Electronic Laboratory Notebook (ELN) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

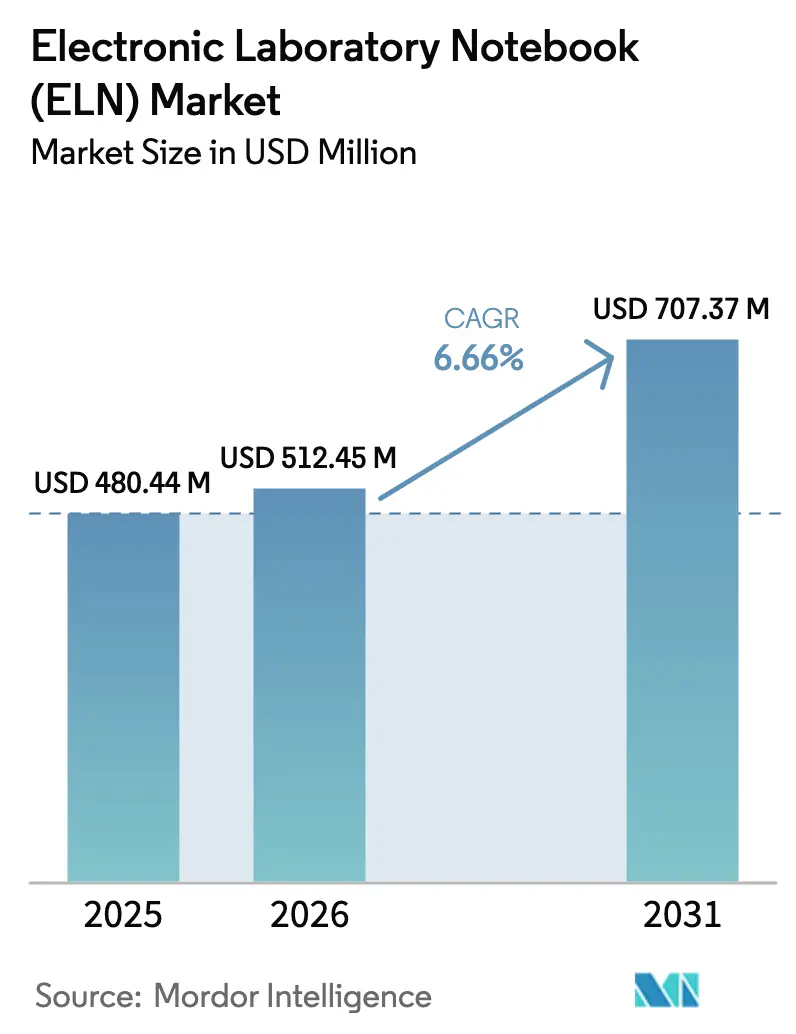

| Market Size (2026) | USD 512.45 Million |

| Market Size (2031) | USD 707.37 Million |

| Growth Rate (2026 - 2031) | 6.66% CAGR |

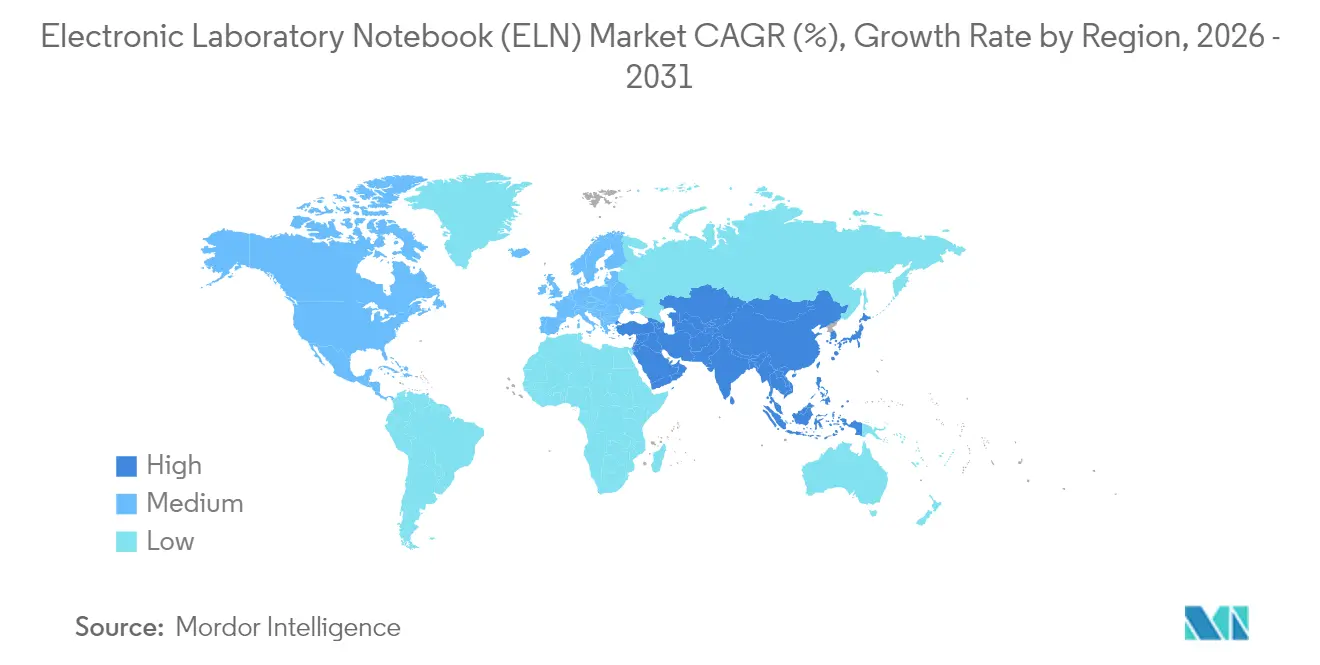

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

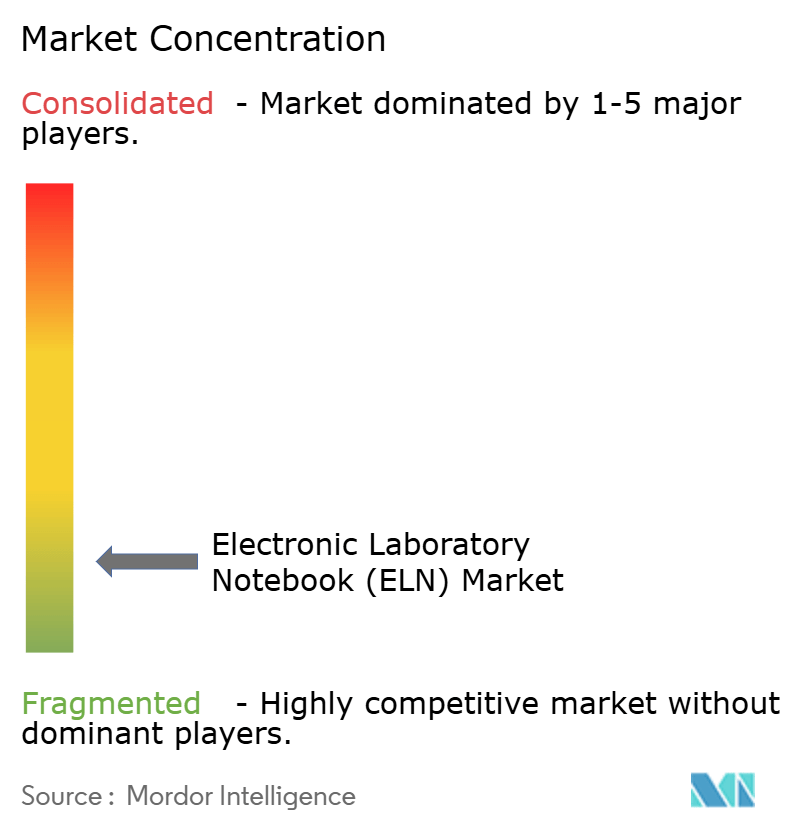

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electronic Laboratory Notebook (ELN) Market Analysis by Mordor Intelligence

The electronic lab notebooks market size in 2026 is estimated at USD 512.45 million, growing from 2025 value of USD 480.44 million with 2031 projections showing USD 707.37 million, growing at 6.66% CAGR over 2026-2031. Strong momentum stems from ongoing digitization across life-sciences laboratories, growing regulatory pressure for data integrity, and the emergence of artificial-intelligence features that convert ELNs from passive record systems into active research assistants. Rapid acceptance of web-based deployments is especially striking in a sector once wary of off-premise computing, with cloud platforms already holding 67.92% share in 2024 despite heightened scrutiny of cybersecurity safeguards. Cross-disciplinary solutions remain the dominant product category at 55.45% share, mirroring the need for unified data models that support chemistry, biology, and analytical functions on a single platform. Vendors that pair these broad capabilities with built-in 21 CFR Part 11 compliance have gained a strategic edge as inspection findings show data-integrity violations continuing to rise in the United States and Europe. On the demand side, contract research organizations (CROs) in Asia-Pacific are scaling rapidly, propelling the electronic lab notebooks market toward high-growth territories where harmonized regulations are still evolving.

Key Report Takeaways

- By product type, cross-disciplinary solutions led with 54.93% revenue share in 2025; specific/domain ELNs are projected to advance at a 6.92% CAGR through 2031.

- By license type, proprietary platforms held a commanding 78.15% of the electronic lab notebooks market share in 2025, while open-source offerings are forecast to register a 7.31% CAGR by 2031.

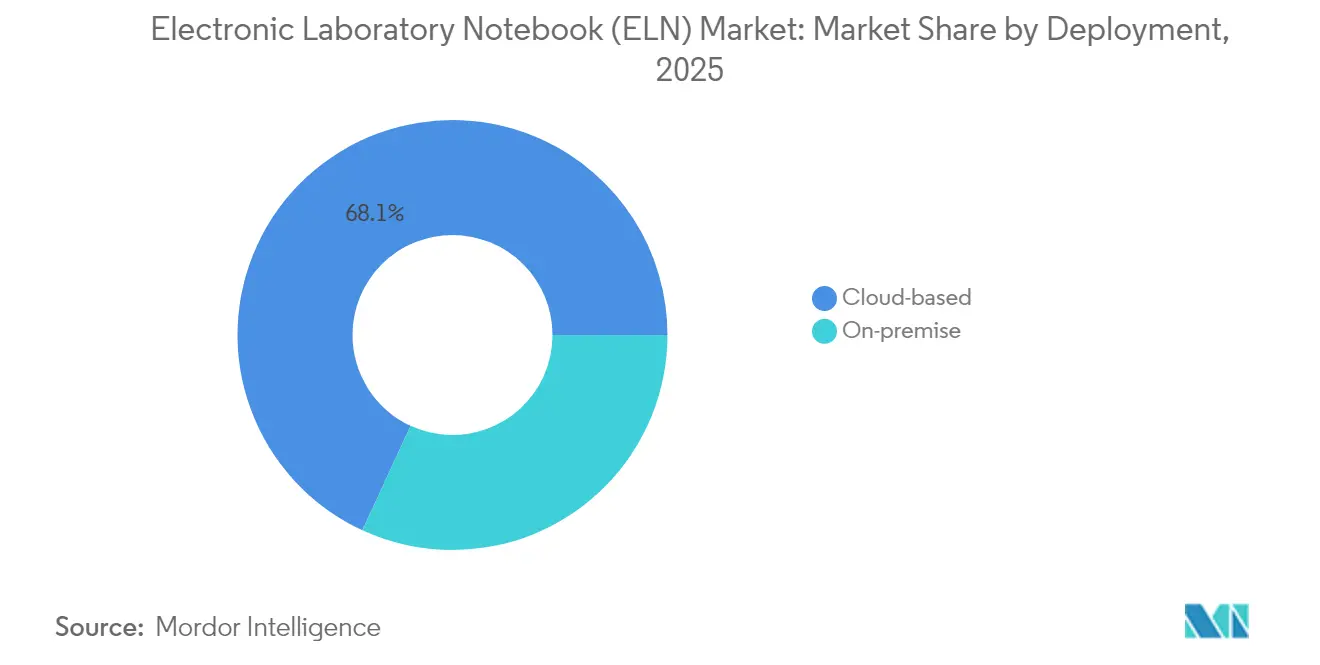

- By deployment mode, web/cloud-based implementations captured 68.12% share in 2025 and are expanding at a 7.75% CAGR through 2031.

- By end user, pharmaceutical & biotechnology companies accounted for 46.12% of the electronic lab notebooks market size in 2025; contract research organizations are the fastest-growing segment with an 8.25% CAGR to 2031.

- By geography, North America commanded 37.65% share in 2025, whereas Asia-Pacific is slated to climb at the highest 8.71% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Electronic Laboratory Notebook (ELN) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in life-sciences R&D digitization | +1.8% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Regulatory push for data integrity (21 CFR 11) | +1.2% | North America & EU primary, expanding to APAC | Long term (≥ 4 years) |

| Shift toward cloud-native lab ecosystems | +1.5% | Global, led by North America | Short term (≤ 2 years) |

| CRO outsourcing boom in Asia-Pacific | +0.9% | APAC core, spill-over to global CRO networks | Medium term (2-4 years) |

| AI-ready ELNs enabling predictive analytics | +0.7% | North America & EU early adoption, APAC following | Long term (≥ 4 years) |

| Venture-capital funding for ELN start-ups | +0.4% | Global, concentrated in North America & EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Life-Sciences R&D Digitization

Life-sciences laboratories are producing roughly 40 exabytes of data annually by 2025, intensifying the need for structured, searchable repositories that marry exploratory research with GxP frameworks[1]Source: Scispot, “Laboratory data to hit 40 exabytes by 2025,” scispot.com . Cross-disciplinary ELNs now function as laboratory operating systems that capture instrument feeds in real time, enforce standardized metadata, and create the audit trails auditors expect. This environment elevates the electronic lab notebooks market because machine-learning models require clean, lineage-rich datasets, and the ELN is fast becoming the principal aggregation node. Pharmaceutical sponsors further accelerate adoption by mandating digital data capture in outsourcing contracts, pushing late-adopting CROs into rapid implementation cycles. Collectively, these developments foster a network effect in which broader user communities generate more shared templates, best-practice workflows, and pre-trained AI models, reinforcing platform value.

Regulatory Push for Data Integrity (21 CFR Part 11)

Regulators intensified electronic-record enforcement in 2024 as data-integrity failures topped FDA warning-letter findings for pharmaceutical manufacturers. Modern ELNs answer this scrutiny through immutable audit trails, granular permission sets, and electronic-signature protocols that mirror those of validated paper records. Companies that adopt fully compliant systems reduce remediation costs, shorten inspection timelines, and improve confidence in cross-border submissions as the EU, China, and India converge on similar requirements. Competitive advantage now accrues to vendors able to deliver validation packages and ongoing patch documentation, removing a sizeable burden from IT groups already stretched thin by quality-management tasks.

Shift Toward Cloud-Native Lab Ecosystems

Web-based deployments account for 67.92% of installations and continue rising as pharmaceutical companies partner with hyperscale providers—Pfizer with AWS and UCB with Microsoft Azure—to modernize R&D infrastructure. Cloud ELNs offer elastic compute, native analytics, and seamless collaboration for globally distributed project teams, features that were instrumental during pandemic-era travel restrictions. The success of these projects demonstrates that encryption, zero-trust identity architectures, and continuous security monitoring can reduce risk while delivering operational agility. Organizations now negotiate robust exit provisions to preserve data portability, signaling a maturing understanding of cloud governance rather than outright resistance.

CRO Outsourcing Boom in Asia-Pacific

Asia-Pacific CRO revenues climbed sharply after Chinese firms such as Wuxi AppTec entered the global top-10 league, cementing regional laboratories as preferred partners for cost-effective early-stage research. Handling multi-sponsor projects demands ELNs that guarantee client data separation, role-based access, and harmonized reporting formats. As regulators in China, Singapore, and South Korea align more closely with ICH and US-FDA guidelines, demand for certified platforms grows, making the electronic lab notebooks market a critical enabler of sustained outsourcing expansion.

Restraints Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent data-security concerns | -1.1% | Global, particularly pronounced in regulated industries | Medium term (2-4 years) |

| Legacy LIMS/ERP integration complexity | -0.8% | North America & EU mature markets | Long term (≥ 4 years) |

| Talent gap in lab informatics | -0.6% | Global, acute in specialized bioprocessing | Long term (≥ 4 years) |

| Plateauing ELN adoption in academia post-COVID | -0.3% | North America & EU academic institutions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent Data-Security Concerns

High-profile breaches at contract development and manufacturing organizations (CDMOs) have raised fears over intellectual-property leakage and patient-data exposure Pharma-Focus-America. Decision-makers often delay cloud migrations, fearing regulatory fines and reputational harm that could dwarf efficiency gains. Effective countermeasures—multi-factor authentication, behavior-based anomaly detection, and continuous penetration testing—add cost and complexity, particularly for midsize firms with limited infosec headcount. Consequently, some buyers keep mission-critical workflows on-premise, diluting the total addressable slice of the electronic lab notebooks market in the near term.

Legacy LIMS/ERP Integration Complexity

Many laboratories run 15-year-old systems customized through ad-hoc scripts and proprietary data models, making bi-directional exchange with modern ELNs non-trivial ISPE. Project delays, data-mapping errors, and the need for costly middleware reduce the ROI of modernization efforts. Although vendor consolidation promises single-stack solutions, heterogeneous estates will persist through this decade, sustaining a layer of friction that tempers otherwise robust growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cross-Disciplinary Solutions Drive Market Consolidation

Cross-disciplinary offerings captured 54.93% of 2025 revenue, illustrating how enterprises prefer a single interface that spans chemistry synthesis, molecular biology, and analytical workflows. The segment’s 6.41% CAGR signals continued convergence as organizations dismantle paper notebooks and standalone specialty apps. Because machine-learning models derive more insight from blended datasets, wide-spectrum platforms improve algorithmic performance, reinforcing buyer preference and further enlarging this slice of the electronic lab notebooks market. Academic labs echo the trend; user studies involving 384 students cited readability, real-time collaboration, and structured search as decisive advantages over hand-written logs. Over the forecast horizon, more domain-specific features—spectral-analysis widgets, cell-culture dashboards—will likely be folded into these umbrella systems rather than remain in niche tools, accelerating consolidation.

Specialized ELNs keep relevance in deep verticals such as synthetic chemistry optimization or microbial-strain engineering, where domain vocabularies and unit operations are highly idiosyncratic. Vendors catering to these niches command premium pricing justified by built-in calculators, stoichiometric balancers, and template libraries attuned to field-specific regulatory clauses. Nevertheless, integration demands often steer large enterprises toward mixed deployments: a central cross-disciplinary backbone augmented by plug-ins that embed specialty functions. This hybrid adoption pattern enlarges the ecosystem for application-programming interfaces, supporting instrumentation vendors that wish to push data directly into structured ELN entries.

By License Type: Proprietary Dominance Faces Open-Source Challenge

Proprietary platforms contributed 78.15% of global sales in 2025, a dominance rooted in bundled validation artifacts, 24/7 support commitments, and aggressive product-road-map velocity. Enterprise buyers appreciate the reduced compliance overhead when vendors supply ready-made installation qualification (IQ) and operational qualification (OQ) documentation. Yet the electronic lab notebooks industry is witnessing a clear pivot: open-source alternatives are forecast to grow at 7.31% CAGR, fueled by universities and SMEs keen to avoid vendor lock-in and steep seat fees. Community projects now deliver modular architectures, containerized deployments, and extensive plugin ecosystems that narrow historic feature gaps.

Hybrid models are gathering steam. Organizations integrate an open-core ELN foundation and layer proprietary extensions for analytics, barcode integration, or electronic signatures. This approach preserves customizability while ensuring regulatory checkpoints remain intact. Over time, as open-source contributors formalize quality-management processes and partner with compliance consultancies, the trust barrier will erode, fostering healthy competition that benefits end users through faster innovation cycles and price discipline.

By Deployment Mode: Cloud Transformation Accelerates Despite Security Concerns

Web or cloud-hosted installations represent 68.12% of current deployments and exhibit the fastest 7.75% CAGR, underscoring paradigm change in how research data are stored and analyzed. The electronic lab notebooks market size for cloud implementations is projected to reach USD 498.6 million by 2031, almost double on-premise equivalents. Drivers include automatic version updates, global-team accessibility, and embedded analytics that process unstructured assay outputs without saturating local infrastructure. High-throughput laboratories leverage elastic compute clusters to run parallel molecular-dynamics simulations, seamlessly storing provenance within the ELN entry.

On-premise solutions hold relevance in highly regulated biologics manufacturing and government labs constrained by data-sovereignty statutes. Here, private clouds or hybrid models emerge as compromise architectures, retaining physical control over data centers while exploiting browser-based UI layers for ease of use. Vendors therefore invest in deployment flexibility, offering single-tenant SaaS, on-premise virtual appliances, and managed-private-cloud options under a unified codebase, allowing customers to migrate as risk appetites evolve.

By End User: CRO Growth Outpaces Traditional Pharma Adoption

Pharmaceutical and biotechnology companies remain the bedrock customer group, accounting for 46.12% of 2025 revenue; nonetheless, contract research organizations are clocking an 8.25% CAGR, outstripping sponsor growth as outsourcing penetrates additional workflow stages. The electronic lab notebooks market share commanded by CROs is expected to broaden as big pharma externalizes everything from lead-optimization chemistry to preclinical toxicology. Multitenancy, granular permissioning, and secure workspace cloning become essential ELN attributes, ensuring sponsor confidentiality while permitting CRO chemists to reuse methodologies across projects.

Academic and research institutes form a stable segment but have plateaued after pandemic-era peaks. Funding constraints and competing infrastructure priorities often delay upgrades. Conversely, the food & beverage and petrochemical sectors see incremental uptake as regulators tighten process documentation for safety and environmental compliance, driving crossover sales that buffer vendors against cyclicality in drug-development spending.

Geography Analysis

North America remains the single-largest contributor, capturing 37.65% of global revenue in 2025 thanks to intensive biotech clustering in Boston–Cambridge, the San Francisco Bay Area, and the Raleigh-Durham corridor. Frequent FDA inspections oblige firms to adopt fully validated platforms early, a practice that continues to propel procurement cycles even as top-tier pharma saturation grows. Investments in artificial-intelligence extensions further deepen the installed base; for example, US biopharma leaders are piloting ELN-embedded generative models to streamline protocol authoring and QA review.

Europe constitutes the second-largest region, supported by Germany’s chemicals expertise, the United Kingdom’s genomics focus, and sustained Horizon Europe funding for cross-border collaborations. Brexit-induced data-sovereignty debates caused some UK labs to reevaluate vendor contracts; however, most elected to maintain existing cloud providers after verifying adequacy under UK GDPR. EU Annex 11 compliance parallels FDA requirements, allowing multinational companies to roll out global ELN templates with minimal regional customization. As a result, the electronic lab notebooks market size in Europe is projected to exceed USD 184.1 million by 2031.

Asia-Pacific posts the fastest 8.71% CAGR, fueled by China’s surge in IND filings and India’s biologics manufacturing ambitions. Regional CRO giants invest aggressively in scalable ELN platforms to satisfy both local regulators and Western clients demanding synchronized data access. Government initiatives—Singapore’s National AI Strategy, Korea’s Bio-Digital initiative—offer grants that subsidize digital-lab conversions, widening the addressable buyer pool. Start-ups in cell-therapy and synthetic-biology niches further amplify demand, as these business models depend on meticulous chain-of-identity documentation best managed via modern ELNs.

Competitive Landscape

The electronic lab notebooks market is moderately fragmented yet displays clear consolidation momentum as industrial-software majors assimilate boutique specialists. Siemens’ USD 5.1 billion acquisition of Dotmatics [2]Source: Siemens AG, “Siemens closes acquisition of Dotmatics,” siemens.com in April 2025 expanded its Digital Twin portfolio and opened a USD 11 billion life-sciences TAM. Management projects USD 100 million in mid-term annual synergies owing to cross-selling into existing MindSphere and Teamcenter accounts. Similar logic underpins Certara’s 2024 purchase of ChemAxon, providing cheminformatics depth and rounding out Certara’s model-informed drug-development suite.

Venture-backed innovators also shape competitive dynamics. Benchling’s freemium model attracted more than 200,000 bench scientists, giving the company invaluable user-experience telemetry that guides product evolution. Partnerships with Merck on vaccine bioanalysis and Moderna on AI-driven research cement Benchling’s positioning at the intersection of biology and data science . Meanwhile, Sapio Sciences differentiates through conversational interfaces; its ELaiN assistant crafts Python snippets, freeing bioinformaticians from boilerplate coding tasks and demonstrating tangible AI productivity gains.

Price, however, is no longer the primary battleground. Buyers evaluate data-interoperability, instrument-driver libraries, and the speed with which vendors issue patches addressing evolving cybersecurity threats. Ecosystem openness—reflected in RESTful APIs and pre-built connectors to mass spectrometers, chromatography systems, and data-visualization tools—often tips RFP decisions. Consequently, even dominant players must sustain aggressive road-map cadence or risk displacement by more nimble entrants as feature parity compresses.

Electronic Laboratory Notebook (ELN) Industry Leaders

Thermo Fisher Scientific Inc.

LabWare

Bruker

Benchling

LabVantage Solutions Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Siemens AG completed its USD 5.1 billion acquisition of Dotmatics, integrating AI-powered scientific software into its Xcelerator portfolio

- April 2025: Semaphore Solutions secured fresh capital from Cypress Ridge to expand Labbit, a BPMN-driven workflow and graph-database platform for regulated labs

- January 2025: Leica Biosystems and Indica Labs announced a joint investment to develop an AI-enabled digital pathology suite spanning biomarker discovery through routine diagnostics

Global Electronic Laboratory Notebook (ELN) Market Report Scope

As per the scope of the report, an electronic laboratory notebook or ELN is a software tool that, in its most basic form, replicates an interface, much like paper in a paper lab notebook. The implementation of ELN enables effective management of huge amounts of data from a remote place. The Electronic Laboratory Notebook (ELN) Market is Segmented by product, delivery mode, license, end-use and geography. Based on product the market is segmented as, cross-disciplinary, and specific. Based on delivery mode the market is segmented as, on-premise, and web-hosted/ cloud-based. Based on license the market is segmented into proprietary, and open. Based on end-use the market is segmented as the pharmaceutical and biopharmaceutical industry, life science research laboratory, and others. The report also covers the market sizes and forecasts for the electronic lab notebook market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Cross-disciplinary ELN |

| Specific/Domain ELN |

| Proprietary |

| Open-source |

| Web/ Cloud-based |

| On-premise |

| Pharmaceutical & Biotechnology Companies |

| Contract Research Organisations (CROs) |

| Academic & Research Institutes |

| Food & Beverage Industry |

| Petrochemical, Oil & Gas Industry |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Cross-disciplinary ELN | |

| Specific/Domain ELN | ||

| By License Type | Proprietary | |

| Open-source | ||

| By Deployment Mode | Web/ Cloud-based | |

| On-premise | ||

| By End User | Pharmaceutical & Biotechnology Companies | |

| Contract Research Organisations (CROs) | ||

| Academic & Research Institutes | ||

| Food & Beverage Industry | ||

| Petrochemical, Oil & Gas Industry | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the electronic lab notebooks market?

The electronic lab notebooks market is valued at USD 512.45 million in 2026 and is set to climb to USD 707.37 million by 2031.

Which deployment mode is growing fastest?

Web or cloud-based deployments hold 68.12% share today and are expanding at a 7.75% CAGR, reflecting heightened comfort with secure, off-premise data management.

Why are CROs adopting ELNs faster than pharmaceutical sponsors?

CROs must manage multiple client projects under strict data-segregation rules, making scalable, multitenant ELNs critical; this need drives an 8.25% CAGR for the segment.

What role does AI play in modern ELNs?

AI transforms ELNs from passive logs to active assistants by drafting protocols, analyzing anomalies, and generating code snippets, thereby reducing experiment cycle times and error rates.

How important is regulatory compliance in ELN selection?

Extremely; platforms that provide out-of-the-box 21 CFR Part 11 and EU Annex 11 features shorten validation timelines and mitigate costly inspection findings.

Page last updated on: