Egypt Residential Construction Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

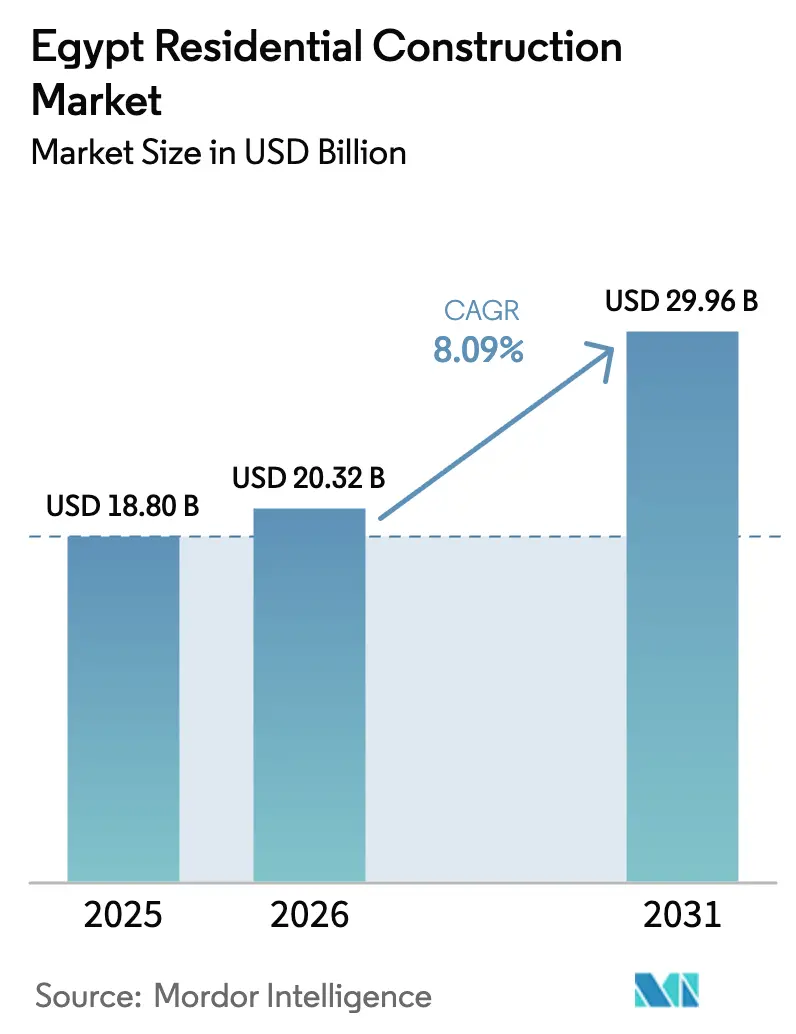

| Base Year Market Size (2025) | USD 18.80 Billion |

| Market Size (2026) | USD 20.32 Billion |

| Market Size (2031) | USD 29.96 Billion |

| Growth Rate (2026 - 2031) | 8.09% CAGR |

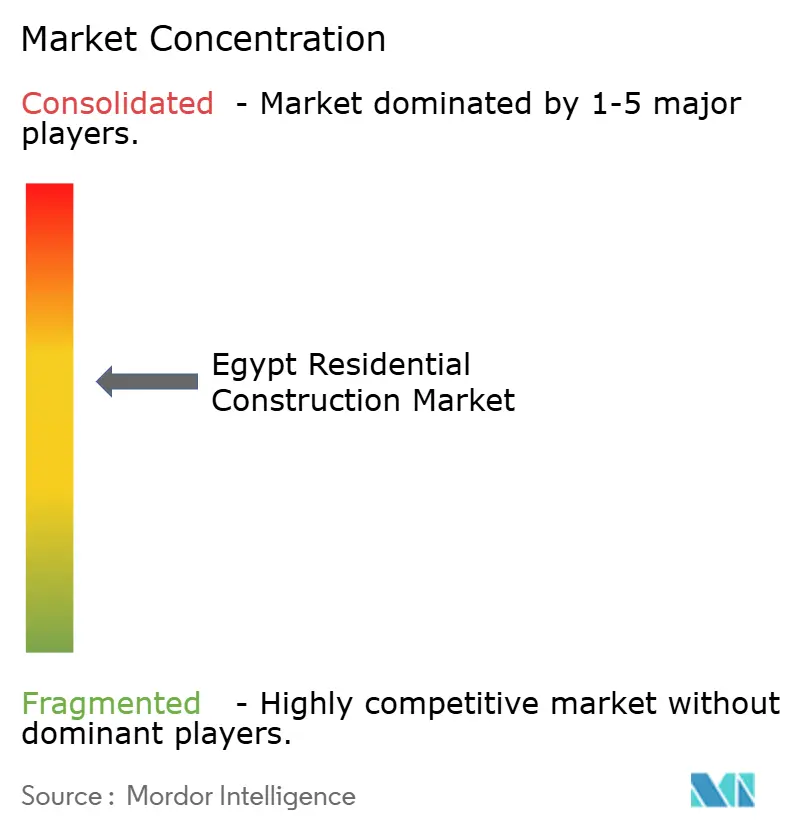

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Residential Construction Market Analysis by Mordor Intelligence

The Egypt residential construction market size is expected to grow from USD 18.80 billion in 2025 to USD 20.32 billion in 2026 and is forecast to reach USD 29.96 billion by 2031 at 8.09% CAGR over 2026-2031. Momentum comes from government-led megaprojects, deep pools of private capital, and steady inflows of foreign direct investment. Rising household formation, a persistent 1.5 million unit deficit, and targeted mortgage subsidies sustain structural demand even when macro conditions tighten. Rapid build-out of the New Administrative Capital and other corridor cities pulls contractors, suppliers, and financiers toward large, phased projects that offer predictable cash-flow and technological scale. Currency volatility adds cost pressure; however, domestic steel capacity, tariff adjustments, and greater use of modular systems limit supply-chain disruption.

Key Report Takeaways

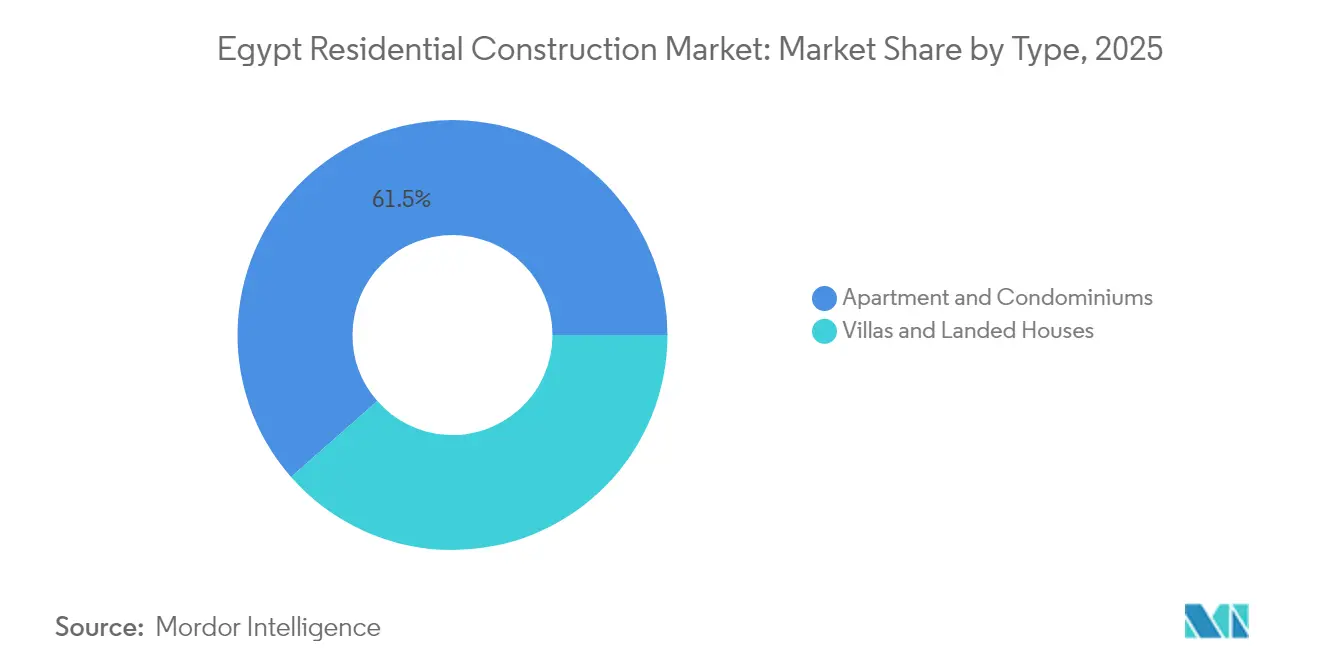

- By type, apartments and condominiums held 61.48% of the Egypt residential construction market share in 2025, while villas and landed houses are projected to expand at a 8.67% CAGR through 2031.

- By construction type, new construction commanded 77.30% of the Egypt residential construction market size in 2025; the renovation segment is advancing at an 8.55% CAGR to 2031.

- By construction method, conventional on-site techniques captured 84.20% revenue share in 2025; modern methods of construction post the highest growth at 8.92% CAGR.

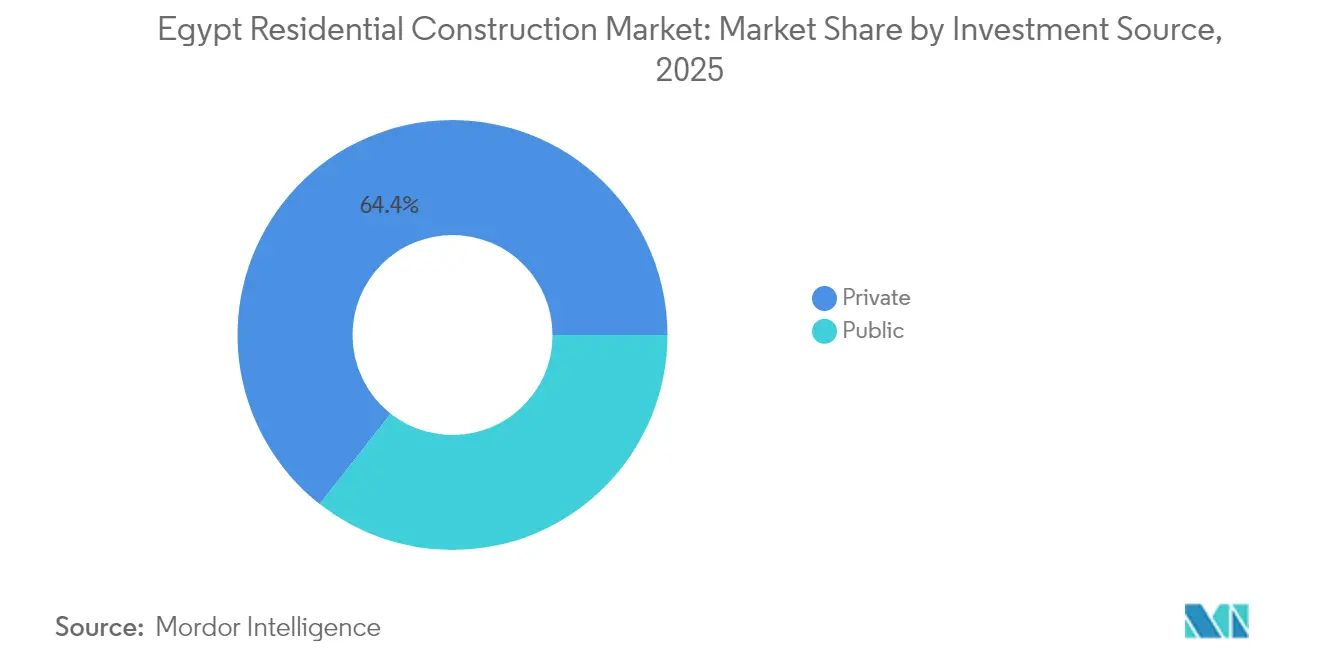

- By investment source, the private segment led with 64.40% share of the Egypt residential construction market in 2025, whereas public spending registers the fastest 10.18% CAGR.

- By region, Greater Cairo accounted for 40.55% revenue share in 2025; Rest of Egypt is the quickest-growing geography at a 9.05% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Egypt Residential Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-backed social-housing schemes | +2.1% | National, concentration in Greater Cairo and new urban communities | Medium term (2-4 years) |

| Rapid household formation outpacing supply | +1.8% | Greater Cairo, Alexandria, urban centers nationwide | Long term (≥ 4 years) |

| Mortgage-refinancing reforms | +1.5% | National, early gains in new urban communities | Short term (≤ 2 years) |

| New Administrative Capital & megacity hubs | +1.4% | Greater Cairo region, North Coast | Medium term (2-4 years) |

| Expatriate remittance-driven demand | +0.9% | North Coast, New Cairo, premium districts | Medium term (2-4 years) |

| Prefabricated and modular adoption | +0.8% | New urban communities, government housing | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government-backed Social-Housing Schemes Reshape Urban Development

National housing programs allocate EGP 100 billion to build 600,000 units and have already delivered 246,000 homes while upgrading 130 informal areas, anchoring demand for standardized, mid-rise apartment blocks that can be replicated quickly[1]Mohamed Sabry, “Government allocates EGP 100 billion for social housing,” ahramonline.com. The scale redirects contractor focus toward high-volume, cost-efficient designs and opens the Egypt residential construction market to suppliers of precast panels, low-carbon cement, and smart-metering systems. Gender-inclusive ownership criteria, backed by a USD 500 million World Bank loan, influence unit sizes and communal services, prompting developers to integrate childcare facilities and safer public spaces. The 7,440-unit Al-Asmarat complex, accommodating 100,000 residents, validates the model’s viability and sets benchmarks for future sites. Together, these schemes shift attention from gated luxury to mass housing that meets affordability thresholds without sacrificing build quality.

Rapid Household Formation Outpacing Supply Creates Structural Demand

Egypt’s population is expected to approach 127 million by 2030, necessitating 700,000 new units each year against a current delivery capacity of 500,000 units[2]World Bank Staff, “Housing gap update for Egypt,” worldbank.org . This persistent gap embeds long-run growth into the Egypt residential construction market, ensuring steady workflows for builders and related trades. Informal settlements house 40% of Cairo’s residents, driving parallel streams of new-build and in-situ redevelopment projects. The demographic dividend also supplies labor: construction already employs over 4 million direct workers and another 3 million in supporting roles, mitigating wage inflation risk while reinforcing consumption of building materials. Thirty-year mortgages at 3% interest expand eligibility for first-time buyers, thereby turning latent demand into contracted sales rather than speculative intent.

Mortgage-Refinancing Reforms Unlock Latent Demand

The Central Bank allocates EGP 10 billion to subsidize long-tenor loans for low- and middle-income buyers and caps rates at 3%, slicing monthly payments and widening the pool of qualified borrowers. Complementary legislation under Law No. 194 of 2020 modernizes credit markets and enables fintech lenders to originate micro-mortgages. Egypt’s secondary liquidity facility, modeled on Malaysia’s Cagamas, promises to recycle mortgage assets and keep bank balance sheets fluid, albeit impact remains embryonic. Early uptake is strongest in new urban communities where clear land titles accelerate loan approvals, while core city districts lag due to lingering documentation hurdles. Nonetheless, the Egypt residential construction market benefits as financiers package mortgages into securitized products, providing developers with assured offtake and lower working-capital cycles.

New Administrative Capital & Megacity Corridors Transform Regional Development

The USD 58 billion New Administrative Capital stretches across 270 square miles and is designed for 6.5 million inhabitants. Phase I is already housing 48,000 civil servants, triggering commuter demand for satellite districts and mixed-use catchment zones. Smart infrastructure—from district-cooling to automated waste management—raises baseline specifications for upcoming projects, pushing contractors toward digital tools and energy-saving materials. Parallel North Coast complexes such as New Alamein and the USD 35 billion Ras El-Hekma plan replicate the blueprint, ensuring geographic diversification of the Egypt residential construction market. Connectivity via high-speed rail and upgraded highways further multiplies residential plots along transit corridors, embedding construction activity in a multi-node urban system rather than a single metropolis.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Currency-driven spikes in material costs | −2.8% | National, acute in import-dependent projects | Short term (≤ 2 years) |

| Lengthy land-registration & permit delays | −2.2% | National, severe in older urban districts | Medium term (2-4 years) |

| Tight domestic liquidity for developers | −1.7% | National, mid-tier builders most exposed | Short term (≤ 2 years) |

| Imported building-system dependency risk | −1.8% | National, affects premium and commercial segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Currency-Driven Spikes in Material Costs Challenge Project Viability

The Egyptian pound has lost 70% of its value since March 2022, raising the local price of imported fixtures, elevators, and finishing items even as global billet prices eased. Developers forecast a 10-30% surge in 2025 input costs, compressing margins on fixed-price contracts. Egypt’s annual steel capacity of 9.8 million tons tempers exposure, and the cement sector’s 50% utilization offers room for supply ramp-up, yet specialized MEP systems still rely on dollar-priced imports. The Central Bank’s transition to a free float is expected to narrow black-market spreads, but cost spikes hit project feasibility faster than tender prices can adjust. Tariff tweaks on iron imports supply temporary relief, though the uncertainty prompts contractors to hedge via staggered procurement or index-linked clauses.

Lengthy Land-Registration & Permit Bureaucracy Constrains Development Velocity

Obtaining clear title and building permits can add 6-12 months compared with regional norms, especially in central cities where multiple agencies share oversight. While the “Golden License” fast-track exists for strategic projects, execution varies by governorate, limiting its impact beyond headline cases. Smaller developers face security clearance layers and fee schedules that erode working capital and deter new entrants, leading to narrower competition and potential cost inflation for buyers. Digital cadasters and one-stop shops are under roll-out, yet full deployment remains a medium-term prospect. Until processes simplify, the Egypt residential construction market absorbs bureaucratic delay as a quasi-fixed cost baked into sales pricing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Apartments Drive Volume While Villas Capture Premium Growth

Apartments generated the largest slice of revenue, reflecting 61.48% of the Egypt residential construction market share in 2025 and anchoring the Egypt residential construction market size through high-density, mid-rise blocks across Greater Cairo. Demand stems from affordability, government design templates, and the need to maximize scarce urban land. Developers prefer pre-sold apartment towers to monetize cash flow early, leveraging installments that reduce reliance on bank debt. Social-housing programs amplify the trend by standardizing four-to-ten-story designs that streamline procurement and labor training. Urban workforce households, particularly younger demographics, choose condominium formats near job nodes to cut commuting time and access mass transit.

Villas and landed houses, though a smaller base, log the fastest 8.67% CAGR as coastal mega-developments such as Ras El-Hekma attract high-net-worth Egyptians and expatriates. Price points topping USD 8,000 per square meter in New Alamein support profit margins that subsidize infrastructure in adjacent apartment districts. Developers bundle branded hospitality and private beach access, converting lifestyle preferences into pre-launch bookings that often sell out entire tranches in days. Remittance flows and relaxed foreign-ownership rules deepen the buyer pool, while improved highway links shrink travel time from Cairo to the Mediterranean. Consequently, villa projects increasingly balance the volume dominance of apartments, creating a dual-speed Egypt residential construction market that serves both mass and premium segments.

By Construction Type: New Construction Dominates While Renovation Accelerates

New builds represented 77.30% of the Egypt residential construction market size in 2025, propelled by a 1.5 million unit backlog that positions residential delivery as essential infrastructure. Greenfield sites in the New Administrative Capital and 37 planned smart cities permit master-developers to integrate utilities, renewable grids, and digital platforms from day one, lowering life-cycle cost for occupants and municipalities. State agencies bundle residential blocks with schools and hospitals, ensuring immediate community viability and therefore faster sales absorption. Contractors benefit from predictable sequencing and economies of scale in material procurement.

Renovation, though smaller, is forecast to outpace GDP at an 8.55% CAGR because legacy districts require seismic upgrades, energy-efficiency retrofits, and façade refurbishments. Alexandria’s Gheit El-Enab project shows that mixed finance—municipal grants plus developer equity—can transform unsafe buildings while preserving neighborhood identity. Energy-code enforcement pushes owners to install double-glazed windows, solar water heaters, and LED lighting, generating demand for skilled retrofit labor and specialized products. Financing instruments such as green mortgages are beginning to appear, facilitating homeowner investment in upgrades. As urban cores densify, renovation becomes a cost-effective alternative to relocation, ensuring a steady contribution to the Egypt residential construction market.

By Construction Method: Conventional Methods Prevail Despite Modern Innovation

Traditional on-site labor-intensive methods still captured 84.20% share in 2025, sustained by abundant labor, established contractor expertise, and entrenched supply chains. Large Egyptian builders scale operations through craft specialization and subcontractor networks, enabling them to tackle simultaneous megaprojects without resource clash. Cost visibility and lender familiarity keep conventional techniques the default on most mid-market schemes. Yet productivity ceilings and waste levels prompt gradual change.

Modern methods of construction, expanding at 8.92% CAGR, include precast, volumetric modules, and emerging 3D-printing pilots. Building Information Modeling, capable of reducing rework by up to 20%, gains traction as developers chase thinner contingencies. Factories producing façade panels for the New Administrative Capital cut erection time, freeing cranes sooner for follow-on trades. Early adopters report lower insurance premia because precision manufacturing reduces on-site accidents. High upfront investment and the need for skilled technicians temper mass adoption, but public housing deadlines and sustainability metrics ensure steady penetration into the Egypt residential construction industry.

By Investment Source: Private Capital Leads While Public Accelerates

Private developers held 64.40% of 2025 spending, buoyed by bank consortium financings like the EGP 10.3 billion Badya facility that underwrites multi-phase smart-city delivery. Diversified groups such as TMG deploy internal cash from record presales to fund land acquisition, thereby reducing leverage and interest exposure. Foreign investors expand their footprint through headline commitments—UAE’s USD 35 billion Ras El-Hekma chief among them—bringing hard currency and international branding that de-risk marketing.

Public investment, advancing at a 10.18% CAGR, focuses on social-housing and catalytic infrastructure. Ministries bundle transportation, utilities, and civic amenities into turnkey packages that lower operating costs for residents while encouraging private infill. The government’s Vision 2030 goals call for private-sector participation to exceed 50% of national investment, yet mega-schemes financed via sovereign funds remain pivotal. This complementary balance shields the Egypt residential construction market from abrupt budget shifts and keeps tender pipelines diversified across income segments.

By Region: Greater Cairo Dominates While Coastal Areas Drive Growth

Greater Cairo contributed 40.55% of the Egypt residential construction market share in 2025 owing to its role as the administrative and economic core. Relocation of ministries to the New Administrative Capital maintains steady unit demand for civil servants and service providers, while metro extensions improve east-west connectivity. Premium enclaves in New Cairo and 6th of October City absorb aspirational middle-class buyers seeking gated environments and international schools. Supply pipeline visibility encourages lenders to offer competitive mortgage packages, sustaining liquidity in the resale market.

Rest of Egypt posts the highest 9.05% CAGR through 2031, mainly inside North Coast and Western Desert corridors. New Alamein’s skyline and TMG’s SouthMED set a fresh benchmark for integrated coastal living, combining tourism, retail, and medical clusters to support permanent residency. Inland, the 114-kilometer New Delta canal unlocks agricultural land and spurs ancillary townships that broaden the geographic footprint of the Egypt residential construction market. Alexandria and Giza capture renovation budgets and brownfield redevelopment, ensuring balanced growth between frontier districts and mature metropolitan centers.

Geography Analysis

Greater Cairo’s outsized presence rests on a USD 58 billion capital relocation program that injects continuous civil-service housing demand and anchors auxiliary private projects. High-speed rail links shrink commuter time to satellite cities, allowing younger households to accept longer journeys in exchange for modern housing stock. Social-housing clusters like Al-Asmarat provide 7,440 units and showcase government prowess in rehousing informal-settlement residents without livestock displacement, building social trust. Grade-A office demand spilling over from the New Administrative Capital encourages mixed-use developments that place residential towers atop retail podia.

Alexandria and Giza combine urban-renewal spending with heritage preservation. Alexandria’s EGP 39 billion public-works plan over five years rewires utilities and stabilizes waterfront structures, thereby raising the ceiling for higher-density infill. Giza leverages proximity to Cairo’s job market and the Grand Egyptian Museum to attract residential tourism workers who prefer suburban townhouses close to ring-road interchanges. Energy-efficiency mandates in both governorates create retrofit activity that offsets any slowdown in greenfield launches.

Rest of Egypt gathers momentum as highway upgrades slash drive times to Red Sea and Mediterranean resorts. Ras El-Hekma and New Alamein bring global master-planners and marquee architects, injecting design diversity into the Egypt residential construction market. Inland governorates tap rural-to-urban migration, especially along the New Delta canal, where pilot agro-towns incorporate worker housing, silos, and community services. Government targets for doubling the share of population residing in new urban communities to 12% by 2030 imply sustained allocation of land and infrastructure budgets. Together these dynamics spread residential investment beyond Cairo, reducing concentration risk and fostering regional economic balance.

Competitive Landscape

Market concentration is moderate. Heavyweights such as Talaat Moustafa Group reported a 310% profit jump in H1 2024, supported by EGP 17 billion revenue and USD 21 billion in new North Coast commitments Hassan Allam Holding’s backlog ballooned to USD 5.5 billion, evidencing scalability in EPC services across housing, infrastructure, and utilities. Palm Hills secured Egypt’s largest real-estate finance package—a EGP 10.3 billion syndicated loan—to fund its 3,000-acre Badya project, demonstrating creditor appetite for landmark schemes even during currency volatility.

Technology adoption distinguishes front-runners. SODIC’s Nobu-branded venture integrates hospitality and residences, leveraging Building Information Modeling to compress design cycles by 20% and reduce material variance by 44% itcon.org. Hassan Allam pilots robotic rebar-tying, lowering accident rates and satisfying rising ESG tender requirements. Mid-tier developers without access to low-cost financing pivot toward renovation and infill, niches less capital-intensive but still profitable if process expertise is strong.

Strategic alliances continue. UAE-based ADQ’s USD 35 billion Ras El-Hekma pledge pairs Gulf capital with Egyptian land and labor, while Saudi PIF’s USD 5 billion announcement signals multi-country interest in Egyptian residential yields. Contractors form joint ventures with specialized modular manufacturers to meet megaproject timelines, diversifying risk and knowledge. Despite intensified rivalry, land banks, regulatory familiarity, and credit relationships keep incumbents ahead, yet open competition in smart-city services provides entry points for technology-centric SMEs.

Egypt Residential Construction Industry Leaders

Orascom Construction

BIC for Contracting & Construction

Consolidated Contractors Company

Detac

Palm Hills Developments

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Nawy acquired ROA to launch “Nawy Unlocked,” a property monetization platform designed to streamline asset liquidity for owners.

- January 2025: Egypt’s House of Representatives amended the Desert Land Law, permitting full foreign ownership of land for investment projects.

- October 2024: Baker McKenzie Cairo advised Palm Hills on a EGP 10.3 billion syndicated financing for the Badya smart-city project.

- September 2024: Saudi Public Investment Fund committed USD 5 billion to Egypt, widening funding avenues for large-scale residential schemes.

Egypt Residential Construction Market Report Scope

Residential construction is expanding, renovating, or building a new house or area designed for residential reasons. Residential development can be a complicated process with many phases and parties.

The market is segmented by type (apartment & condominiums, villas, and other types) and construction type (new construction and renovation). The report offers market size and forecasts for Egypt's Residential Construction Market in value (USD billion) for all the above segments. The report also covers the impact of geopolitical events and pandemic on the market.

| Apartment & Condominiums |

| Villas and Landed Houses |

| New Construction |

| Renovation |

| Conventional On-Site |

| Modern Methods of Construction (Prefabricated, Modular, etc) |

| Public |

| Private |

| Greater Cairo |

| Alexandria |

| Giza |

| Rest of Egypt |

| By Type | Apartment & Condominiums |

| Villas and Landed Houses | |

| By Construction Type | New Construction |

| Renovation | |

| By Construction Method | Conventional On-Site |

| Modern Methods of Construction (Prefabricated, Modular, etc) | |

| By Investment Source | Public |

| Private | |

| By Region (Egypt) | Greater Cairo |

| Alexandria | |

| Giza | |

| Rest of Egypt |

Key Questions Answered in the Report

How big is the Egypt residential construction market in 2026?

It is valued at USD 20.32 billion and is projected to reach USD 29.96 billion by 2031 at an 8.09% CAGR.

Which region leads the Egypt residential construction market?

Greater Cairo holds 40.55% share, driven by the New Administrative Capital and existing infrastructure links.

What segment is growing fastest?

Villas and landed houses record the highest 8.67% CAGR as coastal megaprojects attract premium buyers.

How is the government supporting affordable housing?

It has committed EGP 100 billion to build 600,000 social-housing units and offers 3% mortgage interest on 30-year terms.

What role do modern methods of construction play?

Prefabricated and modular techniques grow at 8.92% CAGR, cutting waste by 48% and labor costs by 78% in pilot projects.

How exposed is the sector to currency risk?

Input costs rise when the pound weakens, yet local steel capacity and tariff adjustments partly offset the impact on project viability.

Page last updated on: