Aerospace TIC Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 12.47 Billion |

| Market Size (2031) | USD 15.26 Billion |

| Growth Rate (2026 - 2031) | 4.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

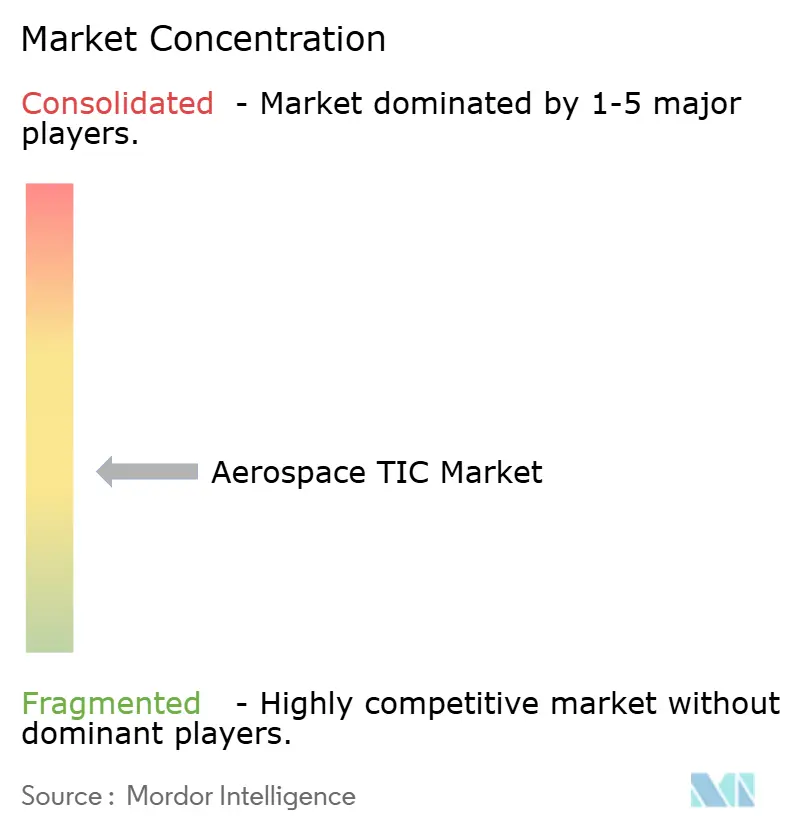

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aerospace TIC Market Analysis by Mordor Intelligence

The aerospace TIC market size is expected to increase from USD 11.98 billion in 2025 to USD 12.47 billion in 2026 and reach USD 15.26 billion by 2031, advancing at a CAGR of 4.12% during 2026-2031. The aerospace TIC market is being supported by a strong commercial aircraft production cycle, with large Airbus and Boeing backlogs extending the need for testing, inspection, and certification work across several years. That demand does not end at final assembly, because new tooling, substitute suppliers, engineering changes, and process updates all trigger fresh qualification and conformance work across the supply chain. The aerospace TIC market is also being lifted by tighter airworthiness, supplier quality, and cross-border validation requirements that leave less room for internal sign-off and require greater external verification. At the same time, OEMs and tier-1 suppliers are directing more capital toward production systems, digital manufacturing, and workforce readiness, pushing more capex-intensive qualification work to external specialists. Capacity constraints at Nadcap-accredited facilities remain the clearest near-term brake on the aerospace TIC market, but those same constraints are improving pricing power and raising the value of providers with recognized labs, broader approvals, and faster turnaround times.

Key Report Takeaways

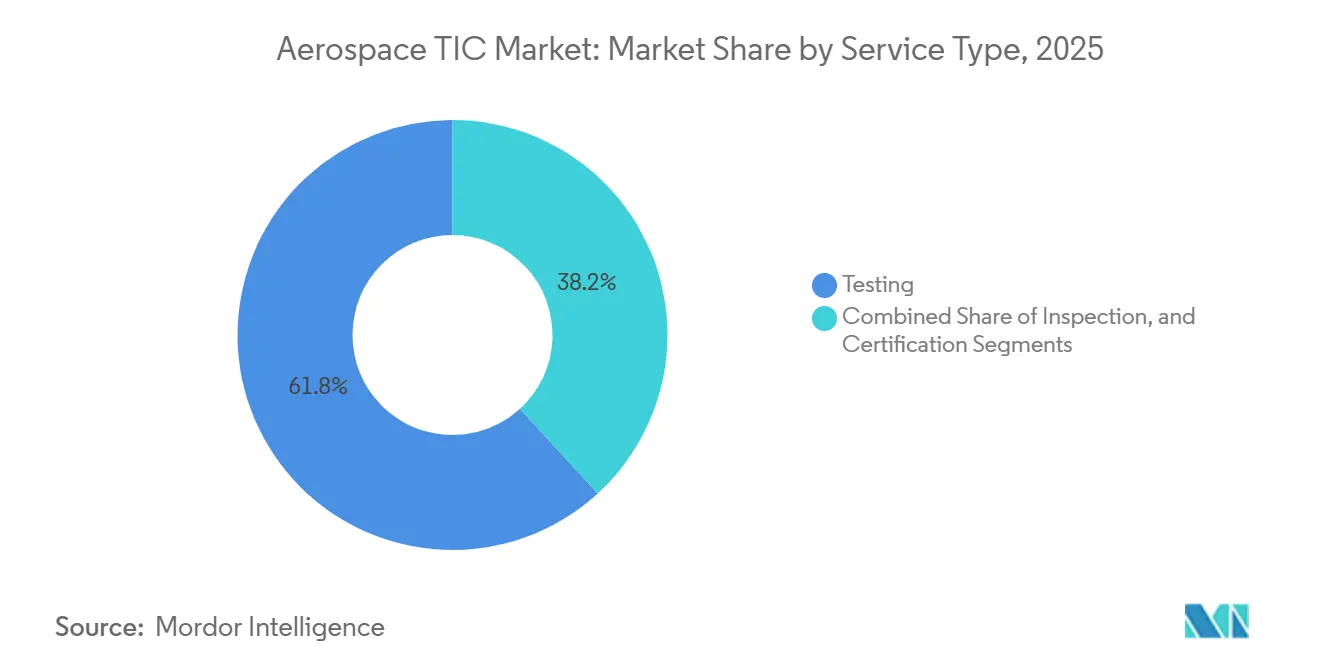

- By service type, testing held 61.81% share of the aerospace TIC market in 2025, while certification is projected to expand at a 4.25% CAGR through 2031.

- By sourcing type, outsourced TIC captured 63.06% share of the aerospace TIC market in 2025 and also recorded the fastest projected CAGR at 5.02% through 2031.

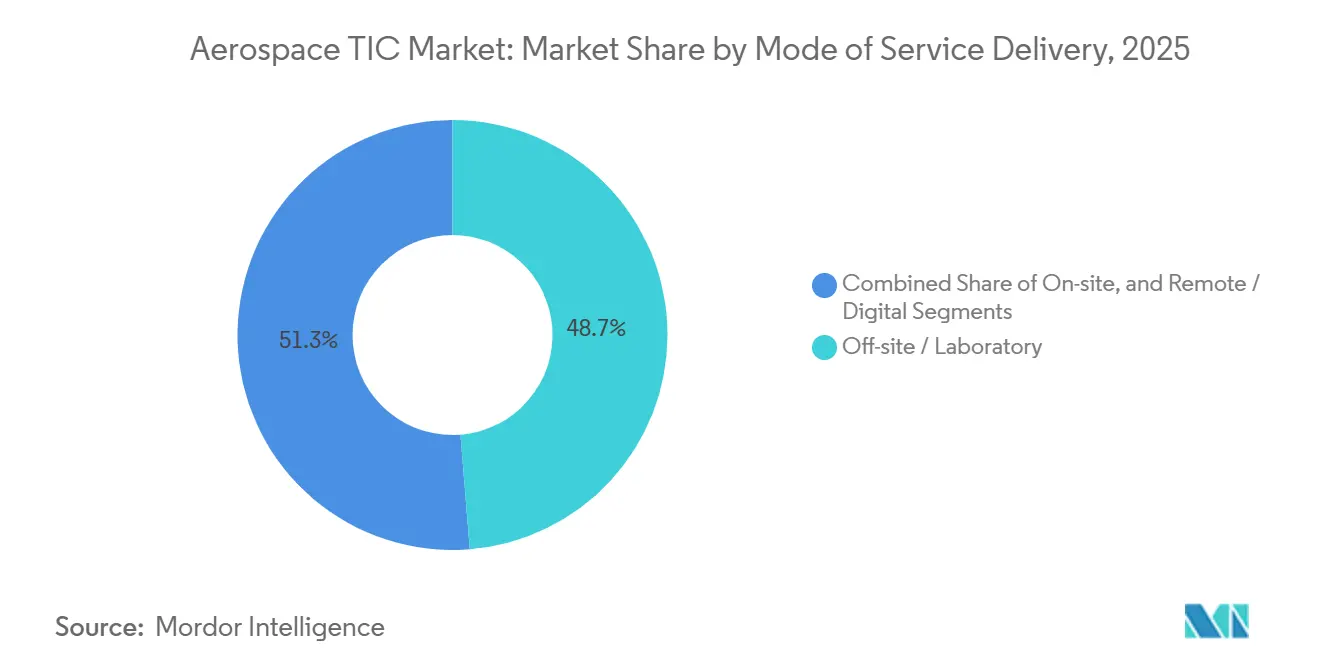

- By mode of service delivery, off-site laboratory delivery accounted for 48.73% share of the aerospace TIC market in 2025, while remote and digital delivery is expected to grow at a 4.66% CAGR through 2031.

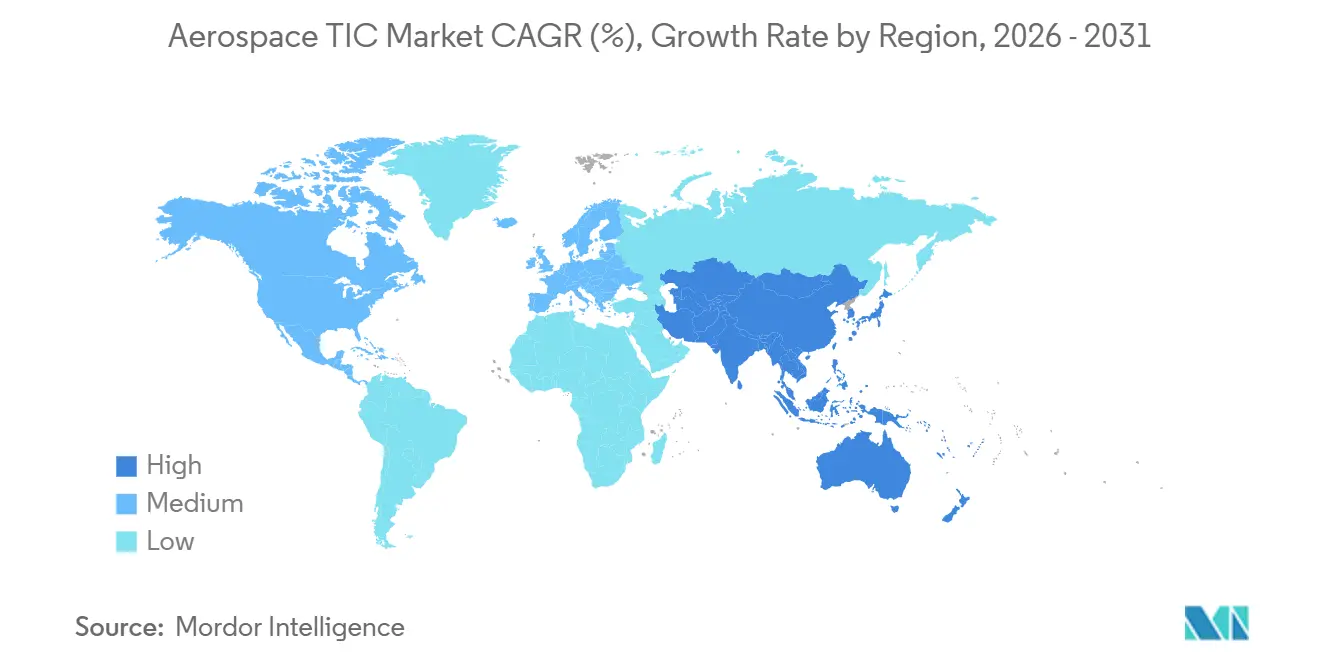

- By geography, Asia-Pacific held 41.92% share of the aerospace testing, inspection, and certification (TIC) market in 2025 and is forecast to advance at a 4.83% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Aerospace TIC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Commercial Aircraft Production and Fleet Renewal | +1.4% | Global, with concentration in North America, Europe, and Asia-Pacific | Short term (≤ 2 years) |

| Tightening Airworthiness, Safety, and Supplier Quality Mandates | +1.1% | Global, with regulatory intensity highest in North America and Europe | Medium term (2-4 years) |

| Expanding Use of Composites and Advanced Materials | +0.7% | North America, Europe, and Asia-Pacific production hubs | Medium term (2-4 years) |

| Growing Outsourcing of Capex-Intensive Qualification Work | +0.5% | Global, Asia-Pacific core with North America and Europe OEM offload | Short term (≤ 2 years) |

| Certification Demand from More-Electric Aircraft and Advanced Air Mobility Platforms | +0.4% | North America and Europe with spillover to Asia-Pacific | Long term (≥ 4 years) |

| Cybersecurity and Software Assurance Becoming Part of Airworthiness | +0.2% | North America and Europe primarily, emerging Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Commercial Aircraft Production and Fleet Renewal

The aerospace TIC market continues to draw strength from a commercial production base that remains unusually full for both major aircraft manufacturers. Airbus delivered 793 commercial aircraft in 2025 and reported a commercial backlog of 8,754 aircraft, while Boeing delivered 600 commercial aircraft in 2025 and reported a company backlog of USD 682 billion in January 2026. Airbus also reported 408 gross commercial aircraft orders in Q1 2026, up from 280 in Q1 2025, and said its commercial backlog had risen to 9,037 aircraft. Each aircraft in these backlogs passes through a chain of materials allowables, first-article inspection, acceptance testing, and supplier audits, which gives the aerospace TIC market a multi-year revenue base rather than a short-term delivery spike. Rate ramp-ups also raise TIC demand faster than unit output alone suggests, because new tools, substitute sources, and process changes each create additional conformance cycles around the same aircraft family.

Tightening Airworthiness, Safety, and Supplier Quality Mandates

The aerospace TIC market is also being driven forward by stricter airworthiness and supplier-quality oversight in key aviation jurisdictions. The FAA issued an airworthiness directive effective May 26, 2026, requiring thickness inspections on certain Airbus A319, A320, and A321 aircraft following a supplier-related production quality issue.[1]Federal Aviation Administration, “Airworthiness Directives, Airbus SAS Airplanes,” The Federal Register, thefederalregister.org EASA issued AD 2026-0055R1 on the same fuselage-panel issue, demonstrating how parallel compliance demands can arise across multiple regulators simultaneously. EASA also updated its User Guide for Production Organizations in March 2026, adding additive manufacturing assessment checklists and extending formal supplier-quality expectations into a newer production area. The aerospace TIC market is benefiting from this broader shift toward supplier-level visibility because cross-border validation under the FAA and EASA Technical Implementation Procedures still requires substantial documentation, audit support, and export-facing quality evidence.

Expanding Use of Composites and Advanced Materials

The aerospace TIC market is seeing steady support from the growing use of composite structures and other advanced material systems in new aircraft programs. Toray Composite Materials America achieved NCAMP qualification in February 2026 for its 3960/T1100 prepreg system, with FAA- and EASA-accepted material specifications made available for aerospace use after a multi-batch test program. ST Engineering MRAS said in 2026 that composite aerostructures follow a different certification logic than metal parts, because each new geometry needs engineering definition, process qualification, and certification engagement. That means the aerospace TIC market captures more work per production unit when composite content rises, since qualification cannot be treated as a simple repeat of legacy metal workflows. The same pattern is beginning to matter for recycled aerospace composites and metallic additive materials, where qualification pathways are less mature and testing methods still need broader standardization. As those materials move toward structural and semi-structural applications, providers with strong materials laboratories will play a broader role in the aerospace TIC market.

Growing Outsourcing of Capex-Intensive Qualification Work

A steady shift toward outsourced qualification work is also reshaping the aerospace TIC market. Outsourced services indicate that external delivery is expanding faster than the market as a whole. The driver is not only cost, because OEMs and tier-1 suppliers are prioritizing capital for production tooling, digital manufacturing, and workforce development instead of maintaining environmental chambers, fatigue frames, and x-ray CT systems in-house. Element Materials Technology announced a USD 20 million expansion of its Charlotte facility in May 2026, adding stress rupture and creep, tensile, machining, metallurgical, and miniature testing capacity for aerospace and defense qualification work. The aerospace TIC market is gaining volume from this outsourcing wave, but it is also facing tighter bottlenecks as more qualification work is concentrated in a smaller pool of accredited laboratories.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Long Lead Times at Nadcap-Accredited and FAA-EASA-Recognized Labs | -0.8% | Global, with acute pressure in North America and Europe | Short term (≤ 2 years) |

| High Cost and Schedule Burden of Multi-Authority Compliance | -0.5% | Global, with greatest impact on cross-border suppliers | Medium term (2-4 years) |

| Scarcity of Aerospace Auditors, DERs, and Specialized Test Talent | -0.4% | North America, Europe, and nascent Asia-Pacific hubs | Medium term (2-4 years) |

| Export-Control and Data-Residency Frictions in Cross-Border Verification | -0.2% | North America, Europe, and Asia-Pacific export corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Long Lead Times At Nadcap-Accredited and FAA-EASA-Recognized Labs

Long lead times at accredited laboratories remain the most immediate constraint on the aerospace TIC market. Nadcap, administered by the Performance Review Institute, covers 24 critical process accreditation programs and serves as a practical entry point for suppliers seeking to participate in many OEM and tier-1 programs.[2]Performance Review Institute, “Nadcap - National Aerospace And Defense Contractors Accreditation Program,” PRI, p-r-i.org First-time accreditation is still demanding, because suppliers need internal readiness work, process evidence, audit preparation, and sustained conformance before they can enter routine customer programs. The move to 18-month audit intervals in some established cases offers limited relief, but it does not shorten the path for new entrants or solve the shortage of available testing slots. As aircraft production ramps faster than accredited capacity expands, the aerospace TIC market continues to face schedule risk from testing queues that delay qualification, certification, and supplier approvals.

High Cost and Schedule Burden of Multi-Authority Compliance

The aerospace TIC market also faces a drag from overlapping compliance requirements across aviation authorities. Cross-border suppliers often need to satisfy FAA, EASA, UK CAA, Transport Canada, CAAC, DGCA, and other national rules, even when the underlying product has already been validated in its home jurisdiction. The FAA and EASA Technical Implementation Procedures remained under active revision in 2026 to address export documentation mismatches that can still force repeated paperwork or duplicated validation steps. Smaller suppliers are particularly exposed because maintaining AS9100 Rev D compliance, along with customer-specific supplements, can stretch quality budgets and delay approvals. The aerospace TIC market still benefits from the resulting outsourcing trend, but the extra cost and time burden can slow adoption cycles and compress supplier margins before that work reaches outside providers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Certification Momentum Intensifies Beyond Testing's Dominance

Testing retained 61.81% of the aerospace testing, inspection, and certification (TIC) market share in 2025, maintaining its position as the core service block. The segment remained anchored in non-destructive testing, materials testing, and environmental simulation work that moved directly with active aircraft production programs. Its depth stemmed from long-established requirements for structural load testing, fatigue cycling, ultrasonic inspection, and other procedures that remain mandatory at every aircraft build stage. Inspection services continued to sit between major qualification milestones, especially in maintenance, repair, and overhaul settings where airworthiness limitation documents define formal inspection intervals. This installed base means the aerospace TIC market still depends primarily on testing and inspection, even as newer aircraft concepts broaden future certification workloads.

Certification is projected to grow at a 4.25% CAGR through 2031, making it the fastest-growing service type in the aerospace TIC market. eVTOL aircraft, more-electric aircraft, hybrid-electric propulsion, and hydrogen-fueled aircraft are expanding the scope of type certification beyond traditional commercial and defense platforms. The FAA's powered-lift framework and EASA's SC-VTOL pathway have established formal pathways that require extensive testing and evidence before operators can move toward broader deployment. Toray's NCAMP qualification campaign also showed that certification work begins well before first flight, because material-level acceptance can generate long laboratory programs on its own. That pattern is widening the addressable scope of the aerospace TIC industry, especially in categories where regulatory pathways are still taking shape.

By Sourcing Type: Outsourcing Consolidates Structural Dominance

Outsourced TIC captured 63.06% of the aerospace testing, inspection, and certification (TIC) market size in 2025 and also posted the fastest forecast CAGR at 5.02% through 2031. That made sourcing the only segmentation type where the segment leader was also the fastest-growing part of the aerospace TIC market. OEMs and tier-1 suppliers are investing more in production tooling, digital manufacturing systems, and workforce readiness rather than maintaining a full set of specialized qualification assets in-house. In-house TIC still retains a place in defense and export-controlled programs, where data-handling limits and program sensitivity can restrict outside participation. Even so, the center of gravity in the aerospace TIC market continues to shift toward external providers with accredited capacity and multi-customer lab economics.

This sourcing shift is also changing ownership patterns inside the aerospace TIC industry. MISTRAS reported that aerospace and defense revenue rose by USD 7.2 million in Q1 2026, up 30.1%, suggesting stronger outsourced demand for structural inspection and NDT services. Element's Charlotte expansion showed the same trend from the capacity side, with independent labs adding engine and component testing capability rather than leaving those investments with OEMs.[3]Element Materials Technology, “Element Invests USD 20M To Expand Aerospace Materials Testing Facility In Charlotte,” Element Materials Technology, element.com The downside is the concentration of bottlenecks, because a smaller pool of Nadcap-accredited providers can become a single point of delay when demand spikes. That tension is likely to remain a defining feature of the aerospace TIC market over the next several years.

By Mode of Service Delivery: Remote Channels Accelerate While Labs Remain Central

Off-site laboratory delivery accounted for 48.73% of the aerospace testing, inspection, and certification (TIC) market in 2025, keeping laboratory-based work at the center of the market. Much of this segment depends on calibrated equipment such as tensile machines, thermal chambers, and mass spectrometers that cannot be replicated on a routine field basis. On-site delivery still matters for in-situ NDT, large aerostructures, and maintenance events where removing the component would disrupt the repair schedule or increase handling risk. The result is a delivery model in which labs remain the anchor for evidence generation, while field teams handle access-critical work near the aircraft or component. That balance is unlikely to change quickly because many certification and qualification paths still require controlled laboratory conditions.

Remote and digital delivery is projected to grow at a 4.66% CAGR through 2031, making it the fastest-growing service mode in the aerospace TIC market. Waygate Technologies and GE Aerospace deployed automated Menu Directed Inspection templates for GEnx-1B and GEnx-2B borescope inspections in April 2026, combining standardized workflows with AI-assisted defect detection. That move showed how digital methods can reduce variability, support repeatability, and shorten review time without removing the need for formal technical evidence. Jet Aviation also extended its drone- and AI-based exterior inspection service to US locations in May 2026, indicating broader commercial use of digital surface mapping in aircraft inspection operations. As these tools mature, the aerospace TIC market will likely see faster reporting and better workflow efficiency, but not a full replacement of laboratory-led verification.

Geography Analysis

Asia-Pacific held 41.92% of the aerospace TIC market share in 2025 and is projected to grow at a 4.83% CAGR through 2031, making it both the largest and fastest-growing regional market. The region benefits from expanding manufacturing activity in India, China, South Korea, and Japan, which increases the number of suppliers, components, and production processes that need qualification and oversight. India provided one of the clearest recent demand signals when Tata Advanced Systems inaugurated the country's first private-sector helicopter final assembly line for the Airbus H125 in Karnataka in February 2026. That step added fresh need for supplier qualification, first-article inspection, and certification support as local manufacturing moved deeper into final assembly. Asia-Pacific is also becoming more important to the aerospace TIC market because local programs are increasingly expected to operate within stronger production and maintenance compliance frameworks.

North America and Europe formed the second-largest combined block in the aerospace TIC market, supported by deep OEM-supplier ecosystems and mature regulatory institutions. North America remained active because Boeing delivered 600 commercial aircraft in 2025 and reported a company backlog of USD 682 billion in January 2026, both of which support sustained testing and inspection demand. The United States also remains central to advanced air mobility certification, where FAA air-taxi and powered-lift activities are creating workstreams distinct from legacy fixed-wing programs. In Europe, EASA widened the regulatory perimeter through updated Production Organization Approval guidance in March 2026 and formal operating frameworks for manned VTOL-capable aircraft, which increased supplier quality and certification activity.[4]European Union Aviation Safety Agency, “Production Organisations Approvals - User Guide UG.POA.00067,” EASA, easa.europa.eu

Middle East and Africa and South America remain smaller parts of the aerospace TIC market, but both regions show pockets of demand tied to fleet growth and localized manufacturing ambitions. In the UAE, Strata Syensqo's large-scale production of carbon fiber prepreg materials for Boeing 777X program test components demonstrated how regional aerocomposites activity can create specialized materials-testing and process-qualification needs. Africa has remained more MRO-led, and EGYPTAIR's first Airbus A350-900 delivery in 2025 highlighted additional inspection and support requirements for newer widebody fleets. In South America, Brazil continues to anchor regional demand through Embraer's commercial and defense activity, where export compliance and third-party product validation remain important to international delivery programs.

Competitive Landscape

The aerospace TIC market is moderately concentrated, with SGS SA, Bureau Veritas SA, TÜV SÜD AG, Intertek Group plc, and Element Materials Technology Group forming the leading global tier. Their edge comes from their depth of Nadcap accreditation, multi-authority recognition, and large laboratory networks that can support work across several jurisdictions and program stages. That combination matters because customers often want a single provider that can handle testing, inspection, documentation, and follow-on audits under a single quality umbrella. At the same time, regional specialists still hold ground in the aerospace TIC market, where customers value faster turnaround, closer site access, or niche technical capabilities. This keeps the aerospace TIC market competitive even as accreditation density raises barriers for new entrants.

Element has taken one of the clearest expansion paths in the aerospace TIC market. The company said it operates 29 Nadcap-accredited labs with 41 distinct Nadcap accreditations globally, and it became the first TIC company to adopt blockchain-verified test reports in January 2026. This was followed by a USD 20 million expansion in Charlotte in May 2026, naming Huntsville a strategic innovation hub for space, aerospace, and defense testing. DEKRA also made a targeted move by acquiring Force Aerospace Testing, deepening its aerospace NDT coverage in Scandinavia across penetrant, magnetic particle, ultrasonic, eddy current, radiographic, and thermographic testing.[5]DEKRA, “DEKRA Acquires Force Aerospace Testing,” DEKRA, dekra.se These actions show that leading firms are not relying solely on scale, as they are also expanding trust, regional coverage, and technical depth.

The aerospace TIC market is also seeing strategic positioning through broader network integration. ATS formally joined the SGS Group in 2025, expanding SGS's US testing footprint with metallurgical, chemical analysis, and NDT capabilities that meet aerospace qualification needs. MISTRAS has also been gaining relevance where customers want outsourced structural inspection support, and its aerospace and defense revenue rose 30.1% in Q1 2026. Open areas remain in digital NDT with remote report delivery, in software and cybersecurity assurance for avionics programs, and in materials qualification for recycled composites and metallic additive powders. The aerospace TIC market, therefore, combines meaningful entry barriers with enough technical gaps for smaller specialists to build durable positions around newer workflows.

Aerospace TIC Industry Leaders

SGS SA

Bureau Veritas SA

TÜV SÜD AG

Intertek Group plc

DEKRA SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Element Materials Technology announced an investment of over USD 20 million in its Charlotte, North Carolina, laboratory to expand stress-rupture/creep, tensile, metallurgical, and miniature testing capacity for aerospace and defense customers, specifically targeting demand for engine and component qualification.

- May 2026: Jet Aviation extended its drone and AI-based aircraft exterior inspection service to US locations, enabling digital surface mapping and AI-driven defect detection for a wide range of business jets and airliners at its MRO facilities, building on capabilities first deployed in Basel in 2023.

- May 2026: The FAA published a new airworthiness directive, effective May 26, 2026, mandating thickness inspections and dispatch restrictions on certain Airbus A319, A320, and A321 family aircraft following a fuselage-panel quality deviation identified by an Airbus supplier, generating immediate demand for inspection services across the affected fleet.

- April 2026: Waygate Technologies, a Baker Hughes business, and GE Aerospace deployed automated Menu Directed Inspection templates for GEnx-1B and -2B engine borescope inspections, integrating AI-assisted defect detection under their Joint Technology Development Agreement, a step toward fully standardized, automated engine maintenance inspections.

Global Aerospace TIC Market Report Scope

The Aerospace Testing, Inspection, and Certification (TIC) market comprises services that assess, verify, validate, and certify the quality, safety, reliability, performance, and regulatory compliance of aerospace products, components, systems, manufacturing processes, and maintenance operations. These services support aircraft manufacturers, aerospace component suppliers, maintenance, repair, and overhaul (MRO) providers, defense contractors, space organizations, and aviation operators in meeting industry standards and regulatory requirements throughout the product lifecycle.

The Aerospace TIC Report is Segmented by Service Type (Testing, Inspection, and Certification), Sourcing Type (In-House, and Outsourced), Mode of Service Delivery (On-Site, Off-site/Laboratory, and Remote/Digital), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

| Testing |

| Inspection |

| Certification |

| In-house |

| Outsourced |

| On-site |

| Off-site / Laboratory |

| Remote / Digital |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Testing | |

| Inspection | ||

| Certification | ||

| By Sourcing Type | In-house | |

| Outsourced | ||

| By Mode of Service Delivery | On-site | |

| Off-site / Laboratory | ||

| Remote / Digital | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size and forecast for the aerospace TIC market?

The aerospace TIC market was valued at USD 11.98 billion in 2025 and is forecast to reach USD 15.26 billion by 2031 at a 4.12% CAGR during 2026-2031.

Which region leads aerospace TIC demand?

Asia-Pacific led with 41.92% revenue share in 2025 and is also projected to post the fastest regional growth at a 4.83% CAGR through 2031.

Which service category is largest in aerospace testing, inspection, and certification?

Testing was the largest service type in 2025 with 61.81% share, supported by steady demand for NDT, materials testing, and environmental simulation.

Why is outsourced aerospace TIC growing faster than in-house work?

Outsourced services held 63.06% share in 2025 and are forecast to grow at a 5.02% CAGR because OEMs are prioritizing capital for production tooling, digital systems, and workforce expansion instead of lab ownership.

What is driving certification growth in aerospace TIC?

Certification is projected to grow at a 4.25% CAGR as eVTOL, more-electric aircraft, hybrid-electric propulsion, and hydrogen-related programs move through new regulatory pathways.

What is the main near-term challenge for aerospace TIC providers and customers?

The most immediate constraint is long lead times at Nadcap-accredited and FAA or EASA-recognized labs, which are creating qualification bottlenecks as production ramps faster than accredited capacity.

Page last updated on: