North America Electric Wheelchair Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

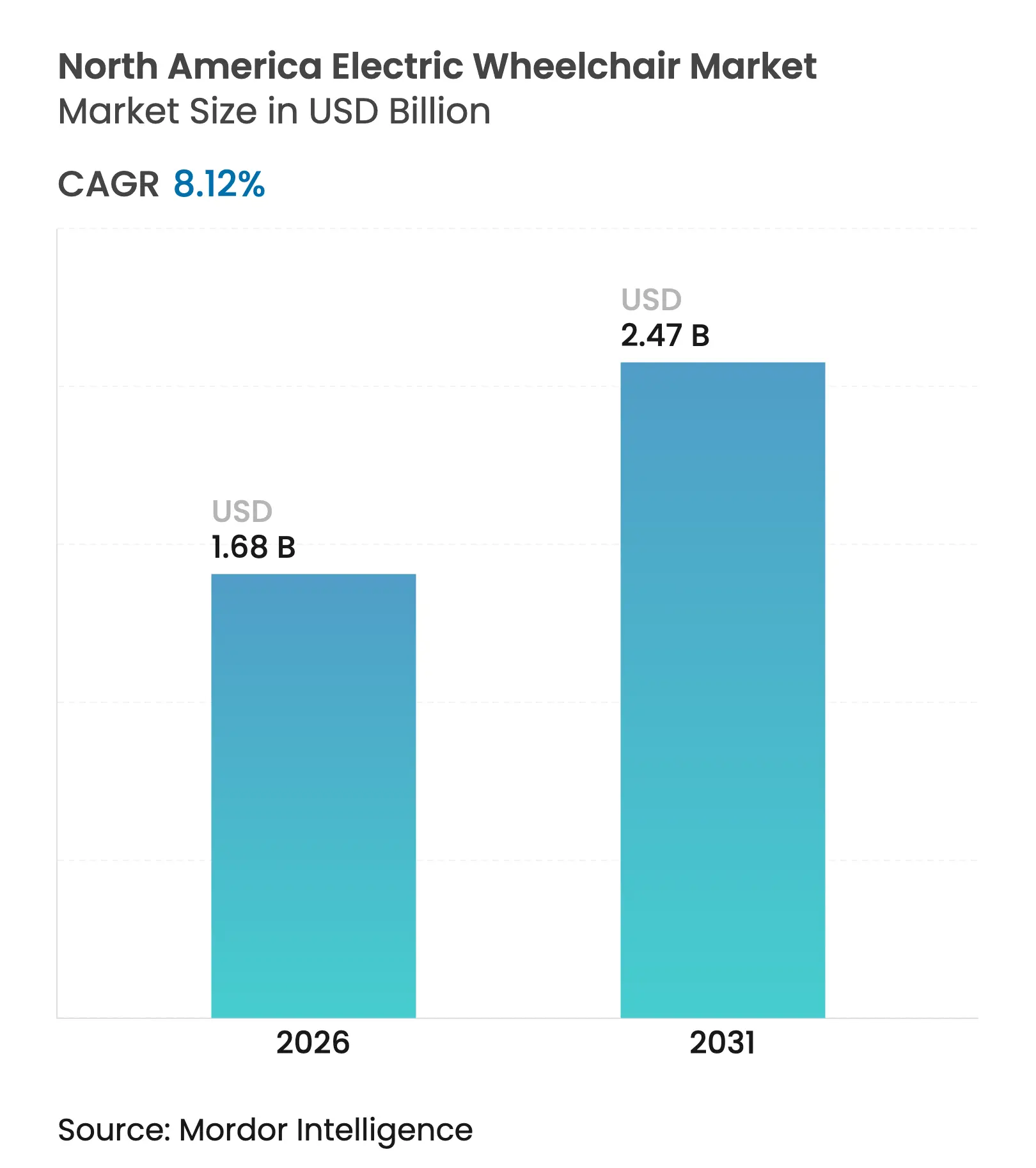

| Market Size (2026) | USD 1.68 Billion |

| Market Size (2031) | USD 2.47 Billion |

| Growth Rate (2026 - 2031) | 8.12 % CAGR |

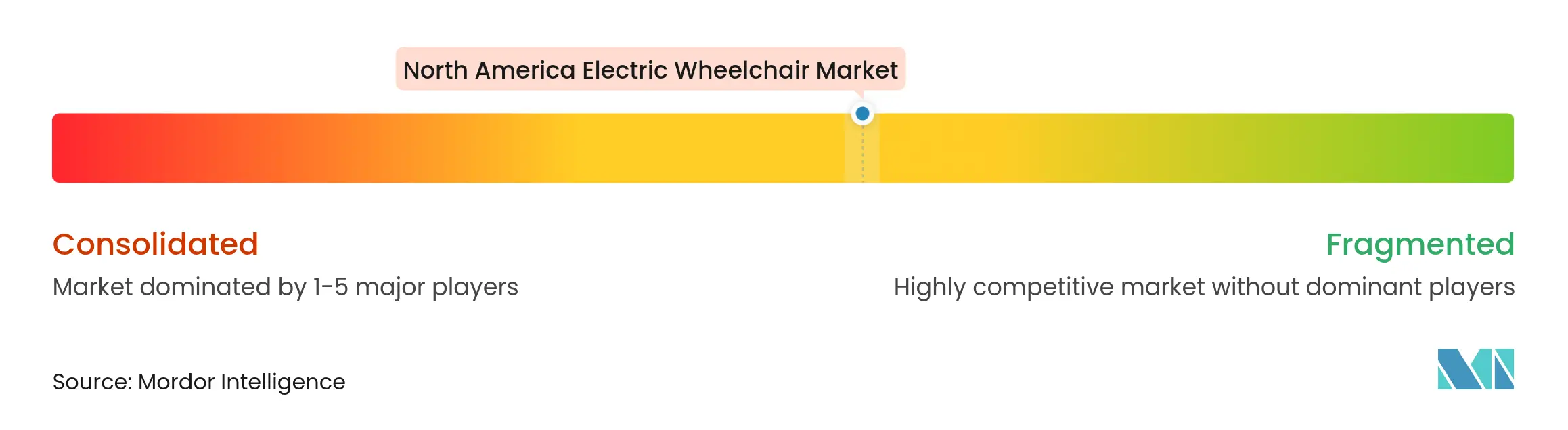

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

North America Electric Wheelchair Market Analysis by Mordor Intelligence

The North America electric wheelchair market size was valued at USD 1.55 billion in 2025 and estimated to grow from USD 1.68 billion in 2026 to reach USD 2.47 billion by 2031, at a CAGR of 8.12% during the forecast period (2026-2031). Demographic ageing, policy-driven reimbursement advances, and battery innovation combine to keep demand strong. Rear-wheel drive chairs dominate usage, e-commerce expands faster than any other sales route, and lithium-ion technology retains a decisive cost-performance edge. Private-equity-led consolidation reshapes competitive behavior, while safety recalls and servicing shortfalls temper momentum across rural areas and lower-income groups. The electric wheelchair market now sits at the intersection of home-care decentralization, digital retail, and lightweight energy storage, allowing suppliers that master all three forces to secure durable advantages.

Key Report Takeaways

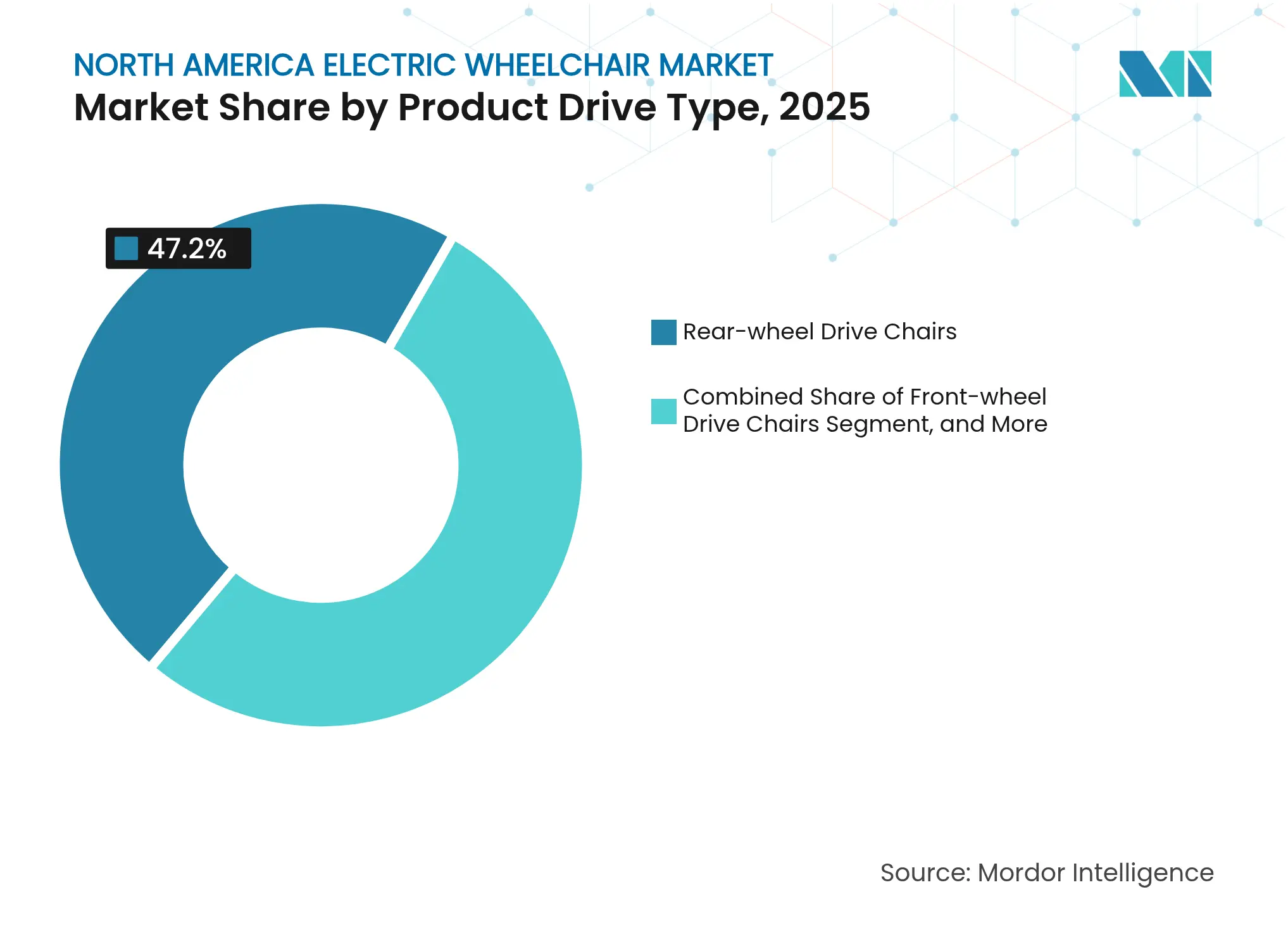

- By product drive type, rear-wheel chairs held 47.20% of the electric wheelchair market share in 2025 and are advancing at a 9.35% CAGR to 2031.

- By end-user, hospitals controlled 60.72% of the electric wheelchair market in 2025, whereas personal/homecare is expanding at a 9.18% CAGR over the same period.

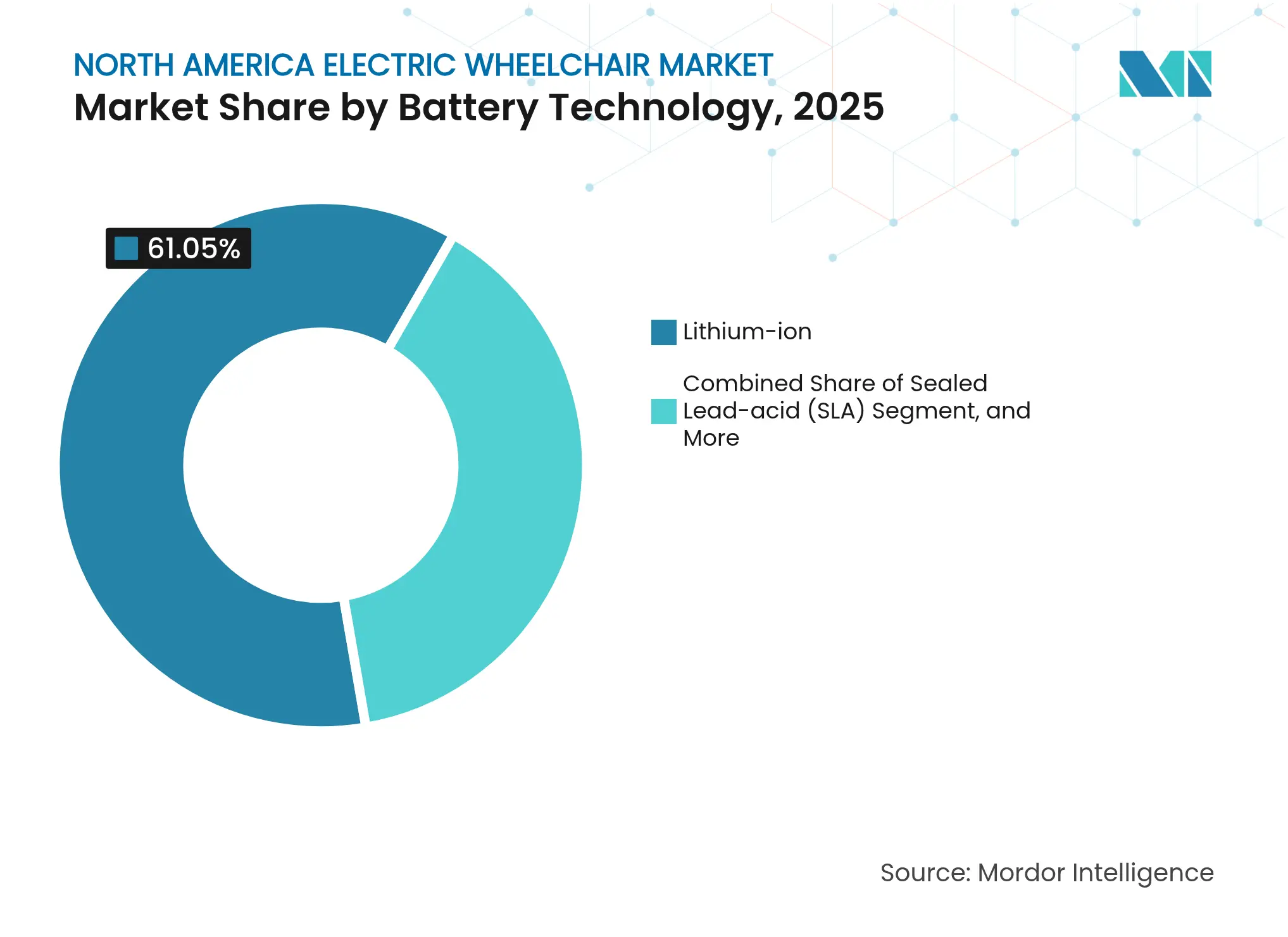

- By battery technology, lithium-ion systems accounted for 61.05% of the electric wheelchair market size in 2025 and are growing at 9.06% through 2031.

- By distribution channel, Offline DME Providers and Retailers retained a 53.85% share of the electric wheelchair market in 2025; e-commerce is registering a 12.12% CAGR to 2031.

- By country, the United States commanded 79.05% of the electric wheelchair market share in 2025 and is progressing at an 8.31% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Electric Wheelchair Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Aging Population and Mobility Disabilities Surge Aging Population and Mobility Disabilities Surge | +2.1% | North America-wide, concentrated in US Northeast, Canadian urban centers | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:+2.1% | Geographic Relevance:North America-wide, concentrated in US Northeast, Canadian urban centers | Impact Timeline:Long term (≥ 4 years) |

Home-Healthcare Reimbursement Expansion Home-Healthcare Reimbursement Expansion | +1.8% | US Medicare regions, Canadian provincial health systems | Medium term (2–4 years) | |||

Advancements in Lithium-Ion Battery Packs Advancements in Lithium-Ion Battery Packs | +1.4% | Global, with US West Coast innovation clusters leading | Medium term (2–4 years) | |||

Retrofit Power-Assist Modules Adoption Retrofit Power-Assist Modules Adoption | +0.9% | US metropolitan areas, Canadian accessibility-focused provinces | Short term (≤ 2 years) | |||

E-Commerce-Enabled Custom-Fit Ordering E-Commerce-Enabled Custom-Fit Ordering | +0.7% | North America urban/suburban markets with broadband access | Short term (≤ 2 years) | |||

Rise of Inclusive Sports Leagues Rise of Inclusive Sports Leagues | +0.5% | US Paralympic training centers, Canadian adaptive sports hubs | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Aging Population and Mobility Disabilities Surge

Demographic transformation drives fundamental market expansion as North America confronts an unprecedented aging wave that reshapes healthcare infrastructure requirements. The 57.8 million Americans aged 65 and older, representing 17.3% of the population, will surge to 22% by 2040, while 33% of this cohort already reports disability conditions requiring mobility assistance. Canada's trajectory proves even more pronounced, with projections indicating the 65+ population could reach 32.3% by 2073, with the 85+ segment potentially tripling to 4.3 million individuals[1]"Population projections: Canada, provinces and territories, 2023 to 2073", Statistics Canada, www150.statcan.gc.ca.. This demographic shift creates compounding demand pressure as age-related conditions like stroke, arthritis, and neurological disorders increase exponentially beyond age 75. The strategic implication extends beyond raw numbers: healthcare systems must transition from episodic treatment models to continuous mobility support infrastructure, fundamentally altering procurement patterns and reimbursement frameworks.

Home-Healthcare Reimbursement Expansion

Medicare and Medicaid policy evolution accelerates market growth through expanded coverage criteria and streamlined approval processes that reduce financial barriers for end users. CMS implemented significant HCPCS code updates effective April 2025, introducing E1032 for joystick interfaces, E1033 for headrest systems, and E1034 for lateral support components, all classified under capped rental payment categories[2]"New HCPCS Codes for Wheelchair Accessories – Coding and Billing", New HCPCS Codes for Wheelchair Accessories – Coding and Billing, CGS, cgsmedicare.com.. The 2025 Medicare Physician Fee Schedule updates include revised practice expense relative value units that affect wheelchair-related services, potentially improving provider margins and accessibility[3]"Medicare and Medicaid Programs; CY 2025 Payment Policies Under the Physician Fee Schedule and Other Changes to Part B Payment and Coverage Policies; Medicare Shared Savings Program Requirements; Medicare Prescription Drug Inflation Rebate Program; and Medicare Overpayments", Federal Register, federalregister.gov.. Canadian provincial health systems demonstrate parallel expansion, with enhanced coverage for complex rehabilitative technology that reduces out-of-pocket expenses. These policy shifts fundamentally alter the value proposition for personal/homecare segments, explaining their 9.78% CAGR leadership despite hospitals maintaining current market dominance.

Advancements in Lithium-Ion Battery Packs

Battery technology breakthroughs position electric wheelchairs for transformational performance improvements that address range anxiety and charging limitations constraining adoption. Lithium iron phosphate (LFP) batteries gain traction for wheelchair applications due to superior safety profiles and cost-effectiveness, with recent advances achieving 97.2% capacity retention over 700 cycles through innovative lithium replenishment strategies. Japan Advanced Institute of Science and Technology developed poly(vinyl phosphonic acid) binders that enhance silicon oxide-based anodes, improving durability and discharge capacity for extended mobility applications.

Retrofit Power-Assist Modules Adoption

Power-assist technology transforms manual wheelchair economics by extending usability and delaying electric wheelchair purchases, creating unexpected market expansion through accessibility democratization. Permobil's SmartDrive MX2+ reduces propulsion effort by up to 81% and integrates with Apple and Samsung smartwatches for intuitive control, making advanced mobility features accessible to manual wheelchair users. Despite recent recall challenges affecting 781 units due to speed control dial malfunctions, the underlying technology demonstrates market viability with Medicare coverage under HCPCS code E0986 for qualifying users. Sunrise Medical's Empulse R90 power assist device offers long-range capabilities that bridge manual and electric wheelchair functionality, addressing the mid-market segment seeking enhanced mobility without full electric conversion. This retrofit approach expands the addressable market by capturing users who previously relied solely on manual propulsion, while creating upgrade pathways that ultimately drive electric wheelchair adoption.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High Upfront Purchase and Maintenance Cost High Upfront Purchase and Maintenance Cost | -1.9% | North America-wide, acute in rural/underinsured areas | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-1.9% | Geographic Relevance:North America-wide, acute in rural/underinsured areas | Impact Timeline:Medium term (2-4 years) |

Safety Recalls and Product Liability Cases Safety Recalls and Product Liability Cases | -1.2% | US regulatory environment, Canadian safety standards | Short term (≤ 2 years) | |||

Lithium Battery Airline Transport Limits Lithium Battery Airline Transport Limits | -0.8% | Cross-border travel corridors, tourism-dependent regions | Long term (≥ 4 years) | |||

Shortage of Certified Repair Technicians Shortage of Certified Repair Technicians | -0.6% | Rural North America, underserved metropolitan areas | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High Upfront Purchase and Maintenance Cost

Cost barriers persist despite insurance coverage improvements, as complex rehabilitative technology pricing often exceeds reimbursement limits and creates affordability gaps for middle-income users. Electric wheelchairs range from USD 15,000 to USD 40,000 for advanced models, while Medicare typically covers 80% of approved amounts after deductibles, leaving substantial out-of-pocket expenses for beneficiaries. Maintenance costs compound the challenge, with lithium-ion battery replacements averaging USD 2,000-4,000 every 3-5 years, and specialized repairs requiring certified technicians who command premium rates due to supply constraints. The 2023 Profile of Older Americans reveals a median income of USD 29,740 for seniors, with USD 7,540 average out-of-pocket healthcare expenditures, highlighting the financial strain imposed by mobility equipment costs. This economic reality explains the e-commerce channel's 12.80% CAGR as consumers seek cost-effective alternatives to traditional DME provider markups.

Safety Recalls and Product Liability Cases

Product safety incidents create market headwinds through regulatory scrutiny and consumer confidence erosion that affect adoption rates and manufacturer innovation strategies. The FDA issued a warning letter to Trexo Robotics in February 2024 for marketing mobility assistance devices without required premarket approval, highlighting regulatory enforcement intensity. These incidents necessitate comprehensive quality control investments and liability insurance costs that manufacturers pass through to end users, while creating regulatory compliance burdens that favor established players over innovative entrants. The recall pattern suggests accelerated innovation cycles may compromise reliability testing, requiring industry-wide recalibration of development timelines and safety protocols.

Segment Analysis

By Product Drive Type: Rear-Wheel Dominance Sustained

Rear-wheel drive configurations maintain market leadership with 47.20% of the North America electric wheelchair market share in 2025 while driving fastest growth at 9.35% CAGR through 2031, reflecting technological maturity that enhances rather than constrains adoption. This counterintuitive dynamic stems from rear-wheel systems' superior outdoor performance and stability characteristics that align with aging users' preference for versatile mobility solutions capable of handling diverse terrain conditions. Mid-wheel drive chairs capture significant market presence through superior indoor maneuverability, particularly in healthcare facilities where tight-turning radii are essential for navigation efficiency. Front-wheel drive options serve specialized applications requiring enhanced climbing capability, while all-terrain variants address niche outdoor recreation markets that benefit from adaptive sports league expansion.

The rear-wheel segment's sustained growth leadership challenges conventional product lifecycle assumptions, as mature technologies typically experience declining growth rates. Instead, continuous refinement in motor efficiency, suspension systems, and battery integration creates performance improvements that drive replacement cycles and new user adoption. Permobil's M-Series innovations demonstrate this evolution, featuring FlexLink suspension and ActiveHeight systems that enhance stability and accessibility. The segment benefits from economies of scale in manufacturing and component sourcing that enable competitive pricing while maintaining profit margins, explaining its dual position as market leader and growth driver.

Note: Segment shares of all individual segments available upon report purchase

By End-User: Personal Segment Disrupts Hospital Dominance

Hospital and clinical settings command 60.72% of the North America electric wheelchair market share in 2025, yet personal/homecare applications drive fastest growth at 9.18% CAGR through 2031, signaling fundamental shifts in purchasing patterns and user empowerment. This transformation reflects Medicare policy evolution that expands home healthcare reimbursement coverage and reduces institutional care preferences among aging populations seeking independence and maintenance. Sports and conditioning centers represent emerging growth opportunities as adaptive athletics gain mainstream acceptance, with wheelchair basketball, rugby, and tennis driving specialized equipment demand that emphasizes performance over basic mobility.

The personal segment's growth acceleration stems from direct-to-consumer purchasing trends enabled by e-commerce platforms and improved product customization capabilities. Pride Mobility's November 2024 launch of the Jazzy Ultra Light power wheelchair, featuring carbon fiber construction and 16.4-mile range, targets personal users seeking travel-friendly solutions with premium performance characteristics. Sunrise Medical's acquisition of Ride Designs brings 3D printing capabilities that enable mass customization for personal users, addressing individual ergonomic requirements that institutional purchasing cannot accommodate. This technological convergence positions personal segments to capture increasing market share as users prioritize customization and direct purchasing relationships over institutional intermediaries.

By Battery Technology: Lithium-Ion Maintains Innovation Edge

Lithium-ion systems capture 61.05% of the North America electric wheelchair market share in 2025 and sustain growth leadership at 9.06% CAGR through 2031, driven by energy density improvements and safety enhancements that address historical adoption barriers. Recent breakthroughs achieving 711 Wh/kg energy density in laboratory settings establish pathways toward commercial applications that could triple current wheelchair range capabilities. Sealed lead-acid (SLA) batteries maintain presence in cost-sensitive applications but face declining adoption due to weight penalties and limited cycle life that increase total ownership costs. Other hybrid chemistries serve specialized applications requiring specific performance characteristics, such as extreme temperature operation or rapid charging capabilities.

The lithium-ion segment's sustained dominance reflects continuous innovation in battery management systems, thermal control, and charging infrastructure that address early adoption concerns about reliability and maintenance complexity. Lithium iron phosphate (LFP) variants gain traction for wheelchair applications due to superior safety profiles and cost-effectiveness, with recent advances achieving 97.2% capacity retention over 700 cycles. Japan Advanced Institute of Science and Technology's development of poly(vinyl phosphonic acid) binders enhances silicon oxide-based anodes, improving durability and discharge capacity for extended mobility applications. These technological advances position lithium-ion systems to maintain market leadership while enabling next-generation features like predictive maintenance and smart charging optimization.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: E-Commerce Disrupts Traditional DME

E-commerce and direct-to-consumer channels drive the fastest growth at 12.12% CAGR through 2031, despite offline DME providers maintaining 53.85% of the North America electric wheelchair market share in 2025, reflecting digital transformation prioritizing customization and cost transparency. This channel disruption stems from consumers' increasing comfort with online healthcare purchases and manufacturers' investment in virtual fitting technologies that reduce traditional showroom dependencies. Institutional procurement through VA and long-term care facilities represents stable demand sources but lacks the growth dynamism of consumer-driven channels that benefit from Medicare Advantage expansion and improved reimbursement processes.

The e-commerce surge reflects fundamental changes in consumer behavior accelerated by accessibility improvements and customization capabilities that traditional DME providers struggle to match. Permobil's introduction of the Permobil Store enables real-time configuration and ordering of TiLite wheelchairs with over 1 billion possible combinations, demonstrating how digital platforms can deliver mass customization at scale. The channel's growth trajectory benefits from reduced overhead costs compared to physical showrooms, enabling competitive pricing that appeals to cost-conscious consumers facing high out-of-pocket expenses. However, complex rehabilitative technology often requires professional fitting and training that favors hybrid models combining online ordering with local service delivery.

Geography Analysis

The United States commands the region both in scale and growth. It contributed 79.05% of the North America electric wheelchair market revenue in 2025 and is projected to rise 8.31% through 2031. The country hosts 57.8 million seniors and benefits from the April 2025 HCPCS expansions that reimburse advanced joystick, headrest, and lateral-support components, lifting utilization. Local manufacturers respond by staffing field repair hubs; Permobil serviced 578 chairs at seven Abilities Expos in 2024, proving post-sale commitment. Demographic clustering in the Northeast and Pacific states concentrates premium purchases with the highest healthcare budgets and broadband adoption.

Canada presents the strongest relative ageing trend. The share of residents aged 65+ is set to surpass 21.9% by 2030. Provincial assistive-device programs are raising ceiling prices to cover complex rehabilitation technology, and urban settlement patterns in Ontario, British Columbia, and Québec focus demand in three multilingual metro corridors. Canadian buyers typically adopt innovations 12-18 months after US release, aligning replacement cycles with favorable exchange rates and warranty enhancements. This lag creates a reliable follow-through for suppliers scaling production after the American debut.

The rest of North America covers Mexico and the Caribbean territories. Growing middle-class affluence and returning retirees stimulate baseline demand, yet public insurance is limited, and private coverage is uneven. Import duties and logistical hurdles lift consumer price points. As assembly partners south of the border assume contract manufacturing roles for US brands, average unit costs may decline, raising penetration once financing products develop. Until then, demand remains niche, weighted toward urban private hospitals and expatriate communities. Overall, geography trends imply the electric wheelchair market will stay US-centric but with a measurable pick-up in Canada.

Competitive Landscape

Market Concentration

Private equity is reshaping leadership. Platinum Equity acquired Sunrise Medical in January 2025, while MIGA Holdings bought Invacare’s North American operations in November 2024. Fresh capital budgets underpin mass-customization moves such as Sunrise Medical’s purchase of Ride Designs to integrate 3-D printed seating shells. Pride Mobility, Permobil, and Ottobock compete on differentiated ergonomics and smart-assist firmware, investing in data analytics that track battery health, seating pressure, and usage.

Strategic focus revolves around three axes: battery extension, digital control ecosystems and omnichannel reach. Pride Mobility’s Charge360 magnetic plug simplifies nightly charging. Ottobock pairs chairs with myo-electric accessories for stroke rehabilitation. Online configurators enable billions of permutation options without bloating inventories. Firms also court sporting partnerships; World Wheelchair Rugby uses high-torque models to showcase durability, indirectly validating everyday commuting devices.

Recalls remain the main reputational hazard. The March 2025 FDA Class I action on Permobil SmartDrive dials exemplifies the stakes. Companies are enhancing in-process testing and doubling warranty lengths to reassure buyers. Meanwhile, specialized service franchises are proliferating to address technician deficits that slow repair turnarounds in rural settings. The overall competitive pattern reflects moderate consolidation, high R&D investment, and rising consumer influence in purchase decisions inside the electric wheelchair market.

North America Electric Wheelchair Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: KERDOM, a trailblazer in personal mobility solutions from the United States, has unveiled its latest innovation: the Model DX04, its most advanced electric wheelchair yet. Merging top-tier technology with sleek design, the DX04 aims to elevate user mobility and autonomy, redefining benchmarks in comfort, functionality, and performance.

- November 2024: Pride Mobility launched two new products: the Jazzy Ultra Light power wheelchair featuring carbon fiber frame and 16.4-mile battery range, and the Go Go Super Portable scooter with foldable design and 10-mile range. Both products incorporate innovative features like Charge360 magnetic charger to enhance travel mobility convenience.

- October 2024: Permobil launched TiLite X and TiLite Z ultra-lightweight manual wheelchairs featuring over 1 billion configurations and 5-day lead times. The TiLite X weighs 12.1 pounds with folding frame design, while the TiLite Z weighs 11.3 pounds with rigid mono-tube construction, both emphasizing durability and customizability for diverse user needs.

- October 2024: Sunrise Medical introduced Empulse R90 power assist device offering long-range capabilities for manual wheelchair users. The device enhances range and performance while bridging manual and electric wheelchair functionality, addressing mid-market segments seeking enhanced mobility without full electric conversion.

Table of Contents for North America Electric Wheelchair Industry Report

1. Introduction

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Aging population and mobility disabilities surge

- 4.2.2Home-healthcare reimbursement expansion

- 4.2.3Advancements in lithium-ion battery packs

- 4.2.4Retrofit power-assist modules adoption

- 4.2.5e-Commerce-enabled custom-fit ordering

- 4.2.6Rise of inclusive sports leagues

- 4.3Market Restraints

- 4.3.1High upfront purchase and maintenance cost

- 4.3.2Safety recalls and product liability cases

- 4.3.3Lithium battery airline transport limits

- 4.3.4Shortage of certified repair technicians

- 4.4Technological Outlook

- 4.5Porter’s Five Forces Analysis

- 4.5.1Threat of New Entrants

- 4.5.2Bargaining Power of Buyers / Consumers

- 4.5.3Bargaining Power of Suppliers

- 4.5.4Threat of Substitute Products

- 4.5.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value (USD))

- 5.1By Product Drive Type

- 5.1.1Front-wheel Drive Chairs

- 5.1.2Mid-wheel Drive Chairs

- 5.1.3Rear-wheel Drive Chairs

- 5.2By End-user

- 5.2.1Personal / Homecare

- 5.2.2Hospitals and Clinics

- 5.2.3Sports and Conditioning Centers

- 5.3By Battery Technology

- 5.3.1Sealed Lead-acid (SLA)

- 5.3.2Lithium-ion

- 5.3.3Other / Hybrid Chemistries

- 5.4By Distribution Channel

- 5.4.1Offline DME Providers and Retailers

- 5.4.2E-commerce / Direct-to-Consumer

- 5.4.3Institutional Procurement (VA, LTC, etc.)

- 5.5By Country

- 5.5.1United States

- 5.5.2Canada

- 5.5.3Rest of North America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1Permobil

- 6.4.2Pride Mobility Products Corp.

- 6.4.3Invacare Corporation

- 6.4.4Sunrise Medical Inc.

- 6.4.5Ottobock SE & Co. KGaA

- 6.4.6Golden Technologies Inc.

- 6.4.7Hoveround Corporation

- 6.4.8Karman Healthcare Inc.

- 6.4.9Merits Healthcare Products Inc.

- 6.4.10Whill Inc.

- 6.4.11EZ Lite Cruiser

7. Market Opportunities and Future Outlook

- 7.1White-space and Unmet-need Assessment

North America Electric Wheelchair Market Report Scope

Electric wheelchairs, commonly referred to as power or motorized wheelchairs, are wheeled seating devices driven by electric motors. They cater to individuals unable to manually operate traditional wheelchairs, such as those with mobility challenges and seniors residing in retirement homes, assisted living facilities, or their own homes.

North America Electric Wheelchair Market is segmented product, portability, age, end use and country. Based on the product, the market is segmented into Front Wheel, Middle Wheel, Rear Wheel and Others. Based on end use, the market is segmented into Personal, Hospital, and Sport Conditioning. Based on the country, the market is segmented into the United States, Canada, and the Rest of North America. For each segment, market sizing and forecast have been done on the basis of value (USD).