Dried Apricots Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

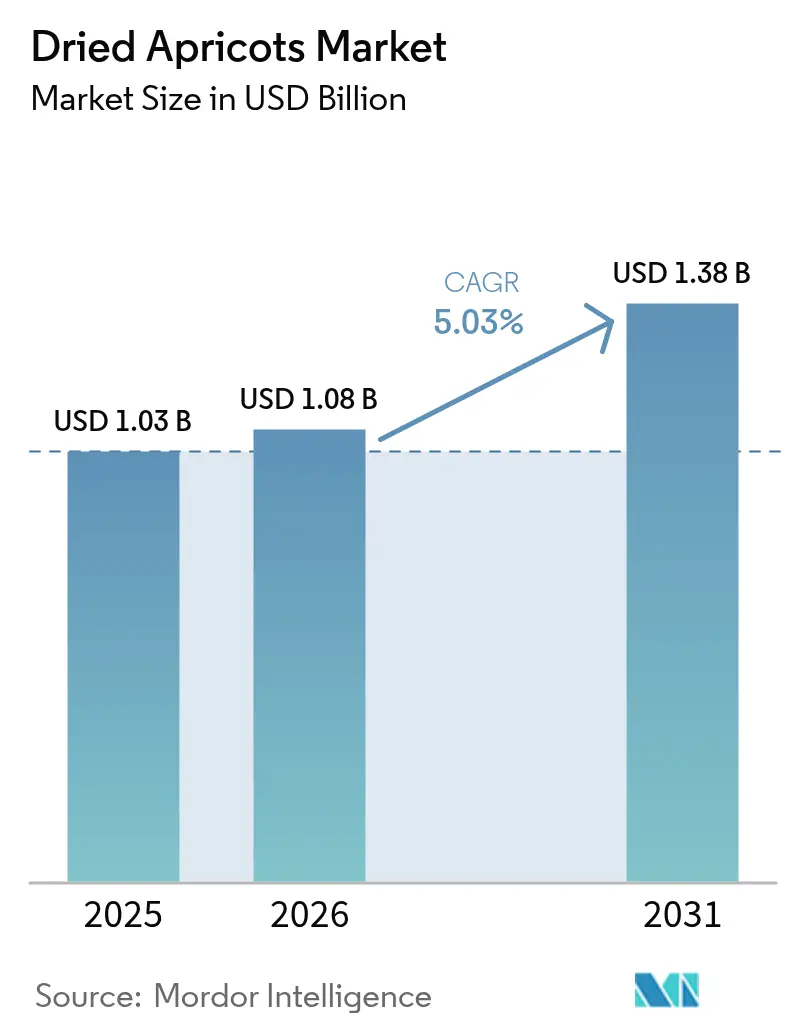

| Market Size (2026) | USD 1.08 Billion |

| Market Size (2031) | USD 1.38 Billion |

| Growth Rate (2026 - 2031) | 5.03% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Dried Apricots Market Analysis by Mordor Intelligence

The dried apricots market size is expected to grow from USD 1.03 billion in 2025 to USD 1.08 billion in 2026 and is forecast to reach USD 1.38 billion by 2031 at 5.03% CAGR over 2026-2031. This growth is driven by the increasing consumer preference for nutrient-dense snacks, the growing adoption of organic food products, and price premiums that help offset the higher production costs faced by growers. Rising health awareness in urban areas post-pandemic, coupled with the clean-label movement, has further strengthened the perception of dried fruits as a safe and shelf-stable alternative to traditional confectionery. Additionally, the expansion of digital commerce is providing greater market access for specialty brands that emphasize organic certifications and sulfur-free processing methods. Furthermore, the sports nutrition industry is contributing to the market's growth by incorporating apricot powder as a natural substitute for refined sugar, thereby broadening the ingredient's demand.

Key Report Takeaways

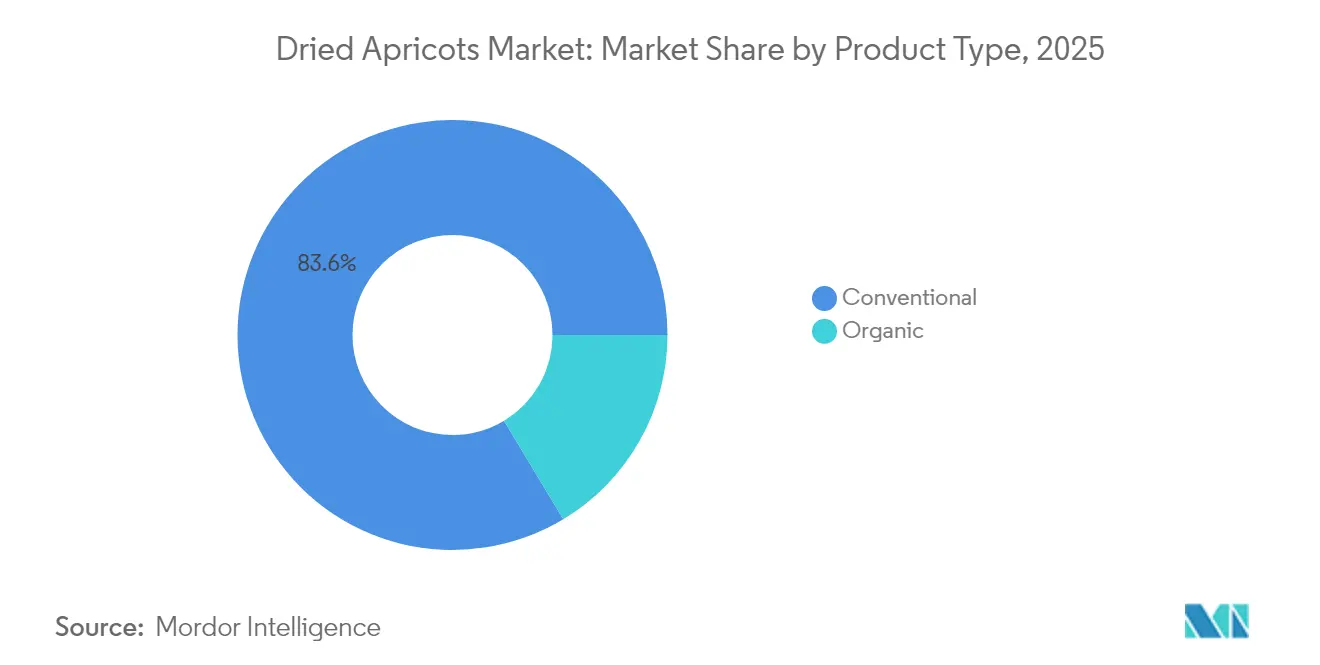

- By product type, conventional dried apricots led with 83.62% of the dried apricots market share in 2025, and organic is projected to grow at 7.29% CAGR to 2031.

- By form, whole fruit accounted for 60.88% share of the dried apricots market size in 2025, and powdered form is projected to grow at a 6.74% CAGR to 2031.

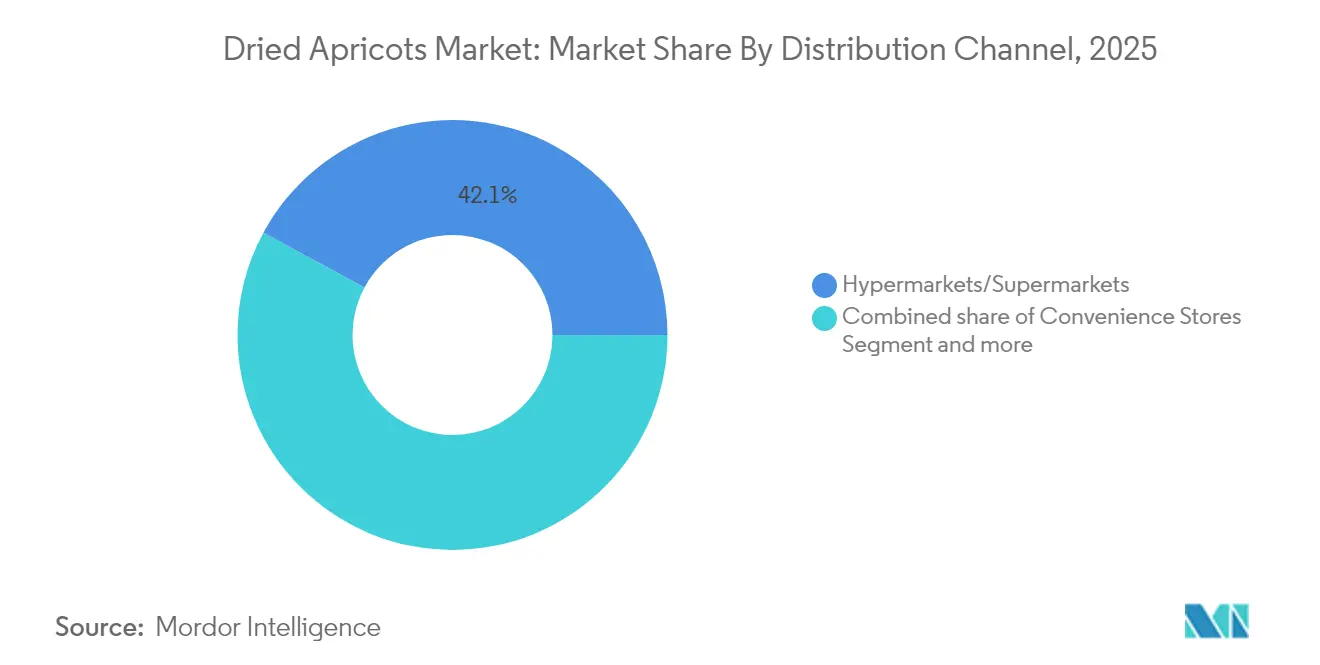

- By distribution channel, hypermarkets and supermarkets controlled 42.11% revenue, whereas online retail posted the fastest CAGR at 7.85% through 2031.

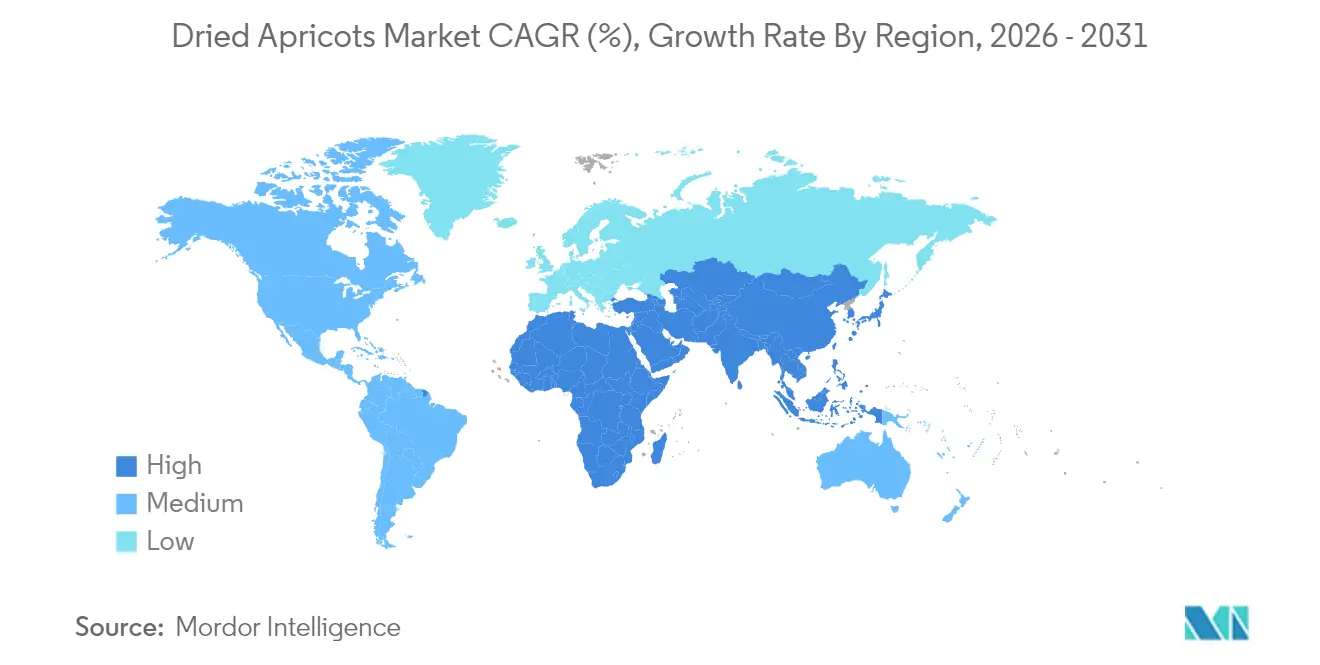

- By geography, North America commanded 31.93% of global revenue in 2025; Asia-Pacific is projected to grow at 6.59% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dried Apricots Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising preference for convenient, healthy snacks in urban households | +1.2% | Global, with early gains in North America, Europe, Asia-Pacific urban centers | Medium term (2-4 years) |

| Growth in packaged dried apricots through retail and e-commerce platforms | +1.8% | Global, spill-over from North America to APAC and Europe | Short term (≤ 2 years) |

| Extended shelf life and logistical advantages of dried apricots | +0.9% | Global, particularly beneficial for emerging markets with limited cold storage | Long term (≥ 4 years) |

| Increasing demand from health-conscious consumers seeking nutrient-rich foods | +1.5% | North America & EU core, expanding to APAC metropolitan areas | Medium term (2-4 years) |

| Rising demand for natural sugars in sports and energy bars | +0.8% | North America, Europe, with growth in APAC fitness markets | Medium term (2-4 years) |

| Growing Popularity of Plant-Based and Vegan Diets | +1.1% | Europe core, North America, urban APAC centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising preference for convenient, healthy snacks in urban households

Urban populations are increasingly gravitating towards health-conscious snacking, leading to a surge in demand for dried apricots. World Bank data reveals that in 2023, over 4.6 billion people, or more than half of the global population, resided in urban areas. This trend shows no signs of slowing, with projections indicating that by 2050, urban dwellers will account for nearly 70% of the global populace, further fueling the demand for health-centric snacks like dried apricots[1]World Bank, "Urban Development", www.worldbank.org. The segment has also reaped benefits from innovations in portion-controlled packaging, catering to the rising trend of on-the-go consumption. Moreover, placing dried apricots strategically alongside nuts and premium dried fruits in retail settings has bolstered their perceived value, drawing in a wider audience. Their innate sweetness, which curbs sugar cravings sans artificial additives, has further cemented their role in workplace wellness programs and school nutrition agendas. This evolving consumer behavior has sparked a preference for bulk purchases and larger packaging, moving away from single-serve options, underscoring a trend towards both cost-effectiveness and sustainability.

Growth in packaged dried apricots through retail and e-commerce platforms

The growing penetration of e-commerce in food retail has significantly enhanced the accessibility of dried apricots. Online platforms now enable direct-to-consumer sales, eliminating traditional distribution markups and allowing specialty producers to expand their geographic reach. The pandemic-driven shift toward digital grocery shopping has further accelerated this trend, particularly benefiting organic and premium dried apricot brands that effectively utilize detailed product storytelling and emphasize nutritional transparency. Subscription-based delivery models have emerged as key growth drivers, as consumers increasingly prefer recurring shipments of shelf-stable products, reducing the need for frequent shopping trips. Moreover, algorithmic recommendations have created cross-selling opportunities by pairing dried apricots with complementary products such as nuts, seeds, and other dried fruits, thereby increasing basket sizes and enhancing customer lifetime value. To address prior concerns about texture degradation in online purchases, the integration of temperature-controlled last-mile delivery has ensured consistent product quality, fostering greater consumer trust in e-commerce channels.

Extended shelf life and logistical advantages of dried apricots

The 12-18 month shelf life of properly processed dried apricots offers significant advantages in inventory management for retailers and distributors. This extended shelf life minimizes waste-related losses commonly associated with fresh produce and enables strategic stockpiling during periods of favorable pricing. Furthermore, the reduced weight and volume of dried apricots compared to fresh equivalents enhance transportation efficiency, lowering per-unit logistics costs. These factors support market penetration in geographically dispersed regions where fresh apricots are only seasonally available. The stability of dried apricots becomes especially critical during supply chain disruptions. For example, during the 2025 Turkish frost crisis, dried apricot inventories ensured market continuity, while fresh supplies faced complete interruption. Export-oriented producers leverage these logistical benefits to access distant markets that are economically unfeasible for fresh fruit distribution, thereby expanding their addressable market opportunities and strengthening their competitive positioning.

Increasing demand from health-conscious consumers seeking nutrient-rich foods

The rising convergence of nutritional awareness and the demand for convenience has significantly boosted the positioning of dried apricots within the functional foods market. Their high concentration of vitamin A and natural fiber appeals to health-conscious consumers seeking targeted health benefits rather than generic snacking options. Enhanced transparency through FDA nutritional labeling requirements has further empowered consumers to make informed decisions based on their specific dietary needs. The clean label movement has particularly driven the popularity of sulfur-free dried apricot variants. Despite their darker appearance and shorter shelf life, these variants align with the growing consumer preference for minimally processed and natural ingredient profiles. Additionally, their integration into meal replacement products and protein bars has expanded their applications beyond traditional snacking. Food manufacturers are leveraging the natural sweetness of dried apricots to reduce added sugar content while maintaining product palatability, further enhancing their appeal in the health-focused food segment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuations in raw apricot supply due to weather and agricultural challenges | -2.1% | Global, with concentrated impact from Turkey, Central Asia production regions | Short term (≤ 2 years) |

| Stringent quality and safety regulations | -0.7% | Global, with heightened enforcement in North America, EU import markets | Medium term (2-4 years) |

| Rising freight costs for temperature-controlled containers | -0.9% | Global trade routes, particularly Asia-Europe, Turkey-North America corridors | Short term (≤ 2 years) |

| Competition from Alternative Dried Fruits and Substitutes | -1.2% | Global, with intensified competition in mature North American and European markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fluctuations in raw apricot supply due to weather and agricultural challenges

Climate variability has significantly increased supply chain vulnerabilities for dried apricot producers. In 2025, a severe frost event in Turkey's Malatya region devastated 85% of the crops, highlighting the sector's acute exposure to extreme weather conditions. The Turkey Analyst Organization emphasizes that climate change poses a substantial threat to Turkey's position as a global food supplier. Notably, 97% of farmers in the country have reported reduced harvests due to environmental challenges, with key cash crops like apricots being severely affected[2]The Central Asia-Caucasus Institute & Silk Road Studies Joint Center, "Climate Change Threatens Turkey’s Role as a Food Supplier to Europe and the Middle East", www.turkeyanalyst.org. Water scarcity further exacerbates production difficulties, as groundwater depletion in traditional cultivation areas forces producers to invest in costly irrigation systems to sustain operations. The concentration of global supply in geographically limited regions amplifies systemic risks, leading to price volatility and challenges in fulfilling contracts. In response, buyers are increasingly diversifying their sourcing strategies by exploring alternatives in Central Asia. These supply chain disruptions extend to processing facilities, causing inventory shortages that directly impact product availability. Consequently, manufacturers are compelled to reformulate their products or identify substitute ingredients to mitigate the effects of these disruptions.

Stringent quality and safety regulations

Regulatory complexities have significantly increased across major importing markets, driven by evolving standards and enforcement measures. The USDA National Organic Program has intensified its enforcement activities and introduced new import oversight regulations, directly impacting the certification process for organic dried apricots[3]U.S. Department of Agriculture, "USDA Organic Oversight and Enforcement Update Summary of Activities – Calendar Year 2023", www.ams.usda.gov. Similarly, the FDA has updated its laboratory testing methods for dried fruits, incorporating advanced protocols to detect insect damage and mold contamination. In the European Union, sustainability requirements for processed fruit imports have added another layer of complexity for non-EU suppliers. These requirements not only increase certification burdens but also elevate compliance costs, creating challenges for market access. Additionally, traceability mandates now require comprehensive documentation throughout the supply chain, from farm-level production records to certifications at processing facilities. This administrative demand disproportionately impacts smaller producers, who often lack the resources to manage such extensive requirements. However, these changes also create significant barriers to entry, favoring established players with existing compliance infrastructure and resources to navigate the evolving regulatory landscape effectively.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Conventional Dominance Through Established Supply Networks

In 2025, conventional dried apricots command an 83.62% market share, due to established supply chains and a focus on price-sensitive consumers. These apricots, primarily sourced from Turkish production centers, benefit from economies of scale and streamlined processing, ensuring cost efficiency without compromising quality. Mature distribution relationships and consumer trust in traditional sulfur-treated products bolster the segment. These products, favored by mainstream retailers for their extended shelf life and consistent appearance, enjoy year-round availability due to efficient preservation techniques. Furthermore, a robust export infrastructure from major producing regions ensures competitive pricing, appealing to both cost-conscious consumers and institutional buyers. The segment's stability is underscored by consistent supply from established growing regions and consumer acceptance of traditional processing methods, even in the face of recent weather-related disruptions.

Organic dried apricots are on a growth trajectory, boasting a 7.29% CAGR through 2031. This momentum is fueled by expanding certification programs and premium positioning strategies, notably backed by the USDA's USD 300 million Organic Transition Initiative launched in 2024. Enhanced enforcement activities under the National Organic Program bolster consumer confidence in organic certification. Meanwhile, processing innovations are tackling shelf-life challenges associated with sulfur-free preservation. Reflecting a broader trend, consumers are willing to pay a premium for perceived health and environmental benefits. Here, organic certification acts as a quality beacon, attracting not just traditional health food enthusiasts but also mainstream grocery shoppers in search of added value.

By Form: Whole Fruit Tradition Versus Powder Innovation

In 2025, whole dried apricots dominate the market with a 60.88% share, driven by established consumer preferences for traditional snacking and their visual appeal, which allows for quality assessment based on color, size, and texture. This segment's prominence is deeply rooted in cultural consumption patterns and gift-giving traditions, especially in Middle Eastern and Mediterranean markets, where whole dried apricots hold both symbolic significance and culinary heritage. Whole fruit formats, benefiting from minimal processing, not only preserve nutritional integrity but also enjoy cost advantages over their value-added counterparts. This supports competitive pricing strategies, particularly appealing to price-sensitive consumers. The segment's stability is anchored in established consumer habits and the tactile satisfaction derived from traditional dried fruit consumption, a sensation that processed alternatives struggle to replicate.

Powdered dried apricots are on a growth trajectory, accelerating at a 6.74% CAGR. This surge is attributed to their expanding roles in functional food formulations and as enhancers in beverages, a trend notably embraced by the sports nutrition industry. The National Center for Biotechnology Information highlights apricot powder's prowess in protein formulations, offering natural sweetness and a rich micronutrient profile without compromising on texture or shelf stability. Advances in manufacturing, particularly in freeze-drying and spray-drying technologies, have not only slashed processing costs but also ensured the preservation of nutritional content, making apricot powder a competitive alternative to synthetic options. The segment's growth is further fueled by its foray into nutraceuticals and functional beverages, sectors that prioritize concentrated nutrition and processing convenience.

By Distribution Channel: Traditional Retail Versus Digital Disruption

In 2025, hypermarkets and supermarkets command a 42.11% market share, capitalizing on established consumer shopping habits and strategic product placements. These tactics not only boost impulse buying but also promote cross-merchandising with related items. This dominance underscores consumers' preference for tactile evaluations, especially when selecting dried fruits, where visual cues like color, size, and freshness play pivotal roles. Traditional retail outlets, bolstered by strong supplier ties and bulk purchasing power, offer competitive pricing. Moreover, by strategically positioning products near checkout counters and emphasizing health-centric items, they effectively capture impulse buys. This channel's resilience is rooted in consumers' comfort with in-store experiences and the instant gratification of immediate product access, free from delivery delays.

Online retail channels are on an upward trajectory, boasting an 7.85% CAGR. This growth mirrors the swift digital shift in food buying habits and the rise of direct-to-consumer brands, all made possible by enhanced logistics. The Food and Agriculture Organization highlights that shifts in behavior during the pandemic have left a lasting mark on food buying trends. Today, consumers are more at ease purchasing shelf-stable items, like dried apricots, online. E-commerce's growth is further fueled by subscription models, offering producers steady revenue while allowing them to charge a premium for convenience, a price point often higher than traditional retail. This channel's ascent is a testament to evolving consumer habits, especially the trend towards omnichannel shopping, where online research shapes buying choices. Brands that ensure consistent messaging across all platforms stand to gain significantly.

Geography Analysis

In 2025, North America commands a 31.93% market share, bolstered by a robust health food retail infrastructure and premium strategies emphasizing organic certifications and artisanal claims. This leadership is underscored by mature cooperatives like Sun-Maid Growers, which leverage scale advantages and brand recognition for broader retail penetration. California's 2023 apricot output of 35,820 tons, valued at USD 49.03 million, not only ensures supply security but also bolsters local processing and curbs import reliance. The region's supremacy is further enhanced by established distribution networks and a consumer base willing to pay a premium for quality.

Asia-Pacific is set to be the fastest-growing region, boasting a 6.59% CAGR through 2031. This growth is fueled by urbanization and a burgeoning middle class that increasingly favors health-centric snacks over traditional confections. Rising disposable incomes and a shift in dietary habits, especially in urban centers adopting Western lifestyles, further propel this trend. Countries like China and India, with their local processing capabilities, not only diminish import reliance but also enable competitive pricing, broadening market access beyond just premium segments. Moreover, the surge in e-commerce is revolutionizing market dynamics, allowing online platforms to sidestep traditional retail hurdles.

Despite facing economic challenges, Europe witnesses consistent demand growth. This is largely attributed to a shift towards certified organic products and alternative sourcing, aimed at diminishing reliance on Turkish imports. The region's regulatory landscape increasingly champions clean-label products and sustainability, granting a premium edge to producers who prioritize responsible sourcing. Meanwhile, Central Asian nations like Uzbekistan and Afghanistan are carving a niche in the market, thanks to EU trade agreements and quality certifications, positioning them as credible alternatives to traditional Turkish suppliers grappling with climate-induced production hurdles.

Regulatory Landscape

International trade in dried apricots is shaped by Codex Alimentarius (Codex Standard for Dried Apricots, CXS 130-1981) and UNECE DDP-15, which anchor product specifications, dehydration targets, storage stability, and labeling expectations. The UNECE standard sets a general moisture target around 22%, with allowances up to 25% for specific varieties, guiding processing controls and claims such as soft-moist positioning.

In the United States, market access and grading align with USDA Agricultural Marketing Service (AMS) grade standards, while food safety and import compliance sit under FDA oversight and the Food Safety Modernization Act (FSMA). The FDA Foreign Supplier Verification Programs (FSVP) place responsibility on US importers to verify that foreign suppliers control relevant hazards, and FDA entry screening can trigger additional review when documentation, labeling, or safety controls do not meet requirements, making traceability and supplier-approval programs operational necessities for exporters.

Competitive Landscape

The global dried apricots market remains highly fragmented, with numerous local players dominating production and processing regions. Manufacturers are increasingly leveraging diverse marketing channels, with online platforms emerging as a significant opportunity for new entrants to gain market share. Strategic priorities are shifting toward vertical integration and enhanced supply chain management. Leading players are investing in direct partnerships with farmers and developing advanced processing capabilities to ensure consistent quality and secure supply chains, especially in the face of volatile raw material markets.

A focus on organic certifications, sustainable packaging solutions, and value-added processing techniques drives innovation in the market. These efforts enable differentiation beyond traditional price-based competition. Established brands continue to capitalize on strong consumer recognition and well-established distribution networks to maintain their competitive edge. Regional dynamics vary significantly, with North American players benefiting from cooperative business models and strong brand equity, while European markets emphasize sustainability credentials and supply chain transparency. This focus on certifications and transparency creates significant barriers for conventional producers who lack these capabilities.

Emerging opportunities are evident in direct-to-consumer sales channels and specialized applications, such as sports nutrition. Smaller players can effectively compete in these niches by emphasizing premium quality and targeted positioning. The fragmented nature of the market also presents acquisition opportunities for larger food companies aiming to expand their dried fruit portfolios. However, regulatory challenges and the complexities of managing supply chains limit the potential for consolidation compared to other food categories.

Dried Apricots Industry Leaders

-

Fruits of Turkey

-

Sun-Maid Growers of California

-

Traina Dried Fruit

-

Anatolia AS

-

Bergin Fruit and Nut Company

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Premiumization around organic, clean-label, and sulfur-free positioning continues to create whitespace for brands that pair verified certification with consistent sensory quality, especially as online retail accelerates discovery for specialty SKUs and subscription replenishment models. The USDA National Organic Program enforcement focus, alongside the USDA Organic Transition Initiative launched in 2024 (USD 300 million), reinforces the commercial value of credible organic claims and raises the bar for documentation and chain-of-custody practices that favor processors with strong supplier management.

Supply volatility centered on Turkey remains a defining market lever and is directly shaping sourcing strategies, contract structures, and inventory planning. The 2025 frost shock in Turkey (Malatya) highlighted the role of carryover inventories in keeping shelves stocked, and 2026 trade commentary around the new crop and export bookings underscores how quickly EU buyers respond to changes in availability. This environment supports opportunities for diversified origin programs (including Central Asia), closer processor-farmer linkages, and value-added formats such as powder for sports nutrition applications where formulators use apricot ingredients to reduce added sugars while maintaining texture and sweetness within shelf-stable products.

Recent Industry Developments

- July 2026: Turkish dried apricot market updates highlighted the new-season crop being affected by localized weather, including April hail in parts of the producing region, with crop estimates discussed in the 75,000 to 80,000 MT range. This kept buyer attention on supply risk management and reinforced the importance of diversified sourcing and inventory buffers for importers and packers.

- May 2025: A major retailer expanded its dried fruit category by launching a private-label dried apricot snack line, signaling increased demand visibility for processors and accelerating branded competition in shelf-stable formats.

- November 2024: Traina Dried Fruit, Inc. acquired Martin Farms in Patterson, California, adding production capacity for sun-dried agricultural products. The move strengthened vertical integration and supply control, supporting consistent quality and availability for retail and ingredient customers amid raw fruit volatility.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers dried apricots sold as shelf-stable food, where water is removed through sun-drying or mechanical dehydration and the product is bought for direct human consumption in retail or foodservice.

Scope exclusions: It does not count ingredient-grade apricot paste, puree, or blended inclusions that are already part of another finished food product.

Segmentation Overview

-

By Product Type

- Organic

- Conventional

-

By Form

- Whole

- Diced

- Powder

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Specialist Retailers

- Online Retail

- Other Retail Channels

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clean view of supply, trade, and demand signals that can be checked year over year. We refer to public sources such as FAOSTAT for fruit production context, UN Comtrade for dried fruit trade flows, and USDA and EU market and trade notes where relevant, plus national statistics offices for inflation and household food spend indicators.

Company annual reports, investor presentations, and credible press are then used to understand product positioning, packaging shifts, and channel mix changes across regions. For cross-checks, we also use paid subscriptions for company financials and intelligence, shipment-level import and export data, and patent databases when drying methods and preservation approaches affect product form. The specific desk sources listed here are illustrative, and many other references were used for data collection, validation, and clarification during the research process.

Primary Interviews and Surveys

Primary interviews are used to confirm what desk signals cannot explain well, such as observed pricing behavior, grade mix (natural versus sulphured), and how demand moves between retail, bakery, and food manufacturers. We spoke with growers, processors, traders, distributors, and large buyers across APAC, EMEA, and the Americas so that regional crop swings and trade seasonality could be reflected in the final assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 15% | APAC: 44% |

| Mid tier: 43% | Functional/Unit leaders: 27% | EMEA: 36% |

| Smaller Players: 19% | Managers: 58% | Americas: 20% |

Market-Sizing & Forecasting

Sizing starts from a top-down demand pool where production and trade data are reconstructed into apparent consumption by region, then adjusted using interview-backed splits for retail packs versus bulk use. The total is corroborated with selective bottom-up approximations, where sampled supplier volumes and a checked ASP-by-grade range are applied to validate the order of magnitude and correct obvious gaps.

Key inputs we track include dried apricot import and export volumes, crop yield swings in major origin countries, price spreads between organic and conventional lots, shares of whole versus diced and powder forms, and channel shifts toward online and modern grocery. When data is missing for smaller consuming countries, gaps are handled by proxying from similar income and diet baskets, and then the result is pressure-tested against trade receipts and buyer feedback.

Forecasts rely on scenario analysis supported by simple regression checks, where variables like historical volume trends, expected harvest conditions, inflation-adjusted food spending, and trade policy or freight disruption signals are used to shape the base case. Before numbers are finalized, we verify that the assumptions can be repeated and explained, which helps keep the model stable during annual updates.

Data Validation & Update Cycle

Validation is done through a step-by-step triangulation process so one data stream does not drive the whole answer. Model outputs are compared with independent signals such as trade totals, price movements, and major origin season outcomes, and then anomalies are reviewed and corrected before sign-off.

If a large variance appears, such as an unexpected price jump without a matching supply shock, we re-check the inputs and re-contact relevant interviewees to confirm what changed. Reports are refreshed annually, and interim updates are made when material events occur, such as crop failures, major policy shifts, or sharp freight changes. Right before delivery, an analyst does a final pass so clients receive the latest updated view that matches the most recent data cut.

Mordor Intelligence's Dried Apricots Market Size Versus Other Published Estimates

Published market sizes for dried apricots often look different because the scope line is drawn differently and the price logic is not the same across studies. The base year used, the way forms are grouped, and the handling of bulk trade versus packaged consumption can all move the final number.

Differences also come from how each study treats product types like organic, natural, and sulphured, and whether powders and diced formats are counted as direct market sales or as ingredient inputs. Currency timing, inflation treatment, and refresh cadence matter as well, especially when harvest outcomes and trade flows change quickly from one season to the next.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.08 B (2026) | |

| Global Consultancy A | USD 0.94 B (2024) | Uses an earlier base year and mixes offline channels into broad baskets, which can understate recent price and mix changes after newer harvest cycles and trade resets. |

| Industry Publisher B | USD 0.87 B (2024) | Applies a wider end-use lens that can blur direct dried apricot sales with adjacent ingredient usage, and the price curve assumptions are not clearly tied to trade-linked grade spreads. |

The benchmark table shows a spread that is largely explained by timing and what is treated as direct dried apricot sales, and in Mordor Intelligence's model the value is tied to shelf-stable dried apricot products meant for direct consumption, while excluding ingredient-grade paste or puree that would otherwise inflate totals. Once the same year and the same inclusion rules are applied, the gap typically narrows, and the remaining differences are mostly driven by how prices are progressed and cross-checked against trade and crop signals.

Key Questions Answered in the Report

What is the current value of the dried apricots market?

The dried apricots market reached USD 1.08 billion in 2026 and is forecast to reach USD 1.38 billion by 2031.

Which region holds the largest share of dried apricot sales?

North America led with 31.93% of global revenue in 2025 due to well-developed health-food retail channels and strong cooperative brands.

How fast is the organic segment growing within dried apricots?

Organic dried apricots are projected to rise at a 7.29% CAGR from 2026 to 2031, outpacing conventional products as certification gains consumer trust.

Why are powdered dried apricots attracting sports-nutrition brands?

Apricot powder provides natural sugars, potassium, and moisture-binding pectins that improve protein bar texture without artificial sweeteners, supporting a 6.74% CAGR in this form.

Page last updated on: