United States Laboratory Informatics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

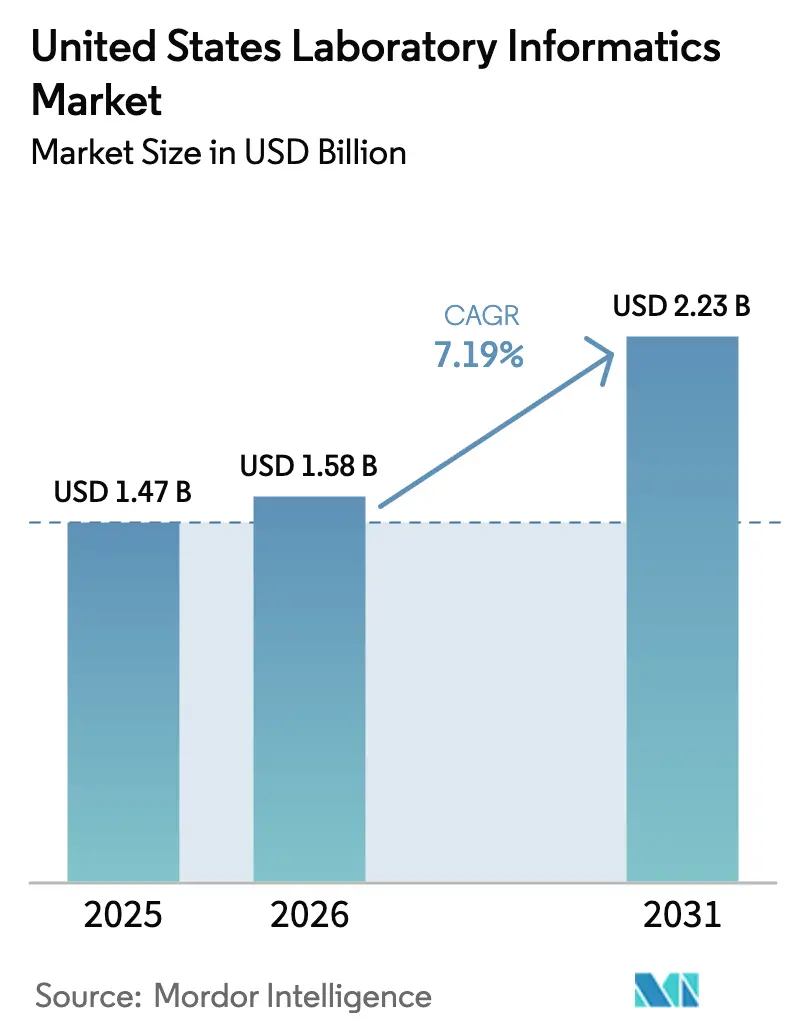

| Base Year Market Size (2025) | USD 1.47 Billion |

| Market Size (2026) | USD 1.58 Billion |

| Market Size (2031) | USD 2.23 Billion |

| Growth Rate (2026 - 2031) | 7.19% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Laboratory Informatics Market Analysis by Mordor Intelligence

The United States laboratory informatics market size is expected to grow from USD 1.47 billion in 2025 to USD 1.58 billion in 2026 and is forecast to reach USD 2.23 billion by 2031 at 7.19% CAGR over 2026-2031. Robust spending on digital science platforms, stricter federal oversight and the growing need to harmonize vast data streams are sustaining this upward trajectory. The market’s momentum is further reinforced by rising adoption of cloud-native solutions, consolidation of testing networks, and continuous advances in analytics that help laboratories shorten cycle times, improve quality metrics and comply with increasingly complex regulations. Vendor competition is intensifying as global suppliers expand their software-as-a-service portfolios, while newer entrants differentiate through artificial-intelligence-enabled applications that target niche workflows. End-user priorities have also shifted: regional health systems are re-platforming legacy systems to centralize data governance, whereas contract research organizations (CROs) invest in flexible informatics stacks to accelerate outsourced discovery and clinical operations. These combined drivers indicate lasting demand resilience in the United States laboratory informatics market through the end of the decade.

Key Report Takeaways

- By product type, laboratory information management systems led with 54.12% of the United States laboratory informatics market share in 2025, whereas electronic lab notebooks are poised for the fastest CAGR of 8.85% to 2031.

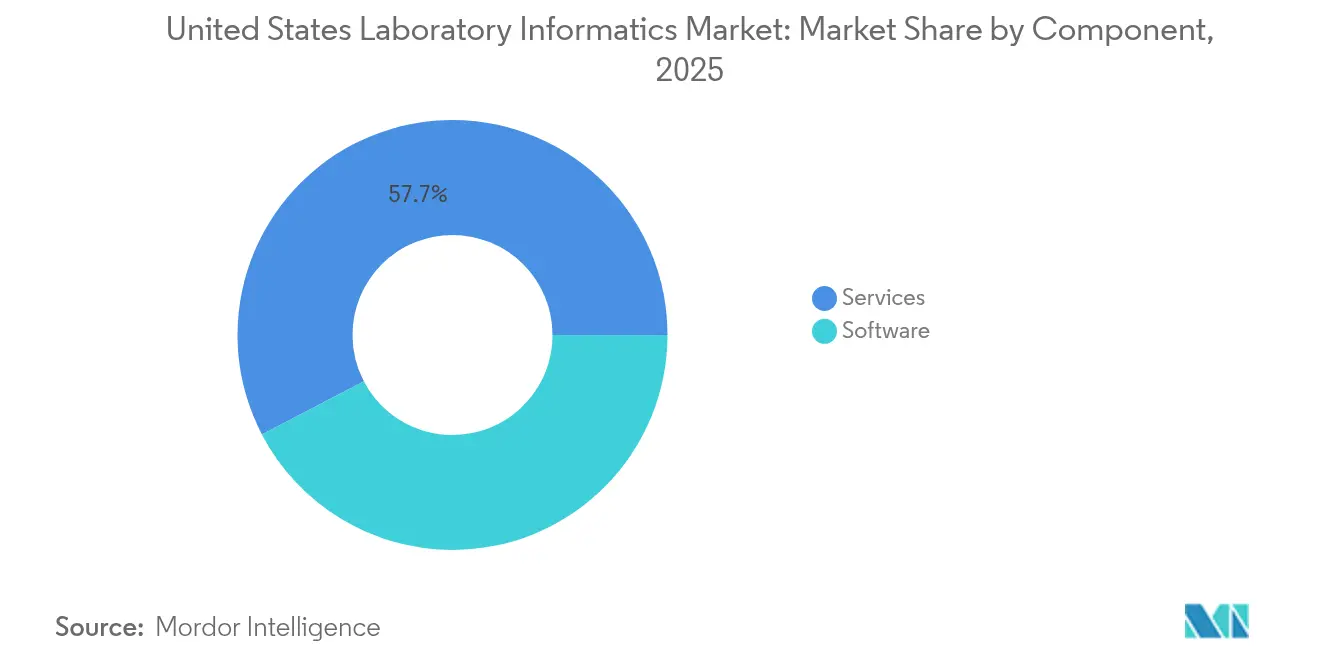

- By component, services accounted for 57.65% of the United States laboratory informatics market size in 2025; software is projected to expand at the highest rate of 8.22% over the forecast window.

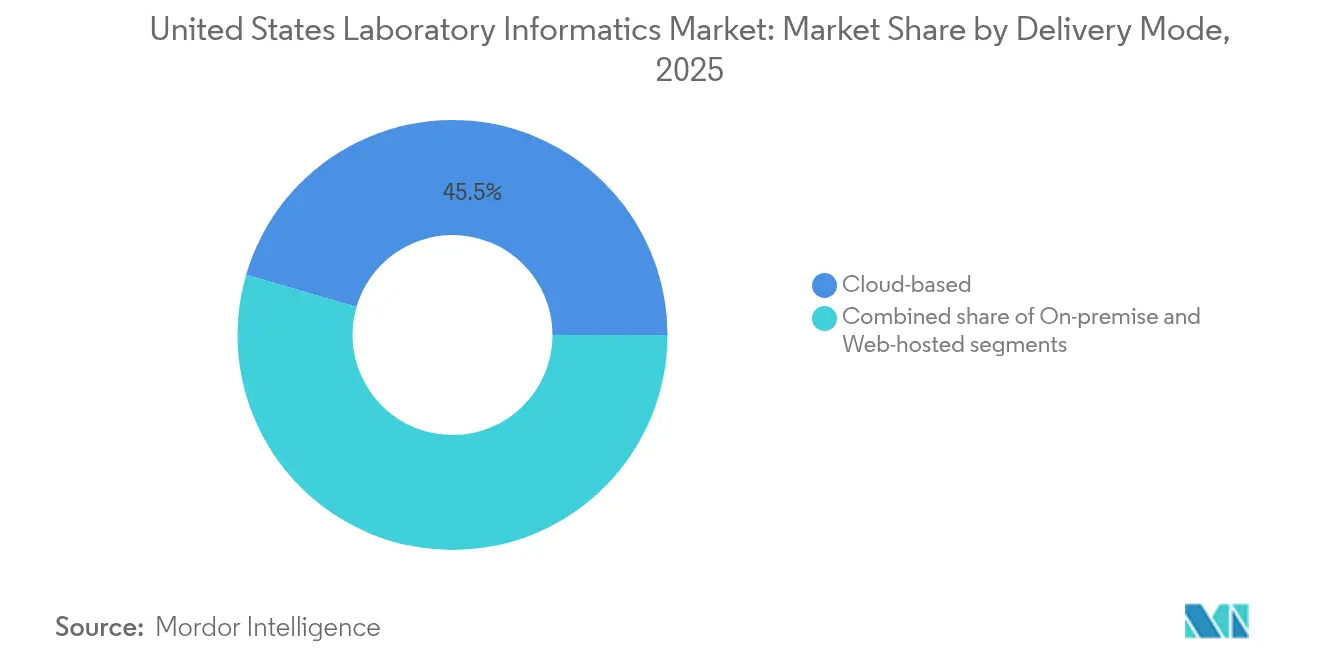

- By delivery mode, cloud-based solutions captured 45.48% revenue share of the United States laboratory informatics market in 2025 and continue to record the strongest growth momentum of 8.6%.

- By end user, pharmaceutical and biotechnology companies held 40.62% of the United States laboratory informatics market size in 2025, while CROs post the quickest CAGR of 8.55% through 2031.

- Thermo Fisher Scientific, LabWare and Abbott together retained the largest collective position, underscoring moderate concentration across the supplier landscape.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with United states representing one among them. The global report on laboratory informatics market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

United States Laboratory Informatics Market Trends and Insights

Drivers Impact Analysis*

| Drivers Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging laboratory data volume & complexity | +2.1% | National, concentrated in research hubs (Boston, San Francisco, San Diego) | Medium term (2-4 years) |

| Stricter regulatory & quality compliance mandates | +1.8% | National, emphasis on FDA-regulated industries | Short term (≤2 years) |

| Expansion of biopharma R&D and precision medicine | +1.5% | National, focused in biopharma clusters | Medium term (2-4 years) |

| Rapid shift toward cloud-based & SaaS platforms | +2.3% | National | Short term (≤2 years) |

| Consolidation of laboratories driving workflow standardization | +1.2% | National, emphasis on clinical diagnostics sector | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Laboratory Data Volume & Complexity Across Life Sciences and Healthcare

Laboratories across the United States generate exponentially larger data sets as high-throughput sequencing, mass spectrometry and multiplex imaging become standard. Traditional point solutions struggle to process multiformat files, leading to duplicated effort and information silos. Integrated informatics platforms able to ingest, contextualize and analyze unstructured and structured outputs are therefore in high demand. Organizations that implemented enterprise-wide systems reported faster hypothesis testing and cross-functional collaboration gains[1]Matt Grulke, “Leveraging an Enterprise Laboratory Informatics Platform to Maximize Scientific Data Advantage,” Chromatography Online, chromatographyonline.com. These outcomes highlight why the United States laboratory informatics market continues to scale, particularly among discovery labs needing real-time analytics for decision support.

Stricter U.S. Regulatory & Quality Compliance Mandates (CLIA, FDA 21 CFR Part 11, GMP)

Regulation remains a central catalyst. Enhanced FDA scrutiny of data integrity now spans device submissions and laboratory developed tests (LDTs). The agency’s May 2024 rule reclassified LDTs as medical devices and introduced a phased enforcement schedule starting July 2024[2]U.S. Food and Drug Administration, “Medical Devices; Laboratory Developed Tests: Final Rule,” federalregister.gov. Laboratories must therefore implement validated, auditable and access-controlled systems to secure electronic records. Compliance costs rise, yet informatics providers that embed e-signatures, version control and audit-trail functionality benefit from accelerated uptake. Consequently, the United States laboratory informatics market experiences sustained purchasing activity among diagnostics providers seeking to mitigate regulatory risk.

Expansion of Biopharma R&D and Precision Medicine Initiatives

Growth in monoclonal antibody pipelines and personalized therapeutics amplifies the need for interoperable digital ecosystems capable of managing complex bioprocess data. Machine-learning applications in antibody discovery shorten screening cycles and enhance yield prediction accuracy, thereby reducing manufacturing expense[3]Thanh Tung Khuat et al., “Applications of Machine Learning in Antibody Discovery,” Computers and Chemical Engineering, doi.org. Heavy R&D investments from established and emerging entities drive broader platform deployments, reinforcing the outlook for the United States laboratory informatics market.

Consolidation of Laboratories Driving Demand for Workflow Standardization & Efficiency

Health-system mergers and national reference-lab networks require unified informatics frameworks to harmonize protocols across dispersed sites. Standardized workflows boost sample-throughput consistency and simplify quality audits, prompting multi-site deployments. The resulting enterprise deals enlarge average contract values and contribute incrementally to United States laboratory informatics market revenue.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capital & integration costs | -1.4% | National, greater impact on small/mid-sized labs | Short term (≤2 years) |

| Data security & patient-privacy concerns | -1.0% | National | Short term (≤2 years) |

| Fragmented legacy systems lacking interoperability standards | -0.9% | National, emphasis on established healthcare institutions | Medium term (2-4 years) |

| Shortage of skilled Lab-IT professionals for complex implementations | -0.8% | National, more pronounced in non-metropolitan areas | Long term (≥5 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital & Integration Costs for Enterprise-Scale Deployments

Full-function LIMS rollouts entail extensive configuration, instrument interfacing and validation that can surpass existing IT budgets. Although SaaS eases hardware burdens, integration of bespoke workflows still requires expert services, slowing decisions by resource-constrained organizations. This cost hurdle trims short-term uptake across parts of the United States laboratory informatics market but is expected to moderate as modular subscription offerings mature.

Data Security & Patient-Privacy Concerns in Cloud Environments

Healthcare breaches remain a headline risk; 80.0% of incidents in 2023 stemmed from hacking, exposing 133 million records. Laboratories migrating to cloud architectures must therefore demonstrate encryption, access control and incident-response readiness. The FDA’s March 2024 draft guidance amplifies cybersecurity expectations for medical-device sponsors. Vendors that present rigorous security certifications win greater trust within the United States laboratory informatics market, yet residual concerns continue to temper migration speed.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Product: LIMS Dominates While ELN Accelerates

Laboratory Information Management Systems anchor 54.12% of the United States laboratory informatics market share in 2025 because they orchestrate sample tracking, batch release and regulatory documentation with high reliability. Demand remains steady among quality-control and diagnostic facilities that rely on audit-ready workflows. At the same time, Electronic Lab Notebooks exhibit the fastest expansion curve of 8.85% as R&D users pivot away from paper to searchable, cloud-hosted records. The United States laboratory informatics market size attributable to ELN solutions is projected to more than double over the coming decade, reflecting their growing role in safeguarding intellectual property and fostering collaboration. Complementary platforms such as scientific data-management systems and chromatography data systems sustain relevance by capturing instrument outputs directly into structured repositories, lowering transcription errors and easing review cycles. Vendors are gradually adopting an ELN-centric integration model that provides a single interface to initiate, monitor and validate end-to-end scientific workflows, thereby streamlining user training and decision support.

Second-generation enterprise content-management modules and laboratory execution systems now appear more frequently in bundled proposals as organizations seek to unify document control, SOP management and e-signature compliance within the same ecosystem. These add-ons strengthen revenue diversification for suppliers and create upsell pathways that reinforce the stickiness of the United States laboratory informatics market.

Component: Services Lead While Software Gains Momentum

Implementation, validation and maintenance services comprise 57.65% of 2025 revenue because most laboratories lack in-house configuration expertise and must outsource system setup. As cloud adoption rises, however, incremental growth tilts toward software subscriptions. Continuous delivery models allow vendors to push new analytics features without extensive customer revalidation, fostering agile updates that align with evolving regulatory guidelines. Lower up-front fees also democratize access for medium-sized research organizations, broadening the installed base across the United States laboratory informatics market.

Services remain indispensable. Multi-site chain consolidations, for instance, require professional consulting to harmonize data dictionaries and reconcile differing SOPs. Yet rising automation in deployment scripting and pre-configured templates is expected to narrow labor hours per project, gradually transferring a larger share of wallet to recurring software income streams.

Delivery Mode: Cloud-Based Solutions Reshape the Landscape

At 45.48% share, cloud delivery now represents the single largest deployment model. Laboratories cite seamless scalability, automatic disaster-recovery and predictable OPEX budgeting as decisive factors. Vendors’ growing library of secure APIs accelerates instrument connectivity, eliminating onsite middleware boxes while cutting integration complexity. Consequently, the United States laboratory informatics market witnesses accelerated displacement of aging on-premise instances, though certain high-containment and government facilities still favor local hosting to maintain air-gapped environments. Web-hosted private-cloud models fill this middle ground by offering dedicated infrastructure with external support, serving as a transitional step for institutions with phased modernization roadmaps.

End User: Pharma & Biotech Lead While CROs Surge

Pharmaceutical and biotechnology companies generated 40.62% of the 2025 United States laboratory informatics market size as they depend on compliant electronic records to underpin Investigational New Drug filings. Large molecule pipelines, cell-and-gene therapy platforms and increasingly complex analytics prompt these firms to adopt modular informatics suites that integrate upstream process data with clinical outcome metrics. CROs, however, demonstrate the fastest CAGR because small and mid-cap sponsors outsource more development tasks. Data-capture harmonization between electronic data-capture (EDC) tools and LIMS shortens site-monitoring effort, evidenced by a 50% time reduction and USD 150,000 per-site savings reported at a leading cancer center. Government reference laboratories and academic research institutes round out demand, often prioritizing grant-funded digital-lab modernization that emphasizes open APIs and flexible licensing.

Geography Analysis

The United States laboratory informatics market displays notable regional variation. The Northeast corridor, anchored by Boston and New York, hosts dense clusters of pharmaceutical R&D and elite academic centers that routinely pilot emerging informatics capabilities. California’s Bay Area and San Diego echo similar patterns, with venture-backed biotechs adopting cloud-native ELN and LIMS platforms from inception to shorten scale-up timelines. These coast-to-coast strongholds represent the highest per-site spending levels, thus accounting for a disproportionate share of total United States laboratory informatics market revenue.

Midwestern states, including Illinois and Minnesota, increasingly invest in central laboratory networks linked to expansive health-system mergers. Consolidation drives uniform data standards across tertiary hospitals and outreach labs, stimulating enterprise-wide procurement contracts. The Southeast experiences accelerated adoption in large academic medical centers that integrate precision-medicine programs. Collectively, these shifts underscore that while high-density innovation hubs remain primary contributors, secondary regions are moving rapidly up the digital-maturity curve, diversifying the geographical revenue base of the United States laboratory informatics market.

Competitive Landscape

Thermo Fisher Scientific, LabWare, Inc. and Abbott command prominent positions through broad software portfolios, deep domain expertise and global support footprints. Their emphasis on secure cloud hosting, microservices architectures and embedded compliance tooling resonates with regulated users. Mid-tier specialists such as Scispot appeal to early-stage biotechs seeking low-code configurability and cost-flexible SaaS subscriptions. Strategic deals shape competitive dynamics: Certara’s 2024 acquisition of ChemAxon enhanced cheminformatics depth and integrated property-prediction algorithms, reinforcing its modeling strengths. Overall, supplier rivalry revolves around faster deployment, AI-driven analytics and verticalized templates that cut validation time.

A secondary differentiation vector is cybersecurity. Vendors tout ISO 27001 certification, end-to-end encryption and secure DevOps pipelines to reassure customers wary of headline breaches. Market share shifts are therefore likely to correlate with demonstrated resilience and rapid response capability. Consolidation is expected to persist as larger players acquire niche innovators to plug portfolio gaps, maintaining moderate concentration across the United States laboratory informatics market.

United States Laboratory Informatics Industry Leaders

Thermo Fisher Scientific Inc.

LabWare Inc.

Abbott

LabVantage Solutions Inc.

Agilent Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: LabWare unveiled LabWare ASSURE, a SaaS suite featuring ready-to-use workflows that shorten validation cycles and embed compliance checkpoints.

- January 2025: Memorial Sloan Kettering reported eSource deployment cut site staff effort by 50% and trimmed per-site costs by USD 150,000, spurring wider adoption of EDC-LIMS integration.

- December 2024: Roche LabLeaders survey revealed heightened executive focus on cybersecurity, prompting budget shifts toward encryption and security posture assessments.

- October 2024: Certara finalized ChemAxon acquisition, integrating cheminformatics tools to assemble a unified model-informed drug-development data backbone.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the United States laboratory informatics market as all licensed software and related services, including Laboratory Information Management Systems, Electronic Lab Notebooks, Scientific Data/Content Management, Laboratory Execution, and Chromatography Data systems that capture, manage, and analyze scientific data generated inside clinical, life-science, and industrial laboratories.

Hardware peripherals, standalone automation robots, and generic analytics platforms that are not purpose-built for laboratory workflows are excluded.

Segmentation Overview

- By Product

- Laboratory Information Management System (LIMS)

- Electronic Lab Notebooks (ELN)

- Enterprise Content Management (ECM)

- Laboratory Execution System (LES)

- Chromatography Data System (CDS)

- Scientific Data Management System (SDMS)

- Electronic Data Capture (EDC) & Clinical Data Management System (CDMS)

- By Component

- Services

- Software

- By Delivery Mode

- On-premise

- Web-hosted

- Cloud-based

- By End User

- Pharmaceutical & Biotechnology Companies

- Contract Research Organizations (CROs)

- Other End Users

Detailed Research Methodology and Data Validation

Primary Research

Interviews and structured surveys with lab IT managers, quality directors, CRO informatics leads, and independent consultants across the Northeast, Midwest, South, and West validated adoption drivers, average selling prices, implementation timelines, and cloud migration pace. Responses clarified gray areas in secondary material and fed directly into assumption tuning.

Desk Research

Our analysts mined public datasets issued by agencies such as the Centers for Medicare & Medicaid Services, the Clinical Laboratory Improvement Amendments registry, and the Food & Drug Administration, alongside trade bodies including the American Association for Clinical Chemistry and the BioInnovation Organization.

Supplemental context came from peer-reviewed journals, SEC 10-Ks, investor decks, and news archives hosted on Dow Jones Factiva and D&B Hoovers.

These sources anchored foundational metrics, including lab counts, test volumes, R&D outlays, and regulatory filings.

The list above is illustrative; many other open and paid references were examined during data gathering and cross-checking.

Market-Sizing & Forecasting

A top-down build starts with the total number of CLIA-certified and industrial labs, multiplied by penetration ratios for each informatics module and calibrated average contract values. Supplier roll-ups and sampled ASP multiplied by volume checks provide bottom-up ballast.

Key variables like pharma R&D spend, biologics clinical-trial starts, cloud-based LIMS share, regulatory update cadence (FDA 21 CFR Part 11), and average interface fee erosion flow into a multivariate regression forecast that projects value through 2030.

Where bottom-up estimates under- or over-shoot, gaps are bridged using scenario analysis bounded by primary research consensus.

Data Validation & Update Cycle

Outputs pass three layers of anomaly and variance review before sign-off.

Model signals are re-benchmarked against fresh lab certification counts, spending trackers, and earnings calls each quarter.

Full report refresh occurs annually, with interim revisions triggered by material policy or technology shifts.

United States Laboratory Informatics Baseline-Why Our Commands Confidence

Published figures often diverge because firms select different scope, cost components, refresh cadences, and currency conversion points.

By aligning scope strictly to licensed software and services, using current-year lab universe counts, and updating variables every twelve months, Mordor Intelligence delivers a balanced baseline that clients can reliably plug into budgeting models.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.47 B (2025) | Mordor Intelligence | - |

| USD 1.32 B (2024) | Regional Consultancy A | Narrow product list; excludes cloud support fees |

| USD 1.12 B (2024) | Trade Journal B | Uses historical ASPs and five-year refresh cycle |

These comparisons show that lower estimates usually stem from omitting services or relying on older pricing. Our disciplined variable selection and annual refresh provide a transparent, reproducible view that decision-makers can trust.

Key Questions Answered in the Report

What is the current value of the United States laboratory informatics market?

The market is worth USD 1.58 billion in 2026 and is projected to reach USD 2.23 billion by 2031 at a 7.19% CAGR.

Which product type dominates spending?

Laboratory Information Management Systems account for 54.12% of United States laboratory informatics market share due to their pivotal role in regulated sample and workflow control.

Why are cloud-based deployments gaining traction?

Cloud platforms convert capital expenditure to operating expense, provide elastic storage and automate updates, supporting faster compliance and collaboration.

Which end-user group is growing the fastest?

Contract research organizations are expanding quickest as small biopharma sponsors outsource a larger share of discovery and clinical operations.

How is stricter FDA regulation influencing demand?

New rules such as the LDT reclassification increase the need for validated electronic record systems, thereby accelerating informatics investments.

What security measures are laboratories prioritizing when selecting informatics vendors?

Buyers emphasize ISO 27001 certification, end-to-end data encryption, multi-factor authentication and documented incident-response protocols to protect sensitive patient and research information.

Page last updated on: