Email Security Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

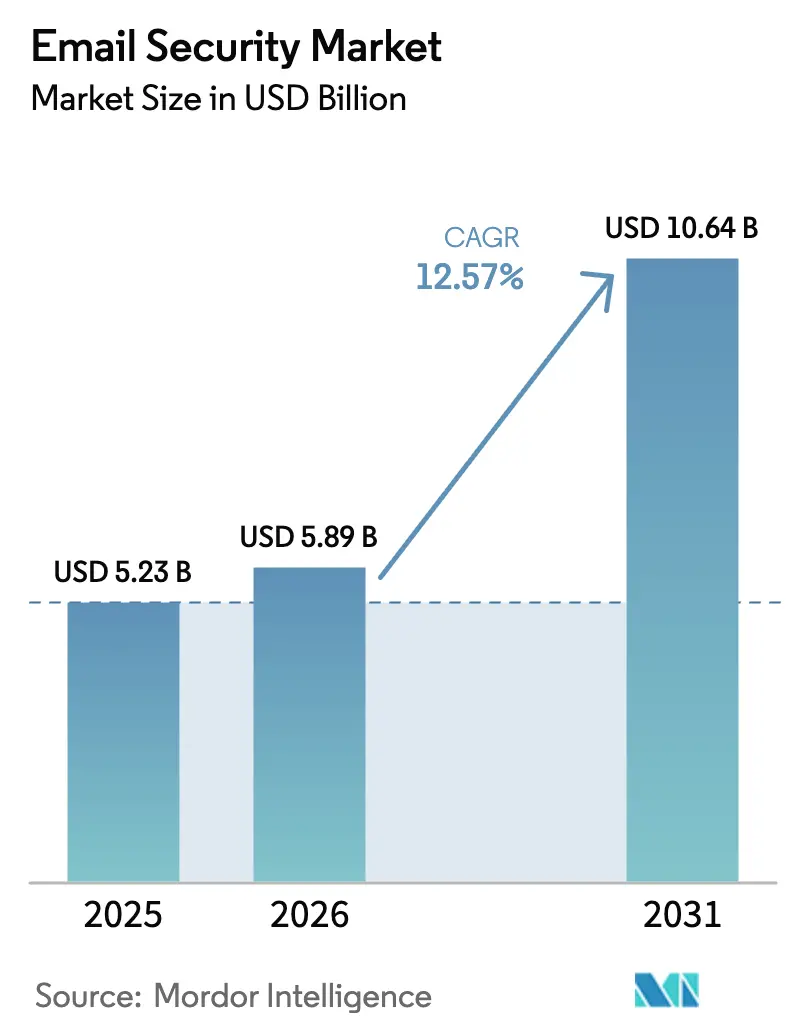

| Market Size (2026) | USD 5.89 Billion |

| Market Size (2031) | USD 10.64 Billion |

| Growth Rate (2026 - 2031) | 12.57% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Email Security Market Analysis by Mordor Intelligence

Email security market size in 2026 is estimated at USD 5.89 billion, growing from 2025 value of USD 5.23 billion with 2031 projections showing USD 10.64 billion, growing at 12.57% CAGR over 2026-2031. Demand rises as phishing, business-email-compromise (BEC) and ransomware campaigns become more sophisticated, forcing organizations to replace perimeter tools with API-level protection. Expansion is further accelerated by data-protection mandates such as the EU’s NIS2 Directive, rapid migration to Microsoft 365 and Google Workspace, and the embedding of AI models that improve detection accuracy while reducing false-positive noise. Vendor consolidation—illustrated by Cisco’s USD 28 billion purchase of Splunk—signals a pivot toward platform strategies that fuse email, endpoint and SIEM telemetry for faster response. At the same time, small and medium enterprises (SMEs) are closing adoption gaps because cloud delivery removes infrastructure complexity and makes enterprise-grade controls affordable.

Key Report Takeaways

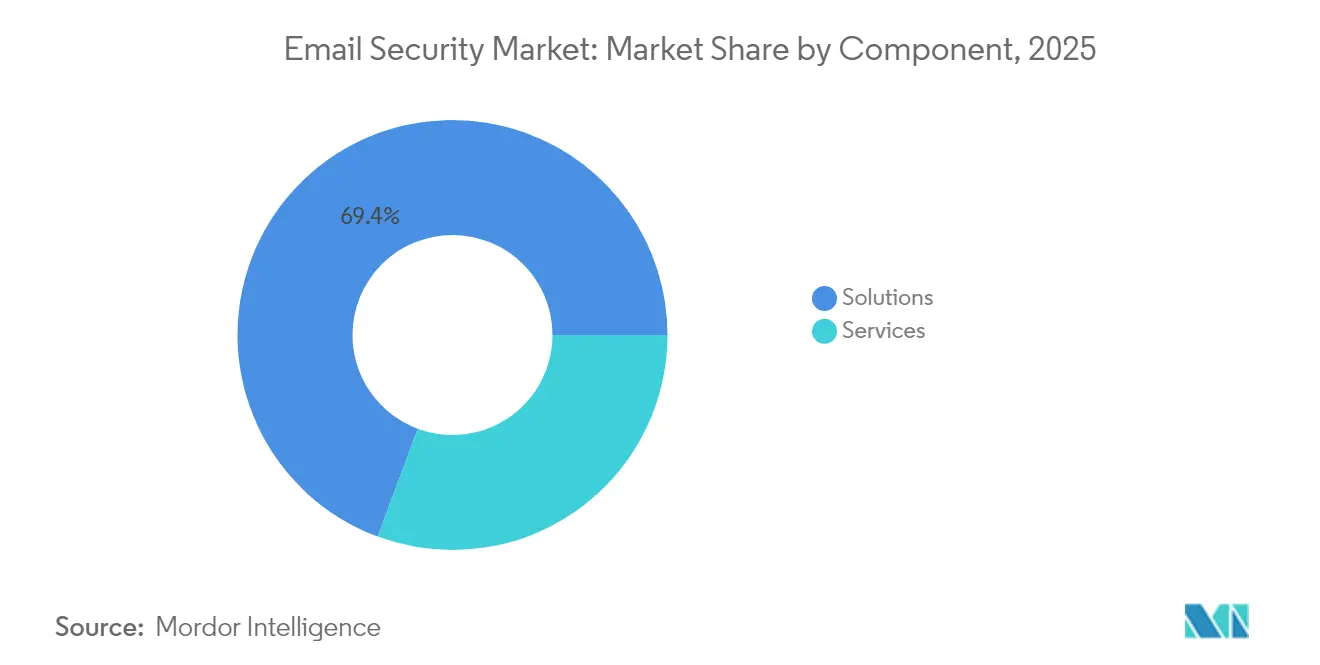

- By component, Solutions held 69.35% revenue share in 2025, whereas services are projected to expand at a 15.02% CAGR to 2031 as firms outsource security operations.

- By deployment mode, Cloud deployment captured 59.10% of the email security market share in 2025 and is advancing at a 16.95% CAGR through 2031.

- By enterprise size, Large enterprises held 60.55% revenue share in 2025, while SMEs exhibit the fastest 18.05% CAGR.

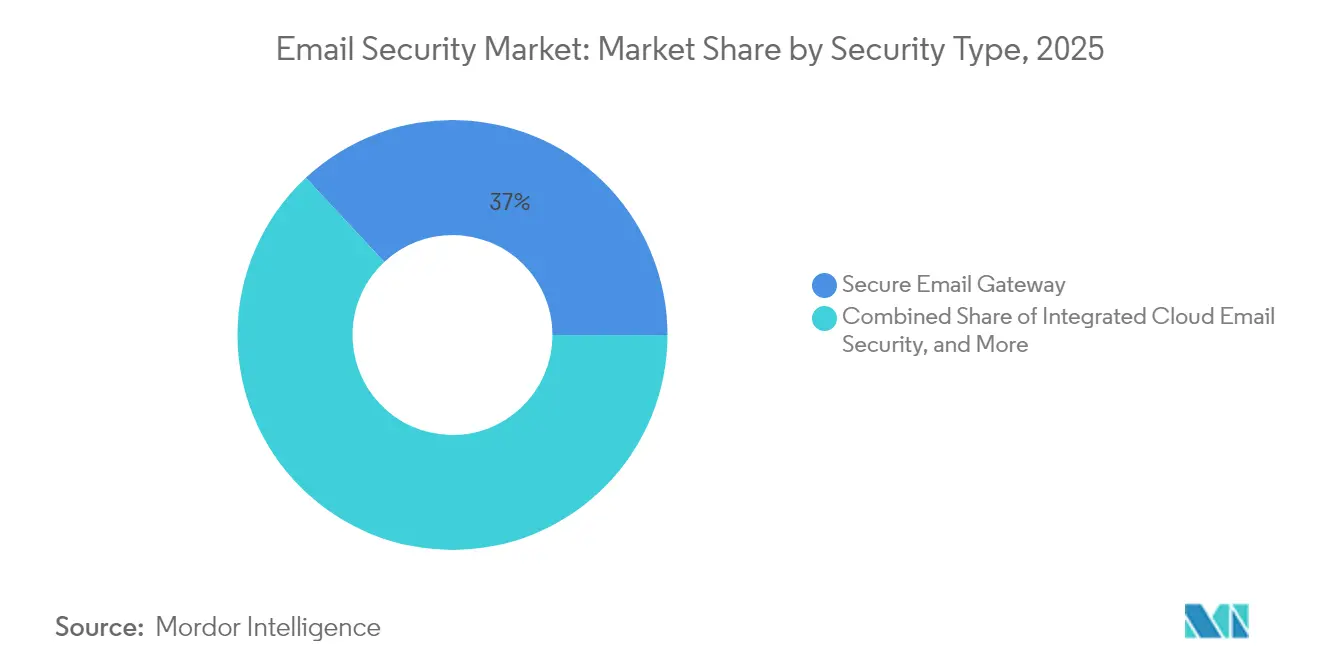

- By security type, Secure Email Gateways retained 36.95% share of the email security market size in 2025, but Integrated Cloud Email Security (ICES) is expanding at a 21.25% CAGR.

- By end-user industry, Healthcare is the fastest-growing vertical at a 16.62% CAGR through 2031, whereas BFSI remained the largest with 27.35% share in 2025.

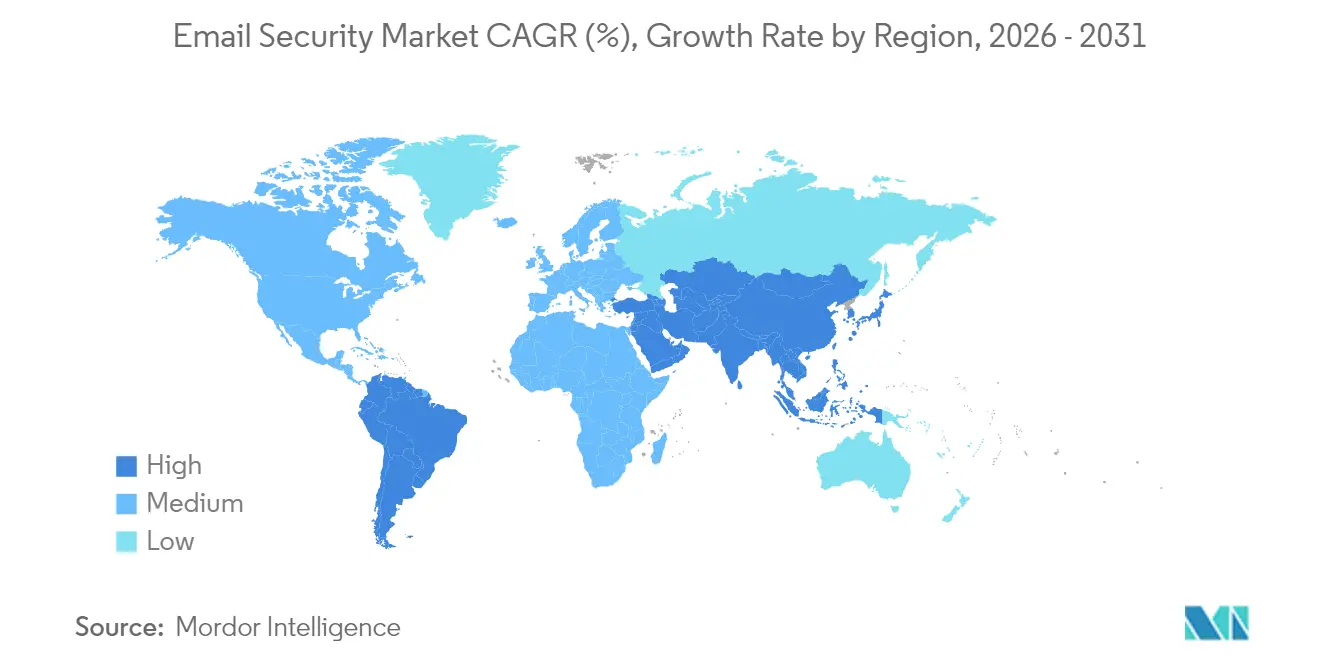

- By geography, North America led with 41.05% revenue in 2025; Asia-Pacific is forecast to post a 14.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Email Security Market Trends and Insights

Driver Impact Analyis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising phishing and BEC incidents | +3.2% | Global; highest in North America and Europe | Short term (≤ 2 years) |

| Shift to cloud email and remote work | +2.8% | Global; led by North America and Asia-Pacific | Medium term (2-4 years) |

| Stringent data-protection regulations | +2.1% | Europe and North America; expanding to Asia-Pacific | Long term (≥ 4 years) |

| AI/ML-driven threat detection | +1.9% | North America and Europe; Asia-Pacific adoption accelerating | Medium term (2-4 years) |

| OT-sector shift to zero-trust email | +1.4% | Global; critical-infrastructure regions | Long term (≥ 4 years) |

| Ecosystem consolidation and API add-ons | +1.2% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising phishing and BEC incidents

Global BEC losses climbed as the average attack cost hit USD 35,000 in 2024, pushing email security from a compliance check to a business-continuity requirement [1]Splunk Inc., “State of Security 2025,” splunk.com. Attackers now blend social-engineering, deepfakes and reply-chain hijacks that evade rule-based gateways, so enterprises are shifting budgets toward ICES platforms that analyze user behavior, language patterns and conversation context in real time. These capabilities shorten mean-time-to-detect and support automated remediation, which is essential when organizations face 1,636 attempted cyberattacks per week. Adoption is most vigorous in regulated industries—finance, healthcare, critical utilities—where BEC campaigns are weaponizing trusted supplier relationships to bypass perimeter defenses.

Shift to cloud email and remote work

With 94% of Asia-Pacific SMEs embracing cloud SaaS and Microsoft’s security business surpassing USD 20 billion annual revenue, perimeter appliances cannot cover distributed teams or collaboration-suite traffic. Organizations therefore prefer API-level controls that plug directly into Microsoft 365, Google Workspace and Slack, enabling full inspection of inbound, outbound and intra-suite messages. Adoption further accelerates because cloud licensing costs scale predictably, and updates to machine-learning models roll out instantly without change-window downtime. SMEs benefit disproportionately because they avoid capital expenditure and specialist staffing, driving the double-digit growth logged in managed security services.

Stringent data-protection regulations

The EU’s NIS2 Directive now covers roughly 30,000 German entities versus 2,000 under NIS1, requiring encryption via S/MIME or OpenPGP, incident reporting within 24 hours and board-level accountability. Parallel rules in the United States Treasury and upcoming UK Cyber Resilience Bill expand disclosure obligations, so buyers select platforms that automate compliance templates and maintain evidentiary audit trails. Vendors offering regional data-residency, client-side key management and tamper-proof archiving gain a defensible edge, particularly among multinational healthcare and finance customers that must juggle HIPAA, GDPR and PCI-DSS.

AI/ML-driven threat detection

Microsoft’s Language AI for Phish Models can parse sentiment and linguistic anomalies, boosting detection of novel lures that lack known indicators. Check Point, meanwhile, achieved 100% phishing prevention and 99.8% new-malware blocking in independent tests, validating the payoff from deep-learning engines that enrich billions of daily signals. Vendors differentiate on model transparency and low false-positive rates because security teams drown if every marketing newsletter is flagged. As AI gains contextual awareness—linking mailbox, endpoint, and identity telemetry—response can shift from block-and-quarantine to guided user coaching and automatic isolation of risky assets.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High implementation and maintenance cost | -2.1% | Global; strongest in price-sensitive SMEs | Short term (≤ 2 years) |

| Skills shortage and expertise gap | -1.7% | Global; acute in emerging markets | Medium term (2-4 years) |

| Free/open-source alternatives | -1.3% | Asia-Pacific and emerging economies | Medium term (2-4 years) |

| Bundled basic security in cloud suites | -1.0% | Global; most pronounced among Microsoft 365 tenants | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High implementation and maintenance cost

Total cost of ownership often triples license expenditure once integration, SOC headcount and 24×7 monitoring are factored in, a pain point when two-thirds of SMEs already spend 4% of annual revenue on cybersecurity. Boards demand quantifiable ROI, so vendors that embed automation and managed-service tiers mitigate sticker shock. Nevertheless, organizations postponing upgrades extend refresh cycles, slowing overall email security market growth in price-sensitive regions.

Free/open-source alternatives

Postfix, SpamAssassin and Microsoft’s built-in Exchange Online Protection set a “good-enough” baseline, especially for smaller firms. Yet these tools lag in language-aware BEC detection, adaptive DLP and granular compliance analytics. Vendors must therefore articulate value beyond spam filtering, demonstrating how AI models catch polymorphic malware or how automated encryption satisfies industry mandates. Pricing pressure persists, but rising threat complexity gradually erodes the free-tool ceiling.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Growth Outpaces Solutions

Solutions commanded 69.35% revenue in 2025, yet managed services are climbing at a 15.02% CAGR as firms outsource threat hunting, playbook tuning and compliance audits CRN. The email security market size for services is therefore set to expand faster than software, reflecting buyers’ need for 24×7 coverage and outcome-based contracts. Proofpoint’s USD 1 billion purchase of Hornetsecurity underscores the pivot toward MSP enablement, providing white-label SOC capabilities that MSPs can resell to SME clients. In parallel, professional services for deployment remain relevant, but their share shrinks because cloud APIs trim integration times from weeks to hours. Vendors with global service footprints and multilingual SOCs win long-term renewals because clients value consistent SLAs across regions.

Enterprises that keep operations in-house still lean on vendor premium support for model tuning, policy design and red-team simulations. Those engagements generate telemetry that feeds machine-learning feedback loops, reinforcing product stickiness. Services portfolios also expand into security-awareness training, phishing simulations and incident-response retainers. As a result, services catalyze cross-sell of adjacent platform modules such as CASB and XDR, positioning providers to capture wallet share as regulations tighten.

By Deployment Mode: Cloud Dominance Accelerates

Cloud-hosted controls captured 59.10% share in 2025 and will outgrow on-premises appliances at a 16.95% CAGR, making the cloud segment the largest contributor to future email security market size. Customers cite elastic scaling, instant rule updates and native integration with Microsoft Graph APIs as decisive benefits. Further momentum stems from government pushes to adopt “cloud-first” procurement policies that require SaaS justifications before approving capital budgets.

Conversely, latency-sensitive industries such as financial trading and defense keep segmented mailflow on private appliances to satisfy deterministic delivery requirements and air-gap constraints. Hybrid architectures therefore persist: inbound scanning remains cloud-based, while outbound policy enforcement or encryption keys stay on-premises. Appliance refreshes increasingly include containerized micro-services so organizations can redeploy functions to Kubernetes clusters when sovereignty rules evolve.

By Enterprise Size: SME Adoption Accelerates

Large enterprises still generate 60.55% of 2025 revenue, but SMEs are expanding at 18.05% CAGR, narrowing the gap each year. More than half of Asia-Pacific SMEs reported a cyber incident in 2024, prompting boards to re-evaluate “good-enough” spam filters. Cloud subscription models priced per active mailbox remove upfront hardware costs, while pay-as-you-grow tiers let firms add sandboxing and DMARC analytics once budget permits.

Meanwhile, Fortune 500 groups are consolidating parallel toolsets after mergers, seeking unified console visibility across business units. Their rationale emphasizes analyst efficiency rather than raw blocking accuracy, so vendors highlight case-management and SOAR integrations. Owing to longer procurement cycles, enterprise renewal waves produce lumpy revenue but high lifetime value. Solution roadmaps that align with NIST 800-207 zero-trust mailflow garner traction because CIOs want controls mapped to federated identity frameworks.

By Security Type: ICES Disrupts Traditional SEG Market

Secure Email Gateways still held 36.95% share in 2025; however, ICES recorded a 21.25% CAGR that will tilt the balance by 2027. Analysts predict that the email security market share for API-based ICES could overtake legacy proxies as soon as 2028. SEG appliances struggle to inspect TLS-encrypted traffic without breaking sessions, whereas ICES tools ingest mailbox telemetry post-delivery, enabling retrospective detonation and conversation-thread rollback.

Encryption, archiving and DLP sub-segments continue steady single-digit growth driven by HIPAA, PCI-DSS and MiFID II retention rules. Spam filtering has become commoditized—often bundled into suites—pushing standalone providers to reposition around AI enrichment layers. Vendors differentiate by mapping MITRE ATTandCK tactics for email, offering phishing risk scoring at user level, and feeding those scores into conditional-access policies that quarantine compromised accounts.

By End-user Industry: Healthcare Drives Compliance-Led Growth

Healthcare’s 16.62% CAGR stems from proposed HIPAA updates that finally require encryption of protected health information and mandate MFA on all user accounts. Hospitals and insurers adopt ICES coupled with automated encryption gateways to satisfy data-at-rest and in-transit requirements. They also use role-based message classification so caregivers can share lab results securely without over-encrypting mundane traffic.

BFSI retains 27.35% revenue share due to high-value wire-fraud risk, but growth moderates because most banks completed SEG rollouts years ago. Manufacturing, energy, and utilities see rising adoption as operational-technology teams extend zero-trust principles to plant-floor mailboxes that were previously isolated. Government and defense agencies specify Common Criteria-certified solutions or FedRAMP Moderate SaaS to meet clearance thresholds, creating barriers to entry for new entrants without accreditation.

Geography Analysis

North America generated 41.05% of global revenue in 2025, propelled by the region’s USD 92.31 billion cybersecurity spend forecast for 2025 and an average 1,636 weekly attack attempts that keep email risk front-of-mind. United States buyers lead consumption of AI-native ICES products, helped by abundant security budgets and an advanced threat landscape targeting critical infrastructure. Canadian enterprises increasingly mirror US compliance frameworks, adopting NIST core controls and selecting SaaS providers that guarantee local data residency in Toronto or Montreal.

Asia-Pacific is the fastest-expanding geography at a 14.28% CAGR. SMEs across India, Vietnam and Indonesia leapfrog legacy gateways, moving straight to cloud email security market offerings because 94% already rely on SaaS productivity suites. Japanese and South Korean conglomerates adopt AI-driven language models fine-tuned for local scripts, while Australian public-sector agencies enforce Essential Eight maturity levels that prioritize email authentication and content disarm. China’s market evolves within a parallel technology stack shaped by domestic encryption standards and cross-border data-transfer limits, creating demand for ICES products that support commercial versions of S/MIME and SM2 algorithms.

Europe posts steady mid-single-digit growth, with compliance acting as the prime catalyst. NIS2 extends obligations to small municipal utilities and mid-sized manufacturers, pushing thousands of firms to implement email encryption and incident-reporting automation . Germany leads adoption thanks to well-established BSI guidance, while France prioritizes SecNumCloud-qualified SaaS for sovereign workloads. Post-Brexit, the United Kingdom pursues its Cyber Resilience Bill, aligning closely with EU rules but adding stress-test requirements that encourage scenario-based phishing simulations.

Competitive Landscape

Competition is moderately concentrated: top-tier vendors such as Microsoft, Cisco and Proofpoint face challengers like Abnormal Security, Darktrace and SlashNext that position around AI specificity instead of breadth. Consolidation intensified in 2024-2025. Proofpoint acquired Hornetsecurity for USD 1 billion to deepen MSP channels, while Cisco closed its USD 28 billion deal for Splunk to synthesize mail, endpoint and SIEM analytics. These moves signal customer appetite for integrated security fabric rather than piecemeal controls.

Strategic roadmaps converge on three pillars. First is AI-native detection: Microsoft injected Copilot for Security across Defender workloads, using large language models to summarize incidents and generate remediation steps automatically. Second is cloud-first delivery: Google enhanced Workspace with client-side encryption keys hosted in customer-chosen regions, satisfying sovereignty mandates without third-party gateways. Third is managed-service packaging: vendors now bundle 24×7 SOC, attack-surface management and phishing-resilience training in tiered subscriptions, targeting resource-constrained SMEs.

Barriers to entry include access to large labeled email datasets, the need for SOC integration hooks, and accreditation such as FedRAMP, ISO 27001 and SOC 2 Type II. Start-ups tackle niche gaps—QR-code phishing, voice-mail lures, business-process compromise—but often partner with incumbents for distribution. Meanwhile, legacy SEG vendors retrofit API connectors to retain installed bases, yet must overcome performance trade-offs linked to proxy architectures. As platform unification progresses, differentiation shifts toward contextual insight, user coaching and risk-based authentication.

Email Security Industry Leaders

Cisco Systems, Inc.

Barracuda Networks, Inc.

Proofpoint, Inc.

Mimecast Limited

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Microsoft introduced Language AI for Phish Model in Defender for Office 365, advancing linguistic anomaly detection.

- April 2025: Abnormal AI launched AI Phishing Coach and AI Data Analyst to automate user training and reporting.

- December 2024: US HHS proposed HIPAA Security Rule updates mandating email encryption and MFA.

- November 2024: ENISA released NIS2 implementation guidance detailing email-encryption measures.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the email security market as all software and managed services that actively prevent, detect, and remediate threats aimed at business email, including phishing, business-email-compromise (BEC), malware, spam, spoofing, and unauthorized data exfiltration, across cloud and on-premise mail platforms worldwide.

Scope exclusion: consumer-grade antispam plug-ins and standalone email marketing hygiene tools are not counted.

Segmentation Overview

- By Component

- Solutions

- Services

- By Deployment Mode

- Cloud

- On-Premises

- By Enterprise Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By Security Type

- Secure Email Gateway

- Integrated Cloud Email Security (ICES/API)

- Email Encryption

- Email Archiving and Compliance

- Spam and Malware Filtering

- By End-user Industry

- BFSI

- IT and Telecom

- Government and Defense

- Retail and E-commerce

- Manufacturing

- Energy and Utilities

- Healthcare

- Other Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- UAE

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed CISOs, managed-security-service leaders, mail-platform product managers, and regional channel partners across North America, Europe, Asia-Pacific, and the Gulf to test assumptions on mailbox growth, per-user spend, and migration pacing. Follow-up surveys with small-enterprise IT heads helped fine-tune SMB penetration rates.

Desk Research

Mordor analysts first mapped the threat landscape with open datasets such as ENISA threat reports, Verizon DBIR, NIST NVD vulnerability feeds, and regional CERT advisories. They then overlaid adoption indicators from Eurostat ICT surveys and OECD cloud-use statistics. Company 10-Ks, SEC filings, and infosec vendor price lists supplied baseline revenue and average-selling-price cues, aided by D&B Hoovers and Dow Jones Factiva snapshots. Trade bodies, such as the Messaging Malware Mobile Anti-Abuse Working Group (M3AAWG) and the Cloud Security Alliance, provided installed-base signals. The sources above illustrate, not exhaust, the wider pool referenced for validation.

Market-Sizing & Forecasting

A top-down model starts with active business mailboxes by region, multiplies them by average security spend (split by cloud and on-premise), and is cross-checked through supplier roll-ups from sampled vendor revenues. Key variables include phishing incident volume, Microsoft 365/Google Workspace penetration, secure-email-gateway price erosion, regulatory fine benchmarks, and API-based protection uptake. Multivariate regression ties these drivers to value growth; bottom-up checks plug remaining data gaps, capping variance at ±5%. Scenario analysis addresses macro-slowdown or regulation-led spikes.

Data Validation & Update Cycle

Outputs pass three-layer peer review, anomaly scans against external threat metrics, and leadership sign-off. We refresh the model yearly and trigger interim updates when material vendor M&A, zero-day waves, or regulatory mandates shift baselines. A last-mile analyst sweep ensures clients receive the latest view.

Why Mordor's Email Security Baseline Commands Reliability

Published figures often diverge because firms pick different product mixes, mailbox counts, and price curves.

Key gap drivers include widened scopes that fold in broader messaging security, reliance on vendor revenue tallies without threat-led demand checks, or static refresh cadences that miss fast-moving exploit patterns.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.23 B (2025) | Mordor Intelligence | - |

| USD 5.17 B (2025) | Global Consultancy A | Omits encryption services; narrow primary outreach; annual refresh only |

| USD 7.39 B (2025) | Trade Journal B | Bundles messaging security add-ons; uses uniform ASP across regions |

| USD 18.5 B (2024) | Industry Tracker C | Counts consumer tools and gateway hardware; limited primary verification |

These contrasts show that, by selecting a threat-aligned scope, blending mailbox demand curves with validated price dispersion, and updating after every major attack cycle, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can retrace with confidence.

Key Questions Answered in the Report

How big is the Email Security Market?

The Email Security Market size is expected to reach USD 5.89 billion in 2026 and grow at a CAGR of 12.57% to reach USD 10.64 billion by 2031.

What is the global email security market size in 2026?

The market is valued at USD 5.89 billion in 2026.

What compound annual growth rate is forecast for the email security market between 2026 and 2031?

It is expected to expand at a 12.57% CAGR through 2031.

Which region is projected to grow the fastest in email security spending?

Asia-Pacific is forecast to lead with a 14.28% CAGR through 2031.

Which security type is expanding the quickest?

Integrated Cloud Email Security solutions are advancing at a 21.25% CAGR, outpacing Secure Email Gateways.

How will regulations such as the EU NIS2 Directive influence purchasing decisions?

Mandates for encryption, incident reporting and board accountability compel thousands of European firms to adopt enterprise-grade email security platforms that automate compliance.

Page last updated on: