Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

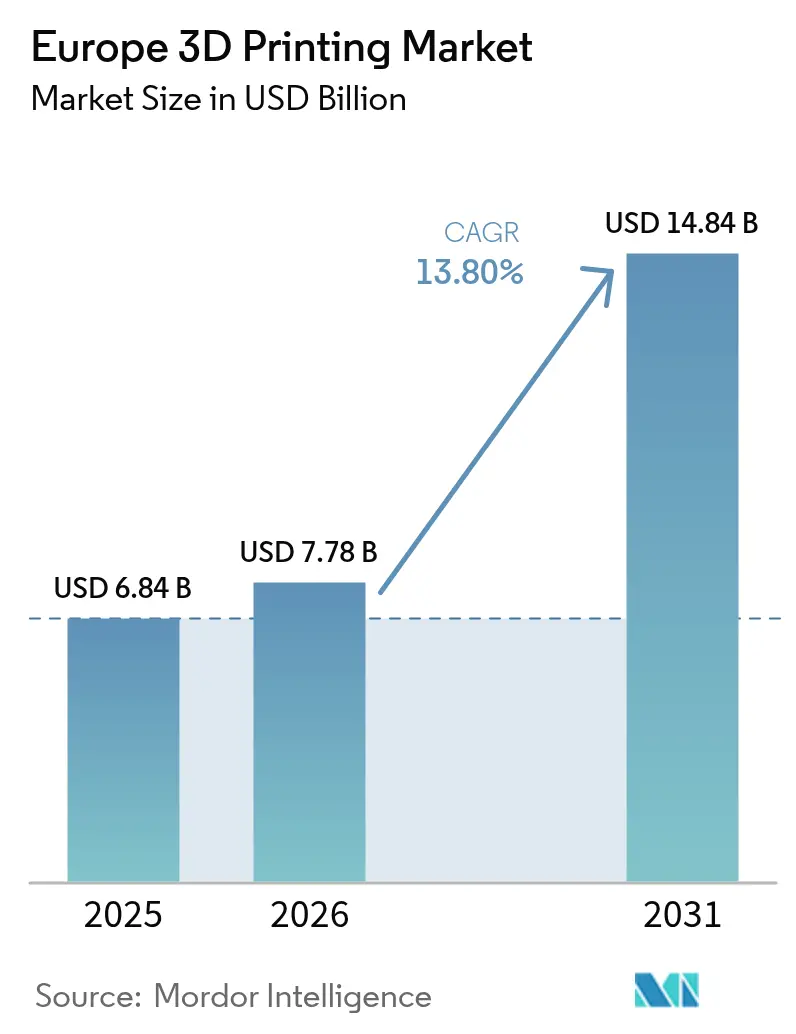

| Base Year Market Size (2025) | USD 6.84 Billion |

| Market Size (2026) | USD 7.78 Billion |

| Market Size (2031) | USD 14.84 Billion |

| Growth Rate (2026 - 2031) | 13.80% CAGR |

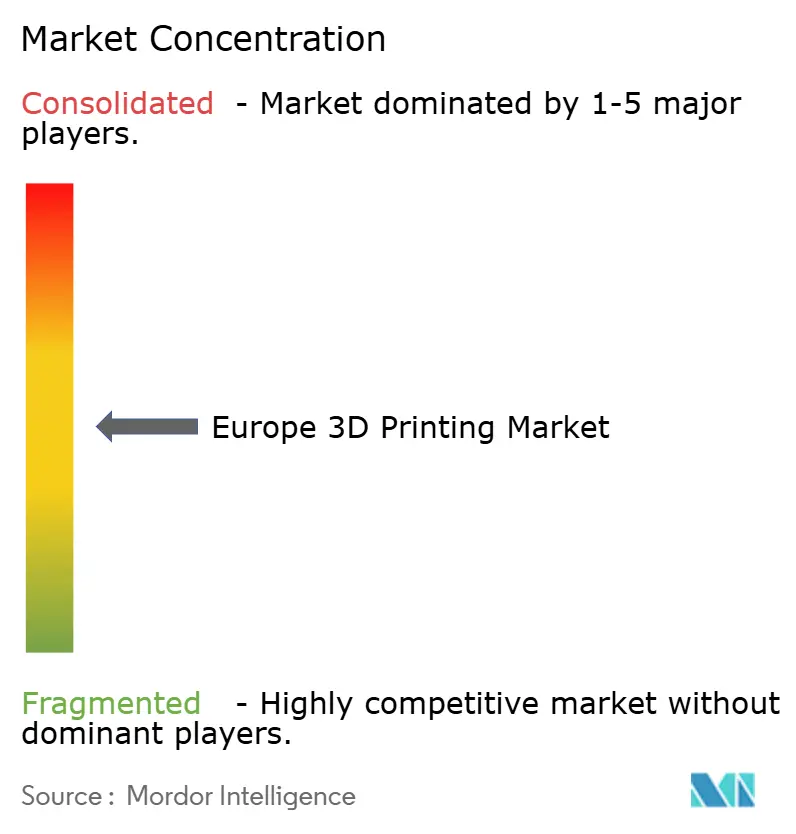

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe 3D Printing Market Analysis by Mordor Intelligence

The Europe 3D printing market size is expected to grow from USD 6.84 billion in 2025 to USD 7.78 billion in 2026 and is forecast to reach USD 14.84 billion by 2031 at 13.8% CAGR over 2026-2031. This expansion occurs as manufacturers across the region accelerate distributed-production strategies to cut lead times, hedge against supply-chain shocks and meet carbon-border adjustment requirements that reward localized output. Fast innovation cycles, falling metal-printer costs and the integration of artificial-intelligence process control underpin a widening set of production-grade use cases across automotive, healthcare and maritime industries. Hardware sales still dominate revenue, yet service-oriented “manufacturing as a service” models are scaling quickly, reflecting user preference for flexible capacity without large capital outlays. Country-level momentum is uneven: Germany leverages patent depth and automation expertise to safeguard its leadership position, while the Netherlands deploys world-class logistics and maritime clusters to register the highest growth pace. Competitive intensity rises as incumbents integrate vertically, newer entrants push novel materials and the European Union harmonizes technical standards to ease cross-border operations.

Key Report Takeaways

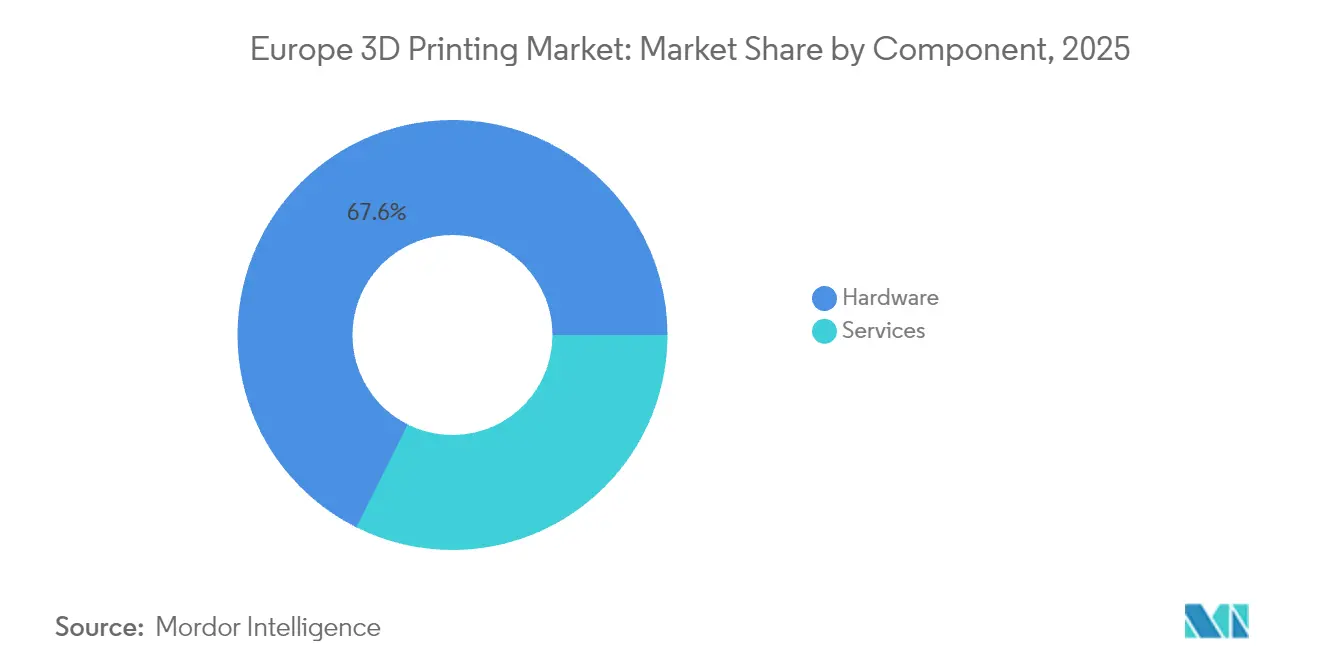

- By component, hardware captured 67.62% of the Europe 3D printing market share in 2025, while services recorded the fastest CAGR at 15.97% through 2031.

- By technology, FDM led with 29.12% revenue share of the Europe 3D printing market in 2025; DLP is projected to expand at 14.42% CAGR between 2026 and 2031.

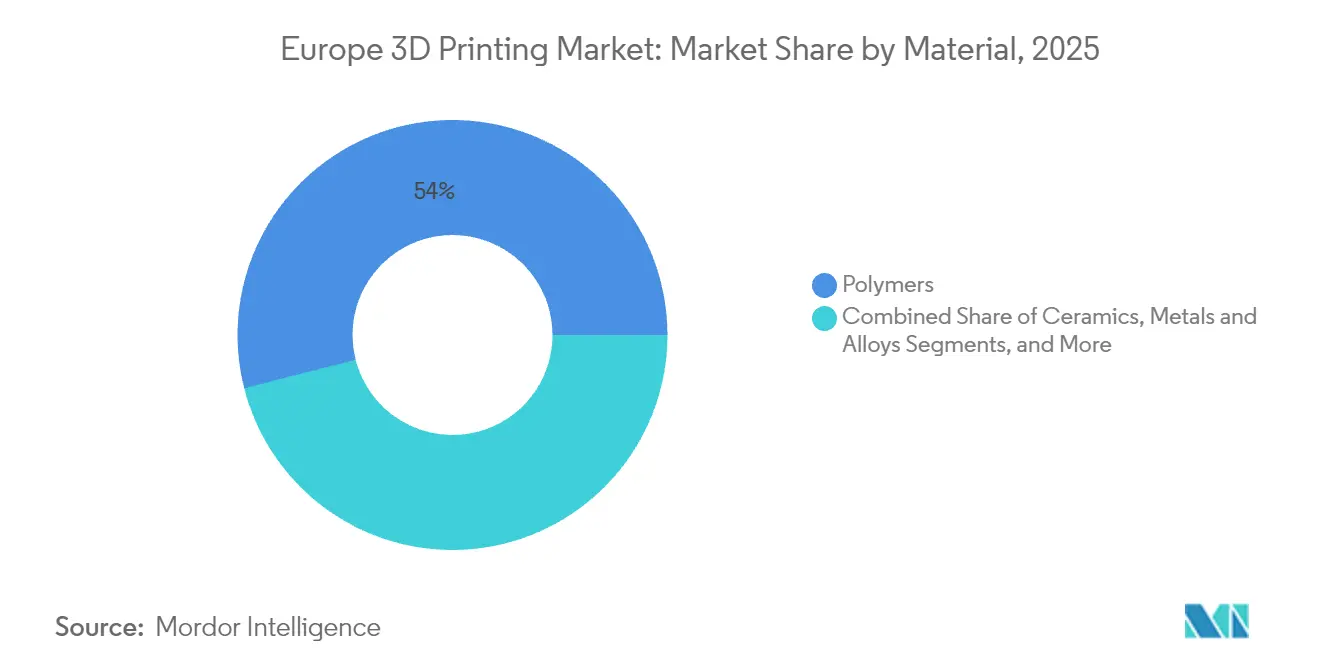

- By material, polymers accounted for 53.98% of the Europe 3D printing market size in 2025 and metals and alloys are advancing at a 15.21% CAGR to 2031.

- By end-user industry, automotive held a 24.22% share of the Europe 3D printing market size in 2025, whereas healthcare is moving at a 14.63% CAGR through 2031.

- By country, Germany commanded 29.41% of the Europe 3D printing market share in 2025, and the Netherlands posts the highest projected CAGR at 14.95% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe 3D Printing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government initiatives and funding for Industry 4.0 and AM | +2.1% | EU-wide (Germany, France) | Medium term (2-4 years) |

| Automotive OEM demand for lightweight prototyping and tooling | +1.8% | Germany, Italy, France | Short term (≤ 2 years) |

| Healthcare adoption for patient-specific devices | +2.3% | EU-wide (Netherlands, Germany) | Long term (≥ 4 years) |

| Declining cost of metal printers and materials | +1.9% | Industrial regions across EU | Medium term (2-4 years) |

| EU carbon-border adjustment boosting localized production | +1.4% | EU manufacturing hubs | Long term (≥ 4 years) |

| On-demand spare-parts needs in rail and maritime sectors | +1.2% | Netherlands, Germany, Nordics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Initiatives and Funding for Industry 4.0 and AM

European governments deploy sizeable capital to speed additive-manufacturing adoption. France’s EUR 54 billion “France 2030” program earmarks funds for advanced manufacturing platforms. Horizon Europe further backs “manufacturing as a service” pilots that network equipment across borders into cloud-managed production lines.[1]Élisabeth Borne, “Understanding France 2030,” info.gouv.fr In Germany, additive-manufacturing firms invest 30.6% of turnover in research, amplified by national and EU grants, cementing leadership in metal systems. The shared funding model drives technology transfer from laboratories to shop floors and builds a cadre of suppliers aligned to common technical standards. As a result, the Europe 3D printing market secures economies of scale that lower entry barriers for mid-sized enterprises.

Automotive OEM Demand for Lightweight Prototyping and Tooling

Automotive manufacturers now pursue additive-manufacturing beyond early prototyping. The EU-funded Multi-FUN project reveals multi-material builds that embed wiring and sensors into lightweight structures.[2]European Commission, “Horizon Europe Multi-FUN Project,” europa.eu German suppliers print low-volume production tooling to manage model-specific parts without storing costly inventory. By exploiting single-build assemblies that cut welds and bolts, companies save weight and shorten production cycles, sustaining momentum for the Europe 3D printing market in core automotive corridors.

Healthcare Adoption for Patient-Specific Devices

Hospitals across Europe scale 3D-printed guides, prosthetics and implants to deliver point-of-care solutions. The European Medicines Agency clarifies approval pathways, giving clinicians confidence to adopt patient-matched devices. EU research consortia such as ENLIGHT explore 3D-printed pancreas prototypes, while PRISM-LT develops living-tissue constructs that could redefine transplant workflows. With reimbursement frameworks catching up, healthcare systems deepen reliance on additive-manufacturing labs, supporting double-digit expansion within the Europe 3D printing market to 2030.

Declining Cost of Metal Printers and Materials

Per-unit metal-printing costs fall as powder recycling techniques—sieving, plasma spheroidization and vacuum degassing—recover feedstock quality for repeated cycles. Equipment makers like EOS bake artificial-intelligence fault prediction into machines to reduce scrap and reprint rates. Higher deposition speeds from electron-beam and selective-laser systems allow mid-volume runs that were once uneconomic, enlarging the reachable addressable base for the Europe 3D printing market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital investment and maintenance costs | -1.6% | EU-wide, particularly SMEs | Short term (≤ 2 years) |

| Shortage of design-for-AM talent | -1.3% | Industrial regions across EU | Long term (≥ 4 years) |

| Fragmented EU certification and standards landscape | -1.1% | EU-wide, concentrated in medical applications | Medium term (2-4 years) |

| Metal-powder supply volatility and recycling hurdles | -0.9% | Germany, Netherlands, industrial hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Investment and Maintenance Costs

Industrial-grade printers carry six-figure price tags, and users must add powder-handling, post-processing, and quality-assurance gear. Small and medium-sized enterprises often defer purchases even as hardware prices decline. Compliance with the EU Medical Device Regulation imposes rigorous documentation and post-market surveillance, inflating overhead for healthcare adopters. Fragmented certification regimes for rail, aerospace, and energy sectors multiply testing budgets, narrowing the addressable base of the Europe 3D printing market until rental or service models offset risk.

Shortage of Design-for-AM Talent

Less than one-fifth of global manufacturers employ qualified additive-manufacturing engineers, and European firms reflect similar gaps.[3]Society of Manufacturing Engineers, “Key AM Trends to Watch in 2025,” sme.org University programs scramble to integrate lattice optimization, multi-material simulation and process-control modules into curricula. Without the right skillsets, companies fail to exploit geometry freedom, leading to costly redesign loops and unrealized throughput gains. This talent deficit tempers near-term uptake across the Europe 3D printing market, especially for complex production-run opportunities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Accelerate as Hardware Matures

Service providers captured a growing slice of revenue as enterprises prioritize flexibility. Although hardware still anchored 67.62% of the Europe 3D printing market in 2025, service-oriented models are scaling at 15.97% CAGR as firms outsource design optimization, build preparation and post-processing. Contract manufacturers such as K3D and FKM deploy multi-printer farms, giving customers just-in-time parts without locking capital into machines. This transition lowers the cost of experimentation and spreads risk across diverse client pipelines.

In parallel, hardware vendors bundle software, maintenance, and training subscriptions, blurring lines between equipment sales and recurring services. Cloud dashboards aggregate fleet-wide data, enabling predictive maintenance and consumable replenishment. These integrated offers reinforce adoption, propelling the Europe 3D printing market toward outcome-based procurement norms.

By Technology: DLP Emerges as Precision Manufacturing Leader

FDM maintained the largest share in 2025 at 29.12% thanks to mature materials, low operating costs, and broad user familiarity. Yet DLP is registering an impressive 14.42% CAGR, propelled by sub-50-micron feature capability that suits dental aligners, hearing aids, and tissue-scaffold research. Advances in plant-based photopolymers reinforce sustainability credentials while widening the bio-compatibility palette. SLA and SLS cater to aerospace and automotive requirements for heat-resistant components, whereas electron-beam melting remains the go-to for titanium lattice structures in orthopedic implants.

Technology differentiation now hinges on automation and closed-loop control. AI-driven voxel-level correction trims support mass and eases depowdering, elevating utilization rates across the Europe 3D printing market. Multi-laser coordination in powder-bed systems balances productivity and surface finish, giving manufacturers confidence to qualify parts for serial production.

By Material: Metals Surge Despite Polymer Dominance

Polymers secured 53.98% of revenue in 2025 via versatility in prototyping and tooling. However, metal and alloy volumes are forecast to rise at 15.21% CAGR as post-processing workflows become less labor-intensive and powder reclaim cycles stretch material value. Stainless steel, nickel super-alloys, and aluminum bronze find demand in spare-parts pools for rail, oil-and-gas, and maritime operators seeking corrosion resistance and weight savings.

Sustainability pressures push the development of recycled composites that meet mechanical performance while lowering carbon footprints. Breton’s wood-fiber biocomposites replace virgin polymer feedstock in large-format printers, aligning with circular-economy objectives.Ceramics and high-temperature composites carve out niches in energy turbines and chemical reactors, indicating how material breadth underpins the Europe 3D printing market’s future revenue mix.

By End-user Industry: Healthcare Outpaces Traditional Manufacturing

Automotive occupied 24.22% of the Europe 3D printing market in 2025 through applications in wind-tunnel models, lattice seat frames, and on-demand jigs. Yet healthcare posted the sharpest trajectory at 14.63% CAGR as hospitals deploy point-of-care print labs for surgical planning guides and bespoke implants. Aerospace programs qualify weight-critical brackets that consolidate multiple sheet-metal parts into single titanium structures, shaving assembly hours and fuel burn.

Energy utilities incorporate additive manufacturing for burner tips and pump impellers, cutting outage downtime. Construction startups experiment with gantry and robotic systems that extrude cementitious material for façade elements, though building-code harmonization remains a hurdle. Collectively these sectors showcase the broadening demand base sustaining the Europe 3D printing market.

Geography Analysis

Germany retained a commanding 29.41% slice of the Europe 3D printing market in 2025 as its Mittelstand suppliers leverage decades-long automation prowess to commercialize metal-powder bed systems. National and EU grants covering up to 50% of R&D budgets widen the patent moat around firms like EOS and SLM Solutions, while automotive OEMs anchor domestic demand for production tooling. The ecosystem benefits from dense clusters of powder suppliers, measurement-equipment makers and research institutes that streamline part qualification workflows.

The Netherlands advances fastest, clocking a 14.95% CAGR to 2031. Rotterdam’s port infrastructure underpins maritime use-cases such as Royal3D’s large-format printed aquatic drones that reduce mold lead-times for composite hulls. Innovation centers in Eindhoven and Twente channel venture capital into medical and electronics startups, reinforcing a national brand around agile hardware prototyping. Government facilitation of cross-border projects with German shipyards highlights a cooperative model expanding the Europe 3D printing market footprint along the North Sea corridor.

France scales additive manufacturing under the EUR 54 billion France 2030 umbrella, focusing on aerospace propulsion, luxury goods and orthopedic implant value networks. Italy and Spain grow through automotive tooling and multi-jet fusion development hubs, while the United Kingdom preserves momentum via defense and energy programs despite new customs frictions. Eastern European markets, notably Poland, reveal lower adoption owing to moderate capital expenditure appetites; however, EU structural funds and multinational contract work are likely to close the gap, unlocking the next growth frontier for the Europe 3D printing market.

Regulatory Landscape

The regulatory environment for additive manufacturing in Europe is being shaped mainly through EU-wide product safety, sector certification, and standards harmonization, rather than AM-only legislation. Implementing Decision (EU) 2026/901, adopted on 17 April 2026, updates European safety standards to align with the EU General Product Safety framework under Regulation (EU) 2023/988. This places greater emphasis on documented safety and traceability for products that can be produced via distributed and digitalized manufacturing workflows.

For standardization, CEN/TC 438 is the core European technical committee for additive manufacturing standards, supporting cross-border qualification approaches across polymers and metals. The S-AM project (European standardisation for additive manufacturing) entered its four-year implementation phase spanning 2025 to 2029, which continues the effort on common terminology, test methods, and conformity practices. Industry bodies such as CECIMO have also called for more coordinated EU-level policy and R&D coordination for AM, reinforcing the push to reduce fragmentation in certification and quality management expectations across medical, rail, and energy end-use sectors.

Competitive Landscape

The Europe 3D printing market maintains moderate fragmentation. Incumbents such as Stratasys, EOS and Materialise integrate vertically, offering design software, printers, materials and post-processing kits in unified portfolios. EOS’s partnership with 1000 Kelvin embeds the AMAIZE AI co-pilot into its polymer systems, reducing print failures and engineering hours for aerospace customers. Materialise expands cloud build-preparation services that drive recurring revenue and lock-in across factories with mixed printer brands.

Consolidation intensifies: Nano Dimension agreed to acquire Desktop Metal to combine printed-electronics workflows with metal-binder-jet platforms, while Synopsys’ EUR 35 billion purchase of Ansys signals growing interest from simulation majors in additive-manufacturing physics models. Start-ups address white spaces, Breton scales recycled biocomposites, Catalonian labs optimize plant-derived resins and Meltio partners with K3D to route wire-laser orders around Europe. Companies able to pair sustainability credentials with regulatory compliance stand to gain share as environmental audits feed sourcing decisions throughout the Europe 3D printing market.

Regulation remains a double-edged sword. EU MDR favors corporates with established quality-management frameworks, potentially squeezing smaller medical device service bureaus. Carbon-border rules promote local output yet raise reporting burdens. Businesses that master digital traceability, recording powder batch, energy use and dimensional inspection—demonstrate resilience and earn preferred-supplier status, cementing long-term positions in the Europe 3D printing market.

Europe 3D Printing Industry Leaders

Materialise NV

SLM Solutions Group AG

Stratasys Ltd.

3D Systems Corporation

ExOne Co.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Industrialization in regulated and high-consequence applications is opening clearer whitespace for qualified production, rather than limited prototyping, across Europe. In France, Framatome reported its 6,000 m2 Amiral Bernard-Antoine Morio de l’Isle Additive Manufacturing Center in Romans-sur-Isere as fully operational in May 2026, featuring wire arc additive manufacturing (WAAM) systems from MX3D for nuclear reactor component workflows. This plant-level deployment expands opportunities for machine OEMs, materials suppliers, inspection metrology, and post-processing providers that can meet nuclear-grade documentation and repeatability requirements.

Defense and aerospace programs are also moving additive manufacturing deeper into long-cycle supply chains, which raises demand for certified materials, stable process windows, and end-to-end digital thread capabilities. Rheinmetall UK shifted industrial 3D printing into a baseline production method for complex ducting components in the Challenger 3 programme in June 2026, while AnyShape and Materialise were selected as qualified additive manufacturing suppliers for the Eurodrone production program in May 2026. Capacity and service consolidation is also emerging as a scaling route, with the May 2026 merger of Sculpteo and 3D Prod creating a combined operation with more than 8,000 m2 of production space and 78 industrial 3D printers, supporting buyers that prefer manufacturing-as-a-service procurement across polymer and metal technologies. CECIMO-led AM-Europe (launched June 2026) and Addliance’s AMin4Y roadmap (launched May 2026) further highlight the need for shared certification practices, data management, and interoperable standards for cross-border production networks.

Recent Industry Developments

- June 2026: Stratasys launched FDM PA6/66-GF30-FR, a rail-certified flame-retardant composite material for Fortus 450mc and F900 systems. The release strengthens additive manufacturing qualification in transportation where fire, smoke, and toxicity requirements can limit deployment, and it helps service bureaus standardize offerings around certified material sets.

- April 2026: 3D Systems secured Class IIa EU MDR certification for the NextDent Jetted Denture Solution, covering materials and the NextDent 300 MultiJet printer, enabling EU commercial launch from May 4, 2026. The certification reduces commercialization friction for dental production workflows and reinforces the role of MDR-aligned, end-to-end validated solutions in European healthcare adoption.

- May 2025: Catalan researchers debuted plant-based resins compatible with DLP and SLA workflows. The work adds to the sustainable materials pipeline for photopolymer printing and supports efforts to reduce reliance on conventional fossil-derived resin chemistries in prototyping and low-volume production.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this market, we size the revenue generated from 3D printing in Europe, covering printers and related services, where additive processes are used to create parts, prototypes, and tooling across industrial and professional use.

Scope exclusions: The sizing excludes conventional subtractive manufacturing equipment, general machining services, and non-additive prototyping methods that do not involve layer-by-layer fabrication.

Segmentation Overview

- By Component

- Hardware

- Services

- By Technology

- Stereolithography (SLA)

- Fused Deposition Modeling (FDM)

- Selective Laser Sintering (SLS)

- Electron Beam Melting (EBM)

- Digital Light Processing (DLP)

- Other Technologies

- By Material

- Polymers

- Metals and Alloys

- Ceramics

- Composites and Others

- By End-user Industry

- Automotive

- Aerospace and Defense

- Healthcare

- Construction and Architecture

- Energy and Utilities

- Food and Beverage

- Other Industries

- By Country

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the fact base and to keep assumptions realistic across Europe. We rely on public, non-paywalled sources such as Eurostat industrial statistics and trade tables, the European Patent Office patent publications, OECD indicators, and selected standards and guidance notes from bodies such as ISO and CEN that describe additive manufacturing terms and processes.

Alongside these, we review company annual reports, investor presentations, and press releases to understand product launches, installed base signals, and service mix shifts. Where needed, our team also uses paid subscription sources for company financials and news screening, plus a paid patent database and a shipment-level trade database to sanity-check import and export direction for relevant materials and equipment. These examples are illustrative, and many other sources were also referred to for data collection, validation, and clarification during the study.

Primary Interviews and Surveys

Primary work is used to test what desk research cannot confirm cleanly, especially pricing movement, utilization trends, and how quickly services are replacing in-house printing for some buyers. We interviewed and surveyed a mix of printer makers, material suppliers, service bureaus, distributors, and end users across key European countries, and then used the feedback to tune assumptions and resolve conflicting signals.

These discussions also helped us confirm adoption pace by end-use, typical buying cycles, and the share of demand tied to regulated uses such as aerospace and medical manufacturing, where qualification timelines can shift revenue recognition.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 15% | |

| Mid tier: 55% | Functional/Unit leaders: 32% | |

| Smaller Players: 16% | Managers: 53% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs the Europe demand pool using manufacturing output signals, additive adoption rates by key end-use industries, and mix splits between equipment and services, which are then translated into revenue using observed price bands. Once the first-cut totals are formed, they are cross-checked with selective bottom-up approximations like sampled printer shipments times typical average selling prices, service bureau revenue range checks, and channel feedback for major countries, and then adjusted where gaps show up.

Inputs used in the model include printer installation trends, service bureau capacity utilization, material consumption direction (polymers versus metals), average selling price movement by printer class, and end-use demand indicators from industries such as aerospace and defense, automotive, healthcare, and construction. For forecasting, scenario analysis is used so that slower qualification cycles, faster service outsourcing, or faster industrialization of metal printing can be reflected transparently, and the scenario weights are aligned to what primary respondents said is most likely over the next few years. Where bottom-up checks cannot cover smaller markets or niche applications, proxy ratios from similar countries and conservative penetration steps are applied, and then revalidated with expert feedback.

Data Validation & Update Cycle

Validation is done through a simple triangulation routine where model outputs are compared against independent signals like trade direction, disclosed revenue ranges, and country-level adoption commentary from industry bodies, and then reviewed for mismatched growth rates or sudden share jumps. If an anomaly is found, the underlying driver is traced back to one assumption at a time (price, volume, mix, or timing), and follow-up calls are triggered when a single fix cannot explain the variance.

Before sign-off, the work is reviewed in multiple steps so that the logic, units, and currency handling stay consistent across countries and segments. Reports are refreshed annually, and interim updates are made when material events occur, such as a major regulatory change, a large capacity addition, or an abrupt pricing shift. Right before delivery, an analyst does a fresh pass so clients receive the latest updated view.

Mordor Intelligence's Europe 3d Printing Market Estimate Compared With Other Published Estimates

Published market sizes for Europe 3D printing often do not match because firms count different revenue streams, anchor on different base years, and apply different pricing and adoption assumptions. Differences also come from how services are treated, since some studies lean heavily on hardware shipments while others expand the scope to include broader software and service revenue.

The main gap drivers in this market are whether service bureau revenue is counted only when it is directly tied to additive part production, how metal printing uptake is timed in regulated industries, and how currency conversion timing is handled across European countries. Another recurring source of spread is refresh cadence, because fast-moving printer pricing and service mix changes can shift a one-year estimate meaningfully when older assumptions are left untouched.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.84 B (2025) | |

| Industry Research Publisher A | USD 6.27 B (2023) | Uses an earlier base year and a component split that can shift revenue recognition toward hardware, which can understate the service share when outsourcing rises. |

| Research Marketplace B | USD 5.32 B (2024) | Reported for a different base year and can reflect a narrower counted revenue set, where some software and service revenues are not consistently captured across all European countries. |

The table shows that timing and what gets counted as core 3D printing revenue explain most of the spread, especially around services and the pace of metal printing commercialization. By keeping assumptions tied to adoption by end-use and checking totals against shipment and pricing signals, the estimate stays repeatable and easier to audit, which is a modeling choice applied by Mordor Intelligence.

Key Questions Answered in the Report

How big is the Europe 3D printing market today?

The market was valued at USD 7.78 billion in 2026 and is forecast to reach USD 14.84 billion by 2031, supported by a 13.8% CAGR.

Which segment is growing fastest within European additive manufacturing?

Services, encompassing design, production outsourcing and post-processing, is expanding at 15.97% CAGR as firms opt for manufacturing-as-a-service over equipment ownership.

Why is the Netherlands outperforming other countries in European 3D-printing adoption?

The Netherlands combines maritime applications, logistics infrastructure and strong innovation funding to post a 14.95% CAGR to 2031.

What materials are gaining share in European additive manufacturing?

Metal powders are the breakout, registering a 15.21% CAGR as costs fall and recycling technologies extend powder life cycles.

How is regulation shaping medical 3D-printing growth in Europe?

Clearer pathways from the European Medicines Agency and the EU Medical Device Regulation support on-site hospital printing while requiring robust quality systems.

Page last updated on: