Electric Vehicle Battery Testing Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.3 Billion |

| Market Size (2031) | USD 7.11 Billion |

| Growth Rate (2026 - 2031) | 16.62% CAGR |

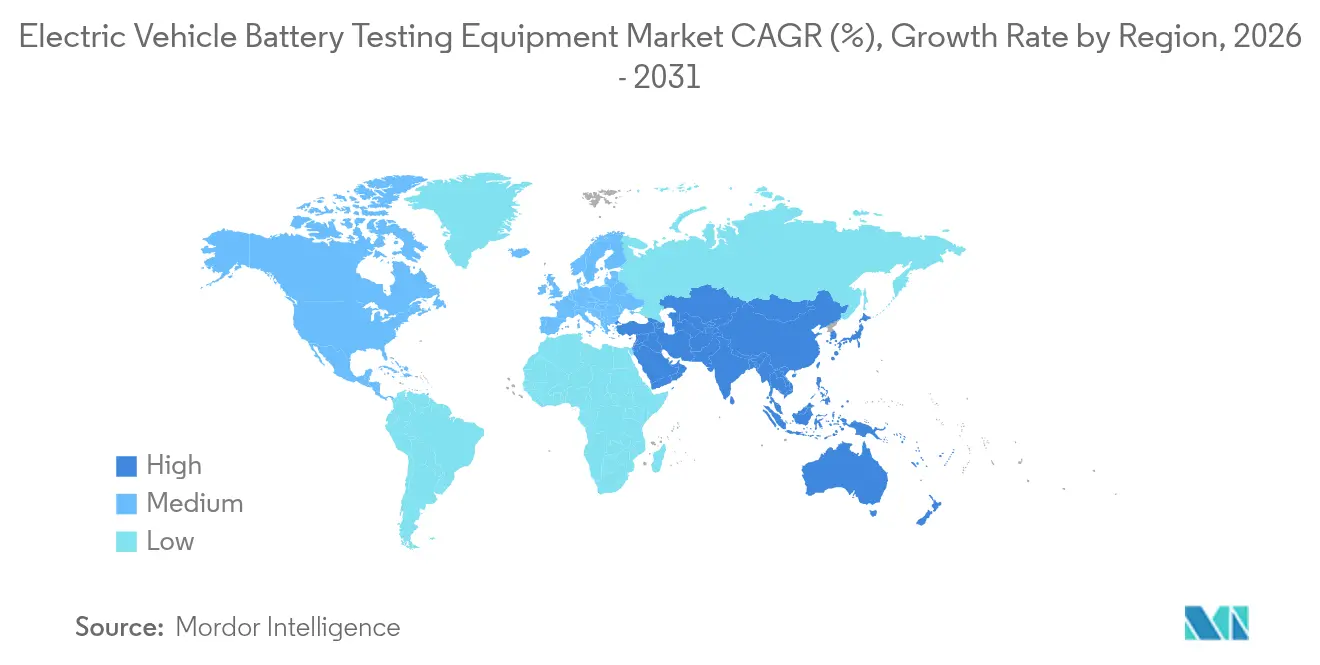

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Electric Vehicle Battery Testing Equipment Market Analysis by Mordor Intelligence

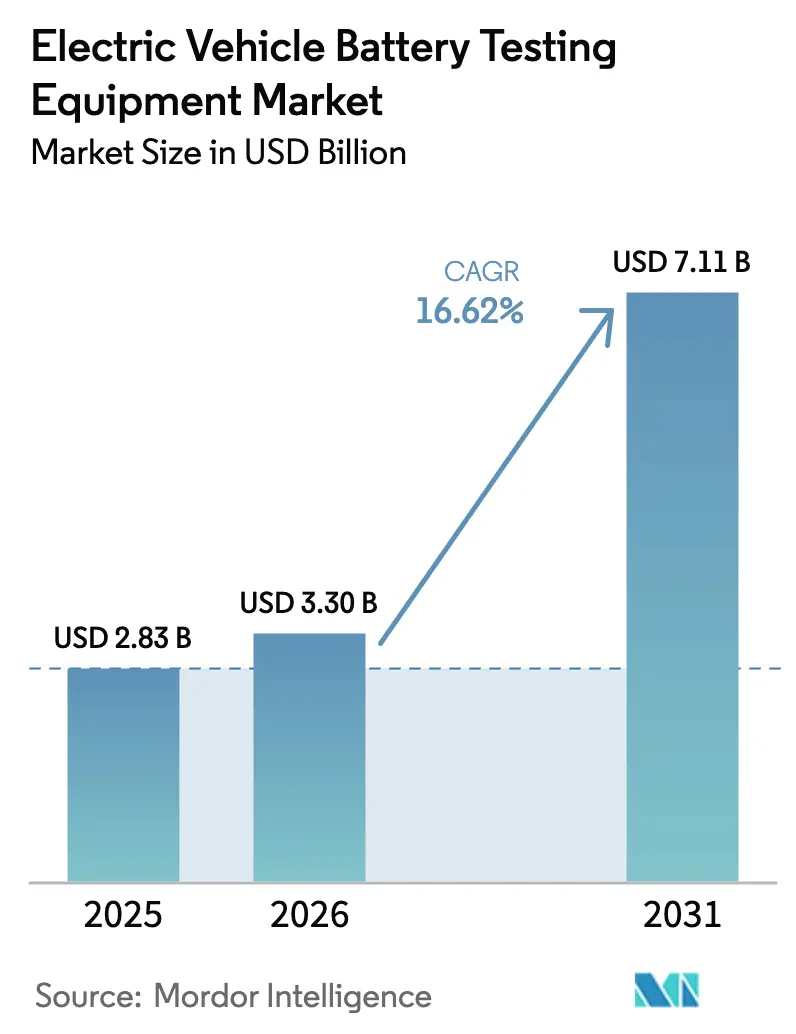

The electric vehicle battery testing equipment market size is expected to grow from USD 2.83 billion in 2025 to USD 3.3 billion in 2026 and is forecast to reach USD 7.11 billion by 2031 at 16.62% CAGR over 2026-2031. Strong growth stems from the convergence of surging EV production volumes, tighter battery-safety regulations, and rapid adoption of high-energy-density chemistries that require more sophisticated validation tools. Intensifying giga-factory construction, particularly across Asia–Pacific and the North American “Battery Belt,” is reshaping capital-equipment demand, while AI-enabled digital-twin software shortens test cycles and helps predict aging patterns. Yet high laboratory build-out costs and long accreditation timelines continue to challenge smaller manufacturers, creating openings for independent laboratories and modular leasing models.

Key Report Takeaways

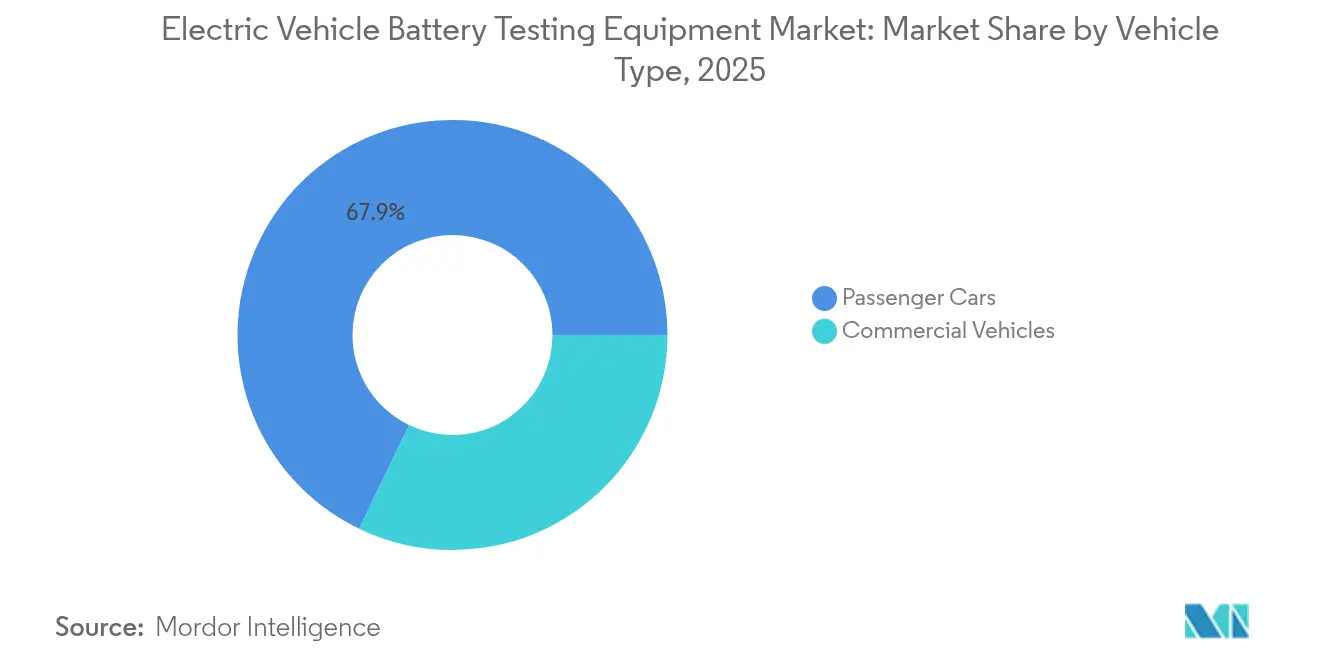

- By vehicle type, passenger cars retained 67.85% of the electric vehicle battery testing equipment market share in 2025, while commercial vehicles are set to grow at an 18.05% CAGR through 2031.

- By propulsion, battery electric vehicles dominated with a 71.35% share of the electric vehicle battery testing equipment market in 2025; fuel-cell electric vehicles are projected to advance at a 23.1% CAGR to 2031.

- By testing methodology, electrical tests captured 45.55% share of the electric vehicle battery testing equipment market in 2025, whereas chemical and abuse tests will post the fastest 18.74% CAGR.

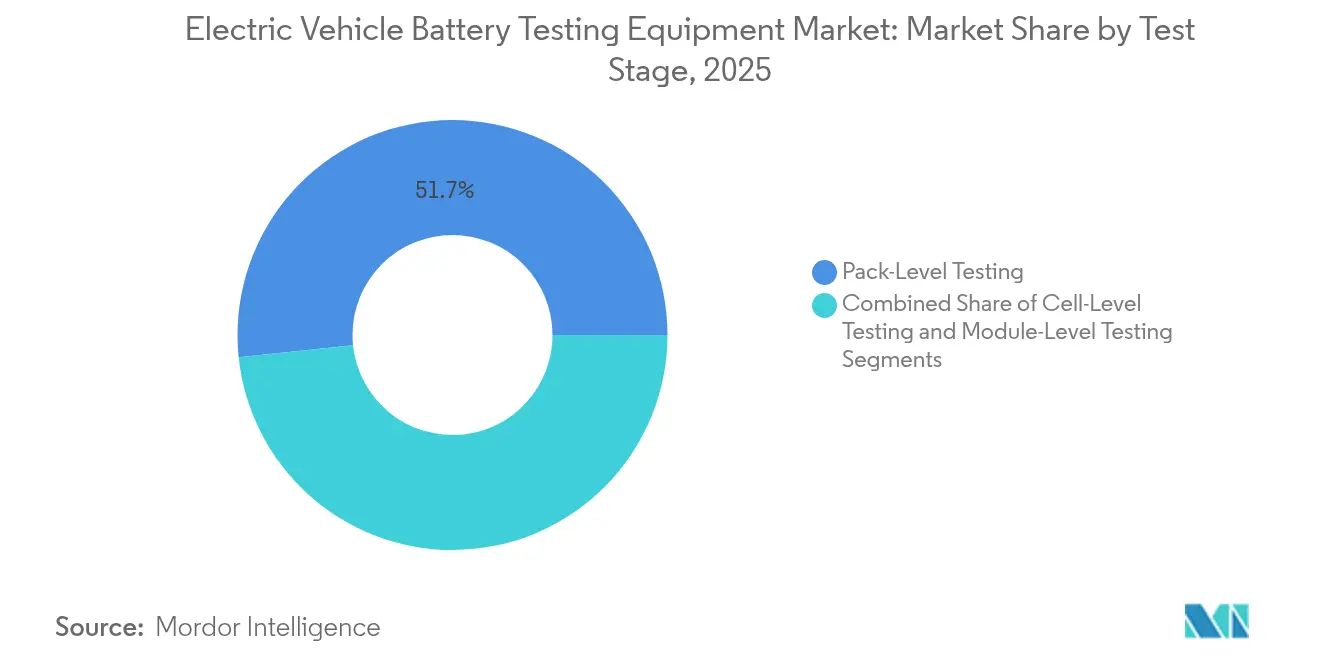

- By the test stage, pack-level testing is led with a 51.65% of the electric vehicle battery testing equipment market share in 2025, but cell-level testing is forecast to expand at a 20.95% CAGR.

- By end-user, automotive OEM laboratories held 56.90% of the electric vehicle battery testing equipment market share in 2025; independent and third-party labs are poised for a 16.95% CAGR through 2031.

- By geography, Asia–Pacific dominated with a 46.05% of the electric vehicle battery testing equipment market share in 2025, and is expected to record the quickest double-digit CAGR of 16.33%.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Electric Vehicle Battery Testing Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging EV Production and Sales Worldwide | +4.2% | Global, with Asia-Pacific Leading at 46% Share | Medium Term (2–4 Years) |

| OEM Giga-Factory Build-Outs Needing In-Line Automated Testers | +3.5% | Global, Concentrated in Battery Belt Regions | Medium Term (2–4 Years) |

| Stringent Battery-Safety Regulations (UN ECE R100, IEC 62660, UL 2580) | +3.1% | Global, with EU and China Driving Compliance | Short Term (≤ 2 Years) |

| Shift to High-Energy-Density Chemistries (Solid-State, NMC 811) | +2.8% | North America and EU, Spill-Over to Asia-Pacific | Long Term (≥ 4 Years) |

| AI-Driven Digital-Twin Test Protocols for Predictive Aging | +1.7% | Asia-Pacific Core, Expanding to North America and EU | Long Term (≥ 4 Years) |

| Battery-Swapping (BaaS) Networks Requiring Ultra-Fast Diagnostic Testers | +1.5% | China Dominant, Pilot Programs in Europe | Medium Term (2–4 Years) |

| Source: Mordor Intelligence | |||

Surging EV Production and Sales Worldwide

Global EV production acceleration creates unprecedented demand for battery testing infrastructure as manufacturers scale from prototype validation to gigafactory-level quality assurance. The International Energy Agency reports EV sales reaching 17 million units in 2024, with battery demand exceeding 750 GWh, requiring comprehensive testing protocols across cell, module, and pack levels[1]"Global EV Outlook 2024", International Energy Agency, iea.blob.. This surge drives testing equipment manufacturers to develop high-throughput solutions that handle diverse battery formats while maintaining precision standards. The shift toward vertical integration among OEMs necessitates in-house testing capabilities, fundamentally altering the traditional outsourced testing model and creating opportunities for automated, integrated testing systems. Honeywell's Battery Manufacturing Excellence Platform exemplifies this trend, utilizing AI to reduce cell manufacturing costs and cut material waste by 60% during startup phases.

OEM Giga-Factory Build-Outs Needing In-Line Automated Testers

Gigafactory expansion across global markets drives demand for integrated, high-speed testing systems capable of real-time quality validation within production lines. Volkswagen's PowerCo advances with a USD 7 billion gigafactory in Ontario, emphasizing flexible manufacturing strategies and technology-agnostic battery cell designs[2]"Volkswagen's EV battery-maker charges ahead with $7 billion gigafactory as rivals’ plans stall", National Observer, nationalobserver.com.. These facilities require end-of-line testing systems to validate electrical performance, thermal management, and safety parameters at production speeds. Digatron's collaboration with HAHN Automation demonstrates this trend, offering comprehensive EOL testing solutions with centralized databases for data analytics and traceability. Integrating testing equipment into production workflows creates opportunities for manufacturers offering turnkey automation solutions.

Stringent Battery-Safety Regulations (UN ECE R100, IEC 62660, UL 2580)

Regulatory tightening across major markets transforms testing requirements from basic compliance to comprehensive safety validation, driving demand for advanced testing equipment. China's new GB38031-2025 standard, effective July 2026, mandates enhanced thermal diffusion testing and a two-hour no-fire/no-explosion condition after thermal events, setting global benchmarks for battery safety. The EU's Battery Regulation 2023/1542 requires digital passports for batteries exceeding 2kWh by 2027, necessitating comprehensive lifecycle tracking and testing documentation. US FMVSS 305a implementation creates additional compliance layers, requiring manufacturers to demonstrate risk mitigation strategies for thermal runaway scenarios[3]"Federal Motor Vehicle Safety Standards; FMVSS No. 305a Electric-Powered Vehicles: Electric Powertrain Integrity Global Technical Regulation No. 20 Incorporation by Reference", Federal Register, federalregister.gov.. These evolving standards drive testing equipment sophistication, with TÜV Rheinland investing EUR 24 million in new traction battery laboratories to meet growing compliance demand.

Shift to High-Energy-Density Chemistries (Solid-State, NMC 811)

The transition toward next-generation battery chemistry fundamentally alters testing requirements, creating demand for specialized equipment that validates solid-state and advanced lithium-ion technologies. Solid-state batteries promise energy densities exceeding 500 Wh/kg but require novel interface stability and thermal management testing protocols, with mass production expected around 2027-2028. Japan leads solid-state patent development with USD 2.24 billion in government subsidies, while US manufacturers focus on commercialization to leapfrog Chinese dominance in traditional lithium-ion technologies. Testing equipment manufacturers adapt by developing higher voltage capabilities up to 2,000V and power levels exceeding 600kW to accommodate these advanced chemistries. The complexity of validating solid-state interfaces and thermal behavior creates opportunities for AI-enhanced testing protocols that can predict performance degradation patterns.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost of Advanced Test Benches | -2.1% | Global, particularly affecting smaller manufacturers | Short term (≤ 2 years) |

| Long Lead Times to Build Accredited Battery Labs | -1.8% | North America and EU, with regulatory bottlenecks | Medium term (2-4 years) |

| Shortage of Skilled Battery-Test Engineers | -1.4% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Rapidly Evolving Standards Risk Equipment Obsolescence | -1.2% | Global, with faster cycles in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Advanced Test Benches

The substantial investment required for comprehensive battery testing infrastructure creates barriers for smaller manufacturers and limits market accessibility, particularly as testing requirements become more sophisticated. Advanced testing systems capable of handling next-generation battery chemistries require investments exceeding USD 10 million for complete laboratory setups, with specialized equipment like thermal runaway chambers and high-voltage testing systems commanding premium pricing. TÜV SÜD's EUR 3 billion revenue milestone in 2024 reflects the scale of investment required for global testing infrastructure, with the company continuously expanding laboratory facilities to meet demand. This capital intensity drives consolidation among testing service providers while creating opportunities for equipment leasing and shared testing facilities. The emergence of AI-powered testing solutions offers potential cost reduction through improved efficiency and reduced testing time. US Army research demonstrates testing time reduction from years to days using machine learning algorithms.

Long Lead Times to Build Accredited Battery Labs

Extended development timelines for certified testing facilities constrain market growth as regulatory requirements and technical complexity increase project duration and costs. Accreditation processes for battery testing laboratories require compliance with ISO 17025 standards and specific automotive requirements, often extending project timelines beyond 24 months from conception to operation. UL Solutions' establishment of its North America Advanced Battery Laboratory in Auburn Hills demonstrates the complexity involved, requiring extensive equipment integration and regulatory approval processes. The shortage of skilled battery testing engineers compounds these delays, with specialized expertise required for advanced testing protocols and equipment operation. Siemens' USD 150 million investment in Canada for a global EV battery R&D hub illustrates the scale of commitment required to develop comprehensive testing capabilities. These extended timelines create opportunities for modular testing solutions and accelerated deployment strategies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Fleets Drive Testing Demand

Passenger cars maintain a 67.85% of the electric vehicle battery testing equipment market in 2025, while commercial vehicles represent the fastest-growing segment at 18.05% CAGR through 2031. Fleet electrification mandates and total cost of ownership advantages drive commercial vehicle adoption, requiring specialized testing protocols for high-duty-cycle applications and extended operational lifespans. Commercial vehicle batteries face unique stress patterns, including frequent charging cycles, varied load conditions, and extended operational hours, necessitating enhanced durability testing and thermal management validation.

The shift toward commercial electrification creates demand for testing equipment capable of simulating real-world operating conditions, including regenerative braking cycles and payload variations. Southwest Research Institute's EVESE-II consortium, launched in August 2024, focuses on battery cell aging and fast charging protocols relevant to commercial applications. Passenger car testing remains the largest segment but faces commoditization pressures as testing protocols standardize. In contrast, commercial vehicle testing commands premium pricing due to application-specific requirements and extended validation periods.

By Propulsion Type: Fuel Cell Growth Challenges BEV Dominance

Battery Electric Vehicles command 71.35% of the electric vehicle battery testing equipment market in 2025. Yet, Fuel Cell Electric Vehicles emerge as the fastest-growing segment at 23.1% CAGR through 2031, driven by heavy-duty applications and hydrogen infrastructure investments. FCEV testing requires specialized fuel cell stack validation protocols, hydrogen storage system safety, and hybrid powertrain integration, creating niche opportunities for testing equipment manufacturers. HORIBA's launch of the C05-LT 100W PEM fuel cell test station in May 2025 demonstrates growing market recognition of FCEV testing requirements.

Plug-in Hybrid EVs maintain steady demand for dual powertrain testing capabilities, while Hybrid EVs face declining testing requirements as manufacturers shift toward full electrification strategies. CamMotive's launch of a dedicated hydrogen fuel cell test facility in Cambridge, UK, with capacity up to 150kW, reflects the specialized infrastructure required for FCEV validation. The complexity of FCEV testing protocols, including durability assessment under varying temperature and humidity conditions, creates barriers to entry and supports premium pricing for specialized testing services.

By Testing Type: Abuse Testing Gains Prominence

Electrical tests dominated the market with a 45.55% of the electric vehicle battery testing equipment market in 2025, reflecting fundamental validation requirements for battery performance and safety characteristics. However, abuse/chemical tests represent the fastest-growing category at a 18.74% CAGR through 2031, driven by regulatory emphasis on thermal runaway prevention and safety validation. China's new GB38031-2025 standard mandates enhanced thermal diffusion testing and bottom impact tests, while EU regulations require comprehensive abuse testing for battery passport compliance.

Thermal testing gains importance as battery energy densities increase and thermal management becomes critical for performance and safety. Developing solid-state batteries requires novel thermal testing protocols to validate interface stability and heat dissipation characteristics. Mechanical testing evolves to address new battery formats and packaging designs, while chemical testing expands to cover advanced electrolyte formulations and solid-state interfaces. AVL's introduction of the Stingray™ One battery fire suppression system demonstrates the growing focus on thermal runaway mitigation and testing.

By Test Stage: Cell-Level Innovation Drives Growth

Pack-level testing maintains a 51.65% of the electric vehicle battery testing equipment market share in 2025, reflecting the critical importance of system-level validation for vehicle integration and safety certification. Cell-level testing emerges as the fastest-growing segment at 20.95% CAGR through 2031, driven by advanced chemistry development and quality control requirements at the manufacturing stage. The shift toward solid-state and next-generation chemistries necessitates comprehensive cell-level characterization to understand performance degradation mechanisms and optimize manufacturing processes.

Module-level testing is an intermediate validation stage, particularly important for manufacturers using standardized cell formats in custom module configurations. Hioki's launch of the Precision Battery Tester BT6065 and BT6075 in 2024 demonstrates the growing sophistication of cell-level testing equipment, with capabilities for next-generation battery cell grading and end-of-line testing. Integrating AI-powered testing protocols at the cell level enables predictive quality assessment and reduces downstream testing requirements, creating efficiency gains throughout the validation process.

By End-User: Independent Labs Expand Market Reach

Automotive OEM laboratories command 56.90% of the electric vehicle battery testing equipment market share in 2025, reflecting manufacturers' preference for in-house testing capabilities and proprietary validation protocols. Independent/third-party labs represent the fastest-growing segment at 16.95% CAGR through 2031, driven by smaller manufacturers' outsourcing needs and specialized testing requirements. The complexity of regulatory compliance across multiple markets creates opportunities for independent labs offering comprehensive certification services and global market access.

Research institutes and universities contribute to fundamental battery research and next-generation technology development, often partnering with industry for collaborative testing programs. HORIBA India's partnership with IIT Delhi for EV and green hydrogen research exemplifies this collaboration model. The Fraunhofer Battery Alliance's extensive research infrastructure supports battery testing, simulations, and techno-economic assessments, bridging scientific research and industrial application. Independent labs benefit from economies of scale and specialized expertise, offering cost-effective testing solutions for manufacturers lacking in-house capabilities.

Geography Analysis

Asia–Pacific anchored 46.05% of the electric vehicle battery testing equipment market in 2025 and will expand at a 16.33% CAGR to 2031. Japan sustains technological leadership in solid-state IP, supported by USD 2.24 billion in state subsidies and a deep bench of material suppliers.

North America is one of the key regions that will play a critical role in driving the market. Driven by USD 40.9 billion in battery manufacturing investments and capacity expansion to 1,200 GWh by 2030. Major projects include LG Energy Solution's USD 5.5 billion Arizona facility producing 53 GWh annually starting in 2026 and Volkswagen PowerCo's USD 7 billion Ontario gigafactory beginning production in 2027. The Inflation Reduction Act provides substantial incentives for domestic battery production, while UL Solutions' establishment of its North America Advanced Battery Laboratory in Auburn Hills supports regional testing infrastructure development. Siemens' USD 150 million investment in Canada for a global EV battery R&D hub, utilizing AI and digital twin engineering, demonstrates the region's focus on advanced testing technologies. The US Department of Energy's USD 25 million investment in next-generation battery manufacturing projects further supports testing equipment demand growth. Europe carves differentiation through regulation. The EU Battery Regulation enforces recycling, carbon footprint disclosure, and digital passports from 2027. Northvolt’s 60 GWh plant in Germany and the Fraunhofer research factory in Münster extend regional supply security. Testing players enjoy rising demand for lifecycle assessments, including second life and recycling validation.

Competitive Landscape

The electric vehicle battery testing equipment market exhibits moderate fragmentation, intensifying consolidation as established players acquire specialized capabilities and emerging technologies. Market leaders leverage vertical integration strategies, combining hardware manufacturing with software analytics and AI-driven testing protocols to create comprehensive solutions.

Strategic acquisitions reshape competitive dynamics as companies seek to expand their technological capabilities and geographic reach. UL Solutions' acquisition of Germany's BatterieIngenieure GmbH in May 2024 strengthened its European battery testing footprint. Emerson's investment in AI-powered testing startup EecoMobility demonstrates the growing importance of artificial intelligence in battery diagnostics.

The Test and Measurement sector experienced an uptick in M&A activity, with notable acquisitions including Spectris's USD 630 million purchase of Micromeritics. Technology differentiation increasingly centers on AI integration, digital twin capabilities, and predictive maintenance solutions, with companies like Honeywell revolutionizing battery manufacturing through AI-powered platforms that reduce material waste by 60% and improve cell yields.

Electric Vehicle Battery Testing Equipment Industry Leaders

-

TUV Rheinland Group

-

Keyinsight Technologies, Inc.

-

National Instruments Corporation

-

Horiba Ltd.

-

AVL List GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: UL Solutions Inc. opened its Europe Advanced Battery Testing Laboratory in Aachen, Germany. This facility will test batteries for electric vehicles (EVs) and large-scale energy storage systems, significantly enhancing the company's battery technology testing capabilities and expanding its presence in Europe.

- April 2025: SGA SA expanded its battery testing and certification services at its Suwanee lab near Atlanta, Georgia, USA. This expansion enables the company to offer testing services across the country.

- August 2024: UL Solutions, a provider of testing, inspection, and certification services for the clean energy sector, inaugurated its North America Advanced Battery Laboratory in Auburn Hills, Michigan. This facility will focus on testing batteries for electric and hybrid vehicles alongside industrial applications. The lab's testing repertoire encompasses thermal fire propagation, electrical, mechanical abuse, and environmental assessments, all compliant with standards set by UL, the International Electrotechnical Commission (IEC), the United Nations (UN), and the Society of Automotive Engineers (SAE).

- August 2024: The Indian Union Ministry of Consumer Affairs inaugurated an electric vehicle battery testing facility in Bengaluru, India. This state-of-the-art facility is located at the National Test House (NTH) within the Regional Reference Standard Laboratory complex in Jakkur. Catering to EV manufacturers in South India, the facility provides essential battery testing services, focusing on performance indicators, safety standards, and battery efficiency.

Global Electric Vehicle Battery Testing Equipment Market Report Scope

Electric vehicle battery testing equipment assists in evaluating the health of the electric vehicle battery and its reliability to ensure peak performance. Several tools and software are designed to conduct mechanical, electrical, and other tests on these batteries to investigate and analyze their performance capability.

The electric vehicle battery testing equipment market is segmented by vehicle type, propulsion type, testing type, and geography. By vehicle type, the market is segmented into passenger cars and commercial vehicles. By propulsion type, the market is segmented into battery electric vehicles (BEVs), plug-in hybrid electric vehicles (PHEVs), hybrid electric vehicles (HEVs), and fuel cell electric vehicles (FCEVs). By testing type, the market is segmented into mechanical tests, thermal tests, electrical tests, and others (chemical tests, etc.). By geography, the market is segmented into North America, Europe, Asia-Pacific, and Rest of the World.

The report offers market size and forecasts in value (USD) for all the above segments.

| Passenger Cars |

| Commercial Vehicles |

| Battery Electric Vehicles (BEVs) |

| Plug-in Hybrid Electric Vehicles (PHEVs) |

| Hybrid Electric Vehicles (HEVs) |

| Fuel-Cell Electric Vehicles (FCEVs) |

| Mechanical Tests |

| Thermal Tests |

| Electrical Tests |

| Chemical/Abuse Tests |

| Cell-Level Testing |

| Module-Level Testing |

| Pack-Level Testing |

| Automotive OEM Laboratories |

| Independent/Third-Party Labs |

| Research Institutes and Universities |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Egypt | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Vehicle Type | Passenger Cars | |

| Commercial Vehicles | ||

| By Propulsion Type | Battery Electric Vehicles (BEVs) | |

| Plug-in Hybrid Electric Vehicles (PHEVs) | ||

| Hybrid Electric Vehicles (HEVs) | ||

| Fuel-Cell Electric Vehicles (FCEVs) | ||

| By Testing Type | Mechanical Tests | |

| Thermal Tests | ||

| Electrical Tests | ||

| Chemical/Abuse Tests | ||

| By Test Stage | Cell-Level Testing | |

| Module-Level Testing | ||

| Pack-Level Testing | ||

| By End-User | Automotive OEM Laboratories | |

| Independent/Third-Party Labs | ||

| Research Institutes and Universities | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Egypt | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the electric vehicle battery testing equipment market?

The market is valued at USD 3.3 billion in 2026 and is projected to reach USD 7.11 billion by 2031.

Which region leads the market today?

Asia–Pacific holds 46.05% of global revenue, powered by China’s dominant cell-manufacturing footprint.

How fast is the commercial-vehicle segment rising?

Testing demand for commercial-vehicle batteries is forecast to climb at an 18.05% CAGR as fleet electrification accelerates.

Why are independent labs gaining traction?

High capital costs and long accreditation timelines push smaller manufacturers to outsource validation, spurring a 16.95% CAGR for independent labs.

What role does AI play in this market?

AI-driven digital-twin platforms cut material waste, shorten test cycles, and enable predictive maintenance, giving suppliers a competitive edge.

Page last updated on: