Dimethyl Terephthalate (DMT) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

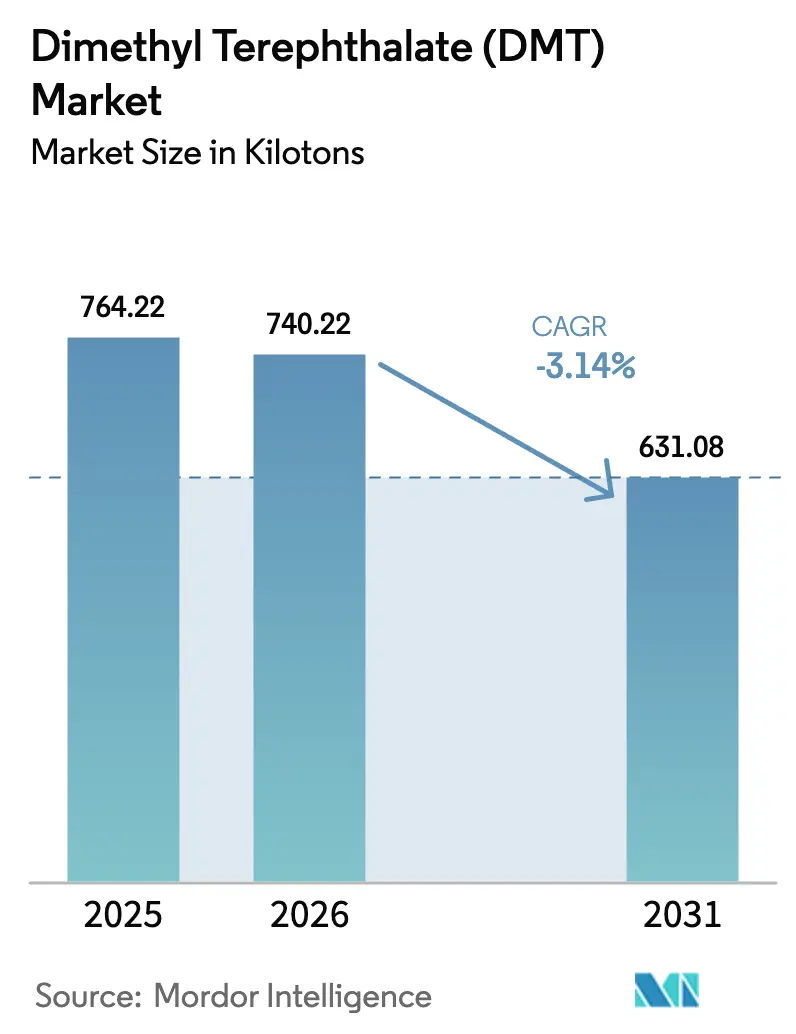

| Market Volume (2026) | 740.22 kilotons |

| Market Volume (2031) | 631.08 kilotons |

| Growth Rate (2026 - 2031) | -3.14% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dimethyl Terephthalate (DMT) Market Analysis by Mordor Intelligence

The Dimethyl Terephthalate Market size is expected to decline from 764.22 kilotons in 2025 to 740.22 kilotons in 2026 and is forecast to reach 631.08 kilotons by 2031 at -3.14% CAGR over 2026-2031. High operating costs in Europe, the commissioning of mega-scale PTA units in China, and volatile methanol prices continue to erode demand, yet chemical-recycling investments and niche copolymer applications keep a floor under volume loss. Asia-Pacific remains the largest demand center, North America pivots toward circular DMT via methanolysis, and Europe searches for competitiveness through low-carbon energy and possible CBAM protection. Competitive intensity is moderate as legacy plants close, integrated polyester chains consolidate, and innovators channel capital into recycled or bio-attributed intermediates. As a result, the dimethyl terephthalate market navigates a dual narrative of structural decline in virgin demand and selective resilience in circular value chains.

Key Report Takeaways

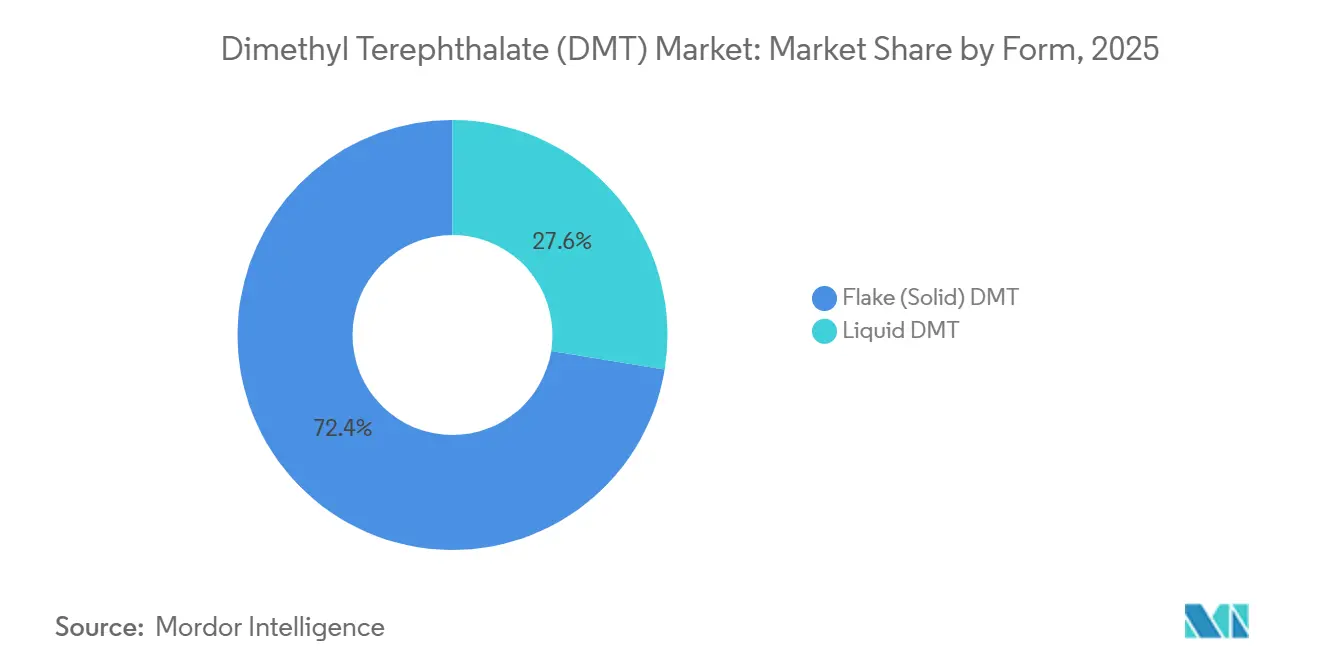

- By form, flake solid captured 72.44% of dimethyl terephthalate market share in 2025 and is contracting at a –2.43% CAGR through 2031.

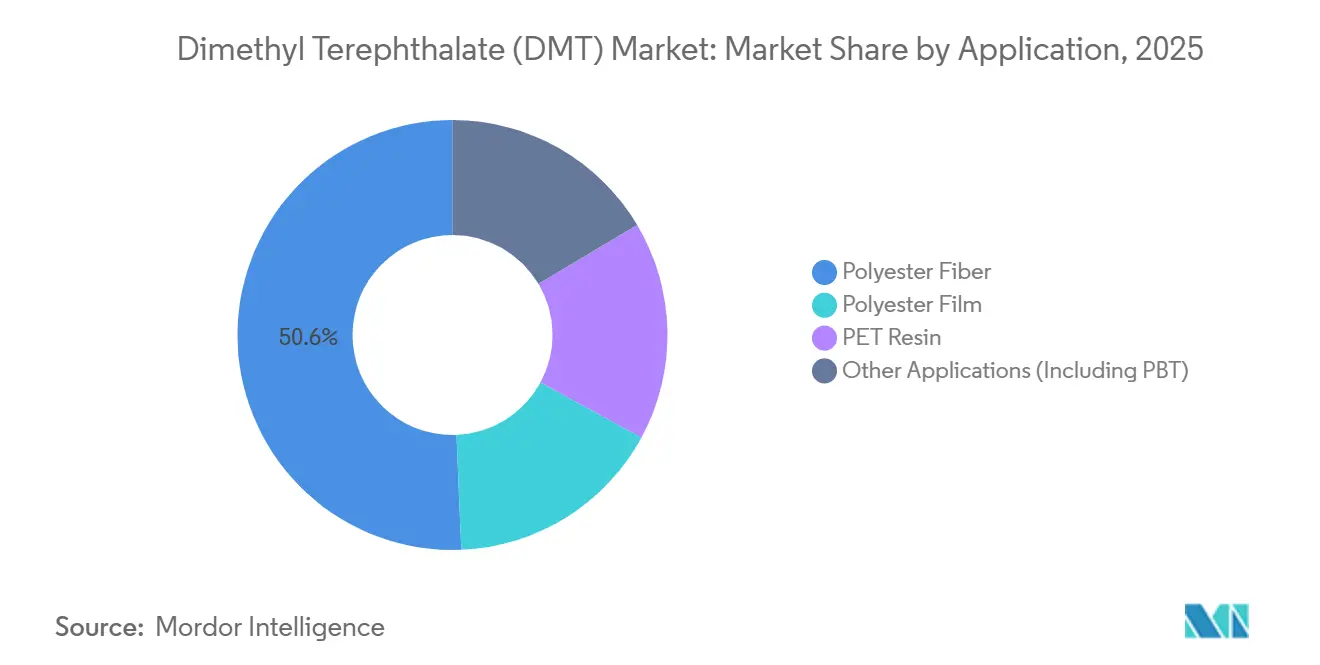

- By application, polyester fiber held 50.65% of the dimethyl terephthalate market size in 2025, while PET resin records the least negative CAGR at -1.95% through 2031.

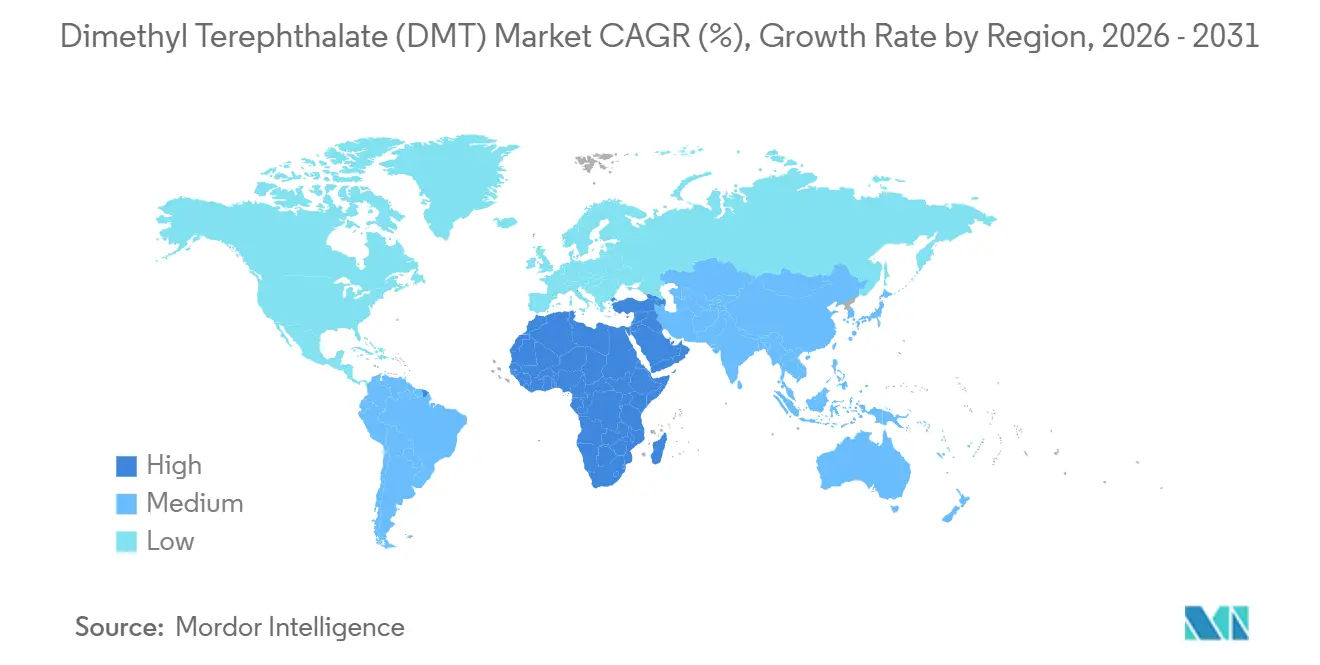

- By geography, Asia-Pacific retained 51.85% revenue share of the dimethyl terephthalate market in 2025; the Middle East and Africa represents the least negative regional trajectory at –1.72% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Dimethyl Terephthalate (DMT) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PET and PBT Demand Resurgence | +0.8% | Asia-Pacific, North America | Medium term (2-4 years) |

| Polyester-Fibre Consumption in Asia | +0.6% | Asia-Pacific (China, India, ASEAN) | Short term (≤ 2 years) |

| Packaging-Light-Weighting Initiatives | +0.4% | Global, with leadership in North America and EU | Medium term (2-4 years) |

| Chemical-Recycling Routes Supplying r-DMT | +0.5% | North America, Europe, spill-over to Asia-Pacific | Long term (≥ 4 years) |

| EU Carbon-Border-Pricing Favouring Local DMT | +0.3% | Europe, indirect effects on Asia-Pacific exports | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

PET and PBT Demand Resurgence

PET packaging demand is stabilizing as brand owners adopt circular-content targets, while PBT gains volume in automotive connectors that require flame-retardant precision molding. Eastman’s partnership with Rumpke guarantees 100% of opaque and colored PET waste as feedstock for its Kingsport molecular-recycling unit, exemplifying how circular loops underpin PET stability. Incremental PET growth partially offsets resin intensity lost to lightweighting, preserving feedstock pull for DMT-based intermediates in specialty films. In tandem, PBT’s specification wins in electric-vehicle architectures create niche opportunities for DMT copolymer chemistry. Together, these trends add a modest 0.8 percentage-point uplift to the dimethyl terephthalate market CAGR.

Polyester-Fiber Consumption in Asia

China’s polyester plants ran at 90% utilization in May 2025 as apparel exports rebounded, while India and ASEAN nations ramped spinning capacity to capture near-shoring orders. Smaller trans-esterification units in these regions still rely on DMT because retrofit capital for PTA direct-esterification is scarce. Nevertheless, headline PTA mega-projects under construction in Jiangsu, Zhejiang, and Fujian will widen the cost gap, steadily siphoning feedstock away from DMT. The dichotomy between high-volume PTA fiber and DMT’s foothold in smaller mills results in a 0.6 percentage-point CAGR cushion that is unlikely to reverse the long-run decline.

Packaging Lightweighting Initiatives

Global brand owners cut average PET bottle weight and boost recycled content, a move that trims absolute resin demand yet raises quality specifications. Molecular-recycling platforms that revert post-consumer PET to monomers supply virgin-grade polymer meeting food-contact standards, sustaining demand for r-DMT intermediates. Eastman’s Normandy facility secured offtake covering 80% of Phase 1 capacity before mechanical completion, validating market appetite for circular feedstock. Lightweighting therefore shifts the revenue mix towards value-added recycled DMT rather than virgin tonnage, delivering a 0.4 percentage-point positive impact on the dimethyl terephthalate market trajectory.

Chemical-Recycling Routes Supplying r-DMT

Methanolysis converts waste polyester to dimethyl terephthalate and ethylene glycol, enabling closed-loop packaging solutions. The Kingsport plant, designed for 110 000 t per year, is forecast to add USD 75 million incremental EBITDA in 2024, and Eastman is negotiating U.S. DOE support for a similarly sized Longview unit. Teijin Frontier’s BHET catalyst offers an energy-efficient alternative, broadening geographic adoption potential. As collection networks mature, recycled DMT could displace a portion of virgin feedstock, lifting the long-term dimethyl terephthalate market growth curve by 0.5 percentage points.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost Advantage of PTA Over DMT | -2.1% | Global, most pronounced in Asia-Pacific | Short term (≤ 2 years) |

| Volatile P-Xylene and Methanol Pricing | -1.3% | Global, acute in Asia-Pacific and North America | Short term (≤ 2 years) |

| Tightened Methanol VOC Regulations | -0.6% | North America, Europe, emerging in China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cost Advantage of PTA Over DMT

Single-train PTA plants exceeding 3 million t per year deliver unbeatable unit costs, pushing DMT routes to the margin. Sinopec’s Jiangsu complex exemplifies this scale economy, while Teijin realized JPY 17.5 billion operating-income gains after mothballing internal DMT capacity. The relentless PTA cost edge removes 2.1 percentage points from the dimethyl terephthalate market CAGR despite recycled-content tailwinds.

Tightened Methanol VOC Regulations

U.S. EPA rule 40 CFR 60.112c mandates vapor-recovery systems for methanol storage, requiring multi-million-dollar retrofits. Similar policies appear in the EU Industrial Emissions Directive updates and select Chinese provinces. Compliance costs penalize smaller esterification units, encouraging consolidation into larger, emission-controlled assets. These upgrades impose a -0.6 percentage-point drag on the dimethyl terephthalate market outlook.[1]United States Environmental Protection Agency, “National Emission Standards for Storage Vessels,” epa.gov .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Solid Flake Maintains Logistics Advantage

Solid-flake product commanded 72.44% of dimethyl terephthalate market share in 2025 and is projected to shrink at a -2.43% CAGR through 2031, outperforming liquid grades. Lower vapor pressure minimizes VOC losses, and flake moves conveniently in railcars and FIBC bulk bags, reinforcing its role in smaller polyester mills that lack molten-feed systems. Liquid DMT, in contrast, incurs higher freight and safety costs, limiting uptake to integrated complexes where direct piping eliminates packaging steps. As recycled DMT capacity ramps, crystallization loops inherently yield solid output, further anchoring flake’s predominance. However, even flake volumes ultimately contract alongside PTA substitution, leaving the segment to stabilize only if methanolysis achieves scale by 2028. In that scenario, the dimethyl terephthalate market size for solid flake could plateau near 450 kilotons.

Liquid grades face steeper declines because new PTA lines eradicate adjacent molten-feed demand. Regulatory scrutiny of hot-melt storage tanks raises capex hurdles, while logistics providers seek to retire aging heated-tank fleets. Producers with dual-form capability increasingly tilt output toward flake for spot sales, relegating liquid DMT to captive polymerization back-integration. Given these dynamics, liquid’s share is expected to fall by 2031, cementing flake as the default trans-esterification feed even in a shrinking dimethyl terephthalate market.

By Application: Fiber Still Leads, Resin Decline Moderates

Polyester fiber accounted for 50.65% of the dimethyl terephthalate market in 2025, yet the segment will continue to lose ground as high-volume Chinese spinning lines favor PTA direct esterification. Smaller mills in India, Vietnam, and Pakistan, lacking retrofit capital, preserve residual DMT demand but cannot offset attrition at scale. PET resin, conversely, contracts at the slowest pace, posting a -1.95% CAGR, aided by brand commitments to circular packaging. Molecular-recycling plants using methanolysis route DMT back into bottle-grade polymer, slowing virgin-feed erosion.

Specialty polyester film and polybutylene terephthalate capture smaller volume yet present differentiated growth profiles. Film demand erodes due to polypropylene competition in flexible packaging, while PBT benefits from electrification and miniaturization trends in vehicles and consumer electronics. Although PBT adds incremental tonnage, the absolute base remains modest, limiting material impact on total dimethyl terephthalate market momentum. Ultimately, application diversification slows but does not arrest the overall contraction trajectory.

Geography Analysis

Asia-Pacific retained 51.85% of dimethyl terephthalate market share in 2025, driven by entrenched polyester fiber clusters across China, India, and Southeast Asia. Mega PTA build-outs along China’s east coast are displacing DMT feed, yet pockets of trans-esterification persist where mills operate legacy lines or consume recycled flake from domestic methanolysis pilots. India shows resilience as mid-scale players defer capital-intensive PTA retrofits, keeping an addressable DMT pool alive. Emerging recycling projects in Indonesia and Thailand could also regenerate local demand, although timelines beyond 2028 remain tentative. Collectively, these factors deliver the highest absolute volume but contribute materially to the dimethyl terephthalate market decline.

North America hosts limited virgin DMT capacity but has become the epicenter of chemical recycling, anchored by Eastman’s Kingsport and planned Longview sites. These plants convert mixed-color PET waste into r-DMT, supplying food-contact resin and specialty copolymers. Methanol supply, however, remains tight after recurring outages along the Gulf Coast, exposing operators to feedstock spikes. Canada and Mexico rely on imports, primarily from the United States and occasional Asia-Pacific spot cargoes, with logistics costs influencing arbitrage decisions.

Europe experienced the sharpest structural retreat after Indorama announced intentions to shutter its Rotterdam PTA-PET complex. Oxxynova’s German DMT plant closure in 2022 further depleted regional output. Yet Europe also pioneers regulatory levers that may eventually shield local DMT segments. The prospective CBAM expansion to organic chemicals, together with anti-dumping duties on Chinese PET, could grant residual producers a niche competitive window. Eastman’s Normandy project leverages renewable electricity and proximity to feedstock suppliers, embodying a model where European dimethyl terephthalate market participants can still thrive by combining green energy, circular feed, and specialty grades.

South America and the Middle East and Africa remain small but strategically important. Middle East PTA additions, supported by low-cost feedstock, generate modest DMT pull for specialty polyester copolymers. Africa’s nascent packaging sector imports bottle-grade resin from Gulf suppliers, occasionally sourcing DMT for local PBT compounding. Brazil, Argentina, and neighboring markets in South America lack domestic DMT assets; they depend on Asia-Pacific shipments, leaving volumes sensitive to freight swings and currency depreciation.

Competitive Landscape

Market concentration is moderate, with fewer than 10 producers controlling a majority of capacity, yet the roster is shrinking. Teijin exited internal DMT output in 2015 and reallocated capital toward PTA procurement, unlocking significant cost savings[2]Teijin Limited, “Polyester chain consolidation yields cost savings,” teijin.com . Indorama’s Rotterdam withdrawal highlights rationalization in high-cost regions, while Oxxynova’s German shutdown underscores limited standalone competitiveness. Asian conglomerates such as Sinopec have largely pivoted to PTA megaprojects, leaving only niche or captive DMT operations in place.

Eastman spearheads a recycling-centric strategy, committing more than USD 2.25 billion to three molecular-recycling lines that collectively exceed 400 000 t per year of capacity. These plants will generate r-DMT and BHET for circular polymers, targeting premium customers willing to pay for low-carbon content. Several Japanese and South Korean conglomerates explore similar depolymerization, though most remain at pilot scale.

Smaller Indian and ASEAN companies sustain regional presence by serving polyester mills that still run trans-esterification units. Their survival hinges on flexible feedstock procurement, low overheads, and selective upgrades to meet tightening VOC rules. Niche European suppliers focus on pharmaceutical-grade and high-purity DMT, leveraging stringent quality norms and short supply chains. Across the board, integration into downstream polyester or upstream methanol offers a defensive moat, as standalone merchant producers face margin compression and stricter environmental compliance.

Dimethyl Terephthalate (DMT) Industry Leaders

Eastman Chemical Company

SASA

OXXYNOVA GmbH

SK chemicals

Mogilevkhimvolokno

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Loop Industries entered into an offtake agreement with Taro Plast to supply Loop DMT (dimethyl terephthalate) from its planned Infinite Loop India facility. The Loop DMT will be utilized in automotive and specialty polymer applications, making Taro Plast the first company to incorporate this 100% recycled product into its portfolio.

- March 2024: Loop Industries and Ester Industries Ltd. announced a joint venture agreement to establish an Infinite Loop manufacturing facility in India. The facility will produce recycled dimethyl terephthalate (rDMT) using Infinite Loop technology, which provides notable advantages over traditional mechanical PET recycling methods.

Global Dimethyl Terephthalate (DMT) Market Report Scope

Dimethyl terephthalate is a diester resulting from the formal condensation of the carboxy groups of terephthalic acid with methanol. It is a primary ingredient widely used in polyesters and industrial plastics manufacture. It is a methyl ester, a diester, and a phthalate ester. It is functionally related to terephthalic acid.

The dimethyl terephthalate market is segmented by form, application, and geography. By form, the market is segmented into flake (solid) DMT and liquid DMT. By application, the market is segmented into polyester film, polyester fiber, PET resin, and other applications. The report also covers the market size and forecasts for the dimethyl terephthalate in 15 countries across major regions. For each segment, market sizing and forecasts have been done on the basis of volume (tons).

| Flake (Solid) DMT |

| Liquid DMT |

| Polyester Fiber |

| Polyester Film |

| PET Resin |

| Other Applications (Including PBT) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Form | Flake (Solid) DMT | |

| Liquid DMT | ||

| By Application | Polyester Fiber | |

| Polyester Film | ||

| PET Resin | ||

| Other Applications (Including PBT) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected global volume for dimethyl terephthalate in 2031?

The dimethyl terephthalate market size is forecast to reach 631.08 kilotons by 2031.

Which application segment is contracting the slowest?

PET resin shows the least negative trajectory at a -1.95% CAGR through 2031 as circular-packaging programs backstop demand.

Why is solid flake preferred over liquid grades?

Flake offers lower vapor pressure, simpler bulk logistics, and better compatibility with downstream polymerization, sustaining a 72.44% share in 2025.

How will EU carbon-border pricing affect producers?

A CBAM extension to organic chemicals would impose levies on high-carbon imports, potentially improving the cost position of European DMT made with renewable energy.

Page last updated on: