Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

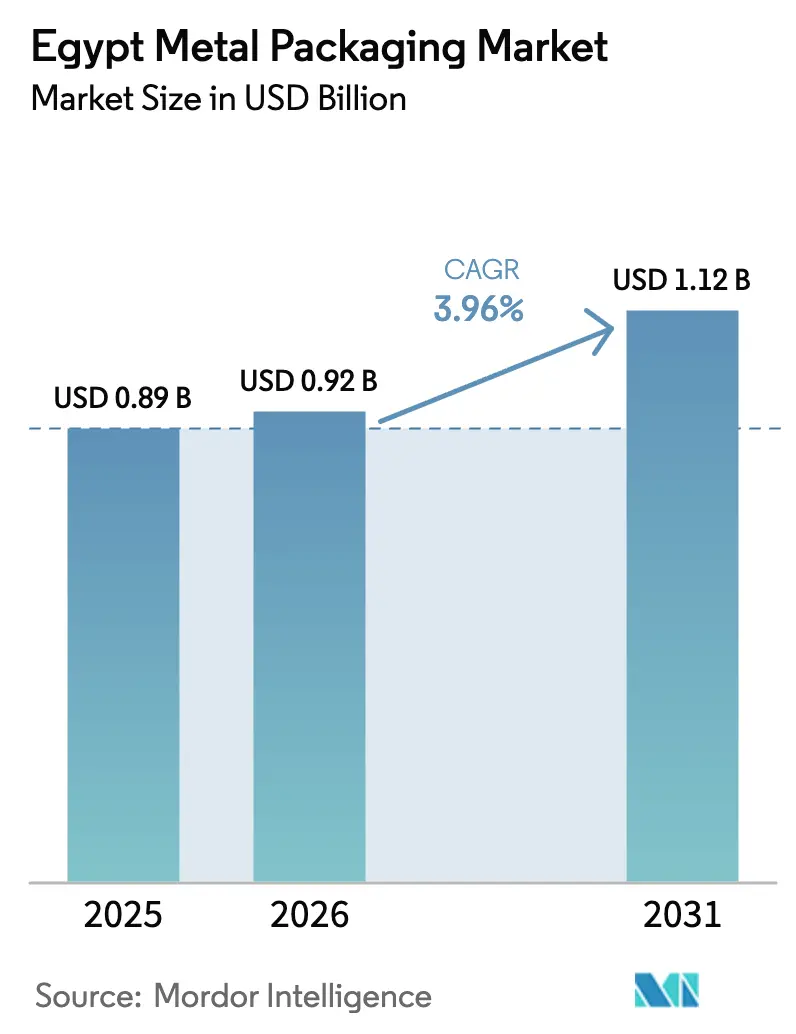

| Base Year Market Size (2025) | USD 0.89 Billion |

| Market Size (2026) | USD 0.92 Billion |

| Market Size (2031) | USD 1.12 Billion |

| Growth Rate (2026 - 2031) | 3.96% CAGR |

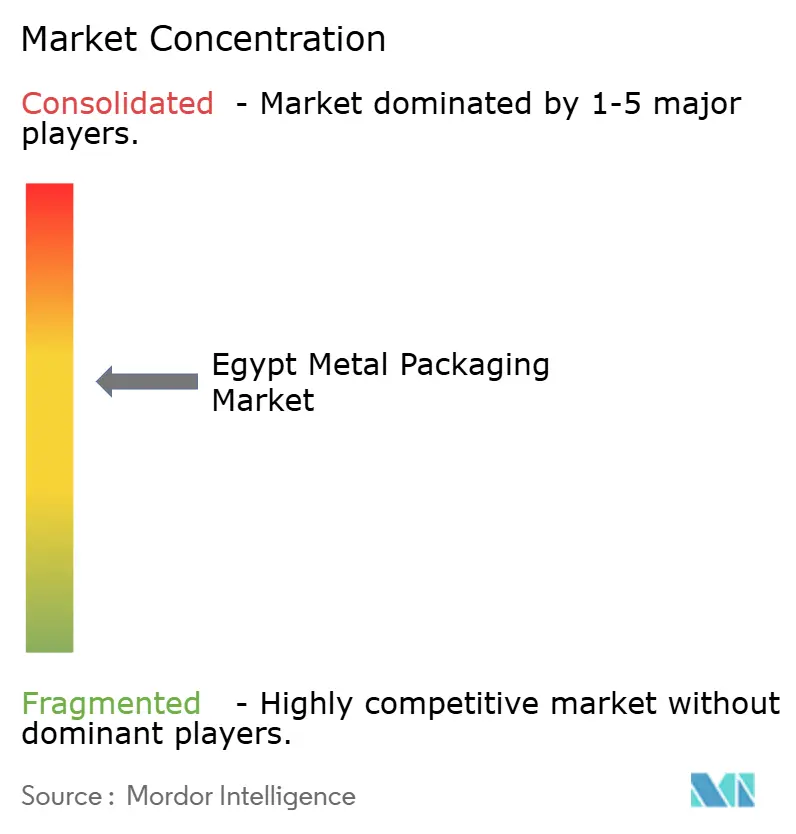

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Metal Packaging Market Analysis by Mordor Intelligence

The Egypt metal packaging market size is projected to expand from USD 0.89 billion in 2025 and USD 0.92 billion in 2026 to USD 1.12 billion by 2031, registering a CAGR of 3.96% between 2026 to 2031. A surge in beverage production, growing agro-processing exports, and new domestic aluminium smelter investments are widening end-user demand while limiting the impact of foreign exchange swings on imported raw materials. Tourism-driven consumption in the HoReCa channel, government incentives under the Golden License regime, and rising adoption of premium QR-coded cans continue to favor the Egypt metal packaging market, even as PET suppliers inject fresh capacity. Domestic recycling pilots, though nascent, are beginning to improve scrap availability. At the same time, volatile London Metal Exchange pricing and the Egyptian pound’s prior depreciation introduce short-term cost variability that converters must manage through hedging and long-term supply contracts with Egyptalum and other regional smelters.

Key Report Takeaways

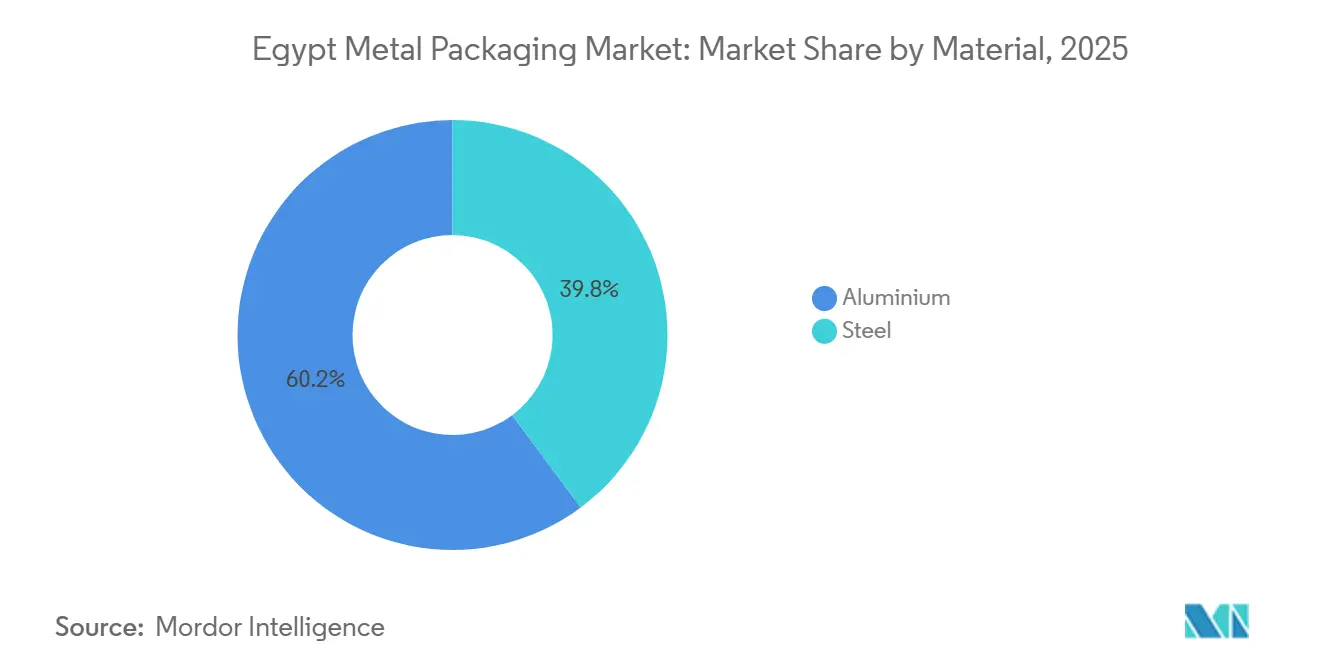

- By material, aluminium led with 60.17% of Egypt metal packaging market share in 2025 while steel is forecast to post a 4.56% CAGR through 2031.

- By product type, cans held 58.17% revenue share in 2025 whereas shipping barrels and drums are projected to expand at a 5.23% CAGR to 2031.

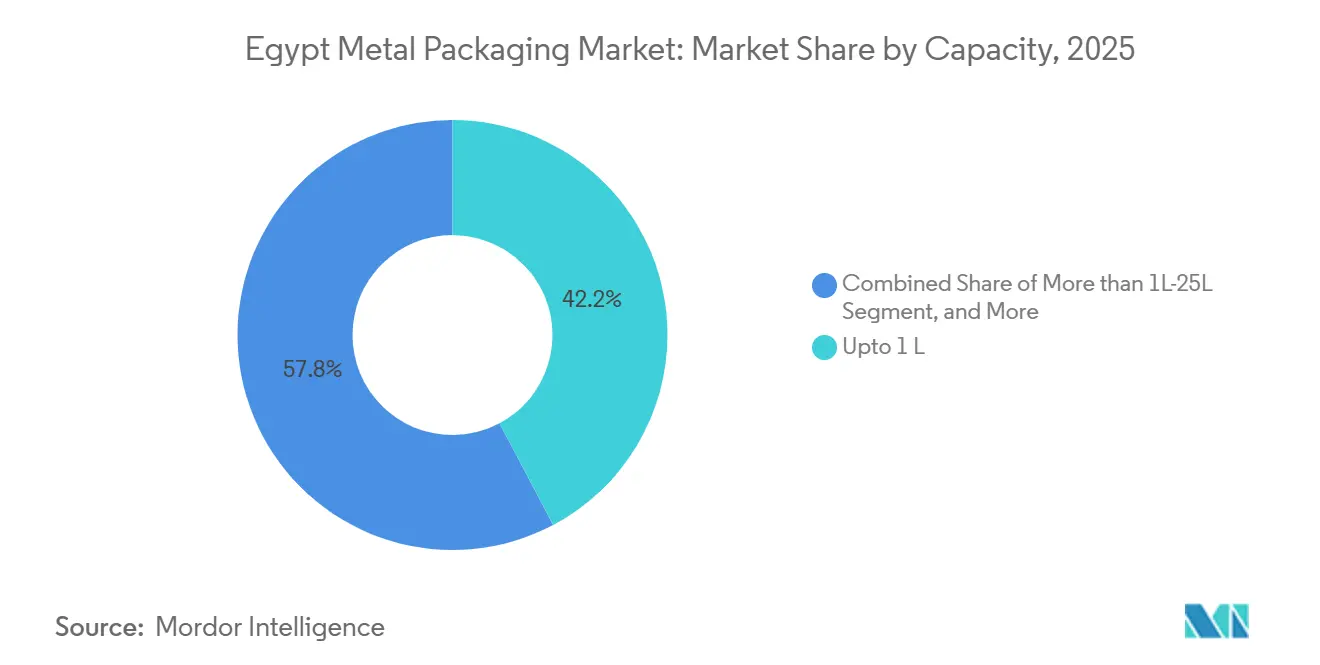

- By capacity, containers up to 1 litre commanded 42.23% share of the Egypt metal packaging market size in 2025 and the >1L-25L segment is set to grow at a 4.78% CAGR during 2026-2031.

- By end-use industry, beverages captured 39.23% share in 2025 while the industrial segment is advancing at a 5.44% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Egypt Metal Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Domestic Aluminium-Smelter Expansion Boosts Local Can-Sheet Supply | +0.8% | National, Alexandria and Nag Hammadi industrial zones | Medium term (2-4 years) |

| Rising Beverages Demand from Tourism and HoReCa Channel | +0.9% | National, early gains in Cairo, Alexandria, Red Sea resorts | Short term (≤ 2 years) |

| EPR and Deposit-Return Pilots Favor Highly Recyclable Metal Containers | +0.6% | National, pilot in Red Sea area | Long term (≥ 4 years) |

| Brand-Owner Shift to Premium, Smart , and QR-Coded Cans | +0.4% | National, led by multinational beverage brands | Medium term (2-4 years) |

| Growth of Agro-Processing Export Cans | +0.5% | Nile Delta and Suez Canal Economic Zone | Medium term (2-4 years) |

| Government Incentives for Import-Substitution Industrialization | +0.5% | Nationwide under Golden License regime | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Domestic Aluminium-Smelter Expansion Boosts Local Can-Sheet Supply

Egyptalum and Aluminium Bahrain signed a USD 3 billion memorandum of understanding in September 2025 to develop an alumina refinery that will feed 1.5 million tonnes of raw material into downstream rolling mills.[1]Egyptalum, “Egyptalum and Alba Sign Alumina Refinery MoU,” Egyptalum, egyptalum.comEgyptalum’s profits rose 160% in the first quarter of fiscal 2024/25 as higher aluminium prices and planned solar power investments lowered energy intensity.[2]Scatec, “Scatec Partners with Egyptalum on Solar Plant,” Scatec, scatec.comGreater local can-sheet availability shortens lead times for converters and reduces hard-currency exposure, helping the Egypt metal packaging market meet just-in-time orders from beverage brands trialing seasonal flavors. The refinery is expected to enable a doubling of domestic can capacity by 2030, create high-skill jobs in Upper Egypt, and reinforce the supply-security narrative that aluminium producers use when competing with PET. Shorter supply chains also permit smaller production runs, which align with the trend of SKU proliferation in the craft soda and energy drink niches.

Rising Beverages Demand from Tourism and HoReCa Channel

Egypt welcomed 15.7 million tourists in 2024, and the tourism sector expanded 13.8% in the first quarter of fiscal 2025/26. Hotels, restaurants, and cafés prefer single-serve aluminium cans that chill quickly and minimize back-of-house waste. Beverage manufacturing jumped 37% in the same quarter, vastly outpacing overall non-oil manufacturing growth of 14.5%. The Red Sea corridor, which hosts roughly 40% of Egypt’s hotel rooms, is widening premium drink menus, including craft sodas packed exclusively in cans to support brand storytelling. This demand feeds directly into the Egypt metal packaging market, sustaining high throughput at Ball and Crown lines while opening capacity-utilization headroom for local converters. Strong regional air connectivity into Hurghada and Sharm el Sheikh also accelerates cold-chain turnover, another variable that favors lightweight cans over glass.

EPR and Deposit-Return Pilots Favor Highly Recyclable Metal Containers

The United Nations Industrial Development Organization and GIZ assisted Egypt in designing an Extended Producer Responsibility framework, which entered the pilot phase in the Red Sea in 2024.[3]UNIDO, “Extended Producer Responsibility Framework for Packaging Waste,” UNIDO, unido.orgIn September 2025, SIG, Plastic Bank, Carta Misr, and TileGreen launched Egypt’s first closed-loop beverage carton system, aiming to recover 700 tonnes of materials within three years. Aluminium cans already contain 74% recycled content globally, a figure Ball plans to raise to 85% by 2030. Egypt’s evolving EPR targets will penalize low-recyclability substrates more sharply than infinitely recyclable metals, which positions the Egypt metal packaging market for incremental volume from sustainability-minded brand owners. Coca-Cola HBC Egypt’s collection of 29,000 tonnes of PET in 2024 signals that beverage multinationals foresee mandatory deposit-return obligations in the near term. Formalizing such schemes will raise the competitive bar for plastics while rewarding converters that can certify recycled content under the Aluminium Stewardship Initiative protocols.

Brand-Owner Shift to Premium, Smart and QR-Coded Cans

Variable-data printing now enables every can to carry a unique QR code, unlocking loyalty programs, provenance checks, and dynamic recycling instructions. Ball’s digital presses support rapid artwork changes with no plate costs, allowing Egyptian beverage marketers to synchronize limited-edition launches with social media campaigns. Egypt’s packaging sector, which includes over 8,000 companies, is ordering more matte lacquer, tactile varnish, and thermochromic ink to elevate shelf presence, especially in the energy-drink segment, where unit prices exceed standard soft drinks by 20-30%. Smart cans also deter counterfeiting, an issue for high-margin imports sold through informal retail in Greater Cairo. As smartphone penetration climbs above 90%, scan-and-win promotions become more effective, tightening the feedback loop between brand owners and consumers and further anchoring the Egypt metal packaging market in high-value applications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Aluminium and Steel Input Prices | -0.5% | Global, pass-through to Egypt via LME-linked contracts | Short term (≤ 2 years) |

| Nascent Organized Scrap-Collection and Recycling Infrastructure | -0.3% | National, informal sector dominance | Long term (≥ 4 years) |

| Intense Competition from Lightweight Flexibles and PET Bottles | -0.4% | National, especially dairy, juice, edible-oil lines | Medium term (2-4 years) |

| Foreign-Exchange Swings Raising Imported Lacquer and Liner Costs | -0.3% | National, converters sourcing from Europe and Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Aluminium and Steel Input Prices

London Metal Exchange contracts have swung 15-20% quarter over quarter in the past two years, compressing margins for converters that lack hedging arrangements. Egypt’s net international reserves stood at USD 48.7 billion in November 2025, yet external debt reached USD 161.2 billion, limiting fiscal room for industrial subsidies. Greif reported thinner drum margins in fiscal Q4 2024 after customers resisted cost-pass-through clauses. When aluminium prices spike alongside a weakening pound, converters serving export clients face a double hit because output is invoiced in USD while inputs are denominated in EGP. Short-term agreements with Egyptalum for billet supply at indexed discounts offer some relief but rarely cover imported lacquers, rivets, or coil coatings sourced in Europe and Asia.

Nascent Organised Scrap-Collection and Recycling Infrastructure

Roughly 60,000-80,000 informal waste pickers retrieve post-consumer material, but a lack of centralized sorting and washing limits the purity of aluminium scrap entering remelters. A USD 20 million PET plant is under construction in the Suez Canal Economic Zone, yet no comparable large-scale aluminium facility has been announced. Domestic smelters therefore rely on imported pre-consumer scrap, adding logistics cost and diluting the circular-economy narrative that metal packagers use to differentiate from PET. Without a nationwide deposit-return system, beverage cans continue to be included in mixed municipal waste streams, increasing contamination and reducing collection economics. Until formal scrap aggregation scales up, recycled-content targets will hinge more on foreign feedstock than on local collection, slowing progress relative to public sustainability commitments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Steel Gains Momentum in Export-Oriented Drums

Aluminium retained 60.17% of Egypt metal packaging market share in 2025 because it anchors beverage cans, aerosols, and premium retort food packs. Steel, however, is set to grow at a 4.56% CAGR through 2031, the fastest rate among materials, thanks to rising demand for conical drums from tomato paste and tuna exporters. Aluminium revenues track beverage output, which jumped 37% in the first quarter of fiscal 2025/26, while steel benefits from Egypt’s agro-processing exports that reached USD 6.1 billion in 2024. The Egypt metal packaging market size for aluminium is expanding steadily, yet steel’s affordability and robustness make it the preferred option for bulk concentrates moving through the Suez Canal corridor.

Domestic smelter projects will lower aluminium sheet import dependence and may temper price volatility, but steel enjoys an established tinplate-coating base that serves chemical and paint customers on short lead times. Greif Egypt leverages ISO-certified plants to supply both standard drums and conical formats to North Africa, reinforcing the material’s cross-border appeal. Tinplate cans manufactured in 10th of Ramadan City reach edible-oil and adhesive lines in Upper Egypt, further diversifying steel’s order book. Consequently, procurement managers balance weight savings and recycling narratives with total delivered cost, ensuring both materials retain strategic relevance within the Egypt metal packaging market.

By Product Type: Cans Dominate, Drums Accelerate

Cans accounted for 58.17% of 2025 revenue, underscoring their central role in carbonated soft drinks, beer, ready-to-drink coffee, and aerosols slated for domestic sale and re-export into the Levant. Shipping barrels and drums, though smaller in base volume, are forecast to advance at a 5.23% CAGR to 2031 as Egypt’s industrial and agro-processing clusters rely on large-format steel containers for bulk logistics. Up-to-70 cl beverage cans underpin plant utilization at Ball and Crown sites near Cairo, but new tomato-paste lines in the Suez Canal Economic Zone are booking three-piece conical drums months ahead of commissioning. The Egypt metal packaging market size tied to drums is therefore rising in tandem with processed-food export contracts secured under duty-free trade schemes with COMESA partners.

CairoPac’s expansion to 1.2 million food cans per day widens fast-rotation SKUs for tuna and legumes stocked by Middle Eastern retailers, while MetalPrint’s aerosol lines benefit from growing household-and-personal-care demand among Egypt’s urban middle class. Supply chain resilience drives some paint makers to dual-source cylinders from EuroPack and Greif, reducing risk of line stoppages. The product-type profile thus mirrors Egypt’s industrial strategy: cans remain the workhorse for beverages, yet drums carve the fastest lane as bulk-export infrastructure scales.

By Capacity: Mid-Range Containers Catch Up

Containers up to 1 litre held 42.23% of Egypt metal packaging market share in 2025, reflecting the dominance of 250-500 ml cans consumed in HoReCa and retail multipacks. The 1L-25L bracket is forecast to grow 4.78% annually, driven by paint, chemical, and edible-oil fillers seeking tamper-evident metal formats that withstand hot-fill and stacking pressures. As tourism rebounds, bar owners in Hurghada are ordering slim 330ml energy-drink cans that chill quickly and free up fridge space. Meanwhile, paint producers in 6th of October City shift to 18 litre pails with child-safe lids, a niche where the Egypt metal packaging market size still shows headroom for import substitution.

Large-capacity ranges exceeding 25 litres are growing in line with lubricant and specialty chemical output, yet they face palletization constraints in land transport to Sub-Saharan Africa. Egypt’s conical designs enable nested stacking, reducing shipping volume, and underpin its franchise in tomato paste exports to Europe. Single-serve formats will remain indispensable to fast-moving beverages, but mid-range packs increasingly attract capital spending as Egypt targets deeper penetration into regional construction and agro-input markets.

By End-Use Industry: Industrial Lines Outpace Beverage Growth

Beverages commanded 39.23% of the share in 2025, buoyed by tourism, rising disposable income, and multi-flavor rollouts among global soda brands. Yet the industrial segment is on track for a 5.44% CAGR through 2031, outstripping all peers due to government incentives for domestic chemical and lubricant plants that mandate local packaging content. The Egypt metal packaging market size booked by beverage fillers continues to climb, largely from energy drinks and ready-to-drink coffee that rely on sleek aluminium cans for brand differentiation. Crown’s ongoing capacity upgrade supports this trajectory and signals sustained confidence from multinational partners.

Export-oriented food processors added 21% value in 2024 and still expand, but now share capacity with paint, adhesive, and specialty chemical players seeking ISO-approved steel drums. Greif Egypt meets this demand by offering conformance to global hazardous goods regulations, which in turn lowers insurance premiums for exporters. Pharmaceutical and cosmetics users, aided by Abdos FMCG’s new plant, are pivoting toward metal aerosols for antiseptic sprays and deodorants to improve their barrier properties. As the industrial supply chain matures, order volumes shift toward larger drums and pails, tilting revenue toward the sector with the fastest forecast CAGR inside the Egypt metal packaging market.

Geography Analysis

Greater Cairo generates nearly 45% of national demand, featuring beverage can filling lines, pharmaceutical production, and a dense HoReCa footprint that consumes single-serve formats daily. Nile Delta governorates contribute roughly 30%, driven by agro-processing plants in Dakahlia and Gharbia that can tomatoes and fruit concentrates in steel conicals for onward shipment through Damietta and Port Said. The Suez Canal Economic Zone emerges as a third anchor where integrated logistics, bonded storage, and export rebates attract packaging investors, including Huhtamaki’s USD 48 million fiberboard project approved in January 2025.

Alexandria and the Red Sea resort corridor collectively account for around 40% of hotel rooms and therefore drive high turnover rates in tourist season. Port Said hosts GCAN’s facility, which targets Levant exports, leveraging its proximity to the canal and straightforward customs procedures. Upper Egypt contributes under 10% today but may rise if Egyptalum’s refinery in Nag Hammadi triggers further downstream investment.

Transport economics shape plant siting. Rail and river barge options along the Nile reduce backhaul costs, encouraging converters to cluster close to beverage or petrochemical fillers. Golden License approvals, which hit 43 by January 2025, are deliberately mapped to diversify industrial capacity beyond the congested Cairo hub, easing pressure on domestic freight rates while enlarging the geographic footprint of the Egypt metal packaging market.

Competitive Landscape

Market concentration is moderate, as two global heavyweights coexist alongside a number of agile local converters. Ball Corporation’s EMEA sales reached USD 1.059 billion in Q3 2025, up 11.5% year-over-year, aided by its recycled content credentials, which secure contracts with multinational beverage brands. Crown operates a two-line plant outside Cairo and continues to debottleneck end lines to handle sleek can diameter shifts demanded by energy drink marketers. Greif Egypt, founded in 1992, leads the supply of steel drums for chemicals and lubricants, capitalizing on its parent company’s quality systems and regional distribution network.

Mid-tier players, such as CairoPac and MetalPrint, differentiate themselves through shorter lead times, lower minimum order quantities, and a willingness to accommodate mixed pallets of diameters for SME food brands. ISO 9001 certifications are commonplace, but only a handful of companies invest in ISO 14001 or PAS 2060 carbon neutrality audits, which large consumer packaged goods firms now require. Digital printing and QR coding are still niche services offered by Ball, although local converters are exploring modular retrofit kits to help existing decorators close that gap.

Competitive intensity is rising as PET suppliers complete fresh lines and court beverage fillers with lightweight bottles. Metal packagers respond by highlighting recyclability, tamper evidence, and cold-chain efficiency. The absence of a mandatory EPR fee gives converters little economic incentive to fund collection infrastructure, yet forward-looking players pilot can-back schemes to lock in contracts ahead of forthcoming regulation. Overall, the Egypt metal packaging market balances multinational capital strength with domestic market agility, sustaining room for specialization in high-margin niches.

Egypt Metal Packaging Industry Leaders

Greif Inc.

Willy Group

Ghandour Brothers Metal Industries(Gcan)

EuroPack

Ball Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Beyti Food Industries inaugurated a EGP 1 billion (USD 32 million) expansion that introduced Egypt’s first UHT milk line in PET bottles, adding five production lines and 650,000 tonnes annual capacity.

- November 2025: The Ministry of Planning, Economic Development and International Cooperation reported 5.3% GDP growth for Q1 2025/26, with beverage production up 37%, chemicals up 44%, and non-oil manufacturing up 14.5%.

- September 2025: Egyptalum and Aluminium Bahrain signed a USD 3 billion agreement to build an alumina refinery projected to supply 1.5 million tonnes annually.

- September 2025: SIG, Plastic Bank, Carta Misr, and TileGreen have launched Egypt’s first closed-loop beverage carton recycling system, targeting 700 tonnes of recovery over the next three years.

Egypt Metal Packaging Market Report Scope

Packaging provides a protective covering for the product, protecting it during handling, storage, and transportation, while also supplying information about the contents of the package to the user. The use of metals, such as steel, tin plate, and aluminum, for packaging is referred to as metal packaging. The study tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. Also, the study includes revenue accrued from the sales of metal products offered by various vendors in the market. Tin cans have been considered under the steel can segment for this study.

The Egypt Metal Packaging Market Report is Segmented by Material (Aluminium, and Steel), Product Type (Cans, Bulk Containers, Shipping Barrels and Drums, Caps and Closures, and Other Product Types), Capacity (Upto 1 L, >1L-25L, >25L-200L, and Above 200L), End-use Industry (Beverage, Food, Paint and Chemical, Industrial, and Other End-use Industries). The Market Forecasts are Provided in Terms of Value (USD).

By Material

| Aluminium |

| Steel |

By Product Type

| Cans | Food Cans |

| Beverage Cans | |

| Aerosol Cans | |

| Bulk Containers | |

| Shipping Barrels and Drums | |

| Caps and Closures | |

| Other Product Types |

By Capacity

| Upto 1 L |

| >1L-25L |

| >25L-200L |

| Above 200L |

By End-use Industry

| Beverage |

| Food |

| Paint and Chemical |

| Industrial |

| Other End-use Industries |

| By Material | Aluminium | |

| Steel | ||

| By Product Type | Cans | Food Cans |

| Beverage Cans | ||

| Aerosol Cans | ||

| Bulk Containers | ||

| Shipping Barrels and Drums | ||

| Caps and Closures | ||

| Other Product Types | ||

| By Capacity | Upto 1 L | |

| >1L-25L | ||

| >25L-200L | ||

| Above 200L | ||

| By End-use Industry | Beverage | |

| Food | ||

| Paint and Chemical | ||

| Industrial | ||

| Other End-use Industries | ||

Key Questions Answered in the Report

What is the current value of the Egypt metal packaging market?

The market was valued at USD 0.92 billion in 2026 and is projected to hit USD 1.12 billion by 2031.

Which material leads demand in Egyptian metal containers?

Aluminium holds 60.17% share, led by beverage cans, although steel is the fastest growing at a 4.56% CAGR.

Why are drums the fastest expanding product type?

Export-oriented tomato paste, chemicals, and lubricants need large-format steel drums, driving a 5.23% CAGR in this category.

How is tourism affecting packaging demand?

Tourism growth of 13.8% in Q1 2025/26 is lifting HoReCa beverage orders, accelerating can consumption in coastal resorts.

Which end-use sector shows the highest growth outlook?

The industrial segment, spanning chemicals and lubricants, is forecast to grow at 5.44% CAGR through 2031.

What role will recycling regulation play in future demand?

Egypt’s evolving Extended Producer Responsibility framework is likely to favor infinitely recyclable aluminium, improving long-term demand for metal containers.

Page last updated on: