Laboratory Information Management System Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 595.62 Million |

| Market Size (2030) | USD 946.24 Million |

| Growth Rate (2025 - 2030) | 9.70% CAGR |

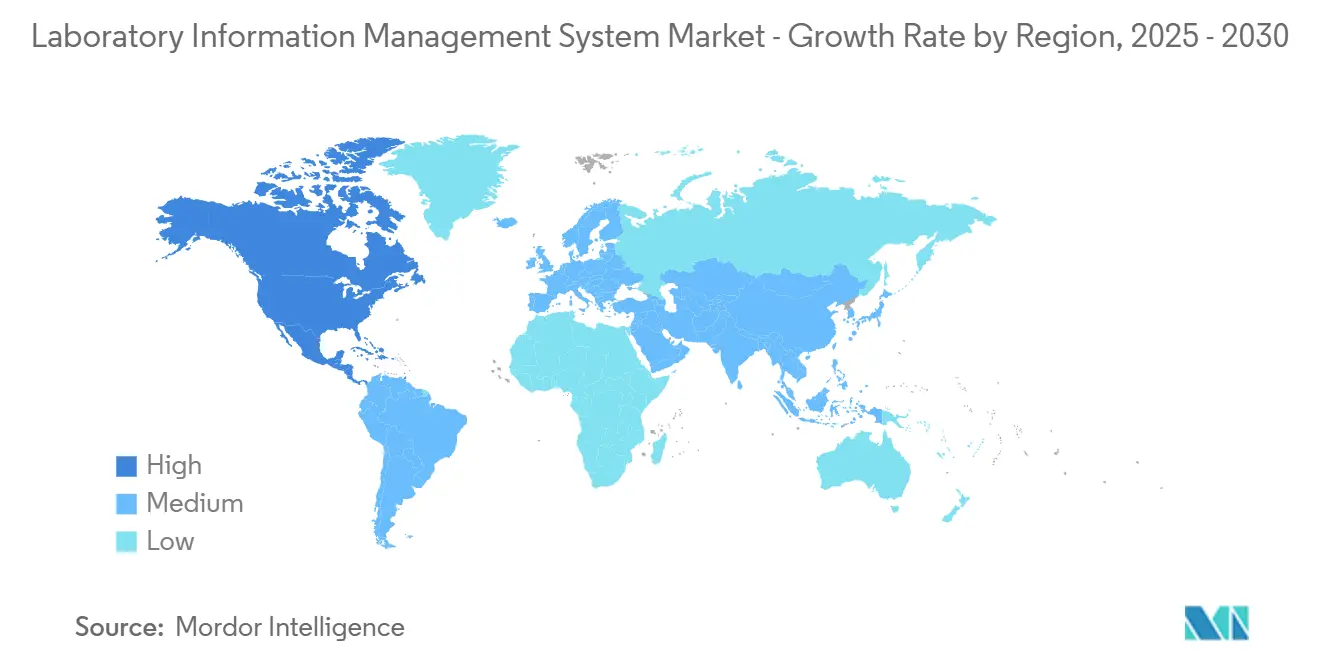

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Laboratory Information Management System Market Analysis by Mordor Intelligence

The laboratory information management system market size reached USD 595.62 million in 2025 and is projected to climb to USD 946.24 million by 2030, reflecting a 9.7% CAGR. This momentum springs from sustained digitalization across research and quality-driven laboratories, where end-to-end data traceability now sits at the core of regulatory inspections. Growth also benefits from artificial-intelligence workflows that convert raw assay data into decision-ready insights, freeing scientists from repetitive curation tasks. Heightened demand for remote sample oversight, born out of pandemic-era decentralization, keeps investment focused on platforms that offer mobile accessioning, automated chain-of-custody, and real-time analytics. Providers that bundle LIMS, scientific data management, and electronic laboratory notebooks into unified cloud offerings continue to widen adoption by removing silo-bound workflows. Finally, the fast-rising volume of genomic, biobanking, and cell-therapy samples reinforces the value proposition of systems that secure data integrity from collection to long-term archival.

Key Report Takeaways

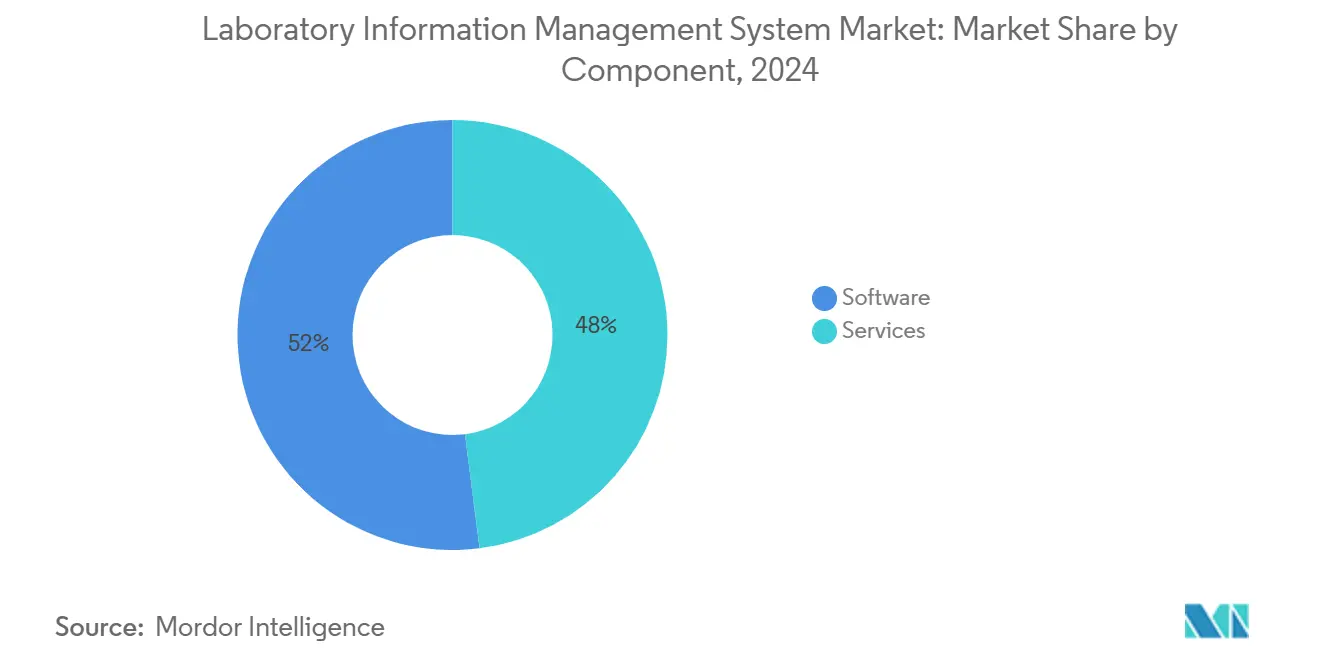

- By component, services captured 52% of laboratory information management system market share in 2024, while cloud-native software revenues are forecast to expand at a 10.8% CAGR through 2030.

- By deployment model, on-premise installations led with 55% revenue share in 2024; cloud/SaaS is projected to advance at a 10.2% CAGR between 2025-2030.

- By product type, broad-based platforms held 63% of the laboratory information management system market size in 2024; pharma-specific solutions are expected to grow at 10.5% CAGR to 2030.

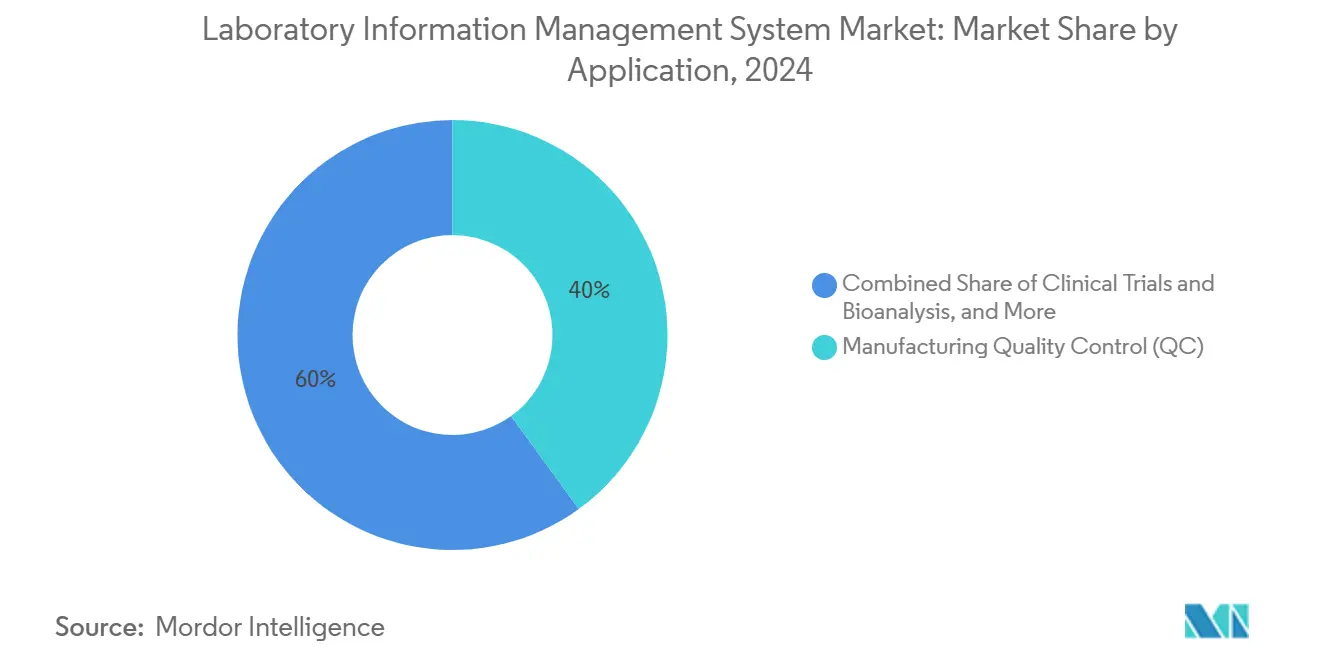

- By application, manufacturing quality control accounted for 40% of the laboratory information management system market size in 2024, whereas cell & gene therapy labs are set to expand at a 10.9% CAGR over the same horizon.

- By geography, North America maintained 35% share of the laboratory information management system market size in 2024, while Asia-Pacific is forecast to post an 11.3% CAGR through 2030.

- By end user, pharmaceutical and biotech companies generated 48% of revenue in 2024, with CRO/CDMO customers anticipated to grow at a 10.8% CAGR to 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Laboratory Information Management System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid growth of pharmaceutical & biotech R&D pipeline | +2.3% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Growing demand for biobanking | +1.8% | Global with focus on North America & Europe | Long term (≥4 years) |

| Rising adoption of contract research and manufacturing outsourcing | +1.5% | Global; strongest uptake in Asia-Pacific, North America, Europe | Medium term (2-4 years) |

| AI-enabled genomic-testing workflows | +2.7% | North America, Europe, emerging Asia-Pacific | Medium term (2-4 years) |

| Rapid expansion of decentralized clinical trials | +1.9% | Global | Short term (≤2 years) |

| Precision-agriculture soil microbiome testing | +1.2% | North America, Europe, Australia | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth of Pharmaceutical & Biotech R&D Pipeline

Global drug-development programs now exceed 20,000 active candidates, a figure 38% higher than in 2020. Each new molecule multiplies laboratory data volumes, intensifying the need for scalable LIMS that automate contextualization and audit trails. Platforms equipped with AI-driven outlier detection are shortening data-review cycles by 43% in quality-control labs, freeing analyst capacity and accelerating batch release [1]Thermo Fisher Scientific, “Pharmaceutical LIMS,” thermofisher.com. Seamless integration of LIMS with electronic notebooks and scientific data hubs breaks down informational barriers, letting multidisciplinary teams interrogate datasets from discovery through scale-up without manual exports. This capability speeds go/no-go decisions and supports adaptive trial designs that cut overall development timelines.

Growing Demand for Biobanking

More than 70% of precision-medicine programs depend on biorepositories that safeguard consented samples across decades. Modern systems pair IoT-enabled freezer monitoring with event-driven alerts that avert temperature excursions. Barcode-centred inventory in leading institutions has trimmed retrieval times by 67% while eliminating count discrepancies [2]LabWare, “Laboratory Software for Bio-Banking and Clinical Research Labs,” labware.com.Blockchain-anchored chain-of-custody is entering production environments, providing immutable provenance logs critical for gene-therapy samples whose usage rights link directly to donor consent. These advanced features elevate LIMS from passive record-keepers to proactive guardians of specimen integrity.

AI-Enabled Genomic-Testing Workflows

Sequencing labs processing upwards of 500,000 samples yearly rely on AI to slash variant-interpretation time by up to 85%. Embedded machine-learning engines continuously refine classification accuracy by correlating genetic findings with clinical outcomes. One flagship deployment taps algorithmic run-scheduling that aligns instrument capacity with reagent stocks and clinical urgency, boosting throughput without expanding headcount. Tight coupling of LIMS and bioinformatics pipelines eliminates file-transfer bottlenecks, producing regulatory-ready reports that trace each analytical step back to the accession barcode.

Rapid Expansion of Decentralized Clinical Trials

Remote sampling now features in 60% of new trials, compelling sponsors to track specimens that travel from patients’ homes to dispersed laboratories. Smartphone apps linked to the central LIMS capture collection metadata and initiate secure chain-of-custody in real time. Such connectivity lifted participant retention to 97% in a recent Singapore study while lowering the logistics carbon footprint. When paired with eCOA systems, these capabilities provide an end-to-end view of efficacy, safety, and compliance metrics that supports mid-trial protocol adjustments without risking data integrity.

Precision-Agriculture Soil-Microbiome Analysis

Field agronomists are harnessing LIMS to correlate microbial fingerprints with yield data, enabling site-specific nutrient recommendations. Platforms integrate GPS-tagged soil samples, next-generation sequencing reads, and weather feeds to build machine-learning models that predict crop performance. Early adopters report sizeable fertilizer reductions and resilience against drought stresses, underlining how informatics accelerates the transition toward regenerative farming [3]Scispot, “The Laboratory Data Platform Built for 2025’s Data-Driven Labs,” scispot.com.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High total cost of ownership & prolonged validation | -1.6% | Global, higher impact in emerging markets | Medium term (2-4 years) |

| Data security and sovereignty concerns | -1.2% | Europe, Asia-Pacific, Middle East | Medium term (2-4 years) |

| Interoperability challenges with legacy laboratory information systems & heterogeneous instrument interfaces | -1.4% | Global | Medium term (2-4 years) |

| Scarce bioinformatics talent | -1.9% | Global, acute in emerging markets | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Ownership and Prolonged Validation

Enterprise deployments may exceed USD 1 million in license fees and require validation periods that stretch 6–9 months, delaying return on investment. A Vermont public-health lab documented a USD 1.7 million spend covering customization and maintenance. Subscription-priced SaaS options mitigate capital outlay yet still confront conservative quality-assurance teams reluctant to outsource infrastructure. Vendors are countering with prevalidated templates that shorten qualification cycles and bundled managed-services contracts that cap lifetime costs.

Data Security and Sovereignty Concerns

Regulations such as GDPR and sector-specific data-localization laws mandate that personally identifiable and genomic data remain within defined borders. Laboratories in pharmaceuticals and diagnostics often default to on-premise architectures to guarantee compliance, slowing cloud migration despite clear operational gains. Private-cloud deployments hosted in in-country data centres provide a compromise, but they add complexity around vendor oversight and shared-responsibility models.

Scarce Bioinformatics Talent Slowing Advanced LIMS Uptake

Around 30-40% of informatics roles stay vacant longer than six months, hampering rollouts that rely on cross-disciplinary skill sets spanning laboratory science, software configuration, and data analytics. The regenerative-medicine sector alone forecasts a 600-employee shortfall by 2035 [4]ADC Consulting, “Uncovering Workforce and Skills Gaps in Regenerative Medicine,” adc-consulting.com. As a stopgap, suppliers are embedding low-code workflow builders and guided configuration wizards that allow bench scientists to adjust processes without deep scripting knowledge.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Anchor ROI Amid Growing Software Flexibility

The laboratory information management system market recorded services commanding 52% revenue in 2024, underscoring laboratories’ reliance on external expertise for validation, integration, and continuous refinement. These engagements often extend for multiple years, ensuring workflows evolve with regulatory updates and new instrumentation. In parallel, demand for cloud-native subscriptions is accelerating at 10.8% CAGR, encouraged by elastic scaling and automatic feature rollouts that avoid interruption to bench activities. Service providers are broadening portfolios to include validation-as-a-service and AI-model stewardship, giving clients turnkey access to capabilities otherwise constrained by talent gaps. This pattern illustrates how software utility is maximized only when paired with strategic domain guidance that aligns system configuration with evolving scientific aims.

Second-generation managed-service models increasingly assume responsibility for algorithm training and performance monitoring, creating recurring revenue streams that mirror the software-as-a-service mindset. Laboratories appreciate predictable expenditure and quicker time-to-value, especially when tackling novel modalities such as single-cell sequencing. Several vendors now embed outcome-based pricing that links service fees to quantified efficiency gains, a structure that encourages ongoing optimization rather than one-off implementation milestones. The laboratory information management system market therefore rewards suppliers able to combine configurable platforms with consultative depth that navigates both technology and compliance landscapes.

By Deployment Model: Cloud Gains Ground Without Displacing On-Premise Mainstays

On-premise systems retained 55% of 2024 revenue because heavily regulated facilities favour direct control over infrastructure, validation scripts, and data-access policies. However, the cloud cohort is forecast to grow 10.2% CAGR as laboratories seek remote accessibility and lighter IT overhead. Hybrid designs that mirror familiar workstation UIs while storing data in sovereign clouds provide an acceptable bridge, satisfying auditors yet permitting elastic compute for analytics bursts. For smaller labs, cloud subscriptions slash capital outlay and compress deployment into weeks, democratizing best-practice workflows once confined to big-pharma budgets.

Operational experience gained during pandemic lockdowns demonstrated the resilience of browser-based access, prompting even conservative quality leaders to pilot SaaS sandboxes for non-GxP functions. As confidence builds, production workloads migrate, often beginning with stability studies or environmental monitoring modules before moving critical release assays. Over time, the laboratory information management system market is expected to show a converged architecture in which edge appliances handle instrument ingestion while regulatory-grade copies reside in regional cloud vaults, ensuring both latency control and compliance.

By Product Type: Broad Platforms Dominate as Vertical Solutions Accelerate

Broad-based suites accounted for 63% of 2024 spend thanks to their ability to map diverse disciplines—from analytical chemistry to microbiology—into a single data backbone. They appeal to multi-site enterprises pursuing harmonized workflows and consolidated analytics dashboards. Yet pharma-centric packages, tracking a 10.5% CAGR, capitalize on preconfigured processes such as stability pull scheduling, batch genealogy, and electronic signatures compliant with 21 CFR Part 11. These out-of-the-box templates shorten validation timelines and free resources for scientific tasks. The laboratory information management system market therefore balances universality with niche precision, allowing organizations to match functionality depth with risk tolerance and resource availability.

Artificial-intelligence modules are becoming standard differentiators. Broad suites incorporate anomaly detection across varied test panels, whereas vertical offerings position AI toward context-specific predictions such as potency trends or deviation root-cause analysis. Providers that refine models on anonymized, domain-specific data demonstrate higher accuracy and faster time-to-insight, adding competitive weight to their propositions.

By Enterprise Size: Modular Architectures Serve Both Global Networks and Emerging Labs

Large networks invest in multi-language, multi-site instances that enforce enterprise master data and enable centralized oversight of method performance. They rely on configurable role-based access and interface gateways linking manufacturing execution, ERP, and electronic batch records to create a unified informatics ecosystem. Conversely, startups and regional labs favour light-footprint SaaS plans with pay-as-you-grow licensing, allowing expansion from a handful of users to hundreds without re-platforming. When Timor-Leste’s national microbiology lab adopted a cloud solution, weekly throughput rose from under 80 to 178 samples while transcription errors fell sharply.

Modern architectures permit incremental module activation, so smaller facilities can begin with sample reception and reporting before layering on instrument interfaces, stability testing, or advanced analytics. This staged approach aligns expenditure with maturity, ensuring sustained adoption. Suppliers offering packaged industry templates further expedite go-live timelines, converting complex best-practice workflows into guided configurations.

By Application: QC Workhorses Hold Lead; Advanced Therapies Accelerate

Manufacturing quality control represented 40% of 2024 revenue, reflecting stringent batch-release requirements across biopharma, food, and specialty chemicals. High-volume assays demand robust specification libraries, automated instrument calibration checks, and instant certificate of analysis generation—all core strengths of mature LIMS modules. Meanwhile, cell & gene therapy laboratories clock a 10.9% CAGR as patient-specific products surge through clinical pipelines. These facilities need tight chain-of-identity tracking from leukapheresis to final dose, integration with MES, and support for variable-volume sampling inherent in autologous processes.

Unified QC-MES platforms reduce production hold times by pushing real-time assay results to shop-floor dashboards, enabling immediate disposition decisions and minimizing inventory costs. In discovery spaces, drug-screening labs benefit from integrated chemical-registration, dose-response modeling, and AI-driven hit triage, expediting lead optimization. Biobanking modules expand footprint by embedding consent tracking and longitudinal sample metadata, supporting multi-omics correlation studies central to precision medicine.

By End User: Pharma & Biotech Dominate, while Outsourcing Specialists Outpace

Pharmaceutical and biotechnology firms delivered 48% of 2024 revenue, anchored by their need to satisfy stringent regulatory frameworks and manage complex analytic portfolios spanning discovery to commercial release. Contract research and manufacturing organizations, propelled by 10.8% CAGR, implement multi-tenant LIMS that segregate client data and support sponsor-specific reporting. This capability is critical as outsourcing now encompasses roughly half of global clinical trials. Academic institutions turn to LIMS for reproducibility and grant-mandated FAIR data principles, while hospitals integrate informatics with EHR systems to shorten diagnostic turnaround and support precision oncology services.

Geography Analysis

North America generated the largest share of laboratory information management system market revenue in 2024 at 35%, underpinned by extensive pharmaceutical R&D investment and a mature ecosystem of informatics vendors and integrators. Regulatory scrutiny from agencies such as the FDA prioritizes data integrity, pressing laboratories to maintain comprehensive audit trails and electronic signatures that LIMS deliver. Integration of AI for proactive quality monitoring is progressing rapidly, with leading manufacturers deploying predictive analytics that flag potential deviations before release-blocking events occur. High adoption of precision medicine, coupled with reimbursement pathways for genomic testing, further stimulates demand for platforms that capture sequencing data and patient consents within unified records.

Asia-Pacific registers the fastest trajectory, with an 11.3% CAGR projected through 2030. Regional expansion of vaccine and biologics manufacturing in China and India is paired with government incentives encouraging digital transformation of laboratory infrastructure. Contract research organizations operating in Singapore and South Korea deploy LIMS to demonstrate Good Laboratory Practice compliance, winning contracts from multinational sponsors seeking cost-effective yet quality-assured partners. Japan’s national genomics initiatives integrate privacy-centric consent workflows, making LIMS central to ethical data stewardship. Meanwhile, Australian agri-tech stakeholders adopt soil-microbiome informatics in support of sustainable-farming imperatives, extending LIMS penetration beyond healthcare.

Europe maintains a sizable footprint driven by stringent data-protection regulations and a robust biopharma manufacturing base. GDPR influences system design, mandating region-locked data residency and granular consent management. Pharmaceutical laboratories integrate LIMS with Qualified Person release systems, ensuring traceability from raw material intake through final product certification. The continent’s extensive biobanking network leverages specialized modules for longitudinal sample tracking and cross-border data exchange within pan-European research consortia. Post-Brexit divergence of U.K. regulatory codes triggers configuration projects to meet Medicines and Healthcare products Regulatory Agency guidelines, generating fresh service revenue for implementation partners.

Competitive Landscape

The top five vendors collectively hold roughly 57% of revenue, placing the laboratory information management system market in a moderately concentrated state. Long-established providers such as Thermo Fisher Scientific, LabWare, and LabVantage command loyalty through broad module libraries and global support teams. Cloud-native challengers like Benchling and Scispot differentiate via rapid API-first integration and modern user experiences aimed at emerging biotech laboratories. Recent acquisitions, including Datacor’s purchase of Baytek and MasterControl’s addition of Qualer, demonstrate strategic moves to deepen vertical capabilities rather than merely expand installed base.

Artificial-intelligence integration stands out as the central battleground. Vendors that embed machine learning for outlier detection, instrument predictive maintenance, and dynamic resource scheduling provide measurable efficiency gains, raising switching barriers. Blockchain-based audit trails gain traction in biobanking and advanced-therapy workflows where immutable provenance is mission-critical. Meanwhile, open-standards advocacy accelerates instrument connectivity, reducing costly custom drivers and encouraging best-of-breed architectures.

Specialized niches continue to attract focused entrants. Soil-microbiome testing, decentralized clinical-trial logistics, and cell-therapy manufacturing each exhibit workflow idiosyncrasies not fully addressed by generic platforms, creating space for purpose-built solutions. Established suppliers respond with template accelerators that adapt core functionality to these domains, striving to preserve account control as clients diversify scientific portfolios.

Laboratory Information Management System Industry Leaders

Abbott Laboratories

LabVantage

LabLynx

McKesson Corporation

Siemens Healthineers AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: MasterControl acquired Qualer, integrating calibration and maintenance tracking into asset workflows to improve end-to-end compliance.

- February 2025: Scispot introduced an enhanced Laboratory Data Platform with API-first architecture and embedded AI aimed at biotech and precision-medicine labs.

- June 2024: Confience acquired Computing Solutions Inc. to bolster LIMS capabilities in chemical and food sectors, accelerating product development.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Laboratory Information Management System (LIMS) market as software-centric platforms, plus related implementation and support services, that laboratories deploy to track samples, automate workflows, store data, and generate compliant reports across life-science, industrial, and public-sector settings.

Scope exclusion: the assessment deliberately omits narrower clinical Laboratory Information Systems (LIS) that interface directly with hospital HIS/EMR modules.

Segmentation Overview

- By Component

- Software

- Services

- By Product Type

- Broad-based / Multi-purpose LIMS

- Pharma-specific LIMS

- By Deployment Model

- On-premise

- Web-hosted

- Cloud-based

- By Enterprise Size

- Large Laboratory Networks

- Small & Medium-sized Laboratories

- By Application

- Drug Discovery & Pre-clinical

- Clinical Trials & Bioanalysis

- Manufacturing Quality Control (QC)

- Biobanking & Sample Tracking

- By End User

- Pharmaceutical & Biotech Companies

- Contract Research / Development & Manufacturing Orgs (CROs / CDMOs)

- Academic Medical & Research Institutes

- Hospital & Clinical Diagnostic Labs

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- GCC

- South Africa

- Rest of Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We complemented desk work with interviews and short surveys targeting QA managers in pharma QC labs, LIMS product leads at regional distributors, CRO IT directors in North America, Europe, and Asia, and independent validation consultants. Their feedback tightened penetration assumptions, price bands, and migration timelines from on-premise to cloud SaaS.

Desk Research

Mordor analysts first collated public data from tier-1 sources such as the U.S. FDA 510(k) database, Eurostat R&D expenditure files, laboratory accreditation lists from ILAC, import-export codes in UN Comtrade, and white papers by trade bodies like the International Society for Biological and Environmental Repositories. Company 10-Ks, instrument vendor investor decks, and peer-reviewed papers on lab automation trends added granularity. Paid repositories, including D&B Hoovers for revenue splits and Dow Jones Factiva for deal flow, filled remaining financial and competitive blanks. The sources cited here are illustrative; many additional references guided data checks and contextual framing.

Market-Sizing & Forecasting

A top-down build started with the global laboratory count by segment and region, reconstructed from accreditation and licensing registries, then multiplied by average LIMS spend curves that vary with bench count and data-compliance tier. Select bottom-up cross-checks, supplier revenue roll-ups and sampled ASP x active license volumes, helped calibrate totals before final reconciliation. Key model drivers include growth in FDA-registered bio-manufacturing sites, average test volume per regulated lab, share of cloud deployments, and annual software maintenance ratios. Forecasts run through a multivariate regression that ties LIMS investment to lab capital budgets, regulatory citation trends, and R&D intensity, with scenario buffers applied where primary experts flagged volatile funding cycles.

Data Validation & Update Cycle

Outputs undergo variance screening against external spending benchmarks; anomalies are escalated to a senior analyst panel. The dataset refreshes each year, with interim revisions if material events, major M&A, new GMP mandates, or abrupt currency swings, shift baseline assumptions.

Why Mordor's Laboratory Information Management System Baseline Earns Decision-Maker Confidence

Published values often differ because firms choose wider informatics bundles, apply blanket price points, or refresh less frequently.

Key gap drivers we observe include bundled inclusion of LIS and ELN modules, aggressive cloud uptake scenarios, one-size ASP application across regions, and less frequent currency rebaselining.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 595.6 million | Mordor Intelligence | - |

| USD 2.88 billion | Global Consultancy A | Combines LIMS with LIS and broader lab software stack; applies uniform global ASP |

| USD 2.63 billion | Industry Journal B | Counts hardware services and multi-year maintenance upfront; five-year refresh cadence |

These comparisons show how Mordor's narrower, software-only lens and annual update rhythm yield a grounded, transparent baseline that clients can trace back to verifiable lab counts and spend ratios rather than sweeping aggregates.

Key Questions Answered in the Report

How big is the Laboratory Information Management System Market?

The Laboratory Information Management System Market size is expected to reach USD 595.62 million in 2025 and grow at a CAGR of 9.70% to reach USD 946.24 million by 2030.

What is the current Laboratory Information Management System Market size?

In 2025, the Laboratory Information Management System Market size is expected to reach USD 595.62 million.

What is driving the strong CAGR in the laboratory information management system market?

Growing digitalization of laboratory workflows, regulatory emphasis on data integrity, and adoption of AI-enabled analytics are combining to generate a 9.7% CAGR through 2030.

Which component segment leads current revenue?

Services lead with 52% share in 2024 due to the need for validation, integration, and ongoing optimization support.

Which application area is expanding fastest?

Cell & gene therapy laboratories, with a 10.9% CAGR, are adopting LIMS to manage patient-specific chain-of-identity and integrate with manufacturing execution systems.

Page last updated on: