Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.99 Billion |

| Market Size (2031) | USD 2.59 Billion |

| Growth Rate (2026 - 2031) | 5.39% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

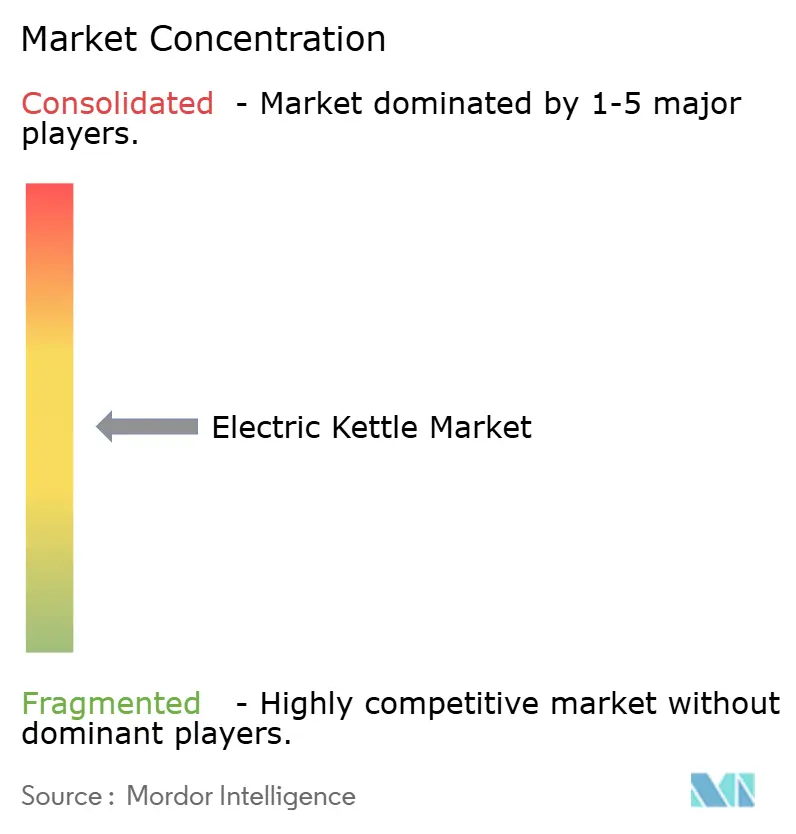

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electric Kettle Market Analysis by Mordor Intelligence

The electric kettle market size in 2026 is estimated at USD 1.99 billion, growing from 2025 value of USD 1.89 billion with 2031 projections showing USD 2.59 billion, growing at 5.39% CAGR over 2026-2031. Rising demand for smart, energy-efficient appliances, coupled with stricter standby-power rules, is re-shaping design priorities and propelling connected models into the mainstream. Europe’s 0.5-watt standby mandate that took effect in May 2025 accelerates innovation in heating elements, insulation materials, and firmware controls, while Asia-Pacific manufacturers exploit cost advantages and export momentum to serve both developing and mature consumer segments. Competitive rivalry remains moderate because the top five players control only most of the sales, yet differentiation through IoT integration, recyclable materials, and rapid-boil technologies provides defendable moats. Stainless steel remains the preferred construction material, but compact sub-1.0-liter kettles post the fastest growth as single-person urban households seek space-saving solutions and lower per-use energy consumption. Digital retail continues to erode the dominance of brick-and-mortar outlets, with online sales growing more than double the channel average.

Key Report Takeaways

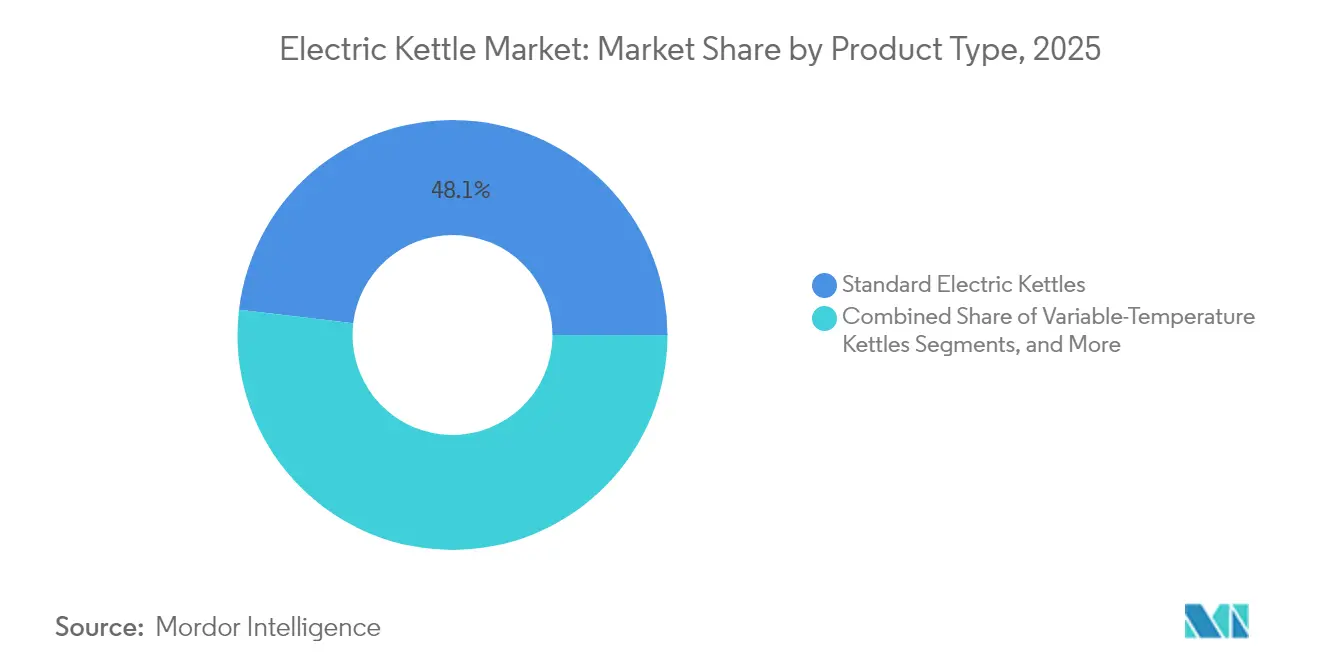

- By product type, standard kettles led with 48.12% revenue share of the electric kettle market in 2025; smart/connected variants are advancing at a 9.86% CAGR through 2031.

- By material, stainless steel retained 57.92% of the electric kettle market share in 2025, whereas stainless steel is projected to post the highest growth at 5.53% CAGR to 2031.

- By capacity, the 1.0–1.5 L segment accounted for 64.02% of the electric kettle market size in 2025, while Less than 1.0 L models are expanding at a 7.68% CAGR between 2026-2031.

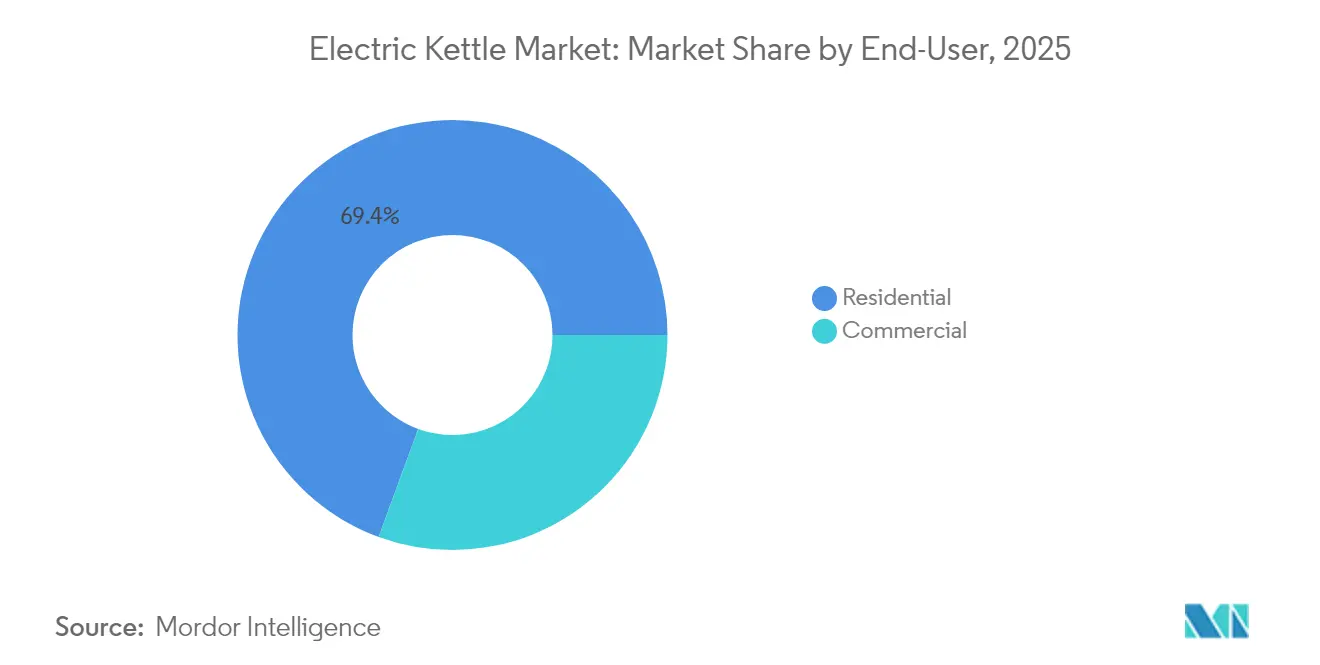

- By end-user, the residential segment accounted for 69.42% of the electric kettle market size in 2025, while the commercial segment is expanding at a 5.61% CAGR between 2026-2031.

- By distribution channel, supermarkets & hypermarkets held 43.52% share of the electric kettle market size in 2025, but online is growing at a 11.12% CAGR over the same period.

- By geography, Europe dominated with 33.84% revenue share of the electric kettle market in 2025, whereas Asia-Pacific is forecast to grow at 9.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Electric Kettle Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-efficient home appliance demand | +1.2% | Global, led by EU | Medium term (2-4 years) |

| Specialty tea & coffee chain expansion | +0.8% | North America & Europe, emerging APAC | Long term (≥ 4 years) |

| Smart/IoT-enabled kettle adoption | +1.5% | Global, developed markets lead | Short term (≤ 2 years) |

| Growth in single-person households | +0.9% | Urban centers worldwide | Long term (≥ 4 years) |

| Corporate pantry & co-working installations | +0.6% | North America, Europe, APAC metros | Medium term (2-4 years) |

| E-commerce flash sales | +0.7% | Global, strongest APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Energy-Efficient Home Appliances

Energy efficiency has moved from a purchase preference to a market admission ticket. Europe’s Regulation 2023/826 enforces a 0.5-watt standby-power ceiling, a benchmark many brands now treat as a floor to showcase superior engineering. The rule is reinforced by the Eco-design for Sustainable Products Regulation, which codifies recyclability and durability metrics that influence every phase of a kettle’s lifecycle [1]European Commission, “Ecodesign for Sustainable Products Regulation,” europa.eu. Chinese manufacturers have responded by launching greener lines that align with domestic energy-saving incentives while keeping export doors open. The convergence of policy pressure and operating-cost awareness ensures that energy labeling and actual consumption figures remain front-of-pack communication rather than footnotes. Early movers who meet or surpass the EU threshold already enjoy simplified market entry in regions preparing similar statutes.

Proliferation of Specialty Tea & Coffee Chains

Specialty cafés require water-heating equipment capable of tight temperature tolerances and repeated duty cycles, a demand profile materially different from household use. Their willingness to pay for reliability and flavour accuracy raises the performance bar and inadvertently educates consumers on the benefits of precision brewing. As more chains franchise into secondary cities, suppliers gain scale economies, which then spill over into premium consumer models. Manufacturers that validate designs in commercial settings transfer credibility to retail buyers, strengthening brand equity without heavy consumer advertising.

Adoption of Smart/IoT-Enabled Kettles

Smart variants command price premiums yet are posting double-digit volume growth, proving that connected features overcome higher initial outlays. Voice-assistant compatibility, boil-history analytics, and predictive descaling alerts convert once-passive appliances into data-rich touchpoints within broader home ecosystems. Brands collecting anonymized usage data refine firmware updates that optimize heating curves, creating feedback loops that legacy models cannot replicate. As mainstream ecosystems—from security to lighting—normalize device control via unified apps, a seamless kettle becomes an extension of the smart-home fabric rather than a novelty.

Expansion of Single-Person Households Driving Compact Models

Rising urban rents and delayed family formation keep average dwelling sizes in check, nudging consumers toward appliances that steward both space and power. Sub-1.0 L kettles appeal by reducing countertop footprint and avoiding energy waste from heating surplus water. Manufacturers answer with vertical or collapsible profiles that host double-layer walls for safe exterior touch, keeping thermal performance intact. Given demographic projections that favor one-person households in most OECD cities, this segment offers durable volume growth rather than a fad.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Microwave ovens & instant boilers | -0.8% | Global, the strongest North America | Medium term (2-4 years) |

| Volatile stainless-steel prices | -0.5% | Global manufacturing hubs | Short term (≤ 2 years) |

| EU scrutiny on standby power | -0.3% | Europe, global echo | Long term (≥ 4 years) |

| Microplastic leaching in plastics | -0.4% | Health-aware developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Microwave Ovens & Instant Boilers as Substitutes

High microwave penetration in the United States favors reheating water in multifunction devices, challenging dedicated kettles in convenience. Meanwhile, plumbed-in instant boilers in modern kitchens deliver water at drinkable temperatures without waiting. Kettle makers respond with rapid-boil elements that take 60–90 seconds for a mug and highlight flavor retention and lower standby power to reclaim the convenience narrative. Regional marketing stresses cultural rituals—such as tea brewing in the United Kingdom—to counter purely functional comparisons.

Volatile Stainless-Steel Prices

Stainless steel accounts for over half of the total bill-of-materials cost in many mid-range to premium units. Price volatility squeezes margins because promotional calendars are fixed months in advance, while alloy surcharges can swing week-to-week. Large brands hedge through long-term contracts and partial vertical integration, whereas smaller firms explore hybrid designs marrying steel interiors with heat-resistant glass exteriors to lower metal dependency. Material innovation becomes not just a sustainability imperative but also a buffer against commodity cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Smart Variants Drive Premium Evolution

In 2025, Standard Electric Kettles contributed 48.12% of the total revenue, maintaining their dominance in the market. However, Smart kettles achieved a 9.86% CAGR outlook to 2031, even though standard units still own nearly half of the revenue. Their acceleration signals an inflection where embedded connectivity migrates from early adopters into the mass mid-tier. Variable-temperature models act as transitional products for customers focused on specialty beverages but not yet convinced by full IoT control. Rapid adoption of firmware-updatable bases and companion apps illustrates how software is displacing pure hardware as the seat of value. Premium positioning also shields brands from price wars that often characterize the legacy portion of the electric kettle market.

Consumer data underscore a bifurcation: one cohort seeks minimalistic boil-only units for price attractiveness, while another cohort embraces multi-sensor platforms that integrate scheduling, alt-mode energy savings, and child-lock features. As production costs fall, connected features will cascade downward, eventually becoming standard across nearly the entire electric kettle market.

By Material: Sustainability Reshapes Material Preferences

Stainless steel retained a 57.92% share in 2025 and is forecast to expand at 5.53% CAGR through 2031, underpinning the premium segment’s solidity. Recyclability and flavour neutrality reinforce its leadership despite higher material outlays. Glass occupies a visible but fragile niche, marketed for aesthetic transparency and chemical inertness, particularly among health-conscious buyers. Plastic is losing ground under micro-plastic scrutiny; however, it retains relevance in budget ranges where cost sensitivity exceeds environmental concern.

The Ecodesign for Sustainable Products Regulation spotlights end-of-life impacts, incentivizing manufacturers to switch to mono-material designs or easily separable assemblies. Groupe SEB’s commitment to 60% recycled content exemplifies how ESG metrics turn into procurement mandates . Brands experimenting with biopolymer handles and bamboo accents illustrate a search for lower-footprint alternatives without undermining thermal safety.

By Capacity: Compact Models Capture Urban Demographics

In 2025, the 1.0–1.5 L category dominated the market, contributing 64.02% of total revenue by effectively meeting family consumption needs while ensuring heating efficiency. The less than 1.0 L segment is anticipated to grow at a compound annual growth rate (CAGR) of 7.68%, driven by the increasing adoption of single-occupancy units and micro-apartments. Larger capacities, specifically those exceeding 2.0 L, are primarily utilized in institutional and office settings, where higher volume requirements take precedence over space constraints. This segmentation reflects diverse consumer preferences based on usage scenarios and capacity needs. The market dynamics highlight the importance of aligning product offerings with specific end-user demands.

Compact models are gaining traction due to their focus on energy efficiency, as they heat only the required amount of water, thereby reducing energy wastage. This feature resonates with cost-conscious households while supporting global sustainability goals. The category's compatibility with portable induction cookers and collapsible cookware further enhances its appeal, particularly among consumers prioritizing mobility. These models address the growing demand for versatile and space-saving solutions in modern households. The alignment with mobility trends underscores the strategic positioning of compact models in the market.

By End-User: Commercial Growth Outpaces Residential Volume

The residential segment commands 69.42% market share in 2025, reflecting the electric kettle's fundamental role as a household appliance where daily beverage preparation drives consistent replacement demand and feature upgrades. However, the commercial segment's 5.61% CAGR through 2031 significantly outpaces overall market growth, indicating a structural shift toward professional applications that demand higher performance specifications and premium pricing tolerance. Commercial users, encompassing Hotels, Restaurants, Cafes (HoReCa), corporate offices, and co-working spaces, prioritize durability, rapid heating cycles, and consistent performance over aesthetic considerations that influence residential purchases.

The commercial segment's growth acceleration stems from expanding foodservice industries, co-working space proliferation, and corporate wellness initiatives that emphasize quality beverage preparation as employee amenities. Corporate pantry installations and co-working space expansion create sustained demand as workplace culture evolves toward productivity enhancement through premium beverage access. The commercial segment's willingness to pay premium prices for reliability creates opportunities for manufacturers to develop specialized product lines with higher margins than residential models, while professional-grade features eventually cascade to consumer products through feature democratization.

By Distribution Channel: Digital Transformation Accelerates

In 2025, Supermarkets & Hypermarkets contributed 43.52% of the total revenue, maintaining their dominance in the market. However, online marketplaces demonstrated a robust growth trajectory with a CAGR of 11.12%, outperforming all other distribution channels. The popularity of flash-sale events has shortened product replacement cycles by encouraging spontaneous purchases. These events leverage consumer behavior by creating urgency through limited-edition offerings and exclusive colorways. This strategy has proven effective in driving sales and enhancing customer engagement.

Brands transitioning to a direct-to-consumer model are optimizing profit margins while gaining access to detailed consumer insights previously unavailable through traditional wholesale channels. This shift requires consistent pricing strategies across all platforms to mitigate potential channel conflicts. Virtual product demonstrations, facilitated through live streaming, are increasingly replicating the in-store experience. These digital interactions address the lack of tactile engagement inherent in online shopping. As a result, brands are enhancing customer experiences and fostering stronger connections with their target audience.

Geography Analysis

Europe contributes 33.84% of 2025 sales and combines high disposable incomes with regulatory pull. The region’s standby-power ceiling has raised the minimum engineering bar, creating exportable design templates for multinational brands. Premiumization accompanies growing attention to recyclability; many EU consumers now filter purchase choices through an environmental lens. Additionally, historically strong tea cultures across the United Kingdom, Ireland, and Germany buoy baseline kettle volumes even as alternative hot-water systems penetrate kitchens.

Asia-Pacific is projected to log a 9.12% CAGR by 2031, becoming the principal volume driver for the electric kettle market. China’s status as the world’s top appliance exporter, shipping 4.48 billion units in 2024, has created scale advantages across the supply chain . The region’s burgeoning middle class values both design and safety upgrades, catalyzing a shift from entry-level plastic units to stainless or glass mid-tier models. Manufacturing clusters in Guangdong and Zhejiang provinces shorten iteration cycles, enabling rapid accommodation of EU compliance tweaks.

North America records mature penetration but faces substitution pressure from microwave usage and integrated instant boilers. Nevertheless, the market remains attractive for premium brands that emphasize design language and IoT capabilities. Hamilton Beach’s USD 156.7 million Q3 2024 revenue showed category resilience when paired with margin-expanding product mixes . South America, the Middle East, and Africa trail in adoption but deliver pockets of high growth whenever GDP per-capita thresholds intersect with retail infrastructure expansion. Localization of color palettes and plug standards is central to winning early share in these emerging territories.

Competitive Landscape

The top five vendors collectively account for a substantial share of global revenue, resulting in a moderately fragmented market structure. Strix Group maintains dominance in the critical safety control sub-component segment, leveraging its strong presence in regulated markets to establish an oligopolistic position. This dominance creates a competitive layer beneath the finished goods market. Midea Group secures its position as the global leader in unit production, supported by an annual capacity of 100 million units. This capacity enables Midea to serve both its proprietary house brands and original design manufacturing (ODM) clients effectively.

Competitive strategies in the market are divided into two primary approaches. Large-scale players capitalize on their extensive manufacturing capabilities to target multiple price segments. In contrast, premium-focused companies prioritize high-quality materials, design aesthetics, and seamless ecosystem integration to differentiate themselves. Component innovation plays a pivotal role in driving competition, with features like low-noise induction coils and double-wall insulation increasingly incorporated into mid-range products. These advancements are partly driven by compliance with European acoustic comfort regulations. As IoT technology continues to evolve, data ownership is expected to become a critical competitive advantage, enabling companies to bundle consumables and subscription-based services around hot beverage consumption habits.

Electric Kettle Industry Leaders

Hamilton Beach Brands Holding Co.

Koninklijke Philips N.V.

Breville Pty Limited

Groupe SEB (Tefal & Krups)

Spectrum Brands Holdings (Russell Hobbs)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: China’s home-appliance exports reached 4.48 billion units for 2024, a 20.80% year-on-year increase, under Belt and Road facilitation.

- October 2024: Hamilton Beach posted Q3 2024 revenue of USD 156.7 million, citing premium line extensions.

- September 2024: Midea Group launched a share offering in Hong Kong, marking the largest listing in over three years with approximately 492.1 million shares priced between HKD 52-54.80 each. This capital raise supports Midea's international expansion and R&D investments in smart home technologies, including electric kettles.

- February 2024: Hamilton Beach Brands acquired HealthBeacon to enhance its health and wellness product offerings, expanding beyond traditional kitchen appliances into connected health devices that could integrate with smart kettle technologies

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the electric kettle market as all plug-in countertop appliances that heat water to boiling or preset temperatures through an enclosed electric element; it covers standard, variable-temperature, travel, and smart/connected models sold through retail and institutional channels worldwide.

Scope exclusion: Stovetop, induction-base, and built-in water boilers are kept outside the scope to keep comparisons meaningful.

Segmentation Overview

- By Product Type

- Standard Electric Kettles

- Variable-Temperature Kettles

- Travel / Compact Kettles

- Smart / Connected Kettles

- By Material

- Stainless Steel

- Plastic

- Glass

- Mixed / Others

- By Capacity

- Less than 1.0 L

- 1.0 – 1.5 L

- 1.6 – 2.0 L

- Greater than 2.0 L

- By End-User

- Residential

- Commercial/HoReCa

- By Distribution Channel

- Supermarkets & Hypermarkets

- Specialty Electronic Retailers

- Online

- Other Distribution Channels

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX

- NORDICS

- Rest of Europe

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South-East Asia

- Rest of Asia-Pacific

- Middle East & Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East & Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts then interview heating-control suppliers, kettle OEMs, kitchen-appliance buyers at big-box retailers, and HoReCa distributors across Asia Pacific, Europe, North America, and the Middle East. The conversations validate material cost shifts, replacement cycles, feature adoption rates, and channel premiums that secondary sources rarely quantify.

Desk Research

We begin with detailed desk work that maps how many kettles actually flow through the global system. Public customs data for HS-851679 (electric water heaters) and UN Comtrade trade balances show unit flows by country, while EU Ecodesign and U.S. DOE appliance efficiency files reveal regulatory triggers shaping product mix. Statistics from the International Energy Agency on small appliance stock, the China Household Electrical Appliances Association shipment survey, and peer-reviewed studies on standby-power use add demand fingerprints. Annual reports pulled from D&B Hoovers and news archives on Dow Jones Factiva let us benchmark vendor revenues and average selling prices. This list is illustrative; several other open and paid sources were tapped for cross-checks.

Market-Sizing & Forecasting

We anchor the 2025 base year with a top-down build that multiplies household and commercial establishment counts by electric-kettle penetration and replacement rates, adjusted with shipment and trade reconciliations; selective bottom-up roll-ups of leading manufacturers' disclosed volumes and sampled ASP × volume checks help fine-tune totals. Key variables include average retail price swings, energy-cost elasticities, online share of small-appliance sales, smart-feature uptake, and stainless-steel material share. An ARIMA time-series forecast, stress-tested through scenario analysis discussed with our expert panel, projects figures to 2030. When data gaps emerge, such as in fragmented emerging markets, we interpolate using regional proxy indicators before rerunning the triangulation loop.

Data Validation & Update Cycle

Outputs pass variance screening against independent metrics (trade flow spikes, raw-material indices, and vendor disclosures). Senior analysts review anomalies, after which the model is frozen for publication. Reports refresh every twelve months, with interim updates if recalls, large tariff moves, or major mergers materially shift our base case.

Why Mordor's Electric Kettle Baseline Commands Reliability

Published market values differ because firms apply unique product scopes, currency conversions, and refresh cadences.

Key gap drivers include whether stovetop kettles are bundled, if coffee brewers inflate volume, the currency year chosen for conversion, and how aggressively smart-feature premiums are projected. Mordor's disciplined scope selection, annual refresh, and dual-method sizing limit such skews, giving decision-makers a steadier baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.89 B (2025) | Mordor Intelligence | - |

| USD 4.56 B (2025) | Global Consultancy A | Includes stovetop units and bundled beverage machines; uses fixed 2022 FX rates |

| USD 1.86 B (2024) | Trade Journal B | Older base year, assumes flat ASP despite premium smart uptake |

In short, our approach ties every figure back to transparent variables and repeatable steps, so clients see a balanced view they can readily track and challenge.

Key Questions Answered in the Report

What is the current size of the electric kettle market in 2026?

The market is valued at USD 1.99 billion in 2026 and is projected to reach USD 2.59 billion by 2031.

Which region holds the largest share of electric kettle revenue?

Europe leads with 33.84% of global revenue in 2025, supported by strict energy-efficiency regulations and premium product adoption.

Which product segment is growing fastest?

Smart or IoT-enabled kettles are expanding at a 9.86% CAGR through 2031 thanks to connectivity features that integrate with wider smart-home ecosystems.

How do energy-efficiency rules affect kettle design?

The EU’s 0.5-watt standby limit requires advanced insulation, sensor shutdown circuits, and firmware optimizations, pushing brands to rethink core architectures.

Why are compact kettles gaining popularity?

Rising single-person households and shrinking urban living spaces drive demand for less than 1.0 L models that conserve both countertop area and energy.

What competitive factor most shapes future market share?

Integration of IoT functions that deliver usage analytics and remote control is expected to become a decisive differentiator as connectivity costs decline.

Page last updated on: