Enteral Feeding Tubes Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

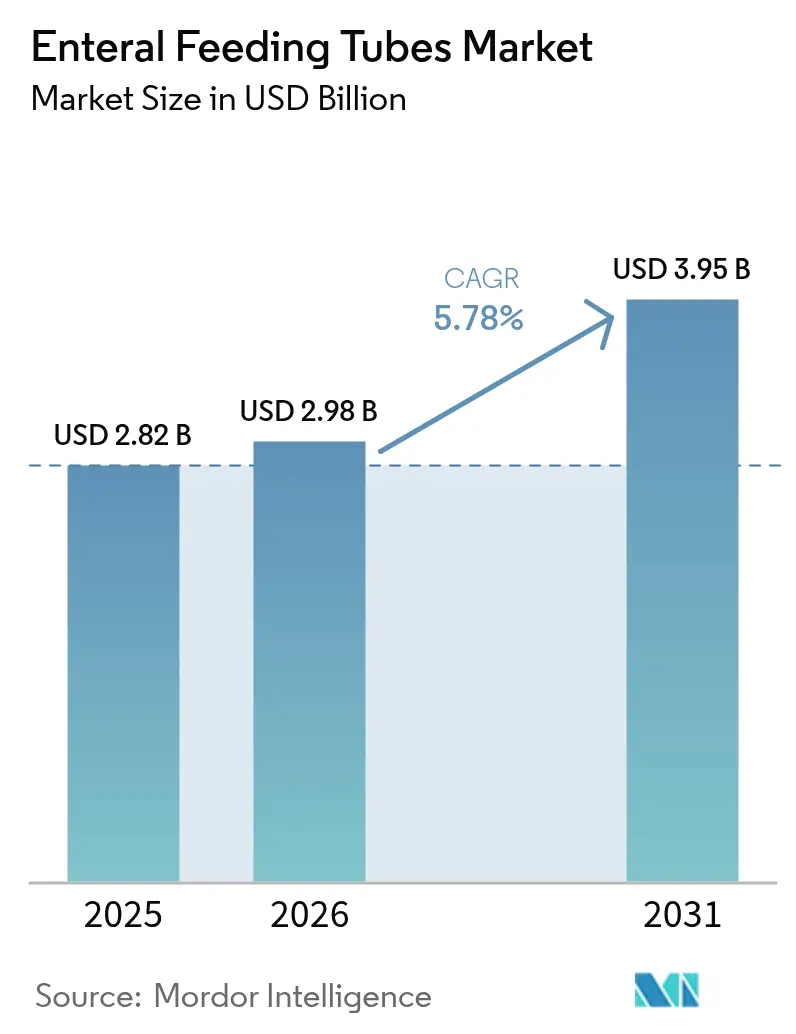

| Market Size (2026) | USD 2.98 Billion |

| Market Size (2031) | USD 3.95 Billion |

| Growth Rate (2026 - 2031) | 5.78% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

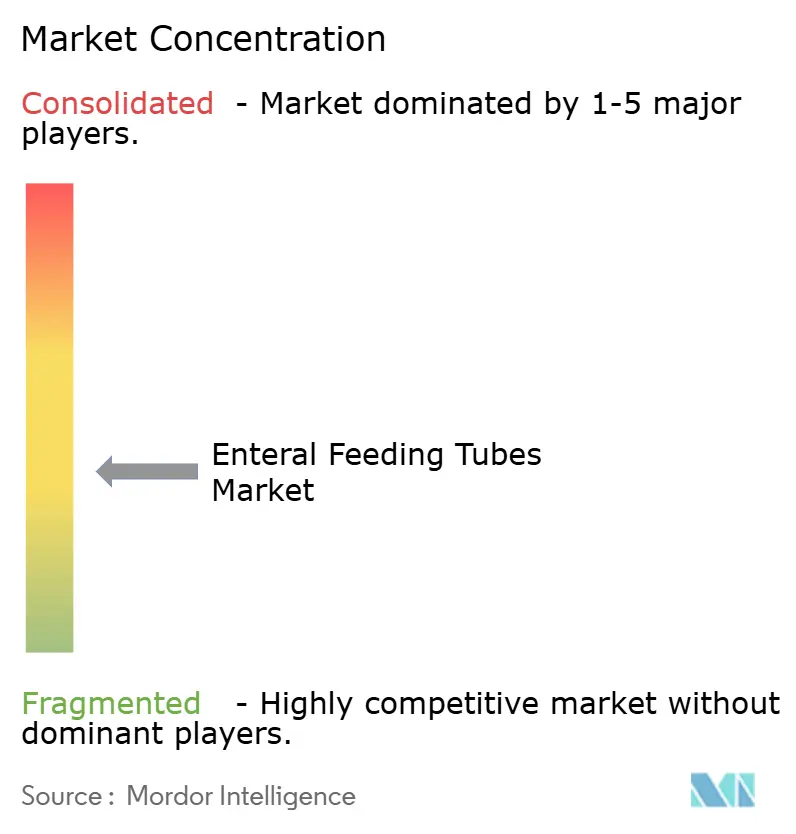

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Enteral Feeding Tubes Market Analysis by Mordor Intelligence

Enteral feeding tubes market size in 2026 is estimated at USD 2.98 billion, growing from 2025 value of USD 2.82 billion with 2031 projections showing USD 3.95 billion, growing at 5.78% CAGR over 2026-2031. Momentum stems from rising gastrointestinal disease prevalence, the global malnutrition burden, and advances such as electromagnetic tracking systems that cut placement-error risk. Consolidation among suppliers, highlighted by BD’s USD 4.2 billion purchase of Edwards Lifesciences’ Critical Care unit, adds scale to smart-connected feeding platforms. New FDA Quality System Regulation amendments, effective February 2026, align international design-control standards, smoothing global product registration. In parallel, payers increasingly reimburse home-based enteral nutrition, accelerating demand from outpatient and telehealth channels.

Key Report Takeaways

- By product category, enterostomy tubes led with 45.86% revenue share in 2025, while self-advancing spiral tubes are projected to expand at 10.63% CAGR to 2031.

- By patient type, adults accounted for 69.98% of the enteral feeding tubes market size in 2025; the neonatal cohort is advancing at an 8.32% CAGR through 2031.

- By application, oncology held 32.44% of the enteral feeding tubes market share in 2025; critical care and trauma is forecast to grow 8.89% CAGR to 2031.

- By end user, hospitals commanded 61.94% share of the enteral feeding tubes market size in 2025, while home care is expanding at a 9.74% CAGR through 2031.

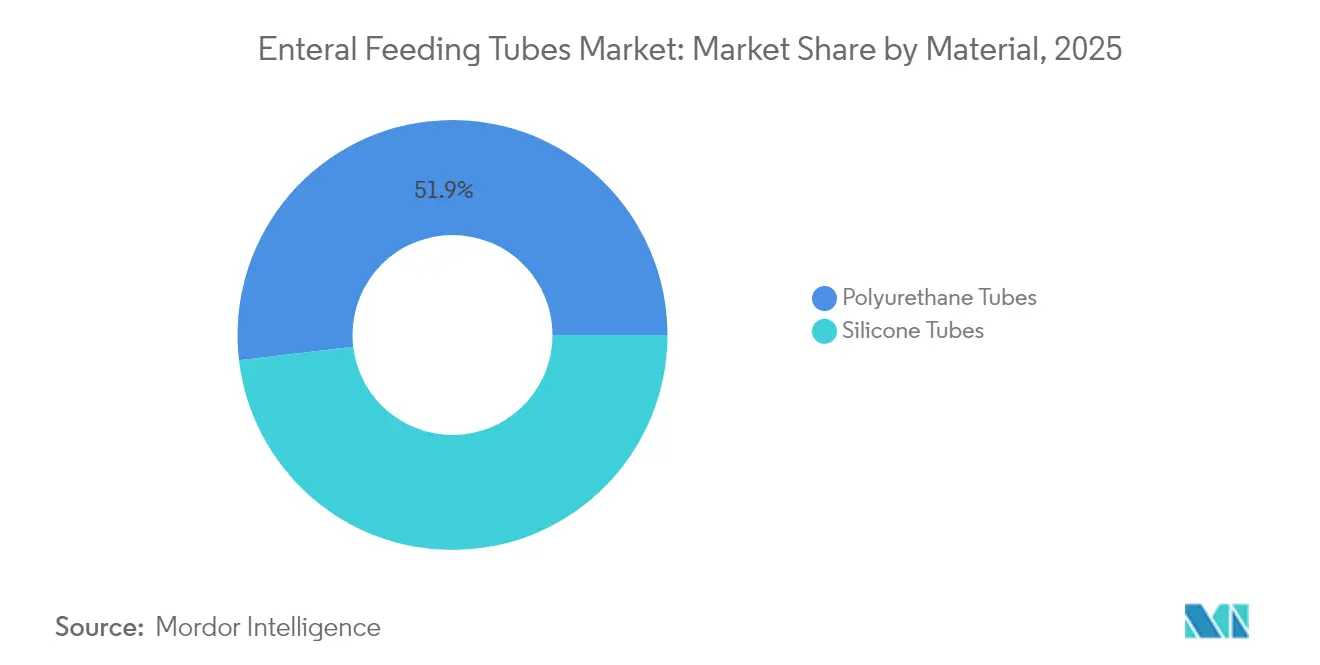

- By material, polyurethane tubes dominated with 51.88% share in 2025; silicone tubes usage is advancing at 8.11% CAGR to 2031.

- By placement technology, endoscopic placement owned the largest 63.92% revenue slice in 2025; the electromagnetic tracking placement is the fastest-growing segment at 9.81% CAGR.

- By geography, North America retained 38.12% of global revenue in 2025; Asia-Pacific is the fastest-growing region at 8.79% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Enteral Feeding Tubes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of chronic gastrointestinal disorders | +1.8% | North America, Europe | Long term (≥ 4 years) |

| Growing global malnutrition burden | +1.2% | Asia-Pacific, MEA, South America | Medium term (2-4 years) |

| Sharp uptick in pre-term births in low-income countries | +0.9% | Asia-Pacific, MEA, South America | Long term (≥ 4 years) |

| Adoption of home enteral nutrition programs by payers | +1.1% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Miniaturised wireless sensors enabling placement verification | +0.7% | Global | Short term (≤ 2 years) |

| Mandates for nasogastric tube mis-placement audits in OECD hospitals | +0.5% | OECD countries | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Chronic Gastrointestinal Disorders

An aging global population, coupled with higher cancer and inflammatory bowel disease prevalence, is fueling long-term demand for enteral nutrition. British Society of Gastroenterology guidance issued in 2025 confirms that most cancer patients present multiple gastrointestinal symptoms requiring early feeding support[1]British Society of Gastroenterology, “Practice Guidance on GI Symptoms in Cancer Patients,” gut.bmj.com. Providers therefore rely on precision placement technologies, especially electromagnetic guidance, to optimize outcomes. Health systems acknowledge the cost avoidance that stems from preventing disease-related malnutrition, sustaining the enteral feeding tubes market’s growth trajectory.

Growing Global Malnutrition Burden

Malnutrition affects up to 80% of oncology patients and continues to burden elderly and critical-care cohorts. Industry players answer with plant-based formulations and tube innovations that improve nutrient delivery. Oncology Nursing Society data showing 17–55% food-insecurity rates among cancer patients underline the social-determinant dimension that keeps enteral nutrition essential.

Sharp Uptick in Pre-Term Births in Low-Income Countries

Survival gains among extremely-low-birth-weight infants create sustained neonatal feeding demand. Cleveland Clinic reported 5.5% mortality for G-tube–only neonates versus 26.9% for tracheostomy-only cases, underscoring enteral feeding’s life-saving role. Hospitals in emerging economies adopt scoring algorithms and ultrasound monitoring to manage intolerance, which expands the enteral feeding tubes market in resource-constrained regions.

Adoption of Home Enteral Nutrition Programs by Payers

Medicare’s 2025 Home Health rule enhanced reimbursement for home nutrition, validating cost savings gained by shifting suitable patients out of hospitals[2]Federal Register, “CY 2025 Home Health PPS Rate Update,” federalregister.gov. UPMC demonstrated that its nasogastric home protocol saved roughly 900 NICU days in 2024 without compromising feeding milestones. Such outcomes encourage private insurers to replicate home-based models, elevating demand for portable, easy-to-monitor tubes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High tube-related infection rates in long-term care facilities | −0.8% | North America, Europe | Medium term (2-4 years) |

| Sub-optimal reimbursement for paediatric home care | −0.6% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Silicone price volatility affecting OEM margins | −0.4% | Global | Short term (≤ 2 years) |

| Sterilisation-capacity shortages post-ethylene-oxide curbs | −0.7% | Global, especially North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Tube-Related Infection Rates in Long-Term Care Facilities

A study of geriatric patients showed 72% mortality during follow-up, spotlighting infection and aspiration challenges that dampen adoption in nursing homes. Inconsistent staff training and limited on-site expertise mean facilities struggle to meet best-practice protocols, restraining the enteral feeding tubes market in this segment.

Sub-Optimal Reimbursement for Paediatric Home Care

Coverage rules lag technological progress, leaving gaps for specialized pediatric formulations and placement aids. The Oley Foundation notes that U.S. reimbursement policies for home enteral products have changed little in 30 years, adding administrative hurdles and slowing therapy initiation[3]Oley Foundation, “Medicare Coverage for HPN,” oley.org. Limited funding discourages manufacturers from fast-tracking pediatric-focused innovations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Enterostomy Dominance Drives Innovation

Enterostomy tubes contributed 45.86% of global revenue in 2025, underscoring their role in long-term nutritional support for oncology and neurology patients. Within the enteral feeding tubes market size, gastrostomy buttons and PEG variants retain clinician preference for comfort and reduced aspiration risk. Manufacturers refine internal retention disks and low-profile ports, elevating patient mobility. Self-advancing spiral tubes, set to grow 10.63% annually, employ embedded micro-motors and guidewires to reach the jejunum without fluoroscopy. That automation lowers procedure time, trims imaging costs, and is gaining acceptance in bariatric and critical-care units.

Nasojejunal and nasogastric tubes stay relevant for acute feeding but share of spend is gradually edging toward advanced spiral devices. Oroenteric tubes remain a neonatal niche used when nasal placement impedes breathing. Jejunostomy demand rises following upper-GI surgeries where gastric feeding is contraindicated, helping hospitals meet enhanced-recovery protocols. Clinical data linking self-advancing designs to higher first-pass success supports wider procurement, reinforcing the enteral feeding tubes market’s premiumization trend.

By Patient Type: Adult Stability Contrasts Neonatal Growth

Adults provided 69.98% of revenue in 2025 as aging populations face dysphagia, stroke, and cancer-related cachexia. Hospitals favor electromagnetic trackers in these cohorts to navigate altered anatomy after surgery or radiation. Yet neonates deliver the fastest expansion at 8.32% CAGR, powered by improved survival of very-low-birth-weight infants and wider NICU capabilities in emerging markets. Studies show eliminating routine gastric residual checks can shorten hospital stays by two days, prompting broader acceptance of early feeding protocols.

Pediatric-specific tubes with narrower French sizes and softer tips improve tolerance, although reimbursement remains a headwind in some regions. Adult demand will stay anchored in chronic diseases, while neonatal gains diversify regional consumption patterns, sustaining the enteral feeding tubes market across age segments.

By Application: Oncology Leadership Faces Critical-Care Challenge

Oncology accounted for 32.44% of 2025 revenue, reflecting high malnutrition incidence and chemotherapy-induced mucositis that impedes oral intake. Radiation oncology centers integrate tube placement before treatment initiation to avoid weight-loss-related interruptions. Critical care and trauma is projected to rise 8.89% CAGR, propelled by guidelines calling for nutrition within 48 hours of ICU admission. Electromagnetic systems reduce bedside insertion time, a crucial advantage in unstable patients.

Neurology indications such as stroke and ALS continue to require long-term tubes with low-migration profiles. Gastroenterology cases, notably Crohn’s disease and gastroparesis, benefit from nasojejunal routes that bypass compromised gastric function. Metabolic and hepatology applications round out demand for specialized formulas. Oncology’s head-start in evidence and reimbursement keeps it the largest slice, yet ICU adoption rates may erode the gap as clinical protocols standardize, expanding the enteral feeding tubes market’s procedural mix.

By End User: Hospital Dominance Challenged by Home Care Expansion

Hospitals captured 61.94% of spend in 2025 because most initial placements still occur in-patient. Operating rooms and endoscopy suites maintain volume for PEG and jejunostomy procedures. However, insurers are channeling appropriate cases to outpatient centers, causing ambulatory surgical sites to grow steadily. Home care, scaling at 9.74% CAGR, benefits from remote monitoring apps that alert clinicians to occlusion or displacement events. UPMC’s NICU program proved cost and stay reductions, prompting other systems to pilot similar home pathways. Long-term care facilities remain a substantial but slower-growing outlet due to infection challenges. As reimbursement aligns with value-based care, the enteral feeding tubes market tilts toward decentralized service models that pair hardware with telehealth oversight.

By Material: Polyurethane Leads Despite Silicone Innovation

Polyurethane delivered 51.88% of 2025 revenue thanks to insertion-friendly stiffness that softens at body temperature, improving patient comfort. Silicone tubes, while pricier, are set to climb 8.11% CAGR as their chemical resistance and low protein adhesion extend device life. Suppliers hedge raw-material volatility by expanding capacity: Avient added medical-grade TPU lines in Suzhou to serve Asia-Pacific growth. Manufacturers also explore bio-based polymers that meet sustainability targets without sacrificing performance. Metal-infused tips for fluoroscopic visibility and antimicrobial coatings that deter biofilm formation surface across both material classes. Polyurethane will keep volume leadership, but silicone’s premium share gain supports margin uplift within the enteral feeding tubes market.

By Placement Technology: Endoscopic Standard Faces Electromagnetic Disruption

Endoscopic guidance represented 63.92% of placements in 2025, valued for direct visualization and high accuracy when specialists are available. Yet staff shortages and radiation concerns spur interest in electromagnetic tracking, forecast to grow 9.81% annually. Avanos’ CORTRAK 2 system provides graphic pathways that confirm location without X-ray, aligning with audit mandates for misplacement prevention. A 2024 trial using low-cost magnet sensors achieved localization within 1.63 cm of X-ray benchmarks, proving feasibility for resource-limited settings. Fluoroscopic techniques still serve complex anatomies but face reimbursement pressure from dose-reduction policies. Camera-tipped tubes such as Cardinal Health’s IRIS deliver real-time internal images, carving a niche for high-risk or pediatric cases. The technology race elevates switching costs and entrenches brand differentiation, reinforcing competitive intensity inside the enteral feeding tubes market.

Geography Analysis

North America held 38.12% of global revenue in 2025 due to robust reimbursement, established clinical guidelines, and early uptake of placement verification technologies. The United States drives R&D investment; companies like Cardinal Health and BD base electromagnetic or imaging platforms on domestic pilot data before global roll-out. Canada’s single-payer model secures province-wide contracts, enhancing vendor scale. Mexico, while smaller, adopts cost-effective polyurethane tubes for public hospitals, broadening regional consumption.

Asia-Pacific is expanding at a 8.79% CAGR, the fastest globally, underpinned by infrastructure upgrades and regulatory harmonization. China’s pending Medical Device Law raises compliance stakes but simplifies foreign registration, favoring global suppliers with quality records. India’s risk-based classification fast-tracks low-risk feeding kits yet still demands local performance data. Japan’s device-act amendments shorten review timelines, attracting launches of wireless sensors. South Korea’s Digital Medical Products Act encourages AI-enabled monitoring, complementing traditional tubes. Collectively these measures inject momentum into the enteral feeding tubes market across Asia-Pacific, where aging populations and neonatal care improvements converge.

Europe delivers steady growth through stringent safety protocols and high public-sector spending. Germany and the United Kingdom lead adoption of electromagnetic guidance, motivated by mandating misplacement audits. Southern and Eastern European markets, though smaller, invest EU recovery funds into modern endoscopy and ICU capacity, widening access to advanced tubes. Middle East and Africa witness incremental gains, driven by Gulf Cooperation Council hospital expansions and training programs that lift procedural volumes. In South America, Brazil and Argentina spearhead uptake despite economic volatility, leaning on public procurement to secure essential nutrition devices. These varied regional dynamics ensure a diversified revenue base for the enteral feeding tubes market.

Competitive Landscape

The enteral feeding tubes market shows moderate consolidation, with top multinationals acquiring smart-monitoring assets to augment core tubing lines. BD’s 2024 purchase of Edwards Lifesciences’ Critical Care portfolio brought advanced hemodynamic sensors that integrate with feeding platforms, enabling holistic patient oversight. Avanos leverages its CORTRAK electromagnetic navigation to retain hospital contracts and recently extended direct UK distribution for MIC-KEY buttons to sharpen service levels.

Production expansion secures supply and hedges sterilization constraints. Gerresheimer invested USD 180 million in a Georgia site for molded components, boosting U.S. capacity. Lubrizol’s partnership with Polyhose commits USD 350 million to a Chennai tubing plant, supporting Asia-Pacific material demand. Patent activity concentrates on wireless sensing, antimicrobial coatings, and self-propelling tips, sustaining high entry barriers.

Competition increasingly revolves around digital ecosystems that pair hardware with analytics dashboards. Cardinal Health integrates IRIS camera streams into its Kangaroo feed pumps, capturing device-linked data for performance reporting. Nestlé Health Science’s formula4success portal helps clinicians navigate reimbursement paperwork, deepening brand loyalty. In pediatrics, white-space remains for miniaturized connectors and family-friendly training apps. Regional manufacturers in China and Brazil compete on price, but premium Western brands retain share where misplacement audits favor advanced technologies, keeping rivalry intense yet focused on value-added differentiation within the enteral feeding tubes market.

Enteral Feeding Tubes Industry Leaders

Cardinal Health

Boston Scientific Corporation

ENvizion Medical Inc.

Applied Medical Technology Inc.

B Braun Melsungen AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Lubrizol and Polyhose signed a memorandum of understanding to build a medical tubing facility in Chennai, expanding capacity five-fold and committing over USD 350 million.

- September 2024: Avient announced healthcare TPU expansion in Suzhou to supply medical-grade polymers for enteral devices.

Global Enteral Feeding Tubes Market Report Scope

As per the scope of the report, enteral feeding can be defined as the delivery of proteins, minerals, other essential nutrient products, and liquefied drugs into the stomach or intestine of the patient via feeding tubes and are used in the management of acute and chronic illness. These feeding tubes are known as enteral feeding tubes and can be inserted through the oral, nasal, or subcutaneous passage. The market is segmented by Product Type (Nasoenteric Feeding Tube, Enterostomy Tube, and Oroenteric Feeding Tube), Patient Type (Adult, Pediatric), Application Type (Oncology, Neurology, Gastroenterology, Metabolic Disorders, Hepatology, and Other Applications), End-user (Hospitals, Ambulatory Surgical Centers and Others) and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| Nasoenteral Feeding Tubes | Nasogastric Tubes |

| Nasojejunal Tubes | |

| Enterostomy Tubes | Gastrostomy Tubes (PEG, Button) |

| Jejunostomy Tubes | |

| Oroenteric Tubes | |

| Self-Advancing Spiral Tubes |

| Adults |

| Paediatrics |

| Neonates |

| Oncology |

| Neurology |

| Gastroenterology |

| Metabolic Disorders |

| Hepatology |

| Critical Care & Trauma |

| Hospitals |

| Ambulatory Surgical Centres |

| Home Care Settings |

| Long-term Care Facilities |

| Polyurethane Tubes |

| Silicone Tubes |

| Endoscopic Placement |

| Fluoroscopic Placement |

| Electromagnetic Tracking Placement |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Nasoenteral Feeding Tubes | Nasogastric Tubes |

| Nasojejunal Tubes | ||

| Enterostomy Tubes | Gastrostomy Tubes (PEG, Button) | |

| Jejunostomy Tubes | ||

| Oroenteric Tubes | ||

| Self-Advancing Spiral Tubes | ||

| By Patient Type | Adults | |

| Paediatrics | ||

| Neonates | ||

| By Application | Oncology | |

| Neurology | ||

| Gastroenterology | ||

| Metabolic Disorders | ||

| Hepatology | ||

| Critical Care & Trauma | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centres | ||

| Home Care Settings | ||

| Long-term Care Facilities | ||

| By Material | Polyurethane Tubes | |

| Silicone Tubes | ||

| By Placement Technology | Endoscopic Placement | |

| Fluoroscopic Placement | ||

| Electromagnetic Tracking Placement | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the enteral feeding tubes market?

The enteral feeding tubes market is estimated at USD 2.98 billion in 2026 and is projected to reach USD 3.95 billion by 2031.

Which product category leads the enteral feeding tubes market?

Enterostomy tubes led with 45.86% revenue share in 2025, driven by long-term oncology and neurology use.

Why is Asia-Pacific the fastest-growing region?

Infrastructure investment, regulatory modernization, and aging demographics push Asia-Pacific growth at a 8.79% CAGR through 2031.

How are payers influencing market dynamics?

Expanded reimbursement for home enteral nutrition programs lowers hospital stays and boosts demand for portable, easy-monitor tubes.

What technology trend is reshaping tube placement?

Electromagnetic tracking systems provide radiation-free, real-time verification and are forecast to grow 9.81% annually as hospitals comply with misplacement audit rules.

Page last updated on: