Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

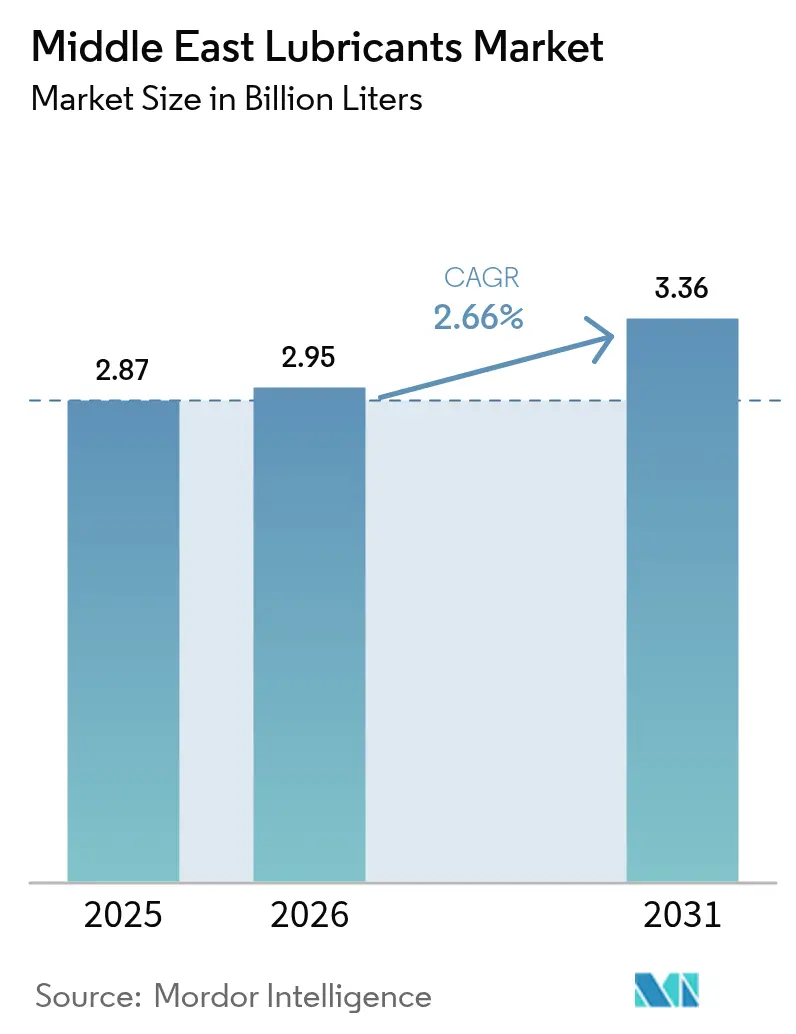

| Base Year Market Size (2025) | 2.87 Billion liters |

| Market Volume (2026) | 2.95 Billion liters |

| Market Volume (2031) | 3.36 Billion liters |

| Growth Rate (2026 - 2031) | 2.66% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Lubricants Market Analysis by Mordor Intelligence

The Middle East Lubricants Market size was valued at 2.87 billion liters in 2025 and estimated to grow from 2.95 billion liters in 2026 to reach 3.36 billion liters by 2031, at a CAGR of 2.66% during the forecast period (2026-2031). This measured trajectory illustrates how diversified industrial programs such as Saudi Vision 2030, Operation 300bn in the United Arab Emirates (UAE), and New Kuwait 2035 are enlarging the demand base while the region’s legacy hydrocarbon infrastructure delivers feedstock and processing advantages. Extended build-outs in petrochemicals, power generation, and logistics corridors continue to elevate lubricant volumes even as longer drain intervals temper unit consumption. Suppliers that localize blending and packaging under 70% iktva content rules enjoy price and lead-time advantages over import-reliant rivals, and this encourages capacity additions in Yanbu, Jebel Ali, and Sohar. Product mix is also shifting: transmission and hydraulic fluids, metalworking oils, and specialty turbine lubricants are outpacing engine oils as the Gulf’s construction machinery fleet grows, renewable energy plants ramp up, and gas turbines replace aging oil-fired power units. Competitive intensity remains moderate; international majors retain technical leadership and certification breadth, yet regional producers that secure halal formulations and API approvals are narrowing the gap.

Key Report Takeaways

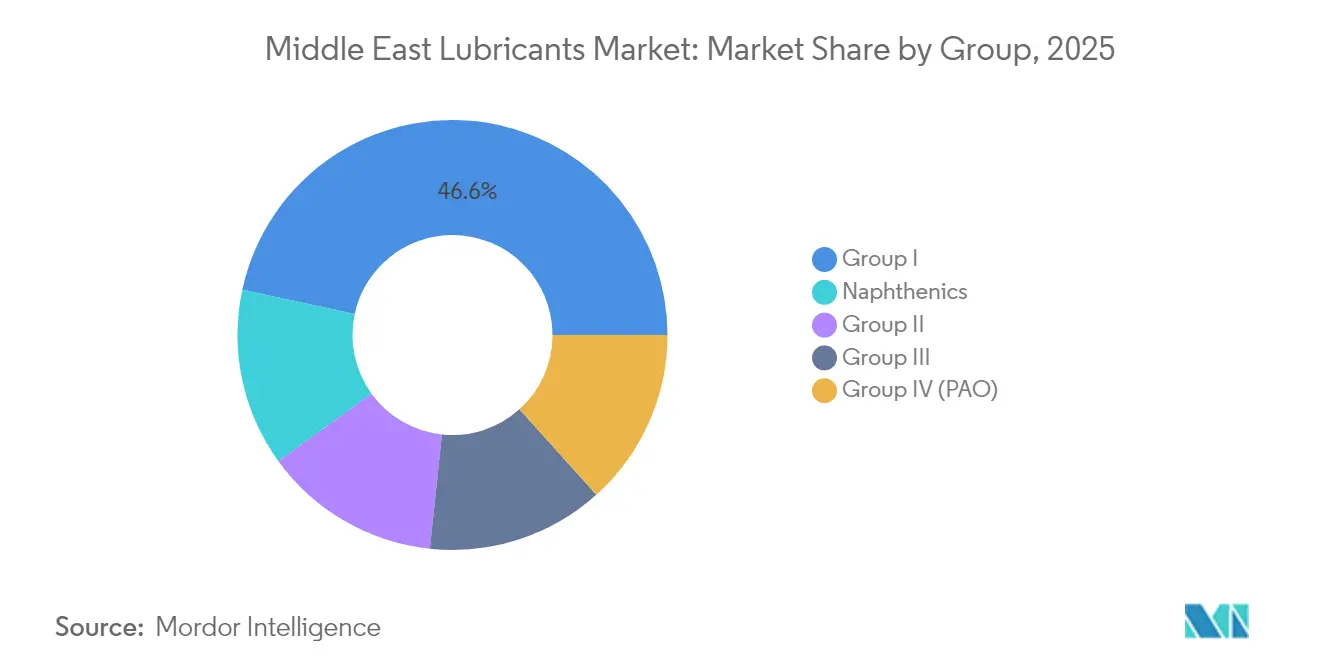

- By Group, Group I captured 46.62% of the Middle East lubricants market share in 2025; Group III is projected to expand at a 2.97% CAGR through 2031.

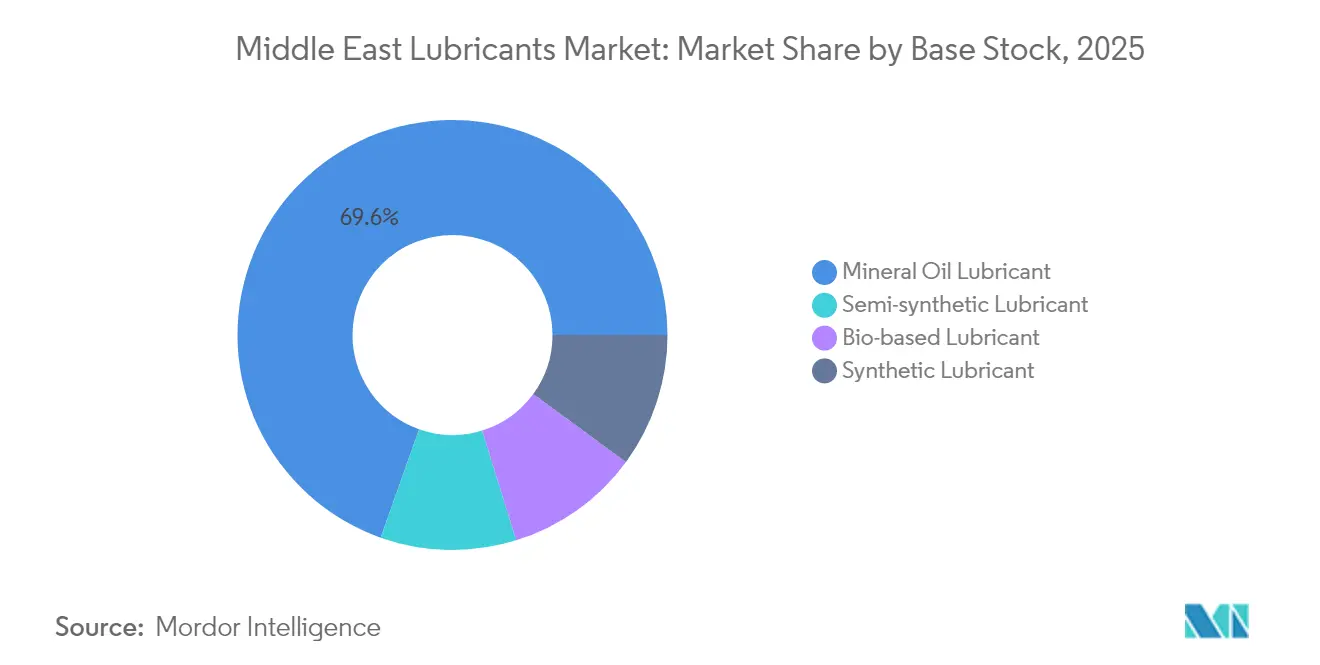

- By Base Stock, Mineral oils accounted for 69.58% share of the Middle East lubricants market size in 2025, while bio-based lubricants are forecast to grow at a 3.12% CAGR to 2031.

- By Product Type, Engine oils held 37.32% revenue share in 2025; transmission and hydraulic fluids are advancing at a 3.01% CAGR between 2026-2031.

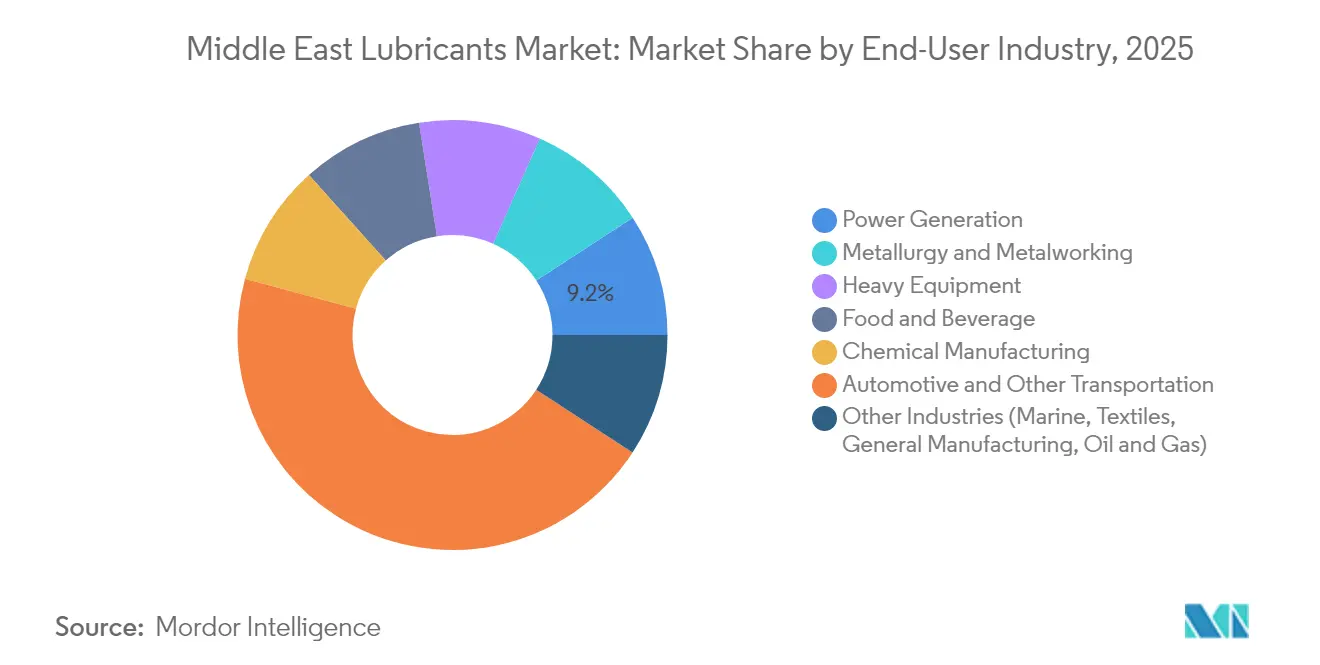

- By End-user Industry, Automotive and other transportation commanded 45.02% of the Middle East lubricants market size in 2025, whereas power generation is registering the fastest 3.09% CAGR to 2031.

- By Geography, Saudi Arabia led with 37.21% of the Middle East lubricants market share in 2025, while the United Arab Emirates is the fastest-growing geography at a 3.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Industrial expansion across GCC petrochemical and manufacturing hubs | +0.80% | Saudi Arabia, UAE, Qatar with spillover to Kuwait, Oman | Medium term (2-4 years) |

| Automotive fleet growth and aftermarket demand surge | +0.60% | Region-wide, concentrated in Saudi Arabia and UAE urban centers | Short term (≤ 2 years) |

| Mega infrastructure and power generation projects pipeline | +0.50% | Saudi Arabia, UAE, Qatar | Long term (≥ 4 years) |

| Shift toward high-performance synthetics for harsh climates | +0.40% | Desert and coastal operating zones across the Middle East | Medium term (2-4 years) |

| Local content mandates spurring domestic blending | +0.30% | Saudi Arabia, UAE, Kuwait | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Industrial Expansion Across GCC Petrochemical and Manufacturing Hubs

New petrochemical complexes, metals plants, and downstream converters are raising localized demand for compressor oils, heat-transfer fluids, and metalworking lubricants. The USD 11 billion Amiral project started up in 2024 with a 1.65 million ton ethylene cracker that relies on synthetic process oils able to tolerate 200 °C discharge temperatures[1]TotalEnergies Press Office, “TotalEnergies and Aramco inaugurate Amiral petrochemical complex,” totalenergies.com . Additions at SABIC Jubail and Qatar’s Ras Laffan extend the same requirement profile. Integrated producers typically specify Group II or Group III base stocks because higher viscosity index and oxidation stability reduce unplanned shutdowns, a critical metric in high-throughput polymer assets. Dense industrial clustering also lowers last-mile logistics costs, allowing distributors to implement vendor-managed inventories that keep plant lube rooms lean while guaranteeing uptime. This virtuous cycle underpins sustained uplift in premium-grade volumes across the Middle East lubricants market.

Automotive Fleet Growth and Aftermarket Demand Surge

Light-duty registrations continue to rise as income growth boosts vehicle ownership and e-commerce accelerates last-mile trucking. Saudi Arabia’s vehicle parc crossed 8 million units in 2024, and commercial segments are expanding at double-digit rates to serve NEOM, Diriyah, and other megaprojects[2]Saudi Arabian Monetary Authority, “Annual Statistics 2024,” sama.gov.sa . The UAE’s re-export hub status pulls in heavy-duty trucks that clock high annual mileage on trans-GCC corridors, driving demand for high-TBN engine oils meeting API CK-4 and low-SAPs Euro VI standards. Although synthetic formulations stretch change intervals to 75,000 miles, per-vehicle lube spend actually climbs because of higher unit prices and additive treat rates. OEM warranty requirements for API SN PLUS and ILSAC GF-6 classes are widening the premium tier, and this helps safeguard margins in the Middle East lubricants market despite plateauing drain volumes.

Mega Infrastructure and Power Generation Projects Pipeline

Desert megacities, port expansions, and cross-border rail links collectively anchor a multidecade construction cadence that leans heavily on hydraulic excavators, cranes, and rock crushers. Lubricants for such fleet assets must sustain viscosity from 10 °C dawn starts to 60 °C midday peaks, resist sand ingress, and permit 500-hour service intervals. NEOM alone is budgeted at USD 500 billion and draws thousands of diesel generators, marine engines, and tunnel-boring machines that together consume high-pressure gear oils and soot-handling 15W-40 heavy-duty engine oils. Parallel power-sector upgrades replace older steam plants with F-class and H-class gas turbines; these require ester-enhanced or PAO-based ISO 32 turbine oils capable of resisting coking at 230 °C bulk fluid temperatures. The pipeline thus provides a steady intake of specialty fluids throughout the forecast horizon.

Local Content Mandates Spurring Domestic Blending

Saudi Arabia’s iktva program, the UAE’s Operation 300bn, and similar frameworks tie project awards to local spend thresholds, pushing EPC contractors to source domestically blended lubricants wherever technically feasible[3]Local Content and Government Procurement Authority, “iktva Program Overview,” lcgpa.gov.sa . Multinationals respond by forming equity partnerships and building toll-blending hubs inside free zones to secure tax incentives and on-time customs clearance. Indigenous brands, in turn, gain better shelf presence in car-care chains and hypermarkets, leveraging domestic origin labels that resonate with both B2B and retail buyers. Over time, this policy-driven reshaping of supply chains elevates resilience, trims import bills, and supports capability transfer into additive dosing, package testing, and halal validation laboratories—areas where historical dependence on foreign expertise was high.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Base oil price volatility tied to crude fluctuations | -0.40% | Regional, particularly affecting Saudi Arabia, UAE, Kuwait refining margins | Short term (≤ 2 years) |

| Longer drain intervals reducing volumetric demand | -0.30% | Global Middle East, concentrated in commercial vehicle segments | Medium term (2-4 years) |

| Halal certification limits on additive chemistries | -0.20% | Regional Islamic markets, particularly Saudi Arabia, UAE, Qatar, Kuwait | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Base Oil Price Volatility Tied to Crude Fluctuations

Due to frequent fluctuations in Brent crude prices within a single quarter, refiners like Luberef are compelled to adjust their posted prices for Group I and Group II fuels every month. Meanwhile, independent blenders face squeezed margins, as base stocks account for as much as 75% of their formulation costs. Additionally, flexible retail pricing is challenging in markets that offer fixed service-package menus. Gross profit therefore compresses when crude rallies, prompting stocking discipline and hedging strategies that add financing costs. Conversely, rapid crude drops compel distributors to mark down inventories, triggering valuation losses. Such oscillations create planning uncertainty and trimmed CAPEX for capacity debottlenecks, restraining near-term growth within the Middle East lubricants market.

Longer Drain Intervals Reducing Volumetric Demand

OEM-approved synthetics now permit 1-year or 35,000-kilometer oil changes for buses and on-highway trucks, cutting annual oil volume per unit by up to 40% compared with 2018 norms. While premium pricing offsets part of the revenue impact, absolute liter throughput still declines, especially where national inspection regimes enforce adherence to OEM schedules. Workshops compensate by upselling ancillary services such as coolant checks and filter-replacement bundles, yet the structural shift toward high-stamina lubricants drags headline demand growth below the underlying equipment population expansion rate.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Group: Premium Migration Gains Traction

Group I held a 46.62% slice of the Middle East lubricants market share in 2025 because many industrial buyers still favor its lower cost for splash-lubed conveyors, piston-type air compressors, and gensets operating under moderate thermal stress. The segment’s installed base derives from decades of conventional refining and well-established additive treat recipes that assure supply continuity. However, OEM technical bulletins released in 2025 recommend Group II for new reciprocating compressor models and mandate Group III for turbocharged, charge-cooled engines running in sustained 50 °C ambient conditions, nudging end users toward higher-quality basestocks.

The performance narrative is compelling. Group III lubricants show 30% lower volatility and 20% higher viscosity index than Group I, extending oxidation life and reducing top-up rates. Saudi Aramco’s Luberef Phase II revamp adds Group II lines specifically targeting this migration. Distributors across Riyadh and Jeddah are already blending multigrades with 40–60% Group II cut to meet evolving SAE XW-30 viscosity demands. Although unit prices climb, total cost of ownership sinks as fleets adopt 500-hour drain cycles, boosting adoption within the Middle East lubricants market.

By Base Stock: Sustainability Nudges Product Mix

Mineral oils still represent 69.58% of total consumption, underpinned by abundant regional refining capacity, cost advantage, and broad additive compatibility. Yet, sustainability charters signed by top logistics operators and petrochemicals producers commit to 30% life-cycle carbon reduction by 2030. Bio-based lubricants—mainly vegetable-ester hydraulic oils and biodegradable metal-forming fluids—therefore attract attention and record a 3.12% CAGR, outpacing the wider market.

Bio-esters deliver greater than 90% biodegradability within 28 days and exhibit superior boundary lubrication, reducing tool wear in aluminum stamping lines by 15%. Nonetheless, oxidative stability lags, necessitating anti-oxidant boosters that increase formulation cost. Semi-synthetic blends combining mineral carriers with 20–30% bio-base strike a practical compromise, retaining ISO 11158 performance while lowering environmental exposure. Such innovations slowly chip away at mineral dominance and broaden the offering landscape inside the Middle East lubricants market.

By Product Type: Specialized Fluids Outpace Engine Oils

Engine oils accounted for 37.32% of 2025 demand as the light-duty and heavy-duty vehicle parc exceeded 15 million units across GCC states. Mandatory periodic vehicle inspection programs anchor stable replacement frequency, yet the fastest incremental volume now stems from transmission and hydraulic fluids, which are tracking a 3.01% CAGR to 2031. Desert construction fleets, tower cranes at port expansions, and tunnel-boring rigs for metro projects collectively require high-viscosity-index anti-wear formulations.

Metalworking fluids enjoy a parallel uplift as fabrication shops supporting NEOM and Ras Al Khair acquire CNC machine tools that rely on emulsifiable cutting oils and synthetic coolants. API RP 1525 bulk oil handling guidelines are gaining traction in distributor depots to prevent cross-contamination among these diversified fluid grades. Consequently, suppliers maintaining broad product lines and on-site laboratory support gain wallet share across the Middle East lubricants market size continuum.

By End-User Industry: Power Generation Emerges as Growth Engine

Automotive and other transportation segments still constitute 45.02% of volume in 2025 due to dense personal car ownership and thriving road-freight corridors. Yet power generation posts the sharpest 3.09% CAGR, propelled by gas turbine fleet additions linked to electrification targets and solar-hybrid installations that require synthetic heat-transfer oils.

Modern F-class turbines call for ester-augmented ISO 32 oils that maintain load-bearing film at 230 °C bulk temperatures. OEMs prescribe varnish-control metrics below 10 mg/L MPC index, a threshold traditional mineral oils struggle to meet. Coupled with the roll-out of 1.5 GW of concentrated solar power in Dubai by 2030, which depends on molten-salt pumps lubricated by high-flash-point fluids, this shift realigns product portfolios and supports revenue diversity within the Middle East lubricants market.

Geography Analysis

The Gulf Cooperation Council (GCC) bloc anchors 2025 regional demand, with Saudi Arabia securing 37.21% market share on the back of its broad industrial base and mega-infrastructure pipeline. Riyadh’s industrial zones in Jubail and Yanbu host integrated base-oil plants that supply local blenders, insulating the domestic market from some import volatility. Vision 2030 programs stipulate 70% local content, which has spurred lubricant packaging line investments in Dammam, further entrenching domestic supply resilience.

The UAE’s lubricants segment is tracking a 3.21% CAGR through 2031, reflecting strong growth in logistics, aviation, and marine bunkering. Jebel Ali Free Zone acts as a transshipment hub feeding Oman, Bahrain, and East Africa, so on-site toll-blenders maintain multi-grade production schedules that mirror diverse export specifications. Dubai’s 2040 Urban Master Plan, together with Abu Dhabi’s clean-energy build-out, elevates demand for turbine and hydraulic oils that must meet both API and halal certification standards.

Elsewhere, Qatar’s post-World-Cup infrastructure maintenance sustains construction equipment volumes, while Kuwait’s Integrated Petrochemical Complex will lift internal process-oil needs upon 2026 startup. Oman capitalizes on its Duqm and Sohar port corridors to draw marine lubricant volumes, and Bahrain’s finance-led diversification introduces data-center cooling projects that specify synthetic refrigeration lubricants. Iran remains a sizable but sanction-constrained market; localized blenders there rely on Group I imports from Russia, but multinationals stay cautious due to compliance risks. Iraq’s reconstruction activities generate spikes in hydraulic and gear oil demand, though political instability often disrupts supply chains and dampens sustained growth.

Competitive Landscape

The Middle East Lubricants Market exhibits consolidated concentration. Global majors command technology depth, certification breadth, and captive additive pipelines that underpin their Middle East leadership. Shell remains the volume leader for the 17th consecutive year and extends its position through a Saudi joint venture with Aljomaih that operates a high-speed blending plant in Jeddah. ExxonMobil and TotalEnergies similarly leverage cross-regional supply chains to feed premium synthetics into GCC markets.

Regional consolidation is accelerating. Saudi Aramco’s exploratory talks for a USD 15 billion Castrol acquisition signal a strategy to integrate internationally recognized retail brands with domestic base-oil feedstock, potentially redefining competitive hierarchies if concluded. FUCHS doubled its Yanbu capacity to 200,000 tonnes in 2025, supporting both industrial OEM fill and aftermarket channels. Petromin, already controlling about 40% of the Saudi passenger-car oil segment, rolled out halal-certified synthetic products that align with strict additive sourcing rules, boosting cross-border sales in Kuwait and Bahrain.

Technology competition now extends into electric-vehicle (EV) fluids, where dielectric coolants and copper-corrosion-inhibited greases represent emerging niches. Smaller disruptors such as Dubai-based Nanol Technologies trial nano-additive booster shots that promise 5–7% fuel savings in marine engines, aiming at IMO carbon-intensity index compliance. Meanwhile, additive specialists focus on halal-compliant detergent and anti-oxidant packages, filling capability gaps for regional blenders that previously relied on imported chemistries.

Middle East Lubricants Industry Leaders

Aljomaih and Shell Lubricating Oil Company Limited

BP p.l.c

Exxon Mobil Corporation

Saudi Aramco Base Oil Company - Luberef

TotalEnergies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: The American Petroleum Institute's 2025 International Standards Report revealed a 20% increase in the global adoption of API standards, with notable growth in Middle Eastern markets driving regulatory harmonization.

- January 2024: Saudi Aramco, following a government directive, will maintain its Maximum Sustainable Capacity at 12 million barrels per day instead of increasing it to 13 million barrels per day. This decision impacts regional refining capacities and base oil production planning.

Middle East Lubricants Market Report Scope

A lubricant is a substance that helps to reduce friction between surfaces in mutual contact, which ultimately reduces the heat generated when the surfaces move. It may also have the function of transmitting forces, transporting foreign particles, or heating or cooling the surfaces.

The Middle East lubricants market is segmented by group, base stock, product type, end-user industry, and geography. By group, the market is segmented into group I, group II, group III, group IV (PAO), and naphthenic. By base stock, the market is segmented into bio-based lubricants, mineral oil lubricants, synthetic lubricants, and semi-synthetic lubricants. By product type, the market is segmented into engine oil, transmission and hydraulic fluid, metalworking fluid, general industrial oil, gear oil, greases, process oil, and other product types (turbine oils, refrigeration oils, aviation oils, marine oils, and transformer oils). By end-user industry, the market is segmented into power generation, automotive and other transportation, heavy equipment, food and beverage, metallurgy and metalworking, chemical manufacturing, and other end-user industries (marine, textiles, manufacturing, and oil and gas). The report also covers the market size and forecasts for the lubricant market in 5 countries across the Middle East.

For each segment, the market sizing and forecasts have been done based on volume (liters).

By Group

| Group I |

| Group II |

| Group III |

| Group IV (PAO) |

| Naphthenics |

By Base Stock

| Bio-based Lubricant |

| Mineral Oil Lubricant |

| Synthetic Lubricant |

| Semi-synthetic Lubricant |

By Product Type

| Engine Oil |

| Transmission and Hydraulic Fluid |

| Metalworking Fluid |

| General Industrial Oil |

| Gear Oil |

| Greases |

| Process Oils |

| Other Types (Turbine, Refrigeration, Aviation, Marine, Transformer) |

By End-user Industry

| Power Generation |

| Automotive and Other Transportation |

| Heavy Equipment |

| Food and Beverage |

| Metallurgy and Metalworking |

| Chemical Manufacturing |

| Other Industries (Marine, Textiles, General Manufacturing, Oil and Gas) |

By Geography

| Saudi Arabia |

| United Arab Emirates |

| Iran |

| Iraq |

| Kuwait |

| Qatar |

| Oman |

| Bahrain |

| Rest of Middle-East |

| By Group | Group I |

| Group II | |

| Group III | |

| Group IV (PAO) | |

| Naphthenics | |

| By Base Stock | Bio-based Lubricant |

| Mineral Oil Lubricant | |

| Synthetic Lubricant | |

| Semi-synthetic Lubricant | |

| By Product Type | Engine Oil |

| Transmission and Hydraulic Fluid | |

| Metalworking Fluid | |

| General Industrial Oil | |

| Gear Oil | |

| Greases | |

| Process Oils | |

| Other Types (Turbine, Refrigeration, Aviation, Marine, Transformer) | |

| By End-user Industry | Power Generation |

| Automotive and Other Transportation | |

| Heavy Equipment | |

| Food and Beverage | |

| Metallurgy and Metalworking | |

| Chemical Manufacturing | |

| Other Industries (Marine, Textiles, General Manufacturing, Oil and Gas) | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Iran | |

| Iraq | |

| Kuwait | |

| Qatar | |

| Oman | |

| Bahrain | |

| Rest of Middle-East |

Key Questions Answered in the Report

What is the current volume size of the Middle East lubricants market?

The market reached 2.95 billion liters in 2026.

How fast is lubricant demand expected to grow in the GCC?

It is projected to rise at a 2.66% CAGR, reaching 3.36 billion liters by 2031.

Which country leads regional lubricant consumption?

Saudi Arabia holds 37.21% of the total volume, driven by the large petrochemical and transportation sectors.

What product category is growing fastest through 2031?

Transmission and hydraulic fluids are expanding at a 3.01% CAGR due to large infrastructure projects.

How do local content policies influence lubricant sourcing?

Programs like iktva require up to 70% domestic procurement, so many suppliers have built blending plants inside Saudi Arabia and the UAE.

Are bio-based lubricants gaining traction?

Yes, they are recording a 3.12% CAGR as industrial buyers introduce sustainability commitments and ISO biodegradable fluid standards.

Page last updated on: