End Load Cartoning Machine Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

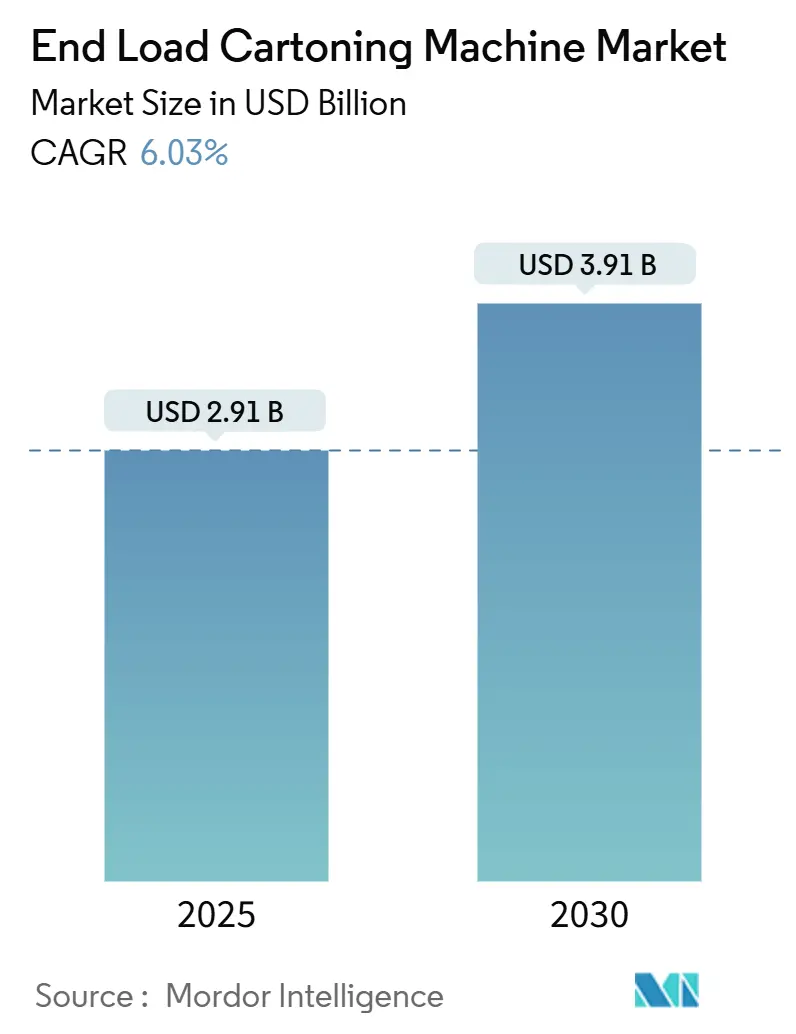

| Market Size (2025) | USD 2.91 Billion |

| Market Size (2030) | USD 3.91 Billion |

| Growth Rate (2025 - 2030) | 6.03% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

End Load Cartoning Machine Market Analysis by Mordor Intelligence

The End load cartoning machine market size stands at USD 2.91 billion in 2025 and is forecast to hit USD 3.91 billion by 2030, advancing at a 6.03% CAGR. Heightened demand for automated secondary packaging across food, beverage, pharmaceutical, and personal-care plants forms the core growth engine, with buyers seeking to curb labor shortages, comply with serialization rules, and cut plastic use. North America retains leadership on the strength of its 38.54% revenue share in 2024, yet Asia-Pacific is adding capacity fastest at 9.89% CAGR thanks to industrial policy incentives and rising consumer spending. Horizontal systems prevail because they marry high throughput with easy integration, while vertical formats win share in space-constrained plants. Mid-range speed machines in the 151-400 CPM band represent the sweet spot between throughput and flexibility, giving vendors a large installed base for upgrade sales. Input-price spikes for carton-grade board will keep margins thin, but regulatory pressure to shift from plastic to paperboard helps maintain volume growth.

Key Report Takeaways

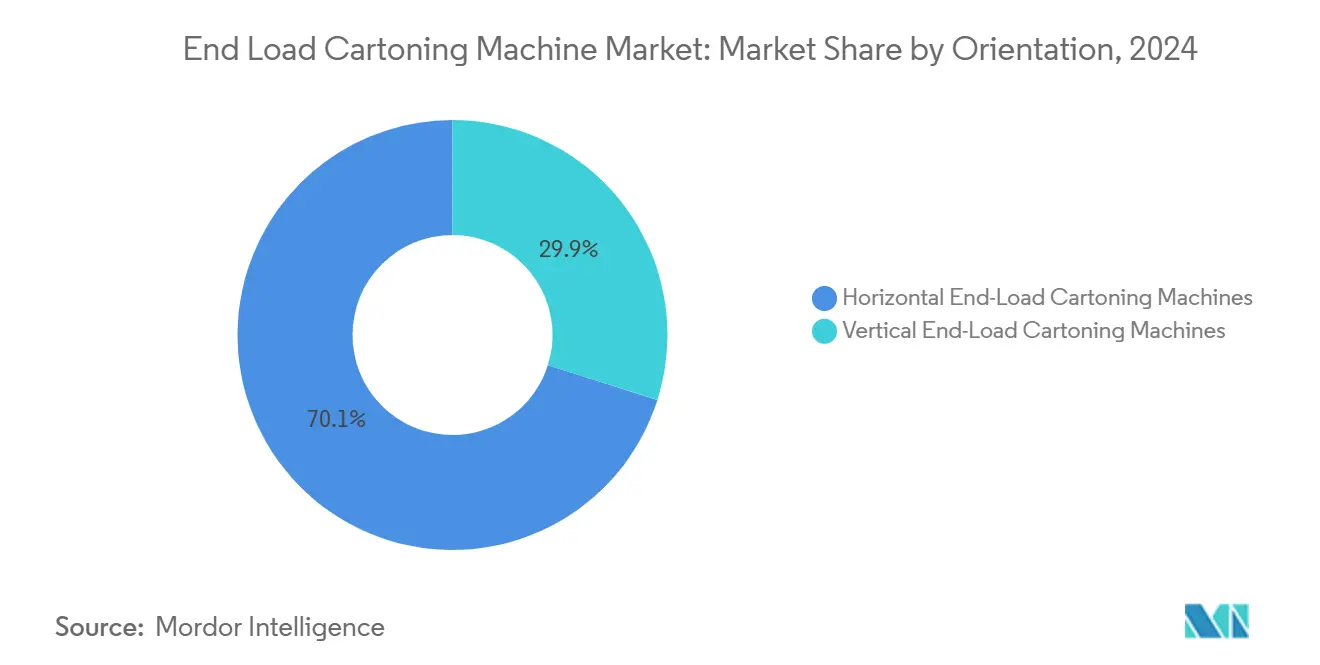

- By orientation, horizontal end-load systems secured 70.12% of End load cartoning machine market share in 2024, while vertical units are projected to post 7.42% CAGR through 2030.

- By speed class, the 151–400 CPM range captured 49.42% share of the End load cartoning machine market size in 2024 and is set to register 8.21% CAGR to 2030.

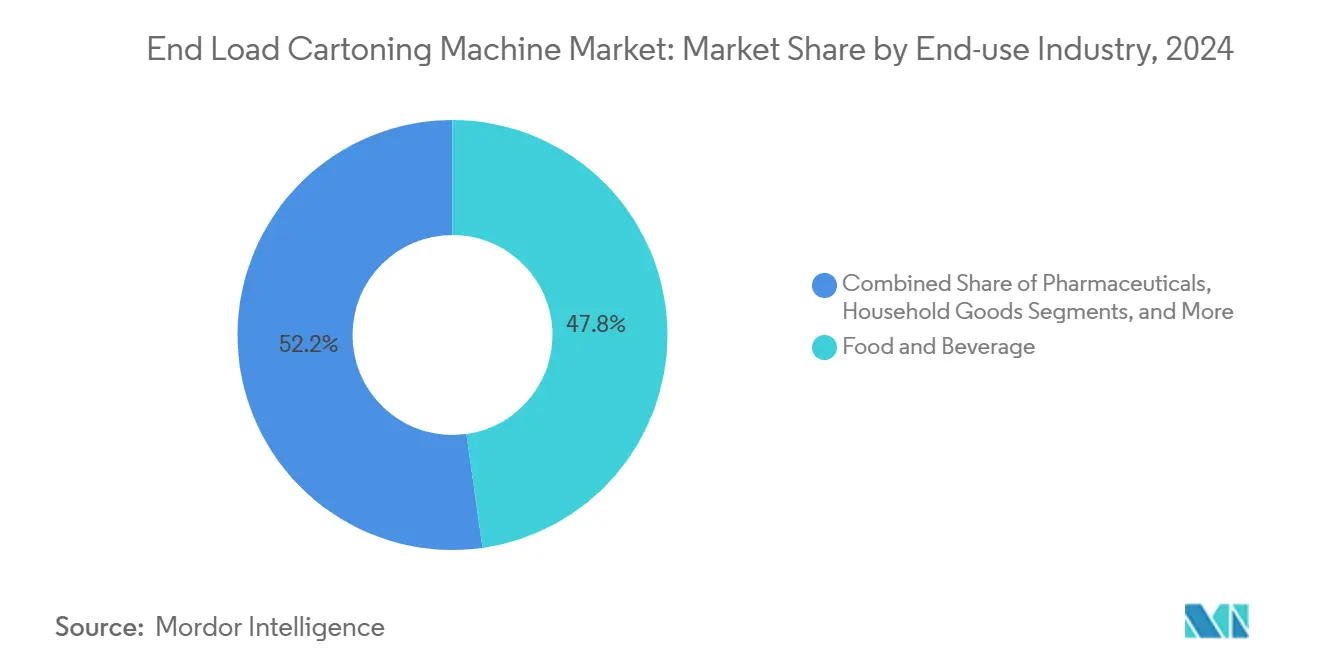

- By end-use industry, food and beverage held 47.78% revenue share in 2024, whereas pharmaceuticals are forecast to grow at 9.12% CAGR through 2030.

- By automation level, fully automatic lines commanded 58.43% share in 2024, with robotic-integrated layouts advancing at 8.32% CAGR.

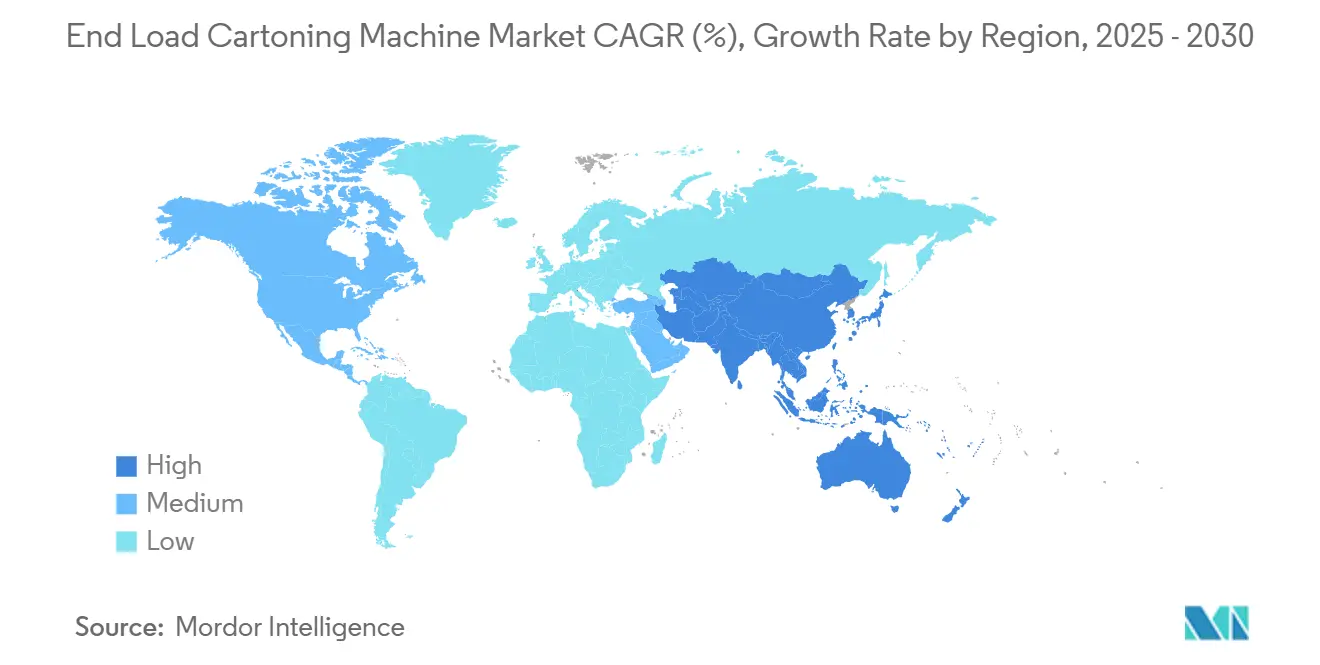

- By geography, North America led with 38.54% share in 2024, while Asia-Pacific is projected to expand at 9.89% CAGR through 2030.

Global End Load Cartoning Machine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for automated packaging in food and beverage | +1.2% | North America, Europe | Medium term (2-4 years) |

| Expansion of pharmaceutical serialization mandates | +1.8% | North America, EU | Short term (≤ 2 years) |

| Sustainability shift from plastic to paperboard cartons | +1.1% | Europe, North America | Long term (≥ 4 years) |

| Servo-driven modular machines enabling rapid SKU changeovers | +0.9% | Developed markets worldwide | Medium term (2-4 years) |

| E-commerce reverse-logistics ready packaging requirements | +0.7% | Asia-Pacific, North America | Medium term (2-4 years) |

| Predictive-maintenance analytics reducing downtime | +0.6% | Developed markets worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Automated Packaging in Food and Beverage

Food processors are scaling automation to tackle labor gaps, hygiene rules, and SKU proliferation. Once Upon a Farm trimmed shop-floor labor from 12 to 4 operators and lifted case output by nearly 40% after installing Somic’s automated packer. [1]Packworld Editorial Team, “Once Upon a Farm Automates Case Packing,” packworld.com ABB-equipped cobot cells show that automation can also cut plastic by 80% while improving ergonomics. [2]Tanner AG, “Cobots Arbeiten in Geschützter Werkstatt,” tannerag.ch Servo-driven horizontal units such as the KC-100F reach 240 CPM and complete changeovers without tools, supporting fast-moving snack lines. Premium product launches fuel demand for precise board handling and enhanced graphics. Industry 4.0-ready sensors raise uptime by more than 10%, making the End load cartoning machine market an early beneficiary of predictive analytics.

Expansion of Pharmaceutical Serialization Mandates

Regulations under the U.S. Drug Supply Chain Security Act and EU Falsified Medicines Directive oblige each carton to carry a unique data matrix code, pushing pharma plants to order high-precision cartoners with integrated printing and vision inspection. Siegfried and TraceLink reported faster compliance using a phased rollout that tied serialization to digital supply-chain dashboards. Turck’s RFID scanners read up to 500 tags in one pass, proving that advanced tracking can coexist with high speed. Vendors embed cameras that reject any pack with faulty codes, ensuring 100% compliance. These requirements lift capital spend, enlarging the End load cartoning machine market.

Sustainability Shift from Plastic to Paperboard Cartons

Brand owners are switching formats to hit 2030 plastic-reduction pledges. Mondelez adopted Sonoco’s EnviroCan, achieving more than 60% recycled fiber content while keeping products curbside recyclable. Mother Parkers Coffee replaced plastic tubs with an 80% FSC certified canister, trimming polymer use by at least 50%. Asia-Pacific mills plan to add 8 million t of cartonboard capacity through 2025, guaranteeing material supply. Cartoner OEMs now calibrate feed systems to accommodate moisture-sensitive fiber, broadening the End load cartoning machine market.

Servo-Driven Modular Machines Enabling Rapid SKU Changeovers

Volume volatility and personalization push manufacturers toward modular servo architectures. Syntegon’s BEC platform integrates a MagTRAC collator so bakery plants can switch cookie formats in under 15 minutes. Three-axis servo motion allows gentle handling of fragile confectionery and high-speed pushers for bar packs within the same frame. BW Packaging’s OpView interface guides operators step by step, cutting training hours. Modular frames also let buyers add robotics later, extending the End load cartoning machine market lifecycle.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capital expenditure | -1.4% | Emerging markets worldwide | Short term (≤ 2 years) |

| Shortage of skilled mechatronics operators | -0.8% | North America, Europe | Medium term (2-4 years) |

| Volatility in carton-grade paperboard supply | -0.6% | North America, Europe | Short term (≤ 2 years) |

| Regulatory pressure toward reusable packaging formats | -0.4% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Expenditure

State-of-the-art end-load cells with robotics, vision, and servo drives can top USD 1 million, stretching payback periods beyond five years for small plants. Install-and-validate costs, training, and line modifications often double total outlay. Rising interest rates harden lending terms, making leasing or Robots-as-a-Service attractive stopgaps. OEMs counter with modular frames that let buyers phase investments, yet sticker shock still slows the End load cartoning machine market in cash-constrained regions.

Volatility in Carton-Grade Paperboard Supply

Corrugated board prices rose USD 70 per ton in 2025, and chemical inputs climbed 30%, tightening converter margins. [3]CE Packaging, “Rising Costs in Corrugated Cardboard,” cepkg.com Plants pause equipment upgrades until raw-material trends stabilize, deferring some end-load cartoning machine market orders.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Orientation: Horizontal Machines Anchor Volume While Vertical Designs Climb

Horizontal units accounted for 70.12% of 2024 shipments, underpinning the End load cartoning machine market size leadership because they fit high-speed snack, cereal, and OTC medicine lines. Vertical machines are gaining at 7.42% CAGR, favored for fragile cosmetics that benefit from gravity loading. Continuous-motion pushers and multi-lane infeeds let horizontal frames exceed 400 CPM without upping footprint. Vertical cells, now paired with cobots, reduce drop height and floor space. OEM product roadmaps indicate future platforms will combine tilt-axis modules so plants can switch between orientations, widening the addressable End load cartoning machine market.

Rapid SKU churn forces even horizontal systems to promise sub-15-minute conversions, shrinking the historical changeover gap with vertical formats. Horizontal machine builders integrate recipe-driven lug chains that self-adjust carton width through servos. Vertical platforms answer with tool-less lane guides and camera-based product alignment. Both camps now embed closed-loop vacuum controls to handle recycled fiber board that can vary in caliper. These innovations ensure neither orientation will cannibalize the other, and they together bolster the End load cartoning machine market.

By Speed Class: Mid-Range Throughput Holds the Sweet Spot

Machines rated 151–400 CPM captured 49.42% of 2024 shipments and will expand at 8.21% CAGR, reflecting balanced capital outlay and flexible performance. The End load cartoning machine market size for this segment will reach significant volume as brand owners seek one frame that covers daily runs from granola bars to cold meds. Sub-150 CPM models stay relevant for specialty or regional brands, while ultra-high-speed above 400 CPM platforms mainly serve commoditized chewing gum or paracetamol.

Mid-range builders incorporate the same servo motion and code verification once exclusive to premium models, narrowing performance gaps. Energy-efficient drives cut kWh use by up to 20%, aligning with plant decarbonization targets. Above-400 CPM machines confront product variety that forces line stoppages, shifting buyer preference toward modular mid-range cells. As a result, vendors focus R&D here, further enlarging the End load cartoning machine market.

By End-use Industry: Food Leads, Pharma Accelerates

Food and beverage accounted for 47.78% of unit demand in 2024, driven by ready-meal, dairy stick, and chocolate bar lines running multiple flavors per shift, while pharmaceuticals, supported by serialization enforcement, are projected to grow at 9.12% CAGR through 2030, increasing their share of the end load cartoning machine market. Cosmetics and personal care lines leverage vertical infeed and window-cut cartons to lift shelf appeal.

Food processors require wash-down frames and stainless guards, pressing vendors to offer IP65 options. Pharma builders must validate GMP documentation and ensure CFR Part 11 data integrity. These divergent needs spur platform modularity so OEMs can swap clean-room kits onto food chassis. Consequently, specialization deepens vendor moats and keeps margins healthy across the End load cartoning machine market.

By Automation Level: Fully Automatic Dominates as Robotics Rises

Fully automatic lines delivered 58.43% of 2024 revenue, confirming plant managers’ bias toward lights-out operation. Robotic-integrated variants are advancing at 8.32% CAGR, supported by cobots that slip into tight footprints and repurpose quickly for new SKUs. Semi-automatic solutions remain for niche craft brands that capex-constrain, yet their share will inch downward.

Cobot case stackers like FANUC’s CRX-25iA, with 30 kg payload, extend lights-out zones in existing halls without cages. Remote-service packages bundle uptime SLAs, enticing risk-averse buyers. Simpler quick-teach pendant modes cut programmer dependency, moderating the skills gap. These factors enlarge the End load cartoning machine market and sustain a path for tiered automation adoption.

Geography Analysis

North America contributed 38.54% of global revenue in 2024, anchored by stringent serialization rules and high labor costs that justify automation. U.S. equipment shipments rose 5.8% to USD 10.9 billion, with cartoners a key beneficiary of demand for tamper-evident secondary packs. Canada’s dairy processors adopted rapid-changeover horizontals to cut SKU lead times. Mexico’s near-shoring trend pulls investment into snack packaging, widening the installed base. Robust aftermarket service contracts further grow the end load cartoning machine market in North America.

Asia-Pacific is the fastest-growing arena at 9.89% CAGR. India’s packaging sector is on course to reach USD 204.81 billion by 2025, giving multinational converters an incentive to expand folding-carton plants. Chinese OEMs push cost-competitive frames, spurring technology uptake in tier-2 cities. Japan’s food machinery builders like Ishida promote paperboard multipacks, syncing with local plastic-reduction drives. ASEAN e-commerce hubs demand return-ready carton designs, inflating unit volumes. Collectively, these forces push the End load cartoning machine market to new highs across the Asia-Pacific.

Europe remains a steady yet innovation-rich hub. Circular-economy legislation accelerates fiber-based packaging adoption, and OEMs in Germany and Italy exploit proximity to automotive and pharma customers. Syntegon invested EUR 54 million in R&D and filed 2,100 patents in 2024, underscoring a technology arms race. The region’s mature plants now retrofit predictive maintenance modules rather than buy new frames, creating a service-heavy revenue mix. All regions combined elevate the End load cartoning machine market toward the 2030 forecast.

Competitive Landscape

The End load cartoning machine market is moderately fragmented. European specialists such as Syntegon, IMA, and Marchesini deliver high-end GMP systems, while U.S. houses like Barry-Wehmiller and ProMach bolt on niche acquisitions to fill portfolio gaps. Asian challengers compete on cost and localized after-sales presence. Technology advantage revolves around servo motion, AI-enabled quality control, and cloud-based predictive service. Syntegon booked EUR 1.8 billion in orders and EUR 1.6 billion in revenue for 2024, signaling robust demand in pharma.

Consolidation picked up when ProMach closed four deals in 2024, including HMC Products, deepening its horizontal form-fill-seal and end-load expertise. Krones posted 12.1% revenue growth to EUR 5.29 billion in 2024 and targets another 7-9% climb for 2025, although cartoners are only a slice of its broad portfolio. IMA acquired Sarong’s machinery division to assemble blister-to-carton lines under one roof, strengthening integrated-line sales.

Vendors court strategic partnerships: Syntegon collaborates with machine-vision firms, while BW Packaging co-develops line analytics with software startups. Intellectual property barriers around serialization software and clean-room validation keep new entrants at bay. As top suppliers occupy roughly half of global revenue, competition remains brisk yet disciplined, underpinning a mid-range profit profile across the End load cartoning machine market.

End Load Cartoning Machine Industry Leaders

Syntegon Technology GmbH

Marchesini Group S.p.A.

Coesia S.p.A.

Körber AG (Medipak Systems)

IMA Industria Macchine Automatiche S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: BW Packaging unveiled an upgraded Thiele UltraStar G2 bag filler at PACK EXPO International.

- October 2024: ProMach acquired HMC Products, its fourth deal of 2024

- August 2024: IMA bought Sarong’s machinery and materials units to expand pharma lines.

- June 2024: Leonard Green and BDT Capital closed a new ownership agreement with ProMach

Global End Load Cartoning Machine Market Report Scope

| Horizontal End-Load Cartoning Machines |

| Vertical End-Load Cartoning Machines |

| Up to 150 Cartons Per Minute (CPM) |

| 151 - 400 CPM |

| Above 400 CPM |

| Food and Beverage | Bakery and Confectionery |

| Dairy Products | |

| Ready Meals | |

| Other Food and Beverages | |

| Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Household Goods | |

| Other End-use Industries |

| Semi-automatic Machines |

| Fully Automatic Machines |

| Robotic-Integrated Lines |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Orientation | Horizontal End-Load Cartoning Machines | ||

| Vertical End-Load Cartoning Machines | |||

| By Speed Class | Up to 150 Cartons Per Minute (CPM) | ||

| 151 - 400 CPM | |||

| Above 400 CPM | |||

| By End-use Industry | Food and Beverage | Bakery and Confectionery | |

| Dairy Products | |||

| Ready Meals | |||

| Other Food and Beverages | |||

| Pharmaceuticals | |||

| Personal Care and Cosmetics | |||

| Household Goods | |||

| Other End-use Industries | |||

| By Automation Level | Semi-automatic Machines | ||

| Fully Automatic Machines | |||

| Robotic-Integrated Lines | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Netherlands | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current value of the End load cartoning machine market?

The market is valued at USD 2.91 billion in 2025 and is set to reach USD 3.91 billion by 2030.

Which region grows fastest for end-load cartoners?

Asia-Pacific records the highest growth with a 9.89% CAGR thanks to manufacturing upgrades and e-commerce expansion.

Which speed class attracts most buyers?

Machines running 151–400 CPM hold 49.42% of shipments and deliver 8.21% CAGR, balancing throughput with flexibility.

How do serialization rules influence equipment demand?

U.S. and EU mandates require unique codes on every pharma carton, pushing plants to purchase cartoners with integrated vision and printing modules.

What restrains adoption among small producers?

High upfront costs and a shortage of skilled mechatronics operators slow investment, though modular and leasing models ease the burden.

Which sustainability trend affects machine specifications most?

The shift from plastic to paperboard drives demand for feeders and glue systems that handle recycled fiber while maintaining carton integrity.

Page last updated on: