Automotive Remote Diagnostics Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 22.78 Billion |

| Market Size (2031) | USD 46.41 Billion |

| Growth Rate (2026 - 2031) | 15.30% CAGR |

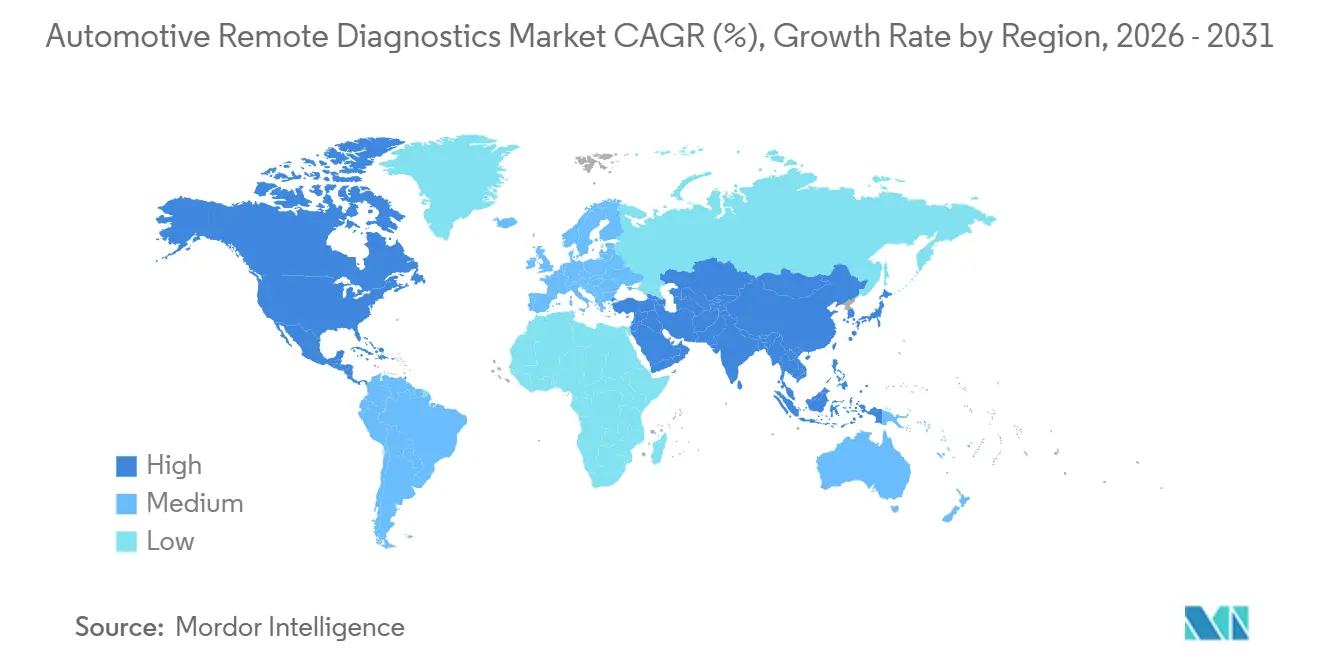

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Remote Diagnostics Market Analysis by Mordor Intelligence

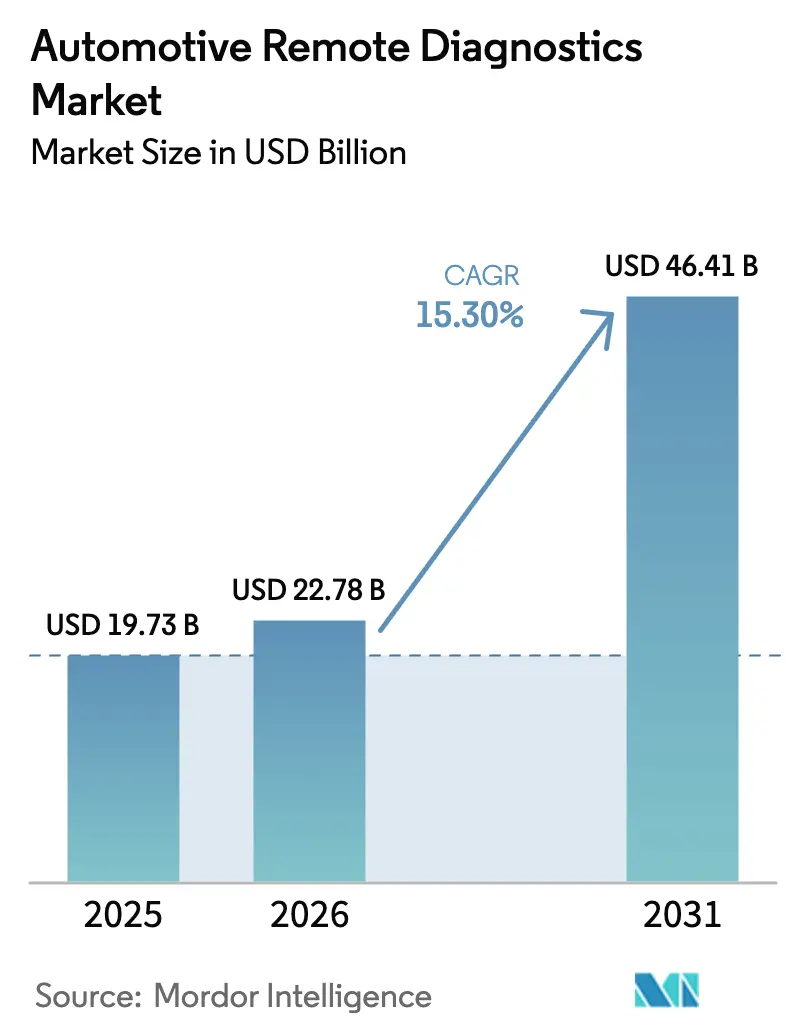

The automotive remote diagnostics market size is expected to grow from USD 19.73 billion in 2025 to USD 22.78 billion in 2026 and is forecast to reach USD 46.41 billion by 2031 at a 15.30% CAGR over 2026-2031. Surging factory-installed connectivity, tighter on-board-diagnostics mandates, and the pivot from one-time hardware sales to recurring software subscriptions are expanding margins for original equipment manufacturers. Tier-1 suppliers are embedding edge-AI chips that process fault codes locally, cutting cellular backhaul costs and enabling sub-second fault detection. Insurers’ usage-based policies now demand continuous telematics feeds, while battery digital-twin analytics reassure used-EV buyers and lift residual values. These converging forces accelerate adoption even as cybersecurity and interoperability gaps push vendors toward common standards and zero-trust architectures.

Key Report Takeaways

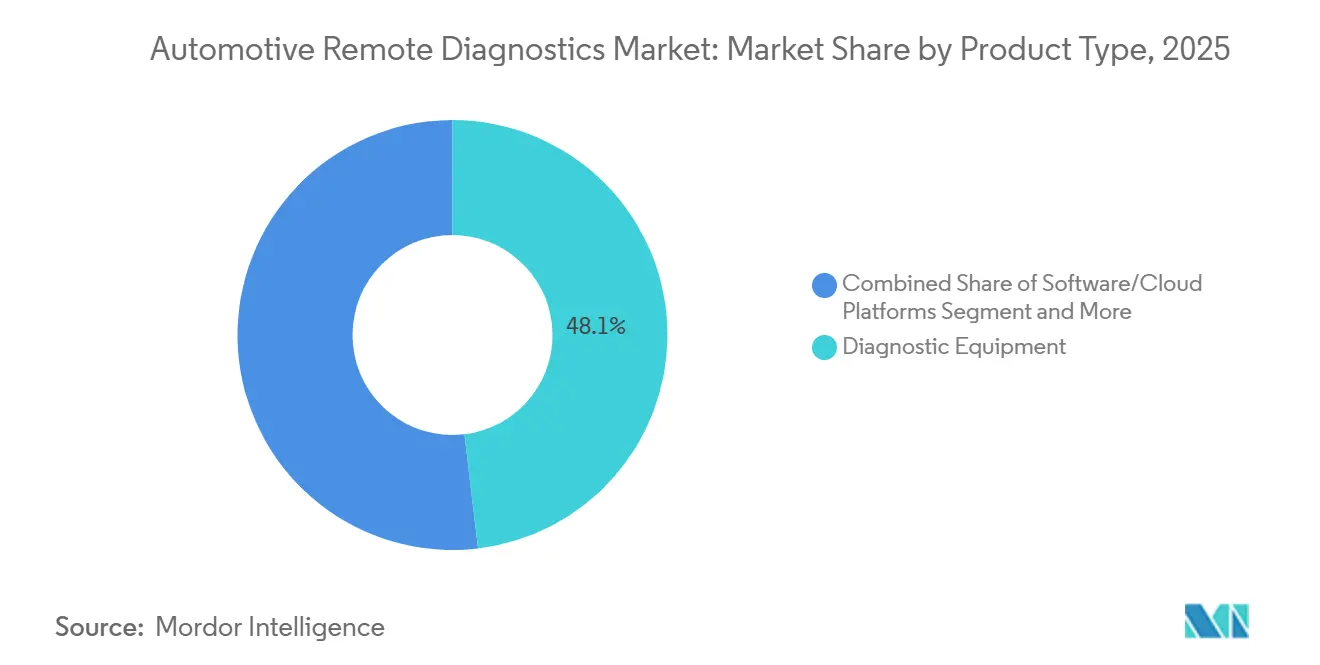

- By product type, diagnostic equipment led with 48.13% of the automotive remote diagnostics market share in 2025, while services are projected to grow at a 16.12% CAGR to 2031.

- By vehicle type, passenger cars commanded 59.25% revenue in 2025; commercial vehicles are expected to advance at a 17.32% CAGR through 2031.

- By connectivity, 3G/4G/5G LTE cellular links held 75.11% share in 2025 and are set to expand at a 17.64% CAGR, outpacing Wi-Fi and satellite options.

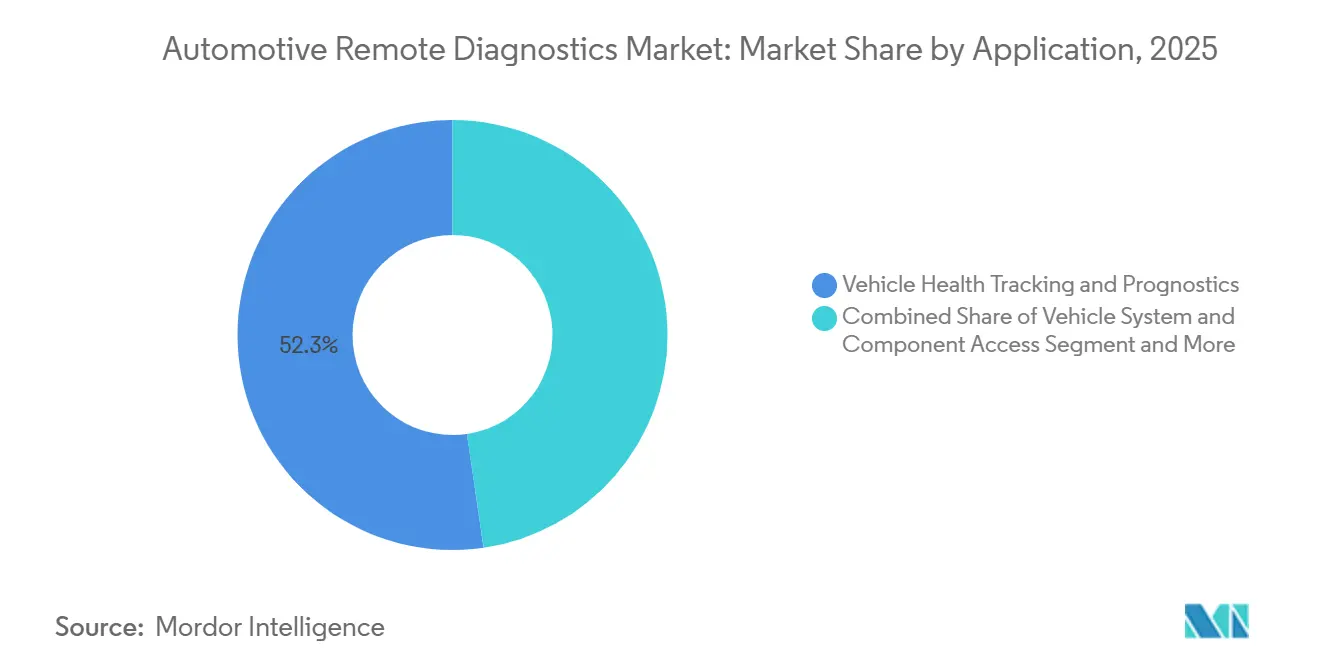

- By application, vehicle health tracking and prognostics captured 52.31% revenue in 2025, whereas over-the-air updates will rise at a 15.81% CAGR to 2031.

- By end-user, OEM-installed systems dominated with 87.44% share in 2025, but aftermarket chains are forecast to climb at a 17.13% CAGR.

- By geography, North America led with 36.18% revenue in 2025; Asia-Pacific is poised for the fastest 16.56% regional CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automotive Remote Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Connected-Car Penetration | +3.2% | Global, led by Asia-Pacific and North America | Short term (≤ 2 years) |

| Diagnostics and Emission Regulations | +2.8% | Europe, North America, China | Medium term (2-4 years) |

| OEM Shift to Subscription | +2.5% | Global, premium segments | Medium term (2-4 years) |

| Edge-AI Deployment | +1.9% | Asia-Pacific core, Middle East and Africa, and South America spill-over | Long term (≥ 4 years) |

| Telematics-Linked Premium Discounts | +1.7% | North America and Europe | Short term (≤ 2 years) |

| Battery Digital-Twin Diagnostics | +1.4% | Global, early in China, Europe, California | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Connected-Car Penetration Surge

In 2024, factory-installed connectivity became a common feature in new vehicles, and by 2029, it is expected to become nearly universal. This shift is transforming remote diagnostics from a luxury add-on to a standard feature. On average, a connected vehicle generates a data stream that enables automakers to seamlessly push software updates, predict component wear, and autonomously schedule service appointments. China’s 2024 mandate for cellular links in all new-energy vehicles added a significant number of endpoints in a single year [1]“Connectivity Requirements for New-Energy Vehicles,” Ministry of Industry and Information Technology, miit.gov.cn. European eCall infrastructure, initially built for emergencies, now underpins commercial diagnostics, while North American brands bundle multi-year data plans to improve customer lifetime value.

Stricter On-Board-Diagnostics and Emission Regulations

Euro 7 rules, effective 2026, require real-time nitrogen oxide and particulate monitoring over a vehicle’s entire life, forcing OEMs to transmit diagnostic logs to regulators [2]“Euro 7: New Rules on Vehicle Emissions,” European Commission, europa.eu. The US EPA’s Tier 3 updates finalized in 2024 impose similar reporting for catalyst and evaporative-system faults. China's National VI(b) standard enforces stringent measures, imposing fines for non-compliance. While these compliance costs drive increased investments, the data generated holds value, allowing resale to city planners. This not only offsets infrastructure expenditures but also steers the automotive remote diagnostics market closer to a universally accepted global standard.

OEM Shift to Subscription Revenue for Predictive Maintenance

In 2024, BMW generated significant revenue from digital services, with diagnostics and over-the-air (OTA) updates playing a major role. In 2025, Mercedes-Benz introduced its "Preventive Care" package, offering forecasts of component failures a month in advance. Research indicates that many buyers in the premium car segment are willing to pay annual fees, especially when it results in reduced downtime. These subscription models not only tether car owners to original equipment manufacturers (OEMs) but also diminish the aftermarket's share, all while amplifying the demand for OEM parts.

Edge-AI Deployment Lowers Data-Backhaul Costs

Onboard accelerators like Qualcomm's Snapdragon Ride are classifying anomalies right on the vehicle, significantly reducing data uploads. This not only streamlines data management but also lowers connectivity costs. Meanwhile, Continental's Edge-AI ECU operates efficiently, allowing for real-time alerts without depleting the vehicle's 12-V battery. By processing data locally, vehicles sidestep GDPR's cross-border challenges and are better equipped for autonomous tasks that could easily saturate cloud connections.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Up-Front Cost | -1.8% | Global, price-sensitive segments | Short term (≤ 2 years) |

| Security and Data-Privacy | -1.5% | Europe, North America, China | Medium term (2-4 years) |

| Lack of Interoperability | -1.2% | Aging fleet segments worldwide | Long term (≥ 4 years) |

| Rural 4G/5G Coverage | -1.0% | Asia-Pacific, South America, Middle East and Africa, rural North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Up-Front Cost of Hardware and Cloud Fees

Retrofitting a non-connected vehicle involves high costs. Additionally, cloud storage and data egress fees create ongoing expenses, discouraging small fleets and individual owners. Start-ups face financial strain as major providers impose charges for outbound traffic. To reduce barriers, vendors have started bundling lower-resolution data streams. However, this compromise on data fidelity weakens predictive accuracy and hampers the adoption of automotive remote diagnostics, particularly among less mainstream users.

Cyber-Security and Data-Privacy Concerns

In 2024, NHTSA reported several incidents of remote access breaches, involving actions such as engine shutdowns and GPS spoofing. While GDPR penalties remain a significant concern, China's PIPL continues to impose strict limitations on cross-border data transfers. Drivers in the United States have shown hesitation in sharing their real-time data due to growing privacy concerns. Although OEMs are heavily investing in end-to-end encryption and ISO/SAE 21434 programs to strengthen cybersecurity, the ongoing conflict between hackers and defenders introduces considerable challenges, including increased costs and uncertainty, to product development roadmaps.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Services Outpace Hardware

Hardware accounted for a significant portion of the automotive remote diagnostics market size in 2025, reflecting 48.13% revenue from scan tools, telematics control units, and OBD-II dongles. Commoditization and cheaper Chinese devices hold hardware growth in the mid-single digits. Services are on a sharper 16.12% trajectory, moving the revenue center toward cloud analytics, predictive maintenance, and over-the-air feature enablement. The subscription model lifts lifetime value: BMW’s annual package generates a greater margin over five years than the initial telematics module itself.

Recurring platforms strengthen network effects because every new data point improves machine-learning precision. Aggregated telemetry from several vehicles allows Bosch Automotive Cloud Suite to flag emerging component failures weeks sooner, lowering warranty risk and reinforcing customer loyalty [3]“Automotive Cloud Suite Vehicle Coverage 2025,” Bosch, bosch.com. Hardware remains vital for legacy fleets, yet its role is increasingly as an on-ramp to higher-margin digital services. This shift underpins the broader evolution of the automotive remote diagnostics market toward software-defined vehicles and continuous value delivery.

By Vehicle Type: Commercial Fleets Drive Growth

Passenger cars held 59.25% revenue in 2025, buoyed by SUV sales in China and the United States. However, commercial vehicles are forecast to register a 17.32% CAGR, twice the pace of light-duty cars. Long-haul trucks face significant losses for every hour they remain idle, highlighting the rapid ROI of predictive diagnostics. Following its implementation, Daimler Trucks' Detroit Connect platform has achieved a notable reduction in unscheduled repairs.

Last-mile vans chasing e-commerce service levels, and buses facing zero-emission zones, likewise depend on real-time monitoring. Mixed-brand logistics fleets value agnostic dashboards that consolidate engine, brake, and tire data. The commercial surge pushes suppliers to certify ruggedized telematics capable of 500,000-mile duty cycles, widening differentiation in the automotive remote diagnostics market.

By Connectivity Type: Cellular Dominates

Cellular links (3G/4G/5G LTE) captured 75.11% share and will compound at 17.64% as carriers sunset 3G and densify 5G. Low-latency 5G enables deep learning models to run over-the-air, supporting autonomous safety overrides. Qualcomm C-V2X chips embed direct sidelink channels so vehicles can push fault summaries to roadside units in real time.

Wi-Fi manages heavy software downloads while parked, easing data costs, and Bluetooth serves do-it-yourself mobile apps. Satellite remains niche but strategic for mines and emergency services beyond cell grids. Hybrid topologies—cellular primary, Wi-Fi offload, satellite fail-over—are emerging as best practice, sustaining robust growth across the automotive remote diagnostics industry without overloading any single network.

By Application: OTA Updates Surge

Vehicle health tracking and prognostics accounted for 52.31% of 2025 revenue, but OTA updates will clock a 15.81% CAGR to 2031 as software-defined vehicles proliferate. Tesla’s major OTA releases since 2012 set consumer expectations, and Mercedes-Benz now schedules quarterly infotainment refreshes that also improve diagnostic granularity.

OTA capability transforms diagnostics from break-fix to continuous enhancement: powertrain tweaks raise efficiency, ADAS patches boost safety scores, and battery profiles optimize longevity. For OEMs, each software push opens fresh upsell pathways such as performance boosts or autonomous-feature unlocks, heightening stickiness within the automotive remote diagnostics market.

By End-User: Aftermarket Gains Share

OEM systems own 87.44% share due to tight ECU integration, yet aftermarket providers will grow at 17.13%, targeting the significant global parc that predates factory telematics. Snap-on Intelligent Diagnostics gives independent shops cloud access to repair databases and remote assistance, tightening the service quality gap with dealer networks.

Rental giants and leasing houses deploy dashboards that visualize multi-brand fleets, enforce maintenance compliance, and safeguard residual value. Regulatory pushes for open data, exemplified by Europe’s forthcoming Right-to-Repair, may accelerate channel diversification and propel the automotive remote diagnostics market toward a more balanced OEM-aftermarket mix.

Geography Analysis

North America generated 36.18% revenue in 2025, leveraging a significant share of connectivity penetration and usage-based insurance policies. FMCSA electronic logging mandates extend telematics to heavy trucks, though growth is now additive rather than exponential. EPA Tier 3 OBD updates ensure steady demand for compliance features.

Asia-Pacific is projected to record a 16.56% CAGR, the fastest of any region. China sold a significant volume of connected new-energy vehicles in 2025, each shipping with mandatory remote diagnostics. India’s BS-VI rollout added 4 million OBD-equipped vehicles yearly, while Japan and South Korea embed telematics in mainstream models. ASEAN nations lag, but rising urban congestion and e-commerce fleets are triggers for catch-up adoption.

Europe benefits from strict Euro 7 rules and GDPR trust. Germany, France, and the United Kingdom drive regional volume, supported by high EV uptake that requires battery digital-twin certification. Southern and Eastern European markets trail in connectivity but adopt standards via imported vehicles. South America, the Middle East & Africa present retrofit opportunities where data costs and patchy 4G impede real-time use, nudging vendors toward buffered or satellite-assisted architectures.

Competitive Landscape

Tier-1 suppliers—Bosch, Continental, and ZF—maintain a dominant position in the automotive remote diagnostics market. Their strong relationships with OEMs and vertically-integrated hardware and software solutions underpin their leadership. They further strengthen their foothold through edge-AI patents and extensive global service networks. However, competition is intensifying as companies like Qualcomm and Ericsson bring telecom expertise, while cloud-native startups such as Airbiquity leverage advanced data analytics capabilities to disrupt the market dynamics.

OEMs are increasingly focusing on vertical integration to enhance control over data and revenue streams. Strategies like Mercedes-Benz's MB.OS and BMW's iDrive 9 reflect efforts to secure data within proprietary platforms and generate subscription-based revenue. At the same time, Chinese module manufacturers, including Huawei and Quectel, are disrupting the market with cost-effective cellular boards, challenging traditional pricing structures. Following cyber incidents in 2024, ISO/SAE 21434 certification has become a critical requirement, emphasizing the growing importance of cybersecurity in the automotive sector.

Growth opportunities exist in interoperable aftermarket solutions and improving rural connectivity, which remain underexplored areas in the market. These domains present significant potential for agile newcomers to scale rapidly and establish a foothold. As the industry evolves, companies that can adapt to these emerging trends and address these white-space opportunities are likely to gain a competitive edge in the coming years.

Automotive Remote Diagnostics Industry Leaders

Robert Bosch GmbH

Continental AG

ZF Friedrichshafen AG

Verizon Business (Telematics)

Trimble Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Bosch Diagnostics released major software updates for its ADS X tools, adding more special tests, faster scanning, and broader vehicle coverage to support service networks across Asia.

- December 2025: Mahle launched RemotePRO Air, the first tool granting multi-franchise workshops remote access to modern connected vehicles, aligning with the United Kingdom’s forthcoming SERMI scheme.

- November 2025: Softing Automotive debuted a hybrid diagnostic solution that unites UDS and SOVD standards for software-defined vehicles, spanning the full vehicle lifecycle.

- October 2025: ZF Aftermarket introduced ZF MultiScan and ZF [pro]Tech Plus at AAPEX/SEMA 2025, integrating parts, distribution and digital support to maximize workshop uptime.

Global Automotive Remote Diagnostics Market Report Scope

The scope includes segmentation by product type (diagnostic equipment, software/cloud platforms, and services), vehicle type (passenger cars and commercial vehicles), connectivity type (3G/4G/5G LTE, wi-fi, Bluetooth/BLE, and satellite and V2X), application (vehicle stystems and component access, vehicle health tracking and prognostics, service/roadside assistance, over-the-air updates and re-flashing, and warranty and recall management), and end-user (OEM-installed, aftermarket repair chains, and fleet and leasing operators). The analysis also covers regional-level segmentation, including North America, South America, Europe, Asia-Pacific, and the Middle East and Africa. Market size and growth forecasts are presented by value in USD.

| Diagnostic Equipment |

| Software / Cloud Platforms |

| Services |

| Passenger Cars | Hatchbacks |

| Sedans | |

| Sports Utility Vehicles and Multi-Purpose Utility Vehicles | |

| Commercial Vehicles | Vans and Pickup Trucks |

| Buses and Coaches | |

| Medium and Heavy-Duty Trucks |

| 3G/4G/5G LTE |

| Wi-Fi |

| Bluetooth / BLE |

| Satellite and V2X Edge Links |

| Vehicle System and Component Access |

| Vehicle Health Tracking and Prognostics |

| Service / Roadside Assistance |

| Over-the-Air (OTA) Updates and Re-flashing |

| Warranty and Recall Management |

| OEM-installed |

| Aftermarket Repair Chains |

| Fleet and Leasing Operators |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| Turkey | |

| South Africa | |

| Rest of the Middle East and Africa |

| By Product Type | Diagnostic Equipment | |

| Software / Cloud Platforms | ||

| Services | ||

| By Vehicle Type | Passenger Cars | Hatchbacks |

| Sedans | ||

| Sports Utility Vehicles and Multi-Purpose Utility Vehicles | ||

| Commercial Vehicles | Vans and Pickup Trucks | |

| Buses and Coaches | ||

| Medium and Heavy-Duty Trucks | ||

| By Connectivity Type | 3G/4G/5G LTE | |

| Wi-Fi | ||

| Bluetooth / BLE | ||

| Satellite and V2X Edge Links | ||

| By Application | Vehicle System and Component Access | |

| Vehicle Health Tracking and Prognostics | ||

| Service / Roadside Assistance | ||

| Over-the-Air (OTA) Updates and Re-flashing | ||

| Warranty and Recall Management | ||

| By End-User | OEM-installed | |

| Aftermarket Repair Chains | ||

| Fleet and Leasing Operators | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| Turkey | ||

| South Africa | ||

| Rest of the Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the automotive remote diagnostics market in 2031?

The market is forecast to reach USD 46.41 billion by 2031.

How fast is the market expected to grow after 2026?

It is projected to register a 15.30% CAGR between 2026 and 2031.

Which region is likely to expand the quickest?

Asia-Pacific is poised for the fastest 16.56% regional CAGR through 2031, led by China and India.

Why are services outpacing hardware sales?

Recurring cloud analytics and predictive-maintenance subscriptions deliver higher margins and leverage network effects, whereas hardware is becoming commoditized.

Page last updated on: