Email Archiving Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 9.38 Billion |

| Market Size (2031) | USD 20.66 Billion |

| Growth Rate (2026 - 2031) | 17.12% CAGR |

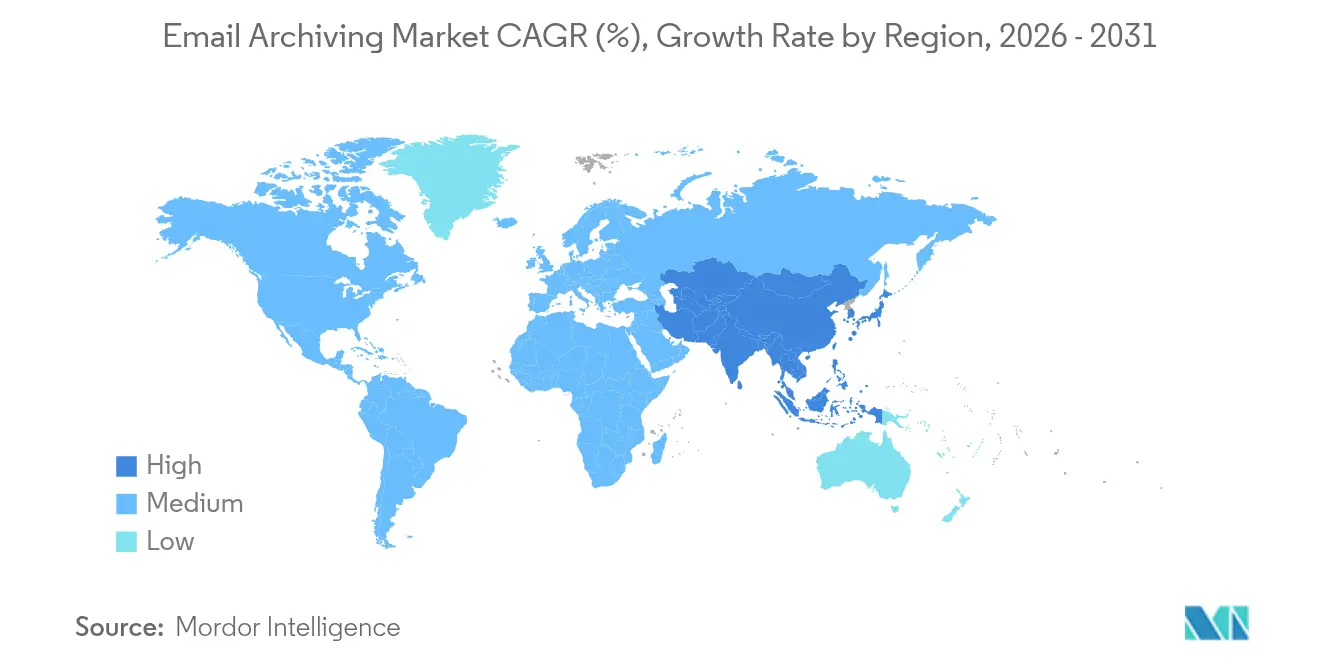

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

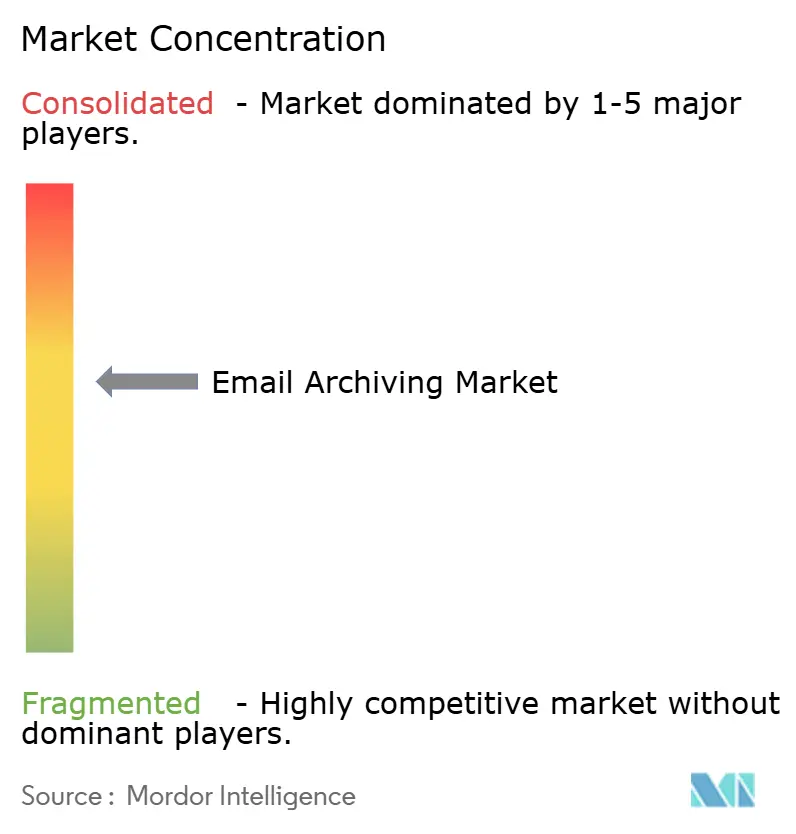

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Email Archiving Market Analysis by Mordor Intelligence

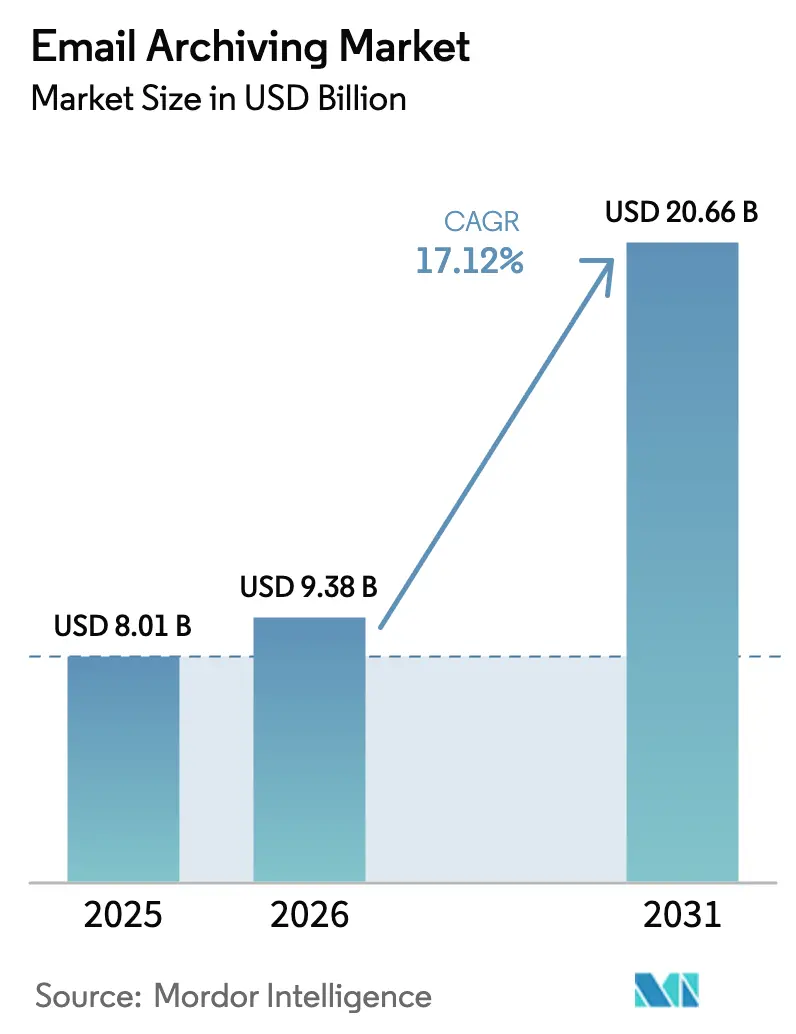

The email archiving market size is expected to grow from USD 8.01 billion in 2025 to USD 9.38 billion in 2026 and is forecast to reach USD 20.66 billion by 2031 at 17.12% CAGR over 2026-2031. Intensifying regulatory scrutiny, escalating ransomware exposure, and widespread migration to cloud-based productivity suites are combining to accelerate demand. The market’s momentum is strongest in highly regulated verticals where non-compliance now entails operational limits and reputational damage in addition to fines. Cloud-first deployment models are outpacing on-premises roll-outs as enterprises seek scalability and immutable storage, while rising Microsoft 365 penetration is prompting third-party archiving adoption to address eDiscovery and sovereignty gaps. Regionally, North America benefits from long-standing rules such as SEC 17a-4 and FINRA 4511, whereas digitization programs and new data-privacy regimes power Asia’s high-growth trajectory. Vendors are repositioning archives from passive compliance repositories to active governance platforms that deliver analytics, risk insights, and cyber-resilience capabilities.

Key Report Takeaways

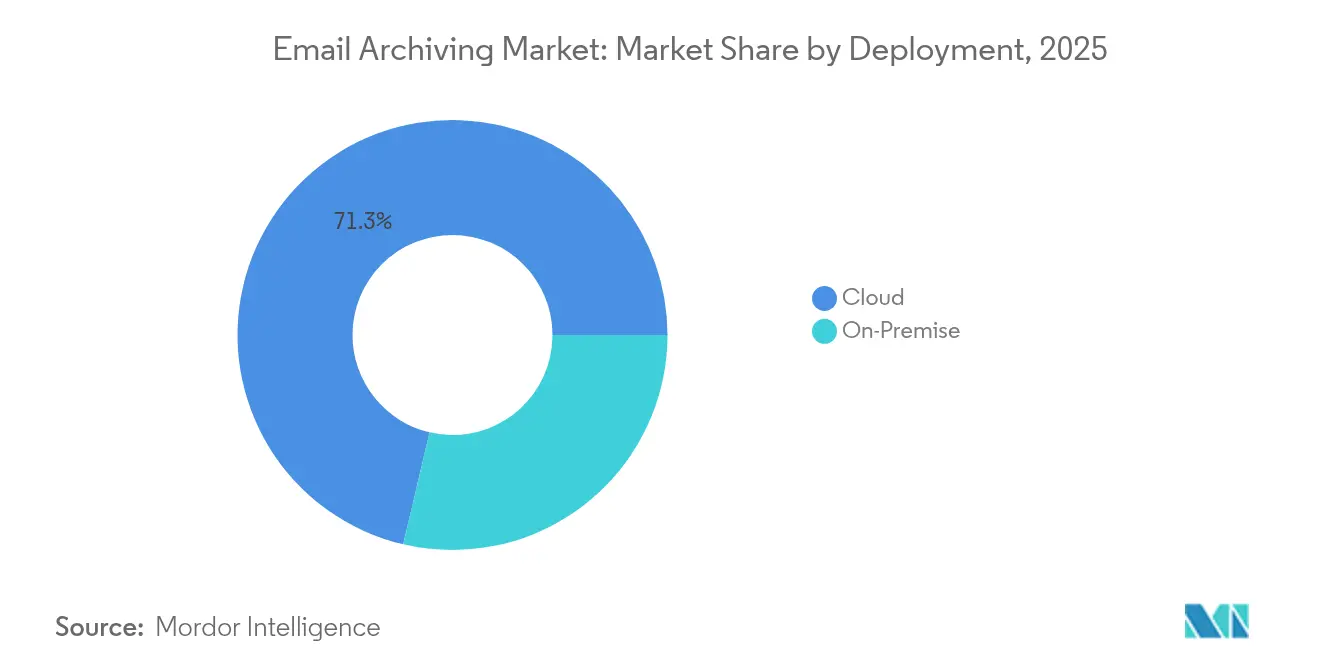

- By deployment, cloud deployment led with 71.32% revenue share in 2025; on-premises is projected to grow at a lower 8.12% CAGR through 2031 while cloud advances at 17.65%.

- By content type, email content accounted for 68.25% of the 2025 email archiving market share, whereas social media & collaboration content is set to expand at 17.74% CAGR to 2031.

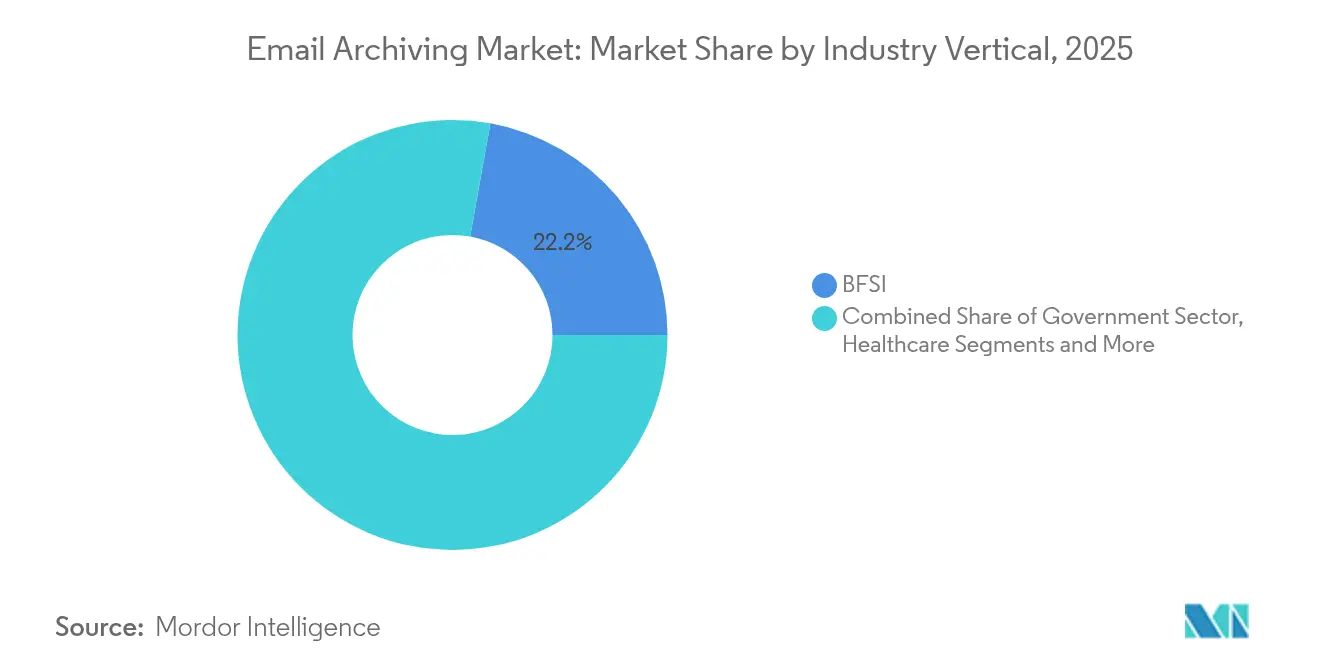

- By industry vertical, BFSI commanded 22.18% share of the email archiving market size in 2025; healthcare & life sciences is forecast to grow at 17.95% CAGR over 2026-2031.

- By organization size, large enterprises held 66.20% revenue share in 2025; SMEs represent the fastest-growing segment at 18.55% CAGR through 2031.

- By service type, software holds the largest share of 64.40% in 2025, in which core archiving platforms remain the revenue engine, with an 17.55% CAGR through 2031.

- By geography, North America captured 39.85% share in 2025; Asia is expected to post the highest regional CAGR of 18.12% during the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Email Archiving Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extra-territorial Data-Privacy Laws Driving Global Retention Mandates | +4.2% | Global, with pronounced effects in EU, North America, and APAC | Medium term (2-4 years) |

| SEC 17a-4(f) & FINRA 4511 Rules Fueling WORM Cloud Storage in US BFSI | +3.5% | North America, with spillover effects in global financial hubs | Short term (≤ 2 years) |

| Rapid Microsoft 365 Adoption Boosting Third-Party Archives in Europe | +3.8% | Europe, North America | Medium term (2-4 years) |

| Ransomware Surge Accelerating Immutable Email Back-ups in North America | +4.1% | North America, Europe, with growing impact in APAC | Short term (≤ 2 years) |

| AI-Powered e-Discovery Demand in APAC Legal Systems | +3.6% | APAC, with focus on developed markets (Japan, Australia, Singapore) | Medium term (2-4 years) |

| Sovereign-Cloud Programs in GCC Nations Requiring In-region Archives | +2.8% | Middle East, particularly GCC countries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Extra-territorial data-privacy laws driving global retention mandates

Data-sovereignty statutes are forcing multinational firms to replace centralized archives with regionally distributed architectures that respect local residency rules. By late 2024, 62 countries had enacted 144 localization restrictions, prompting compliance teams to deploy geo-fencing and automated policy engines that enforce jurisdiction-specific retention schedules.[1]Nick Law, “Data sovereignty: Is it time to rethink your cloud strategy? (Part 1),” Atos, atos.net Organizations that integrate these controls into cloud archives gain faster audit readiness and avoid costly data-transfer remediation.

SEC 17a-4(f) and FINRA 4511 rules fuelling WORM-grade cloud storage in US BFSI

The 2023 amendments permitting electronic recordkeeping systems with immutable audit trails have accelerated cloud migrations among broker-dealers. Archiving vendors now issue SEC attestation letters and appear in the FINRA compliance directory, positioning their platforms as lower-risk alternatives to aging on-premises appliances.[2]FINRA staff, “Books and Records,” FINRA, finra.orgCloud-native archives simultaneously support fraud analytics and litigation response, reinforcing their strategic value to financial institutions.

Rapid Microsoft 365 adoption boosting third-party archives in Europe

Enterprises moving to Microsoft 365 often discover limitations in native retention, prompting demand for specialist platforms that handle MiFID II, GDPR, and multi-channel capture. Legal uncertainty surrounding EU-US transfers, highlighted by the continuing Schrems II fallout and challenges to the Data-Privacy Framework, further incentivizes firms to deploy archives that allow granular control over residency zones.

Ransomware surge accelerating immutable email backups in North America

With 65% of financial services firms hit by ransomware in 2024 and average recovery costs at USD 2.58 million, immutable archives have become a frontline cyber-resilience measure. Organizations are adopting 3-2-1-1 backup architectures and isolated recovery environments, ensuring email restoration without ransom payments and shortening incident recovery windows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy PST Migration Complexity in Tier-1 Banks | -1.8% | Global, with higher impact in mature markets with established financial institutions | Medium term (2-4 years) |

| EU Schrems II Data-Sovereignty Barriers | -2.2% | EU, with global impact for multinational organizations | Medium term (2-4 years) |

| Hidden Hyperscaler Egress/API Costs for SMEs | -1.6% | Global, with pronounced effect on price-sensitive markets | Short term (≤ 2 years) |

| Overlap with Native M365/G-Work Retention Features | -1.9% | Global, higher impact in regions with high cloud adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Legacy PST migration complexity in tier-1 banks

Decades of unmanaged PST files raise corruption, security, and compliance risks. Password-protected archives and wide dispersion across user devices inflate project timelines, prompting demand for specialist migration services and toolsets that preserve chain of custody.

EU Schrems II data-sovereignty barriers

Pending legal challenges to the EU-US Data-Privacy Framework are compelling enterprises to deploy regional instances or adopt advanced encryption and contractual safeguards, adding cost and architectural complexity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Cloud dominance accelerates

Cloud archives generated 71.32% of revenue in 2025, equating to the largest slice of the email archiving market share, and are projected to expand at 17.65% CAGR. On-premises holds relevance for institutions with stringent sovereignty mandates, yet incremental feature parity and lower total cost of ownership continue to shift budgets toward SaaS models. Enhanced eDiscovery, AI-driven analytics, and elastic storage underpin the cloud’s growing appeal to both enterprises and SMEs. The email archiving market size for cloud deployments is forecast to reach USD 15.15 billion by 2031, underscoring its foundational role in future strategies.

Cloud adoption additionally reflects the repositioning of archives as data-governance hubs. Vendors now bundle API-level captures from Teams, Slack, and Zoom, creating integrated repositories that support proactive risk monitoring. As ransomware resilience becomes a board-level priority, immutable storage tiers and isolated recovery environments are standard features, further cementing the cloud model’s strategic importance.

By Content Type: Beyond traditional email

Email content represented 68.25% of 2025 revenue, reinforcing the channel’s regulatory centrality. Nevertheless, social media & collaboration communications register the fastest expansion at 17.74% CAGR as internal chats, reactions, and shared files gain evidentiary significance during litigation. The shift is prompting vendors to enhance ingestion connectors and normalization engines able to translate multi-modal content into searchable journals. The email archiving market size for social media & collaboration capture is set to exceed USD 6.76 billion by 2031 as regulatory bodies clarify expectations around multi-channel governance.

This convergence of content types is driving platform consolidation. Proofpoint’s 2025 acquisition of Nuclei extends capture coverage to 100-plus collaboration tools, highlighting the premium placed on comprehensive content visibility. Buyers increasingly demand single-pane management across channels to streamline legal holds, retention schedules, and AI-assisted investigations.

By Organization Size: SMEs driving growth

Large enterprises controlled 66.20% of spending in 2025, reflecting complex compliance demands and legacy archive refresh cycles. Yet SMEs are projected to deliver a 18.55% CAGR thanks to subscription-based offerings that eliminate capital expenditure. Cost transparency is emerging as a critical differentiator as hidden egress and API fees threaten the SME business case.Vendors targeting this cohort are bundling fixed-fee tiers, automated configuration wizards, and curated compliance templates to reduce onboarding friction.

SMEs also value integrations with popular productivity suites and plug-and-play security stacks, reducing reliance on in-house expertise. As regional regulators lower reporting thresholds, SME adoption is expected to accelerate further, reinforcing the addressable opportunity for specialist providers in the email archiving market.

By Industry Vertical: BFSI leads, healthcare accelerates

BFSI retained the largest contribution at 22.18% in 2025, driven by SEC and FINRA stipulations mandating immutable records with prompt retrieval within two business days. The vertical’s risk-management culture prioritizes comprehensive eDiscovery, trade surveillance, and supervisory review modules, sustaining elevated average contract values. In contrast, healthcare & life sciences are projected to grow at 17.95% CAGR on the back of expanding telehealth, HIPAA compliance, and cross-disciplinary collaboration. The email archiving market size allocated to healthcare workflows is poised to surpass USD 2.63 billion by 2031.

Sector-specific functionality has become a competitive lever. Financial-grade archives incorporate lexicon-based alerting for insider trading, whereas healthcare deployments emphasize PHI detection and redaction. Vendors able to template these vertical nuances at scale are positioned to capture a disproportionate share.

By Service Type: Software-services integration

Software holds the largest share of 64.40% in 2025, in which core archiving platforms remain the revenue engine, but professional services—consulting, migration, managed retention tuning—are gaining share as clients confront legacy infrastructure and new privacy mandates. PST migration engagements alone account for a growing proportion of implementation budgets, especially among banks grappling with decades of unstructured storage.

The fusion of software and services is leading to outcome-based contracting models that tie vendor remuneration to successful compliance audits or recovery time targets.

Geography Analysis

North America secured 39.85% of 2025 revenue, buoyed by mature regulatory regimes and frequent litigation that necessitates defensible retention. The SEC’s allowance for cloud platforms providing immutable audit trails has expanded the addressable market for SaaS vendors and reduced hardware refresh cycles. Simultaneously, rising ransomware incidents have entrenched immutable archives within cyber-resilience playbooks.

Asia Pacific represents the fastest-growing region at an 18.12% CAGR. Massive data-center investments combined with policy reforms such as India’s Digital Personal Data Protection Act are stimulating adoption. The region’s data-center colocation footprint now equals 37% of global capacity, ensuring local storage zones for sovereign-cloud deployments. Governments are additionally encouraging in-region backup strategies to underpin digital-economy growth.

Europe’s growth trajectory is moderated by Schrems II-linked uncertainty. Enterprises are investing in regional instances and contractual safeguards to mitigate transfer risk, driving demand for archives that support flexible residency configurations and advanced encryption controls. Meanwhile, Middle-East growth is led by GCC sovereign-cloud mandates that require regulated workloads to remain in-country. Saudi Arabia’s digital sector already contributes 14% to GDP, underscoring regional appetite for compliant storage infrastructure.

Competitive Landscape

Mimecast, Veritas, Microsoft, and Google anchor the field, yet specialist entrants continue to gain relevance through niche capabilities. Proofpoint’s May 2025 acquisition of Nuclei adds multi-channel capture, reinforcing the firm’s positioning in unified governance. Smarsh targets smaller financial advisers with turnkey SaaS packages that simplify adherence to non-erasable record rules.

Industry restructuring is evident from Cohesity’s purchase of Veritas Technologies, which spun off “DataCo” to oversee Enterprise Vault. Customers now reassess roadmaps, opening doorways for rival vendors that tout rapid innovation pipelines. Hyperscalers simultaneously strengthen native features, exemplified by Microsoft’s late-2024 update detailing how its retention architecture aligns with SEC 17a-4 and FINRA 4511 obligations. AI-driven analytics, immutable storage tiers, and integrated cyber-recovery environments dominate differentiation narratives.

Strategic moves also reflect vertical focus. Global Relay maintains BFSI exclusivity, leveraging a rule-based supervision workflow. Archive360’s PaaS positioning delivers tenant-level isolation for sensitive government workloads, earning Gartner leadership status and underlining shift toward flexible platform architectures.

Email Archiving Industry Leaders

Proofpoint, Inc.

Smarsh LLC

Mimecast Ltd.

Veritas Technologies LLC

Microsoft Corp. (Exchange Online Archiving)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Proofpoint acquired Nuclei to extend capture coverage across 100+ collaboration channels, aiming to deepen governance insights and reduce eDiscovery blind spots

- April 2025: HaystackID launched READI for Email, accelerating triage workflows for legal and cybersecurity practitioners tackling high-volume review projects

- March 2025: Archive360 was positioned as a leader in Gartner’s Digital Communications Governance quadrant, validating its PaaS model that offers tenant isolation and sovereign-cloud options

- January 2025: Cloudficient released Expireon to preserve contemporaneous hyperlink versions embedded in emails, mitigating compliance gaps created by dynamic cloud-storage links

Global Email Archiving Market Report Scope

Email archiving systematically stores and preserves email messages and their attachments securely and in a searchable format. Unlike traditional methods that store messages locally on individual devices or servers, email archiving centralizes data in a dedicated archive repository.

The study tracks the revenue accrued through the sale of email archiving solutions by various players across the globe. It also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The email archiving market is segmented by deployment (on-premise and cloud), application (enterprise, schools, banks, and others), and geography (North America, Europe, Asia Pacific, Middle East and Africa, and Latin America). The market sizes and forecasts regarding value (USD) for all the above segments are provided.

| Cloud |

| On-Premise |

| Social Media and Collaboration |

| Instant Messaging |

| File and Attachment |

| Database and ERP |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| BFSI |

| Government and Public Sector |

| Healthcare and Life Sciences |

| IT and Telecommunications |

| Education |

| Retail and E-commerce |

| Manufacturing and Energy |

| Software | Archiving Platform |

| Services | Consulting and Assessment |

| Integration and Migration | |

| Support and Maintenance |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Nordics | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| Rest of Asia | ||

| Australia and New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | GCC (Saudi Arabia, UAE, Qatar, etc.) |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Deployment | Cloud | ||

| On-Premise | |||

| By Content Type | |||

| Social Media and Collaboration | |||

| Instant Messaging | |||

| File and Attachment | |||

| Database and ERP | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By Industry Vertical | BFSI | ||

| Government and Public Sector | |||

| Healthcare and Life Sciences | |||

| IT and Telecommunications | |||

| Education | |||

| Retail and E-commerce | |||

| Manufacturing and Energy | |||

| By Service Type | Software | Archiving Platform | |

| Services | Consulting and Assessment | ||

| Integration and Migration | |||

| Support and Maintenance | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Nordics | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| Rest of Asia | |||

| Australia and New Zealand | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | GCC (Saudi Arabia, UAE, Qatar, etc.) | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

Why is the email archiving market growing so quickly?

Stringent global regulations, surging ransomware threats, and the migration to cloud productivity suites are combining to drive a 17.12% CAGR between 2026 and 2031.

How large will the email archiving market be by 2031?

Forecast models place the email archiving market size at USD 20.66 billion by 2031.

Which deployment model is preferred today?

Cloud deployment commands 71.32% of 2025 revenue and is projected to grow at 17.65% CAGR thanks to scalability and immutable storage benefits.

Which region offers the highest growth potential?

Asia Pacific is expected to lead expansion with an 18.12% CAGR as data-privacy laws tighten and digital-economy programs scale.

What verticals display the strongest demand?

BFSI leads current spending with 22.18% revenue share, while healthcare & life sciences presents the fastest growth at 17.95% CAGR due to HIPAA-driven digitization.

How does ransomware influence buying decisions?

The high cost of recovery is prompting enterprises to mandate immutable email archives, integrating cyber-resilience into compliance budgets and accelerating vendor selection.

Page last updated on: