Endoscopic Submucosal Dissection Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

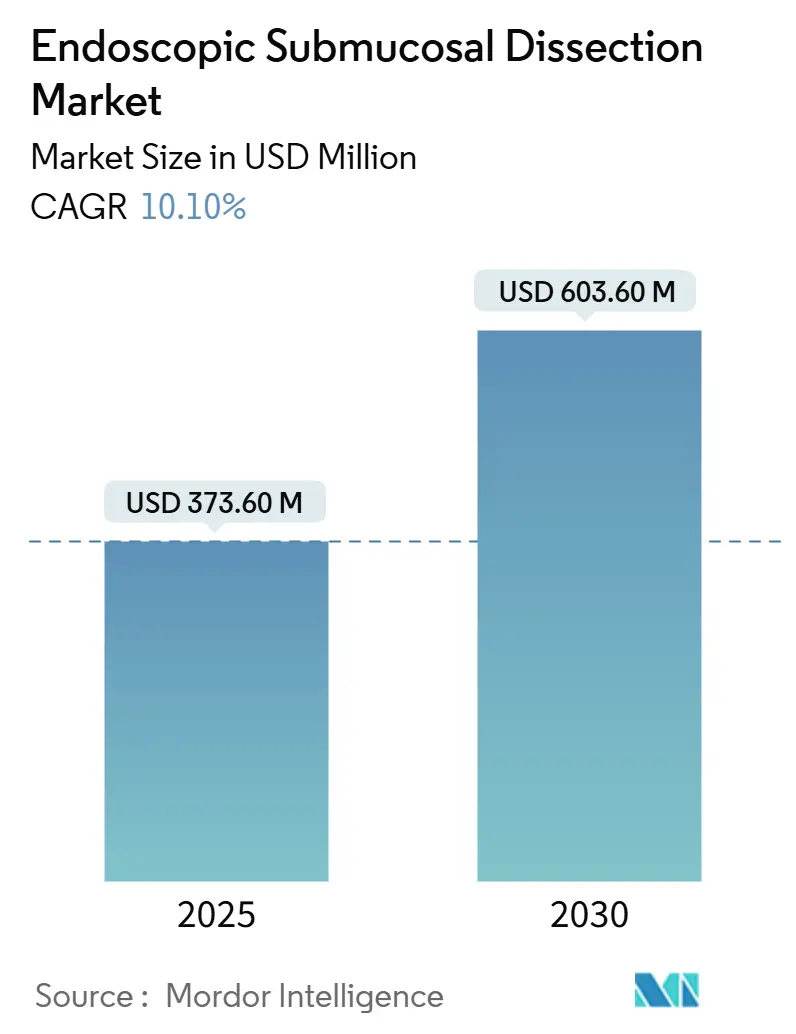

| Market Size (2025) | USD 373.60 Million |

| Market Size (2030) | USD 603.60 Million |

| Growth Rate (2025 - 2030) | 10.10% CAGR |

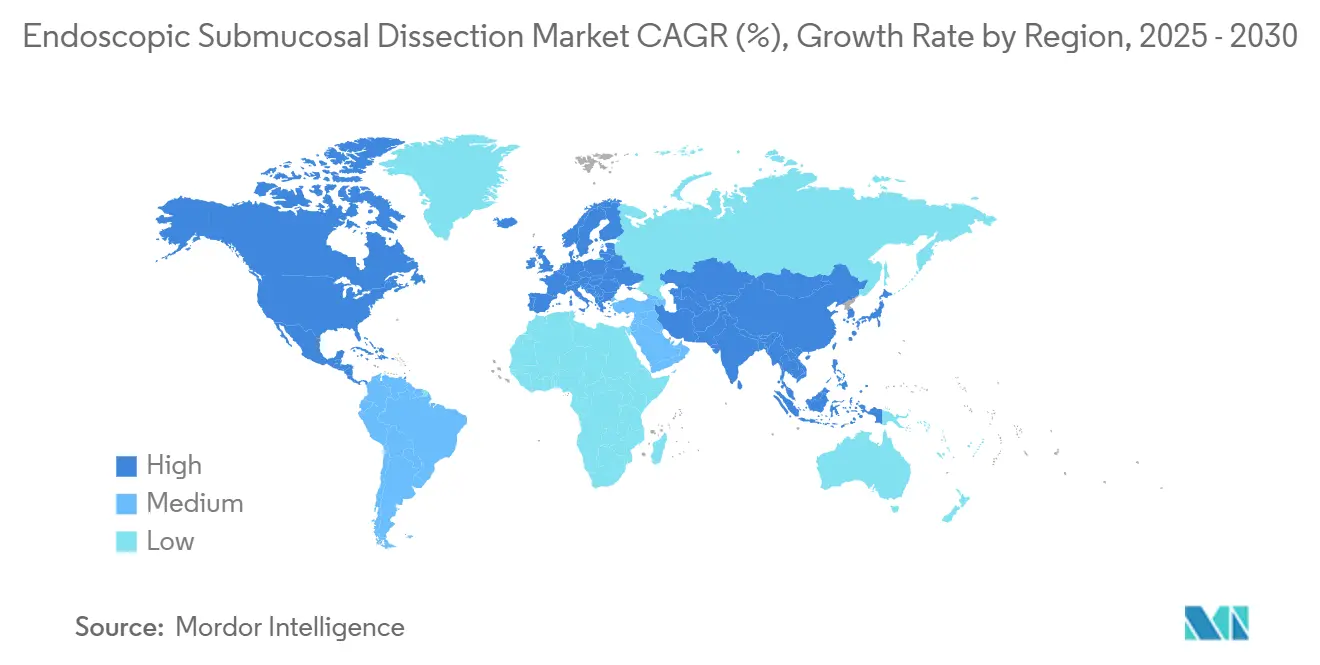

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Endoscopic Submucosal Dissection Market Analysis by Mordor Intelligence

The endoscopic submucosal dissection market reached USD 373.6 million in 2025 and is forecast to attain USD 603.6 million by 2030, advancing at a 10.1% CAGR during the period. Sustained growth stems from payer support for minimally invasive GI oncology, the clinical superiority of en bloc resections, and steady technology refresh cycles that now bundle AI guidance with high-definition imaging. Vendors that synchronize device innovation with ambulatory care protocols are capturing early mover advantage as outpatient GI suites expand procedure schedules. Robotic traction systems, single-use knives, and cloud analytics together shorten room time, reduce staff load, and generate the data sets necessary for reimbursement validation. Competitive intensity remains moderate because proprietary energy platforms and integrated imaging ecosystems create switching costs, yet a rising cohort of venture-backed robotics firms is pressuring incumbents to accelerate release cadences.

Key Report Takeaways

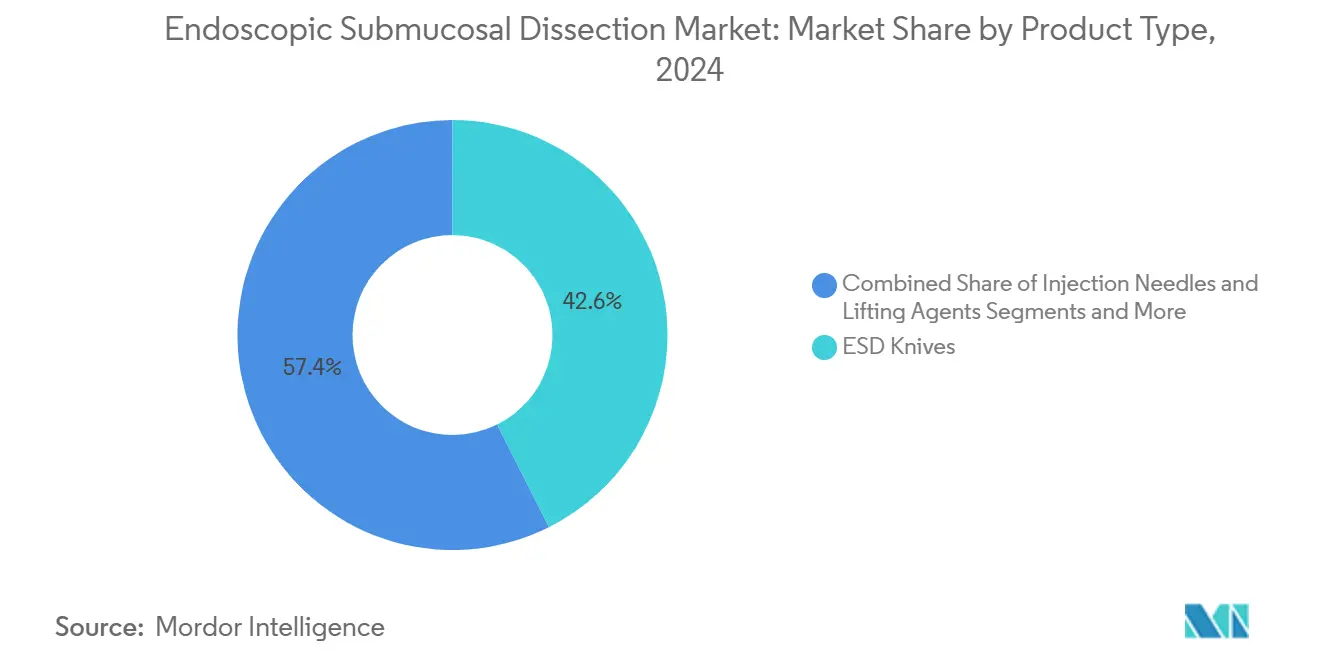

- By product type, ESD knives captured 42.6% of the global endoscopic submucosal dissection (ESD) market share in 2024, while robotic-assisted ESD platforms are projected to grow at the fastest CAGR of 18.7% through 2030.

- By indication, early gastric cancer accounted for 36.4% of ESD procedures in 2024, with colorectal neoplasia expected to expand at a 13.4% CAGR through 2030.

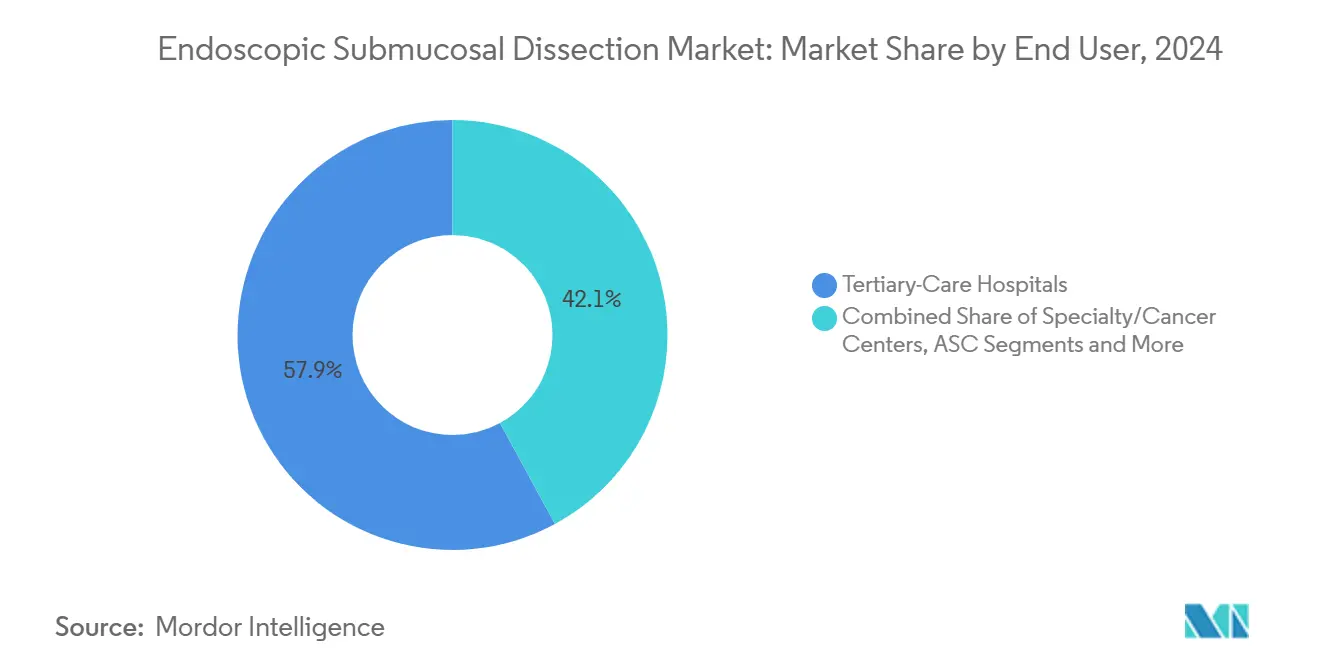

- By end user, tertiary-care hospitals performed 57.9% of total ESD cases in 2024, whereas ambulatory surgery centers are advancing at a 12.6% CAGR through 2030.

- By geography, North America generated a 42.6% revenue share in 2024, while Asia Pacific is forecast to grow at a 9.7% CAGR through 2030.

Global Endoscopic Submucosal Dissection Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise In Early-Stage GI Cancer Screening | +2.10% | Global, with stronger adoption in North America & Japan | Medium term (2-4 years) |

| Preference For Minimally-Invasive En-Bloc Resection | +1.80% | Global, particularly North America & Europe | Short term (≤ 2 years) |

| Surge In Adoption Of ESD-Specific Electrosurgical Knives | +1.40% | Asia Pacific core, spill-over to North America | Medium term (2-4 years) |

| Favorable Reimbursement For Advanced Endoscopy | +1.20% | North America & select European markets | Long term (≥ 4 years) |

| AI-Guided Lesion Mapping Improving R0 Rates | +1.00% | Japan, expanding to North America & Europe | Medium term (2-4 years) |

| Emergence Of Single-Use Robotic ESD Platforms | +0.90% | North America & Europe, limited Asia Pacific penetration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rise in Early-Stage GI Cancer Screening

Nationwide colorectal and gastric screening initiatives are front-loading oncology caseloads with small, resectable lesions that benefit from ESD’s en bloc capability. Japan’s mandatory colonoscopy at age 45 and Korea’s biennial gastric programs proved the economic value of early intervention, lowering long-term treatment budgets and setting a precedent for Western payers.[1]Misawa, Masashi, “Implementation of Artificial Intelligence in Colonoscopy Practice in Japan,” JMA J, jma.jpAI-aided colonoscopy, such as Fujifilm’s CAD EYE, lifted adenoma detection by 17% per exam, guaranteeing that more high-risk lesions funnel into therapeutic lists. Value-based reimbursement packages in the United States now reward early lesion removal, pushing hospitals to market screening days aggressively. Emerging markets are adapting the template, adding double-balloon endoscopy hubs to bring remote populations into the funnel. Together, these moves expand the procedure pipeline and stabilize utilization rates that underpin capital purchases.

Preference for Minimally Invasive En Bloc Resection

ESD achieves ≥90% en bloc rates versus <60% with piecemeal EMR, providing definitive pathology and slashing local recurrence. Robotics-based traction now trims mean dissection time by 40.8%, alleviating earlier duration concerns and opening scheduling windows for ASC throughput. Institutions are revising care pathways to favor ESD for lesions up to 40 mm because higher upfront consumable costs are offset by lower retreatment rates. Virtual reality modules and cloud video libraries standardize credentialing, so hospital credentialing committees can green-light more operators without relying on overseas fellowships. Insurers that once capped payments at EMR levels are issuing add-on codes when R0 documentation accompanies claims, cementing the volume shift.

Surge in Adoption of ESD-Specific Electrosurgical Knives

Multifunctional blades such as Olympus Triangle Tip and Boston Scientific ORISE ProKnife combine injection, cutting, and coagulation in one pass, cutting accessory exchanges by >30% per case. These knives dominate Asian high-volume centers, and Western physicians adopt them after peer-reviewed outcome reports highlight shorter anesthesia times. Single-use formats remove reprocessing costs and eliminate micro-corrosion that can degrade current density. Vendors iterate on tip geometry to address anatomic nuances, like curved insulated shanks for duodenal work where thermal spread must be minimal. Consistent traction compatibility makes new knives integral to robotic platforms, reinforcing a bundled-sale dynamic that favors companies with broader portfolios.

AI-Guided Lesion Mapping Improving R0 Rates

Deep-learning algorithms now delineate dissection planes within 3 mm accuracy, projecting safe margins on the surgical field.[2]Xu, Mengya et al., “ETSM: Automating Dissection Trajectory Suggestion,” arxiv.org Olympus’s CADDIE and CADU systems feed cloud analytics back to operators in real time to flag submucosal vessels that would otherwise trigger intraprocedural bleeding. Japan’s 2024 decision to reimburse AI-assisted endoscopy validated ROI modeling and de-risked hospital purchases. Early adopters report a 4.2 percentage-point jump in curative R0 resections, which directly influences oncologic follow-up strategies. As datasets scale, vendors intend to auto-populate procedure notes, simplifying coding compliance and further anchoring AI as a mandatory workflow component.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Steep Learning Curve & Limited Training Pathways | -1.60% | Global, particularly acute in North America & Europe | Medium term (2-4 years) |

| High Capital & Consumable Costs | -1.20% | Emerging markets & smaller healthcare institutions globally | Long term (≥ 4 years) |

| Inadequate Coding For Hybrid/Robotic ESD Outside Japan | -1.10% | North America & Europe, limited impact in Asia Pacific | Medium term (2-4 years) |

| Supply Chain Bottlenecks For High-Frequency Knife Chips | -1.00% | Global, with acute impact in North America & Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Steep Learning Curve & Limited Training Pathways

Competency typically requires 30-50 proctored cases, yet most Western hospitals log <10 annual ESDs, constraining resident exposure. Fellowship tracks remain informal, and credentialing criteria differ by institution, yielding heterogenous quality. Fujifilm’s EndoGel simulator lets trainees practice full-thickness resections on synthetic tissue, but uptake is nascent outside Japan. ASGE’s digital coaching network pairs mentors with geographically distant learners, though time-zone mismatches hamper live proctoring. Progress depends on scalable virtual reality curricula that embed AI feedback loops to deliver objective skill scoring.

High Capital & Consumable Costs

A full ESD platform, inclusive of imaging tower, energy generator, CO₂ insufflator, and hand instruments, can top USD 500,000, while single-use knives and clips add USD 3,000-5,000 per case.[3]Medicare Payment Advisory Commission, “Ambulatory Surgical Center Services: Status Report,” medpac.gov Reimbursement gaps outside Asia mean hospitals often use unlisted CPT codes, risking partial denials. Ambulatory surgery centers buffer costs through lower overhead and quicker turnover, but their thinner capital budgets limit adoption of premium imaging stacks. Single-use robotic platforms hold promise for shifting expense from capex to opex; however, unit economics remain unproven at scale, keeping CFOs cautious. Vendor financing and procedure-based leasing schemes are emerging stop-gaps until payer coding stabilizes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Specialized Knives Anchor Procedural Efficiency

ESD knives captured 42.6% of the endoscopic submucosal dissection market share in 2024, underscoring their indispensability for precise tissue layer separation. Upgrades such as embedded injection ports and variable stiffness shafts helped standard knives remain relevant even as robotics gains mindshare. Electrosurgical generators co-evolve, adding feedback loops that auto-modulate current to match real-time impedance readings, thereby lowering perforation risk. Robotic-assisted ESD platforms lead growth at an 18.7% CAGR, buoyed by data showing 35% reductions in muscularis propria injuries during porcine trials.

Ancillary accessories—traction clips, caps, hood cones—are expanding as lesion complexity rises. Closure devices migrate from generic metal clips to shape-memory alloys with 360° rotation, exemplified by Olympus Retentia, which secures mucosal edges with single-click deployment. The convergence of AI modules with core instruments blurs product boundaries, encouraging vendors to market entire “intelligent ESD suites” rather than discrete SKUs. This bundling strategy locks in repeat consumable sales and fortifies ecosystem loyalty.

By Indication: Gastric Lesions Remain Core, Colorectal Cases Accelerate

Early gastric cancer accounted for 36.4% of total procedures, sustaining its position since Japan’s R0 benchmarks underpin global guideline adoption. Colorectal neoplasia is set to outpace at 13.4% CAGR, driven by FIT-positive screening cohorts that reveal flat nongranular lesions unsuitable for EMR. The endoscopic submucosal dissection market size for colorectal use is forecast to add nearly USD 70 million by 2030, reflecting payers’ willingness to reimburse organ-sparing resections when histology confirms clear margins.

Esophageal indications gain traction where Barrett-associated neoplasia prevalence climbs. Endoscopists adopt pocket-creation methods to handle fibrotic post-ablation tissue, leveraging dual-channel scopes for retroflex traction. Subepithelial tumors once destined for laparoscopic resection now qualify for ESD using knife designs with extended insulation, broadening clinical utility. With AI systems predicting invasion depth, case selection for duodenal lesions becomes safer, translating into incremental volume for high-acuity centers.

By End User: ASC Expansion Redraws Volume Distribution

Tertiary hospitals retained 57.9% of procedures in 2024, yet ambulatory surgery centers are set to post a 12.6% CAGR through 2030 as payers adjust fee schedules to incentivize outpatient settings. The endoscopic submucosal dissection market size attributed to ASCs will surpass USD 150 million by 2030, buoyed by Medicare’s bundled payment lifts. Same-day discharge protocols now clear 28.8% of eligible esophageal ESD cases, easing capacity constraints in tertiary ICUs.

Academic institutes remain critical for disseminating best practices; they secure industry grants to run simulator labs and host live animal workshops. Specialty cancer centers continue to absorb the most complex, multilesion cases, serving as referral destinations and registry data hubs. Their role in prospective trials ensures that device approvals align with rigorous oncologic endpoints, sustaining evidence pipelines that feed payer dossiers.

Geography Analysis

North America generated 42.6% of 2024 revenue thanks to robust ASC networks, CPT add-on payments, and close industry-clinician collaboration. Early adoption of AI-enhanced imaging positions U.S. centers as reference sites that vendors showcase to international buyers. Canadian provinces, citing U.S. outcomes data, are piloting similar reimbursement carve-outs, potentially adding 3,000 annual procedures by 2027.

Asia Pacific records the fastest 9.7% CAGR, led by Japan’s mature ecosystem and China’s rapid expansion of digestive disease hospitals. The endoscopic submucosal dissection market size in Asia Pacific is projected to climb from USD 152 million in 2025 to USD 242 million by 2030. China’s National Medical Products Administration cleared five domestic knives in 2024, lowering acquisition costs by 28% for local hospitals and accelerating provincial tender volumes. South Korea’s National Cancer Center reports that combined ESD plus AI assessment reduced recurrence at 24 months to 3.2%, bolstering national insurance support. Australia is bridging geographic disparities by equipping rural hubs with mobile endoscopic towers and tele-mentoring links that stream live overlays from urban centers.

Europe shows steady but methodical growth as the Medical Device Regulation tightens evidence demands. German DRG reforms now reimburse ESD at parity with surgical wedge resections when R0 data accompany claims, yet many hospitals hesitate while waiting for CE-marked robotic systems. The United Kingdom’s NHS GI transformation plan allocates GBP 120 million for endoscopy backlog clearance, part of which funds AI-enabled scopes that indirectly fuel ESD readiness. Southern and Eastern European markets lag because of training shortages; collaborative programs with Japanese centers seek to fill the gap via month-long fellow exchanges.

Middle East & Africa and South America remain nascent but promising. Brazil’s private hospital chains adopt Olympus EVIS X1 stacks, incentivized by bundled service agreements that include remote AI analytics. Gulf states are trialing comprehensive cancer screening packages that embed endoscopy tourism into national clinical tourism strategies. Long-term success will depend on localized training ecosystems and region-specific cost-effectiveness data.

Competitive Landscape

Olympus, Fujifilm, and Boston Scientific form the core competitive triad, together holding approximately 55% of device revenue globally. Their integrated imaging-energy portfolios create high customer stickiness, yet growth-stage robotics firms such as EndoQuest and EndoMaster threaten to fracture share by offering full-thickness capabilities at lower hand-tremor transfer. Olympus’s 16% division revenue jump in 2024, fueled by 62% EVIS X1 sales growth in North America, underscores the payoff from iterative imaging upgrades.

Strategic moves concentrate on ecosystem fortification: Olympus partnered with Proximie to broadcast cloud video feeds, enabling remote proctoring that shortens the buyer adoption curve. ERBE’s takeover of Maxer Endoscopy (now Erbe Vision) marries energy delivery with 4K fluorescence imaging, positioning the firm to launch unified resection bundles. Fujifilm counters with AI-first roadmaps that integrate lesion segmentation algorithms across the entire tower.

Investment flows chase robotic traction and AI analytics. Sotelix’s USD 1.7 million seed round highlights investor appetite for niche therapeutic innovation. Canon Medical’s ultrasound alliance with Olympus creates cross-modality synergies that allow single-vendor procurement, simplifying hospital negotiations. Competitive pressures favor companies able to finance post-market surveillance registries demanded under new EU rules, a capability smaller entrants struggle to match.

Endoscopic Submucosal Dissection Industry Leaders

Olympus Corporation

Boston Scientific Corporation

Fujifilm Holdings Corporation

Medtronic

ERBE Elektromedizin

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Olympus received FDA 510(k) clearance for its EZ1500 extended-depth-of-field endoscopes, enhancing lesion visualization for ESD.

- March 2025: Olympus introduced Retentia HemoClip with 360° rotation for reliable defect closure after ESD.

- January 2025: Olympus acquired Sur Medical SpA to accelerate direct channel presence in Chile for advanced endoscopic solutions.

- October 2024: Olympus partnered with Proximie for real-time OR video collaboration, boosting ESD training reach.

Global Endoscopic Submucosal Dissection Market Report Scope

| ESD Knives |

| Injection Needles & Lifting Agents |

| Electrosurgical & HF Generators |

| Closure & Hemostatic Devices |

| Ancillary Accessories (Caps, Traction, Clips) |

| Early Gastric Cancer |

| Early Esophageal Neoplasia |

| Colorectal Neoplasia |

| Duodenal & Small-Bowel Lesions |

| Subepithelial / SMT Lesions |

| Tertiary-Care Hospitals |

| Specialty / Cancer Centers |

| Ambulatory Surgery Centers (ASCs) |

| Academic & Training Institutes |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | ESD Knives | |

| Injection Needles & Lifting Agents | ||

| Electrosurgical & HF Generators | ||

| Closure & Hemostatic Devices | ||

| Ancillary Accessories (Caps, Traction, Clips) | ||

| By Indication | Early Gastric Cancer | |

| Early Esophageal Neoplasia | ||

| Colorectal Neoplasia | ||

| Duodenal & Small-Bowel Lesions | ||

| Subepithelial / SMT Lesions | ||

| By End User | Tertiary-Care Hospitals | |

| Specialty / Cancer Centers | ||

| Ambulatory Surgery Centers (ASCs) | ||

| Academic & Training Institutes | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the endoscopic submucosal dissection market today?

It stood at USD 373.6 million in 2025 and is set to reach USD 603.6 million by 2030 at a 10.1% CAGR.

Which product category leads ESD revenue?

Specialized ESD knives accounted for 42.6% global revenue in 2024, reflecting their central role in every procedure.

What region is growing the fastest for ESD adoption?

Asia Pacific is advancing at a 9.7% CAGR through 2030, driven by Japan, China, and South Korea.

Why are ambulatory surgery centers important for ESD growth?

Medicare payment boosts and lower overhead enable ASCs to deliver outpatient ESD, which is projected to grow 12.6% annually.

How is artificial intelligence affecting ESD outcomes?

AI lesion mapping improves R0 resection rates by guiding margin planning and has already earned reimbursement in Japan.

What is the biggest barrier to wider ESD use in Western hospitals?

A steep learning curverequiring 30-50 supervised caseslimits the number of credentialed endoscopists in many centers.

Page last updated on: