Electric Wheelchair Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

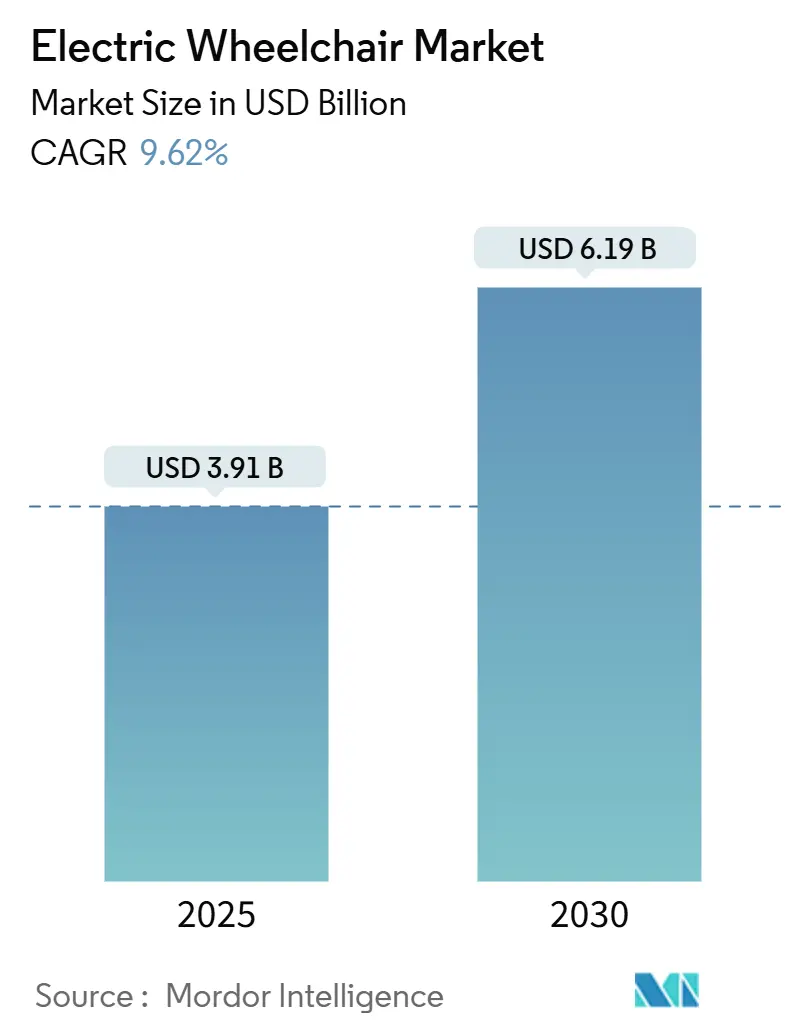

| Market Size (2025) | USD 3.91 Billion |

| Market Size (2030) | USD 6.19 Billion |

| Growth Rate (2025 - 2030) | 9.62% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

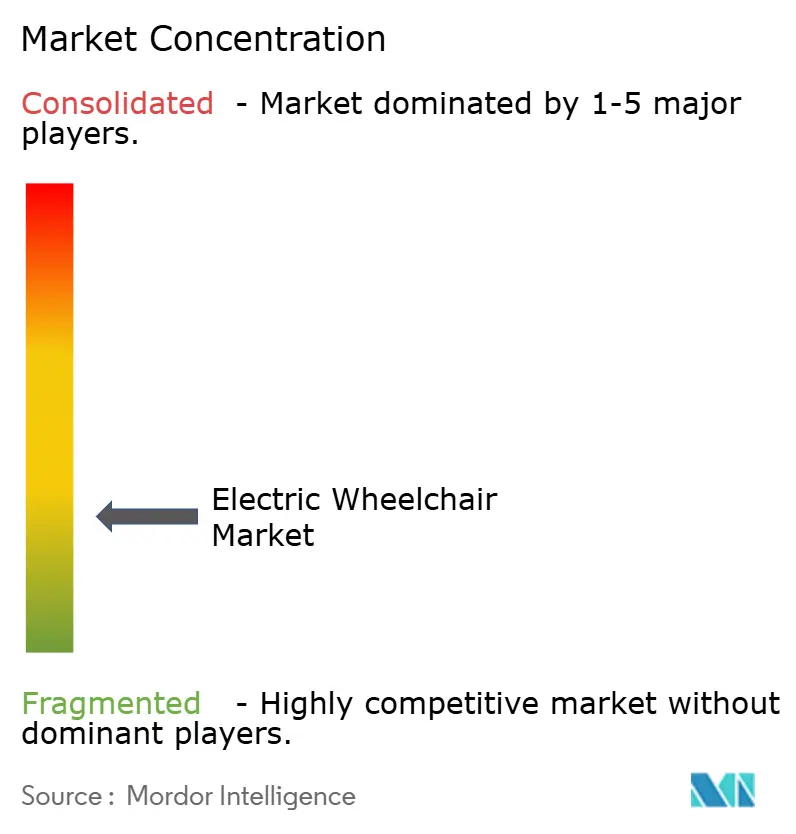

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Electric Wheelchair Market Analysis by Mordor Intelligence

The electric wheelchair market is estimated at USD 3.91 billion in 2025 and is projected to reach USD 6.19 billion by 2030, expanding at a CAGR of 9.62%. This robust growth trajectory reflects the convergence of demographic imperatives and technological breakthroughs reshaping mobility assistance paradigms. The United Nations (UN) projects the global population will peak at 10.3 billion by the mid-2080s, with 63 countries, including China and Japan, already experiencing population decline, creating an unprecedented aging demographic that drives sustained demand for advanced mobility solutions.[1]"World Population Prospects 2024," United Nations, population.un.org.

Key Report Takeaways

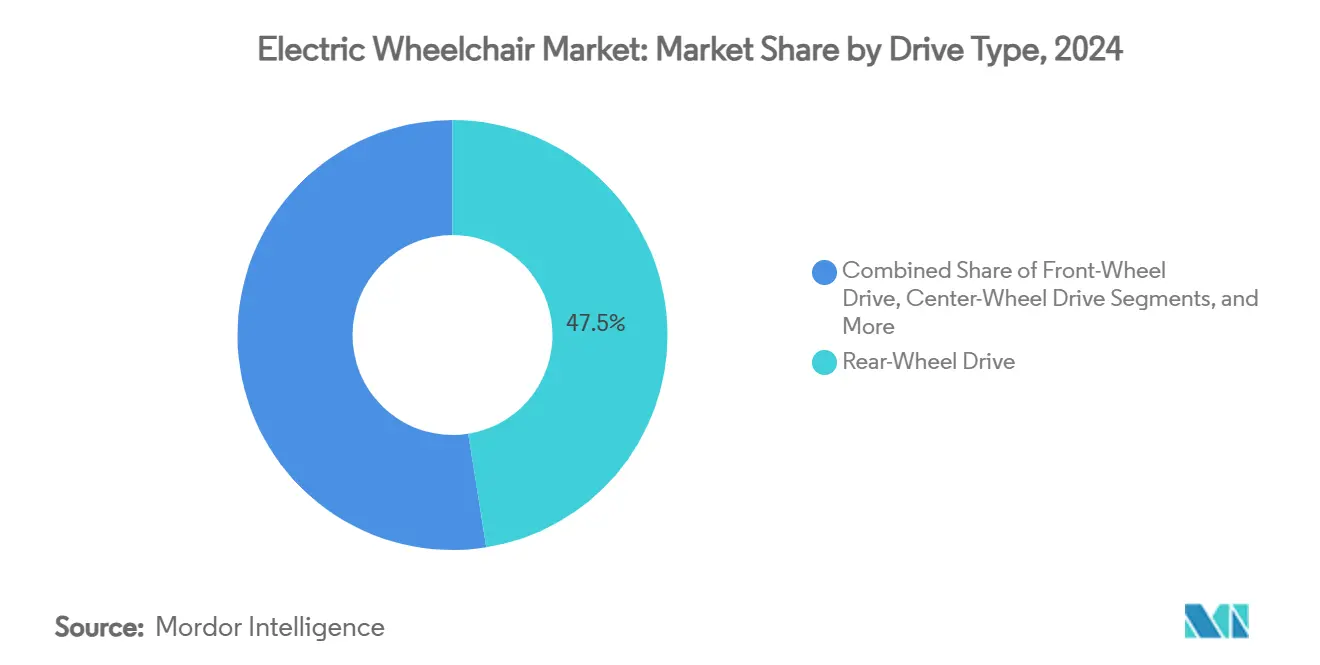

- By drive type, rear-wheel configurations led with 47.49% of the electric wheelchair market share in 2024, and are also projected to post the fastest 10.21% CAGR through 2030.

- By end user, the hospital segment accounted for 61.36% of the electric wheelchair market size in 2024, whereas personal applications are on track for a 9.78% CAGR to 2030.

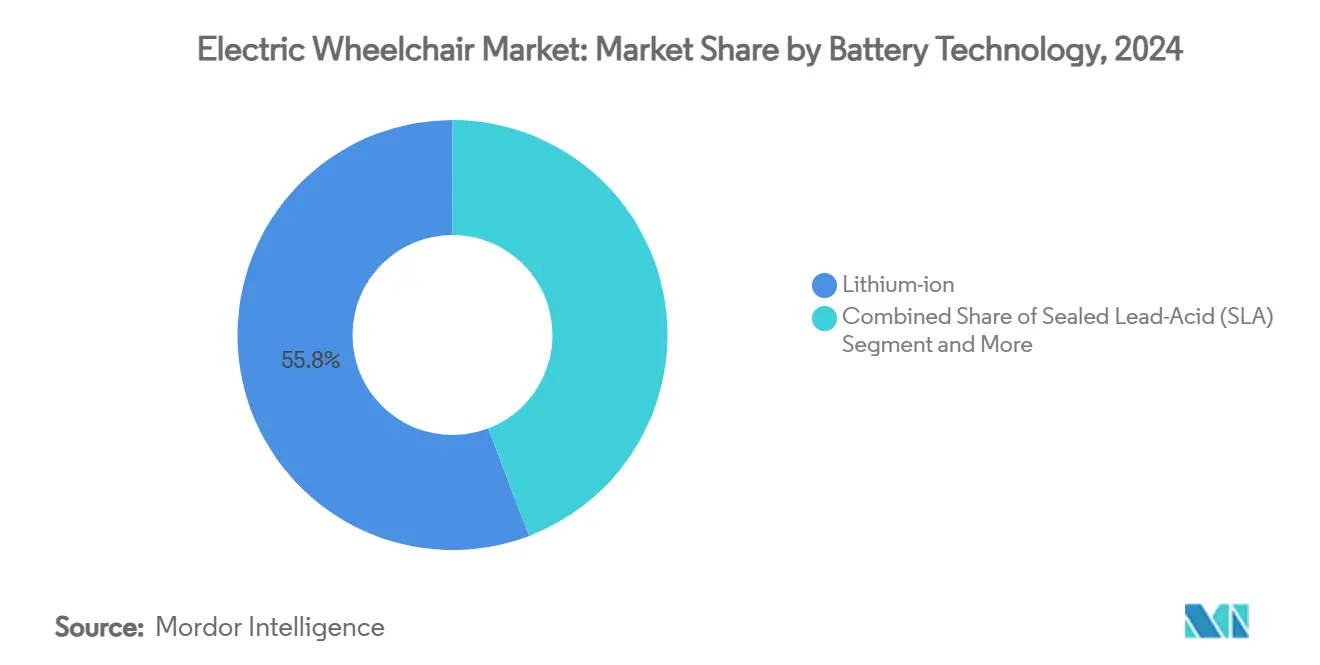

- By battery technology, lithium-ion packs held 55.80% share of the electric wheelchair market size in 2024 and are expanding at an 11.68% CAGR.

- By distribution channel, dealer and offline retail dominated with 66.30% revenue share in 2024; online sales are expected to climb 14.30% annually through 2030.

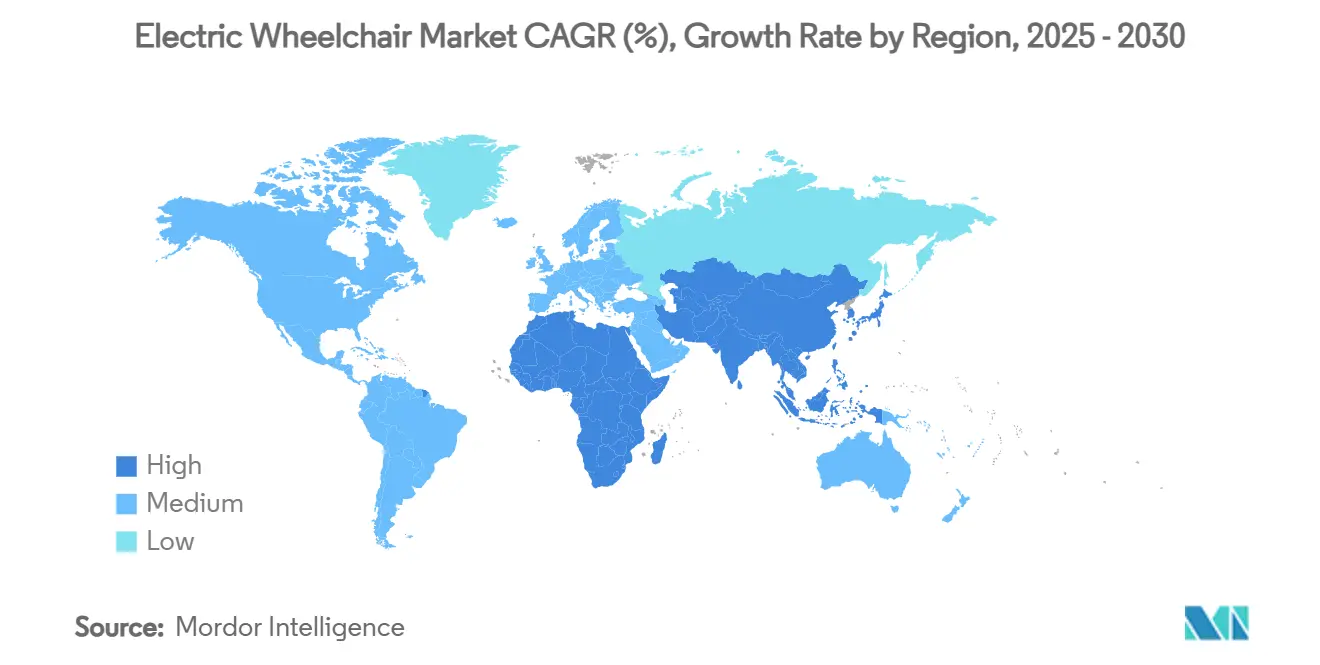

- By geography, North America captured 38.96% of the electric wheelchair market size in 2024, while Asia-Pacific is forecasted to grow the fastest at 11.93% CAGR.

Global Electric Wheelchair Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing Population and Rising Disability Prevalence | +2.8% | Global, concentrated in developed economies | Long term (≥ 4 years) |

| Rapid Lithium-Ion Price Decline Lowers Total Cost of Ownership | +1.9% | Global, led by Asia-Pacific manufacturing hubs | Medium term (2-4 years) |

| OEM Dealer-Network Expansion in Tier-2 Chinese Cities | +1.2% | China, with spillover to Southeast Asia | Medium term (2-4 years) |

| Automotive-Grade Sensor Adoption Enabling Smart Wheelchairs | +1.1% | Global, early adoption in developed markets | Long term (≥ 4 years) |

| Surge in Compact Foldable Power Wheelchairs for Travel Users | +0.8% | North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Rise of Pay-Per-Use Mobility Platforms in Europe | +0.4% | Europe, pilot programs in urban centers | Short term (≤ 2 years) |

Source: Mordor Intelligence

Ageing Population and Rising Disability Prevalence

UN projections show a steep climb in the global cohort aged 65+ through 2050, ensuring unrivalled demand for mobility aids. The number of wheelchairs needed already exceeds 65 million people worldwide and is forecast to rise 22% this decade, propelled by spinal cord injuries, stroke, and osteoarthritis. Mature economies face parallel pressure as labour shortages stretch caregiving resources, making powered mobility vital for independent living. Emerging markets encounter similar demographic shifts but lack reimbursement depth, driving interest in affordable imports. Together, these forces underpin resilient, cross-regional growth for the electric wheelchair market.

Rapid Lithium-Ion Price Decline Lowers Ownership Cost

Argonne National Laboratory pegs average lithium-ion pack costs USD 140/kWh in 2023 and foresees a slide to USD 86/kWh by 2035, with faster drops possible under green-energy incentives.[2]"Cost Analysis and Projections for U.S.-Manufactured Automotive Lithium-ion Batteries," Argonne National Laboratory, publications.anl.gov. Falling chemistry costs let OEMs fit bigger batteries, extending range and reducing charge anxiety. Electric-vehicle supply chains offer scale economies that spill into medical devices, shrinking unit costs for cells, BMS, and chargers. Advanced thermal-management modules originally designed for cars now appear in premium wheelchairs, boosting safety and lifecycle. Combined, these factors cut lifetime operating expense, widening the addressable demand for the electric wheelchair market.

OEM Dealer-Network Expansion in Tier-2 Chinese Cities

China’s ageing curve mirrors developed regions, yet distribution remains thin outside megacities. OEMs are adding showrooms and service workshops in rapidly urbanizing Tier-2 hubs such as Chengdu, Wuhan, and Nanjing. Localized inventory shortens delivery times from weeks to days, a decisive factor for families buying high-ticket medical gear. Community-care reforms and tax breaks further improve sales economics. Regional presence also helps brands navigate provincial tender rules, securing institutional deals that amplify volume. The result is a pronounced uplift in electric wheelchair market penetration across inland China.

Surge in Compact Foldable Electric Wheelchairs for Travel Users

Airline inclusive policies now oblige carriers to accommodate powered mobility devices, yet bulky wheelchairs strain cargo holds. Lightweight frames made from carbon fiber or aerospace-grade aluminum shed up to 40% mass without compromising load rating. Higher-density cells shrink battery footprints, letting travelers fold units small enough for overhead stowage. Older adults with healthy travel appetites value such designs, driving premium adoption in North America and Europe. Short certification cycles and modular accessory kits hasten time-to-market, ensuring rapid turnover of model lines within the electric wheelchair market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Device Purchase and Maintenance Cost | -1.8% | Global, acute in developing economies | Long term (≥ 4 years) |

| Limited Insurance Cover in Developing Economies | -1.4% | Emerging markets, concentrated in Asia-Pacific and MEA | Long term (≥ 4 years) |

| Lithium-Ion Fire-Safety Regulatory Gaps | -0.9% | Global, stricter enforcement in EU and North America | Medium term (2-4 years) |

| Global Aluminum and Rare-Earth Price Volatility | -0.7% | Global, supply chain concentrated in China | Short term (≤ 2 years) |

Source: Mordor Intelligence

High Device Purchase Maintenance Cost

Top-tier models priced between USD 8,000 and USD 30,000 remain out of reach for underinsured users. Complex electronics, servo motors, and custom seating inflate annual maintenance to 15-20% of upfront outlay. Medicare approval often entails lengthy physician documentation that delays funding, prompting cash-strapped buyers to postpone upgrades. In rural zones, certified technicians are scarce, forcing owners to ship their units long distances for repairs. Such hurdles moderate adoption speed and suppress the full potential of the electric wheelchair market.

Limited Insurance Cover in Developing Economies

World Bank data show assistive-technology spend accounting for less than 1% of public health budgets across lower-middle-income nations. Indonesian studies reveal that households with disabilities face living-cost premiums that erode disposable income, pushing electric wheelchairs beyond reach. Private insurers seldom reimburse durable medical equipment, and national schemes prioritize acute care over rehabilitation. Without financing, latent demand remains unconverted, restraining electric wheelchair market acceleration in Asia-Pacific and Africa.

Segment Analysis

By Drive Type: Rear-wheel Drive Wheelchairs Accelerate Growth

The rear-wheel drive segment of the electric wheelchair market accounted for 47.49% of the market in 2024 and emerged as the fastest-growing segment, with a 10.21% CAGR through 2030. Rear-wheel drive systems dominate due to their superior outdoor performance and stability on uneven terrain. In contrast, center-wheel drive configurations serve indoor navigation requirements with tight turning radii, which is essential for residential use.

Front-wheel drive models occupy specialized niches for users requiring maximum forward visibility and obstacle navigation, particularly in occupational therapy and rehabilitation settings. All-wheel and hybrid drive systems represent emerging categories that combine multiple propulsion methods to optimize performance across diverse environments, though adoption remains limited by complexity and cost considerations. The drive type selection increasingly reflects lifestyle preferences rather than medical requirements, as users seek devices that enable participation in recreational activities and social engagement beyond basic mobility assistance.

Note: Segment shares of all individual segments available upon report purchase

By End User: Personal Applications Drive Diversification

Hospitals commanded 61.36% of the market share in 2024. However, the personal segment represents the fastest-growing at 9.78% CAGR through 2030, signaling expansion beyond traditional medical applications. This diversification challenges manufacturers to develop products that balance medical device regulations with performance requirements for active use environments.

Hospitals and clinics maintain steady demand for institutional-grade devices designed for multiple users and intensive daily operation. At the same time, rehabilitation centers increasingly specify advanced models with programmable settings for therapeutic progression. Long-term care facilities represent a stable but mature segment, with purchasing decisions driven by durability and maintenance considerations rather than advanced features. The emergence of sports and adventure applications creates opportunities for specialized product lines incorporating ruggedized components and enhanced performance capabilities, potentially commanding premium pricing while expanding the addressable market beyond traditional healthcare channels.

By Battery Technology: Lithium-Ion Dominates Growth

Lithium-ion technology captures both market leadership with 55.80% share in 2024 and fastest growth at 11.68% CAGR through 2030, benefiting from automotive industry cost reductions and performance improvements. The dual dominance reflects lithium-ion's superior energy density, lighter weight, and longer cycle life than traditional sealed lead-acid alternatives, creating compelling value propositions despite higher initial costs. EU Battery Regulation 2023/1542 introduces sustainability requirements, including carbon footprint disclosure and recycled content mandates, favoring lithium-ion manufacturers with established supply chain traceability.

Sealed lead-acid batteries retain considerable market presence due to lower upfront costs and established recycling infrastructure, particularly in price-sensitive segments and developing markets where total cost of ownership calculations favor initial affordability over long-term performance. Other battery technologies, including nickel-metal hydride and gel variants, serve specialized applications requiring specific performance characteristics or regulatory compliance, though market share continues declining as lithium-ion costs decrease. The regulatory landscape increasingly favors advanced battery chemistries, with NHTSA's FMVSS No. 305a establishing enhanced safety standards for electric vehicle batteries that will likely extend to mobility devices

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Digital Transformation Accelerates

Dealer and offline retail channels maintain dominance with 66.30% market share in 2024, reflecting the importance of personal consultation, product demonstration, and fitting services in electric wheelchair selection and customization. However, online and e-commerce channels represent the fastest-growing distribution method at 14.30% CAGR through 2030, driven by improved virtual consultation capabilities and direct-to-consumer business models that reduce intermediary costs. The digital transformation enables manufacturers to capture higher margins while providing competitive pricing to end users. However, regulatory requirements for medical device sales create compliance complexities in direct-to-consumer models.

Institutional procurement channels serve healthcare facilities and government programs with standardized specifications and bulk purchasing arrangements, creating stable revenue streams but limiting profit margins through competitive bidding processes. The distribution channel evolution reflects broader healthcare trends toward patient-centered care delivery and consumer empowerment in medical device selection. Service-focused delivery models emerge as manufacturers recognize that ongoing support and maintenance services create recurring revenue opportunities while improving customer satisfaction and device utilization outcomes.

Geography Analysis

North America commands the largest revenue pool with a market share of 38.96%, reflecting mature healthcare infrastructure and comprehensive reimbursement systems. However, growth moderates as market penetration approaches saturation levels in key demographic segments. The region benefits from established distribution networks and regulatory clarity through FDA medical device pathways, enabling rapid adoption of technological innovations. Medicare coverage guidelines, despite complexity, provide predictable funding mechanisms that support premium device adoption among qualifying users.

Asia-Pacific is the fastest growing with a CAGR of 11.93% over the forecast period, adding incremental USD 1.1 billion to the electric wheelchair market size over 2025-2030. China’s Tier-2 expansion campaign yields double-digit volume growth as local distributors open warranty depots within a 150 km radius of target populations. Japan’s fast-ageing demographic prefers premium smart-wheelchairs integrated with home-automation systems, a segment growing 15% annually. Australia and South Korea see government-backed voucher schemes subsidizing up to USD 4,000 of purchase cost, directing demand toward mid-range lithium-ion models. Nevertheless, fragmented regulatory regimes and variable GST rates require adaptable pricing and certification tactics for successful entry.

Europe retains a technologically sophisticated consumer base. The EU Battery Regulation 2023/1542 establishes global precedent for sustainability requirements in battery-powered devices, creating competitive advantages for manufacturers with established environmental compliance capabilities.[3]"Regulation (EU) 2023/1542 of the European Parliament and of the Council of 12 July 2023 concerning batteries and waste batteries, amending Directive 2008/98/EC and Regulation (EU) 2019/1020 and repealing Directive 2006/66/EC," EUR-Lex, eur-lex.europa.eu. Urban pay-as-you-go platforms in Germany and Spain proliferate, giving casual users access to premium devices without ownership burdens. Eastern Europe records higher unit growth as EU cohesion funds modernize rehabilitation hospitals and elder-care centers. The Middle East and Africa account for under 5% of global value today. Still, Gulf Cooperation Council states exhibit accelerating procurement driven by public-sector hospital expansion and inclusive-city initiatives ahead of major sporting events. South Africa’s disability-grant uplift boosts household purchasing power, yet after-sales logistics remain a bottleneck. Collectively, these patterns highlight geographic segmentation as a key determinant of the marketing mix within the electric wheelchair market.

Competitive Landscape

Market concentration reflects ongoing consolidation as institutional investors recognize long-term demographic trends and technological convergence opportunities, with major transactions including Platinum Equity's acquisition of Sunrise Medical in September 2024 and MIGA Holdings' purchase of Invacare's North American operations in November 2024. These strategic moves signal confidence in market fundamentals despite regulatory challenges and supply chain complexities affecting the broader durable medical equipment sector. The competitive intensity increases as traditional medical device manufacturers face competition from technology companies leveraging automotive industry innovations in sensors, battery management, and user interface design.

Technology is the new battleground. Suppliers can stand out by integrating lidar arrays, machine-learning controllers, and Bluetooth-based caregiver apps. Brain–computer interface pilots, executed with university partners, promise hands-free control for high-level injury patients, extending product differentiation. Software ecosystems matter; open-API models allow third-party developers to add custom modules, embedding the wheelchair within broader assistive-tech stacks. Component partnerships with EV battery makers such as CATL and LG Energy Solution cut costs and ensure regulatory-grade traceability.

Service innovation complements hardware. Subscription bundles that combine leasing, repair, tele-rehab, and periodic upgrades appeal to urban millennials caring for ageing parents. Predictive-maintenance dashboards trim downtime and reduce warranty claims. Dealer training moves online, lowering onboarding costs and speeding coverage in secondary towns. With users demanding personalized setups, competitive strength now hinges on the interplay of hardware adaptability, digital connectivity, and after-sales responsiveness - core levers that will decide share shifts in the electric wheelchair market.

Electric Wheelchair Industry Leaders

-

Permobil AB

-

OttoBock Healthcare

-

Pride Mobility Products Corp.

-

Sunrise Medical GmbH (Platinum Equity)

-

Invacare Corporation (MIGA Holdings)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Scientists at the Indian Institute of Technology Madras (IIT Madras) developed India’s most customizable Electric Standing Wheelchair, NeoStand. The wheelchair is a compact standing wheelchair where wheelchair users can effortlessly transition from sitting to standing at the touch of a button.

- March 2024: Sunrise Medical announced the launch of the Switch-It Vigo head control, a proportional head control that allows drivers to control their wheelchairs and other devices with gentle and intuitive head movements.

- January 2024: Sunrise Medical announced the launch of the Switch-It Vigo head control, a proportional head control that allows drivers to control their wheelchairs and other devices with gentle and intuitive head movements.

Global Electric Wheelchair Market Report Scope

Electric wheelchairs, commonly referred to as power wheelchairs, serve as vital mobility aids for individuals with limited upper body strength or those unable to maneuver manual wheelchairs. Powered by battery-operated motors, these devices grant users enhanced independence and mobility.

The electric wheelchair market is segmented by type, end-user, and geography. By type, the market is segmented into front-wheel drive, center-wheel drive, rear-wheel drive, and standing electric wheelchair. By end-user, the market is segmented into personal, hospitals, and sports conditioning. By geography, the market is segmented into North America, Europe, Asia-Pacific, and the rest of the world.

The report offers market size and forecasts for the Electric Wheelchair Market in value (USD) for the above-mentioned segments.

| By Drive Type | Front-Wheel Drive | ||

| Centre-Wheel Drive | |||

| Rear-Wheel Drive | |||

| Standing/Standing-Up | |||

| All-Wheel/Hybrid Drive | |||

| By End User | Personal/Homecare | ||

| Hospitals and Clinics | |||

| Rehabilitation Centres | |||

| Sports and Adventure Conditioning | |||

| Long-Term Care Facilities | |||

| By Battery Technology | Sealed Lead-Acid (SLA) | ||

| Lithium-ion | |||

| Others (NiMH, Gel) | |||

| By Distribution Channel | Dealer/Offline Retail | ||

| Online/E-commerce | |||

| Institutional Procurement | |||

| By Geography | North America | United States | |

| Canada | |||

| Rest of North America | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Saudi Arabia | ||

| United Arab Emirates | |||

| Egypt | |||

| Turkey | |||

| South Africa | |||

| Rest of Middle East and Africa | |||

| Front-Wheel Drive |

| Centre-Wheel Drive |

| Rear-Wheel Drive |

| Standing/Standing-Up |

| All-Wheel/Hybrid Drive |

| Personal/Homecare |

| Hospitals and Clinics |

| Rehabilitation Centres |

| Sports and Adventure Conditioning |

| Long-Term Care Facilities |

| Sealed Lead-Acid (SLA) |

| Lithium-ion |

| Others (NiMH, Gel) |

| Dealer/Offline Retail |

| Online/E-commerce |

| Institutional Procurement |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Egypt | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

What is the current value of the electric wheelchair market?

The Electric Wheelchair Market size is expected to reach USD 3.91 billion in 2025 and grow at a CAGR of 9.62% to reach USD 6.19 billion by 2030.

Which region will grow the fastest through 2030?

Asia-Pacific is projected to expand at a 11.93% CAGR, driven by ageing populations, rising incomes, and improving healthcare coverage.

How are manufacturers differentiating new models?

Firms incorporate automotive-grade sensors, brain–computer interfaces, and IoT diagnostics to create safer, smarter, and more user-friendly wheelchairs.

What recent policy change supports premium wheelchair features in the US?

New HCPCS codes effective March 2025 now reimburse advanced control interfaces and seating accessories under Medicare, encouraging adoption of higher-spec models.

Page last updated on: July 7, 2025