Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.45 Billion |

| Market Size (2026) | USD 2.68 Billion |

| Market Size (2031) | USD 4.55 Billion |

| Growth Rate (2026 - 2031) | 9.25% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oman Private K-12 Education Market Analysis by Mordor Intelligence

The Oman Private K-12 Education Market size is expected to grow from USD 2.45 billion in 2025 to USD 2.68 billion in 2026 and is forecast to reach USD 4.55 billion by 2031 at 9.25% CAGR over 2026-2031.

Enrollment momentum is sustained by a 10-year Golden Residency pathway that draws high‑net‑worth expatriate families who seek premium British and IB pathways for their children. Vision 2040’s pro‑investment policies and a school infrastructure PPP pipeline shorten time to market for serious operators, which supports both capacity expansion and service quality upgrades. Digital transformation spending at the Ministry of Education is enabling blended learning models that expand access beyond tier‑one operators. Compliance requirements for Omanisation and tuition‑approval protocols are raising operating discipline and pushing mid‑tier providers to scale networks rather than rely on price increases.

Key Report Takeaways

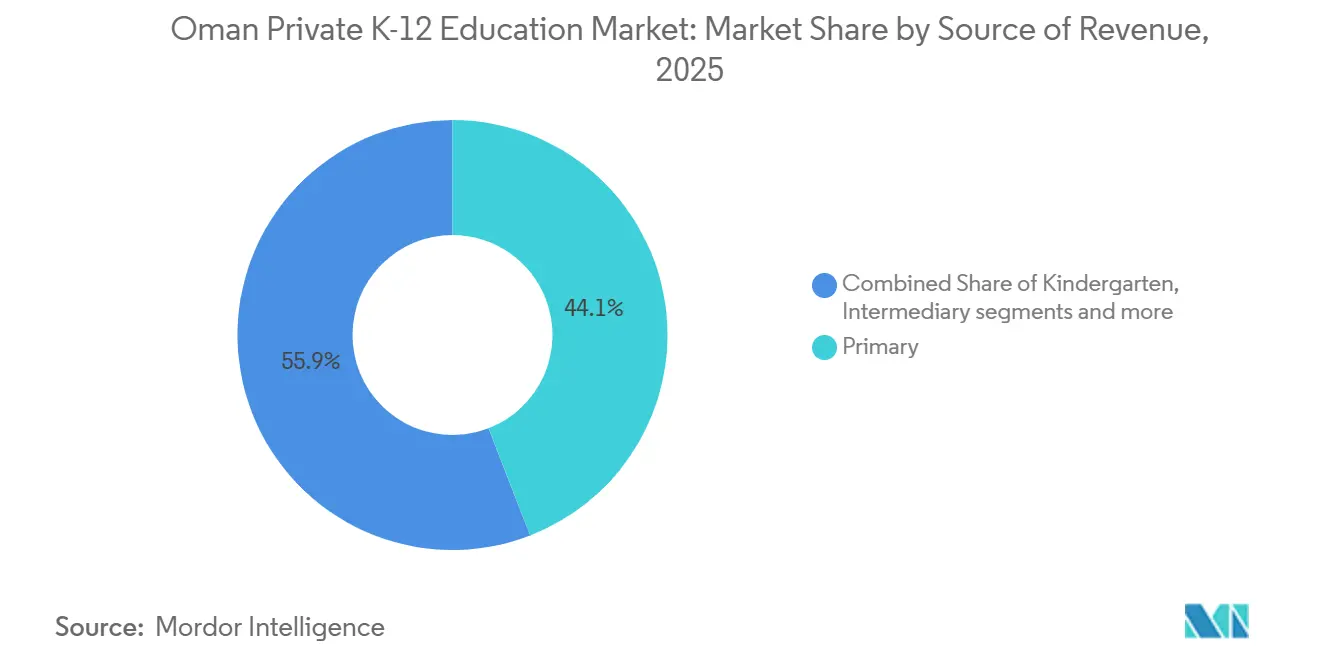

- By source of revenue, primary grades led with 44.12% of the Oman Private K-12 Education market size in 2025 and are forecast to post the highest growth at 9.85% CAGR through 2031.

- By curriculum, British pathways held 65.42% of the Oman Private K-12 Education market size in 2025 and are projected to expand at a 10.21% CAGR through 2031.

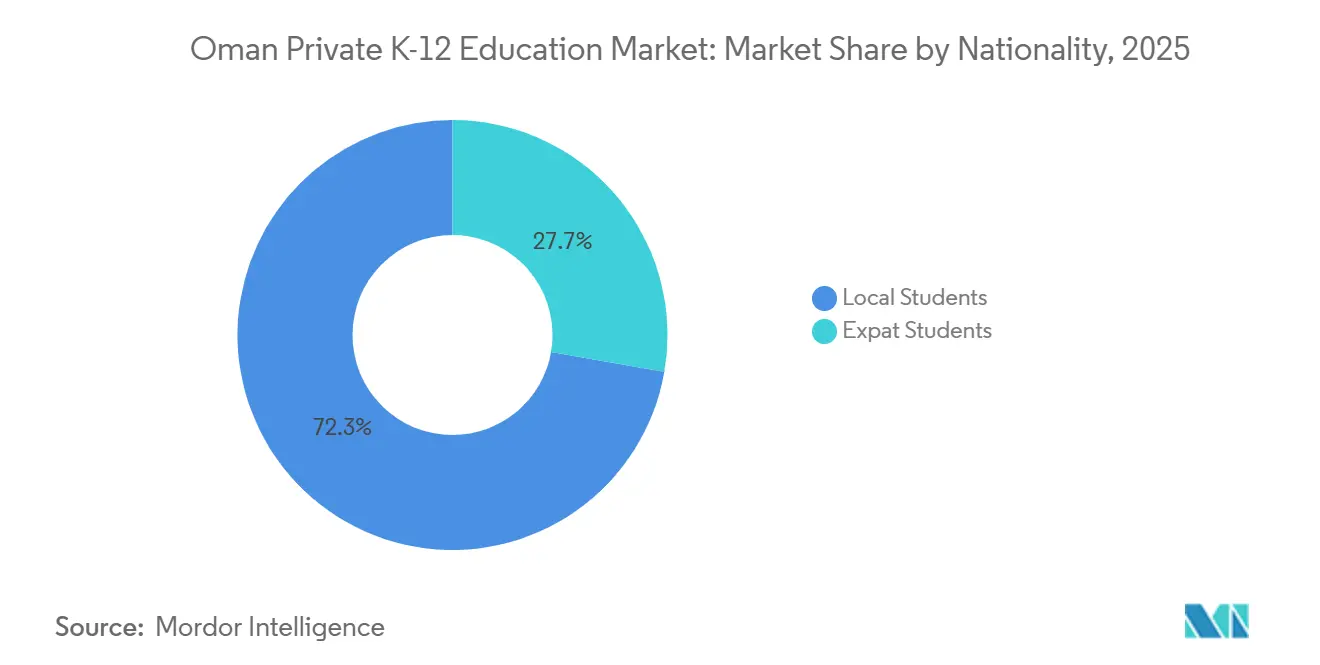

- By nationality, Omani students accounted for 72.25% of the Oman Private K-12 Education market size in 2025, while expatriate enrollments recorded the highest projected growth at 10.53% CAGR to 2031.

- By geography, Muscat held 36.25% of the Oman Private K-12 Education market size in 2025, and Dhofar is the fastest‑growing governorate at an 11.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Oman Private K-12 Education Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising expatriate population & Omani demand for international curricula | 2.8% | Global, with concentrated gains in Muscat, Al Batinah North, and Dhofar governorates | Medium term (2-4 years) |

| Vision 2040 incentives (100% FDI, PPP, land grants) | 1.9% | National, with early gains in Muscat, North Al Batinah, and Duqm SEZ | Long term (≥ 4 years) |

| 42-school PPP pipeline accelerating capacity build-out | 1.2% | Muscat, North Al Batinah, Dhofar | Medium term (2-4 years) |

| Golden-Residency visas expanding the premium-school segment | 0.9% | Global, with spill-over to Muscat, Salalah | Medium term (2-4 years) |

| Omanisation-driven teacher up-skilling lifts perceived quality | 0.5% | National, with early gains in Muscat, North Al Batinah | Medium term (2-4 years) |

| MOE digital-transformation & AI funding enabling blended learning | 0.8% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Expatriate Population & Omani Demand for International Curricula

Oman’s expatriate population has been rising in step with job creation in non‑oil sectors, which sustains demand for English‑medium instruction and globally recognized qualifications. The World Bank reported steady non‑oil expansion in 2024, a trend that kept professional migration flows healthy and underpinned private K12 enrollments into 2026. This shift is accretive to the Oman Private K12 Education market because expatriate families tend to prioritize curricula that offer A‑levels, IB, or AP credentials recognized by universities worldwide. At the same time, more Omani families are choosing international pathways, which aligns with higher‑education equivalency requirements and the preferences of scholarship committees. These dynamics enlarge the pool of students in premium British and IB programs as well as in high‑performing CBSE networks. The combined effect strengthens enrollment depth across Muscat and fast‑growing nodes in Dhofar and North Al Batinah[1]World Bank Staff, “Macro Poverty Outlook, Oman 2025,” World Bank, worldbank.org .

Vision 2040 Incentives

Vision 2040 execution continues to support the Oman Private K12 Education market by permitting 100% foreign ownership in education and channeling projects through PPP concessions. The Ministry of Finance has kept a pipeline of school infrastructure PPPs that contract private partners for non‑instructional services under multi‑year availability‑based models. Land grant and usufruct policies reduce site‑acquisition costs for operators willing to develop campuses in underserved wilayats, which helps spread investment beyond Muscat. These features compress go‑to‑market timelines for international operators that can deploy proven curricula and quality systems. As these facilities come online, parents in secondary cities gain options that previously required long commutes or relocation. The policy mix improves both capacity and service standards in the Oman Private K12 Education market[2]Ministry of Education Oman, “Digital Transformation and AI Initiatives 2025,” Ministry of Education Oman, moe.gov.om..

42‑School PPP Pipeline Accelerating Capacity Build‑Out

The Ministry of Finance advanced a multi‑school PPP package that assigns construction, facilities management, and related services to private concessionaires for the public system. By shifting non‑teaching functions to operators under long‑term contracts, the government can focus on staffing and curriculum delivery while ensuring modern infrastructure standards. The PPPs target high‑density corridors such as Muscat, North Al Batinah, and Dhofar, which are also priority catchment areas for private providers. For private schools, these projects validate enrollment density and de‑risk capital planning in neighborhoods where parents already search for international curricula. Availability‑based payments stabilize contractor cash flows, which may serve as a reference for future co‑location or hybrid models with private K12 brands. The approach increases the overall supply of quality seats and complements private capacity in the Oman Private K12 Education market.

Golden‑Residency Visas Expanding the Premium Segment

The 10‑year Golden Residency program launched on August 31, 2025, with a minimum investment of OMR 200,000, equal to USD 520,000 at the prevailing peg, and it extends education and health access to first‑degree family members. This step addresses the uncertainty of shorter work visas and encourages families to settle and enroll children for full program cycles, including IGCSE and IB Diploma years. Premium British and IB schools in Muscat reported heightened inquiries for the 2025/26 intake in line with this policy change. Fee disclosures indicate that top‑tier schools charge USD 11,024 to USD 26,728, which is consistent with the income profiles targeted by Golden Residency holders. As these families relocate, providers also see demand for tutoring, counseling, and enrichment, which broadens revenue streams beyond tuition. The program therefore expands both enrollment volume and ancillary services in the Oman Private K12 Education market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tuition affordability gap vs median household income | -1.4% | Global, with acute pressure in Muscat's middle-income suburbs and Dhofar | Short term (≤ 2 years) |

| Tuition-fee caps & lengthy MOE approvals | -0.8% | National | Medium term (2-4 years) |

| STEM-teacher shortages from Omanisation quotas | -0.5% | National, with concentrated impact in Muscat, North Al Batinah | Medium term (2-4 years) |

| VAT compliance on ancillary revenue streams | -0.3% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tuition Affordability Gap Vs Median Household Income

GDP per capita readings can obscure variability in household budgets, and many middle-income families face constraints when annual fees exceed their affordability threshold. Median disposable income for Omani households is around USD 3,120, which illustrates how even mid‑tier schools can be a stretch without subsidies. The Ministry of Education has scholarship mechanisms for Omani students in private schools, but caps tied to public‑school per‑pupil outlays limit eligibility to lower‑fee institutions. Expatriate families without corporate sponsorship also encounter budget limits, particularly where schools rely on ancillary charges for transport, activities, and examinations. Fee schedules at large network schools such as Indian School Muscat, which range from USD 1,940 to USD 2,189, show the tension between accessible pricing and the cost of upgrading laboratories and digital content. This affordability pinch is most visible in urban corridors where demand is strong, but headroom for price increases is narrow.

Tuition‑Fee Caps and Approval Timelines

Tuition adjustments require Ministry of Education approval under the School Education Law, and schools must substantiate requests with audited spending and investment plans. The approvals process has formal timelines that reduce pricing flexibility during sudden cost shocks such as wage adjustments or technology upgrades. Premium operators can supplement revenue with boarding services, examination fees, and facility rentals, but smaller schools lack similar levers. Operators that communicate early with parents and regulators on planned upgrades achieve smoother approvals but still face calendar‑driven constraints. The compliance rhythm encourages multi‑year capital planning and pushes operators to pursue scale economies. Over the medium term, fee‑cap governance keeps the Oman Private K12 Education market focused on value and outcomes rather than price alone.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source of Revenue: Primary Grades Drive Enrollment Velocity

Primary grades held the largest share at 44.12% in 2025 and are forecast to grow at a 9.85% CAGR through 2031, which sets the pace for the Oman Private K12 Education market. The expansion of early‑years pathways, including the three‑year Balvatika program across Indian Schools, is pushing demand for classrooms, teachers, and materials beginning in April 2025. Network initiatives to embed financial literacy and AI modules from Class 5 also increase parental preference for early entry into private systems that emphasize foundational skills. Kindergarten and middle grades are sustained by urban demand in Muscat and North Al Batinah, where capacity additions trail enrollment needs. Secondary grades generate higher per‑pupil fees due to international examination costs, but their volume lifts more slowly as students track into vocational and technical pathways. This configuration aligns revenue growth with early‑stage enrollment momentum through 2031.

The Oman Private K12 Education industry is adapting staffing and curriculum planning to support the primary cohort’s larger share of total enrollment. Teacher licensing initiatives tighten supply, which results in higher wages in early years and primary stages where demand is strongest. Schools that scale homerooms and specialist blocks while maintaining quality ratios can spread fixed costs across larger cohorts. The Oman Private K12 Education market benefits when networks coordinate procurement and professional development across campuses. Investment in learning resources and classroom technology at this stage supports attainment later in middle and secondary years. These choices help protect value for families in fee‑sensitive segments.

By Curriculum: British Pathways Dominate, CBSE Scales Rapidly

British‑curriculum providers accounted for 65.42% of the market in 2025 and are projected to expand at a 10.21% CAGR through 2031, reinforcing their lead in the Oman Private K12 Education market. Brand‑name partnerships and consistent GCSE and A‑level outcomes attract Omani and expatriate families who value UK university articulation. CBSE networks are scaling in line with the Indian expatriate presence and curriculum upgrades that add applied skills from upper primary onward. American‑curriculum schools remain niche but have invested in STEM facilities to sharpen their appeal to North American and GCC families seeking SAT and AP pathways. Arabic‑curriculum bilingual schools serve Omani families that desire English proficiency without premium fees, while niche offerings such as French programs cover embassy and multinational cohorts. The mix supports choice across fee bands and academic preferences.

The Oman Private K12 Education industry is seeing accreditation become a baseline requirement across curricula. External quality assurance under the National System for School Performance Evaluation is standardizing reporting and tightening expectations for teaching, assessment, and student growth. Schools invest in staff development aligned with Cambridge, IB, and CBSE frameworks to maintain consistency across grade bands. As admission and equivalency processes formalize, families consider data on student outcomes rather than relying on brand familiarity alone. This transparency supports fair comparisons across curricula and encourages continuous improvement. The net result is broader access to consistent quality for families across governorates.

By Nationality: Omani Enrollments Lead, Expat Growth Outpaces

Omani nationals formed 72.25% of private enrollments in 2025, while expatriate enrollments show the fastest growth outlook to 2031. The Oman Private K12 Education market reflects widespread demand among Omani families for bilingual or international programs that strengthen university options. Expatriate inflows heighten demand for British, IB, and CBSE seats in urban centers and logistics hubs. Indian community density sustains CBSE networks, which plan capacity upgrades and feasibility studies in new catchments. Premium British and American schools attract corporate‑sponsored families and Golden Residency holders who are positioned for multi‑year placements. The mix ensures healthy utilization at both premium and mid‑tier price points.

Data governance now matters to cross‑border student mobility and admissions flows. Oman’s Personal Data Protection Law requires explicit consent and safeguards for handling student records, which is central to families transferring between systems and countries. Private schools are aligning parent communications and consent forms with the law to preserve trust. Quality initiatives and teacher‑training programs also elevate the appeal of Omani‑staffed schools to both national and expatriate families. As capacity expands in Dhofar and North Al Batinah, more expatriates can enroll their children closer to workplaces without relocating to Muscat. These elements reinforce a broad‑based growth pattern in the Oman Private K12 Education market.

Geography Analysis

Muscat held 36.25% of 2025 enrollments, while Dhofar is the fastest‑growing governorate at an 11.01% CAGR through 2031, which redistributes momentum in the Oman private K12 education market. North Al Batinah reports a high count of private schools and continued underserved needs in special education and international curricula. Duqm’s special economic zone shows rising student numbers alongside industrial investment and workforce growth. Private providers evaluating new campuses are balancing land and staffing costs with proximity to industrial clusters. Salalah’s development as a logistics and tourism hub is lifting demand for international curricula in Dhofar. These shifts encourage greenfield builds and expansions outside of Muscat.

As transport infrastructure improves, catchments extend to neighborhoods that previously fell outside practical commute times. The public‑school bus PPP that replaces about 5,000 vehicles between 2024 and 2028 also sets safety and service benchmarks relevant to private school transport providers. Investment forums and licensing improvements raise investor familiarity with zoning and approvals in North Al Batinah and other governorates. Schools that create bilingual and international options in secondary cities can address affordability while preserving academic quality. Network operators use shared services to anchor quality standards as they deploy across multiple sites. This approach is improving resilience and reach in the Oman private K12 education market.

Competitive Landscape

The Oman Private K12 Education market is moderately fragmented, with the top five to seven operators accounting for an estimated 40% to 45% of total enrollments in 2025. Premium British and IB brands in Muscat maintain strong reputation advantages, but accreditation and evaluation reforms are making comparative performance data more visible to families. Network operators scale shared services in HR, procurement, and teacher training to lift consistency and control unit costs. Mid‑tier bilingual providers invest in early‑years facilities and enrichment, competing on value rather than price alone. Special‑education programs remain limited in number, which leaves a gap for capable providers to fill. The system‑wide evaluation framework increases transparency and raises the bar for leadership, teaching, and student outcomes[4]Oman Authority for Academic Accreditation and Quality Assurance of Education, “Performance Evaluation Framework for Schools,” OAAAQA, oaaaqa.gov.om..

Strategic moves by leading schools demonstrate focus on STEM capacity, inclusion, and transparent AI use. The American International School of Muscat opened a new high‑school science and computer‑science wing in 2025 and implemented AI usage protocols for faculty and students in alignment with UNESCO guidance. The Board of Directors of Indian Schools Oman laid out a 2025‑2027 agenda that includes campus upgrades and feasibility work for new locations to meet rising demand in suburban catchments. British curriculum brands promoted student results from the 2024 examination session, reinforcing their positioning with data and expanding inquiry pipelines for the 2025/26 intake. These actions align with parent priorities for laboratory resources, inclusion services, and responsible technology integration. This mix of capacity, curriculum, and governance initiatives supports steady share gains for well‑executed operators in the Oman Private K12 Education market.

Pricing governance and Omanisation shape cost structures and influence competitive strategy. Tuition‑approval workflows favor multi‑year planning and transparency with parents about investment priorities. Localization rules encourage investment in Omani staff capability so schools can maintain service levels across IT, safety, and operations without disruption. Schools that internalize these constraints and leverage digital platforms for blended learning can protect margins while enhancing perceived value. Fee disclosures from premium providers confirm that costs at the high end of the market remain elevated, which segments the offering landscape by willingness to pay. The result is a clear stratification into premium, mid‑tier bilingual, and value segments, with network effects helping mid‑tier brands achieve stability in the Oman Private K12 Education market.

Oman Private K-12 Education Industry Leaders

British School Muscat

Indian School Muscat

American International School of Muscat

A’Soud Global School

Knowledge Gate International School

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: The Ministry of Finance announced plans to advance 20 PPP and Offset projects in 2026, including the Public School Buses Management, Operation and Improvement Project that will deliver around 5,000 modern buses with safety and monitoring systems in phases between 2024 and 2028.

- September 2025: The Ministry of Commerce, Industry and Investment Promotion launched the Golden Residency program effective Aug 31, 2025, offering 10-year renewable visas at a reduced OMR 200,000 threshold with education and healthcare access for first-degree family members.

- November 2025: The Board of Directors of Indian Schools Oman announced a 2025–2027 Strategic Agenda that includes major infrastructure projects at Indian School Muscat, Indian School Darsait, Indian School Seeb, Indian School Sur, and Indian School Salalah, plus feasibility studies for new campuses in Barka and Sinaw.

- May 2025: Indian Schools Oman introduced Financial Literacy and Artificial Intelligence for students from Class 5 onward, with the Financial Literacy rollout starting the week of May 10, 2025 and AI deployment scheduled after the summer break.

Oman Private K-12 Education Market Report Scope

A comprehensive background analysis of the Oman Private K12 Education market, covering the current market trends, restraints, investment analysis and detailed information on various segments and competitive landscape of the education industry.

By Source of Revenue

| Kindergarten |

| Primary |

| Intermediary |

| Secondary |

By Curriculum

| American |

| British |

| Arabic |

| CBSE / Indian |

| Other Curriculum |

By Nationality

| Expat Students |

| Local Students |

By Geography

| Muscat |

| Al Batinah North |

| Dhofar |

| Other Governorates |

| By Source of Revenue | Kindergarten |

| Primary | |

| Intermediary | |

| Secondary | |

| By Curriculum | American |

| British | |

| Arabic | |

| CBSE / Indian | |

| Other Curriculum | |

| By Nationality | Expat Students |

| Local Students | |

| By Geography | Muscat |

| Al Batinah North | |

| Dhofar | |

| Other Governorates |

Key Questions Answered in the Report

What is the current size and growth outlook of the Oman Private K12 Education market?

The Oman Private K12 Education market size was USD 2.68 billion in 2026 and is forecast to reach USD 4.55 billion by 2031 at a 2026-2031 CAGR of 9.25%.

Which curriculum segment leads in Oman’s private K-12 space?

British curriculum providers led with a 65.42% share in 2025 and are projected to grow at a 10.21% CAGR through 2031, supported by exam outcomes and university articulation.

Which region is growing fastest for private K-12 in Oman?

Dhofar is the fastest-growing governorate, forecast at an 11.01% CAGR through 2031, while Muscat remained the largest by share in 2025.

How is policy shaping the Oman Private K12 Education market?

Vision 2040 incentives, a 42-school PPP pipeline, and digital transformation funding by the Ministry of Education are accelerating capacity and modernizing delivery.

How do tuition approvals and affordability affect operators?

Ministry tuition approval processes and fee caps moderate price changes, while median income levels push mid-tier schools to compete on value and scale rather than price.

Page last updated on: