Energy As A Service (EaaS) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 119.67 Billion |

| Market Size (2031) | USD 203.74 Billion |

| Growth Rate (2026 - 2031) | 11.23% CAGR |

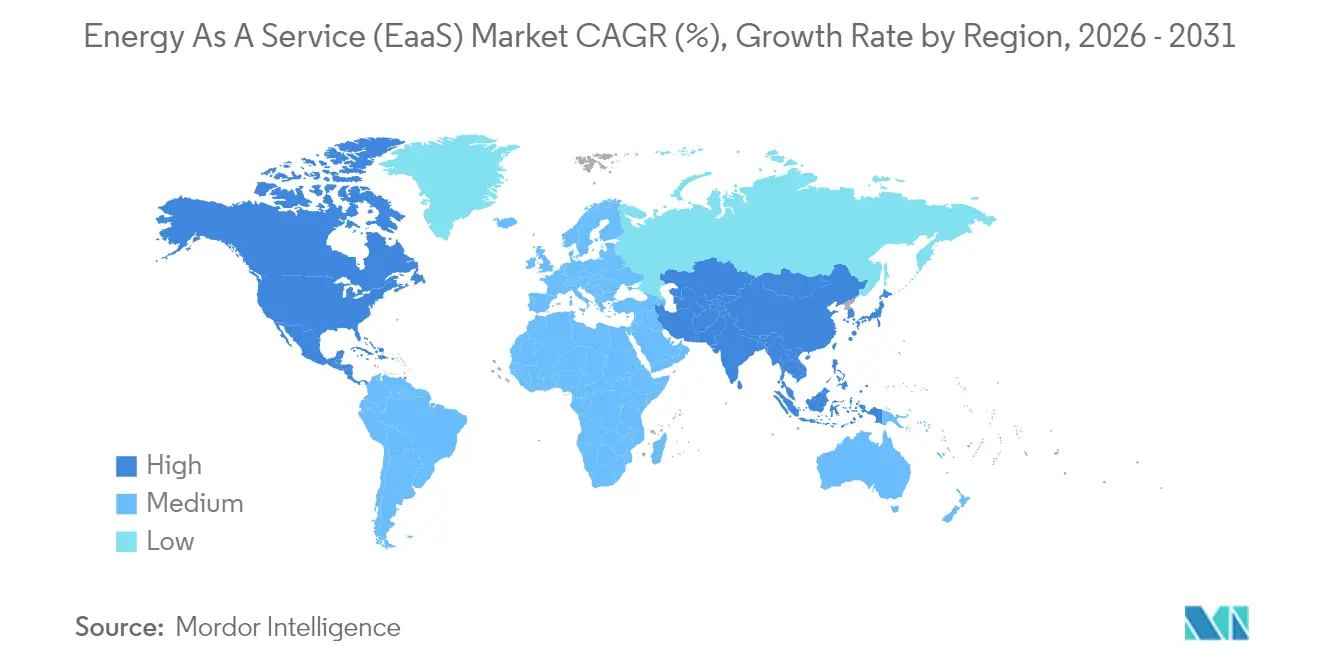

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Energy As A Service (EaaS) Market Analysis by Mordor Intelligence

The Energy As A Service Market size was valued at USD 107.59 billion in 2025 and estimated to grow from USD 119.67 billion in 2026 to reach USD 203.74 billion by 2031, at a CAGR of 11.23% during the forecast period (2026-2031).

Corporate decarbonization mandates, grid reliability concerns, and the financial appeal of shifting from capital to operating expenditure models anchor this sustained momentum. Large enterprises are increasingly outsourcing energy procurement, generation, storage, and analytics to avoid upfront investments and secure predictable costs. Policy tailwinds such as the Inflation Reduction Act (IRA) in the United States and comparable green-funding pools across the European Union further improve project economics by layering grants, tax credits, and low-interest financing. Simultaneously, advanced analytics and distributed energy technologies—such as solar PV, battery storage, and intelligent load control—are now bundled into subscription-style contracts that deliver measurable emissions reductions and resiliency benefits.

Key Report Takeaways

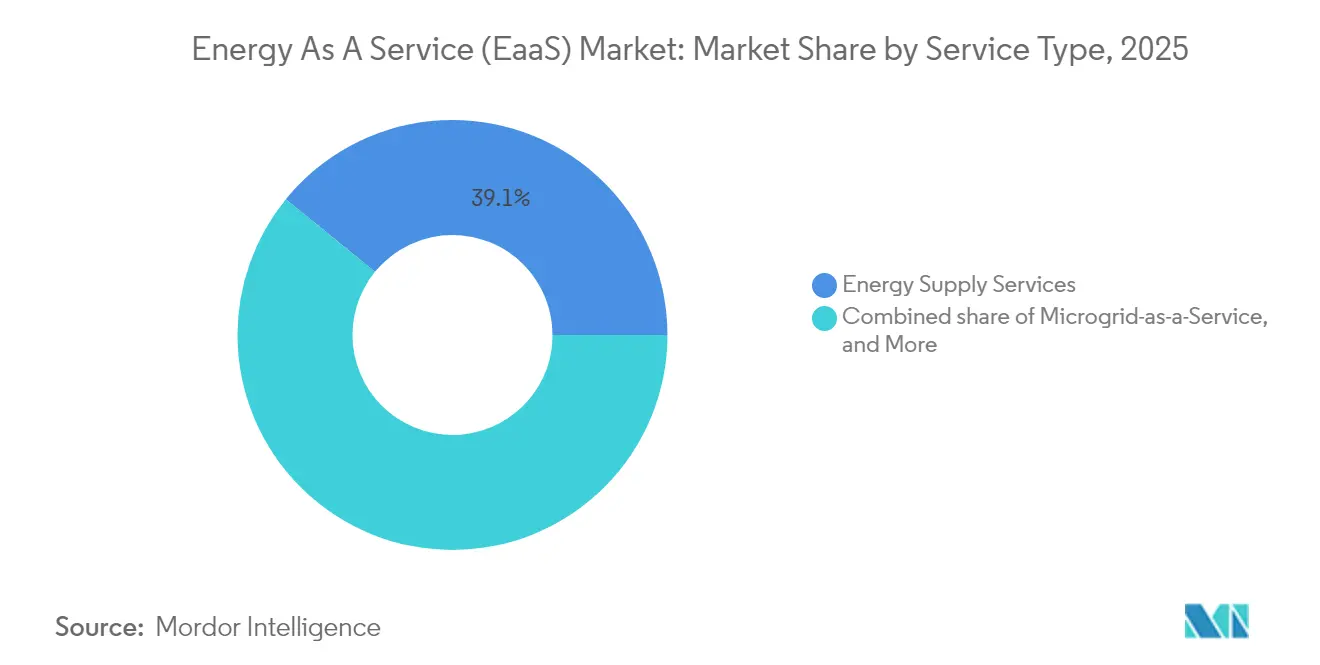

- By service type, Energy Supply Services accounted for 39.12% of global revenue in 2025, while Microgrid-as-a-Service is projected to grow at a 14.05% CAGR through 2031.

- By service-delivery model, Pay-for-Service captured 39.55% of the Energy as a Service market share in 2025; leasing and rental are advancing at an 18.02% CAGR through 2031.

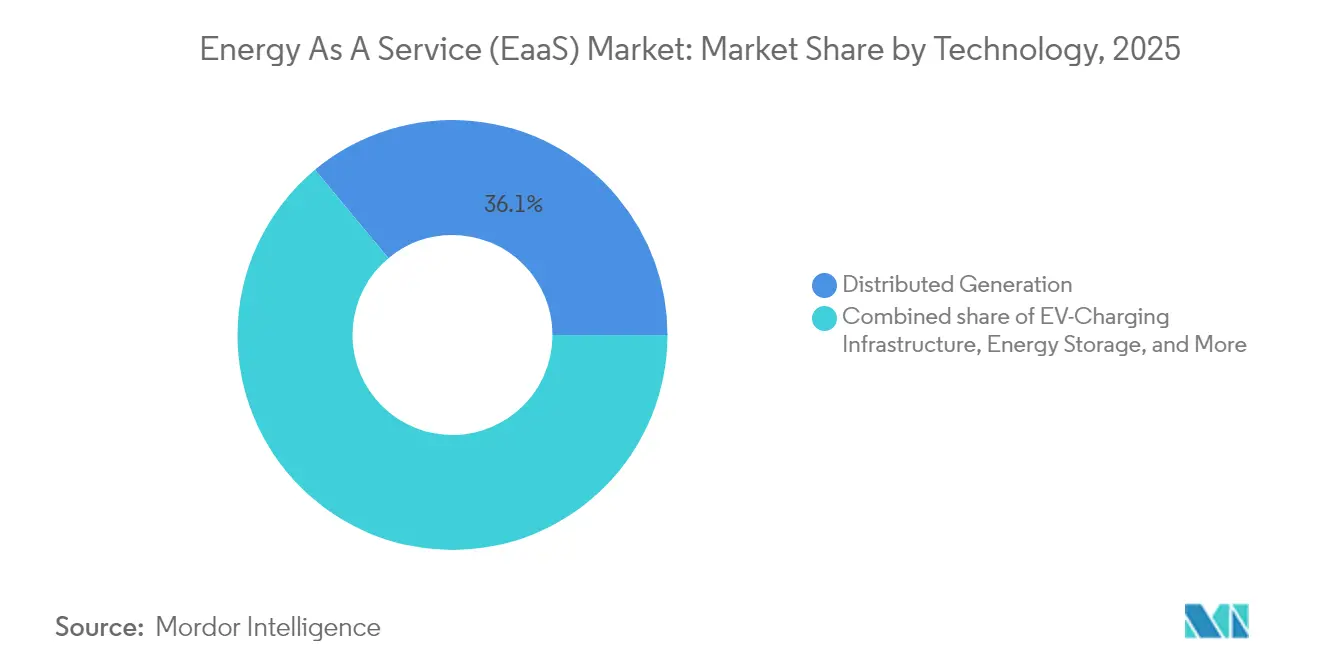

- By technology, Distributed Generation accounted for a 36.05% share of the Energy as a Service market size in 2025, while EV-charging infrastructure is expanding at a 19.74% CAGR through 2031.

- By end user, commercial facilities represented 62.78% of 2025 revenue, whereas industrial customers are forecast to grow at a 13.72% CAGR to 2031.

- By geography, North America led with a 42.18% market share in 2025; the Asia-Pacific region recorded the fastest regional CAGR at 16.32% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Energy As A Service (EaaS) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Corporate decarbonization mandates & Scope-3 pressure | 2.10% | Global, early uptake in North America & EU | Medium term (2-4 years) |

| Grid volatility driving microgrid adoption | 1.80% | North America & Asia-Pacific, spill-over to Europe | Short term (≤ 2 years) |

| Shift from CAPEX to OPEX in large facilities | 2.30% | Global, strongest in developed markets | Long term (≥ 4 years) |

| AI-driven energy analytics improving ROI | 1.60% | North America & Europe, widening to Asia-Pacific | Medium term (2-4 years) |

| Inflation Reduction Act & kindred green funds | 1.90% | North America with global knock-on | Short term (≤ 2 years) |

| Rise of C&I battery storage services | 1.40% | Global, led by North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Corporate Decarbonization Mandates & Scope-3 Pressure

Mandatory greenhouse-gas disclosure rules, such as California’s SB 253, require firms with revenue exceeding USD 1 billion to report Scope 3 emissions starting in 2027, prompting procurement teams to prioritize renewable electricity and verified emissions accounting.[1]California Legislature, “SB 253 Climate Corporate Data Accountability Act,” ca.gov Multinational buyers extend these requirements along their supply chains, amplifying demand for turnkey Energy as a Service market solutions that bundle green power, energy efficiency, and transparent reporting. Financial institutions also factor climate risk into lending decisions, so companies perceive service-based energy contracts as a convenient Energy-as-a-Service market that expands the path to greener balance sheets. Mid-sized enterprises lacking in-house sustainability staff benefit the most, outsourcing both technology selection and monitoring. As disclosure deadlines approach, the addressable customer pool for the Energy as a Service market widens across every major sector.

Grid Volatility Driving Microgrid Adoption

Ageing infrastructure, extreme weather, and data center growth stress legacy grids; the International Energy Agency estimates that 80 million km of power lines will need refurbishment or replacement by 2040.[2]International Energy Agency, “Electricity Grids and Secure Energy Transitions,” iea.org Microgrids mitigate outage risk by allowing critical loads to island and self-supply. Demonstrations funded by the California Energy Commission have shown 20-60% energy cost savings while maintaining uptime during blackouts.[3]California Energy Commission, “EPIC Microgrid Demonstration Results,” energy.ca.gov Corporations now view microgrids not as backup assets, but as integrated components of their facility management strategies, and service providers supply them under multi-year pay-for-performance contracts. Regulatory treatment varies by jurisdiction, yet policy experimentation—such as performance-based tariffs and reduced interconnection fees—continues to unlock new demand pockets for the Energy as a Service market.

Shift from CAPEX to OPEX in Fortune-1000 Facilities

Asset-light finance models resonate with boards seeking to conserve capital for core operations. An industrial conglomerate recently bypassed USD 106 million in upfront spend by retrofitting 1,200 sites via an Energy as a Service agreement that tied payments to documented savings. Manufacturers, retailers, and healthcare chains are replicating this template because operational expenses can be budgeted annually, depreciation can be avoided, and site rollouts can be supported more quickly. Providers respond with guarantees covering performance, maintenance, and technology refresh, cementing the Energy as a Service market as a mainstream procurement option for CFOs.

AI-Driven Energy Analytics Improving ROI

Artificial-intelligence platforms now predict load, detect equipment faults, and optimize dispatch across portfolios in near real-time. The International Energy Agency projects cumulative operational savings of USD 110 billion in global power plants by 2035, resulting from the application of AI. Field deployments cut commercial-building energy use by as much as 19% and lengthen equipment life by one-fifth. Vendors increasingly embed machine-learning engines into edge controllers, making sophisticated analytics affordable for mid-tier facilities. The result is a higher net present value for projects and faster expansion of the Energy as a Service market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Long-term contract lock-in concerns | -1.20% | Global, acute in developed markets | Long term (≥ 4 years) |

| Cyber-security liabilities on third-party assets | -0.90% | Global, critical-infrastructure focus | Short term (≤ 2 years) |

| Policy uncertainty on behind-the-meter incentives | -1.10% | North America & Europe | Medium term (2-4 years) |

| Inflated WACC on energy infrastructure in emerging economies | -0.80% | Africa & Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Long-Term Contract Lock-In Concerns

Standard Energy Savings Performance Contracts span 5-20 years, raising anxiety about technology obsolescence and operational flexibility. The U.S. Department of Energy advises rigorous measurement and verification to safeguard customer value and audit readiness.[4]U.S. Department of Energy, “Guidance on Energy Savings Performance Contracts,” energy.gov Service providers are increasingly inserting mid-term upgrade clauses or opt-out windows, but these features can raise pricing. Consequently, risk-averse prospects may delay signing, reducing immediate growth potential for the Energy as a Service market.

Cyber-Security Liabilities on Third-Party Assets

The FBI warns that the speed of renewable energy deployment has exceeded the implementation of cyber defenses, exposing distributed assets to potential attacks. Battery-management systems are especially vulnerable because operational-technology protocols often lack encryption or intrusion detection. Regulatory regimes, such as Europe’s NIS2 directive, impose stricter compliance obligations, increasing costs and complexity for small providers. Although these dynamics create consulting opportunities, they also elevate liability exposure and slow contract negotiations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type – Energy Supply Services Retain Leadership While Microgrids Surge

Energy Supply Services generated 39.12% of 2025 turnover, reflecting enterprises’ priority to secure competitively priced, low-carbon electricity without managing complex procurement processes. Within this segment, the Energy as a Service market share advantage stems from bundled power-purchase arrangements, hedging strategies, and management of renewable certificates. Microgrid-as-a-Service is projected to record the fastest 14.05% CAGR through 2031, as hospitals, airports, and manufacturing parks seek island-mode resiliency during grid disturbances. The Energy as a Service market size for microgrids is projected to more than double between 2026 and 2031, supported by falling battery prices and streamlined permitting. Services covering operations & maintenance, as well as lifecycle upgrades, add sticky recurring revenue streams, further entrenching providers.

In parallel, Energy Infrastructure Services—engineering, interconnection, and asset monitoring—gain importance as clients demand seamless integration of generation, storage, and advanced controls. The Energy as a Service market is seeing rising cross-sell opportunities, where a single contract now spans supply, efficiency optimization, and on-site generation. Providers with deep software stacks and nationwide field service crews command premium valuations, reflecting the synergistic value created by integrated offerings.

By Service-Delivery Model – Subscription Stability Outpaces Flexible Leasing Growth

Pay-for-service agreements accounted for 39.55% of 2025 revenue, as they transform volatile utility expenses into a single, predictable monthly line item. These contracts typically bundle performance guarantees and align provider compensation with realized savings, reinforcing customer confidence. Leasing & Rental models gain traction at an 18.02% CAGR by offering shorter tenures and simplified off-balance-sheet treatment, which appeals to tenants or property managers with limited lease horizons. While the Energy as a Service industry occasionally employs Build-Own-Operate-Transfer structures for municipalities seeking eventual ownership, subscription plans are the dominant form of private-sector uptake.to legacy ESCO arrangements, modern Pay-for-Service contracts emphasize modular add-ons, such as demand-response participation, electric vehicle charging, and carbon reporting

Performance-based contracts remain prevalent in the public and institutional arena, supported by statutory frameworks that authorize multi-year repayment from guaranteed savings. Compared with legacy ESCO arrangements, modern Pay-for-Service contracts emphasize modular add-ons such as demand-response participation, electric-vehicle charging, and carbon-reporting dashboards. This evolution reinforces the Energy as a Service market’s positioning as a scalable, tech-enabled solution rather than a one-off retrofit scheme.

By Technology – Distributed Generation Leads; EV Infrastructure Accelerates

Distributed Generation-solar PV, wind turbines, and fuel-cell combined heat and power-held 36.05% of 2025 revenue. Its dominance owes to mature cost curves and broad policy support. The Energy as a Service market size attributable to on-site solar alone is expected to increase steadily as rooftop permitting processes become digitalized. Simultaneously, EV-charging infrastructure is growing at a 19.74% CAGR as logistics fleets, corporate campuses, and parking garage operators electrify. Coupling fast chargers with BESS allows demand-charge mitigation, creating a compelling service value proposition.

Battery-energy storage systems underpin multiple revenue streams, including time-of-use arbitrage, frequency regulation, and backup power. Intelligent energy-management platforms unify these assets, employing AI to orchestrate dispatch and predictive maintenance. The Energy as a Service market greatly benefits when all hardware layers communicate through open protocols, enabling remote firmware updates and real-time optimization.

By End User – Commercial Segment Dominates While Industrial Adoption Accelerates

Commercial buildings-such as retail chains, data centers, hospitals, and universities-accounted for 62.78% of 2025 turnover because their core operations rely on uninterrupted power, yet they often lack internal energy expertise. Data-center electricity demand alone could reach 9.1% of U.S. load by 2030, further intensifying uptake of fully managed service bundles. Industrial customers, although smaller today, are expected to register a brisk 13.72% CAGR as factories modernize under new emissions rules and electricity-intensive processes adopt electrification. The Energy as a Service market size tied to heavy industry is therefore poised to expand rapidly, especially where carbon-border adjustment policies raise export competitiveness stakes.

For commercial portfolios, standardized system designs and centralized monitoring yield economies of scale. In contrast, industrial facilities require bespoke engineering to align with process heat demands and safety codes. Providers that cultivate sector-specific expertise-such as pharmaceutical clean rooms, semiconductor fabs, or food-cold-chain warehouses-secure differentiation in a crowded Energy as a Service market.

Geography Analysis

North America retained 42.18% of global revenue in 2025, powered by the IRA’s USD 370 billion stimulus, state-level storage mandates, and mature corporate procurement programs. The Greenhouse Gas Reduction Fund steers low-interest capital to disadvantaged communities, broadening the customer base beyond Fortune 500 enterprises. Canada reinforces regional momentum through carbon pricing and provincial clean-energy auctions. Cross-border interoperability of smart-metering standards and open-data policies further accelerates platform scalability for energy-as-a-service market participants.

The Asia-Pacific region records the fastest growth, with a 16.32% CAGR to 2031, reflecting rapid urbanization and sustained public-sector investment. China’s multi-gigawatt distributed-generation schemes and India’s transmission build-out unlock substantial opportunities for turnkey microgrid and storage offerings. Japan and South Korea deploy high-penetration renewables paired with advanced predictive maintenance analytics, establishing templates that are replicable across ASEAN nations. Although financing costs remain elevated in certain jurisdictions, blended-finance facilities and export-credit support mitigate risk and catalyze the regional Energy-as-a-Service market.

Europe maintains a sizable share, bolstered by the Fit-for-55 decarbonization targets that compel large emitters to contract for renewable power and energy efficiency guarantees. Harmonized data-sharing frameworks simplify multi-country rollouts, though each member state retains discretion over behind-the-meter incentive design, which introduces execution complexity. South America, the Middle East, and Africa together contribute a modest but growing slice of global revenue. Currency volatility and policy uncertainty temper uptake, yet landmark projects-such as Morocco’s 822,000 m³/day desalination plant incorporating solar-plus-storage under a 35-year concession-demonstrate feasibility for bankable Energy as a Service market structures

Competitive Landscape

The market remains moderately fragmented with clear signals of consolidation. Tier-one multinationals—such as Schneider Electric, Honeywell, Siemens, and ABB—bundle hardware, software, and financing, leveraging their global footprints to win campus-scale deals. Mid-tier specialists—Veolia, Enel X, and NRG—emphasize regional depth and sector-focused expertise, often partnering with equipment OEMs to offer jointly branded solutions. Digital-native entrants supply AI-first platforms that integrate third-party assets via API-based architectures, lowering switching costs for customers and pressuring incumbents to modernize.

Acquisition activity centers on complementary capabilities. Honeywell’s USD 1.81 billion purchase of Air Products’ LNG process unit extends its portfolio into low-carbon fuels. Bosch’s USD 8 billion acquisition of Johnson Controls’ air-conditioning assets creates an HVAC powerhouse positioned to embed subscription-based efficiency services worldwide. Strategic partnerships also flourish: Carrier and Google Cloud co-develop AI-powered home energy management that integrates HVAC hardware, batteries, and real-time optimization. These examples underscore how data analytics and integrated controls now represent key battlegrounds rather than commodity hardware specifications.

Differentiation increasingly hinges on customer-experience metrics—such as deployment speed, billing transparency, and verified emissions reporting—rather than kilowatt-hour price alone. Providers, therefore, invest in user-friendly dashboards, mobile alerts, and automated compliance documentation to enhance their operations. Supply-chain resilience and cybersecurity posture likewise influence purchasing decisions, prompting vendors to pursue SOC 2 certifications and zero-trust network architectures. As scaled players absorb niche innovators, the Energy as a Service market is shifting toward oligopolistic dynamics; however, regional regulations and sector-specific requirements still preserve room for agile challengers.

Energy As A Service (EaaS) Industry Leaders

Schneider Electric SE

Engie SA

Veolia Environnement SA

Honeywell International Inc.

Johnson Controls International plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Carrier Global Corporation and Google Cloud have unveiled a strategic alliance to deliver AI-enabled home energy ecosystems, integrating battery-equipped HVAC equipment with cloud analytics.

- March 2025: Itron and Schneider Electric joined forces with Microsoft to embed distributed intelligence into grid-edge devices, upgrading utility visibility and control.

- March 2025: Hitachi Energy commenced a multi-year collaboration with Amazon Web Services to release cloud-native vegetation-management AI that mitigates outage risk from tree encroachment.

- February 2025: Vantage Data Centers and VoltaGrid announced plans to deploy over 1 GW of natural-gas microgrid capacity to support hyperscale data center campuses in constrained markets.

Global Energy As A Service (EaaS) Market Report Scope

Energy as a Service (EaaS) is a business model where the consumers only pay for energy services without making any initial capital investment. EaaS uses conventional arrangements, including energy supply contracts (ESCs), energy performance contracts (EPCs), and power purchase agreements (PPAs), and employs alternative models that lower or eliminate upfront costs around funding, owning, and operating capital-intensive energy generation and storage systems.

The Energy as a service market is segmented by end-user and geography. By end-user, the market is segmented into commercial and industrial. The report also covers the market size and forecasts for the Energy as a service market across major regions. Each segment's market sizing and forecasts are based on revenue (USD).

| Energy Supply Services |

| Energy Efficiency and Optimisation Services |

| Operation and Maintenance Services |

| Energy Infrastructure Services |

| Microgrid-as-a-Service |

| Pay-for-Service (Subscription) |

| Performance-based Contracting (ESCO/EPC) |

| Build-Own-Operate-Transfer (BOOT) |

| Leasing and Rental Models |

| Distributed Generation (Solar PV, Wind, Combined Heat & Power and Fuel Cells) |

| Energy Storage (Battery Storage, and Thermal Storage) |

| Smart Energy Management & Analytics |

| EV-Charging Infrastructure |

| Commercial (Data Centres, Retail & Shopping Malls, Healthcare Facilities, Educational Institutions, Hospitality and Others) |

| Industrial (Heavy Manufacturing, Food & Beverage Processing, Chemicals & Pharmaceuticals, Mining & Metals and Others) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Service Type | Energy Supply Services | |

| Energy Efficiency and Optimisation Services | ||

| Operation and Maintenance Services | ||

| Energy Infrastructure Services | ||

| Microgrid-as-a-Service | ||

| By Service-Delivery Model | Pay-for-Service (Subscription) | |

| Performance-based Contracting (ESCO/EPC) | ||

| Build-Own-Operate-Transfer (BOOT) | ||

| Leasing and Rental Models | ||

| By Technology | Distributed Generation (Solar PV, Wind, Combined Heat & Power and Fuel Cells) | |

| Energy Storage (Battery Storage, and Thermal Storage) | ||

| Smart Energy Management & Analytics | ||

| EV-Charging Infrastructure | ||

| By End User | Commercial (Data Centres, Retail & Shopping Malls, Healthcare Facilities, Educational Institutions, Hospitality and Others) | |

| Industrial (Heavy Manufacturing, Food & Beverage Processing, Chemicals & Pharmaceuticals, Mining & Metals and Others) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the global Energy as a Service market in 2031?

It is forecast to reach USD 203.74 billion, growing at an 11.23% CAGR from 2026.

Which region leads adoption of Energy as a Service solutions today?

North America held 42.18% of 2025 revenue, driven by strong policy support such as the Inflation Reduction Act.

Why are microgrids gaining popularity within commercial campuses?

They deliver 20-60% cost savings and ensure resilience during grid outages, benefits now available through subscription contracts.

How does the IRA reshape project economics for service providers?

Grants, tax credits, and low-interest loans lower capital costs, letting providers offer more competitive subscription prices.

Which technology segment is expanding fastest through 2031?

EV-charging infrastructure is expected to scale at a 19.74% CAGR as fleet electrification accelerates.

What are the main cybersecurity concerns for distributed energy assets?

Battery-management and control systems can be vulnerable to remote attacks, prompting stricter compliance requirements and higher liability exposure.

Page last updated on: