Electronic Data Interchange (EDI) Software Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 2.60 Billion |

| Market Size (2030) | USD 4.54 Billion |

| Growth Rate (2025 - 2030) | 11.80% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

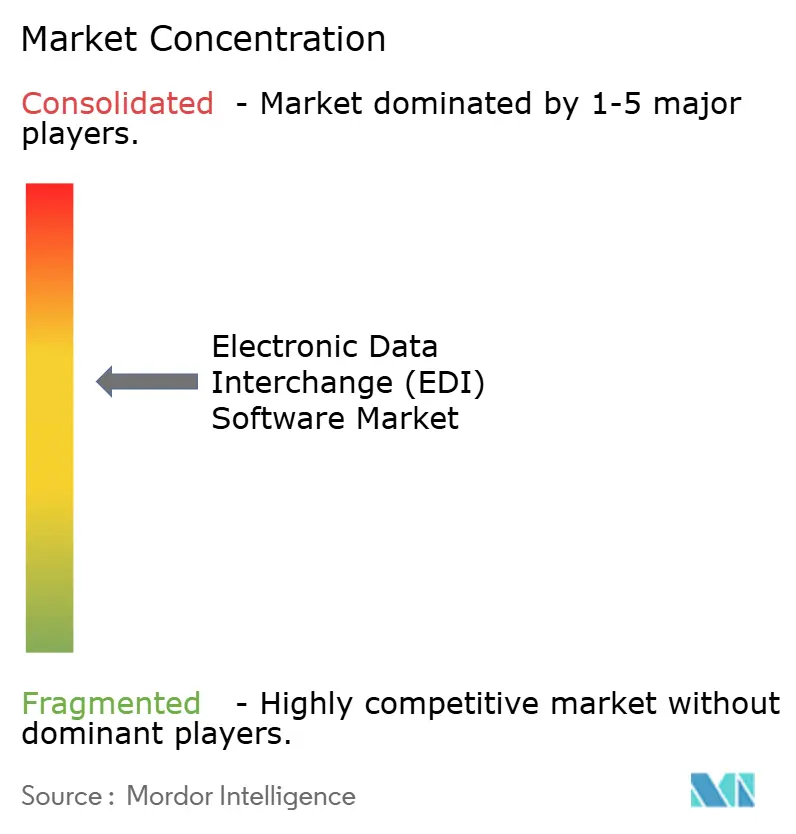

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electronic Data Interchange (EDI) Software Market Analysis by Mordor Intelligence

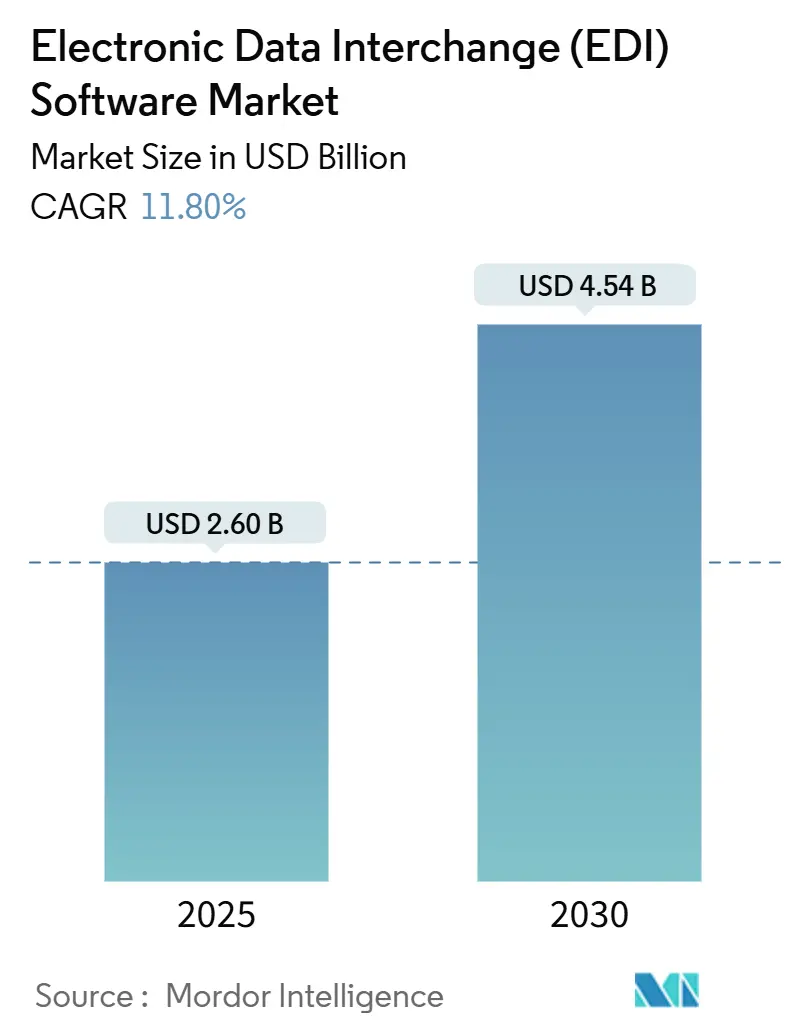

The Electronic Data Interchange (EDI) Software market size is estimated at USD 2.60 billion in 2025 and is projected to reach USD 4.54 billion by 2030, representing a 11.8% CAGR over the forecast period. Elevated demand for real-time data exchange, regulatory compliance pressures, and the convergence of EDI with cloud and API-first integration models underpin this expansion. Adoption accelerates when enterprises prioritize error-free transactions, immutable audit trails, and enhanced partner visibility, prompting vendors to embed blockchain validation, AI-driven mapping, and low-code configuration tools. Heightened cybersecurity vigilance, combined with widening talent gaps in emerging economies, continues to pose implementation hurdles; yet, these challenges also create opportunities for managed EDI services and autonomous iPaaS bundles that lower skill barriers and expedite partner onboarding. Within this competitive setting, market participants that deliver hybrid deployment flexibility, embedded analytics, and vertical-specific compliance modules maintain the clearest growth paths.

Key Report Takeaways

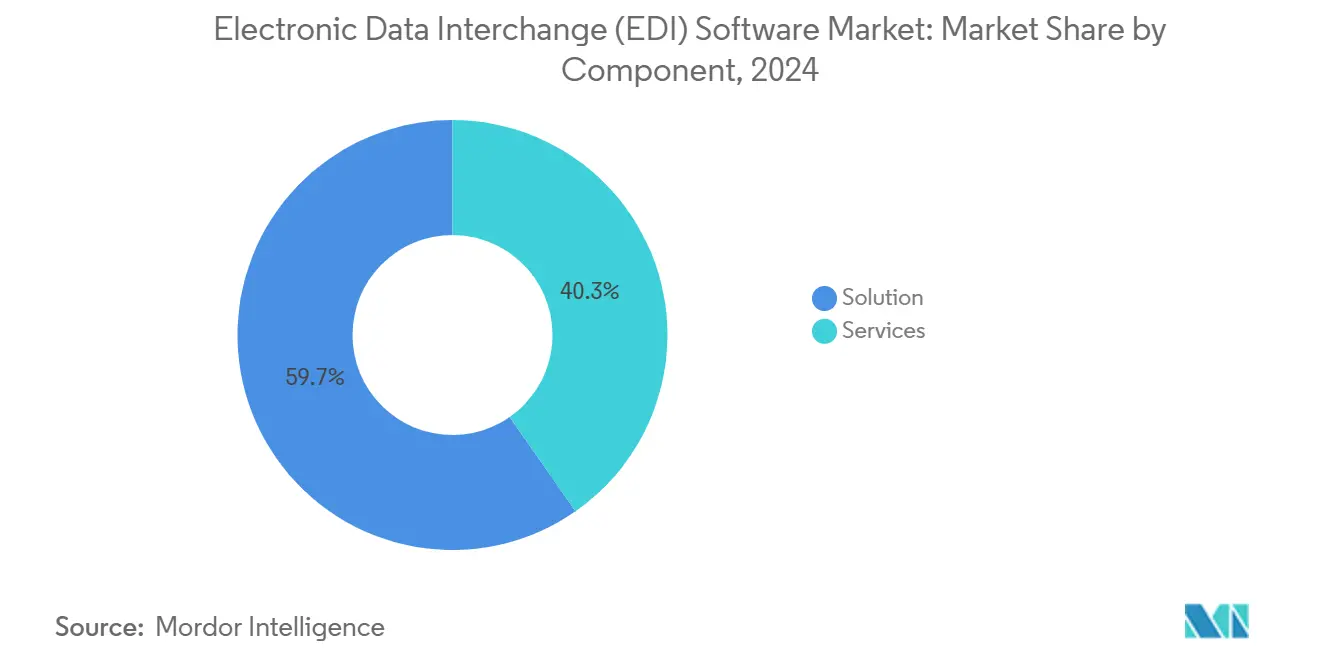

- By component, solution offerings captured 59.7% of the Electronic Data Interchange (EDI) Software market share in 2024, whereas services recorded the highest projected CAGR of 12.6% through 2030.

- By deployment model, cloud-based platforms accounted for 42.8% of the Electronic Data Interchange (EDI) Software market size in 2024, while hybrid architectures are expected to advance at a 13% CAGR to 2030.

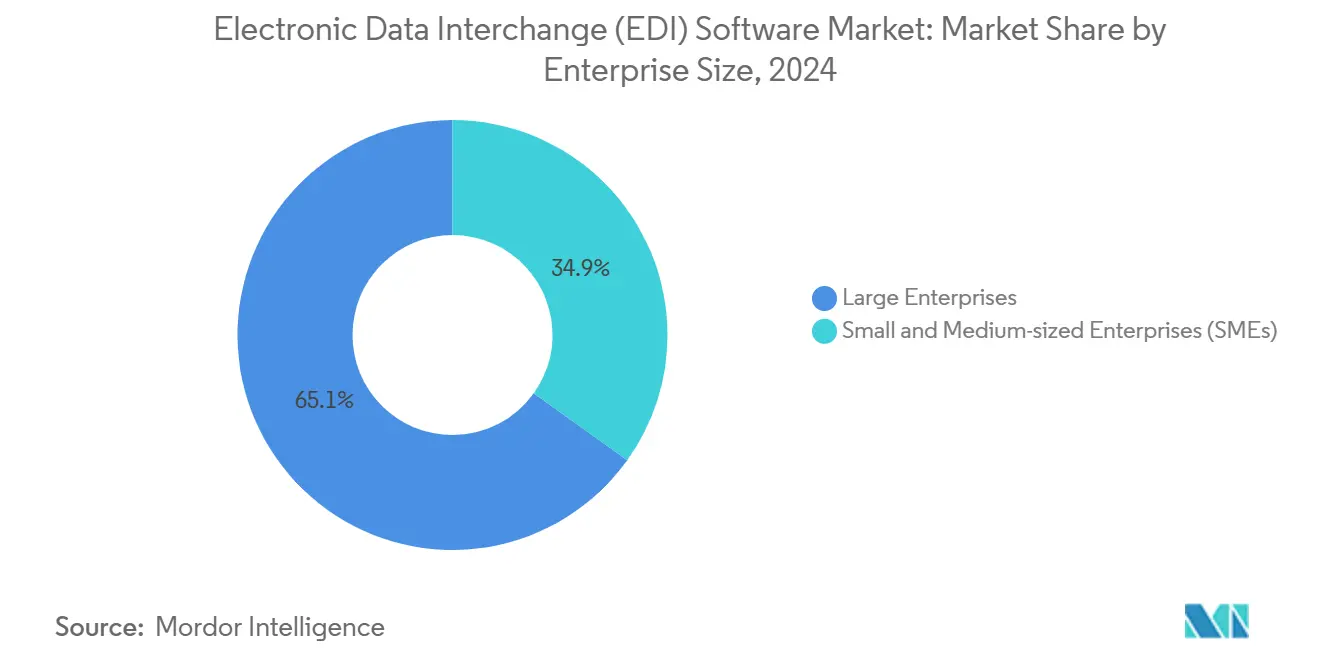

- By enterprise size, large organizations held 65.1% of the Electronic Data Interchange (EDI) Software market share in 2024; small and medium enterprises are poised for the fastest growth at a 12.5% CAGR.

- By industry vertical, retail and consumer goods led the Electronic Data Interchange (EDI) Software market with a 28.02% revenue share in 2024, whereas healthcare and life sciences are forecast to expand at a 14.51% CAGR.

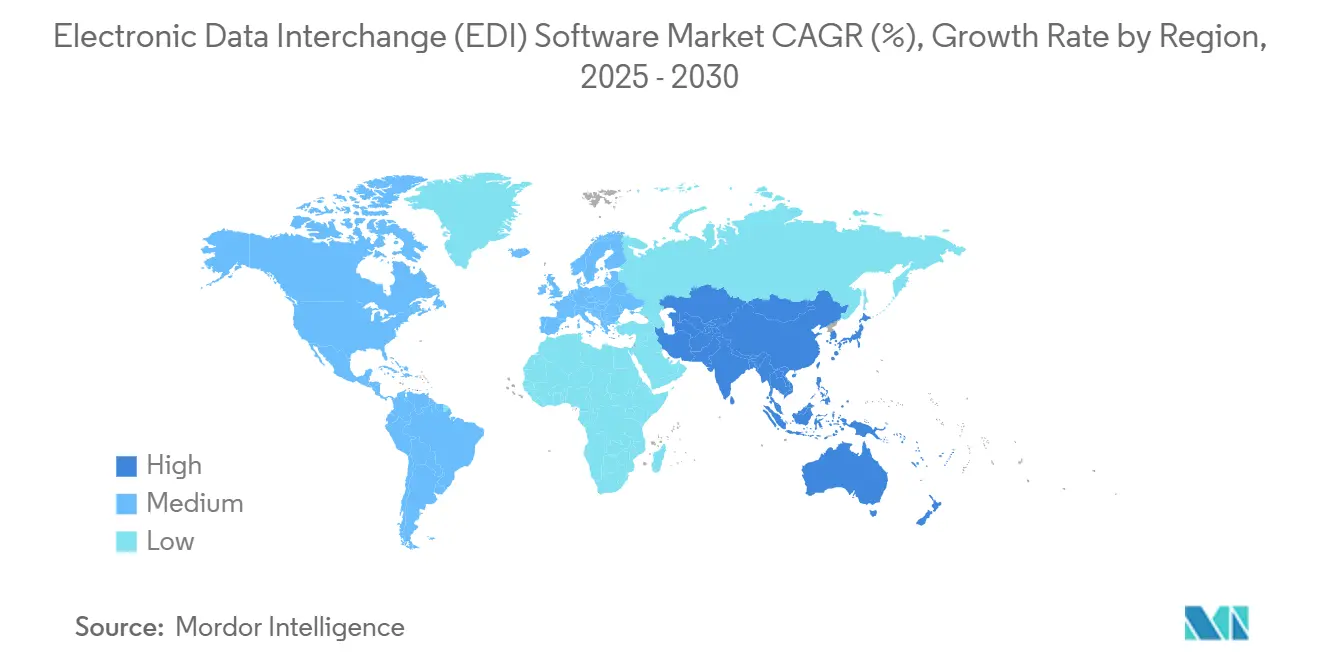

- By geography, North America commanded 38.31% of the Electronic Data Interchange (EDI) Software market in 2024, while the Asia Pacific is projected to grow at a 14.04% CAGR through 2030.

Global Electronic Data Interchange (EDI) Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid digitization of global supply chains | +3.2% | Global, early in North America and Europe | Medium term (2-4 years) |

| Stringent e-invoicing and tax compliance | +2.8% | Europe and Latin America leading, expanding to Asia Pacific | Short term (≤ 2 years) |

| Expansion of omni-channel retail B2B portals | +2.1% | North America and Europe core, spillover to Asia Pacific | Medium term (2-4 years) |

| AI-driven autonomous transaction mapping | +1.9% | North America and Asia Pacific | Long term (≥ 4 years) |

| Blockchain-backed EDI audit trails | +1.2% | Global, focus in regulated financial services | Long term (≥ 4 years) |

| Low-code embedded iPaaS inside ERPs | +1.6% | Global, rapid uptake among SMEs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Digitization of Global Supply Chains

Enterprises now integrate IoT sensors, RFID tags, and advanced analytics platforms with traditional EDI documents to orchestrate real-time inventory views and predictive demand planning. Hybrid integration consolidates transactional and operational data, feeding AI models that flag supplier risks before disruptions materialize. Boomi’s NextGen platform illustrates this convergence by combining EDI adapters with event-stream processing to automate telecom order fulfillment.[1]Boomi, “NextGen Integration for Telco: Accelerating Enterprise Transformation,” boomi.com Such capabilities shift EDI from static data pipes to dynamic decision engines, streamlining partner collaboration and unlocking just-in-time replenishment.

Stringent E-invoicing and Tax Compliance Mandates

Mandated e-invoicing frameworks, such as the African Continental Free Trade Area Digital Protocol, codify electronic documents as legal equivalents to paper across 54 nations.[2]African Union, “Protocol to the Agreement Establishing the African Continental Free Trade Area on Digital Trade,” africanlii.org Multinationals now need EDI stacks that validate multiple tax schemas, apply digital signatures, and archive audit trails per jurisdiction without adding manual compliance overhead. Vendors embedding adaptive rules engines and country-specific certification libraries improve time-to-comply and reduce fines, positioning compliance as a catalyst rather than a burden.

Expansion of Omni-channel Retail B2B Portals

Retailers extend consumer-grade transparency to suppliers, utilizing EDI to provide real-time order status, stock levels, and dynamic pricing information into partner portals. Cloud-native solutions scale effortlessly during peak seasons and manage high-frequency, low-value transactions typical of omni-channel fulfillment. API-first EDI architectures support drop-ship workflows and automatic backorder substitutions, enhancing customer experience while lowering transaction errors for trading partners.

AI-Driven Autonomous Transaction Mapping

Machine learning engines detect patterns in historical documents to generate and maintain mapping rules, slashing onboarding time from weeks to hours. Natural language processing converts free-form purchase orders into structured data, thereby broadening participation for partners that lack standardized EDI capabilities. Jitterbit’s Harmony utilizes AI agents to automatically repair broken integrations and suggest optimized routing.[3]Jitterbit, “AI-Powered Enterprise Automation and Integration,” jitterbit.com Autonomous mapping reduces reliance on scarce EDI specialists, enabling SMEs to scale their digital networks efficiently.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial integration and consulting cost | -2.1% | Global, most acute in emerging markets | Short term (≤ 2 years) |

| Legacy system interoperability bottlenecks | -1.8% | North America and Europe with aging ERP stacks | Medium term (2-4 years) |

| Growing cybersecurity attack surface | -1.4% | Global, heightened in financial services | Short term (≤ 2 years) |

| Skilled EDI talent shortage | -1.2% | Asia Pacific and Africa, limits implementation | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial Integration and Consulting Costs

Mid-market projects often exceed USD 100,000 before going live, covering mapping workshops, trading partner certifications, and user training. Sticker shock delays rollouts among SMEs even when large customers insist on EDI compliance. Cloud subscription models ease capex, yet specialized consulting remains essential for custom workflows and multi-standard environments. Vendors that package fixed-fee onboarding and self-service sandboxes reduce cost anxiety and expand addressable markets.

Legacy System Interoperability Bottlenecks

Decades-old ERPs and manufacturing execution systems rely on batch processing and lack modern APIs, complicating the handoff to real-time EDI gateways. Middleware bridges add conversion overhead, create new failure points, and inflate maintenance budgets. Upgrades are capital-intensive and can disrupt business operations, so many firms opt for hybrid bridges while scheduling phased modernization. Vendors offering lightweight adapters and data virtualization layers mitigate migration pain but cannot fully mask latency in legacy stacks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Catalyze Adoption

Solution platforms remained dominant, claiming 59.7% share in 2024. Services, however, will expand at the fastest rate of 12.6% CAGR as enterprises outsource mapping, compliance updates, and 24/7 monitoring. The Electronic Data Interchange (EDI) Software market size for managed services is projected to increase by almost USD 800 million between 2025 and 2030, reflecting the rising complexity in multi-national e-invoicing. Professional service teams curate pre-built kits for sector-specific mandates, accelerating go-lives and cutting support tickets. Growth also stems from SMEs that bypass do-it-yourself paths, opting instead for pay-as-you-grow managed transactions that include dashboards, exception handling, and support lines for trading partners. Vendors that wrap platform licenses with concierge onboarding services deepen client stickiness and unlock cross-sell opportunities for analytics extensions.

Cloud acceleration amplifies service revenues as customers demand continual schema updates, API security patches, and new connector rollouts. Certification audits in regulated industries drive recurring compliance assessments, generating consulting annuities. In parallel, advisory engagements around AI-enabled mapping, blockchain provenance, and ESG reporting widen the services mix beyond pure technical integration. This evolution positions service arms as strategic transformation partners, rather than tactical implementers, within the Electronic Data Interchange (EDI) Software market.

By Deployment Model: Hybrid Dominates Future Rollouts

Cloud options won early converts, rising to a 42.8% share in 2024; yet, strict data-residency rules in healthcare, banking, and defense sustain on-premise cores. Hybrid frameworks, which combine local processing nodes with cloud-based partner hubs, are forecasted to grow at a 13% CAGR. Under this model, sensitive documents remain behind corporate firewalls, while metadata and non-regulated transactions are routed through public clouds for scalability. The Electronic Data Interchange (EDI) Software market share for hybrid is poised to overtake pure cloud by 2028 as CIOs balance sovereignty with elasticity. Hybrid also aids incremental migration from legacy VANs to modern API gateways by overlaying new endpoints without disrupting entrenched flows.

Advances in container orchestration enable uniform deployment across environments, breaking down DevOps silos and facilitating continuous delivery. Vendors optimizing license meters for burst traffic and providing centralized policy engines simplify governance across distributed nodes. The model thus mitigates cost overruns and preserves performance for latency-sensitive uploads, underpinning the resilience ambitions of multinational supply chains.

By Enterprise Size: SMEs Propel Volume Growth

Large corporates held 65.1% of 2024 revenue, leveraging sizeable partner ecosystems and IT budgets. The Electronic Data Interchange (EDI) Software market size serving SMEs, while smaller, is expanding at a 12.5% CAGR as self-service portals and subscription tiers remove historic barriers. Plug-and-play storefronts enable micro-suppliers to exchange invoices within hours, thereby minimizing the learning curve. Trade finance lenders increasingly require EDI-enabled documentation as proof of shipment, further motivating SME adoption.

Bundled offerings with guided setup, community support, and template libraries foster network effects: as more SMEs integrate, large buyers gain broader visibility, reinforcing platform gravity. Vendors that offer usage-based pricing appeal to seasonal businesses and those wary of being locked into a fixed capacity. AI chatbots that troubleshoot mappings in-app further reduce reliance on specialized help desks, sustaining momentum in the Electronic Data Interchange (EDI) Software market segment.

By Industry Vertical: Compliance Fuels Healthcare Uptake

Retail remained the top vertical, with a 28.02% share, championing high-volume order orchestration across omni-channel networks. Yet healthcare’s 14.51% CAGR positions it as the fastest-growing sector, driven by HIPAA, DSCSA, and global serialization rules that require authenticated and auditable electronic exchanges. The Electronic Data Interchange (EDI) Software market size for healthcare participants is projected to nearly double by 2030 as hospitals, distributors, and pharma manufacturers digitize purchase orders, shipment notices, and billing details. Integrated e-prescription and electronic prior authorization workflows further extend the reach of EDI into patient-centric operations.

Regulatory-driven deals often bundle analytics that flag counterfeit risks and expiration-date issues, adding premium revenue streams for vendors. Retail’s growth persists on the back of drop-ship complexity and holiday peaks requiring elastic scaling. Manufacturing, automotive, logistics, and telecom sectors sustain steady double-digit growth as they align EDI flows with the provisioning of Industry 4.0 and 5G services.

Geography Analysis

North America continued to account for 38.31% of the revenue in 2024, driven by the long-standing ANSI X12 standards and robust VAN ecosystems. North America leads the Electronic Data Interchange (EDI) Software market with its deep integration maturity, comprehensive B2B standards, and mandated e-invoicing requirements for federal suppliers. The United States healthcare and defense sectors drive continuous modernization, while Canada and Mexico align customs data to streamline USMCA trade. Cloud migrations accelerate as enterprises retire legacy VAN contracts while retaining on-premises nodes for sensitive defense and financial workflows. Public-sector grants aimed at digitizing rural SMEs further broaden addressable adoption bases.

Asia Pacific exhibits the most vibrant expansion. The Asia Pacific’s 14.04% CAGR is driven by state-led digitization programs and booming e-commerce. China’s digital VAT invoices and India’s e-waybill ecosystems trigger a cascading process of supplier onboarding across manufacturing, retail, and logistics channels. Japan’s Society 5.0 initiative links EDI feeds to smart-factory data, enabling predictive maintenance and automated ordering. Southeast Asian governments expedite customs clearance via ASEAN Single Window protocols, reducing cargo dwell times and motivating freight forwarders to integrate EDI. Start-ups bundle lightweight EDI APIs into e-commerce storefronts, pushing B2B transaction volumes from micro-enterprises and cross-border sellers.

Europe remains a stable contributor, leveraging harmonized regulations such as EN 16931 and VAT in the Digital Age proposals to standardize e-invoicing across member states. Germany’s automotive OEMs enforce rigorous EDI checkpoints for supplier quality, while France expands Chorus Pro requirements to the private sector. Post-Brexit, the United Kingdom scales EDI for customs declarations and safety and security filings, maintaining frictionless flows with EU partners. Eastern European nations are tapping EU recovery funds to overhaul their tax systems, thereby raising regional demand.

Latin American growth is tied to tax authority clearance models pioneered by Brazil’s Nota Fiscal Eletrônica. Colombia, Peru, and Chile adopt similar real-time invoice reporting, compelling local SMBs to onboard EDI quickly or face penalties. In the Middle East and Africa, digital trade corridors accelerate adoption. Saudi Arabia’s ZATCA e-invoicing phases and the African Continental Free Trade Area Digital Protocol catalyze investment in interoperable platforms that handle Arabic, French, and English schemas simultaneously. Skill shortages encourage hosted and fully managed deployment models, especially among pan-regional distributors.

Competitive Landscape

The Electronic Data Interchange (EDI) Software market remains moderately concentrated, with incumbents SPS Commerce, TrueCommerce, OpenText, and Cleo leveraging decades-old trading networks and comprehensive partner catalogs to anchor renewal revenue. Platform differentiation shifts to autonomous mapping, dynamic cloud scaling, and pay-per-transaction billing, which is attractive to the SME surge. For instance, Cleo extends its Accelerator Starter Kits, which pre-package EDIFACT and ANSI maps for rapid onboarding in the consumer goods sector, while OpenText embeds AI anomaly detection into its Business Network to reduce exception rates during holiday spikes.

New entrants, including iPaaS challengers, embed EDI connectors into broader workflow orchestration suites. SEEBURGER’s business integration platform seamlessly merges classic B2B flows with API management, providing a single pane of glass for hybrid topologies.[4]SEEBURGER, “SEEBURGER Business Integration,” seeburger.com Telecommunications standardization by TM Forum opens avenues for niche vendors to supply CSP-specific provisioning flows. Cybersecurity partnerships deepen as providers integrate zero-trust frameworks and encrypted VAN alternatives to protect expanding endpoint arrays. M&A activity focuses on integrating AI and low-code capabilities into established transaction engines, as demonstrated by Edisoft’s 2025 release of a control-center module featuring automated document signing and reconciliation.

On the services side, system integrators team with platform vendors to offer vertical accelerators. Advisory firms craft compliance toolkits that bundle country tax engines. As customer expectations realign around outcome-based SLAs, vendors shift from license-ledgers toward managed transaction volumes, nudging the competitive arena toward value-added analytics and supply-chain insights.

Electronic Data Interchange (EDI) Software Industry Leaders

SPS Commerce Inc.

TrueCommerce Inc.

Cleo Communications Inc.

OpenText Corporation

Comarch SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: The African Continental Free Trade Area Digital Protocol entered into force, establishing continent-wide legal recognition of electronic invoicing and digital identities.

- January 2025: Edisoft unveiled the Link Enterprise Dataflow Control Center, touting three times faster data entry and a 90% acceleration in supply-chain data exchange.

- December 2024: eOne integrated its iPaaS solution with Microsoft Dynamics 365 Business Central via the 4Sight Marketplace, facilitating no-code EDI flows for SMEs.

- November 2024: SEEBURGER positioned its Business Integration Platform to bridge B2B EDI with iPaaS functionality for hybrid cloud environments.

Global Electronic Data Interchange (EDI) Software Market Report Scope

| Solution |

| Services |

| Cloud-based |

| On-premise |

| Hybrid |

| Small and Medium Enterprises |

| Large Enterprises |

| Retail and Consumer Goods |

| Manufacturing |

| Healthcare and Life Sciences |

| Automotive |

| Logistics and Transportation |

| Financial Services and Banking |

| Telecom and IT |

| Other Industry Verticals |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| South-East Asia | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Solution | |

| Services | ||

| By Deployment Model | Cloud-based | |

| On-premise | ||

| Hybrid | ||

| By Enterprise Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By Industry Vertical | Retail and Consumer Goods | |

| Manufacturing | ||

| Healthcare and Life Sciences | ||

| Automotive | ||

| Logistics and Transportation | ||

| Financial Services and Banking | ||

| Telecom and IT | ||

| Other Industry Verticals | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the 2025 value of the Electronic Data Interchange (EDI) Software market?

The market is valued at USD 2.60 billion in 2025.

How fast will Asia Pacific grow through 2030?

Asia Pacific is projected to expand at a 14.04% CAGR, the fastest among all regions.

Which component segment is growing quickest?

Services will grow at 12.6% CAGR as firms seek managed integration and compliance expertise.

Why is healthcare adopting EDI rapidly?

HIPAA, DSCSA, and global serialization mandates require secure, auditable electronic exchanges, driving a 14.51% CAGR in healthcare.

How does hybrid deployment benefit enterprises?

Hybrid models let firms keep sensitive data on-premise while harnessing cloud scalability for partner connectivity, balancing security and cost.

What risk accompanies EDI expansion?

A larger digital footprint increases cybersecurity exposure, especially in financial services, necessitating zero-trust and encryption measures.

Page last updated on: