Fused Deposition Modeling (FDM) Technology 3D Printer Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

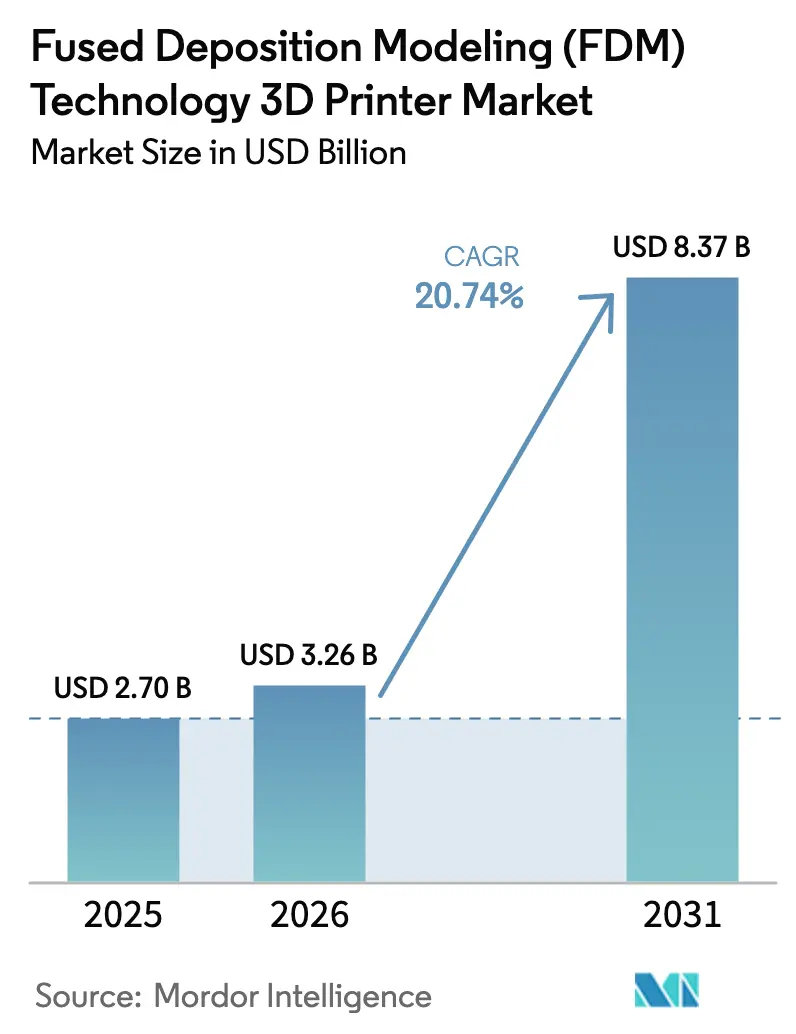

| Market Size (2026) | USD 3.26 Billion |

| Market Size (2031) | USD 8.37 Billion |

| Growth Rate (2026 - 2031) | 20.74% CAGR |

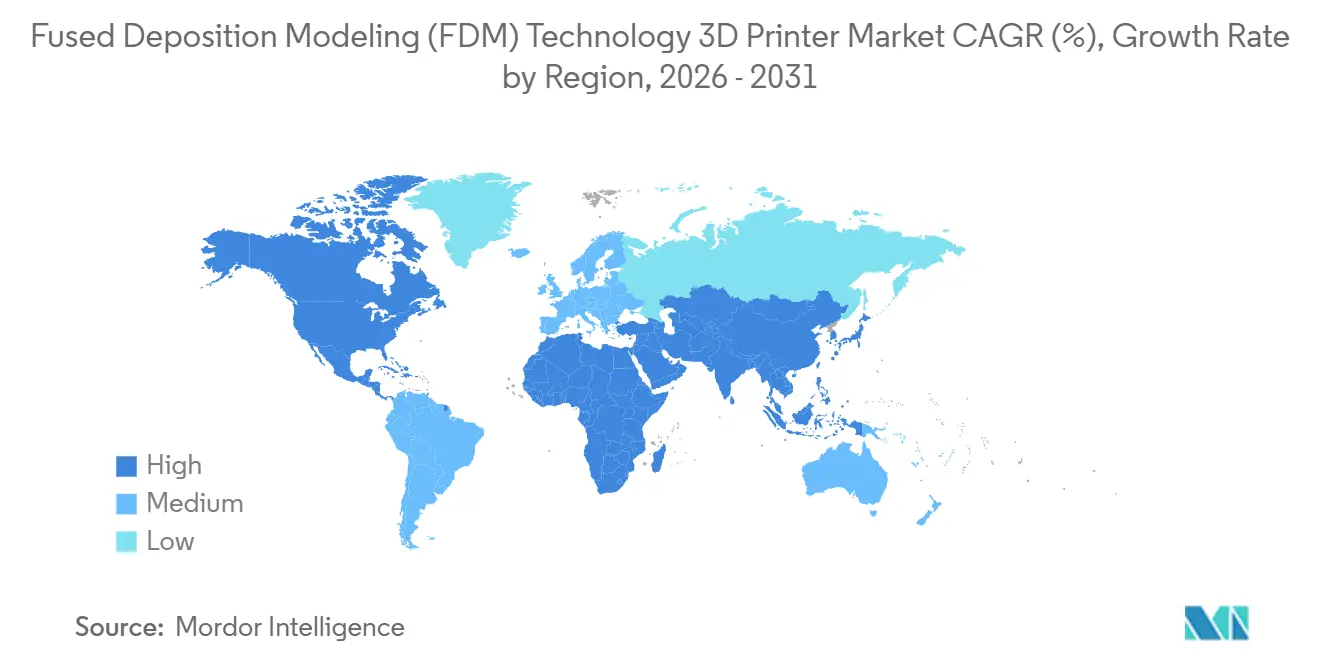

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

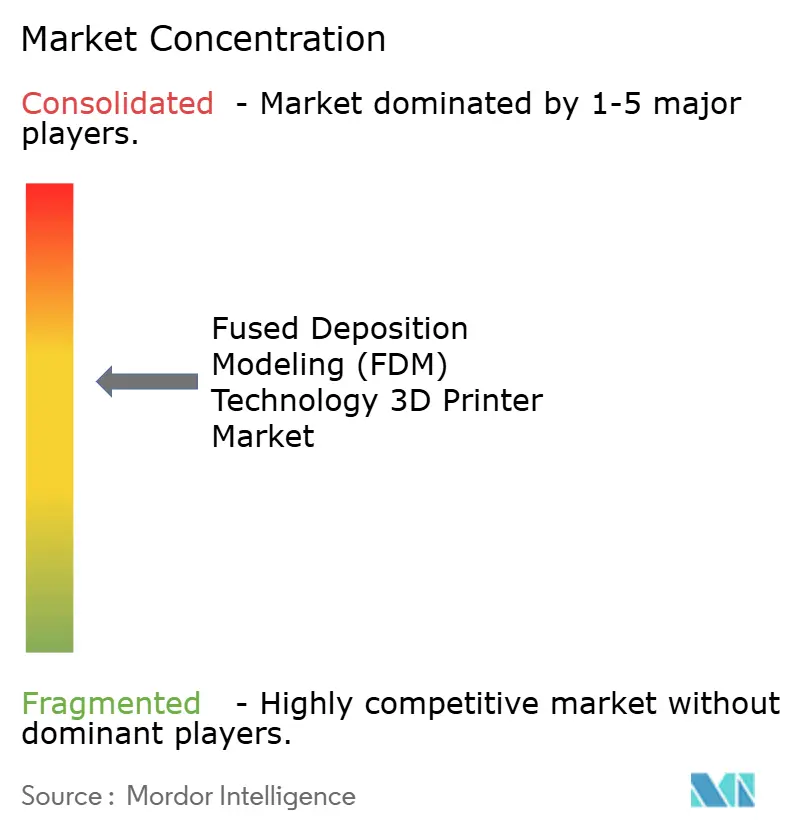

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fused Deposition Modeling (FDM) Technology 3D Printer Market Analysis by Mordor Intelligence

The fused deposition modeling 3d printer market size was valued at USD 2.7 billion in 2025 and estimated to grow from USD 3.26 billion in 2026 to reach USD 8.37 billion by 2031, at a CAGR of 20.74% during the forecast period (2026-2031). Demand is rising as the technology shifts from prototype-only use to serial production of lightweight, function-critical parts across aerospace, automotive, and healthcare settings. Declining prices for engineering-grade thermoplastics, wider availability of composite-filled filaments, and the expansion of distributed manufacturing networks are together pushing adoption closer to end users. North American programs that support on-shoring of defense and space components, combined with Asia’s push for fast consumer-electronics prototyping, reinforce the growth trajectory. At the same time, artificial-intelligence-enabled process monitoring is improving consistency, encouraging buyers to migrate jobs once reserved for machining or molding to FDM platforms.

Key Report Takeaways

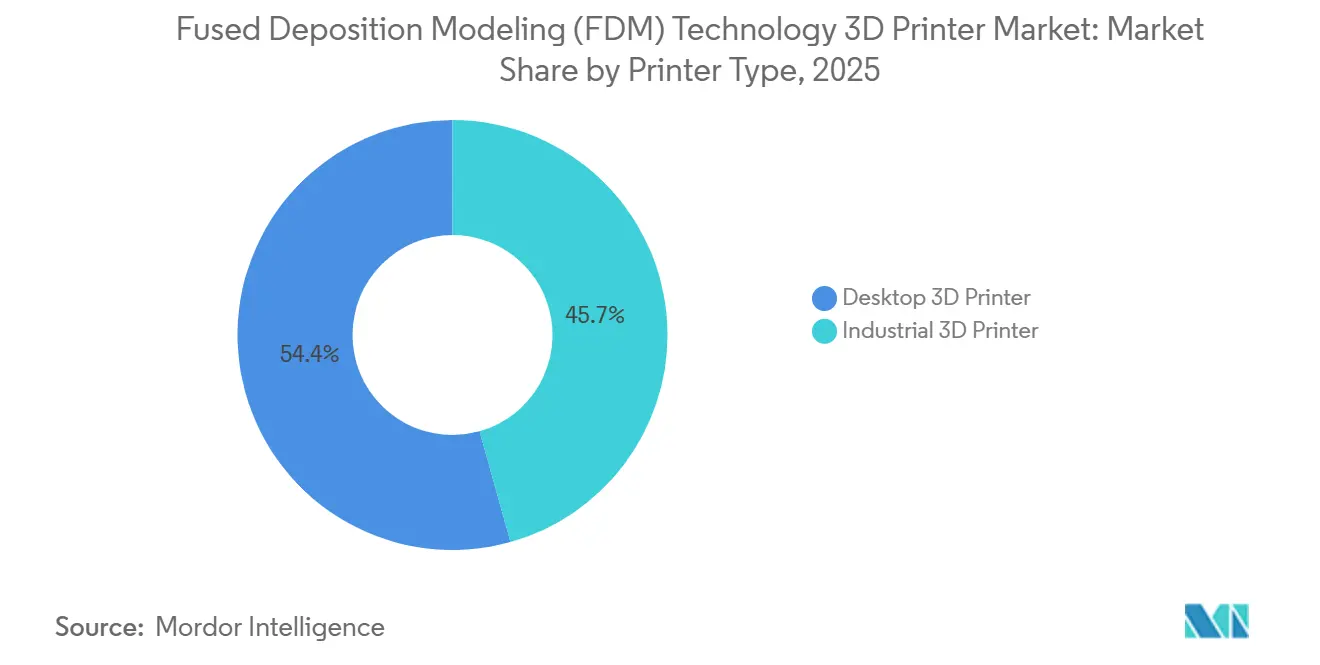

- By printer type, desktop models held 54.35% of fused deposition modeling 3d printer market share in 2025, while industrial systems are projected to expand at a 21.25% CAGR to 2031.

- By material, standard thermoplastics captured 59.25% of revenue in 2025; composite filaments are on track to grow at a 21.37% CAGR through 2031.

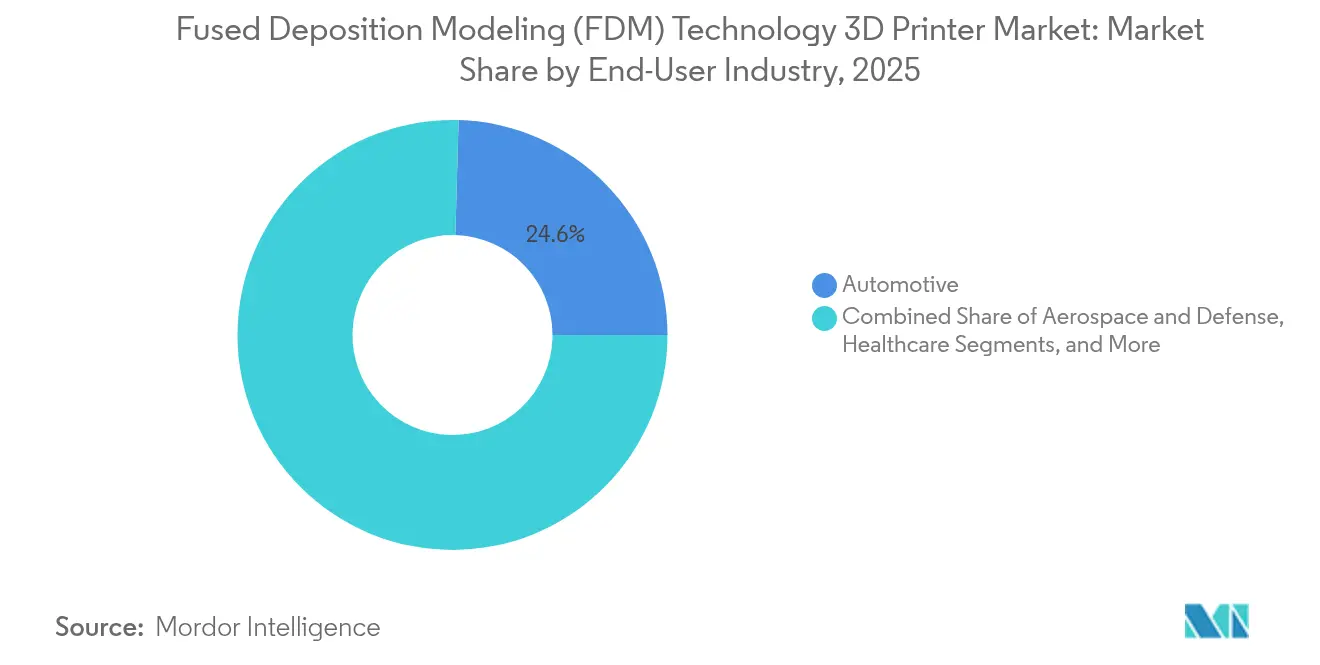

- By end-user industry, automotive led with 24.55% fused deposition modeling 3d printer market share in 2025, while healthcare applications are poised to grow at a 19.62% CAGR to 2031.

- By component, hardware commanded 81.05% of the fused deposition modeling 3d printer market size in 2025; services are advancing at a 22.38% CAGR through 2031.

- By application, prototyping represented 47.75% of sales in 2025, whereas end-use parts are expected to grow at a 23.28% CAGR through 2031.

- By price range, entry level segment commanded 66.10% share in 2025, while Professional segment is set to grow at 18.95% CAGR.

- By geography, North America accounted for 36.85% of revenue in 2025; Asia is set to register the fastest 19.78% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fused Deposition Modeling (FDM) Technology 3D Printer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adoption of High-Performance Engineering Thermoplastics by Aerospace and Defense OEMs in North America | +5.80% | North America, with spillover effects in Europe | Medium term (2-4 years) |

| Surge in Demand for Rapid, Low-Cost Prototyping among Asian Consumer-Electronics Brands | +4.70% | Asia, particularly China, Japan, and South Korea | Short term (≤ 2 years) |

| Rising Hospital Spend on Patient-Specific Surgical Models across Europe | +3.90% | Europe, with initial concentration in Germany, UK, and France | Medium term (2-4 years) |

| Localization of Automotive Tooling in South America Using FDM Systems | +3.20% | South America, primarily Brazil and Argentina | Medium term (2-4 years) |

| Integration of AI and Machine Learning for Print Optimization and Quality Control | +2.90% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Emergence of Bio-Based/Recycled Filaments Enhancing Sustainability Credentials in Oceania | +2.60% | Oceania, with adoption spreading to Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High-Performance Thermoplastics Propel Aerospace Adoption

The uptake of PEEK, PEKK, and carbon-fiber-reinforced nylon is enabling certified, lightweight cabin and engine components that lower airframe weight by up to 30%, cutting fuel costs [1]INTAMSYS, “3D Printing Composite Materials,” intamsys.com. Planned investment by North American OEMs is rising from USD 714.5 million in 2017 to more than USD 3 billion in 2025, indicating a decisive pivot toward additive serial production.

Asian Electronics Brands Accelerate Iteration Cycles

Chinese, Japanese, and South Korean firms now deploy fleets of desktop FDM units on design floors to slash enclosure and connector prototype times by 60% and costs by 80%, compressing product-launch windows in intensely competitive markets.

European Hospitals Embrace Patient-Specific Models

Surgeons across Germany, the United Kingdom, and France use anatomical FDM prints to rehearse procedures, cutting operating-room minutes by 25% and enhancing outcomes, with the regional healthcare 3D printing market forecast to reach USD 8.36 billion by 2032.

South American Tooling Moves In-House

In a move to bolster supply-chain resilience, automakers in Brazil and Argentina have begun fabricating production jigs in-house. This approach has significantly reduced reliance on external suppliers, slashing external tooling expenses by as much as 90%. Additionally, it has streamlined operations by cutting lead times by 50%, enabling faster production cycles. By adopting in-plant fabrication, these automakers are not only achieving cost efficiency but also enhancing their ability to respond swiftly to market demands and potential disruptions in the supply chain.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Warping and dimensional-accuracy limits for tight-tolerance parts | −3.6% | Global; highest in aerospace and precision machining | Medium term (2-4 years) |

| Lack of harmonized certification for flight-ready FDM parts | −3.2% | North America, Europe | Medium term (2-4 years) |

| Dependence on imported high-grade pellets | −2.8% | Middle East, Africa | Long term (≥4 years) |

| Vat-photopolymerization competition in dental applications | −2.4% | Developed markets worldwide | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Dimensional-Accuracy Constraints Limit Penetration

Dimensional accuracy and warping issues continue to constrain FDM adoption in high-precision industrial applications, particularly in aerospace and medical device manufacturing. FDM typically achieves tolerances of ±0.5% (lower limit: ±0.5 mm), which falls short of the precision offered by competing technologies like SLA and SLS, limiting its application in components requiring tight tolerances.

Certification Gaps Stall Flight Hardware

Cross-industry efforts, spearheaded by ANSI, are working to codify design-for-additive guidelines. This initiative has gained importance as the absence of unified material-process standards continues to hinder the qualification of FDM (Fused Deposition Modeling) flight components. The lack of standardization creates challenges in ensuring consistency, reliability, and compliance with industry requirements, which are critical for aerospace applications. By establishing these guidelines, the industry aims to streamline the qualification process, enhance collaboration, and promote the broader adoption of additive manufacturing technologies in the aerospace sector.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Printer Type: Industrial Systems Gaining Momentum

The industrial-system slice of the fused deposition modeling 3d printer market is expected to post a 21.25% CAGR, outpacing desktop units that nonetheless held 54.35% fused deposition modeling 3d printer market share in 2025. Smaller build volumes and sub-USD 1,000 price points keep desktops dominant in schools and design studios.

Industrial machines equipped with enclosed chambers, actively heated print zones, and dual high-temperature extruders now run PEEK and PEKK continuously, pushing FDM into safety-critical aerospace ducting and automotive under-hood brackets. Vision Miner’s 22 IDEX platform typifies the push toward automation-ready additive cells with integrated material tracking and predictive maintenance. Manufacturers value reduced changeover times and higher first-time-right part rates, cementing long-term fleet upgrades.

By Material Type: Composites Redefine Performance Boundaries

Standard thermoplastics such as PLA, ABS, and PETG account for 59.25% of revenue, anchored by low cost and plug-and-play usability. The segment still attracts new users, especially in academia and maker communities, ensuring baseline demand for entry-level systems.

Composite-filled filaments are the main growth lever, expanding at 21.37% CAGR. Carbon-fiber-reinforced PLA now reaches tensile strengths of 56.1 MPa, closing the gap with injection-molded engineering plastics . Continuous development of chopped-fiber blends for high-temperature tools and end-use parts keeps material suppliers and printer OEMs in close codevelopment cycles, an advantage that incumbents leverage for stickier customer relationships.

By Component: Services Ecosystem Expands

Hardware sales contributed 81.05% to fused deposition modeling 3d printer market size in 2025. Modular gantry designs, auto bed-leveling, and nozzle swapping systems improve uptime in production cells.

Service revenue is forecast to climb 22.38% annually as companies outsource design-for-additive optimization, pilot runs, and post-processing advisory. Tier-one suppliers lacking in-house additive expertise turn to specialists for material selection and parameter tuning. This consulting pull-through strengthens long-term consumables revenue for leading OEMs, reflecting the transition from product to platform economics.

By Application: End-Use Parts Drive Future Growth

Prototyping accounted for 47.75% of 2025 spending; however, end-use parts are on a 23.28% CAGR trajectory. OEMs are shifting low-volume service components and legacy spares to additive to avoid tooling costs. Automotive sheet-metal plants now print custom cutting guides that meet tolerance windows while cutting tool costs by 90%.

Decision makers weigh total landed cost, including inventory holding and obsolescence risk, when approving additive routes. As AI-driven monitoring predicts surface roughness in real time, first-time-right rates improve, accelerating the migration of higher-value parts into the fused deposition modeling 3d printer market.

By End-User Industry: Healthcare Applications Accelerate

Automotive remained top contributor at 24.55% revenue in 2025, supported by an entrenched culture of rapid iteration and lightweighting goals in electric drivetrains.

Hospitals and device makers are the fastest risers, logging a 19.62% CAGR on patient-specific surgical guides, cranial implants, and anatomical teaching aids. A systematic spine-surgery review covering 2,088 patients linked printed guides to reduced complication rates. Expanding biocompatible materials pipelines and on-site print labs shorten lead times and unlock procedure-specific reimbursement models.

By Price Range: Professional Segment Expands

Entry-level printers priced below USD 1,000 represented 66.10% of unit shipments in 2025 as education and hobby markets widened. Nevertheless, professional-grade systems above USD 10,000 are forecast to record a 18.95% CAGR to 2031, reflecting enterprises’ willingness to pay for industrial reliability and larger build envelopes.

Composite-capable printers such as Stratasys’s F123CR series combine heated chambers and hardened nozzles to address production tooling demands, further accelerating the upgrade cycle among high-value manufacturers.

Geography Analysis

North America captured 36.85% of global revenue in 2025 as concentrated aerospace and defense clusters adopt high-temperature FDM for non-critical flight hardware and cabin interiors. Federal agencies such as NASA validate printing processes in microgravity, reinforcing industrial confidence and speeding standards development. Canada's medical-device firms and Mexico’s vehicle assemblers add incremental demand, supported by cross-border supply-chain integration.

Asia is the fastest-growing territory, registering a 19.78% CAGR to 2031. China’s “Made in China 2025” program channels grants into domestic printer OEMs, while Japan and South Korea pursue high-precision consumer-electronics prototyping. India’s additive policy aims to expand domestic capability from prosthetics to aerospace tooling, feeding localized manufacturing needs in a price-sensitive environment. Government-backed skill-development centers further reduce adoption barriers.

Europe remains a mature yet innovative market. German automotive suppliers deploy composite-ready FDM lines to cut tooling weight, while British and French hospitals install on-site labs for patient-specific models. Policy incentives that tax landfill usage promote recycled-filament adoption, aligning with the European Green Deal.

Latin American interest centers on automotive and agricultural equipment tooling in Brazil and Argentina. Local universities transfer process-optimization research into factory settings, trimming dependence on imported fixtures. The Middle East and Africa show modest uptake, constrained by imported pellet costs and limited service bureaux, though energy-sector operators trial FDM for on-site maintenance parts to mitigate long-lead international logistics.

Competitive Landscape

The fused deposition modeling 3d printer market is moderately fragmented. Stratasys and 3D Systems hold legacy patents and extensive installed bases, yet face agile challengers from Asia and specialized composite-printer startups. Stratasys reported Q1 2025 revenue of USD 136.0 million, with 7% sequential growth in consumables, reflecting stronger fleet utilization [3]Stratasys Ltd., “Form 6-K Q1 2025,” stratasys.com.

Strategically, incumbents deepen vertical integration into filament development to lock in recurring margins, while horizontal moves, such as Vision Miner’s high-temperature printer launch, target underserved industrial niches. Partnerships with software analytics firms embed digital twin capabilities, enabling real-time feedback loops. Startups such as Bambu Lab court first-time users with automated calibration and cloud ecosystems that flatten the learning curve. The American National Standards Institute’s additive manufacturing gap survey signals collaborative efforts to harmonize design rules, a prerequisite for broader aerospace certification.

White-space opportunities include function-specific filaments, antimicrobial medical-grade materials, ESD-safe electronic housings, and ultra-high-temperature resins for hypersonic testing. Vendors capable of packaging material, hardware, and software into validated workflows will capture premium margins as buyers shift toward outcome-based procurement models.

Fused Deposition Modeling (FDM) Technology 3D Printer Industry Leaders

Stratasys Ltd.

3D Systems Corporation

Markforged Holding Corp.

Ultimaker BV

Desktop Metal, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Stratasys raised its 2025 revenue outlook to USD 570–585 million and highlighted aerospace and automotive as priority verticals.

- May 2025: Vision Miner launched the 22 IDEX high-temperature FDM system, extending its industrial solutions into aerospace and medical production.

- April 2025: NASA demonstrated live heart-tissue printing and stainless-steel deposition aboard the ISS, validating additive in microgravity.

- March 2025: Cracow University of Technology began a project to formulate biocompatible dental materials from natural feedstocks for 3D printing.

Global Fused Deposition Modeling (FDM) Technology 3D Printer Market Report Scope

Fused deposition modeling (FDM) is a prevalent 3D printing technology that constructs objects by sequentially depositing melted material. As a form of additive manufacturing, FDM operates by feeding a thermoplastic filament, commonly PLA, ABS, or PETG, into a heated nozzle, where the filament is melted.

The study tracks the revenue accrued through the sale of fused deposition modeling (FDM) technology 3d printers by various players across the globe. It also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The fused deposition modeling (FDM) technology 3D printer market is segmented by type (desktop 3D printer and industrial 3D printer), end-user industry (automotive, aerospace & defense, healthcare, consumer electronics, industrial machines, and others), and geography (North America, Europe, Asia Pacific, Middle East and Africa, and Latin America). The market sizes and forecasts regarding value (USD) for all the above segments are provided.

| Desktop 3D Printer |

| Industrial 3D Printer |

| Standard Thermoplastics (PLA, ABS, PETG) |

| Engineering-Grade Thermoplastics (Nylon, PC, PEEK, PEKK) |

| Composite-Filled Filaments (Carbon, Glass, Kevlar) |

| Bio-Derived and Recycled Filaments |

| Hardware |

| Software |

| Services |

| Prototyping |

| Tooling and Fixtures |

| End-Use Functional Parts |

| Education and Research Models |

| Automotive |

| Aerospace and Defense |

| Healthcare |

| Consumer Electronics |

| Industrial Machinery |

| Education |

| Others |

| Entry-Level (< USD 1,000) |

| Mid-Range (USD 1,000 - 10,000) |

| Professional (> USD 10,000) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Printer Type | Desktop 3D Printer | |

| Industrial 3D Printer | ||

| By Material Type | Standard Thermoplastics (PLA, ABS, PETG) | |

| Engineering-Grade Thermoplastics (Nylon, PC, PEEK, PEKK) | ||

| Composite-Filled Filaments (Carbon, Glass, Kevlar) | ||

| Bio-Derived and Recycled Filaments | ||

| By Component | Hardware | |

| Software | ||

| Services | ||

| By Application | Prototyping | |

| Tooling and Fixtures | ||

| End-Use Functional Parts | ||

| Education and Research Models | ||

| By End-User Industry | Automotive | |

| Aerospace and Defense | ||

| Healthcare | ||

| Consumer Electronics | ||

| Industrial Machinery | ||

| Education | ||

| Others | ||

| By Price Range | Entry-Level (< USD 1,000) | |

| Mid-Range (USD 1,000 - 10,000) | ||

| Professional (> USD 10,000) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current fused deposition modeling 3d printer market size?

The fused deposition modeling 3d printer market is valued at USD 3.26 billion in 2026 and is projected to reach USD 8.37 billion by 2031.

Which region is growing the fastest?

Asia is forecast to post a 19.78% CAGR through 2031, driven by electronics prototyping demand and manufacturing policy incentives.

Why are composite filaments important?

Composite-filled materials such as carbon-fiber PLA elevate tensile strength by more than 20%, enabling end-use parts that previously required metal or machined plastics.

How are hospitals using FDM printers?

European hospitals create patient-specific surgical models that cut operating times by 25% and improve procedural accuracy.

Page last updated on: