Naphthalene Derivatives Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.98 Billion |

| Market Size (2031) | USD 2.31 Billion |

| Growth Rate (2026 - 2031) | 3.11% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

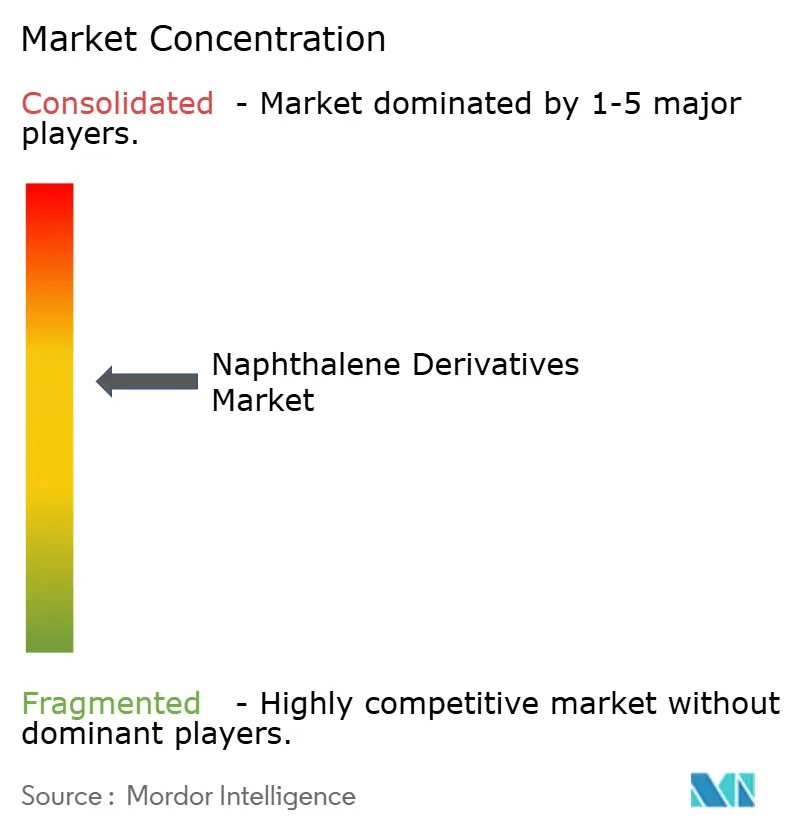

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Naphthalene Derivatives Market Analysis by Mordor Intelligence

The naphthalene derivatives market size is expected to grow from USD 1.92 billion in 2025 to USD 1.98 billion in 2026 and is forecast to reach USD 2.31 billion by 2031 at 3.11% CAGR over 2026-2031. This growth rate signals a mature but resilient landscape where sustained construction demand offsets regulatory pressures. Coal-tar dependence still dominates feedstock strategies, yet producers increasingly diversify into petroleum and renewable streams to hedge supply risk. Electronics applications, particularly battery electrolytes and graphene dispersants, now shape premium revenue pools and influence R&D priorities. At the same time, regulatory initiatives under TSCA and REACH elevate compliance costs, creating a competitive advantage for vertically integrated players that can fund emission-control upgrades while preserving market reach in Asia-Pacific, North America, and Europe. Asia-Pacific remains the volume anchor, but supply chain realignments and sustainability mandates in the West continue to nudge product portfolios toward higher-purity, higher-margin specialties across the naphthalene derivatives market.

Key Report Takeaways

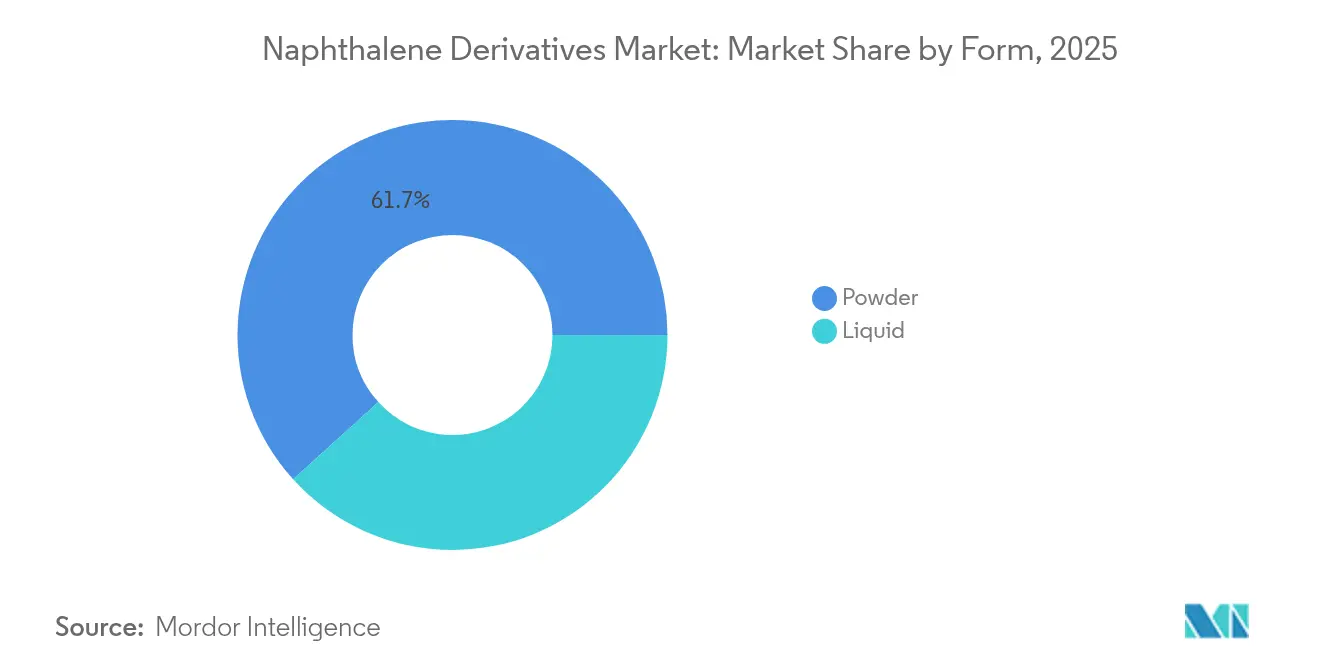

- By form, powder products accounted for 61.71% of the naphthalene derivatives market size in 2025; liquid forms are forecast to expand at 3.66% CAGR to 2031.

- By source, coal tar supplied 57.02% of the 2025 volume, but other sources are growing at 3.92% CAGR through 2031.

- By derivative, sulphonated naphthalene formaldehyde led with 43.48% of the 2025 naphthalene derivatives market share, while NDCA & high purity naphthols are projected to grow at a 3.55% CAGR through 2031.

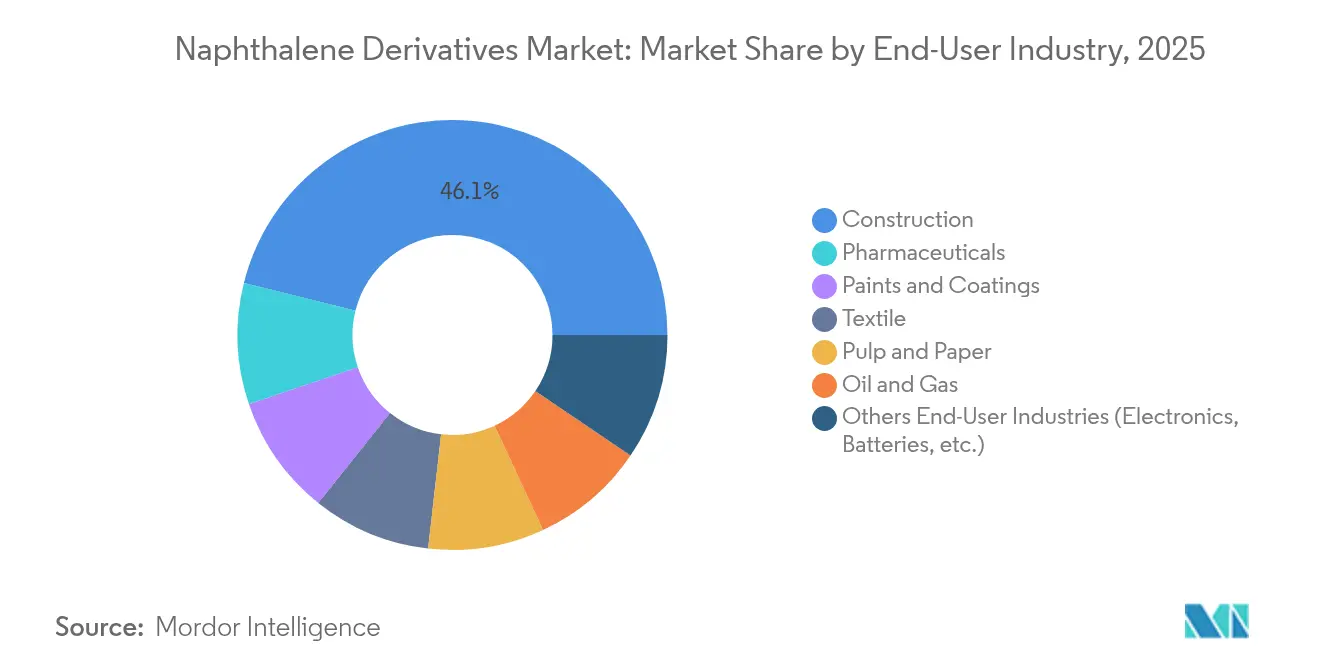

- By end-user industry, construction commanded 46.11% revenue share in 2025; electronics and batteries are expected to log the fastest 4.02% CAGR between 2026 and 2031.

- By geography, Asia-Pacific held 53.35% of the 2025 volume and is on track for a 4.06% CAGR, thanks to infrastructure programs and electronics manufacturing growth.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Naphthalene Derivatives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding construction demand for naphthalene-based super-plasticizers | +1.2% | Global, with APAC leading | Long term (≥ 4 years) |

| Rising consumption in textile dye intermediates | +0.8% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Surging demand for phthalic anhydride plasticizers | +0.6% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Growth of agrochemical wetting-agent applications | +0.4% | Global, concentrated in agricultural regions | Long term (≥ 4 years) |

| Adoption in graphene & advanced composite dispersants | +0.3% | North America & EU, early APAC adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Construction Demand for Naphthalene-Based Superplasticizers

Global infrastructure upgrades extend the life of the naphthalene derivatives market by underpinning steady SNF throughput. Field trials show SNF dosing near 0.9% combined with 20% silica fume improves compressive strength and workability in ultra-high-performance concrete. China’s stimulus packages worth more than USD 1.3 trillion steer a large share toward rail, bridge, and public-housing programs, keeping regional demand buoyant[1]American Chemical Society Staff, “Asia Builds More Aromatics Plants,” Chemical & Engineering News, cen.acs.org. Developers prefer SNF because its performance is robust under extreme temperature swings, a requirement in megaprojects across Asia and the Middle East. Stable pricing for SNF helps contractors contain budget overruns, sustaining order volumes even when other derivative categories fluctuate. Consequently, construction remains the demand floor for the naphthalene derivatives market through the decade.

Rising Consumption in Textile Dye Intermediates

Textile production rebound across South and Southeast Asia has restored the purchasing of naphthol and naphthalene sulphonic acid. India’s specialty-chemicals revenue path to USD 50 billion by 2025 feeds a growing base of high-performance dye plants that favor naphthalene-based intermediates for superior colorfastness. Despite margin pressure, consolidation among Chinese dye makers funnels output into fewer, larger facilities that value consistent supply security. Regional free-trade pacts also incentivize local sourcing, reducing exposure to ocean freight volatility. This textile-dye pull supports incremental volume on top of construction base demand, ensuring diversified growth for the naphthalene derivatives market.

Surging Demand for Phthalic Anhydride Plasticizers

Automotive lightweighting and flexible-packaging needs preserve a market for phthalic anhydride, although some traditional phthalates face regulatory headwinds. India records 7.9% annual consumption growth as downstream PVC and polyester resin plants expand capacity. On the supply side, Koppers’ plan to exit phthalic anhydride output at Stickney in mid-2025 will remove 160,000 t of annual capacity and alleviate oversupply, a shift that could firm prices for remaining producers. Bio-based phthalic anhydride routes, using iso-butyric fermentation or renewable naphtha, fetch premium margins and appeal to ESG-focused brand owners. This balance of traditional and bio-based demand sustains another leg of growth within the naphthalene derivatives market.

Growth of Agrochemical Wetting-Agent Applications

Crop-protection formulations increasingly specify alkyl naphthalene sulphonate salts to enhance spray dispersion at lower surfactant loadings. China’s agrochemical capacity additions since its 13th Five-Year Plan boost annual output by 1.2 million t and create downstream pull for dispersants. Precision-agriculture tools that reduce pesticide waste require surfactants that maintain uniform droplet size; naphthalene chemistry meets that need while showing acceptable biodegradability profiles. Export-oriented formulators in India and Brazil value the compatibility of these wetting agents with a wide pH window, limiting re-formulation work across markets. As acreage under intensive cultivation rises, agrochemical use will continue to lift the naphthalene derivatives market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Carcinogenic-toxicity regulations | -0.9% | Global, with EU and North America leading | Short term (≤ 2 years) |

| Coal-tar supply & price volatility | -0.7% | Global, particularly APAC manufacturing hubs | Medium term (2-4 years) |

| Substitution by bio-based/polycarboxylate super-plasticizers | -0.5% | Europe and North America, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Carcinogenic-Toxicity Regulations

The EU’s Revision of Annex XVII to REACH now caps polycyclic-aromatic-hydrocarbon emissions from clay targets and similar articles by April 2026, effectively mandating 99% reductions for naphthalene content. In the United States, the EPA began a formal risk evaluation of naphthalene in December 2024, broadening data-collection obligations and foreshadowing stricter workplace-exposure limits[2]U.S. Environmental Protection Agency, “Risk Evaluation for Naphthalene,” epa.gov. The CDC updated its toxicological profile, spotlighting hemolytic-anemia risk for populations with G6PD deficiency[3]Centers for Disease Control and Prevention, “Toxicological Profile for Naphthalene,” cdc.gov. Producers now budget for higher monitoring costs, engineering controls, and possible reformulations, expenses that weigh on profitability in the naphthalene derivatives market. Larger, diversified firms can absorb these costs, but smaller regional players may exit or seek mergers.

Coal-Tar Supply & Price Volatility

Steel-sector decarbonization constraints reduce coke-oven gas output, tightening coal-tar supply in China, South Korea, and parts of Europe. Spot quotes for industrial-grade naphthalene rose 18% during 2024’s second half as coking rates dipped, pushing downstream users to seek petroleum or renewable substitutes. The volatility complicates forward contracts and inventory planning. While refinery-sourced naphthalene improves supply diversity, its availability hinges on competitive aromatics margins and regional refining throughput. Feedstock uncertainty, therefore, erodes planning visibility across the naphthalene derivatives market until alternative supply streams scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Powder Dominance Reflects Handling Advantages

Powder products generated 61.71% of 2025 revenue, underscoring their logistics friendliness in high-volume applications such as concrete admixtures. Powder’s lower bulk density and moisture tolerance allow long-distance shipping without caking, an advantage for construction megaprojects that draw on imported material. Cement producers also favor dry dosing because it simplifies automated batching and reduces on-site cleanup. This entrenched preference lends stability to the naphthalene derivatives market.

Liquid derivatives, expanding at a 3.66% CAGR, satisfy niche needs in pharmaceuticals, micro-electronics and specialty coatings where exact dosing and immediate dissolution matter. Their contamination risk is lower because sealed drums prevent dust ingress that can interfere with high-purity applications. Growth in battery-electrolyte additives likewise tilts toward liquid formats, supporting gradual share gain while powder remains dominant.

By Source: Coal Tar Dependency Creates Strategic Vulnerabilities

Coal tar retained a 57.02% share of the feedstock supply in 2025, enabling economical aromatics extraction via established distillation units with coke plants. The resulting price edge sustains competitiveness for bulk SNF and phthalic-anhydride chains. However, vulnerability arises as global steel production plateaus and environmental mandates target coke ovens. Diversification into petroleum-derived streams and renewable naphtha thus ranks high on executive agendas within the naphthalene derivatives market.

Alternative sources show a 3.92% CAGR, buoyed by pilot plants converting waste cooking oil into renewable naphtha and by FCC refineries that integrate aromatic recovery. Technology vendors like Topsoe report commercial interest in circular-aromatics units co-producing benzene, toluene, xylenes, and naphthalene. Although absolute volume is low, the trajectory points to a more balanced supply mix by 2031.

By Derivative: SNF Leadership Reflects Construction Demand

Sulphonated naphthalene formaldehyde secured 43.48% derivative revenue in 2025, riding infrastructure spending across Asia-Pacific and the Middle East. Its cost-performance ratio and an extensive track record in high-strength concrete keep SNF at the center of bulk consumption. Even as polycarboxylate rivals gain attention, SNF’s ease of synthesis from commodity raw materials preserves a price moat that shields volume on the naphthalene derivatives market.

High-purity naphthols and NDCA post the quickest growth, 3.55% CAGR, as semiconductor, pharmaceutical, and agrochemical users prioritize narrow-specification products. Battery-grade 1,4-naphthoquinone and sodium-naphthalide precursors command premiums, encouraging multi-step purification investments. Phthalic-anhydride derivatives face margin compression from regulatory scrutiny on ortho-phthalates, although moves to bio-based PA could restore appeal.

By End-User Industry: Electronics Growth Signals Market Evolution

Construction continued to dominate at 46.11% of 2025 revenue, reflecting ongoing urbanization and retrofits that rely on SNF flowability enhancement. Nevertheless, electronics and batteries, growing at 4.02% CAGR, increasingly shape product-development roadmaps within the naphthalene derivatives market. Demands for ultra-low metal content and high oxidative stability push suppliers to tighten purification protocols.

Paints and coatings benefit from architectural shifts toward long-life exterior finishes, tapping NDCA and naphthalene sulphonates as dispersants that improve pigment wetting. Textile industry recovery in Southeast Asia revives demand for dye intermediates, although wastewater regulations narrow the list of acceptable facilities. Although smaller in volume, pharmaceutical synthesis delivers healthy margins for GMP-compliant naphthol grades.

Geography Analysis

Asia-Pacific generated 53.35% of global volume in 2025 and is projected to log the fastest 4.06% CAGR to 2031. Government-backed megaprojects anchor construction demand in China, India, and Indonesia, while regional consumer-electronics clusters drive specialty-grade uptake. China’s refining sector processed 14.8 million barrels daily of crude in 2024, ensuring ample aromatics feedstock. The region’s aromatics build-out, adding 11.8 million t of capacity, intensifies competition and secures raw-material availability, strengthening the naphthalene derivatives market.

North America shows a mature demand profile, with steady replacement of aging bridges and highways underpinning SNF volumes. The EPA’s ongoing risk evaluation injects compliance uncertainty, encouraging producers to invest early in emission-control technologies to safeguard access. Canada’s petrochemical corridor in Alberta explores renewable-naphtha integration that could eventually supply naphthalene cuts, while Mexico’s proximity to US construction markets sustains cross-border trade in powder SNF.

Europe faces structural headwinds from high energy prices and stringent carbon regulations, yet it remains at the forefront of sustainable-chemistry innovation. BioBTX’s plan to commission a waste-to-aromatics unit by 2026 exemplifies circular-economy alignment. Germany’s R&D leadership in automotive coatings keeps specialty naphthalene derivatives on procurement lists, although suppliers must certify lower residual PAH levels to comply with REACH. Southern European infrastructure upgrades tied to EU recovery funds provide a modest uplift for SNF demand.

Regulatory Landscape

Regulation around naphthalene and several naphthalene-derived intermediates is tightening across major consuming regions, which is raising compliance costs for producers and downstream formulators. In the European Union, naphthalene is prohibited as an ingredient in cosmetics under Regulation (EC) No 1223/2009, and it is restricted in toys under Directive 2009/48/EC due to its carcinogenic classification. Policy attention continues through REACH, where the European Commission updates its REACH restriction roadmap via the CARACAL expert group process (including discussions referenced in July 2026). Separately, REACH-related restriction activity and product-compliance updates in 2025 reinforced the need for tighter control of naphthalene and PAH content in relevant articles and mixtures, and buyers increasingly prefer suppliers that can document low-residual content and maintain robust monitoring.

In the United States, naphthalene remains under EPA oversight within the TSCA framework, and it is also being reassessed under the EPA IRIS program, broadening toxicology and exposure scrutiny for manufacturers and importers. EPA actions in December 2024, which required reporting of unpublished health and safety data for naphthalene (among other chemicals), increased the administrative and data-governance burden. Industry groups including the American Chemistry Council and the American Petroleum Institute formed a Naphthalene Workgroup to engage on draft assessment activities. Together, these dynamics support a compliance-led differentiation pattern, where larger or more integrated suppliers can fund emission controls, testing, and documentation to maintain access to North America and Europe.

Value Chain Analysis

The value chain begins with upstream aromatics generation, primarily from coal tar distillation linked to coke and steel operations, complemented by petroleum-based streams from refinery aromatics recovery. Refined naphthalene then feeds derivative manufacturing routes, including sulphonation and condensation to produce sulphonated naphthalene formaldehyde and related condensates, oxidation to phthalic anhydride, and specialty syntheses for high-purity naphthols and other performance intermediates. The market remains sensitive to feedstock variability and purity requirements, which is why coal-tar dependence and volatility continue to affect procurement and production planning for both bulk construction chemicals and higher-spec electronics or pharma applications.

Midstream and downstream, integrated or scale players convert intermediates into products sold to construction chemicals, dyes, agrochemical formulators, pulp and paper additives, oil and gas chemicals, and specialty applications. Examples of scale and specialization include Indorama Ventures commissioning a purified 2,6-naphthalene dicarboxylic acid (PNDA) unit at its integrated Decatur, Alabama site (announced June 2021), supporting merchant supply into polyester and high-performance materials chains. On the construction side, large SNF capacity footprints such as Shandong Wanshan Chemical Co. Ltd. (reported 500,000 metric tons per year of sodium naphthalene sulfonate formaldehyde capacity) illustrate the role of high-volume plants feeding admixture formulators and ready-to-blend distribution networks. Distribution typically runs through regional chemical distributors and direct supply to major formulators, with compliance documentation, consistent quality, and logistics reliability increasingly used as qualification gates by multinational buyers.

Competitive Landscape

The naphthalene derivatives market is moderately consolidated. Technological advancements are critical, as achieving sub-5 ppm metal content in battery-grade derivatives accelerates qualification with cathode and separator manufacturers. Sustainability is increasingly influencing procurement, with electronics OEMs requiring life-cycle assessment data. Regional production remains vital, with Asia-Pacific buyers favoring local plants to reduce lead times, while EU buyers prioritize suppliers adhering to REACH and environmental footprint regulations. Over the next five years, portfolio optimization and selective M&A are expected as companies focus on specialized niches.

Naphthalene Derivatives Industry Leaders

Cromogenia Units

Rain Carbon Inc.

Huntsman International LLC

Koppers Inc.

Himadri Specialty Chemical Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A clear opportunity is the shift from commodity-grade volumes toward higher-value, performance-oriented derivatives where purity, consistency, and application support are monetized. Electronics and battery-related uses are pulling specifications toward lower metals and tighter impurity control, while pharmaceutical intermediates depend on premium-grade refined naphthalene and validated supply chains. This premiumization theme is reinforced by active industry moves such as King Industries bringing a new alkylated naphthalene production facility online in Waterbury, Connecticut (March 2026), which adds capacity for lubricant applications and signals continued investment into specialty naphthalene-based fluids beyond only construction-linked SNF demand.

Compliance-driven reformulation and documentation also create whitespace for suppliers that can meet tighter residue and safety requirements across end markets. For example, the European Union published Regulation (EU) 2026/1314 (June 2026), updating maximum residue levels for 1,4-dimethylnaphthalene in plant-origin products to 0.03 mg/kg, which adds another control point for producers and downstream users managing trace levels and product stewardship. Alongside ongoing TSCA and REACH scrutiny for naphthalene, these developments favor investments in analytical capability, tighter process control, and regionalized, high-purity supply options that reduce exposure to feedstock volatility and cross-border compliance friction.

Recent Industry Developments

- July 2026: Himadri Speciality Chemical Ltd. approved capital expenditure to build India's first carbon nano tubes manufacturing facility, along with additional investment to convert existing carbon black capacity into super speciality carbon black, while continuing work on its anthraquinone and carbazole project. These moves strengthen its advanced carbon materials platform linked to coal-tar derivative chains and expand the company's capability set beyond commodity distillates, improving its positioning with higher-spec end markets.

- December 2025: KG Chemical and Dong-Suh Chemical signed an MOU to form a joint venture in Indonesia for naphthalene oil and polynaphthalene sulfonate formaldehyde condensate (PNS) production, with a planned capacity of 30,000 tons per year. The proposed JV adds regional SNF/PNS supply optionality for Southeast Asia and supports faster, shorter-lead-time sourcing for construction-admixture and related customers.

- December 2024: The Ministry of Commerce and the General Authority of Foreign Trade (GAFT) enacted definitive anti-dumping measures on imports of sulphonated naphthalene formaldehyde (SNF) from China and Russia, effective December 2024 for five years. The action reshapes trade flows into the affected market by raising the cost of imported SNF and improving the competitive window for compliant domestic or alternative-origin suppliers.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is sized as the sales value of key naphthalene-derived intermediates produced from coal-tar or petroleum distillates and supplied in liquid or powder form for industrial use.

Scope exclusions: finished downstream goods, such as ready-mix concrete, finished plastics, and retail textile dyes, are not counted in this market total.

Segmentation Overview

- By Form

- Powder

- Liquid

- By Source

- Coal-Tar

- Petroleum-based

- Other Source (Bio-refinery, etc.)

- By Derivative

- Sulphonated Naphthalene Formaldehyde (SNF)

- Phthalic Anhydride

- Naphthalene Sulphonic Acid

- Naphthols (α, β)

- Alkyl Naphthalene Sulphonate Salts

- Others (1,6- & 1,8-Dihydroxynaphthalene, NDCA etc.)

- By End-User Industry

- Construction

- Paints and Coatings

- Textile

- Pulp and Paper

- Oil and Gas

- Pharmaceuticals

- Others End-User Industries (Electronics, Batteries, etc.)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by mapping naphthalene availability and derivative production routes, then linking them to the main end-use industries that pull demand. For coverage, we used public sources such as USGS mineral and materials statistics, UN Comtrade trade flows for relevant chemical codes, and government or customs trade dashboards where available.

To make the assumptions workable, we also reviewed safety and regulatory references, including SDS classifications and chemical registry entries, along with peer-reviewed chemistry and process journals. For demand context, we used industry association publications that discuss construction chemicals, dyes, and pulp and paper demand trends. Company annual reports, investor presentations, and press coverage were then used to understand capacity announcements, operational changes, and regional demand signals. Select paid database subscriptions were used only in a limited way for company financials, patent activity scans, and shipment-level import and export checks. These desk sources are illustrative, and we also used other public references for data collection, cross-checks, and clarifying open points.

Primary Interviews and Surveys

Primary discussions were used to pressure-test what desk research could not fully confirm, mainly the split between major derivatives, the direction of typical pricing movement by region, and the share of demand coming from construction admixtures versus other industrial uses. We spoke with producers, distributors, and downstream formulators, then used their input to confirm utilization patterns and trade substitution across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 18% | APAC: 46% |

| Mid tier: 47% | Functional/Unit leaders: 32% | EMEA: 32% |

| Smaller Players: 20% | Managers: 50% | Americas: 22% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where upstream naphthalene availability, derivative conversion routes, and regional trade signals were used to reconstruct the addressable demand pool, then translated into value using region-specific price ranges. Totals were checked with selective bottom-up approximations, including a supplier roll-up for a sample of key producers and a volume-by-ASP sanity check for high-consumption uses.

In the model, a few inputs drove most of the sensitivity: coal-tar versus petroleum-based supply mix, operating rates and capacity additions for key derivatives, import dependence in deficit regions, construction activity indicators tied to admixture demand, and the observed price direction for aromatic intermediates. When a direct data point was missing, we used bounded ranges agreed in interviews and applied conservative shares, then re-checked that the outcome stayed consistent with trade and production signals.

For forecasting, we leaned on scenario analysis because derivative demand is pulled by multiple end markets that do not move in the same direction each year. Scenarios were anchored on expected construction chemical demand, regional industrial output trends, and planned capacity changes, then refined using expert views on pricing and substitution risks.

Data Validation & Update Cycle

To validate outputs, we compared model totals against independent signals such as trade balances, public capacity and utilization commentary, and demand-side indicators in construction chemicals and dyes. If a region showed an unrealistic jump, we revisited assumptions and sent follow-up questions to primary contacts before sign-off.

A second analyst review is completed to catch unit errors, currency timing issues, and share splits that do not reconcile. Reports are refreshed annually, and interim updates are made when a material event occurs, such as a plant shutdown, a major expansion, or an abrupt feedstock price swing. Before delivery, an analyst runs a fresh pass so clients receive an updated view aligned with the latest available information.

Mordor Intelligence's Naphthalene Derivative Market Size Compared With Other Published Estimates

Published market values for naphthalene derivatives often differ because the boundary is drawn differently, and the same derivative can be counted at different points in the value chain. Differences also appear when one estimate uses broader downstream demand pools, or when pricing is assumed using a single global average instead of region-level ranges.

Import-export checks for aromatic intermediates, cross-checked with public capacity signals and interview-based utilization ranges, are used to keep Mordor Intelligence tied to the intermediate-chemical demand pool and to avoid counting finished downstream products inside the total.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.92 B (2025) | |

| Industry Research Publisher A | USD 1.82 B (2025) | Uses a narrower realized-demand view in 2025, and the scope notes do not clearly confirm inclusion of the full set of intermediate derivatives or the same end-use linkage, which can undercount smaller derivative streams. |

| Industry Research Publisher B | USD 2.37 B (2025) | Appears to apply a broader boundary and more aggressive value capture, and the publicly visible methodology does not clearly state exclusions for finished downstream products or how regional pricing is normalized, which can lift the stated total. |

The spread mainly comes from how far downstream the boundary is pushed and how prices are applied across regions. When the scope stays on intermediate derivatives sold to industrial users, and the totals are repeatedly checked against trade and capacity signals, the final number stays easier to trace and replicate year to year.

Key Questions Answered in the Report

What is the current Naphthalene Derivative Market size?

The naphthalene derivatives market size stood at USD 1.98 billion in 2026 and is on track to reach USD 2.31 billion by 2031.

Which derivative leads global demand?

Sulphonated naphthalene formaldehyde accounts for 43.48% of revenue owing to its widespread use as a construction superplasticizer.

Why is Asia-Pacific so dominant?

Asia-Pacific hosts the largest construction programs and electronics supply chains, giving it 53.35% of global volume and the highest 4.06% CAGR outlook.

What opportunities exist beyond construction?

High-purity derivatives for batteries, graphene composites, and pharmaceutical intermediates offer premium margins and sustain diversification strategies for suppliers.

Page last updated on: