Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

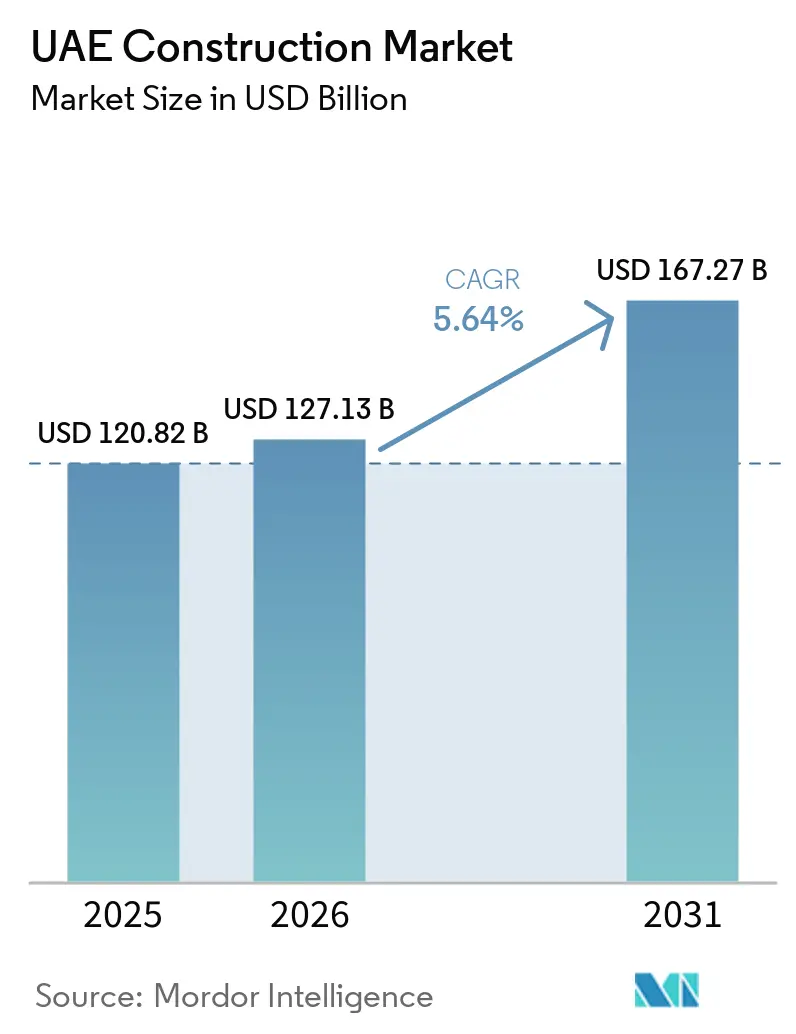

| Base Year Market Size (2025) | USD 120.82 Billion |

| Market Size (2026) | USD 127.13 Billion |

| Market Size (2031) | USD 167.27 Billion |

| Growth Rate (2026 - 2031) | 5.64% CAGR |

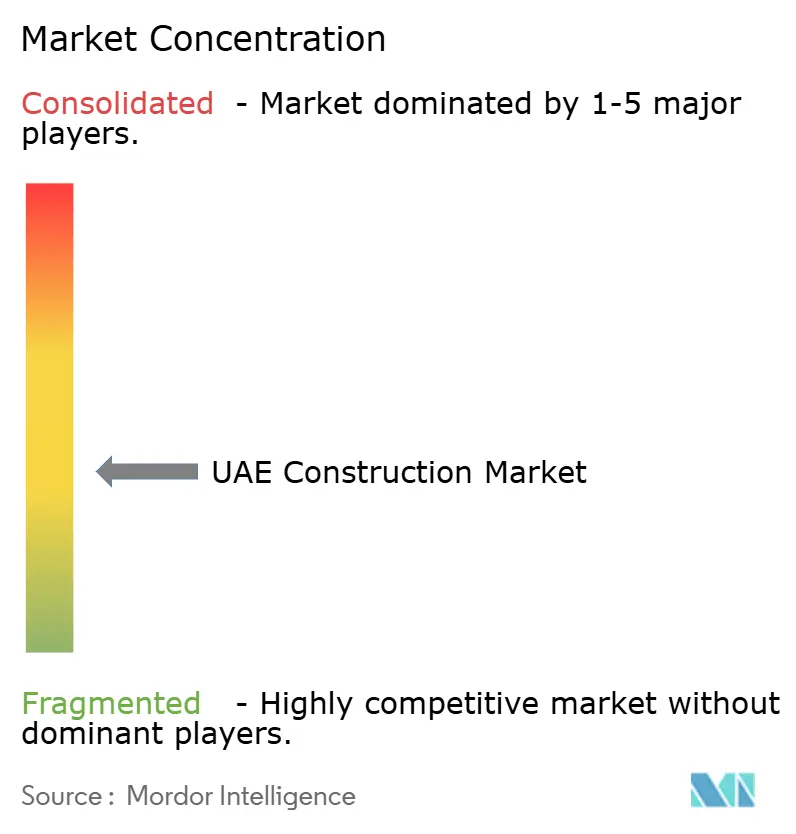

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Construction Market Analysis by Mordor Intelligence

The UAE Construction Market size is projected to be USD 120.82 billion in 2025, USD 127.13 billion in 2026, and reach USD 167.27 billion by 2031, growing at a CAGR of 5.64% from 2026 to 2031.

Robust public investments under Vision 2031, the Dubai 2040 Urban Master Plan, and Abu Dhabi Economic Vision 2030 are extending a predictable opportunity pipeline that shields contractors from cyclical downturns. Private developers continue to bankroll premium residential and hospitality assets, yet federal and emirate budgets are rising faster, reallocating capital toward transportation, energy transition, and water security projects. Tourism-linked buildings, logistics warehouses, and hyperscale data centers add further breadth, ensuring that the UAE construction market remains firmly on a multi-year growth trajectory. At the same time, tightening credit conditions and elevated material costs are prompting a shift to modular methods and integrated supply-chain strategies that protect margins while supporting schedule certainty.

Key Report Takeaways

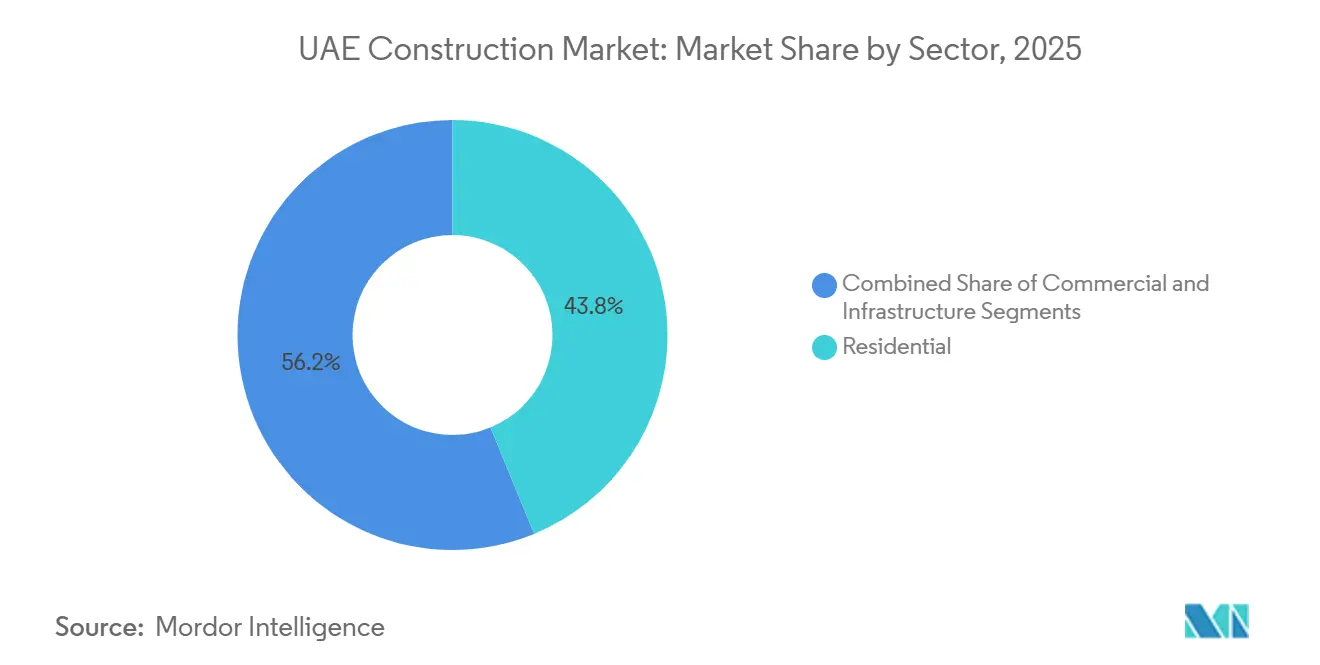

- By sector, residential building captured 43.8% of the UAE construction market share in 2025, whereas infrastructure is forecast to post the fastest 5.23% CAGR through 2031.

- By construction type, new-build activity accounted for 76.9% of the UAE construction market size in 2025; renovation is advancing at a 5.79% CAGR to 2031.

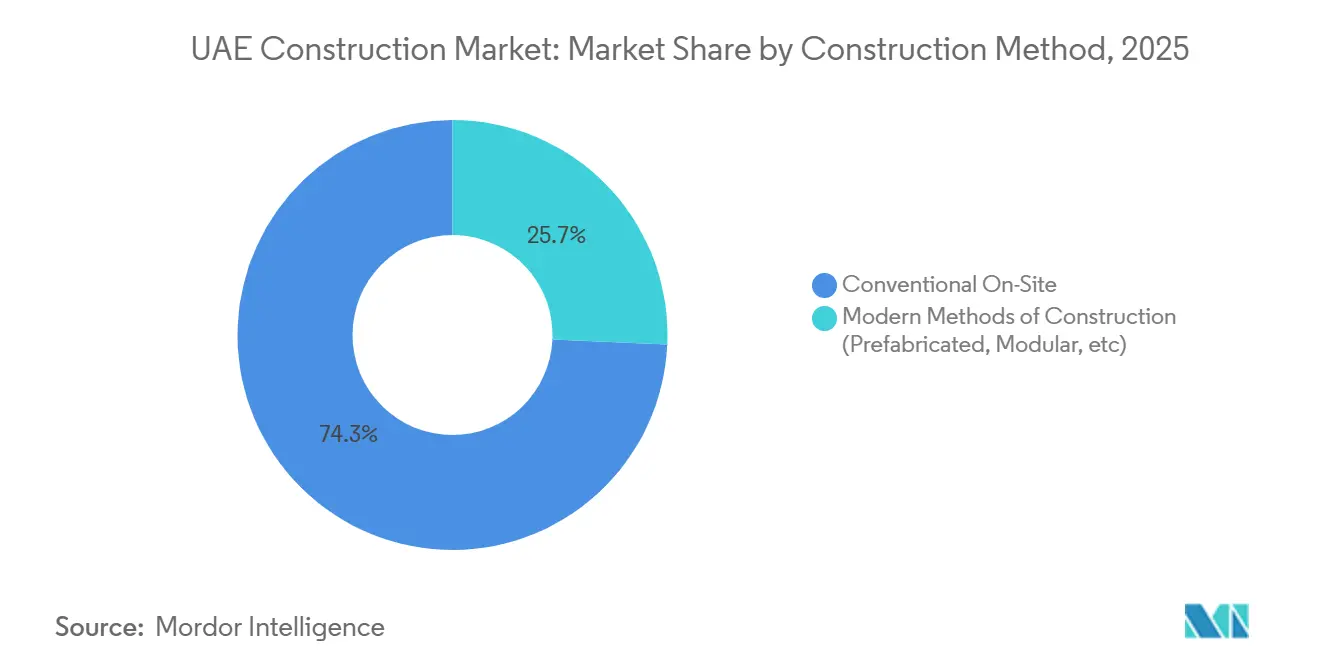

- By construction method, conventional on-site techniques held 74.3% of the 2025 value, while modular approaches are expanding at a 6.54% CAGR.

- By investment source, private outlays formed 65.1% of 2025 spending; public spending is projected to rise at a 5.90% CAGR through 2031.

- By city, Dubai led with 47.2% share in 2025; the group of smaller emirates is recording the quickest 6.71% CAGR out to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

UAE Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2031 and emirate masterplans anchoring multi-year pipelines | +1.2% | National; concentrated in Dubai, Abu Dhabi, Sharjah | Long term (≥ 4 years) |

| Tourism, hospitality, and entertainment capex lifting demand | +1.0% | Dubai core; spill-over to Ras Al Khaimah, Fujairah | Medium term (2–4 years) |

| Housing and community development supported by population and expat inflows | +0.9% | National; early gains in Dubai, Abu Dhabi, Sharjah | Medium term (2–4 years) |

| Logistics, industrial, and data center growth fueling specialized builds | +0.8% | Dubai, Abu Dhabi; emerging zones in Ajman, RAK | Short term (≤ 2 years) |

| Energy and water programs expanding civil and utility works | +0.7% | Abu Dhabi-led, with federal grid projects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vision 2031 and Emirate Masterplans Anchoring Multi-Year Project Pipelines

National and emirate master plans are translating long-range ambitions into funded tenders that stretch through the decade. Dubai 2040 channels new urban clusters along transit corridors, triggering metro extensions and district cooling schemes ahead of vertical work. Abu Dhabi’s USD 65.3 billion infrastructure envelope gives contractors a sequenced slate of roads, housing, and renewable assets that support long-term workforce planning. Sharjah’s logistics corridors redirect building eastward, diversifying risk for firms that once relied on the Dubai-Abu Dhabi axis. Each framework embeds net-zero and circular-economy targets, nudging contractors toward Estidama Pearl and LEED Platinum compliance. The result is a predictable UAE construction market that rewards scale, specialty certifications, and green-build expertise.

Tourism, Hospitality, and Entertainment Capex Lifting Building Demand

Dubai aims to host 40 million overnight visitors by 2031, catalyzing high-profile resorts, theme parks, and mixed-use districts that pack retail, culture, and residences into single footprints. Emaar’s USD 21.8 billion Oasis scheme epitomizes the upmarket trend, demanding premium landscaping and luxury façades. Ras Al Khaimah and Fujairah are positioning themselves as eco-adventure alternatives and awarding hotel packages that entice contractors into less congested geographies. Compressed delivery windows push the adoption of modular interiors and prefabricated MEP racks. Consequently, tourism capex keeps the UAE construction industry flush with diversified demand even as traditional office builds plateau.

Housing and Community Development Supported by Population and Expat Inflows

The national population is projected to top 11.5 million by 2031, feeding a steady appetite for mid-market apartments, build-to-rent precincts, and luxury gated villas[1]Federal Competitiveness and Statistics Centre, “UAE Statistics,” fcsc.gov.ae. Federal housing grants of USD 2.5 billion in 2024 shifted greenfield starts toward Ajman, Umm Al Quwain, and Fujairah[2]Ministry of Energy and Infrastructure, “Home,” moei.gov.ae. Private developers such as Aldar and Emaar are trialing BTR assets that emphasize durable finishes and on-site property tech. High-net-worth buyers still favor smart villas with wellness amenities, raising specification complexity. These parallel trends ensure the residential slice of the UAE construction market remains resilient, though growth tilts from speculative sales to recurring-income models.

Logistics, Industrial, and Data Center Growth Fueling Specialized Builds

Positioned as a global logistics hub, the UAE is adding warehouses, cold-chain depots, and massive data halls requiring precision engineering. DP World alone delivered 500,000 m² of warehousing in 2024 with 12-month schedules. Amazon’s Dubai fulfillment center sets new automation standards, while a USD 545 million du-Microsoft venture and a USD 25 billion ADQ-ECP pledge secure a hyperscale data-center wave. Contractors versed in Tier III/IV specifications and liquid-immersion cooling are in short supply, allowing margin premiums and advancing the UAE construction market toward higher-value technical scopes.

Restraints Impact Analysis*

| Restraints | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Execution capacity constraints and skilled labor shortages | -0.8% | National; acute in Dubai and Abu Dhabi | Short term (≤ 2 years) |

| Cost inflation and higher financing costs compressing feasibility | -0.6% | National; heavier impact on private projects | Medium term (2–4 years) |

| Regulatory and permitting complexity extending schedules | -0.4% | Dubai, Abu Dhabi dense development zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Execution Capacity Constraints and Skilled Labor Shortages Amid Mega-Programs

Roughly 3.1 million construction workers were on UAE sites in 2024, yet overlapping mega-projects now chase the same steel fixers, BIM coordinators, and data-center MEP specialists[3]International Labour Organization, “Labour Migration—United Arab Emirates,” ilo.org. Vocational pipelines lag in complexity, so firms rely on expatriate crews that need months for visa processing. Subcontractor benches are overcommitted, forcing main contractors to self-perform at higher overhead. Competition for niche skills with Saudi and Qatari projects inflates wage bills and risks schedule slippage across the UAE construction market. Training reforms are underway, but will not ease shortages before 2027.

Cost Inflation and Higher Financing Costs Compressing Feasibility

Steel rebar rose 15-20% and cement 10-12% during 2024-2025, eroding fixed-price contract margins. Central-bank rates at 5.4% lifted debt service, shrinking feasibility windows for mid-market condos and speculative offices. IMF watchdogs flag growing non-performing loans as overruns strain developers’ cash flows. Smaller contractors face working-capital shortfalls, triggering exits or mergers and reducing bid competition. These pressures temper growth but also accelerate modular adoption and supply-chain integration across the UAE construction market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Infrastructure Outpacing Residential on Energy Transition

Infrastructure secured the fastest 5.23% CAGR outlook for 2026-2031, overtaking residential, which still held a 43.8% UAE construction market share in 2025. Transportation megaprojects such as Etihad Rail’s inter-emirate corridor and Dubai Metro extensions are absorbing civil budgets, while solar farms, desalination plants, and hydrogen hubs anchor Abu Dhabi’s USD 65.3 billion public envelope. This shift compels traditional tower specialists to add rail, grid-integration, and remote-desert logistics expertise, a capability mix that now influences pre-qualification scoring. Contractors that already house heavy-equipment fleets and Tier-1 MEP teams are winning repeat packages, locking in multi-year revenue even as residential launches decelerate inside mature Dubai districts.

Demand is not evaporating from housing; instead, it is rotating toward build-to-rent, mid-market apartments, and villa communities tied to federal housing aid, preserving baseline volume while margins tighten. Commercial activity also bifurcates, with softer core-office uptake offset by surging warehouse and data-hall fit-outs that follow e-commerce and cloud-computing projects. Energy-and-water infrastructure, meanwhile, benefits from net-zero targets that compel a pipeline of grid reinforcements and utility extensions through 2031. The net result is a broader workload mix, allowing contractors to hedge cyclical apartment cycles with long-duration public infrastructure contracts, strengthening earnings resilience across the UAE construction industry.

By Construction Type: Renovation Accelerating as Sustainability Retrofits Gain Urgency

New-builds captured 76.9% of 2025 activity, yet renovation is expanding at a 5.79% CAGR as aging towers on Sheikh Zayed Road, Deira malls, and early-2000s villas are being retrofitted to comply with rising energy-performance codes. Landlords face occupancy risk if buildings lack smart HVAC, LED lighting, and indoor-air monitoring, so retrofit capex is now embedded in most asset-management budgets. Contractors specializing in selective demolition and night-shift installations command premium fees because jobs require precision around occupied areas and strict noise windows. Parallel demand emerges from adaptive-reuse conversions - obsolete warehouses in Al Quoz transform into co-working lofts, while Mina Zayed fish markets become art galleries - broadening the retrofit niche and rewarding firms able to navigate heritage approvals.

Regulators add momentum by extending Estidama audits to existing stock, creating a compliance countdown for inefficient assets in Abu Dhabi business districts. Financing is increasingly tied to retrofit metrics; banks and green-bond investors price loans off LEED or Estidama ratings, shifting owner economics decisively toward refurbishment. For contractors, renovation pipelines supply shorter, repeatable engagements that smooth cash-flow dips between slower new-build awards. The segment’s rising share also intensifies demand for skilled labor - plumbers, electricians, façade engineers - able to work within confined, live environments, tightening the labor market and pushing daily rates higher across the UAE construction sector.

By Construction Method: Modular Techniques Gaining Traction Amid Labor Scarcity

Conventional site-cast methods still controlled 74.3% of 2025 spend, but modular systems now grow at a 6.54% CAGR, fueled by labor shortages and schedule compression on hospitality, education, and data-center jobs. Dubai’s refreshed 3D-printing roadmap targets 25% modular content by 2030, and early pilots show bathroom pods arriving fully tiled, wired, and plumbed before stacking into shafts, trimming interior fit-out labor nearly in half. Hospitality brands insist on turnkey guest-room modules to guarantee finish uniformity and capture seasonal opening dates, while hyperscale data-hall EPCs pre-fabricate cooling skids under factory QC, sidestepping desert heat tolerances that plague on-site assembly.

Capital investment defines winners; large contractors finance proprietary plants near Jebel Ali or KIZAD, pairing digital design with robotic welding to scale output. Smaller firms unable to fund factories retreat to installation-only roles or pivot to villa renovation niches. Regulators help mainstream off-site manufacturing by issuing fast-track approvals once third-party fire and structural tests are lodged, reducing perceived permitting risk. Still, owners demand detailed lifecycle data to verify modular durability under Gulf climate extremes. As proof points mount, confidence rises, supporting modular penetration beyond early adopters and further diversifying delivery models available within the UAE construction market.

By Investment Source: Public Spending Accelerating to De-Risk Private Participation

Private developers supplied 65.1% of 2025 construction finance, led by premium villa, hospitality, and data-center sponsors, yet public budgets are growing at 5.90% annually as the government pre-builds enabling works that coax private co-investment. Abu Dhabi’s USD 65.3 billion program exemplifies the model by funding roads, utilities, and site grading in industrial zones ahead of developer entry. Housing grants and free-zone utility rebates in Ajman and Fujairah do likewise, allowing mid-market apartment builders to break ground with less execution risk. Contractors accustomed to lump-sum private contracts now cultivate government framework agreements, mastering different payment terms and arbitration venues.

Public-private partnerships gain momentum in rail, desalination, and district cooling, bundling sovereign land with long-term concessions that tap institutional capital. Private capital, for its part, concentrates on high-margin niches where customer depth and brand premiums offset higher interest rates, such as branded residences, ultra-luxury resorts, and hyperscale data centers. Bank syndicates scrutinize developer leverage more closely, favoring projects with public-sector anchors or utility off-take contracts. Contractors capable of flexible procurement—able to satisfy both sovereign tender rules and developer design-build preferences—capture the widest bid slate, cushioning order books against swings in either funding channel across the UAE construction landscape.

Geography Analysis

Dubai’s 47.2% 2025 share underscores its role as the epicenter of mega-projects such as the USD 21.8 billion Oasis and data-center clusters backed by du and Microsoft. The emirate’s Route 2020 metro line is operational, and further extensions aim to connect new mixed-use districts, offering steady MEP and tunneling work. Land scarcity is steering developers toward infill towers, adaptive reuse, and vertical mixed-use schemes, shifting contractor focus from vast greenfields to complex logistics over tight footprints.

Abu Dhabi pivots to energy transition and heavy industry, buoyed by a USD 65.3 billion infrastructure plan that places solar farms, hydrogen hubs, and desalination plants at the center of public tenders. The 2-gigawatt Al Dhafra solar park, now online, demonstrates the emirate’s appetite for remote, utility-scale builds demanding specialist thermal-resilience engineering. Industrial zones clustered near Khalifa Port and Etihad Rail spurs draw logistics and manufacturing investors who seek shovel-ready land with backbone utilities in place, broadening the UAE construction market footprint.

Beyond the two heavyweights, Ajman, Ras Al Khaimah, Fujairah, and Umm Al Quwain are scaling at a combined 6.71% CAGR, backed by housing grants, industrial free zones, and tourism diversification. Ras Al Khaimah’s resort corridor captures spill-over from Dubai’s visitor overflow, awarding hospitality packages fitted to eco-adventure branding. Fujairah and Umm Al Quwain extend port and logistics capacity that filters new warehouse and light-industrial contracts to mid-tier contractors willing to accept leaner margins for geographic spread. Collectively, this diffusion stabilizes national order books and cements a multidimensional UAE construction market landscape.

Competitive Landscape

Competition is moderate, with the top 10 contractors holding roughly 35-40% of spend, leaving a sizable long-tail of mid-tier and niche specialists. Global giants such as Bechtel and Fluor secure complex utility and energy transition projects where deep engineering benches and risk-management track records prove decisive. Regional leaders ALEC, ASGC, Shapoorji Pallonji, and Arabian Construction Company sustain an edge in high-rise residential and hospitality due to agile decision chains and entrenched subcontractor ecosystems. Chinese SOEs, leveraging bundled financing, undercut bids on large public schemes, pressuring incumbents to sharpen value propositions around quality and speed.

Digitization separates front-runners from followers. Leading firms deploy BIM for clash detection, drones for progress tracking, and prefabrication for MEP skids, cutting rework and winning owner confidence on lump-sum contracts. Sustainability mandates now function as gatekeepers; ISO, BIM-Level 2, and Estidama credentials routinely appear in prequalification screens, squeezing under-capitalized contractors from top-tier tenders. Those that pivot quickly to modular factories or green-material sourcing lock in premium workloads and reinforce competitive moats within the UAE construction market.

White-space niches emerge in data center EPC, green-hydrogen facilities, and heritage adaptive reuse, where demand outruns the supply of certified expertise. Smaller firms shielded by local relationships thrive on villa renovations and secondary-emirate projects dismissed as sub-scale by mega-builders. Yet persistent labor shortages and material volatility spur consolidation as weaker players struggle with working-capital swings. Over the medium term, the UAE construction industry is expected to trend toward higher concentration around digital-ready, sustainability-qualified contractors capable of delivering multi-sector portfolios.

UAE Construction Industry Leaders

ALEC Engineering & Contracting LLC

ASGC Construction LLC

China State Construction Eng. Corp. Middle East

Arabian Construction Company (ACC)

Consolidated Contractors Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Emirates Nuclear Energy Corporation signed an MoU with Samsung C&T to explore civil-nuclear projects and modular reactor deployment, broadening specialised infrastructure prospects.

- November 2024: du and Microsoft committed USD 545 million to UAE AI infrastructure, including hyperscale data centers.

- September 2024: Emaar revealed The Oasis, a USD 21.8 billion luxury mixed-use project in Dubai.

- June 2024: The 2-gigawatt Al Dhafra Solar PV plant entered commercial operation.

UAE Construction Market Report Scope

The construction market includes several activities covering upcoming, ongoing, and growing construction projects in different sectors. It has but is not limited to geotechnical (underground structures) and superstructures in residential, commercial, and industrial systems, infrastructure construction (like roads, railways, and airports), and power generation and transmission-related infrastructure.

A complete background analysis of the UAE construction market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends, and COVID-19 impact, is covered in the report.

The UAE construction market is segmented by sector (commercial construction, residential construction, industrial construction, infrastructure (transportation) construction, and energy and utility construction). The report offers market size and forecasts for all the above segments in value (USD).

By Sector

| Residential | Apartments/Condominiums |

| Villas/Landed Houses | |

| Commercial | Office |

| Retail | |

| Industrial and Logistics | |

| Others | |

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) |

| Energy & Utilities | |

| Others |

By Construction Type

| New Construction |

| Renovation |

By Construction Method

| Conventional On-Site |

| Modern Methods of Construction (Prefabricated, Modular, etc) |

By Investment Source

| Public |

| Private |

By City

| Dubai |

| Abu Dhabi |

| Sharjah |

| Other Emirates (Ajman, Ras Al Khaimah, Fujairah, UAQ) |

| By Sector | Residential | Apartments/Condominiums |

| Villas/Landed Houses | ||

| Commercial | Office | |

| Retail | ||

| Industrial and Logistics | ||

| Others | ||

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) | |

| Energy & Utilities | ||

| Others | ||

| By Construction Type | New Construction | |

| Renovation | ||

| By Construction Method | Conventional On-Site | |

| Modern Methods of Construction (Prefabricated, Modular, etc) | ||

| By Investment Source | Public | |

| Private | ||

| By City | Dubai | |

| Abu Dhabi | ||

| Sharjah | ||

| Other Emirates (Ajman, Ras Al Khaimah, Fujairah, UAQ) | ||

Key Questions Answered in the Report

What is the projected value of the UAE construction market by 2031?

The sector is forecast to reach USD 167.27 billion by 2031, expanding at a 5.64% CAGR.

Which segment is expected to grow fastest through 2031?

Infrastructure construction leads with a 5.23% CAGR as public energy and transport projects dominate tenders.

How quickly is modular construction advancing?

Modular and prefabricated techniques are expanding at a 6.54% CAGR, the highest rate among construction methods.

Which emirate is growing fastest?

Collectively, Ajman, Ras Al Khaimah, Fujairah, and Umm Al Quwain are growing at a 6.71% CAGR through 2031.

What is the main restraint facing contractors?

Capacity constraints and skilled-labor shortages are shaving 0.8% off forecast growth in the near term.

How large is the private investment share today?

Private funding accounted for 65.1% of 2025 spending, though public outlays are now rising faster.

Page last updated on: