Market Overview

| Study Period | 2019 - 2031 |

|---|---|

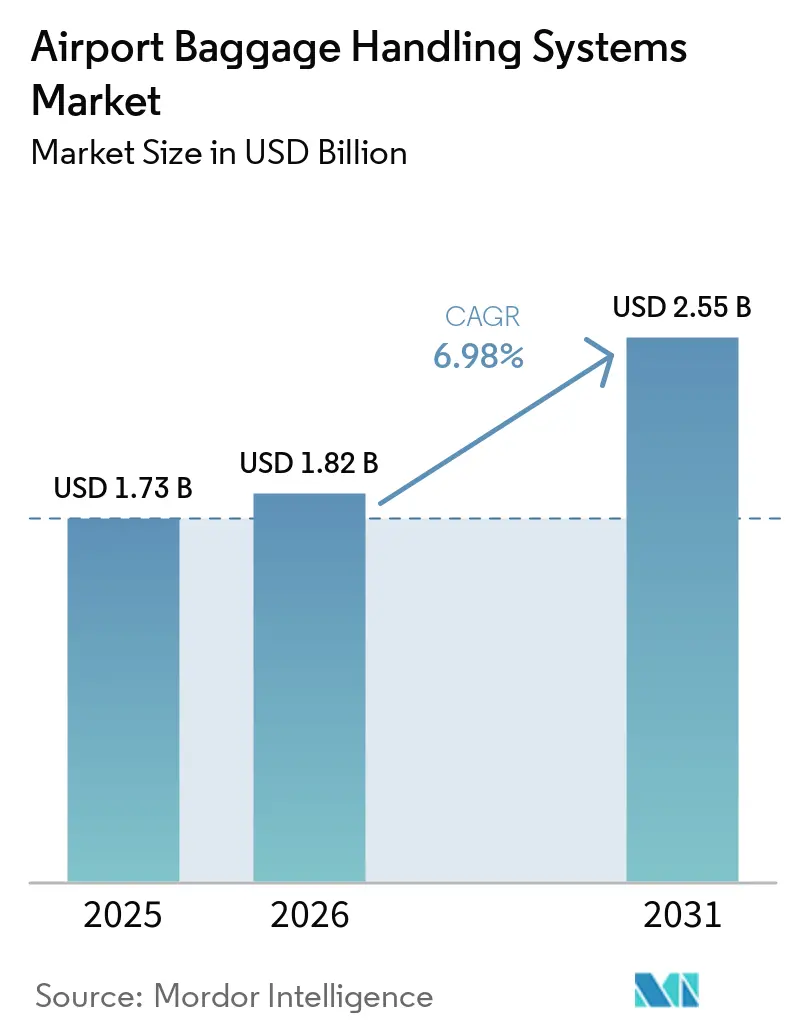

| Market Size (2026) | USD 1.82 Billion |

| Market Size (2031) | USD 2.55 Billion |

| Growth Rate (2026 - 2031) | 6.98% CAGR |

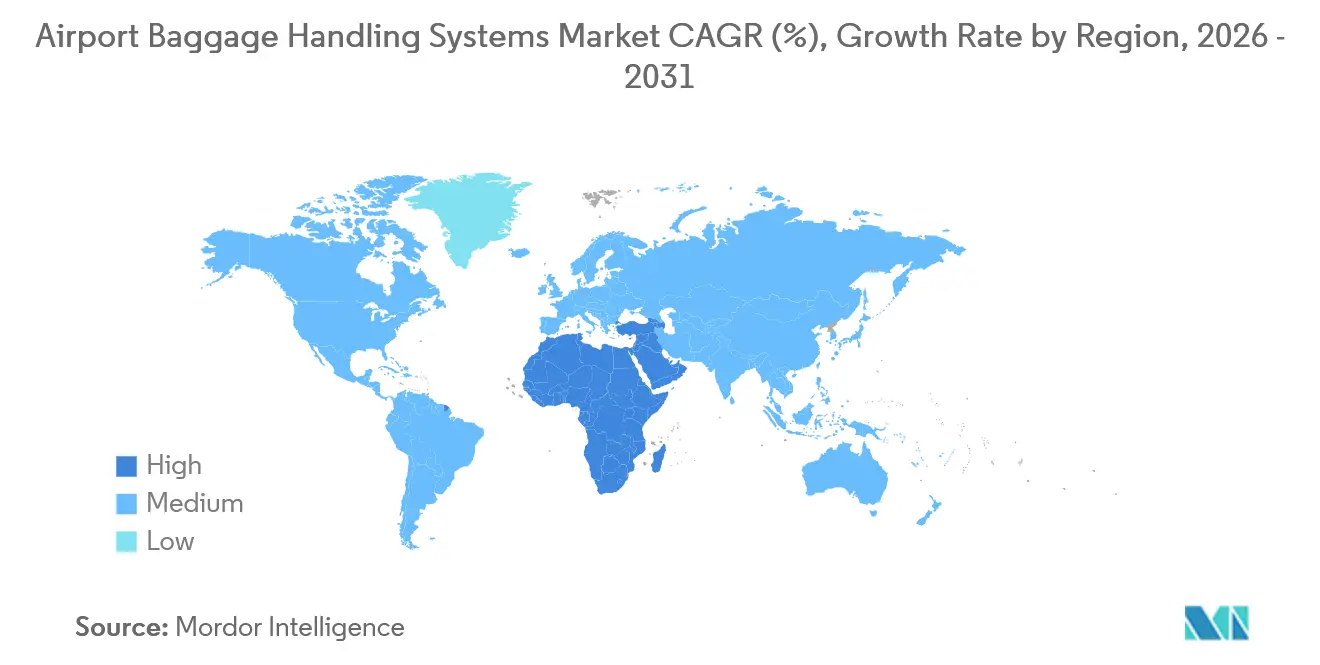

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Airport Baggage Handling Systems Market Analysis by Mordor Intelligence

The airport baggage handling systems market size is expected to grow from USD 1.73 billion in 2025 to USD 1.82 billion in 2026 and is forecast to reach USD 2.55 billion by 2031 at a 6.98% CAGR over 2026-2031. Growth is reinforced by global passenger volumes that surpassed 9.8 billion in 2025, with a long-term trajectory toward 19.3 billion by 2045, a scale that forces airports to replace legacy systems to prevent rising mishandling and delays at peak loads. With load factors at a record 83.8% in 2026, operators have little slack for disruptions, underscoring the operational priority of high-speed sortation, predictive controls, and end-to-end tracking across the airport baggage handling systems market. The industry loses USD 5 billion annually to baggage mishandling at a rate of 6.9 bags per 1,000 passengers, which intensifies the shift toward RFID tracking and data-rich control layers that reduce error rates and support continuous flow. In greenfield megaprojects across the Middle East and Asia, tote-based Individual Carrier Systems with AI-enabled orchestration are now foundational choices. At the same time, North American brownfield projects absorb cost premiums to retrofit similar capabilities into terminals designed around older conveyors. Airports also couple automation with energy management, as seen in run-on-demand conveyor upgrades that cut energy consumption and improve uptime within the airport baggage handling systems market.

Key Report Takeaways

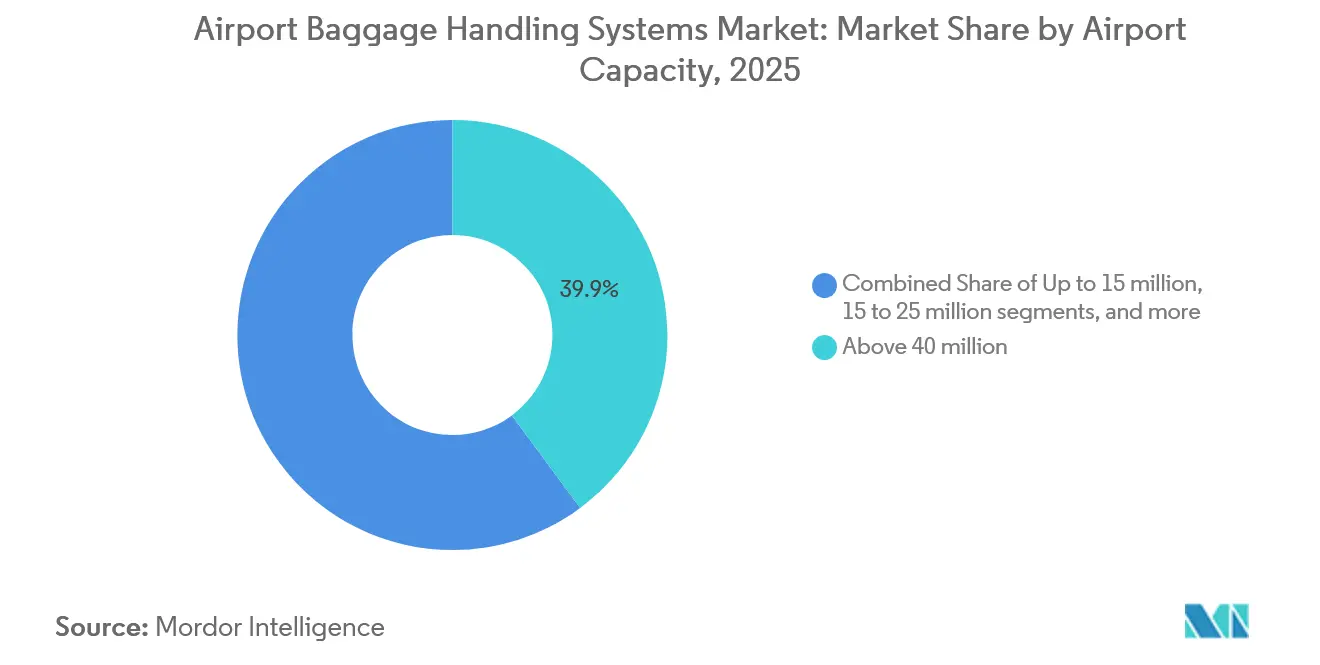

- By airport capacity, airports with over 40 million passengers led with a 39.88% share in 2025, and this segment is forecasted to expand at a 10.25% CAGR through 2031.

- By solution, check-in and ticketing systems held a 31.12% share in 2025, while tracking and tracing recorded the highest projected CAGR at 10.98% during 2026-2031.

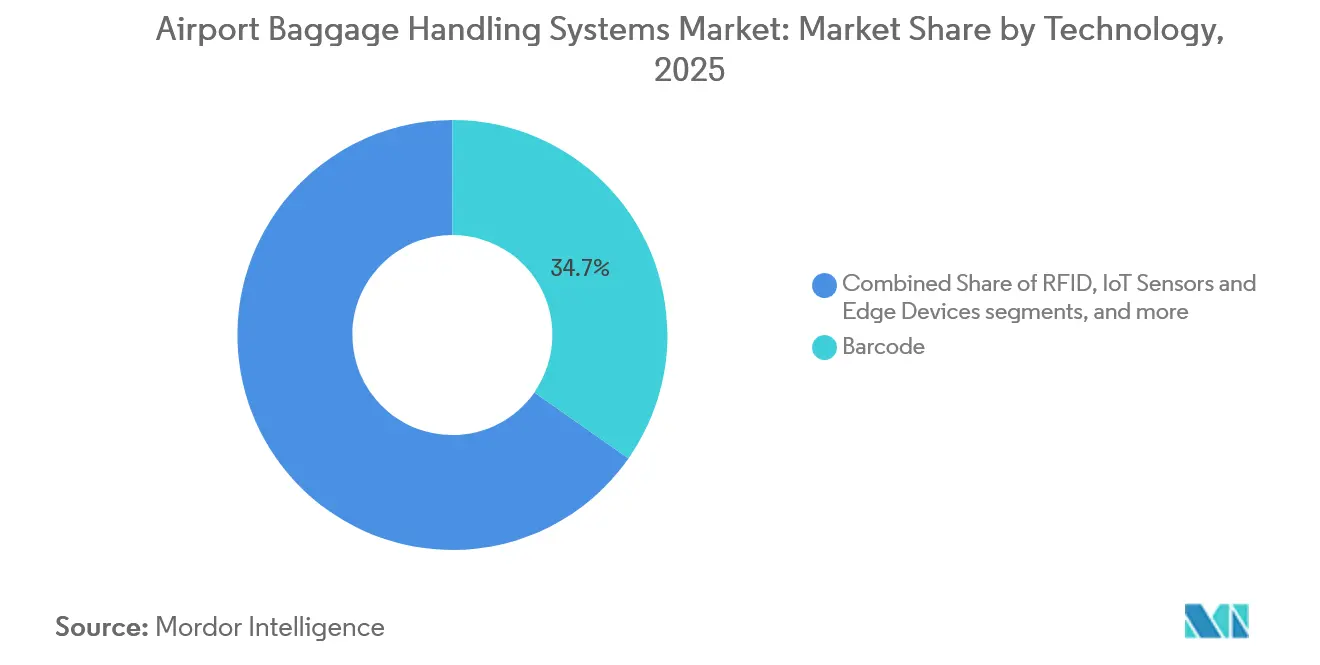

- By technology, barcode systems retained a 34.73% share in 2025, while AI and ML software are projected to grow at an 11.87% CAGR during 2026-2031.

- By system type, conveyor belt systems commanded a 42.61% share in 2025, and hybrid or other emerging systems are forecasted to grow at a 10.18% during 2026-2031.

- By geography, North America held a 31.85% share in 2025, while the Middle East and Africa are projected to grow at a 10.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Airport Baggage Handling Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging global passenger volumes | +2.8% | Global, with acute pressure in Asia-Pacific (4.5% traffic CAGR to 2045) and Middle East (4.3%), moderate in Europe (2.3%), lowest in North America (1.9%) | Medium term (2-4 years) |

| Airport capacity-expansion programs | +2.1% | Middle East and Africa, Asia-Pacific, with spill-over to North American brownfield retrofits | Long term (≥ 4 years) |

| Shift toward integrated RFID tracking | +1.6% | Global, higher adoption in North America and China/North Asia, lagging in Africa | Short term (≤ 2 years) |

| Demand for end-to-end automation | +1.4% | Global, especially Europe, Asia-Pacific, and Middle East, moderate in North America | Medium term (2-4 years) |

| Early-baggage-storage (EBS) as revenue lever | +0.9% | Europe and North America premium airports, transfer-heavy hubs | Short term (≤ 2 years) |

| Pandemic-driven disinfection retrofits | +0.7% | Global, with early adoption in Asia-Pacific and bundling in upgrade programs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Global Passenger Volumes Driving Throughput Demands

Global passenger traffic reached 10.1 billion in 2025 and is projected to reach 19.3 billion by 2045, putting sustained pressure on airport operations and accelerating technology refresh cycles in the airport baggage handling systems market. The mishandling rate of 6.9 bags per 1,000 passengers, which costs the sector an estimated USD 5 billion annually, underlines why airports are scaling tracking and sortation accuracy rather than accepting higher manual workarounds during peaks. With load factors at 83.8% in 2026, carriers leave little slack in aircraft capacity. Hence, baggage halls must absorb volatility through software-driven batching and dynamic rerouting rather than brute-force capacity additions.[1]International Air Transport Association, “Industry Makes Progress to Reduce Baggage Mishandling, New Survey Reveals,” IATA, iata.org Airports are moving from legacy belt-conveyor loops to high-speed platforms and integrated controls that support higher bag-per-hour rates and 24/7 reliability, as seen in US program awards for high-capacity systems with 100% in-line screening. Growth hubs also validate run-on-demand upgrades to curb energy usage and smooth peaks. This pattern keeps the airport baggage handling systems market centered on software intelligence as much as mechanical capacity.

Airport Capacity-Expansion Programs as Catalysts for BHS Investment

Large-scale terminal programs and new hub developments are creating sustained demand for greenfield baggage handling systems in regions that prioritize throughput, digital control, and traceability from the outset, which strengthens long-term adoption dynamics in the airport baggage handling systems market. Mega-hub plans across the Middle East, Africa, and Asia-Pacific are configured around tote-based Individual Carrier Systems and 100% in-line explosive detection, while North American investment centers on phased retrofits that integrate these capabilities into legacy footprints. The retrofit reality includes structural reinforcement for high-speed sorters, staged cutovers to avoid operational downtime, and network-ready control layers engineered for secure segmentation and predictive maintenance. The next investment cycle also aligns with traffic trajectories that remain strongest in Asia-Pacific through 2045, moderate in Europe, and lower in North America, steering near-term system awards toward growth corridors while keeping brownfield upgrades active in mature markets. These dynamics collectively frame a two-track path: new-build gateways leapfrog legacy constraints, while older terminals focus on modernization that enhances resilience, energy efficiency, and compliance at scale within the airport baggage handling systems market.

Shift Toward Integrated RFID Tracking to Meet Regulatory and Operational Imperatives

IATA Resolution 753 has accelerated RFID adoption by requiring tracking at acceptance, loading, transfer, and arrival, which ties compliance directly to lower mishandling and faster recovery when exceptions occur.[2]International Air Transport Association, “IATA Baggage Off-Airport Operations Implementation Guidelines V1 – Dec2024,” IATA, iata.org Trade studies report that RFID delivers near-perfect read accuracy and reduces mishandling, making it a direct lever on cost avoidance and passenger satisfaction in the airport baggage handling systems market. Adoption levels vary by region, with IATA’s 2024 survey indicating stronger airline implementation in China and North Asia and lower penetration in Africa, which shapes deployment priorities at transfer-heavy hubs and large airports. Delta Air Lines’ rollout of hundreds of RFID readers and its gains in hourly bag processing illustrate how end-to-end tracking scales when carriers and airports act in concert. Integrated RFID also enables just-in-time release from EBS systems at mega-airports, reducing congestion around make-up and supporting shorter opening times for flight build processes. Beyond baggage, RFID improves the management of ground support equipment and assets, streamlining daily operations and reducing loss and replacement costs for airport operators.

Demand for End-to-End Automation to Address Labor Shortages and Operational Resilience

Persistent staffing gaps and high turnover have pushed airports toward end-to-end automation to reduce manual handoffs and error risk across functions from self-service bag drop to ULD loading. This shift reinforces sustained technology uptake in the airport baggage handling systems market. Leading integrators outline roadmaps that combine autonomous vehicles, robotic loaders, predictive maintenance, and smart batching to enable airports to handle higher volumes with the same or smaller headcounts while maintaining 24/7 operations.[3]Vanderlande, “Towards a Fully Automated Baggage Hall,” Vanderlande, vanderlande.com European organizations report difficulty attracting and retaining cybersecurity staff, which increases reliance on AI-driven condition monitoring and managed digital services that lower on-site resourcing needs. Automation complements sustainability goals, as run-on-demand conveyor retrofits in major hubs have demonstrated meaningful reductions in energy consumption without sacrificing throughput. Robotics also addresses operator safety by reducing repetitive lifting and strain, which helps airport leaders balance labor negotiations with ergonomic improvements during phased deployments. These combined forces, from labor scarcity to safety and uptime imperatives, keep automation at the center of capital and O&M plans within the airport baggage handling systems market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital expenditure with 10–15 year ROI cycles deterring risk-averse airport authorities | -1.8% | Global, most acute in North America and emerging markets, less constraining in sovereign-backed greenfield projects | Long term (≥ 4 years) |

| Legacy IT infrastructure and interoperability gaps forcing patchwork upgrades | -1.2% | Primarily North America and Europe, with Asia-Pacific new builds bypassing legacy constraints | Medium term (2-4 years) |

| Cybersecurity compliance costs mandated by EU NIS2 and TSA programs | -1.1% | Europe and North America, acute for medium and large airports without in-house security teams | Short term (≤ 2 years) |

| Airport labor unions’ automation pushback and understaffing friction | -0.8% | North America and Europe, minimal resistance in Middle East and some Asia greenfield sites | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure and Extended ROI Cycles as Adoption Barriers

Major baggage handling investments come with long payback periods and complex commissioning, which temper the pace of upgrades despite strong operational cases in the airport baggage handling systems market. Multi-year programs often package high-speed sorters, 100% in-line screening, dynamic storage, and new controls under one contract, as seen in recent US awards for modern high-capacity systems. Brownfield retrofits face an additional complexity premium, including structural reinforcements and cutover staging to avoid service outages that can stretch timelines and elevate contingency budgets. Airports balance these capital needs against regulated aeronautical revenues and municipal financing constraints, which encourage phased scopes and incremental deployment paths in mature markets. In the United States, federal programs help offset select security elements, but funding remains targeted and does not remove the need for multi-year local financing. These factors make sovereign-backed greenfield hubs in high-growth regions more agile in deploying advanced ICS, robotics, and AI orchestration from day one within the airport baggage handling systems market.

Legacy IT Infrastructure and Interoperability Gaps Constraining System Performance

Airports built on legacy control frameworks and older messaging standards often encounter integration hurdles when layering modern analytics, predictive maintenance, and RFID tracking, which slows digital transformation in the airport baggage handling systems market. Patch management and segmentation are more complex in mixed OT and IT environments, and security updates can require downtime that is difficult to schedule at busy hubs. European NIS2 rules and US TSA cybersecurity directives have raised the minimum bar for network segmentation, access control, monitoring, and patching, adding near-term costs and execution complexity for airports without mature in-house cyber teams. Migration from older baggage messaging protocols to modern XML and system-wide data quality improvements also requires airline collaboration, which can extend timelines for predictive flow optimization. Airports are responding with staged upgrades and managed services that keep critical systems available while they harden networks and rationalize software stacks. This staged approach reduces risk but elongates the realization of full digital benefits across the airport baggage handling systems market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Airport Capacity: Mega-Hubs Lead Adoption While Mid-Sized Airports Follow a Phased Path

In 2025, airports processing over 40 million passengers captured 39.88% of the airport baggage handling systems market share. These airports are projected to expand at a 10.25% CAGR through 2031, driven by ongoing technology refreshes and comprehensive digitization. Such extensive operations channel both capital and expertise into systems that maximize bag-handling efficiency and minimize exceptions via complete tracking and automated recovery flows. Leading integrators boast installations in numerous major airports, supported by worldwide service networks and standardized modules that expedite installation timelines and enhance lifecycle support.

Mid-sized airports, catering to 25 to 40 million passengers, prioritize peak smoothing, storage optimization, and compliance-driven tracking. These measures position them for future advancements in sortation and robotics, once they stabilize core performance metrics. Airports handling 15 to 25 million passengers are making notable strides in baggage tracking, indicating a focus on compliance before pursuing further upgrades in throughput and storage capacity. Meanwhile, smaller airports continue to rely on modular conveyors and barcode readers, transitioning to RFID, dynamic storage, and AI-driven controls only when traffic volumes justify such investments.

Major airports are initiating system planning with digital twins, peak simulations, and integrated cybersecurity. This proactive approach minimizes rework and curtails the need for retrofits post-commissioning in the airport baggage handling systems market. Busy US airports are strategically implementing on-demand retrofits and high-speed conveyors to reduce energy costs while improving throughput and reliability. While security funding alleviates some screening costs, local authorities still shoulder significant capital expenditures to modernize structures and networks and achieve resilience targets to safeguard operations during disruptions. Major global airports are trialing autonomous vehicles, robotic loaders, and advanced storage solutions to shorten make-up windows, favoring platforms that prioritize detailed tracking and predictive flow-control orchestration. Such advancements highlight a growing divide: mega-hubs are leading the charge in adopting new technologies within the airport baggage handling systems market, while mid-sized hubs are laying the groundwork for the forthcoming automation wave.

By Solution: Check-In Dominates, Tracking and Tracing Scales Fast on Compliance and Cost Avoidance

Check-in and ticketing systems held a 31.12% share in 2025 as the primary passenger interface, while tracking and tracing is the fastest-growing solution, with a 10.98% CAGR, driven by Resolution 753, airline cost-avoidance priorities, and consumer expectations for real-time status. Tracking improves exception handling and reduces mishandling risk at transfer points, which is critical where load factors remain tight and recovery time is limited. Screening systems retain steady momentum under regulatory mandates, and recent US awards confirm that high-capacity baggage handling now assumes 100% in-line screening as a design premise. Conveying and sortation remain the backbone of daily operations, with upgrades often staged to maintain service continuity and to limit changeovers that would otherwise impact flight schedules. Early baggage storage, once a niche buffer, is now part of the mainstream solution set because it stabilizes operations during peaks and supports premium offerings that improve satisfaction and yield. Baggage reclaim innovation progresses at a measured pace, with ergonomic and automation enhancements focused on safety and consistency rather than headline throughput.

As tracking coverage expands, more airports publish bag status in traveler-facing apps, reducing call volumes and agents’ time spent on exception queries in the airport baggage handling systems market. Mobile and kiosk check-in features also distribute demand across the day and shrink queues at peak hours, improving space utilization around ticketing islands. Operators increasingly link solution choices to cybersecurity and data governance to ensure that passenger-facing and operations systems remain segmented and resilient under stress. This awareness keeps digital investments centered on business continuity while guiding adoption toward scalable platforms with clear upgrade paths. As a result, Check-in retains its share leadership on installed base and utilization, while tracking and tracing sets the growth pace on a global compliance and cost-savings agenda within the airport baggage handling systems market.

By Technology: Barcode Retains Interoperability, AI and Machine Learning Lead Growth on Predictive Control

Barcode systems held a 34.73% share in 2025 due to long-standing interline compatibility and the widespread availability of optical scanners, while AI and ML software are the fastest-growing technologies, growing at a 11.87% CAGR as airports scale predictive analytics and digital twins. The shift to AI is evident in control rooms that forecast volumes, identify bottlenecks, and balance resources in real time, thereby directly improving bag flow and airside logistics. RFID adoption is rising under Resolution 753, with significant hubs and transfer-intensive airports leading the way as they benefit most from precision tracking. Airline implementations at scale show measurable improvements in bag processing rates and exception management, confirming the operational case for RFID, where traffic density and connections amplify risk. IoT sensors and edge computing are now standard in high-availability components, and predictive maintenance routines reduce unplanned downtime and spare parts use across monitored lines. Robotics remains emergent but is increasingly deployed for repetitive or strenuous tasks, paving a path for supervised autonomy on the floor that complements rather than replaces staff.

Over the forecast horizon, Barcode continues to provide a baseline of interoperability. At the same time, RFID builds scale, and AI-enabled control layers become the primary source of system gains in the airport baggage handling systems market. This balance reflects a pragmatic approach that protects existing investments while channeling growth into software and sensing that elevate reliability and efficiency without complete mechanical rebuilds. Airports that couple AI with RFID and IoT sensing can quantify benefits in resource optimization, faster exception recovery, and smoother ramp-side coordination. This combination establishes a de facto reference architecture for new builds and deep retrofits, supported by vendor portfolios that now include digital services alongside physical systems. These patterns signal sustained demand for analytics-driven value creation in the airport baggage handling systems market.

By System Type: Conveyor Belts Anchor Installed Base, Hybrid and Emerging Platforms Add Flexibility

Conveyor belt systems commanded a 42.61% share in 2025 on the strength of their installed base and proven reliability for continuous movement, while hybrid and other emerging systems are projected to grow at a 10.18% CAGR as airports seek flexible, software-orchestrated flows. Cross-belt and tilt-tray sorters extend capabilities beyond fixed conveyors by enabling higher-speed, gentler handling and smarter discharge that adapts to bag types and destinations. ICS platforms that place each bag in a tracked carrier enable any-order retrieval from storage and precise routing for just-in-time make-up, reducing the need for buffer space while improving punctuality. Vendors have advanced to low-height designs and modular kits that fit tight retrofit envelopes, expanding the options available to secondary airports that cannot accommodate tall sortation structures. These choices span from conventional belts to integrated carrier systems, allowing airports to align system type with throughput, footprint, and control sophistication.

The direction of travel favors hybrid layouts that combine belts for cost-efficient movement with ICS elements and smart storage for flexibility, all coordinated by AI-based control layers in the airport baggage handling systems market. Robotics and autonomous guided vehicles are joining this mix when repetitive manual tasks limit productivity or increase safety risks, and operators typically deploy these components in supervised modes before scaling. As digital orchestration matures, airports can shift from static routing to predictive control that anticipates peaks and reacts to disruption without heavy manual intervention. This evolution gradually reduces the performance gap between greenfield and brownfield facilities, enabling retrofits to deliver flexibility without substantial structural change. These trends keep hybrid and emerging systems as the fastest-growing class, while belts hold the lead in share due to the global installed base.

Geography Analysis

North America commanded 31.85% of the airport baggage handling systems market in 2025, anchored by a large installed base and a steady cadence of brownfield modernization that prioritizes cybersecurity, 100% in-line screening, and energy efficiency. Retrofit programs often require staged installation to prevent operational downtime, as seen in extensive conveyor upgrades that sequence dozens of steps while keeping flights running. Federal programs help cover select security elements, but airports still plan multi-year funding and phased execution to align structural, mechanical, and digital work.[4]U.S. Congress, “Transportation Security: Background and Issues for the 119th Congress,” Congressional Research Service, congress.gov TSA cybersecurity directives raise the baseline for network segmentation and monitoring, which influences procurement choices for controls and digital services and shapes O&M models built around predictive maintenance. These realities keep the region’s focus on resilience and modernization rather than net-new hubs within the airport baggage handling systems market.

The Middle East and Africa are the fastest-growing regions with a CAGR of 10.92% through 2031 as sovereign-backed megaprojects bypass legacy constraints and deploy ICS, AI orchestration, and 100% in-line screening from inception. These airports target high passenger capacities and fast connections, which push design toward modular, high-speed systems that provide full traceability across acceptance, screening, storage, and make-up. Labor availability and centralized governance facilitate the decisive adoption of robotics and autonomous systems, reducing friction in some mature markets. Operators also invest in digital twins and AI-based flow management to optimize connection windows and ground transport resources across large footprints. The region sets a benchmark for integrated design that other geographies seek to emulate in phased upgrades within the airport baggage handling systems market.

Asia-Pacific is forecasted to post the strongest long-term passenger growth to 2045, which channels capital toward cloud-ready platforms that integrate RFID, IoT sensors, and advanced analytics from the start. Large projects in India, Vietnam, and Southeast Asia favor scalable tote-based carriers and dynamic storage that support tight banked schedules. Europe advances under cyber and sustainability mandates, aligning investments with NIS2 requirements and energy-saving measures that cut electricity use and emissions while improving monitoring. Across both regions, airports plan for end-to-end traceability and predictive flow control, supported by vendor portfolios that combine mechanical systems with digital services. These strategies bolster the airport baggage handling systems market as operators standardize around resilient, data-driven architectures.

Competitive Landscape

The airport baggage handling systems market is led by a group of established integrators with comprehensive portfolios that span design, manufacturing, installation, and lifecycle services. Vanderlande’s consolidation of Siemens Logistics, including the 2026 finalization of US operations, expanded the combined portfolio to include high-speed sorters, ICS platforms, and digital services such as Baggage 360 and SmartService. Daifuku maintains a top-tier position with growth supported by an expanded production footprint and a record of complex brownfield retrofits in North America, Europe, and Asia.[5]Daifuku Co., Ltd., “Daifuku Report 2025,” Daifuku, daifuku.com BEUMER Group advances tote-based ICS and dynamic storage modules backed by new manufacturing capacity in India and China, emphasizing speed, quality control, and closer support for regional projects. Leonardo’s high-capacity cross-belt systems and 100% in-line screening references in the US strengthen its competitive footing in large hub upgrades.

Competition centers on technology differentiation and lifecycle value rather than headline price, with vendors promoting predictive maintenance, energy optimization, and uptime guarantees that address operator priorities. Siemens Logistics’ digital platforms, documented in its 2024 sustainability report, highlight reductions in dolly trips and downtime at high-volume terminals, validating the advantages of AI-based orchestration. Alstef focuses on modular sortation and compact designs for constrained environments, complementing the broader market’s move to flexible, software-defined architectures. Airports also segment service work away from OEMs to independent specialists in some cases, as seen in multi-year maintenance contracts that provide round-the-clock support under defined service levels and secure data-handling requirements, and in creating a service ecosystem where OEMs anchor complex upgrades. At the same time, the third-party providers compete on responsiveness and cost.

Across regions, operators value suppliers that can blend mechanical reliability with software and cyber readiness, a requirement sharpened by regulatory mandates in Europe and the United States. Integrators now position network segmentation, secure remote support, and certified component chains as standard features rather than options, reflecting procurement criteria shaped by NIS2 and TSA rules. Robotics roadmaps are moving from pilot-scale to supervised production in oversized baggage and ULD work cells, providing ergonomic and productivity benefits that help overcome labor bottlenecks. This mix of mechanical depth, digital capability, and cyber assurance defines the current basis of competition in the airport baggage handling systems market. It is likely to stay central through the next deployment cycle.

Airport Baggage Handling Systems Industry Leaders

Siemens AG

Alstef Group

Leonardo S.p.A

Vanderlande Industries B.V.

Daifuku Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Daifuku opened a new manufacturing facility in Hyderabad, India, quadrupling production space for airport baggage handling systems.

- December 2024: IDEMIA and SITA expanded their partnership to deploy ALIX computer-vision baggage identification globally.

- August 2024: Schiphol Airport launched a EUR 6 billion (USD 7.07 billion) modernization project, which includes a comprehensive overhaul of the baggage handling system, including a complete rebuild of the baggage basement.

- January 2024: Cincinnati/Northern Kentucky Airport deployed Aurrigo autonomous baggage tugs, increasing unit-load capacity by 30%.

Global Airport Baggage Handling Systems Market Report Scope

A baggage handling system, or BHS, is a type of conveyor system installed in an airport that enables the transportation of passenger baggage from ticket counter areas to the loading area where it is loaded onto the aircraft. BHS helps transport checked baggage from the aircraft to the baggage claim area.

The airport baggage handling systems market is segmented based on airport capacity, solution, technology, system type, and geography. By airport capacity, the market is segmented into up to 15 million, 15 to 25 million, 25 to 40 million, and above 40 million. By solution, the market is segmented into check-in and ticketing systems, security screening systems, conveying and sorting systems, early baggage storage, baggage reclaim/unloading, and tracking and tracing. By technology, the market is segmented into barcode, RFID, IoT sensors and edge devices, robotics and autonomous vehicles, and AI/ML software. By system type, the market is segmented into conveyor belt systems, tilt-tray and cross-belt sorters, destination-coded vehicles, tote-based/individual carrier systems, and hybrid and other emerging systems. The report also covers the market sizes and forecasts for the airport baggage handling systems market in major countries across different regions. For each segment, the market size and forecast are provided in terms of value (USD).

By Airport Capacity

| Up to 15 million |

| 15 to 25 million |

| 25 to 40 million |

| Above 40 million |

By Solution

| Check-In and Ticketing Systems |

| Security Screening Systems |

| Conveying and Sorting Systems |

| Early Baggage Storage |

| Baggage Reclaim/Unloading |

| Tracking and Tracing |

By Technology

| Barcode |

| RFID |

| IoT Sensors and Edge Devices |

| Robotics and Autonomous Vehicles |

| AI/ML Software |

By System Type

| Conveyor Belt Systems |

| Tilt-Tray and Cross-Belt Sorters |

| Destination-Coded Vehicle (DCV) |

| Tote-based/Individual Carrier Systems |

| Hybrid and Other Emerging Systems |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Airport Capacity | Up to 15 million | ||

| 15 to 25 million | |||

| 25 to 40 million | |||

| Above 40 million | |||

| By Solution | Check-In and Ticketing Systems | ||

| Security Screening Systems | |||

| Conveying and Sorting Systems | |||

| Early Baggage Storage | |||

| Baggage Reclaim/Unloading | |||

| Tracking and Tracing | |||

| By Technology | Barcode | ||

| RFID | |||

| IoT Sensors and Edge Devices | |||

| Robotics and Autonomous Vehicles | |||

| AI/ML Software | |||

| By System Type | Conveyor Belt Systems | ||

| Tilt-Tray and Cross-Belt Sorters | |||

| Destination-Coded Vehicle (DCV) | |||

| Tote-based/Individual Carrier Systems | |||

| Hybrid and Other Emerging Systems | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size and growth outlook for the Airport Baggage Handling Systems market?

The airport baggage handling systems market size is USD 1.73 billion in 2025 and is projected to reach USD 2.55 billion by 2031 at a 6.98% CAGR.

Which regions are leading and growing fastest in Airport Baggage Handling Systems?

North America leads on installed base with 31.85% share in 2025, while the Middle East and Africa are the fastest-growing region with 10.92% CAGR through 2031 on sovereign-backed greenfield projects.

Which segments show the highest share and the fastest growth?

By solution, check-in and ticketing systems lead with 31.12% share, and tracking and tracing grows fastest at a 10.98% CAGR; by technology, Barcode leads with 34.73% share, and AI or machine-learning software advances fastest at 11.87% CAGR.

How are airports reducing baggage mishandling in the Airport Baggage Handling Systems market?

Airports are implementing RFID to comply with IATA Resolution 753, improving read accuracy and end-to-end traceability while enabling faster exception recovery and smarter Early Baggage Storage release.

What are the top restraints to new deployments and upgrades?

High capex with 10–15 year ROI cycles, legacy IT and interoperability gaps, and rising cybersecurity compliance needs under NIS2 and TSA directives are the most cited barriers.

Which technologies are driving the next wave of value?

AI-enabled orchestration, RFID tracking, dynamic storage, and robotics for repetitive ULD tasks are driving measurable gains in throughput, reliability, and ergonomics across deployments.

Page last updated on: