Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

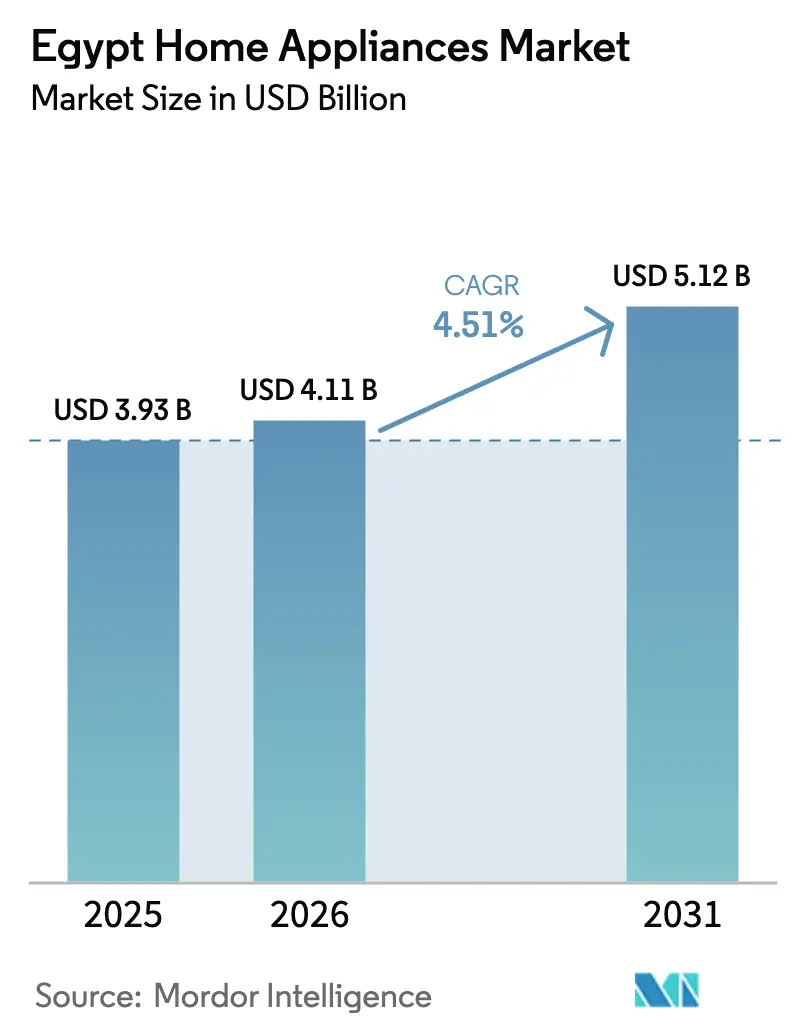

| Base Year Market Size (2025) | USD 3.93 Billion |

| Market Size (2026) | USD 4.11 Billion |

| Market Size (2031) | USD 5.12 Billion |

| Growth Rate (2026 - 2031) | 4.51% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Home Appliances Market Analysis by Mordor Intelligence

Egypt home appliances market size in 2026 is estimated at USD 4.11 billion, growing from 2025 value of USD 3.93 billion with 2031 projections showing USD 5.12 billion, growing at 4.51% CAGR over 2026-2031. Purchase momentum stems from an expanding middle-income cohort moving into satellite cities, mortgage programs that bundle large-ticket goods with new housing, and tighter energy-efficiency rules that guide brand selection. Producers continue to anchor capacity in the 10th of Ramadan and Suez Canal Economic Zones to hedge foreign-exchange swings, secure duty-free inputs, and position for preferential exports, a strategy reinforced by Haier, BSH, and Beko’s combined USD 300 million post-2024 outlays[1]Business Today Staff, “German BSH company to establish €55M stove appliances project in Egypt,” businesstodayegypt.com. Retailers accelerate omnichannel rollouts—flash-sale festivals, zero-interest installments, same-day delivery—to lift online volumes from a low base, while smart-meter deployment and tiered tariffs steer consumers toward high-efficiency models even during sporadic power cuts. Foreign-exchange shortages and gray-market inflows pressure pricing, yet manufacturers that localize production and exceed minimum energy standards are capturing incremental share across the Egypt home appliances market.

Key Report Takeaways

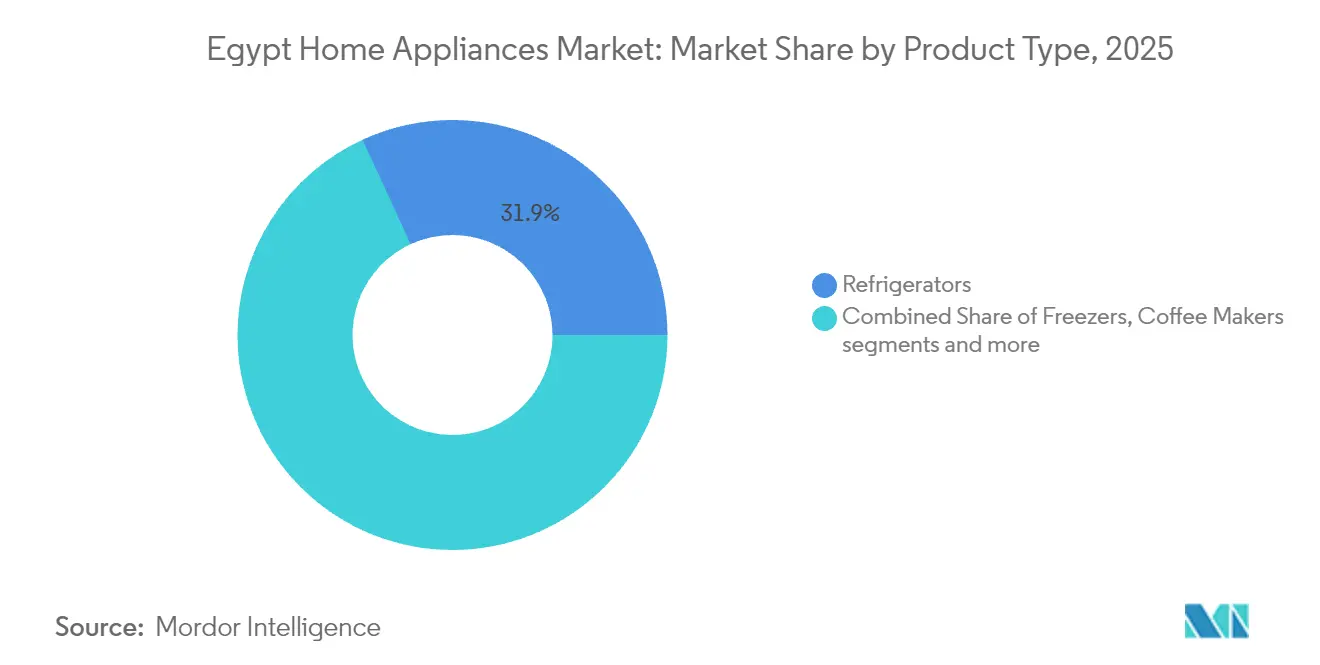

- By product, refrigerators led with 31.87% of Egypt's home appliances market share in 2025, whereas air fryers are advancing at a 5.93% CAGR through 2031.

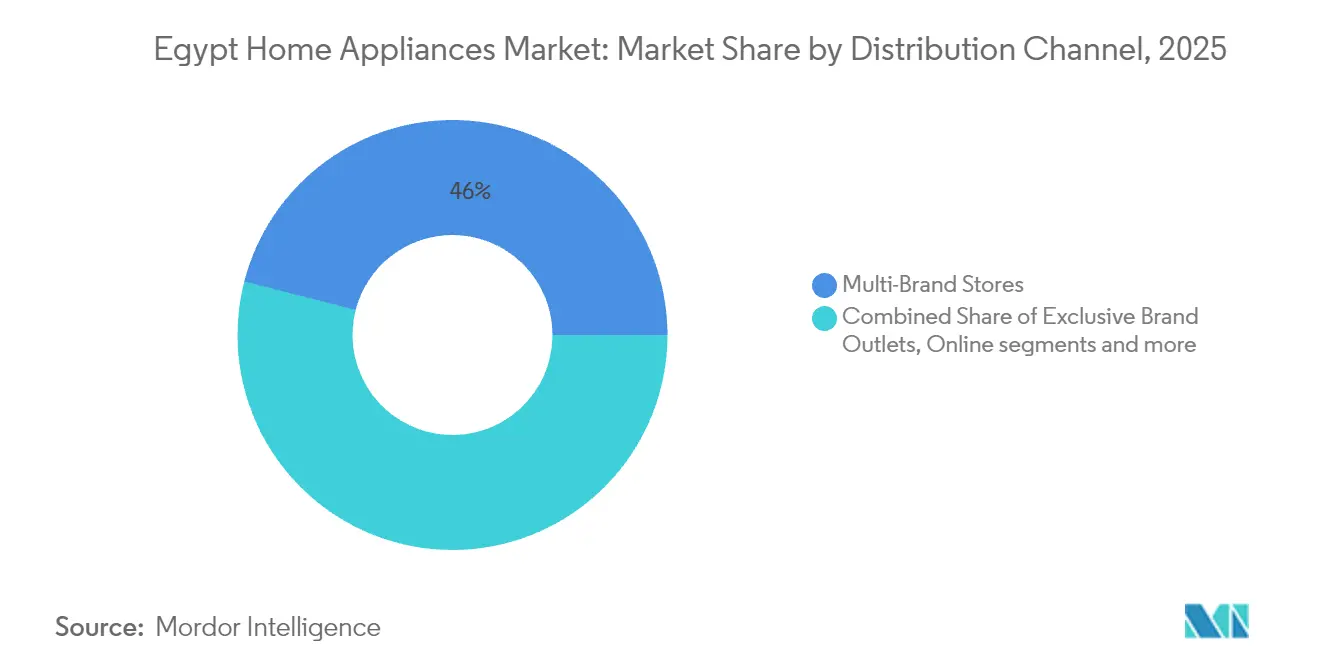

- By distribution channel, multi-brand stores commanded 45.98% of the Egyptian home appliances market size in 2025, while online sales are projected to post a 6.18% CAGR to 2031.

- By geography, Greater Cairo & Giza captured 31.12% of Egypt's home appliances market share in 2025; Canal Cities & Sinai are the fastest-growing regions at 5.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Egypt Home Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Subsidized mortgage + appliance-bundle schemes | +0.8% | Greater Cairo, New Capital, satellite cities | Medium term (2-4 years) |

| Rising middle-income household formation in satellite cities | +0.9% | Greater Cairo periphery, 10th of Ramadan, Badr City | Long term (≥ 4 years) |

| Energy-efficiency labelling tied to tariff incentives | +0.4% | National, early uptake in urban centers | Short term (≤ 2 years) |

| EU rules-of-origin upgrade for exports | +0.7% | Suez Canal Economic Zone, Alexandria | Medium term (2-4 years) |

| E-commerce flash-sale festivals | +0.3% | Greater Cairo, Alexandria | Short term (≤ 2 years) |

| Surge in Chinese OEM contract manufacturing | +0.6% | Ain Sokhna, East Port Said, Canal Cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Subsidized Government Mortgage & Appliance-Bundle Schemes

Egypt’s Social Housing and Mortgage Finance Fund, spearheaded by the Central Bank of Egypt, offers subsidized mortgage programs. These programs feature low interest rates ranging from 3% to 8% and extended repayment periods, empowering hundreds of thousands of low- and middle-income families to achieve home ownership. This surge in home ownership spurs first-time purchases of essential home appliances as these new homes are being furnished. The Central Bank of Egypt's initiative has delivered over 1 million housing units, benefiting approximately 3 million citizens from low- and middle-income backgrounds by 2025. This expansive residential growth has led to a notable uptick in demand for home appliances. Each newly occupied unit has catalyzed purchases of essential items like cookers, refrigerators, and washing machines, particularly boosting sales in the entry to mid-range segments. Consequently, the completion of these housing units has emerged as a pivotal demand driver, fueling the robust growth of Egypt’s home appliance market[2]State Information Service, “Egypt’s Affordable Housing Finance Model,” afi-global.org/.

Rising Middle-Income Household Formation in Satellite Cities

Satellite cities such as the New Administrative Capital, 10th of Ramadan, and Badr City attract middle-class families seeking affordable mortgages and shorter commutes. Demand intensity is evident in the 571,799 applicants for the “Housing for All Egyptians 5” round, dominated by Cairo and Giza residents. Smaller floor plans favor compact appliances; air fryers, mini-ovens, and slim washers outperform national averages, reinforcing a structural shift within the Egyptian home appliances market. Rail and expressway links enable next-day deliveries, and retailers like Elaraby Group bundle zero-interest installments to entice shoppers switching from informal channels. Lifestyle upgrades elevate brand consciousness, boosting premium-segment penetration in refrigerators and air conditioners.

Energy-Efficiency Labelling Compliance Tied to Tariff Incentives

Egypt mandated minimum energy-performance standards for refrigerators, air conditioners, washing machines, and water heaters in 2014 and tightened them in 2022. Residential tariffs climb from 48 to 145 piastres per kWh, turning electricity savings into an immediate consumer payoff[3]Egyptian Electricity Transmission Company, “Residential Tariff 2023-24,” egyptera.org. Pilot procurement programs for high-efficiency split units in public buildings flag institutional appetite for upper-tier labels, and a nationwide smart-meter rollout covering 38 million homes will enable time-of-use pricing. Brands that exceed mandatory thresholds command price premiums yet still offer lifecycle savings, differentiating themselves within the Egyptian home appliances industry. The emphasis on efficient compressors and insulation materials is pushing local suppliers to improve component quality.

Egypt-EU Rules-of-Origin Upgrade Spurs Export-Oriented Local Production

The Suez Canal Economic Zone offers duty-free capital-equipment imports and expedited customs, encouraging global players to reposition Egypt as an export hub for the Middle East, Africa, and Southern Europe. BSH’s EUR 55 million stove plant earmarks half of output for regional exports, and Haier’s USD 135 million Park targets 60–70% local content to meet origin requirements. These moves cut landed costs by up to 8% versus Asian shipments, strengthen supplier ecosystems, and broaden technology transfer. Friend-shoring reports note 34% of Egyptian executives realigning supply chains toward the zone, reinforcing industrial clustering around the Egyptian home appliances market and deepening backward linkages into plastics, compressors, and PCB assemblies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic foreign exchange shortages and tight L/C issuance | –1.2% | National | Short term (≤ 2 years) |

| Recurrent power-grid load-shedding | –0.7% | Upper Egypt, industrial corridors | Medium term (2-4 years) |

| High customs on finished units versus CKD kits | –0.5% | National | Medium term (2-4 years) |

| Gray-market inflows of subsidized GCC appliances | –0.4% | Border cities, informal urban trade hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Chronic FX Shortages Tightening L/C Issuance for Importers

Since 2022, the Central Bank’s letter-of-credit mandate has throttled dollar access for finished-goods importers, extending shipping lead times by up to eight weeks and inflating retail prices by 7–13%[4]Al-Ahram Weekly, “Tightening up on Imports,” ahram.org.eg. Local assemblers, exempt from some restrictions on parts imports, secure a 5–7% cost advantage, nudging distributors to pivot toward domestically produced brands. Inventory gaps periodically surface in premium categories, but installment plans cushion volume declines, preserving baseline demand within the Egyptian home appliances market.

Recurrent Power-Grid Load-Shedding Undermines Appliance Confidence

Prolonged load-shedding of up to 10 hours daily in Upper Egypt has significantly impacted the demand for energy-intensive home appliances, such as split air conditioners. Consumers are increasingly prioritizing cost-efficiency and reliability, opting for products like inverter compressors and battery-compatible mini fridges to mitigate generator expenses and voltage fluctuation risks. This shift in consumer behavior reflects a growing preference for energy-efficient and adaptable solutions. The planned addition of renewable energy capacity and the decommissioning of 5 GW of inefficient gas plants are expected to alleviate energy challenges after 2026. However, the current energy supply uncertainty continues to constrain short-term growth in the Egyptian home appliances market. These dynamics underscore the need for manufacturers to align product offerings with evolving consumer preferences and energy infrastructure developments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Refrigeration Dominance with Counter-Top Upswing

Refrigerators contributed 31.87% to the total revenue in 2025, emphasizing their critical role in households. Haier's initiative to produce 500,000 units annually reflects efforts to expand local manufacturing capacity, which is expected to strengthen domestic supply and enhance export market share. Air fryers, registering a 5.93% CAGR, are gaining traction due to increasing demand for healthier cooking options and space-saving appliances, particularly among satellite-city residents. Washing machines continue to benefit from strong replacement cycles, while air conditioners are experiencing a policy-driven transition toward high-SEER models, aligning with energy-efficient cooling standards.

Midea's TEDA plant demonstrates scalability, with an annual production capacity of 500,000 air fryers, utilizing 70% locally sourced components. Revisions to energy labels are driving mid-tier brands to integrate advanced features such as smart sensors and eco modes, narrowing the gap with multinational competitors. The Egyptian home appliances market for refrigeration is projected to surpass USD 1.78 billion by 2031, supported by demand from first-time buyers in Canal Cities and replacement purchases in Greater Cairo. These trends underscore the growing importance of energy efficiency, local manufacturing, and feature innovation in shaping the competitive landscape of the home appliances market in Egypt.

By Distribution Channel: Store Networks Retain Clout Amid Digital Acceleration

Multi-brand retailers, including B.TECH, Carrefour, and Raya, account for 45.98% of the appliance market value in Egypt, leveraging over 500 touchpoints nationwide. These retailers differentiate themselves through live product demonstrations, immediate order fulfillment, and access to branded service centers, which enhance customer satisfaction. Exclusive brand outlets, such as Samsung and LG, are increasingly focusing on experiential retail formats to attract premium consumers. Traditional corner shops remain integral to the market, catering to price-sensitive rural demographics and sustaining a cash-driven segment. This segment continues to play a critical role in the overall market dynamics, particularly in underserved regions. Although online channels currently represent less than 2% of the market share, they are growing at a compound annual growth rate (CAGR) of 6.18%, supported by improvements in logistics infrastructure and fintech solutions.

Same-day delivery services now cover 60% of Greater Cairo's ZIP codes, while click-and-collect hubs are emerging in petrol-station convenience stores, enhancing last-mile accessibility. By 2031, the online segment is projected to achieve a turnover of USD 372 million, driven by advancements such as mobile-optimized websites, live-chat customer support, and AI-powered product recommendation systems. These technologies are particularly effective in creating tailored product bundles for mortgage recipients, further boosting online sales potential.

Geography Analysis

Greater Cairo & Giza hold 31.12% of Egypt's home appliances market share, underpinned by dense population, higher disposable income, and a critical mass of hypermarkets and service centers. Flagship showrooms in Heliopolis and 5th Settlement showcase smart refrigerators and inverter air conditioners, while e-commerce penetration outpaces provinces thanks to mature courier networks. Satellite-city migration slightly dilutes the absolute share but deepens the aftermarket demand for compact appliances.

Alexandria & North Coast sustain stable growth as tourism spikes increase seasonal turnover in split ACs and mini freezers. The Ras El Hekma megaproject targets 2 million residents and integrates a 10 million m² industrial zone, creating medium-term uplift in durable-goods consumption. Cross-docking facilities at Borg El Arab cut lead times for coastal retailers, supporting quick replenishment ahead of summer peaks.

Canal Cities & Sinai chart the fastest 5.56% CAGR through 2031 due to concentrated manufacturing employment and housing projects linked to the Suez Canal Economic Zone. Haier, Hisense, and Kax hire thousands of skilled workers, boosting disposable income and premium-product adoption. Proximity to ports slashes inland freight, allowing vendors to price competitively. Smart grid pilots in the zone promise more reliable voltage, encouraging take-up of intelligent dishwashers and high-efficiency dryers. The Egyptian home appliances market thus sees balanced geographic diversification even as the capital retains volume leadership.

Competitive Landscape

The Egyptian home appliances market blends dominant local groups with fast-scaling multinationals. Elaraby Group operates 36 factories and markets 16 global brands through 3,000 distributors and 500 service centers, commanding a strong presence in refrigerators, TVs, and ACs. Unionaire’s EGP 6 billion mega-plant boosts annual freezer and cooker output beyond 2 million units, fortifying domestic supply in price-sensitive tiers. Global entrants localize aggressively: Haier will triple production within five years; BSH’s new stove line splits output evenly between the domestic market and MEA exports; Beko’s USD 110 million complex is now the region’s largest single appliance facility.

Strategic imperatives include higher energy-rating thresholds, inverter technology, and Wi-Fi diagnostic modules that appeal to urban millennials. Marketing pivots toward influencer-led TikTok videos and Instagram live streams timed with flash sales, while store networks invest in AR kiosks that visualize appliances in customer kitchens. Local assemblers leverage speed: model refresh cycles average nine months versus 18 for imported lines, enabling rapid response to shifting consumer tastes. Competition is intensifying around smart-grid-ready refrigerators and washer-dryer combos, segments viewed as the next battleground within the Egypt home appliances market.

Additionally, the market is witnessing a growing emphasis on sustainability and energy efficiency, driven by government regulations and consumer demand. Manufacturers are increasingly adopting eco-friendly materials and production processes to align with these trends. The integration of advanced technologies, such as IoT-enabled appliances, is further reshaping the competitive landscape. These innovations not only enhance functionality but also cater to the evolving preferences of tech-savvy consumers. As the market continues to evolve, companies are focusing on strategic partnerships and investments to strengthen their foothold and expand their product portfolios.

Egypt Home Appliances Industry Leaders

LG Electronics

Samsung

Fresh Electric

Electrolux (Olympic Group)

Beko (Arçelik)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Kax announced a USD 50 million investment to build a 40,000 m² component and assembly facility in the Suez Canal Economic Zone. The plant will manufacture metal racks, electronic boards, and plastic parts, strengthening backward integration for Chinese and Egyptian assemblers and creating 600 direct jobs.

- April 2025: The Suez Canal Economic Zone laid foundation stones for two Chinese-backed industrial projects worth USD 58 million, including the Kaks Investment plant. Officials highlighted the projects’ role in deepening local supply chains and boosting annual appliance output capacity by 750,000 units.

- February 2025: China’s Xinfeng signed to develop a USD 1.65 billion multi-industry complex covering 3.75 million m² in Ain Sokhna. Planned lines include refrigerators, vacuum cleaners, and compressors aimed at exporting 60% of output to Gulf markets, reinforcing Egypt’s export-hub status.

- January 2025: BSH secured a “Golden License” that streamlines permitting for its stove-appliance venture, enabling accelerated construction and access to subsidized training programs for 1,000 technicians.

Egypt Home Appliances Market Report Scope

Home appliances are devices used by households for day-to-day activities of cooking, cleaning, and performing other household activities. Technology and product innovations are leading to the designing of household appliances that are capable of performing tasks more efficiently.

Egypt's home appliances market is segmented by product and by distribution channel. By product, the market is segmented into major appliances of freezers, dishwashing machines, washing machines, ovens, air conditioners, and other major appliances and small appliances of coffee/tea makers, food processors, grills and roasters, vacuum cleaners, and other small appliances. By distribution channel, the market is segmented into multi-branded stores, exclusive brand outlets, online, and other distribution channels.

The report also covers the market sizes and forecasts for the Egyptian home appliance market in value (USD) for all the above segments.

By Product

| Major Home Appliances | Refrigerators |

| Freezers | |

| Washing Machines | |

| Dishwashers | |

| Ovens (Incl. Combi & Microwave) | |

| Air Conditioners | |

| Toasters | |

| Countertop Ovens | |

| Other Major Home Appliances | |

| Small Home Appliances | Coffee Makers |

| Food Processors | |

| Grills & Roasters | |

| Electric Kettles | |

| Juicers & Blenders | |

| Air Fryers | |

| Vacuum Cleaners | |

| Electric Rice Cookers | |

| Toasters | |

| Countertop Ovens | |

| Other Small Home Appliances |

By Distribution Channel

| Multi-Brand Stores |

| Exclusive Brand Outlets |

| Online |

| Other Distribution Channels |

By Geography

| Greater Cairo & Giza |

| Alexandria & North Coast |

| Nile Delta Provinces |

| Upper Egypt |

| Canal Cities & Sinai |

| By Product | Major Home Appliances | Refrigerators |

| Freezers | ||

| Washing Machines | ||

| Dishwashers | ||

| Ovens (Incl. Combi & Microwave) | ||

| Air Conditioners | ||

| Toasters | ||

| Countertop Ovens | ||

| Other Major Home Appliances | ||

| Small Home Appliances | Coffee Makers | |

| Food Processors | ||

| Grills & Roasters | ||

| Electric Kettles | ||

| Juicers & Blenders | ||

| Air Fryers | ||

| Vacuum Cleaners | ||

| Electric Rice Cookers | ||

| Toasters | ||

| Countertop Ovens | ||

| Other Small Home Appliances | ||

| By Distribution Channel | Multi-Brand Stores | |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| By Geography | Greater Cairo & Giza | |

| Alexandria & North Coast | ||

| Nile Delta Provinces | ||

| Upper Egypt | ||

| Canal Cities & Sinai | ||

Key Questions Answered in the Report

What is the current value of Egypt’s home appliances sector?

The sector is valued at USD 4.11 billion in 2026 and is projected to reach USD 5.12 billion by 2031, growing at a 4.51% CAGR.

Which product category leads sales nationwide?

Refrigerators held the largest 31.87% revenue share in 2025, reflecting their essential status in Egyptian households.

Why are Canal Cities & Sinai the fastest-growing region for appliance demand?

Industrial expansion in the Suez Canal Economic Zone is creating jobs and housing, driving a 5.56% CAGR for appliances through 2031.

How are energy-efficiency rules influencing buying decisions?

Tightened minimum energy-performance standards and tiered electricity tariffs make efficient models cheaper to run, prompting consumers to favor inverter compressors and high-SEER units.

What role do online channels play in appliance distribution?

E-commerce currently accounts for under 2% of sales but is expanding at a 6.18% CAGR, helped by flash-sale events, mobile payments and same-day delivery in urban centers.

How are foreign-exchange constraints affecting the market?

Tight letter-of-credit requirements restrict finished-goods imports, raising prices and pushing retailers to source more appliances from local assemblers.

Page last updated on: