Electrocoating (E-coat) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

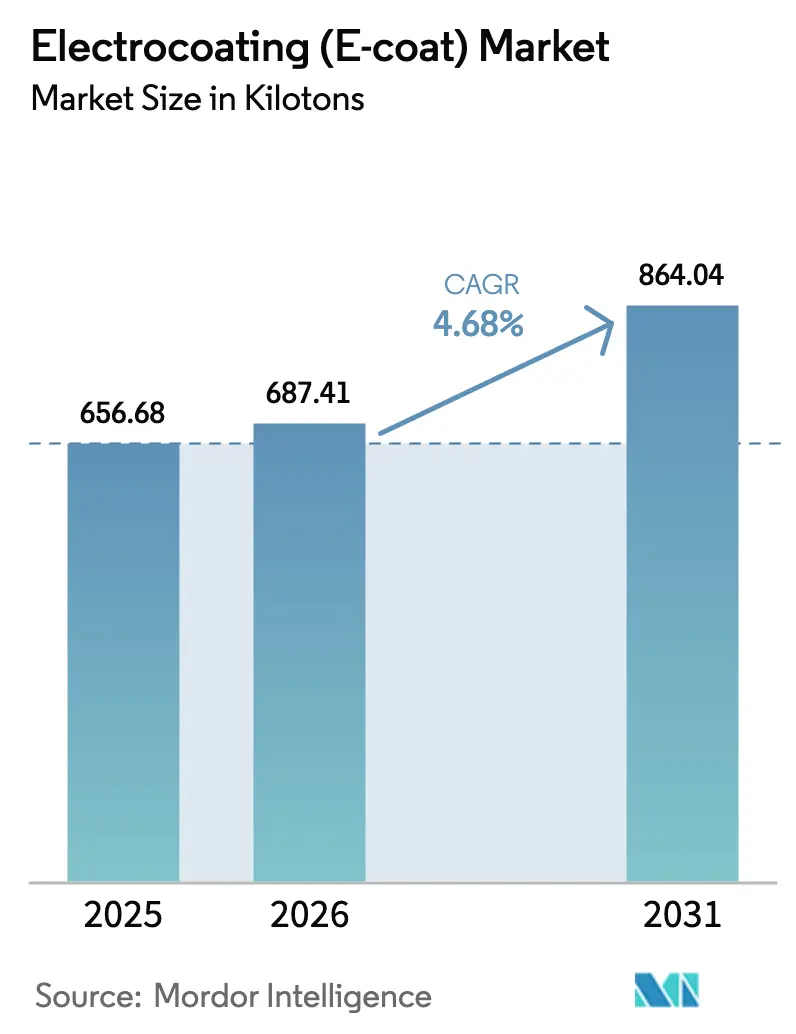

| Market Volume (2026) | 687.41 kilotons |

| Market Volume (2031) | 864.04 kilotons |

| Growth Rate (2026 - 2031) | 4.68% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electrocoating (E-coat) Market Analysis by Mordor Intelligence

The Electrocoating Market size is projected to expand from 656.68 kilotons in 2025 and 687.41 kilotons in 2026 to 864.04 kilotons by 2031, registering a CAGR of 4.68% between 2026 to 2031. Three key shifts are reshaping the landscape: the Asia-Pacific region is increasing its vehicle production, electric-vehicle (EV) battery housings now mandate dielectric shielding for systems surpassing 800 V, and agricultural-equipment assembly is moving closer to home in the Latin America region. This realignment is shifting coating demand away from traditional centers in Europe and North America. Cathodic epoxy systems, known for their high dielectric strength and impressive transfer efficiency, have emerged as the preferred choice. This advantage enables automotive and appliance OEMs to not only adhere to stringent corrosion and sustainability benchmarks but also to significantly reduce volatile organic compound (VOC) emissions compared to conventional spray primers.

Key Report Takeaways

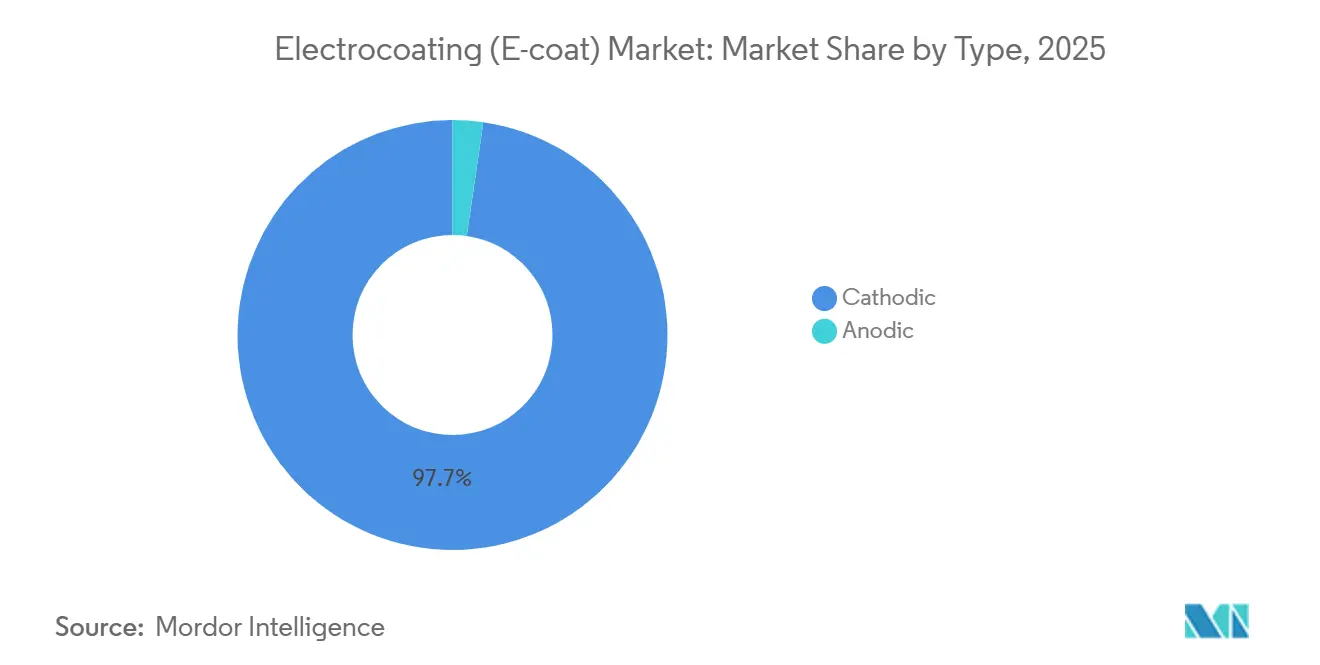

- By type, cathodic systems held 97.72% of the 2025 volume and are slated to expand at a 4.67% CAGR from 2026 to 2031, confirming their grip on corrosion-critical applications.

- By technology, epoxy formulations captured 90.76% of the 2025 total and will grow at a 4.58% CAGR from 2026 to 2031.

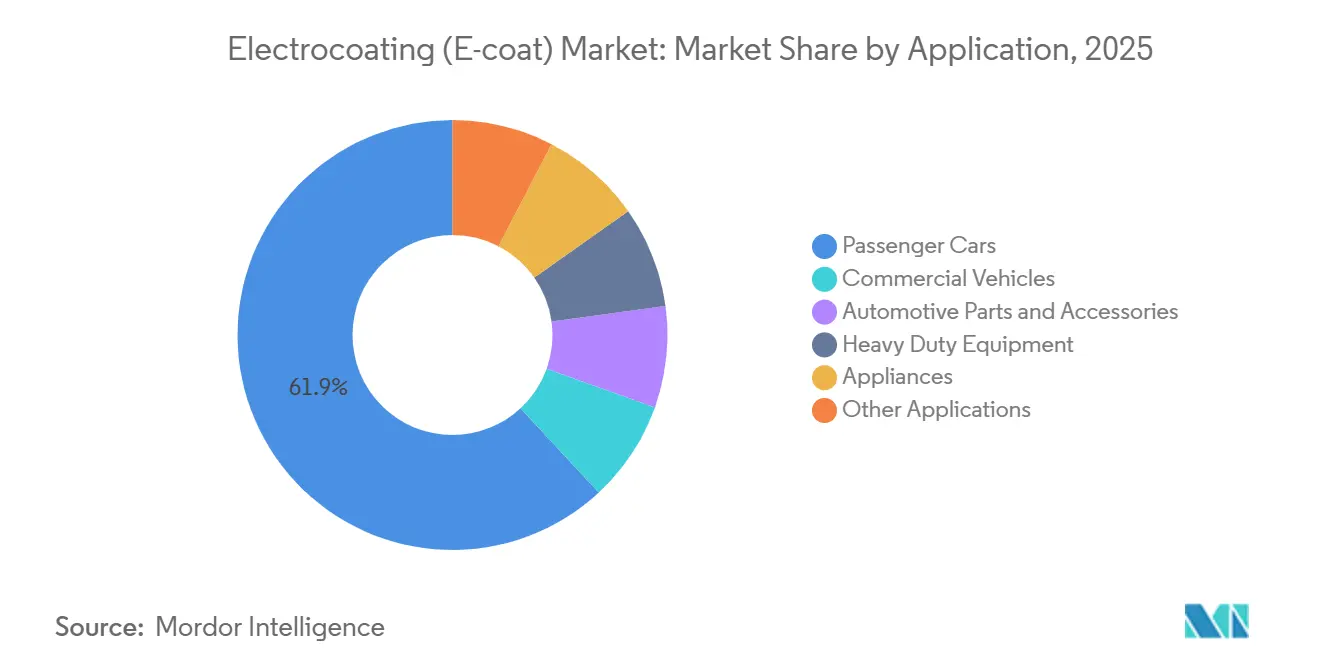

- By application, passenger cars accounted for 61.92% of volume in 2025 and are advancing at a 5.05% CAGR from 2026 to 2031.

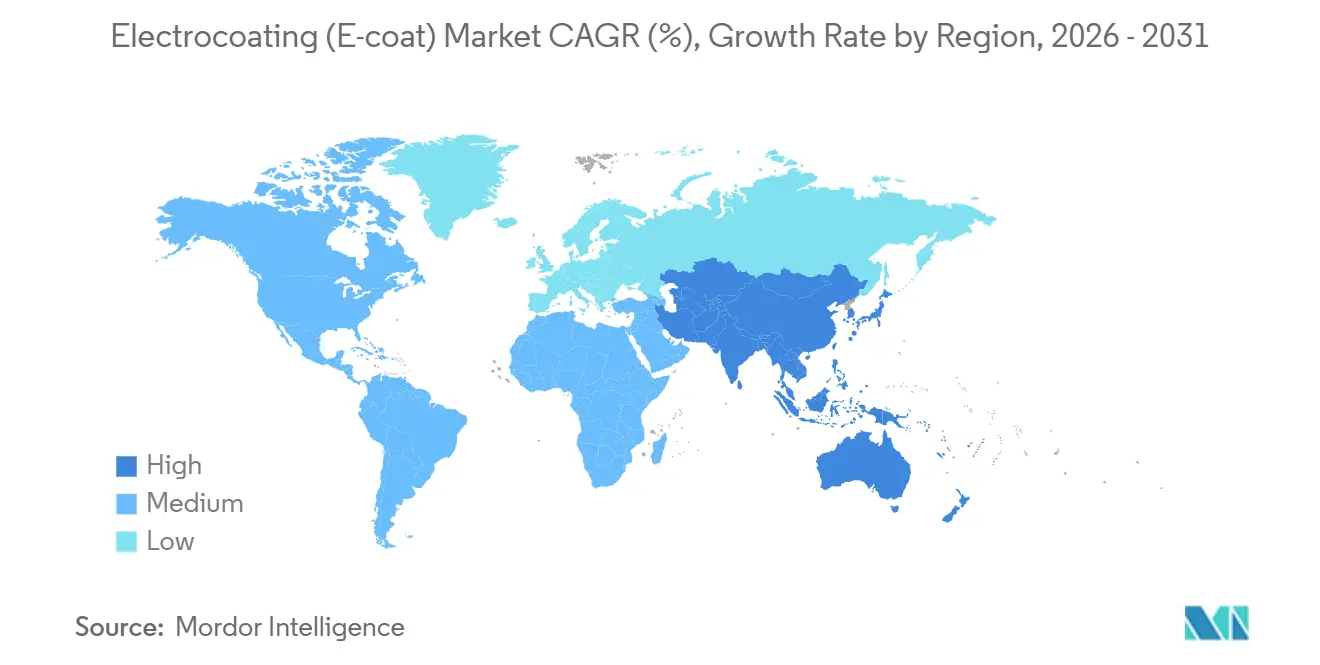

- By geography, Asia-Pacific commanded 55.45% of 2025 demand and is projected to post a 5.05% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Electrocoating (E-coat) Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automotive production growth in Asia-Pacific | +1.8% | Asia-Pacific core, spillover to ASEAN | Medium term (2-4 years) |

| Superior corrosion-resistance vs. solvent-borne primers | +1.2% | Global | Long term (≥ 4 years) |

| EV battery housings adopting e-coat for dielectric shielding | +1.0% | Global, concentrated in China, US, Germany | Medium term (2-4 years) |

| Nano-enabled formulas improving edge-coverage and throw-power | +0.6% | North America, Europe, Japan | Medium term (2-4 years) |

| Nearshoring of ag-equipment production in LATAM countries | +0.4% | South America (Brazil, Argentina, Mexico) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Automotive Production Growth in Asia-Pacific

In 2024, the Asia-Pacific region produced a significant number of vehicles, with China and India being major contributors. This output solidified the region's dominance in structural coating demand. To meet a decade-long OEM corrosion warranty, every body-in-white underwent cathodic e-coat immersion. Following a GST reduction in 2025, India's local vehicle sales experienced substantial growth, compelling toll coaters to implement second shifts. Both Thailand and South Korea saw similar upticks. Additionally, as EVs now bear heavier battery packs, regulations mandate thicker films on their underbodies. With production concentrated in specific areas, formulators strategically co-located plants, effectively mitigating inventory risks associated with short-shelf-life epoxy dispersions. These trends are projected to account for a significant portion of the Electrocoating market volume by 2031.

Superior Corrosion-Resistance vs. Solvent-Borne Primers

Cathodic e-coat exhibits superior salt-spray durability compared to solvent primers. This advantage has become more prominent as OEM warranties have extended. Due to its high transfer efficiency, overspray waste is significantly reduced, leading to lower VOC output per vehicle. This development facilitates compliance with U.S. EPA Tier 3 and EU Stage V regulations. BASF’s CathoGuard 800 RE has successfully reduced bake temperatures, which decreases natural gas consumption while maintaining optimal edge coverage. Although establishing a greenfield dip line requires substantial investment, spreading this cost over time ensures that the per-unit coating expense remains competitive, supporting the growth of the Electrocoating market during the forecast period of 2026–2031.

EV Battery Housings Adopting E-Coat for Dielectric Shielding

Battery enclosures are evolving, transitioning from 400 V to 800 V, and are now testing 1,000 V architectures. This shift increases concerns over dielectric failures. Epoxy e-coats, enhanced with aluminosilicate fillers, achieve a high dielectric strength at just 25 μm thickness. This innovation effectively reduces the risk of arc-tracking, even in challenging, high-salt environments. PPG’s POWERCRON line, now tin-free, has replaced bismuth and zirconium catalysts[1]PPG Industries, “POWERCRON 6000 Series – Tin-Free Cathodic Electrocoat,” ppg.com. This change ensures compliance with EU REACH Regulations, all while preserving edge protection. While OEMs experienced substantial write-downs on EVs during 2024–2025, stalling the swift adoption of 100% BEVs, demand persists. Hybrid and extended-range models continue to require comprehensive e-coats and tray insulation, indicating a cautious but steady growth trajectory during the forecast period of 2026–2031. Henkel’s Alodine pretreatment enhances adhesion on aluminum housings, effectively addressing delamination challenges.

Nano-Enabled Formulas Improving Throw Power

Original Equipment Manufacturers (OEMs) can now reduce immersion time without compromising edge build, as nanometer-scale silica and graphene particles shrink the average resin-particle size to a nanometer scale and elevate throw-power ratios. With the elimination of the muffler, enhanced scratch and chip resistance has become vital for electric vehicle (EV) underbodies. Although nano-enabled e-coats are predominantly found in advanced laboratories across North America, Europe, and Japan, they highlight a productivity advantage in the Electrocoating market with increased line throughput. However, the global rollout encounters challenges, as ISO 12944 and ISO 9001 certifications set stringent benchmarks, requiring a salt-spray test and an adhesion standard[2]International Organization for Standardization, “ISO 12944,” iso.org.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited UV stability for exterior plastic parts | -0.5% | Global, acute in high-UV regions (Middle East, Australia, southwestern US) | Medium term (2-4 years) |

| Skilled-operator gap for automated dip-tank processes | -0.3% | North America, Europe | Short term (≤ 2 years) |

| Volatile supply of bio-based epoxy dispersions | -0.2% | Global, concentrated in Europe and North America with sustainability mandates | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited UV Stability for Exterior Plastic Parts

Extended exposure to 340 nm UV light causes epoxy e-coats to chalk. Consequently, OEMs often apply powder clearcoats or choose acrylic primers, particularly on bumpers and mirror caps. While acrylic e-coats preserve their gloss after extended QUV-A exposure, epoxy e-coats do not fare as well. However, acrylics have limitations, lacking in edge-coverage toughness and dielectric strength. In sun-drenched regions like the Middle-East and Australia, premium vehicle programs are gravitating towards unpainted black plastics. This trend has resulted in a decreased e-coatable surface per unit. Current patent filings indicate no forthcoming advancements in resin technology, posing a continuing challenge for the Electrocoating market, with projections extending through the forecast period of 2026–2031.

Skilled-Operator Gap for Automated Dip-Tank Processes

In the U.S. and Europe, seasoned technicians are retiring at a pace outstripping the influx of new trainees. This comes at a time when bath chemistry demands precise pH ranges, specific solids concentrations, and defined conductivity levels. Some plants in North America have reported declines in first-pass yields, resulting in a notable increase in rejects from batches of coated bodies. Although AI-driven analytics platforms are advancing in diagnosing root causes, a small share of global production lines have integrated these tools. This gap threatens to stretch the capacity of the Electrocoating market until vocational training programs can catch up or until digital controls see broader adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Cathodic Systems Anchor Corrosion Performance

In 2025, cathodic systems dominated the market, capturing 97.72% of the volume, and are projected to grow at a compound annual growth rate (CAGR) of 4.67% during the forecast period of 2026–2031. Their dominance is attributed to features such as a high salt-spray endurance and strong dielectric ratings, both of which are crucial for modern electric vehicle (EV) bodies. This segment represented a significant portion of the Electrocoating market in 2025. Ongoing reformulations ensure that cathodic options remain compliant with EU REACH regulations while maintaining strong edge-coverage ratios. Although anodic e-coat occupies a small niche for aluminum extrusions, benefiting from oxide formation that enhances adhesion, its growth rate lags behind the broader Electrocoating market. Anodic baths, which dissolve more metal and generate higher sludge loads, have led many architects and appliance original equipment manufacturers (OEMs) to shift toward powder coatings. This transition, while limiting anodic coatings' growth potential, highlights their favorable adhesion properties on non-ferrous substrates.

Despite the near-monopoly of cathodic technology, which stifles new entrants, opportunities exist in bio-based epoxy dispersions and nano-pigment packages. These innovations could further optimize film build in concealed cavities. Given that ISO 12944 qualification cycles span up to 24 months, any disruptive chemistries aiming to challenge established cathodic suppliers must demonstrate clear sustainability or cost advantages. Looking ahead, anodic coatings are expected to maintain a small market share in the Electrocoating sector through 2031, focusing primarily on architectural aluminum and select consumer electronics housings.

By Technology: Epoxy Formulations Dominate Dielectric Demands

In 2025, epoxy systems dominated the Electrocoating market, capturing a substantial 90.76% share. With a projected expansion at a 4.58% CAGR during the forecast period of 2026–2031, epoxies are preferred for their high crosslink density, ensuring superior chemical, chip, and dielectric performance. This makes them indispensable for applications such as EV battery trays and galvanized-steel body shells. Pretreatments enhance epoxy pull-off adhesion on aluminum. On the other hand, the acrylic e-coat, with a smaller market share, is renowned for its UV durability and flexibility. While it is a staple on refrigerator shelves and patio furniture, powder systems are increasingly replacing it due to their wastewater elimination advantage.

Recent advancements in nano-silica technology have enhanced epoxy's throw power, allowing OEMs to shorten dip times. This efficiency helps offset the premium cost of epoxy over acrylics. Although bio-epoxy grades are emerging as a solution for reduced Scope 3 emissions, they face hurdles in achieving both volume and price parity.

By Application: Passenger Cars Drive Volume and Innovation

In 2025, passenger cars dominated the Electrocoating market, representing 61.92% of the total volume. These vehicles are experiencing a growth rate of 5.05% CAGR during the forecast period of 2026–2031, primarily driven by the trend of multi-metal lightweighting. This trend not only enhances vehicle performance but also increases the coated surface area per vehicle. As the popularity of crossovers rises, SUVs, which require a higher quantity of e-coat solids than their smaller counterparts, are driving this heightened demand. Meanwhile, commercial vehicles, which command a substantial volume share, are evolving. With mandates from California and Europe pushing for electric delivery vans, these vehicles still require full-body immersion in e-coats. Additionally, the automotive parts and accessories segment holds a significant stake, influenced by trends in aftermarket cycles and outsourcing dynamics from Tier-1 suppliers.

Heavy-duty equipment is gaining attention, particularly with the introduction of nano-enabled formulas. These advanced coatings are now being used to protect boom interiors from the corrosive effects of fertilizer salts. In the realm of appliances, while there is a preference for acrylic e-coats that ensure UV stability for whites, many are considering a transition to powder coatings. A diverse range of residual industrial goods occupies the remaining market share. The stronghold of passenger cars not only cements their dominance but also establishes a stable demand foundation. This stability enables the Electrocoating market to withstand fluctuations typically observed in sectors such as construction or consumer electronics.

Geography Analysis

In 2025, the Asia-Pacific region dominated the electrocoating market, accounting for 55.45% of the volume. Projections indicate steady growth at a CAGR of 5.05% during the forecast period of 2026–2031. China's robust output, coupled with a sales surge in India, driven by the GST, fuels this expansion. In 2025, China's production of BEVs spiked the demand for dielectric shielding. Concurrently, Thailand and South Korea rolled out hybrid lines, necessitating thicker 25 μm films for their heavier battery packs. Japan's pivot towards hybrids has ensured its base volumes remain stable.

North America, boasting a significant share in 2025, is poised for consistent growth. Mexico's export boom has spurred the creation of new dip tanks in Guanajuato and Querétaro, serving both automotive and agricultural machinery frames. However, a notable write-down on EV assets has tempered enthusiasm for ultra-high-voltage battery trays. In the United States, a shortage of skilled operators has constrained capacity utilization, inching first-pass yields towards their optimal mark.

Europe, commanding a substantial portion of the 2025 volume, is on a steady growth path. The region faced hurdles with a slower-than-expected BEV adoption and stringent tin catalyst restrictions, resulting in costly reformulations. While Germany led the demand charge, the United Kingdom and Italy experienced volume declines as OEMs pivoted to more cost-effective eastern plants. South America, with its modest share, saw growth driven by tractor nearshoring in Brazil and Argentina. In contrast, the Middle-East lagged, hindered by limited local vehicle assembly and a reliance on pre-coated imports.

Competitive Landscape

The electrocoating (E-Coat) market is moderately consolidated. Regional toll coaters and captive OEM lines are introducing fragmentation and creating new opportunities in the market. Startups focusing on bio-based resins are targeting niches aimed at carbon reduction. However, they face challenges such as cost premiums and feedstock price fluctuations. Patent activity is heavily concentrated on tin-free catalysts and nano-additives. This trend is compelling established players to update their portfolios while safeguarding decades of validation data from OEMs. A new competitive frontier is emerging with process analytics software, which links bath chemistry to defect maps. This innovation aims to bridge the skilled-labor gap, while also seeking to elevate first-pass yields closer to the optimal mark in established plants.

Electrocoating (E-coat) Industry Leaders

PPG Industries Inc.

Axalta Coating Systems

BASF SE

The Sherwin-Williams Company

Nippon Paint Holdings Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: PPG unveiled pretreatment and e-coat for corrosion protection and dielectric-isolation platforms, including PPG CORATHERM TCA-4000, at The Battery Show Europe.

- April 2024: BASF expanded its Mangalore e-coat plant to supply CathoGuard 800 RE across India, South Asia, and ASEAN, citing escalating EV and lightweight-vehicle demand.

Global Electrocoating (E-coat) Market Report Scope

Electrocoating (E-Coat) is defined as a water-based painting process that utilizes electric currents to deposit paint onto conductive metal substrates. This technique is recognized for its ability to deliver uniform, durable, and corrosion-resistant finishes, making it ideal for coating complex geometries with precise film thicknesses.

The market is segmented by type, technology, application, and geography. By type, the market is segmented into cathodic and anodic. By technology, the market is segmented into epoxy coating technology and acrylic coating technology. By application, the market is segmented into passenger cars, commercial vehicles, automotive parts and accessories, heavy-duty equipment, appliances, and other applications. The report also covers the market size and forecasts for the market in 15 countries across major regions. For each segment, the market sizing and forecasts are done based on volume (Tons).

| Cathodic |

| Anodic |

| Epoxy Coating Technology |

| Acrylic Coating Technology |

| Passenger Cars |

| Commercial Vehicles |

| Automotive Parts and Accessories |

| Heavy Duty Equipment |

| Appliances |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Cathodic | |

| Anodic | ||

| By Technology | Epoxy Coating Technology | |

| Acrylic Coating Technology | ||

| By Application | Passenger Cars | |

| Commercial Vehicles | ||

| Automotive Parts and Accessories | ||

| Heavy Duty Equipment | ||

| Appliances | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large will the global Electrocoating market demand be by 2031?

Volume is forecast to reach 864.04 kilotons by 2031, up from 687.41 kilotons in 2026 at a 4.68% CAGR in this period.

Which segment will add the most incremental volume?

Passenger cars will lead, expanding at a 5.05% CAGR (2026-2031) as Asia-Pacific vehicle builds climbs and EV architectures widen coated surface areas.

What is the main geographic growth engine?

Asia-Pacific, led by China and India, captures 55.45% of 2025 volume and posts a 5.05% CAGR through 2031 as regional OEM clusters expand.

How are suppliers responding to sustainability pressure?

Formulators are pushing bio-based epoxies, tin-free catalysts, and 160 °C bake chemistries that cut Scope 1 and Scope 3 emissions without compromising performance.

What challenges could slow market expansion?

Limited UV stability on exterior plastics, a skilled-operator shortfall in automated dip lines, and volatile pricing for bio-epoxy feedstocks could trim CAGR.

Page last updated on: