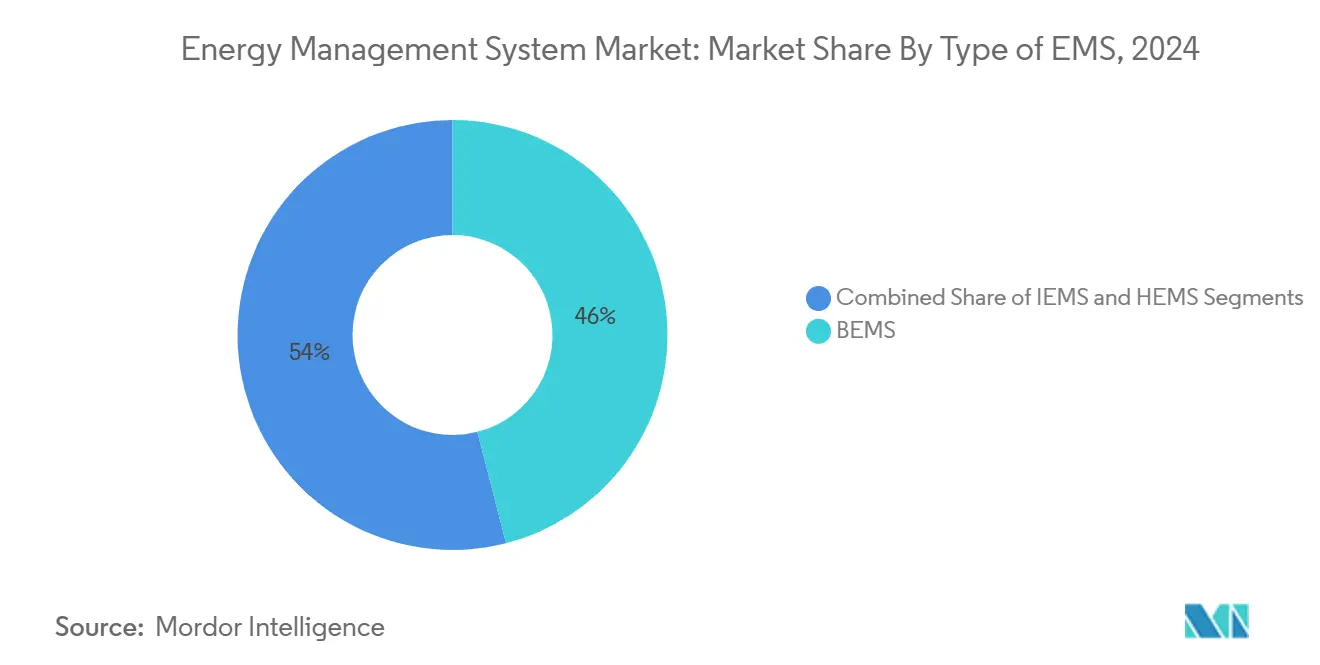

- By EMS type, Building Energy Management Systems led with 46.0% of Energy Management Systems market share in 2024, while Home Energy Management Systems are projected to expand at a 17.2% CAGR through 2030.

- By end user, the manufacturing segment held 31.4% share of the Energy Management Systems market size in 2024; healthcare facilities record the highest projected CAGR at 16.25% to 2030.

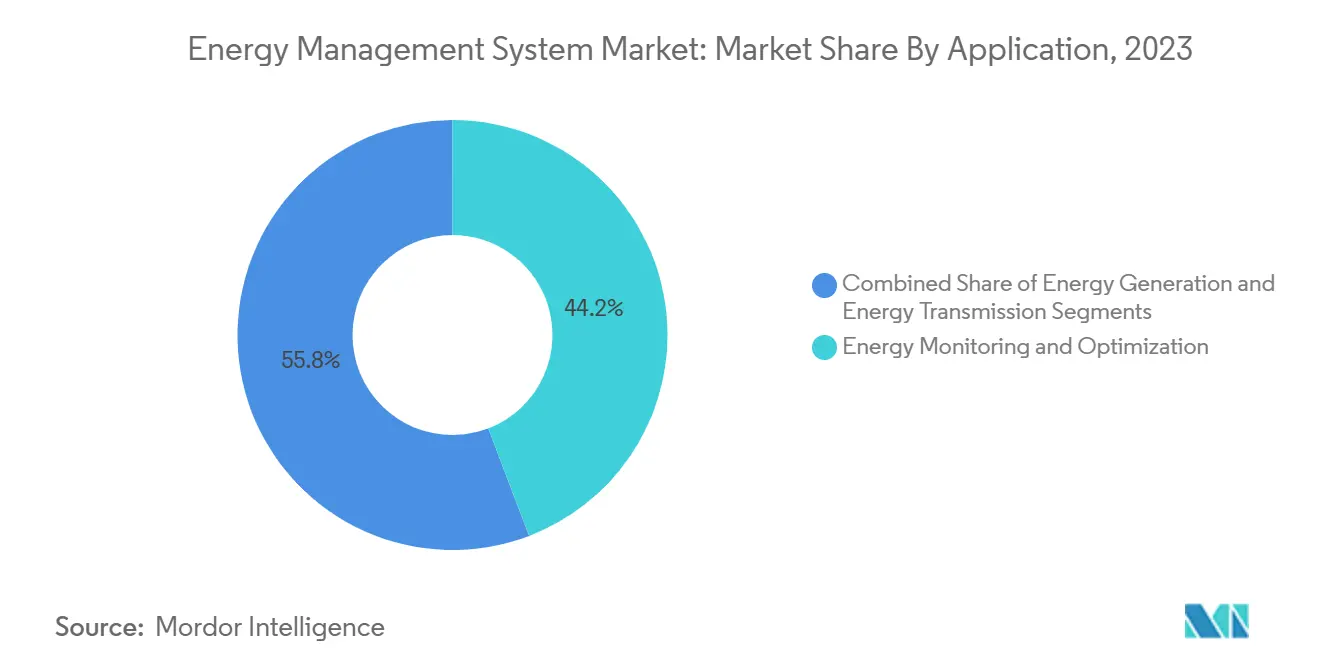

- By application, energy monitoring and optimization commanded a 44.2% share of the Energy Management Systems market size in 2024 and is advancing at a 15.75% CAGR through 2030.

- By component, software solutions captured 51.1% revenue share in 2024, whereas services exhibit the fastest growth at 15.68% CAGR to 2030.

- By region, North America maintained a 35.6% share of the Energy Management Systems market in 2024; Asia-Pacific is the fastest-growing region at a 16.05% CAGR to 2030.

Global Energy Management Systems Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid roll-out of AMI | +3.2% | Global (North America, EU spearhead) | Medium term (2-4 years) |

| Mandatory net-zero building codes from 2026 | +2.8% | North America, EU; APAC follow | Short term (≤ 2 years) |

| AI-powered predictive maintenance | +2.1% | Global; early uptake in developed markets | Medium term (2-4 years) |

| Corporate PPAs requiring granular data | +1.9% | Global; concentrated in North America, EU | Long term (≥ 4 years) |

| Blockchain P2P energy trading pilots | +1.4% | EU, APAC; limited North America | Long term (≥ 4 years) |

Source: Mordor Intelligence

Understand The Key Trends Shaping This Market

Download PDF

Rapid Roll-out of Advanced Metering Infrastructure Transforms Grid Intelligence

Utilities across mature economies accelerated AMI programs in 2024, installing millions of smart meters that stream interval data to cloud analytics engines. Eversource finished a 1.3 million-meter project spanning Massachusetts and Connecticut, while National Grid connected 3.4 million endpoints in the Northeast. The data feed underpins automated demand response, outage self-healing, and predictive load forecasting, all core modules in modern Energy Management Systems market platforms.[1]Eversource, “Advanced Metering Infrastructure,” eversource.com AI algorithms re-route power within seconds, cutting restoration times and trimming distribution losses. As distribution operators monetize grid services and accommodate renewables, AMI forms the essential layer linking field assets with cloud-based optimization.

Mandatory Net-Zero Building Codes Accelerate Commercial EMS Adoption

Jurisdictions such as New York City, Washington State, and California enacted rules that push large buildings toward net-zero operations, starting as early as 2026. Local Law 97 requires facilities over 25,000 ft² to cut emissions 40% by 2030, with steep fines for non-compliance. California’s Title 24 updates stipulate advanced controls and measurement, turning Energy Management Systems market deployments from voluntary upgrades into compliance necessities.[2]NYC Mayor’s Office, “Local Law 97 Compliance Guide,” nyc.gov Similar mandates ripple across Canada and the EU, expanding addressable demand for integrated HVAC, lighting, and renewable-ready platforms.

AI-Powered Predictive Maintenance Revolutionizes Utility Operations

Research from the University of Texas at Dallas demonstrated a graph-reinforcement-learning model that reconfigures distribution grids in microseconds, warding off outages and lowering OPEX by 15-25%. Coupled with growing IoT sensor penetration, utilities and heavy-industry sites can shift from time-based to condition-based maintenance, lengthening asset life and deferring capex. The Energy Management Systems market taps these algorithms to schedule equipment service, allocate workforce, and balance network loads—delivering quantifiable ROI that justifies enterprise-wide rollouts.

Corporate Power Purchase Agreements Drive Granular Energy Data Requirements

Corporate renewable PPAs surpassed 46 GW in 2024. Buyers committed to Science-Based Targets now demand hourly matching of consumption with clean power, as well as automated reporting for CDP and SEC climate disclosures. Energy Management Systems market vendors respond by integrating certificate registries, battery dispatch models, and tariff engines into unified dashboards that harmonize operations and sustainability accounting for multinationals like Microsoft and Google.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High up-front system integration costs | -2.4% | Global; acute in emerging markets | Short term (≤ 2 years) |

| Legacy OT/IT interoperability gaps | -1.8% | North America, EU; aging sites | Medium term (2-4 years) |

| Cyber-security liability | -1.2% | Global; stringent in developed markets | Long term (≥ 4 years) |

| Shortage of EMS-skilled technicians | -0.9% | APAC, MEA; limited LATAM | Long term (≥ 4 years) |

Source: Mordor Intelligence

High Up-Front System Integration Costs Constrain SME Market Penetration

Comprehensive deployments still command USD 50,000–500,000, a hurdle for cash-constrained facilities. Hardware, integration, and training extend payback to 18–36 months, delaying adoption in small enterprises. Energy-as-a-Service subscriptions now re-cast capex as opex, lowering entry barriers; Iris Ohyama’s 2025 launch of the ENEverse cloud suite typifies that pivot, bundling sensors, analytics, and remote operations into a no-hardware model.

Legacy OT/IT Interoperability Gaps Complicate Brownfield Deployments

Older plants rely on proprietary protocols and siloed data historians. Integration therefore demands gateways, edge controllers, and protocol translation, inflating project cost and risk. ABB and other automation majors ship universal I/O kits and low-code mapping tools that shrink retrofit timelines, yet brownfield complexity remains a drag on the Energy Management Systems market roll-out pace.[3]ABB, “Edge Gateway Integration White Paper,” abb.com

Segment Analysis

By Type of EMS: Building Systems Lead While Residential Accelerates

Building Energy Management Systems capture the largest slice of the Energy Management Systems market at 46.0% in 2024. Tighter codes, tenant sustainability reporting, and the premium on healthy indoor environments keep commercial campuses investing in advanced controls that trim 25–40% of utility spend. Home solutions post the fastest trajectory, rising at a 17.2% CAGR as rising electricity tariffs, smart-appliance penetration, and utility demand-response incentives nudge households toward voice-controlled thermostats and automated EV-charger scheduling. Integrated platforms now fuse occupancy sensors, PV inverters, and battery dispatch to create self-balancing nanogrids. Suppliers differ on architecture—edge hubs versus cloud-first—but all route data into AI engines for real-time optimization, broadening the Energy Management Systems market addressable base.

Recent advancements illustrate the shift from rule-based automation to predictive orchestration. C3.ai models combine physics-based equipment libraries with machine learning to anticipate load peaks and pre-condition HVAC for minimal energy intensity. Carrier’s BluEdge Command Center streams chiller-level data to remote engineers who tweak set points in minutes, achieving double-digit savings without on-site staff. The result is a feedback loop: verified savings fund further retrofits, cementing long-term service contracts that anchor vendor revenue.

Note: Segment shares of all individual segments available upon report purchase

By End User: Manufacturing Dominance Challenged by Healthcare Growth

Manufacturing facilities accounted for 31.4% of Energy Management Systems market share in 2024 owing to energy bills that routinely reach 20% of operating costs. Sectors such as cement, steel, and chemicals leverage high-speed sensors and digital twins to orchestrate furnaces, compressors, and process lines, seeking every kilowatt of productivity. Nevertheless, the healthcare vertical is expanding at a 16.25% CAGR. Hospitals run 24/7, with stringent humidity and temperature thresholds, making them ideal candidates for AI-guided HVAC and boiler sequencing. Apollo Hospitals reports 30% utility savings after deploying a cloud EMS that integrates medical equipment scheduling and cogeneration controls.

Power utilities, the second-largest end-user, rely on EMS modules for demand forecasting and renewables integration. IT and telecom operators apply similar logic inside data centers where cooling loads approach 40% of total consumption. As server densities jump with AI workloads, advanced airflow modeling and liquid-cooling optimization enter mainstream facility roadmaps. Residential and commercial mixed-use complexes round out demand, driven by net-metering policies and the urge to monetize rooftop solar.

By Application: Monitoring Dominance Reflects Optimization Priority

Energy monitoring and optimization occupied 44.2% of the Energy Management Systems market size in 2024 and is slated to grow at 15.75% CAGR as firms embrace continuous improvement loops. Sensors feed second-by-second consumption profiles into analytics dashboards that benchmark sites, flag anomalies, and auto-dispatch controls. Generation-side EMS modules coordinate rooftop solar, batteries, and diesel gensets to shave peaks and maximize self-consumption. Transmission-oriented features, such as fault-location and automated switching, support utilities pursuing reliability metrics and outage-minute reductions.

Convergence is accelerating. Schneider Electric’s One Digital Grid melds planning, operations, and customer engagement into one platform. Utilities can model DER hosting capacity, simulate storm impacts, and push tariff signals to behind-the-meter assets in a closed loop. The hybrid-cloud stack ensures data continuity from substation relays to mobile apps, helping regulators accept digital evidence for outage reporting.

Note: Segment shares of all individual segments available upon report purchase

By Component: Software Leadership Drives Service Growth

Software maintained 51.1% revenue share in 2024 because algorithms and user experience dictate value creation. Edge gateways, IoT sensors, and controllers are commoditizing, but the machine-learning models that forecast, diagnose, and prescribe actions remain proprietary differentiators. Services, however, are gaining fastest at 15.68% CAGR as clients outsource not just installation but ongoing optimization. Subscription bundles wrap platform licenses with 24/7 network operations centers that fine-tune parameters, respond to alarms, and verify savings—solving the skilled-labor shortage outside OECD markets.

Market leaders push toward outcome-based contracts. Iris Ohyama offers guaranteed-savings models paid from realized utility cuts, while ABB’s Energy-Efficiency-as-a-Service targets industrial multinationals that prefer predictable monthly fees over sporadic capex. These shifts expand the Energy Management Systems market by drawing in customers previously deterred by capital constraints.

Geography Analysis

North America retains its pole position with 35.6% of Energy Management Systems market revenue in 2024. Federal funding through the Inflation Reduction Act and state tax credits catalyze metering, EV-charging, and building-retrofit projects. Utilities such as Eversource and National Grid added millions of smart endpoints in 2024, laying the data fabric that underpins advanced analytics. Schneider Electric responded with a USD 700 million expansion across U.S. plants to localize production of switchgear, microgrid controllers, and software R&D, signalling confidence in policy stability and customer demand.

Europe follows closely, propelled by the European Green Deal and Fit-for-55 package that stipulate 55% emission cuts versus 1990 by 2030. Member states embed digital-building requirements in local codes, fostering robust demand for integrated building analytics. Germany’s roll-out of P2P trading sandboxes and the Netherlands’ aggressive heat-pump incentives showcase regulatory breadth. Investment appetite surfaced when TPG paid EUR 6.7 billion for Techem, attracted by recurring revenues from sub-metering and efficiency services. Utilities accelerate grid-edge digitization to handle variable renewable flows, further enlarging the Energy Management Systems market.

Asia-Pacific is the growth engine with a projected 16.05% CAGR. China invests in ultra-high-voltage transmission and AI-enhanced dispatch centers to balance its 1,200 GW of wind–solar capacity planned by 2030. Japan’s subsidies for Home EMS and Building EMS, backed by JPY 4 billion earmarked in 2025, bolster vendor pipelines. India’s Smart Cities Mission embeds EMS requirements in tenders for public buildings and street-lighting networks, while Southeast Asian economies seek grid-stability solutions to cope with rapid rooftop-solar adoption. Multinationals setting up regional manufacturing hubs specify EMS from day one, accelerating greenfield demand.

Competitive Landscape

The Energy Management Systems market remains moderately fragmented, with the top five suppliers controlling roughly 45% of global revenue. Incumbent automation companies—Schneider Electric, Siemens, ABB, and Honeywell—bundle hardware, software, and services into end-to-end offers, leveraging global channels and balance sheets to win multi-region deals. Acquisition pipelines are robust: ABB bought Siemens’ wiring-accessories arm in China to deepen its smart-building stack, and Trane added BrainBox AI to embed self-learning HVAC control in its chiller fleet. These moves illustrate a race to infuse AI into legacy portfolios and secure data access at the edge.

Specialist entrants target niches. Edgecom Energy applies generative AI to flatten industrial peaks, while blockchain startups pilot secure settlement layers for micro-trades of rooftop-solar output. Device makers such as Tesla file patents on hierarchical energy-distribution grids that automate DER orchestration, foreshadowing next-generation architectures. Competitive intensity therefore swivels from pure features to ecosystems: vendors that curate open APIs, app marketplaces, and developer communities stand to lock in partners and expand use cases.

Pricing models shift as well. Subscription, outcome-based, and revenue-sharing contracts spread risk between provider and customer, appealing to CFOs wary of capex. Vendors differentiate by cybersecurity posture, given rising liability for critical-infrastructure incidents. Firms able to certify to ISA/IEC 62443 and maintain 24/7 security operation centers gain an advantage, especially in healthcare, finance, and utility verticals where downtime tolerances are minimal. Collectively, these dynamics anchor a vibrant yet consolidating Energy Management Systems market.

Energy Management Systems Industry Leaders

-

IBM Corporation

-

Rockwell Automation, Inc.

-

General Electric

-

Schneider Electric

-

Eaton

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: Schneider Electric launched the One Digital Grid Platform, claiming 40% outage reduction and 25% faster DER interconnection through AI analytics.

- May 2025: Iris Ohyama unveiled ENEverse, a cloud EMS that eliminates up-front hardware by bundling sensors, analytics, and remote control services.

- March 2025: ABB purchased Siemens’ China wiring-accessories unit for more than USD 150 million, adding 230-city distribution reach.

- January 2025: ABB invested in Edgecom Energy, a Toronto AI startup focused on industrial demand-peak optimization

Global Energy Management Systems Market Report Scope

An energy management system (EMS) is a tool for monitoring, analyzing, and optimizing the operation of the electric transmission system. The system is widely used in various industries, and EMS implementation includes SCADA, Automatic Generation Control (AGC), and alarms, among others. The studied market is segmented by types of EMS, such as BEMS, IEMS, and HEMS, among various end-user industries such as manufacturing, power and energy, it and telecommunication, healthcare, residential and commercial in various applications such as energy generation, energy transmission, and energy monitoring.

The energy management system is categorized by segmentation type of EMS (BEMS, IEMS, and HEMS), end user (manufacturing, power & energy, IT& telecommunication, healthcare, and residential and commercial), application (energy generation, energy transmission, and energy monitoring), component (hardware, software, and services), and geography (North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa).

The market sizes and predictions are provided in terms of value in USD for all the above segments.

| By Type of EMS | Building EMS (BEMS) | |||

| Industrial EMS (IEMS) | ||||

| Home EMS (HEMS) | ||||

| By End-User | Manufacturing | |||

| Power and Energy | ||||

| IT and Telecommunication | ||||

| Healthcare | ||||

| Residential and Commercial | ||||

| By Application | Energy Generation | |||

| Energy Transmission | ||||

| Energy Monitoring and Optimization | ||||

| By Component | Hardware | |||

| Software | ||||

| Services | ||||

| By Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| South America | Brazil | |||

| Argentina | ||||

| Chile | ||||

| Rest of South America | ||||

| Europe | Germany | |||

| United Kingdom | ||||

| France | ||||

| Italy | ||||

| Spain | ||||

| Netherlands | ||||

| Russia | ||||

| Rest of Europe | ||||

| Asia Pacific | China | |||

| India | ||||

| Japan | ||||

| South Korea | ||||

| ASEAN | ||||

| Rest of Asia Pacific | ||||

| Middle East and Africa | Middle East | GCC (Saudi Arabia, UAE, Qatar, etc.) | ||

| Turkey | ||||

| Rest of Middle East | ||||

| Africa | South Africa | |||

| Nigeria | ||||

| Kenya | ||||

| Rest of Africa | ||||

By Type of EMS

| Building EMS (BEMS) |

| Industrial EMS (IEMS) |

| Home EMS (HEMS) |

By End-User

| Manufacturing |

| Power and Energy |

| IT and Telecommunication |

| Healthcare |

| Residential and Commercial |

By Application

| Energy Generation |

| Energy Transmission |

| Energy Monitoring and Optimization |

By Component

| Hardware |

| Software |

| Services |

By Geography

| North America | United States | ||

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Netherlands | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| ASEAN | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | GCC (Saudi Arabia, UAE, Qatar, etc.) | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the Energy Management Systems market?

The Energy Management Systems market size is USD 63.64 billion in 2025 and is projected to reach USD 131.67 billion by 2030.

Which EMS type holds the largest share today?

Uilding Energy Management Systems lead with 46.0% of Energy Management Systems market share in 2024.

Which region is growing fastest for EMS vendors?

Asia-Pacific is forecast to expand at a 16.05% CAGR through 2030, outpacing all other regions.

Why are services growing faster than software or hardware?

Enterprises prefer subscription models that shift capex to opex, driving 15.68% CAGR in managed services and Energy-as-a-Service bundles.

What restrains EMS adoption among smaller facilities?

High integration costs, legacy equipment incompatibility, and limited access to skilled technicians remain key barriers, though cloud subscriptions are lowering entry hurdles.

How do AI-powered EMS platforms improve utility operations?

AI models forecast demand, detect faults, and reroute power automatically, delivering 15–25% OPEX reduction and faster outage recovery for utilities.

Page last updated on: July 7, 2025