Electronic Flight Bag (EFB) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 3.03 Billion |

| Market Size (2030) | USD 4.38 Billion |

| Growth Rate (2025 - 2030) | 7.65% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electronic Flight Bag (EFB) Market Analysis by Mordor Intelligence

The electronic flight bag (EFB) market size is valued at USD 3.03 billion in 2025 and is projected to reach USD 4.38 billion by 2030, growing at a 7.65% CAGR; this outlook highlights the expanding EFB market amid rising cockpit digitalization and safety mandates. Airlines, MROs, and regulators view integrated EFB platforms as catalysts for paperless operations, lower fuel burn, and more accurate compliance records, enabling aviation stakeholders to streamline data flows across flight planning, maintenance, and crew training. The growing adoption of AI-driven analytics, fast broadband connectivity, and cloud-hosted document libraries is accelerating the EFB market as operators shift from hardware-centric procurement toward recurring software subscriptions. Competitive reshuffling, highlighted by Boeing’s 2024 divestiture of Jeppesen and ForeFlight, signals an increasing interest in private equity in software-heavy business models that promise high margins and predictable cash flows. At the same time, supply-chain constraints on rugged tablets and semiconductors complicate near-term hardware deliveries. Yet, these headwinds are offset by strong demand from Asia-Pacific fleets and regulatory harmonization between the FAA and EASA, reinforcing a steady growth trajectory for the EFB market.

Key Report Takeaways

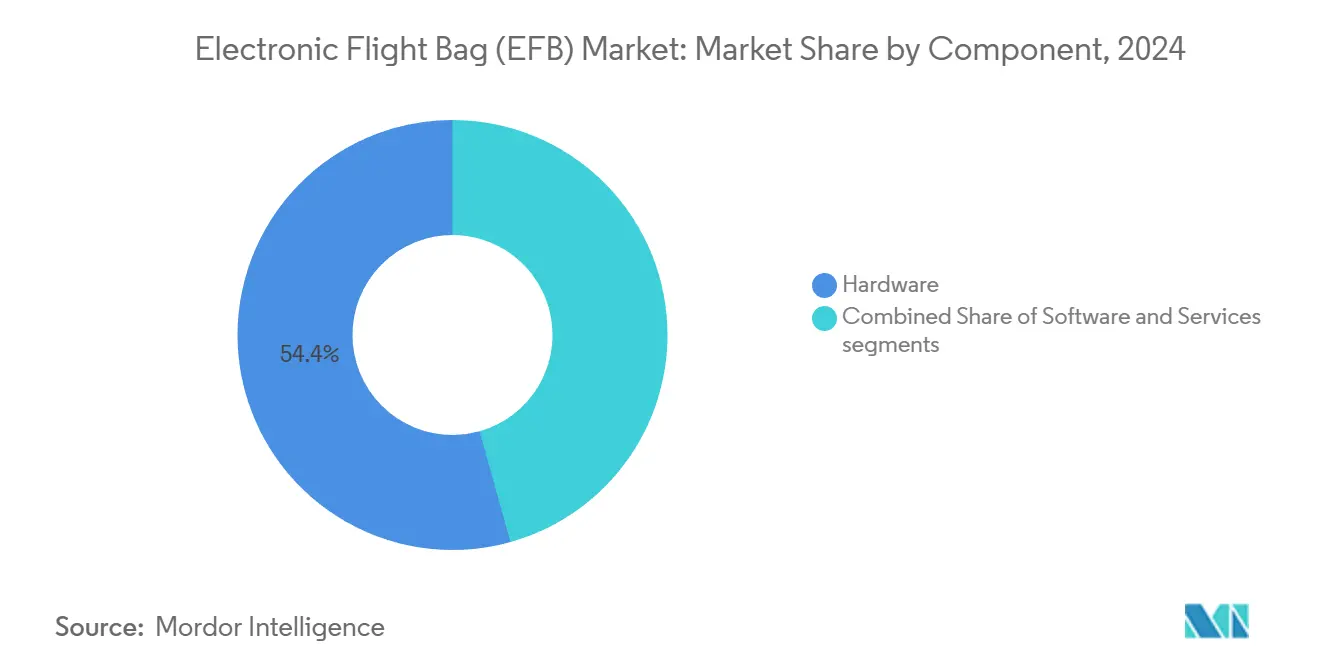

- By component, hardware accounted for 54.35% of the EFB market share in 2024, while software is projected to advance at the fastest 8.98% CAGR through 2030.

- By platform, commercial aviation held 65.81% of the EFB market in 2024, whereas general aviation is expected to expand at an 8.12% CAGR over the same period.

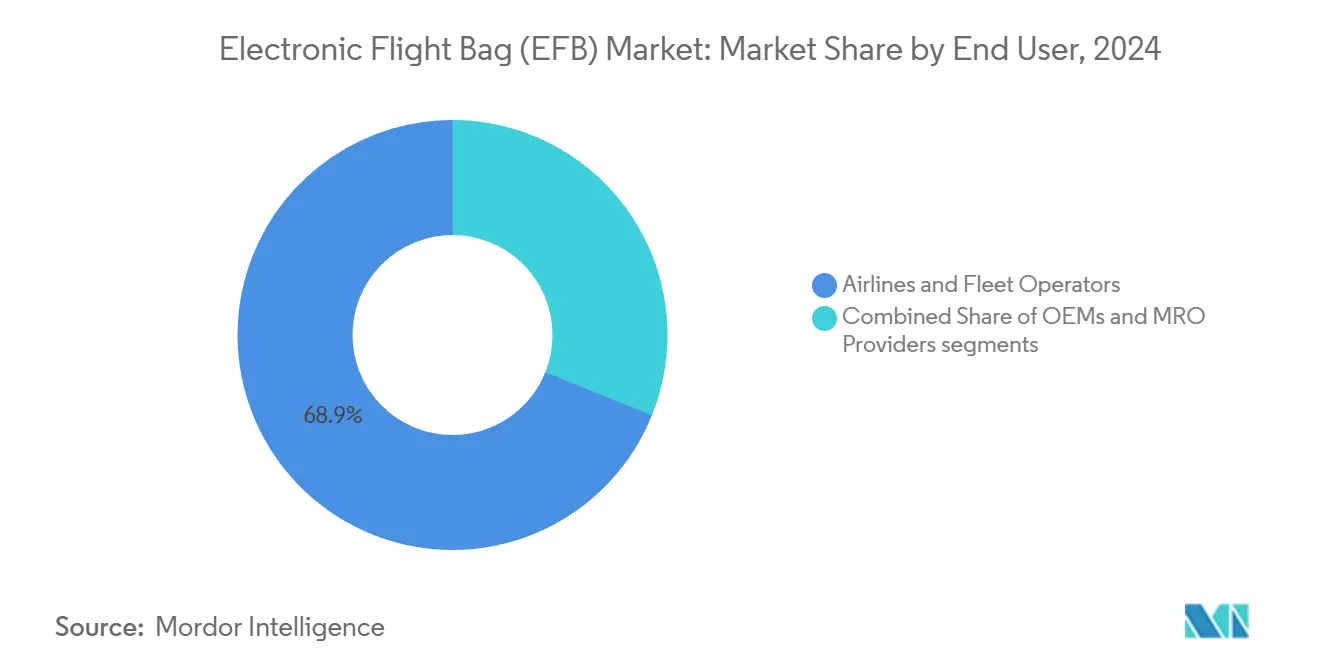

- By end user, airlines and fleet operators captured 68.92% of revenue in 2024; MRO providers are forecasted to post the highest 8.75% CAGR to 2030.

- By connectivity, connected systems commanded 71.98% of the EFB market size in 2024 and will continue to grow at a 7.91% CAGR through 2030.

- By geography, North America led with 32.66% revenue share in 2024, while Asia-Pacific is projected to register the strongest 9.32% CAGR to 2030.

Global Electronic Flight Bag (EFB) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global regulatory adoption of enhanced flight safety mandates | +1.2% | Global | Medium term (2-4 years) |

| Digital transformation of cockpits through EFB and paperless operations | +1.1% | North America and Europe, expanding to APAC | Short term (≤ 2 years) |

| Next-generation avionics modernization and system interoperability | +0.9% | Global | Long term (≥ 4 years) |

| Increased use of commercial tablets in flight decks | +0.8% | North America and APAC | Short term (≤ 2 years) |

| Shift toward predictive safety through real-time flight analytics | +0.7% | Global | Medium term (2-4 years) |

| Sustainability imperatives driving paperless and lightweight avionics | +0.6% | Europe-led, global expansion | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Adoption of Enhanced Flight Safety Mandates

Updated guidance, such as FAA AC 120-76E in 2024, eases approval of Class 1 and Class 2 EFB applications while preserving stringent safety thresholds, prompting airlines to hasten fleet-wide rollouts. EASA’s Safety Information Bulletin 2024-14 mirrors this momentum by standardizing electronic chart accuracy tests and smoothing cross-border certifications. Secure-data requirements are now embedded in many regulatory frameworks, aligning EFB approval with broader cybersecurity rulemaking under ICAO SARPs. Such regulatory clarity transforms EFBs from optional aids into core components of modern safety management systems, adding 1.2 percentage points to the forecasted CAGR. Harmonized rules accelerate procurement decisions across major carriers in North America, Europe, and rapidly expanding Asia-Pacific fleets.

Digital Transformation of Cockpits Through Paperless Operations

Airlines accelerate digitalization as unified EFB suites integrate flight planning, weather briefs, and real-time maintenance logs; easyJet’s 2025 program covering 346 aircraft exemplifies this shift.[1]AviationPros Staff, “easyJet to Digitize Onboard Aircraft Technical Log,” aviationpros.com Automated version control and cloud-hosted manuals eliminate the need for costly printing, while electronic technical logs streamline defect reporting processes and reduce ground delays. The immediate operational savings, fewer paper kilograms on board, faster dispatch, and precise audit trails have created board-level urgency to adopt digital workflows. Data synchronization between cockpit, dispatch, and MRO back offices reduces clerical errors and supports predictive maintenance scheduling. The driver adds a 1.1 percentage-point uplift to CAGR through tangible cost reductions and sustainability gains that resonate with regulators and investors alike.

Next-Generation Avionics Modernization and System Interoperability

EFB evolution converges with broader avionics upgrades as fast IP connectivity links EFBs with flight management computers, terrain avoidance systems, and ACARS over IP gateways from Collins Aerospace.[2]Collins Aerospace, “ACARS over IP,” collinsaerospace.com Airframes undergoing mid-life retrofits now specify open-architecture bridges that enable EFB apps to pull real-time fuel flow, weather radar, and engine health data directly from onboard sensors. Plug-in software frameworks ensure third-party route optimization or performance monitoring apps operate seamlessly within cockpit ecosystems, expanding EFB value. Integrated architectures foster network effects: every additional system that connects to an EFB multiplies its utility, lengthening replacement cycles for older avionics and encouraging airlines to standardize on single-vendor digital suites.

Increased Use of Commercial Tablets in Flight Decks

Cost efficiency drives airlines and general-aviation pilots toward ruggedized iPads or Android tablets certified as Class 1 EFBs, democratizing advanced capabilities once confined to expensive cockpit-installed units. Consumer-grade supply chains shorten lead times yet expose operators to semiconductor shortages, prompting strategies that combine commercial procurement with supplemental certified docks. Intuitive touch interfaces set new UX benchmarks, influencing even Class 2 designs. Software vendors optimize gesture-based navigation and offline caching to handle remote operations. The trend’s 0.8 percentage-point contribution to CAGR reflects its broad appeal across fleet sizes and regions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising concerns over avionics cybersecurity and data breaches | -0.8% | Global, acute in North America/Europe | Short term (≤ 2 years) |

| Complex and time-intensive certification processes for avionics software | -0.7% | Global | Medium term (2-4 years) |

| Pilot workload saturation and digital system overload | -0.6% | North America and Europe | Medium term (2-4 years) |

| Limited availability of ruggedized tablet hardware amid supply chain volatility | -0.5% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Concerns Over Avionics Cybersecurity and Data Breaches

GPS spoofing demonstrations and proof-of-concept intrusions into popular flight apps have elevated cybersecurity to a board-level risk, compelling airlines to fund penetration testing, network segmentation, and secure-boot firmware.[3]Military & Aerospace Electronics Staff, “Dell and Airbus Deliver Electronic Flight Bag Services,” militaryaerospace.com These controls increase project budgets and elongate deployment timelines, subtracting 0.8 percentage points from CAGR. As EFB platforms integrate deeply with airline data centers, any breach can cascade into dispatch systems or passenger-service portals, amplifying reputational risk and triggering regulator scrutiny.

Complex and Time-Intensive Certification Processes for Avionics Software

Traditional DO-178C verification methods struggle with AI-driven algorithms, resulting in 18–24 month approval cycles and multimillion-dollar validation bills that smaller vendors cannot afford. Uncertainty over acceptable assurance cases for machine-learning modules stalls innovation, slowing new-feature releases and dampening competition. The drag reduces CAGR by 0.7 percentage points during the medium term until harmonized AI guidance matures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Expansion Outpaces Hardware Dominance

The EFB market size linked to hardware stood at a 54.35% revenue share in 2024, driven by steady replacement cycles for tablets, mounts, and connectivity docks installed across narrow and wide-body fleets. Yet software revenues are forecast to climb 8.98% annually through 2030 as cloud-based flight-planning engines, predictive-maintenance dashboards, and AI-driven fuel optimizers become mission-critical for carriers seeking deeper operational insights. Subscription-pricing models underpin recurring cash flow, giving investors confidence in long-term margins. Boeing’s USD 10.55 billion sale of Jeppesen and ForeFlight to Thoma Bravo exemplifies private-equity appetite for scalable SaaS assets that complement commoditized hardware.[4]Boeing Communications, “Thoma Bravo Completes Acquisition of Jeppesen and ForeFlight,” boeing.mediaroom.com

Services, ranging from integration consulting to 24/7 help-desk support, account for the smallest share of the EFB market. Yet, they post steady gains as airlines outsource configuration, cybersecurity audits, and data migration projects. Hardware, as it matures, will deliver resilient revenue as airlines refresh their Class 2 displays to support higher-resolution terrain mapping and 5G modems. Over time, commoditization pressures prompt OEMs to bundle hardware at cost while monetizing advanced analytics layered on top of unified data platforms.

By Platform: General Aviation Scales While Commercial Retains Volume

Due to fleet scale and compliance mandates, commercial airlines generated 65.81% of the EFB market revenue in 2024. Still, general aviation is on track for an 8.12% CAGR as business jet operators and charter providers pursue airline-grade situational awareness at consumer tablet price points. The US Air Mobility Command’s fleet-wide EFB deployment illustrates parallel momentum in military aviation, although security requirements slow the adoption compared to the civilian sector.

ForeFlight and Garmin Pilot have democratized high-fidelity route planning, synthetic vision, and real-time weather overlays for piston twins and turboprops, propelling the EFB market deeper into owner-flown segments. Airline operators, meanwhile, emphasize interoperable ecosystems that link EFBs with flight-operations-quality-assurance tools, crew-scheduling suites, and maintenance ERP stacks, reinforcing their volume leadership.

By End User: MRO Providers Accelerate Digital Logbook Adoption

Airlines and fleet operators represented 68.92% of 2024 revenue. Still, MRO organizations are projected to expand at an 8.75% CAGR as they migrate from paper cards to electronic tech logs that feed predictive-maintenance algorithms. easyJet’s selection of ULTRAMAIN ELB for its 346-aircraft fleet exemplifies this pivot toward integrated maintenance workflows. OEMs leverage linefit programs to embed EFB suites at delivery, thereby capturing aftermarket service agreements that secure long-term software upgrades.

As airframes age, independent MROs seek platform-agnostic EFB modules that interface seamlessly with multiple airline back-office systems. This demand incentivizes vendors to open their APIs, ensuring continuity of maintenance records across operator transitions and lease returns.

By Connectivity: Real-Time Data Exchange Fuels Value Creation

Connected solutions commanded 71.98% of the EFB market size in 2024, and their 7.91% CAGR reflects operator hunger for real-time route adjustments, live NOTAM feeds, and predictive-maintenance alerting. Stand-alone devices persist in military and remote-route applications where security protocols or bandwidth costs restrict perpetual connectivity. Low-Earth-orbit constellations and 5G air-to-ground links will broaden coverage and cut data-transfer costs, inviting even smaller charter firms to join the always-connected mainstream.

Collins Aerospace’s ACARS over IP retrofit package demonstrates how legacy VHF messaging can be migrated to broadband channels, thereby freeing bandwidth for more advanced EFB applications, such as high-resolution radar overlays and live fuel-flow analytics. As connectivity normalizes, airlines will demand cybersecurity-hardened gateways, encouraging vendors to offer turnkey hardware-plus-firewall bundles.

Geography Analysis

North America retained a 32.66% revenue share in 2024, supported by established certification pathways, extensive broadband in-flight connectivity infrastructure, and early-adopter carriers such as Delta and American, which utilize EFB analytics to reduce fuel burn and gate-turn times. Canada’s close alignment with FAA rules accelerates cross-border standardization, while Mexico’s expanding low-cost-carrier segment adopts cost-effective tablet-based EFB kits to bypass legacy paper procedures.

Asia-Pacific is projected to log a 9.32% CAGR to 2030, the fastest among all regions, propelled by China’s forecast for 9,740 aircraft deliveries by 2043 and India’s airport-modernization roadmap. Carriers such as IndiGo and China Eastern are increasingly selecting European EFB suites, like Thales Aviobook, to unify disparate fleet types under a single digital operations umbrella. Southeast Asian LCCs favor modular solutions that scale across mixed fleets and variable route lengths, highlighting price sensitivity but strong appetite for fuel-saving tools.

Europe maintains a significant share, thanks to stringent sustainability regulations that effectively require paperless cockpits and optimal flight path algorithms. Carriers like Ryanair adopt FliteDeck Pro 5.0 to support these mandates while cutting taxi-time emissions. Middle East airlines leverage new-build fleets to install fully connected EFB ecosystems from day one, whereas many African carriers focus on offline-capable solutions because of patchy terrestrial bandwidth. These regional contrasts sustain multiple go-to-market strategies within the broader EFB market.

Competitive Landscape

The electronic flight bag (EFB) market exhibits moderate consolidation, with diversified avionics giants, such as Collins Aerospace (RTX Corporation), Honeywell International, Inc., and Thales Group, integrating EFB modules with their own integrated flight decks. Meanwhile, software-focused contenders such as SITA, Garmin Ltd., and Lufthansa Systems are cultivating leadership in user experience. Thoma Bravo’s 2024 acquisition of Jeppesen and ForeFlight for USD 10.55 billion created a stand-alone powerhouse capable of investing heavily in AI analytics and cybersecurity frameworks, thereby intensifying competitive pressure on niche vendors.

Smaller specialists thrive in regional airline and charter niches by tailoring workflow forms, MEL integrations, and implementing military-grade encryption to meet local requirements. Yet rising certification costs and cybersecurity expectations may spur further consolidation as airlines gravitate toward suppliers with robust regulatory affairs resources. Strategic moves in 2025 feature Collins Aerospace expanding ACARS over IP capacity and ULTRAMAIN scaling ELB deployments across European LCCs, underscoring a technology race centered on real-time data exchange and predictive analytics.

Pricing models continue to shift from perpetual licenses to subscription tiers that bundle continuous data updates, threat intelligence feeds, and 24/7 support. Vendors differentiate themselves via open-API ecosystems that enable airlines to plug EFB outputs into flight-operations-quality-assurance dashboards or enterprise resource-planning suites, creating sticky network effects that raise switching costs.

Electronic Flight Bag (EFB) Industry Leaders

The Boeing Company

Honeywell International Inc.

Thales Group

Teledyne Technologies Incorporated

Collins Aerospace (RTX Corporation)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: The UK Ministry of Defence (MoD) awarded Jeppesen UK Limited a direct contract for EFB software that is compatible with existing Jeppesen Foreflight Dispatch systems.

- January 2025: Fokker Services Group (FSG) received an order from SriLankan Airlines to install a new EFB provision solution across its Airbus A320 and A330 fleet. The installation includes a pivot mount, USB-C outlet, and DC-DC converter.

Global Electronic Flight Bag (EFB) Market Report Scope

| Hardware | Class 1 |

| Class 2 | |

| Class 3 | |

| Software | Flight Planning and Dispatch |

| Performance Calculations | |

| Electronic Documents Management | |

| Training and Charting | |

| Services | Integration and Installation |

| Maintenance and Support | |

| Cloud Hosting and Data Analytics |

| Commercial Aviation | Narrowbody |

| Widebody | |

| Regional Jets | |

| Military Aviation | Combat |

| Transport | |

| Special Mission | |

| Helicopters | |

| General Aviation | Business Jets |

| Commercial Helicopters |

| OEMs |

| Airlines and Fleet Operators |

| MRO Providers |

| Connected |

| Stand-Alone |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Component | Hardware | Class 1 | |

| Class 2 | |||

| Class 3 | |||

| Software | Flight Planning and Dispatch | ||

| Performance Calculations | |||

| Electronic Documents Management | |||

| Training and Charting | |||

| Services | Integration and Installation | ||

| Maintenance and Support | |||

| Cloud Hosting and Data Analytics | |||

| By Platform | Commercial Aviation | Narrowbody | |

| Widebody | |||

| Regional Jets | |||

| Military Aviation | Combat | ||

| Transport | |||

| Special Mission | |||

| Helicopters | |||

| General Aviation | Business Jets | ||

| Commercial Helicopters | |||

| By End User | OEMs | ||

| Airlines and Fleet Operators | |||

| MRO Providers | |||

| By Connectivity | Connected | ||

| Stand-Alone | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the electronic flight bag (EFB) market?

The electronic flight bag (EFB) market stands at USD 3.03 billion in 2025.

How fast is the electronic flight bag (EFB) market expected to grow?

The market is forecasted to register a 7.65% CAGR and reach USD 4.38 billion by 2030.

Which region will post the fastest growth in EFB adoption?

Asia-Pacific is projected to expand at a 9.32% CAGR through 2030, driven by fleet expansion in China and India.

Which EFB segment grows quickest by component?

Software revenues are expected to rise at an 8.98% CAGR as airlines shift toward cloud-based platforms and predictive analytics.

What drives MRO demand for electronic flight bag (EFB) solutions?

Maintenance organizations adopt electronic tech logs and real-time defect reporting to reduce ground delays and enable predictive maintenance, fueling an 8.75% CAGR in the segment.

Page last updated on: