Market Overview

| Study Period | 2020 - 2032 |

|---|---|

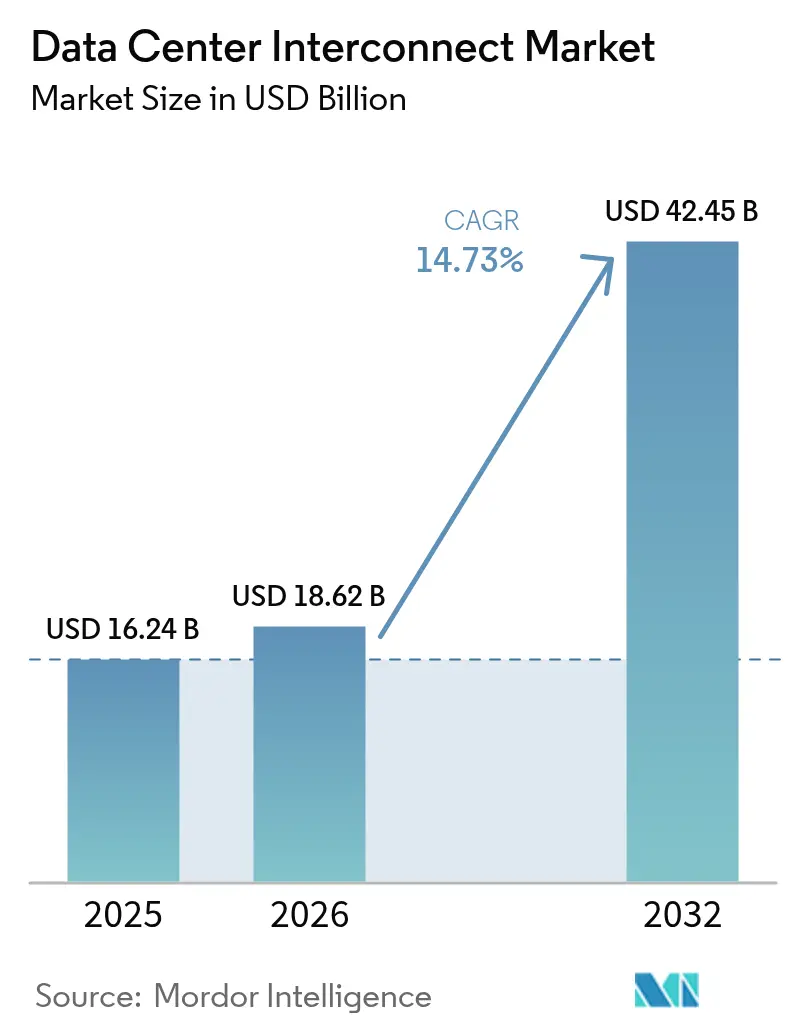

| Market Size (2026) | USD 18.62 Billion |

| Market Size (2032) | USD 42.45 Billion |

| Growth Rate (2026 - 2032) | 14.73% CAGR |

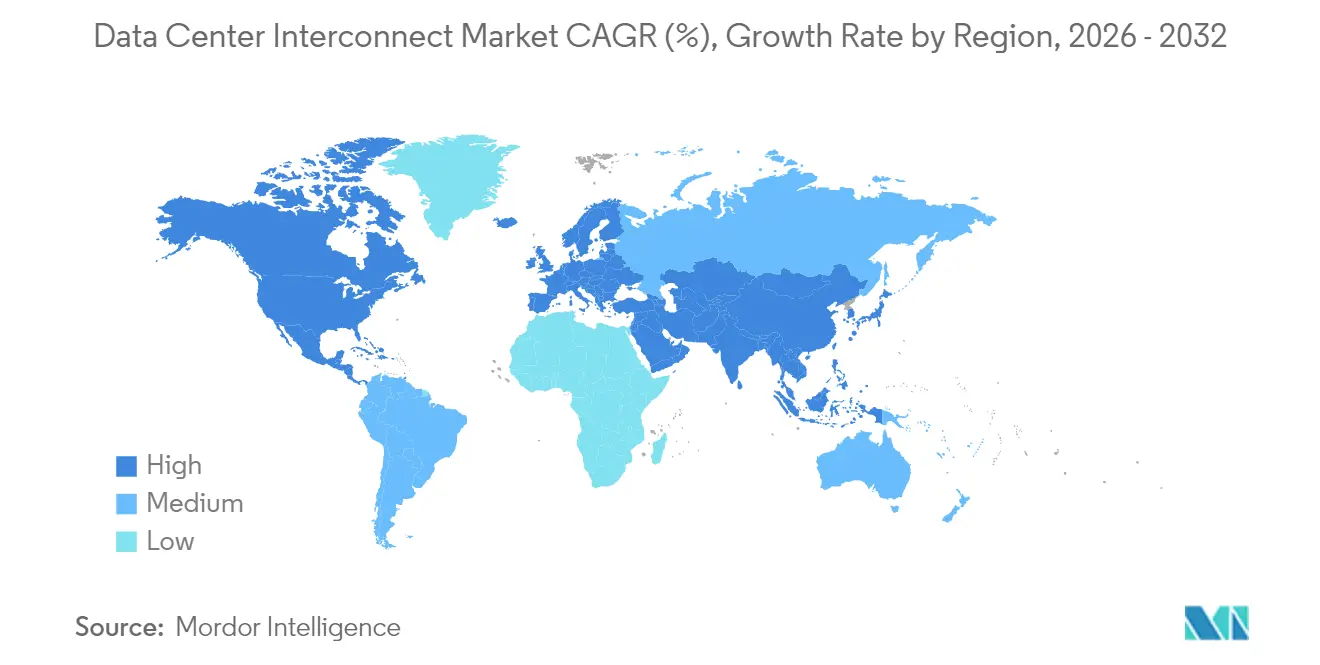

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Data Center Interconnect Market Analysis by Mordor Intelligence

The data center interconnect market size was valued at USD 16.24 billion in 2025 and estimated to grow from USD 18.62 billion in 2026 to reach USD 42.45 billion by 2032, at a CAGR of 14.73% during the forecast period (2026-2032). Strong capital spending by hyperscale operators, the migration of artificial intelligence workloads that need ultra-high bandwidth, and expanding edge deployments are reshaping network-architecture priorities. Operators are moving away from monolithic enterprise links toward AI-optimized, low-latency fabrics built on coherent optics, photonic switching, and software-defined control. Near-term growth concentrates on metropolitan corridors where 400 Gbps and 800 Gbps links replace legacy 100 Gbps waves. Supply-side innovation in co-packaged optics and 1.6 Tbps coherent engines reinforces the long-run expansion outlook, while sustainability mandates spur adoption of energy-efficient switching and liquid-cooling–ready short-reach optics. Regional investment patterns remain heterogeneous: Asia-Pacific leads in capacity additions, North America dominates in R&D, and Europe scales green interconnect designs to satisfy carbon-neutral goals.

Key Report Takeaways

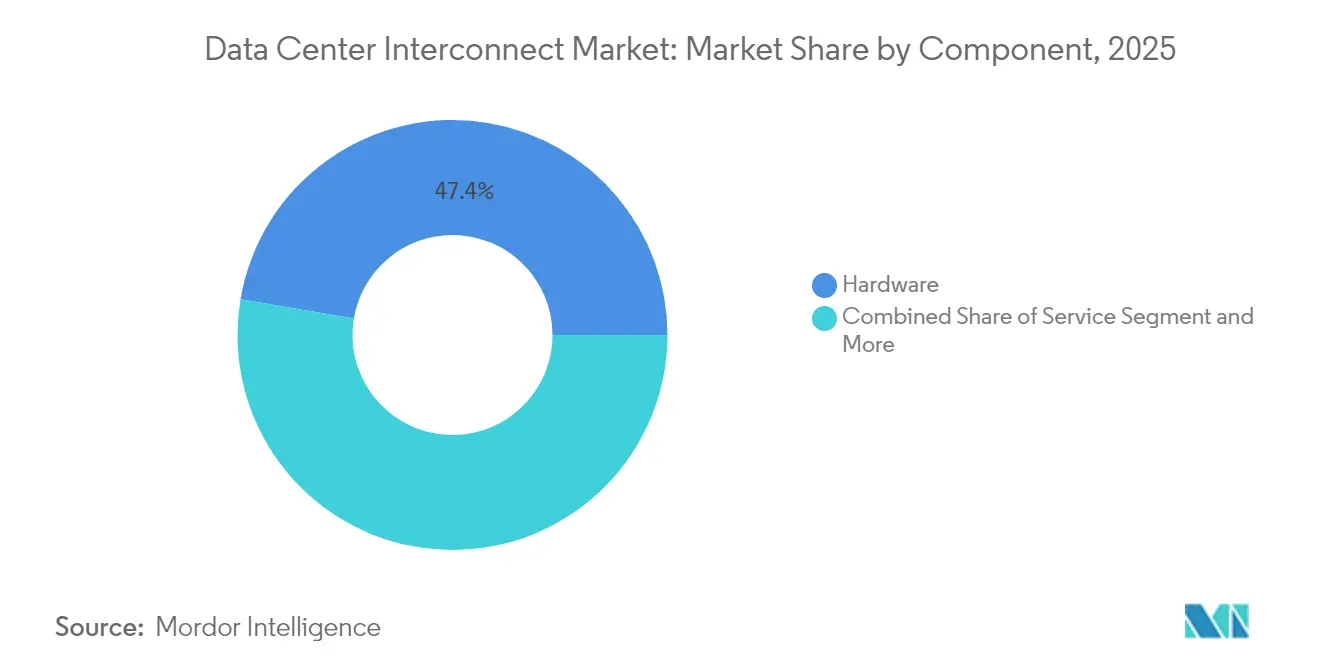

- By component, hardware accounted for a 47.35% slice of the data center interconnect market share in 2025; software-defined networking and control platforms are poised to post the fastest 16.12% CAGR through 2032.

- By connectivity type, short-haul links captured 60.25% of the data center interconnect market size in 2025, while long-haul connections are expected to grow at a 14.88% CAGR from 2026 to 2032.

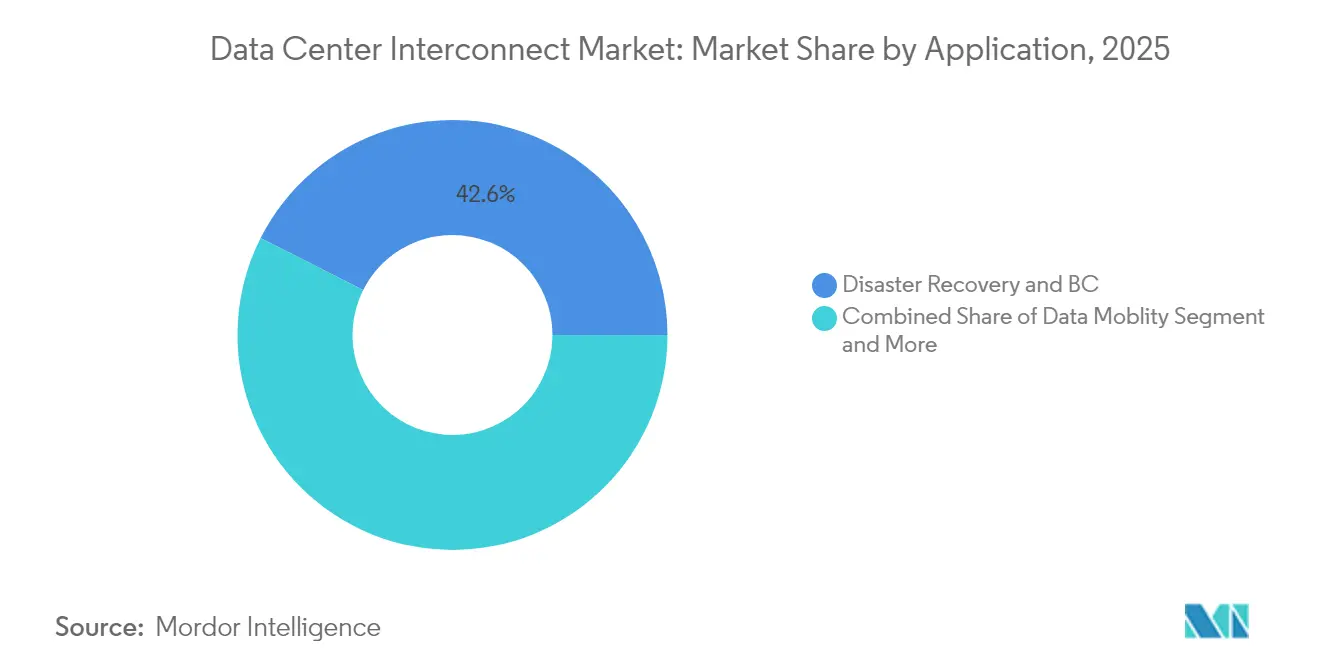

- By application, disaster recovery and business continuity represented 42.55% of 2025 revenue; data mobility is projected to expand at a 15.05% CAGR to 2032.

- By end-user industry, communication service providers held 58.25% of 2025 revenue, yet internet content and carrier-neutral providers will record a 14.66% CAGR over the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Data Center Interconnect Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Expanding edge and hyperscale data-center footprints | +2.8% | Global, led by North America and Asia-Pacific | Medium term (2-4 years) |

| Surge in AI/HPC traffic requiring greater than 400 Gbps links | +3.2% | North America, China, Western Europe | Short term (≤ 2 years) |

| Commercial 5G roll-outs accelerating low-latency backhaul demand | +1.9% | Asia-Pacific core, spill-over to Europe and North America | Medium term (2-4 years) |

| Campus liquid-cooling retrofits boosting short-reach optical spend | +1.1% | Global hyperscale markets | Short term (≤ 2 years) |

| Satellite ground-station colocation creating novel DCI nodes | +0.8% | Rural North America, Northern Europe, Australia | Long term (≥ 4 years) |

| Net-zero mandates driving adoption of photonic switching fabrics | +1.4% | Europe, California, select Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Edge and Hyperscale Data-Center Footprints

Hyperscale operators have earmarked USD 180 billion for distributed infrastructure that places compute close to users,[1]Vicor Team, “Defining Future Edge Computing Using Micro-Data Centers,” Vicor Corporation, vicorpower.comforcing interconnect designs to support dense mesh topologies rather than hub-and-spoke layouts. Amazon’s USD 100 billion expansion and Meta’s USD 65 billion program typify this shift. Edge micro-facilities, projected to grow at a 37.9% CAGR, require power-efficient short-reach optics paired with programmable routing that can rebalance traffic in real time. Carrier hotels now double as edge nodes where cloud, content, and network operators converge, adding fresh demand for multi-tenant intra-metro links.

Surge in AI/HPC Traffic Requiring greater than 400 Gbps Links

AI model training generates all-to-all traffic patterns that saturate legacy 100 Gbps networks. Optical module shipments for 400G/800G exceeded 20 million units in 2024,[2]Eliza Strickland, “A Crucial Optical Technology Has Finally Arrived,” IEEE Spectrum, spectrum.ieee.org underscoring aggressive migration timelines. NVIDIA’s 800G photonic switch roadmap and IEEE’s 800G Ethernet standard illustrate the ecosystem’s pivot to coherent optics that push toward 1.6 Tbps lanes. Photonic switching fabrics reduce hop counts and latency, enabling AI clusters to scale without the oversubscription penalties of electrical spine-leaf trees.

Commercial 5G Roll-outs Accelerating Low-Latency Backhaul Demand

5G radio access requires sub-5 ms round-trip latency, compelling operators to interconnect edge aggregation sites with core data centers using fiber paths under 20 km. Vapor IO and NVIDIA deployed an AI-enabled 5G edge in Las Vegas,[3]Staff Writers, “Vapor IO and NVIDIA Launch AI-Driven 5G Edge Deployment,” Edge Industry Review, edgeir.com illustrating the tight coupling between mobile edge compute and data center interconnect fabrics. Software-defined segmentation and dynamic bandwidth allocation ensure slices with strict QoS meet varying application profiles.

Campus Liquid-Cooling Retrofits Boosting Short-Reach Optical Spend

Liquid cooling allows higher rack densities, raising intra-facility bandwidth requirements. Each retrofit coincides with server refreshes where operators adopt 16-fiber MPO 400G optics to sustain east-west traffic caused by AI inference loads. Sustainability commitments, such as EdgeConneX’s plan for carbon-neutral operations by 2030, align with these thermal-and-optical upgrades.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High upfront cost of coherent optics and ROADMs | -1.8% | Global, notably emerging markets | Short term (≤ 2 years) |

| Multi-vendor interoperability and network-complexity issues | -1.2% | Global | Medium term (2-4 years) |

| Shortage of skilled fiber-construction labor | -2.1% | North America, Western Europe | Medium term (2-4 years) |

| Municipal permitting delays for metro-haul trenching | -0.9% | Urban centers worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Coherent Optics and ROADMs

Advanced coherent engines and reconfigurable optical add-drop multiplexers (ROADMs) command premiums up to 300% over legacy gear, stretching capex budgets for mid-tier carriers. The ROADM market is projected at USD 1.2 billion by 2026, reflecting heavy investment needs. Operators in cost-sensitive regions postpone upgrades, reinforcing a two-tier global adoption pattern.

Shortage of Skilled Fiber-Construction Labor

Telecom build-outs face a workforce gap that the Semiconductor Industry Association estimates will need 1 million additional technicians by 2030. Wage inflation escalates metro trenching costs, and lengthy training cycles delay project completion. Rural deployments suffer the most severe constraints, slowing last-mile connectivity to edge zones.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Orchestration Drives Next-Generation Architectures

Hardware held 47.35% of 2025 revenue as operators procured dense DWDM shelves and coherent transceivers that underpin the data center interconnect market. The software tier will post a 16.12% CAGR as controllers automate bandwidth pooling, latency steering, and failover. Vendors pursuing co-packaged optics blend silicon switching with embedded lasers, lowering power per bit and shrinking footprints. Services revenue grows in tandem, reflecting demand for design, integration, and lifecycle support.

The data center interconnect market size for hardware is forecast to rise alongside AI cluster roll-outs, yet programmable orchestration remains the strategic differentiator. Operators use open APIs to stitch multi-vendor optics into a single intent-based fabric, cutting provisioning cycles from weeks to hours.

By Connectivity Type: Long-Haul Growth Accelerates Inter-Regional Expansion

Short-haul links (< 80 km) delivered 60.25% of 2025 revenue because metro campuses, cloud on-ramps, and carrier hotels require dense east-west bandwidth. Long-haul systems will outpace with a 14.88% CAGR as hyperscalers pursue resilience across regions. The data center interconnect market size for long-haul will benefit from 1.6 Tbps coherent platforms that squeeze more capacity into existing fiber.

Projects such as the Medusa submarine cable add fresh routes linking Europe and Africa, creating new demand pools. Meanwhile, edge growth sustains short-haul volumes, ensuring balanced capex allocation between metro and backbone domains.

By Application: Data Mobility Emerges as Strategic Differentiator

Disaster recovery led 2025 spending with a 42.55% share as enterprises hardened business-continuity postures. Data mobility will grow fastest at 15.05% CAGR as AI models, databases, and container images move fluidly among clouds. The data center interconnect market share for mobility solutions rises because multi-cloud strategies rely on low-latency replication and object-storage shuttling.

Shared resource clustering supports HPC bursts while edge intelligence pushes models to inference nodes, raising temporal traffic peaks. Vendors offering bandwidth-on-demand and encryption at line rate stand to capture these latency-critical workflows.

By End-User Industry: ICPs/CNPs Drive Innovation Through Scale

Communication service providers retained 58.25% revenue in 2025, leveraging nationwide fiber footprints to monetize wholesale waves. Internet content and carrier-neutral providers will clock a 14.66% CAGR as hyperscale platforms and neutral colos race to add capacity. Government, research, and education demand remains stable as public agencies modernize legacy network backbones.

Hyperscalers vertically integrate optics—exemplified by Microsoft’s in-house transceiver program—to control cost and supply risk. Neutral colocation chains such as Equinix expand cross-connect marketplaces, reinforcing secular demand for vendor-agnostic interconnect fabrics.

Geography Analysis

North America leads the data center interconnect market owing to concentrated hyperscale campuses, advanced fiber corridors, and an active open-source ecosystem. DE-CIX Dallas’s 400 GE upgrade highlights metro densification. U.S. projects spearhead photonic-switch adoption, aided by robust venture funding and favorable tax incentives.

Asia-Pacific is the fastest-growing region, with data-center capacity expected to triple by 2033 on the back of cloud adoption in China, Japan, India, and ASEAN markets. Domestic AI ambitions and 5G roll-outs accelerate both short-haul metro builds and cross-border long-haul corridors.

Europe balances sustainability rules and digital sovereignty objectives. Germany alone is projected to reach a USD 25.3 billion data-center valuation by 2029, purchasing high-efficiency optics to align with the EU’s carbon-neutral pledge. Submarine cables such as 2Africa improve resilience, supporting content exchange with Middle Eastern and African hubs.

Latin America is a rising investment theater; Brazil accounts for 40% of regional spend, and Brookfield’s search for an Ascenty partner underscores confidence in hyperscale growth. Mexico’s Querétaro cluster attracts cloud majors seeking sub-20 ms latency to U.S. markets.

The Middle East and Africa pursue sovereign AI and cloud initiatives. Gulf states deploy liquid-cooled campuses tied to solar plants, while terrestrial routes along the Red Sea and new cable landings in Kenya widen continental reach.

Competitive Landscape

Competition remains moderate with ongoing consolidation. Nokia’s USD 2.3 billion Infinera acquisition marries coherent DSP silicon with global channel reach, intensifying the fight for end-to-end optical portfolios. Zayo’s USD 4.25 billion Crown Castle fiber deal bolsters metro presence in tier-2 U.S. cities.

Vendors differentiate through integrated hardware-software stacks, AI-driven network telemetry, and sustainability features. Startups targeting photonic switching or co-packaged optics disrupt the status quo by slashing cost per bit. Ecosystem alliances—such as Kyndryl with Cloudflare or Lumen with Google Cloud—bundle connectivity and managed services, deepening value capture.

Patent filings accelerate around multi-core fiber, quantum-safe encryption, and silicon photonics. Intellectual-property depth becomes a strategic shield as hyperscalers weigh in-house build versus buy decisions.

Data Center Interconnect Industry Leaders

Ciena Corp

Cisco Systems Inc

Juniper Networks Inc

Fujitsu Ltd

Microsemi Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Brookfield seeks partner for Ascenty amid Brazil’s data-center boom

- December 2024: MDC Data Centers enters Mexico with Querétaro facility

- November 2024: Equinix issues EUR 1.15 billion in green bonds to fund efficiency projects

- October 2024: Nokia completes USD 2.3 billion Infinera buyout

Global Data Center Interconnect Market Report Scope

The Data Center Interconnect (DCI) technology connects two or more data centers together over short, medium or long distances using high-speed packet-optical connectivity. Some large operations use DCI to connect their own data centers within their extended enterprise infrastructures, while others connect to partners, cloud providers or data center operators to enable simpler data and resource sharing or handle disaster recovery needs. The market studied focuses on end-user industries utilizing DCI to address space and power challenges.

The data center interconnect market is segmented by Application (Disaster Recovery and Business Continuity, Shared Data and Resources, Data (Storage) Mobility), by End-user Vertical (Communications Service Providers (CSPs), Internet Content and Carrier- neutral Providers (ICPs/CNPs), Government/Research and Education (Government/R&E)), by Geography.

The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

by Component

| Hardware (DWDM, OTN, Packets) |

| Software-Defined Networking and Control |

| Services (Managed, Professional) |

by Connectivity Type

| Short-Haul |

| Long-Haul |

by Application

| Disaster Recovery and Business Continuity |

| Shared Data and Resource Clustering |

| Data (Storage) Mobility |

| Other Applications |

by End-user Industry

| Communication Service Providers (CSPs) |

| Internet Content / Carrier-Neutral Providers (ICPs/CNPs) |

| Government, Research and Education |

| Other Verticals |

by Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Spain | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | UAE |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| by Component | Hardware (DWDM, OTN, Packets) | ||

| Software-Defined Networking and Control | |||

| Services (Managed, Professional) | |||

| by Connectivity Type | Short-Haul | ||

| Long-Haul | |||

| by Application | Disaster Recovery and Business Continuity | ||

| Shared Data and Resource Clustering | |||

| Data (Storage) Mobility | |||

| Other Applications | |||

| by End-user Industry | Communication Service Providers (CSPs) | ||

| Internet Content / Carrier-Neutral Providers (ICPs/CNPs) | |||

| Government, Research and Education | |||

| Other Verticals | |||

| by Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Spain | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | UAE | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size and growth rate of the data center interconnect market?

Global revenue reached USD 18.62 billion in 2026 and is projected to rise to USD 42.45 billion by 2032 on a 14.73% CAGR.

Which connectivity type is expanding fastest within data center interconnect solutions?

Long-haul (? 80 km) links are forecast to grow at a 14.88% CAGR between 2026-2032, outpacing short-haul deployments.

How are AI and HPC workloads shaping future interconnect investments?

Training clusters that need 400 Gbps 800 Gbps bandwidth are pushing operators to adopt coherent optics, photonic switching, and software-defined control for low-latency performance.

Why do communication service providers remain the largest customer group?

They own wide fiber footprints and wholesale wave services, enabling them to capture 58.25% of 2025 revenue even as content and carrier-neutral providers scale quickly.

Which region is recording the fastest capacity growth?

Asia-Pacific, where total data-center capacity is set to triple by 2033 on the back of cloud adoption in China, Japan, India, and Southeast Asia.

What technologies are vendors deploying to cut power consumption in data center links?

Co-packaged optics and photonic switching eliminate multiple electrical stages, lowering energy per bit and helping operators meet net-zero targets.

Page last updated on: