Electric Cookers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

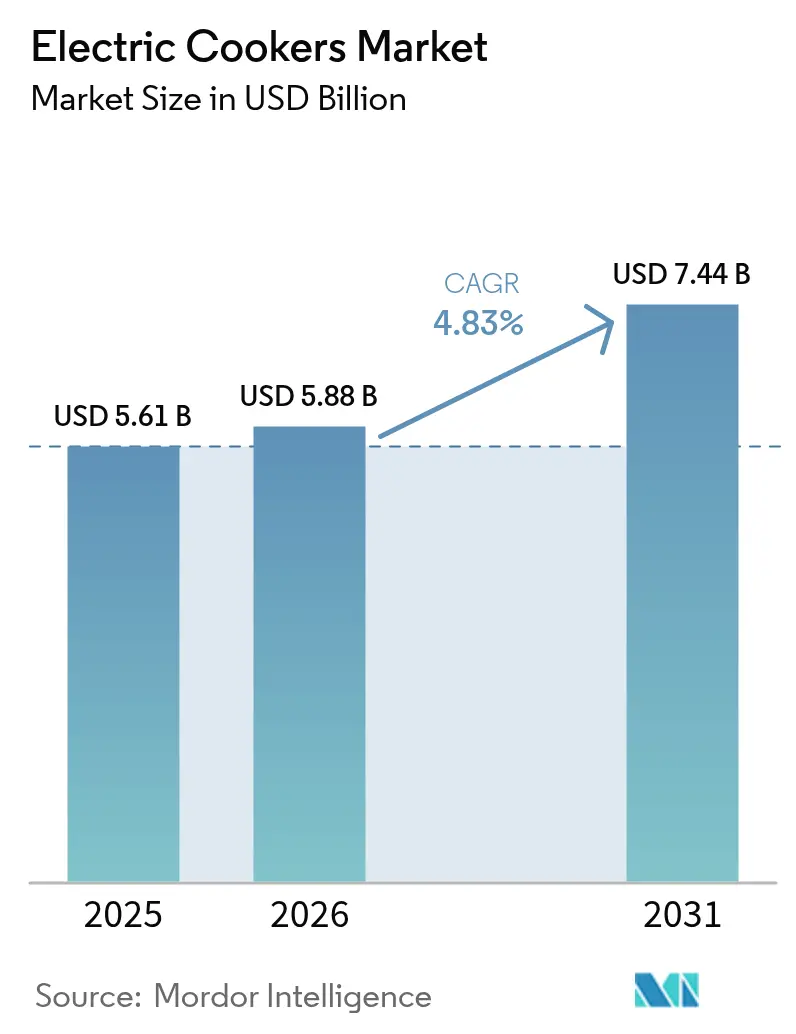

| Market Size (2026) | USD 5.88 Billion |

| Market Size (2031) | USD 7.44 Billion |

| Growth Rate (2026 - 2031) | 4.83% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electric Cookers Market Analysis by Mordor Intelligence

Electric cookers market size in 2026 is estimated at USD 5.88 billion, growing from 2025 value of USD 5.61 billion with 2031 projections showing USD 7.44 billion, growing at 4.83% CAGR over 2026-2031. This growth stems from urban population pressures that shrink average kitchen footprints, rising electricity-LPG price parity, and rapid smart-home adoption that embeds connected appliances into day-to-day routines. Energy-efficiency mandates and carbon-neutral construction rules further encourage households and businesses to shift from flame-based to induction or multi-function cookers, reinforcing the upward trajectory of the electric cookers market. Manufacturers are responding with compact, high-output models that integrate IoT controls, while distributors accelerate omnichannel strategies to reach digitally savvy buyers. Asia-Pacific remains the demand anchor owing to its large consumer base and dense manufacturing ecosystem.

Key Report Takeaways

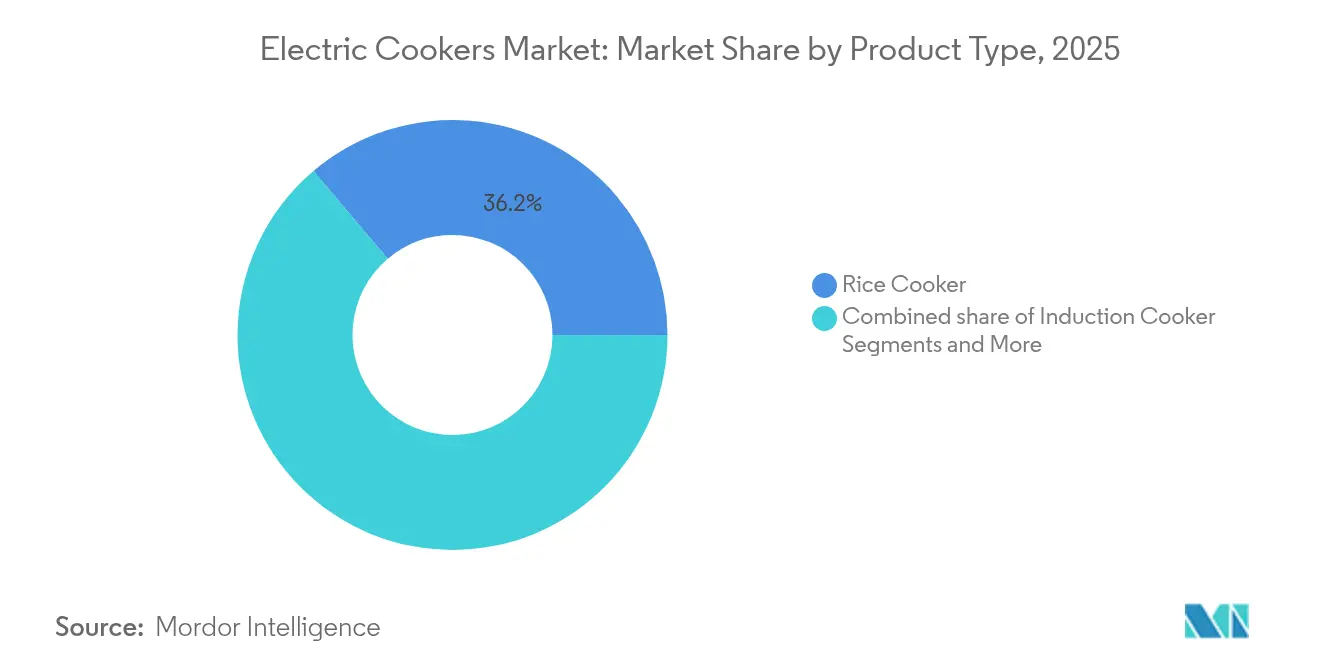

- By product type, rice cookers retained leadership with 36.20% of the electric cookers market share in 2025, while induction cookers recorded the quickest expansion at 6.78% CAGR through 2031.

- By capacity, the 3.1-6 liter segment captured 44.50% share of the electric cookers market size in 2025, whereas the ≤3 Liter segment is projected to grow at 6.28% CAGR between 2026 and 2031.

- By end-user, residential appliances held 69.70% of the 2025 revenue share of the electric cookers market; the commercial HoReCa segment is advancing at 4.98% CAGR through 2031.

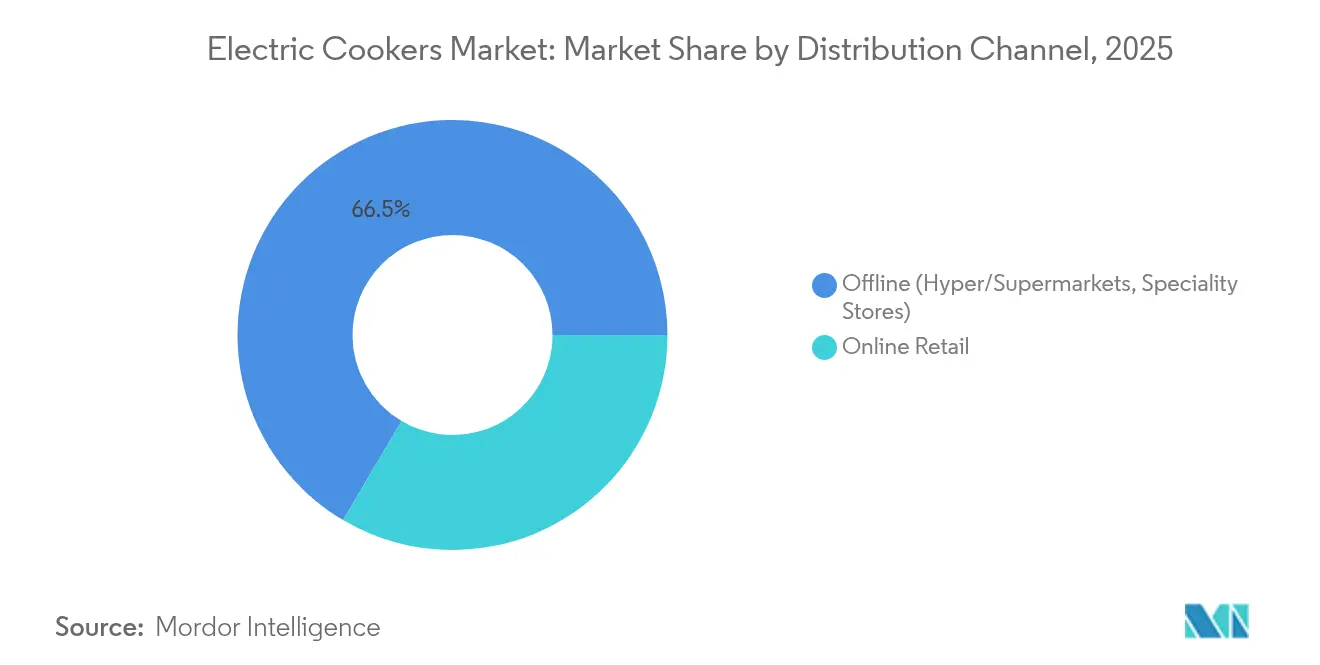

- By distribution channel, offline outlets controlled 66.50% revenue of the electric cookers market in 2025, while online retail is forecast to rise at 7.35% CAGR to 2031.

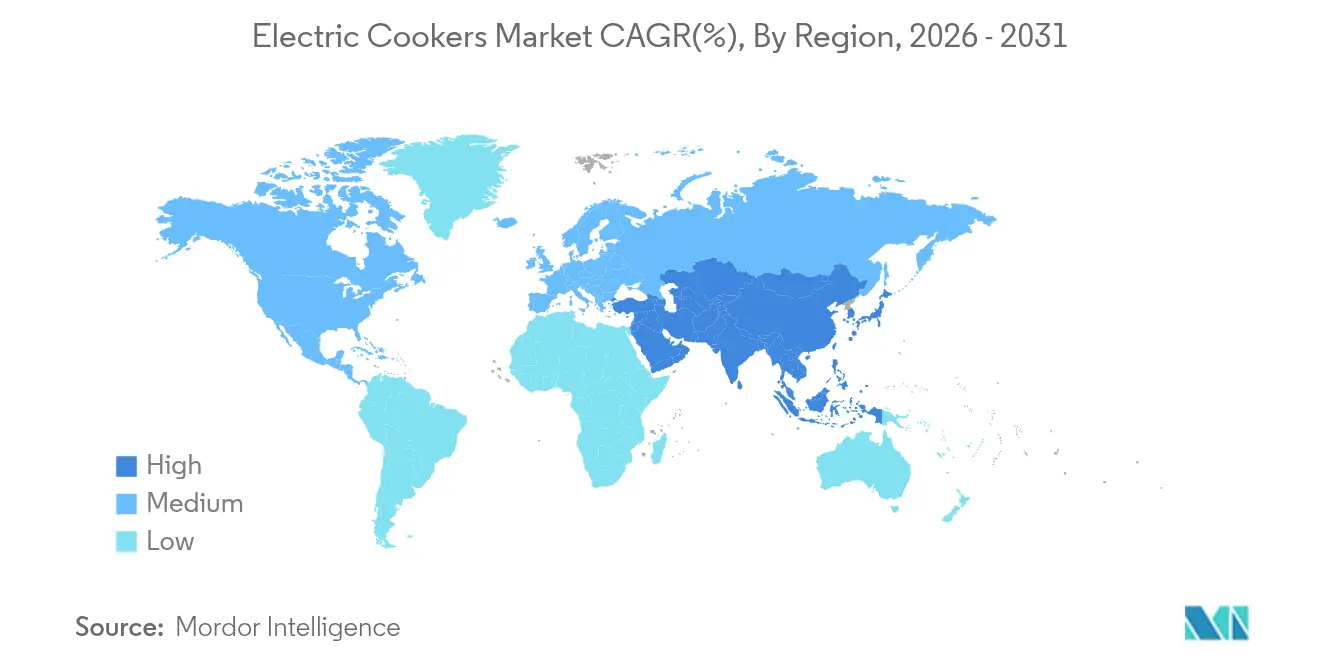

- By geography, Asia-Pacific dominated the electric cookers market with 34.00% revenue and is projected to be the fastest-growing region with a 6.55% CAGR outlook to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Electric Cookers Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urbanization & shrinking kitchens | +1.2% | Global, with a concentration in APAC and MEA urban centers | Medium term (2-4 years) |

| Rising electricity vs. LPG price parity | +0.8% | APAC core, spill-over to South America and MEA | Long term (≥ 4 years) |

| Surge in smart / IoT-enabled cookers | +0.9% | North America & EU, expanding to APAC premium segments | Short term (≤ 2 years) |

| E-commerce penetration in small appliances | +0.7% | Global, led by North America, the EU, and urban APAC | Short term (≤ 2 years) |

| Electrification programmes in emerging Asia | +0.6% | APAC emerging markets, selective MEA adoption | Long term (≥ 4 years) |

| Carbon-neutral mandates for residential cooking | +0.5% | EU core, expanding to North America and developed APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Urbanization & Shrinking Kitchens

City living forces households to maximise every square metre, making multifunction cookers indispensable. The ≤3 Liter class, growing at 6.50% CAGR, suits single-person and couple households that dominate new apartment construction in Chinese, Indian, and Gulf cities. Market analysis of European appliance sales forecasts that revenue from small appliances will achieve significant growth by 2027, as 80% of UK consumers cite energy bills as the main purchase trigger. Similar dynamics appear in Jakarta and Manila, where limited ventilation favours sealed electric solutions over open-flame gas. Developers integrate dedicated appliance niches into kitchen cabinetry, ensuring long-run demand for compact cookers within the electric cookers market. Brands that package rice, pressure, and slow-cook functions into a single countertop device benefit most from the urban downsizing trend.

Rising Electricity vs LPG Price Parity

Volatile LPG import costs and subsidy cuts are narrowing the total-cost gap between electric and gas cooking. Indonesia’s pilot induction programme found that a switch from LPG to electric pressure cookers trimmed annual household fuel spending, supporting wider roll-outs. As utility regulators add more renewables, electricity tariffs flatten, improving household budgeting predictability. The economics strengthen the electric cookers market in regions where grid upgrades coincide with phased reductions of gas subsidies. Over the forecast horizon, energy parity is expected to normalise electric cooking as a default choice among first-time appliance buyers.

Surge in Smart / IoT-Enabled Cookers

Networked cookers transform meal preparation into an automated process guided by cloud-based recipe libraries and sensor analytics. Panasonic’s HomeCHEF line now links to Fresco’s AI platform, allowing users to upload recipes and receive adjusted time-temperature profiles over a smartphone interface[1]Panasonic Corporation, “Panasonic and Fresco Extend Partnership,” panasonic.com . From 2022 to 2027, the smart appliance market is projected to experience significant growth, positioning the electric cookers market as a pivotal component within the connected kitchen ecosystem. Remote monitoring supports busy professionals, while diagnostics data feeds predictive maintenance platforms that extend product life cycles. In premium housing projects, developers market energy dashboards that visualise cooker electricity use, underscoring the efficiency benefits of induction over resistance heating. These digital features produce switching incentives that reinforce the shift from gas hob to smart countertop cooker.

E-Commerce Penetration in Small Appliances

Online channels compress appliance discovery, comparison, and purchase into a single session, scaling especially fast in middle-income economies where smartphone adoption outpaces physical retail development. Global shoppers favour detailed specification sheets and user reviews when choosing between induction, pressure, or rice cooker models. Direct-to-consumer sites allow mid-tier brands to bypass wholesale margins, while flash sales generate volume spikes that help clear inventory across multiple regions. Robust last-mile networks in metropolitan areas close the service gap with physical shops, enhancing buyer confidence and helping online retail outgrow brick-and-mortar within the electric cookers market.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost of induction technology | -0.9% | Global, particularly acute in price-sensitive emerging markets | Medium term (2-4 years) |

| Interoperability issues with legacy cookware | -0.6% | Global, with regional variations in cookware replacement cycles | Short term (≤ 2 years) |

| Intermittent power supply in rural LATAM & Africa | -0.8% | Rural LATAM & Sub-Saharan Africa | Long term (≥ 4 years) |

| EMF-related health perception risks | -0.4% | Developed markets with high health awareness | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Induction Technology

Induction cookers require sophisticated coils, power electronics, and reinforced ceramic glass, pushing retail prices beyond the reach of low-income households. In 2025, a battery-equipped countertop induction stove hit the market, but its price tag remained steep, even after incentives, highlighting a significant affordability gap for the average consumer. Installation often demands new 240-volt circuits, raising the total project cost for renters and older homes. Commercial buyers such as housing authorities can absorb premiums, yet mass residential uptake lags until component prices fall through scale manufacturing. The price hurdle slows the diffusion of high-end models but also opens space for streamlined, single-zone units that match core cooking needs at lower costs.

Intermittent Power Supply in Rural LATAM & Africa

Households in parts of Kenya, Nigeria, and Peru face voltage dips that interrupt cooking cycles, tarnishing the reliability perception of electric appliances. In Latin America, the adoption of electric cooking remains limited compared to the extensive penetration of LPG, primarily due to challenges associated with grid stability[2]International Energy Agency, “Africa Energy Outlook,” iea.org . Solar-integrated systems offer a workaround but add battery expenses that many rural consumers cannot shoulder. Government electrification roadmaps prioritise grid expansion, yet must still confront outage frequency that undermines appliance performance. Until voltage consistency improves, penetration in these regions will build slowly, moderating the global growth outlook for the electric cookers market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Rice Cookers Sustain Leadership While Induction Gains Speed

Rice cookers held 36.20% of the 2025 volume as staple food habits in China, Japan, Indonesia, and the Philippines guarantee daily use occasions. This dominance makes rice cookers the anchor of the electric cookers market and creates a replacement cycle that cushions overall demand fluctuations. Induction cookers, though starting from a smaller base, deliver a significant percentage of energy-transfer efficiency that attracts both eco-conscious consumers and commercial kitchens. Integration with recipe apps spurs experimentation beyond basic boiling functions, broadening appeal. Slow/multi-cookers benefit from urban dwellers seeking one-pot convenience, while pressure cookers occupy the meal-prep niche for time-pressed households. Brands with modular platforms that share heaters and electronics across models capture scale benefits, reinforcing cost leadership across product categories.

Second-generation induction units incorporate adaptive coil zoning, enabling pan-size detection that reduces standby losses and improves safety. Rice cooker innovation now focuses on texture algorithms that tune heat profiles for different grain varieties, catering to premium consumer segments. Electric pressure cookers extend into commercial service lines as hotels seek to cut LPG costs in buffet operations. Multi-cookers, meanwhile, cannibalise single-use appliances by bundling bake, sauté, and sous-vide modes, trimming countertop clutter in small kitchens. Collectively, these shifts diversify the electric cookers market, yet rice cookers remain the largest contributor to electric cookers market size through 2031.

By Capacity: Mid-Range Units Dominate Yet Compact Models Accelerate

The 3.1-6 liter category satisfied family meal volumes and controlled 44.50% of revenue in 2025, establishing it as the mass-market sweet spot for the electric cookers market. Manufacturers deliver this capacity with minimal price premiums, making it accessible to middle-income households. Urbanisation is, however, lifting ≤3 Liter demand at a 6.28% growth clip, mirrored in high-rise apartments across Mumbai, Seoul, and Dubai, where countertop real estate is scarce. Brands market these cookers with fold-in handles and detachable cords to support portability and easy storage.

Above 6 liters, sales concentrate in schools, canteens, and full-service restaurants that prize large batch output. Energy audits show that replacing gas boilers with large induction vats saves up to 40% on monthly utility bills and simplifies ventilation. In the consumer arena, extended families in rural China still prefer 5-liter plus units for batch cooking, sustaining baseline volume. Over time, smaller households and solo living will lift compact-segment contribution to the electric cookers market size, although mid-range models will remain the revenue core thanks to their versatility.

By End-User: Residential Rules While Commercial Kitchens Catch Up

Residential buyers generated 69.70% of 2025 turnover, reflecting the centrality of cooking in daily routines and the continual need to replace ageing units. Safety, convenience, and lower ambient heat are the deciding factors that keep homes loyal to electric formats. Meanwhile, the HoReCa channel is forecast to expand at 4.98% CAGR as restaurants face rising gas prices and labour shortages that elevate the value of precision temperature control. Induction’s near-instant response slashes line-cook idle time and reduces kitchen heat, lowering HVAC costs.

Hotel chains in Singapore and Dubai stipulate induction cooktops for staff canteens during refurbishments, promoting best practice demonstrations that spill into consumer awareness. Ghost kitchens add another growth node, choosing compact induction ranges to maintain flexible layouts for multi-brand menus. In many markets, commercial adoption precedes residential change, reinforcing trust in electric solutions. This feedback loop strengthens the long-run outlook for the electric cookers market despite the present residential dominance.

By Distribution Channel: Offline Still Leads, Online Rises Fast

Brick-and-mortar outlets, hypermarkets, electronics chains, and appliance specialists, retained 66.50% of 2025 sales as shoppers value tactile inspection before investing in a core kitchen tool. Store displays allow live demonstrations of induction responsiveness, building purchase confidence among first-time buyers. The electric cookers market is, however, migrating online at 7.35% CAGR as e-commerce platforms refine return policies and instalment payment options. Marketplace algorithms surface long-tail brands, expanding consumer choice beyond national incumbents.

Omnichannel plays dominate strategic roadmaps: manufacturers encourage showroom visits coupled with QR-code links that route customers to brand web-stores for colour or feature variants unavailable in store. In emerging Asia, social-commerce livestreams showcase cooking demos that convert viewers within minutes via integrated checkout. Supply-chain digitalisation gives brands unprecedented visibility into sell-through rates, enabling dynamic pricing that balances inventory across regions. As connectivity improves, the online route will contribute a rising share of the electric cookers market size without displacing physical retail altogether.

Geography Analysis

Asia-Pacific commanded 34.00% of global revenue in 2025 and is projected to grow at 6.55% CAGR to 2031. China’s dual role as mega-market and production base grants unmatched scale, while Indonesia and Vietnam push adoption through LPG-to-induction conversion schemes backed by tariff subsidies. Rice-centric diets lock in rice cooker demand, and dense urban clusters favour compact multi-function units. Manufacturers such as Midea, with 100 million-unit annual output capacity, flood both domestic and export channels at competitive prices. Parallel investments in smart-appliance R&D help regional brands extend reach into premium segments.

In North America, the market's growth is influenced by gas-restriction regulations in cities such as San Francisco, which mandate the use of electric appliances in new constructions. These regulations are driving builders to prioritize electric solutions, thereby boosting demand. The replacement market is also witnessing growth as property owners upgrade outdated ranges with induction models to comply with energy codes. This trend underscores the increasing importance of energy efficiency in the region's appliance market. Additionally, the rising adoption of IoT-enabled cookers, which integrate with voice assistants, positions connected devices as the fastest-growing segment within the electric cookers market.

The European market is experiencing steady growth at a consistent CAGR, supported by stringent carbon-neutral construction regulations and increasing consumer demand for energy-efficient appliances. The small appliance segment is projected to witness significant revenue growth, driven by the rising adoption of smart appliance categories. E-commerce continues to gain traction in key markets like Germany and the UK, with penetration rates exceeding regional averages and bolstering the online sales channel. Scandinavian utility providers are introducing time-of-use tariffs, encouraging consumers to shift cooking activities to off-peak hours. This initiative further enhances the cost competitiveness of electricity compared to LPG, aligning with broader energy efficiency goals.

Urbanization across key cities such as Lima and Bogotá, along with the expansion of e-commerce platforms, is driving a favorable CAGR outlook for South America. Clean-cooking initiatives targeting the millions of individuals reliant on solid fuels are creating opportunities for subsidy-driven electric cooker programs. However, gaps in distribution networks remain a significant challenge. Meanwhile, increasing smartphone penetration is enhancing consumer awareness and fueling demand in the region.

Africa is experiencing regional growth rate, driven by hydropower-supported electrification initiatives and rapid population growth. Government efforts, such as Uganda's national eCooking roadmap and Kenya's off-grid solar stove pilot programs, highlight a strong commitment to advancing electric cooking solutions despite ongoing grid stability issues. While the market remains in its nascent stage, the rising urban middle class in cities like Lagos and Nairobi is beginning to perceive induction cookers as premium products, positioning Africa as a critical growth frontier for the electric cookers market.

Competitive Landscape

Moderate concentration defines the electric cookers market, with the top five suppliers holding half of the revenue. Midea leverages its 100 million-unit output scale to deliver cost leadership across rice, pressure, and induction categories while integrating Wi-Fi and voice-control modules into flagship lines. Panasonic differentiates through partnerships that embed AI recipe engines, anchoring its premium positioning. Groupe SEB pursues R&D-driven innovation, investing in NUTRICE rice-texture optimisation and Cook2Health digital-coaching projects to maintain brand equity.

Strategic activity spans three paths. First, portfolio consolidation: Whirlpool’s EMEA spin-off into Beko Europe extends geographic presence and synergies in sourcing and logistics. Second, technology intensification: Copper’s battery-equipped induction platform addresses outage-prone areas, although price premiums limit near-term volume. White-space opportunities persist in mid-tier smart cookers that balance affordability and connectivity, especially for emerging-market consumers.

Competitive intensity escalates as new entrants exploit online channels to bypass legacy distribution, compressing product life cycles. Intellectual-property portfolios around induction coil design and smart-control algorithms are becoming decisive as brands seek defensible margins. Market incumbents, therefore, ramp up joint ventures with chipset makers and cloud platforms. Scale operators who couple efficient manufacturing with modular electronics stand to widen their share, yet local specialists that cater to regional taste profiles and cookware norms can still command loyal niches in the electric cookers market.

Electric Cookers Industry Leaders

Panasonic Corporation

Midea Group

Koninklijke Philips N.V.

LG Electronics Inc.

Groupe SEB (Tefal)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Whirlpool posted its highest profit in 13 years and announced plans for 40 new kitchen products in 2025.

- October 2024: California-based Copper launched a plug-and-play induction stove with the New York City Housing Authority ordering 10,000 units for retrofit projects.

- April 2024: Whirlpool completed its EMEA transaction, creating Beko Europe B.V. while retaining a 25% stake.

- February 2024: Groupe SEB finalised the acquisition of Sofilac to enter high-end professional cooking equipment.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the electric cookers market as countertop or range-style appliances that employ electricity via resistive coils, ceramic elements, or induction heating to boil, bake, steam, pressure-cook, or slow-cook food in residential and light-commercial kitchens.

Scope exclusion: stand-alone gas cookers, outdoor camping stoves, and fully professional combi-ovens sit outside this assessment.

Segmentation Overview

- By Product Type

- Induction Cooker

- Rice Cooker

- Slow/Multifunctional Cooker

- Electric Pressure Cooker

- Electric Range & Cooktop

- Other Electric Cookers

- By Capacity

- ≤3 Litre

- 3.1-6 Litre

- >6 Litre

- By End-User

- Residential

- Commercial/HoReCa

- By Distribution Channel

- Offline (Hyper/Supermarkets, Speciality Stores)

- Online Retail

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Peru

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- BENELUX

- NORDICS

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- South-East Asia

- Rest of Asia-Pacific

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Nigeria

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

To resolve gray areas, our team conducted interviews with cookware technologists, appliance distributors, and e-commerce category managers across Asia-Pacific, North America, and Europe. Consumer surveys in multiple cities clarified adoption triggers, typical replacement cycles, and average selling prices. Feedback fine-tuned input assumptions and stress-tested scenario ranges.

Desk Research

Mordor analysts began with public datasets from bodies such as the International Energy Agency, UN Comtrade, and the US Energy Information Administration, which helped size appliance fleets and electricity price trends. We blended these with trade association briefs from APPLiA Europe and the Japan Electrical Manufacturers' Association, customs shipment logs accessed through Volza, patent counts via Questel, and company 10-Ks for leading OEMs. Subscription tools, including D&B Hoovers and Dow Jones Factiva, supplied historical revenue splits and channel snapshots. The sources listed illustrate our approach and are not exhaustive.

Market-Sizing & Forecasting

We applied a top-down construct using recorded household counts, electrification rates, and small-appliance penetration to estimate the in-use stock, which was then multiplied by replacement intervals to derive annual demand. Select bottom-up checks, supplier revenue roll-ups and sampled ASP × unit volumes, validated totals before adjustment. Key variables include induction cooker penetration, e-commerce share of small-appliance sales, regional disposable-income growth, and average kitchen renovation spend. A multivariate regression model projects each driver to 2030, while scenario analysis handles energy subsidy shifts. Gaps in bottom-up data, for informal offline sales, were bridged by calibrated ratios from primary interviews.

Data Validation & Update Cycle

Outputs pass three-step variance checks, peer review, and senior analyst sign-off. We refresh models each year and trigger interim updates after material policy or pricing shocks. A last-mile sense check precedes every client delivery.

Credibility Anchor - Why Mordor's Electric Cookers Baseline Earns Client Trust

Published numbers often diverge because firms pick different product baskets, price levels, and refresh cadences.

Key gap drivers include: some studies merge electric with gas or microwave units, others restrict themselves to rice cookers, and several uplift factory-gate values with retail mark-ups that inflate totals. Mordor's base year is 2025, its scope mirrors real-world buyer choice, and its annual refresh captures rapid induction uptake.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.61 B (2025) | Mordor Intelligence | - |

| USD 7.50 B (2023) | Global Consultancy A | Combines stoves, ovens, and cookers; retail ASPs included |

| USD 3.36 B (2022) | Trade Journal B | Focuses on electric rice cookers only; factory-gate pricing |

| USD 8.21 B (2023) | Industry Report C | Adds gas pressure cookers and small commercial units |

In short, Mordor's disciplined scope selection, double-path modeling, and yearly audits give decision-makers a balanced, transparent baseline they can retrace and rerun with confidence.

Key Questions Answered in the Report

What is the current value of the electric cookers market?

The electric cookers market generated USD 5.88 billion in 2026 and is forecast to reach USD 7.44 billion by 2031 at a 4.83% CAGR.

Which product segment leads the electric cookers market?

Rice cookers dominate with a 36.20% market share in 2025, reflecting consistent demand across Asian households.

Why are induction cookers growing faster than other types?

Induction units convert a significant amount of input energy into heat, offer precise temperature control, and integrate easily with smart-home platforms, driving a 6.78% CAGR through 2031.

What region is expected to grow the fastest?

Asia-Pacific shows the highest regional percentage because of expanding electrification programs and rising urban middle-class consumption.

How significant is online shopping for electric cookers?

Online retail is the fastest-growing channel at 7.35% CAGR, driven by detailed product information, reviews, and direct manufacturer promotions that appeal to digital-first consumers.

What are the main obstacles to the wider adoption of electric cookers?

High upfront costs for induction technology and unreliable power supplies in rural Latin America and Africa remain the principal barriers, trimming global growth potential by almost 1.7 percentage points.

Page last updated on: