Hexamethylenediamine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

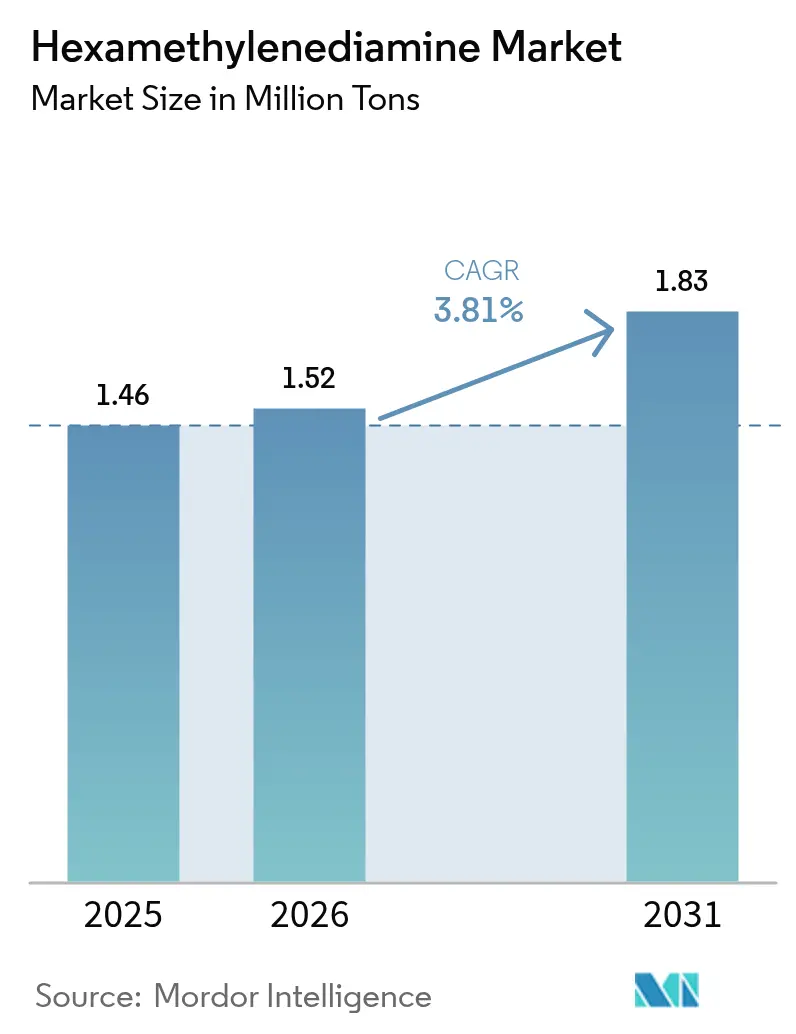

| Market Volume (2026) | 1.52 Million tons |

| Market Volume (2031) | 1.83 Million tons |

| Growth Rate (2026 - 2031) | 3.81% CAGR |

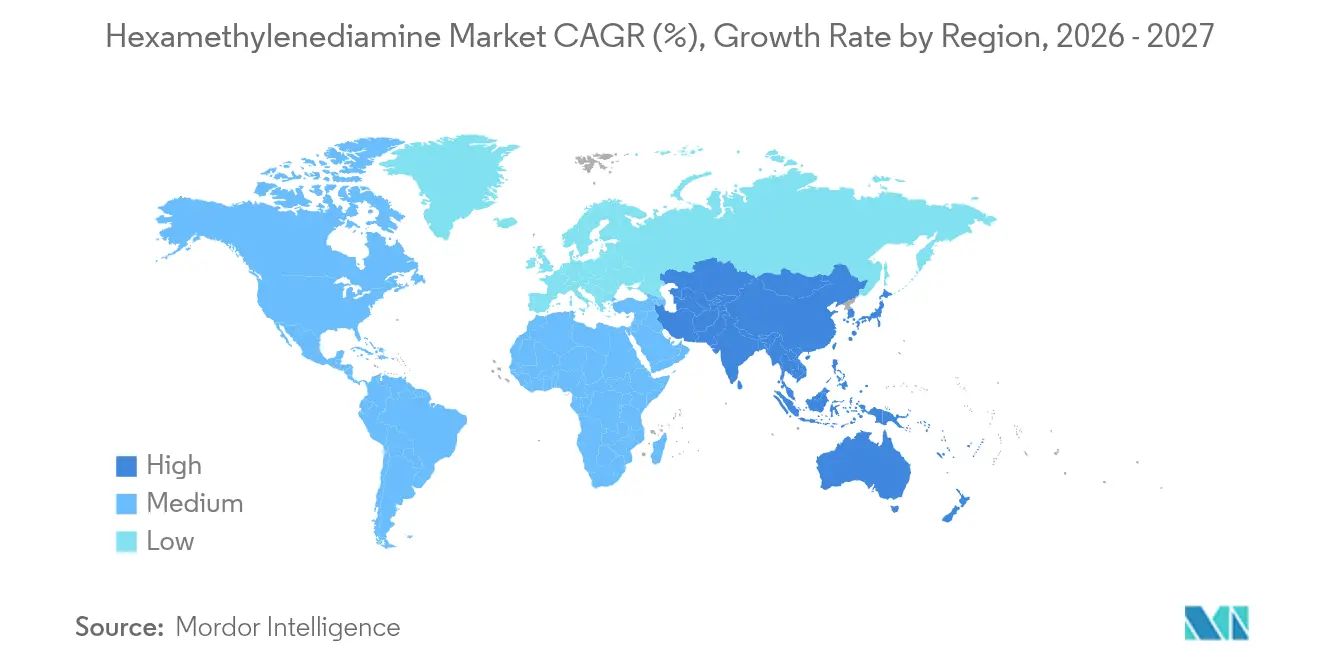

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hexamethylenediamine Market Analysis by Mordor Intelligence

The Hexamethylenediamine market size is expected to grow from 1.46 million tons in 2025 to 1.52 million tons in 2026 and is forecast to reach 1.83 million tons by 2031 at 3.81% CAGR over 2026-2031. Demand strength is rooted in nylon 6,6 production, while capacity constraints in the adiponitrile-to-hexamethylenediamine chain are triggering fresh investment across Asia-Pacific, North America and Europe. Strategic focus on lightweight vehicle parts, the post-pandemic revival of technical textiles and the steady uptake of specialty applications such as epoxy curing agents underpin volume expansion. Producers have responded to recent supply shocks by accelerating vertical integration and by piloting bio-based feedstocks that promise lower cost and reduced emissions. At the same time, crude-linked feedstock volatility, REACH-driven amine-emission limits and scale-up risk for bio routes temper the outlook.

Key Report Takeaways

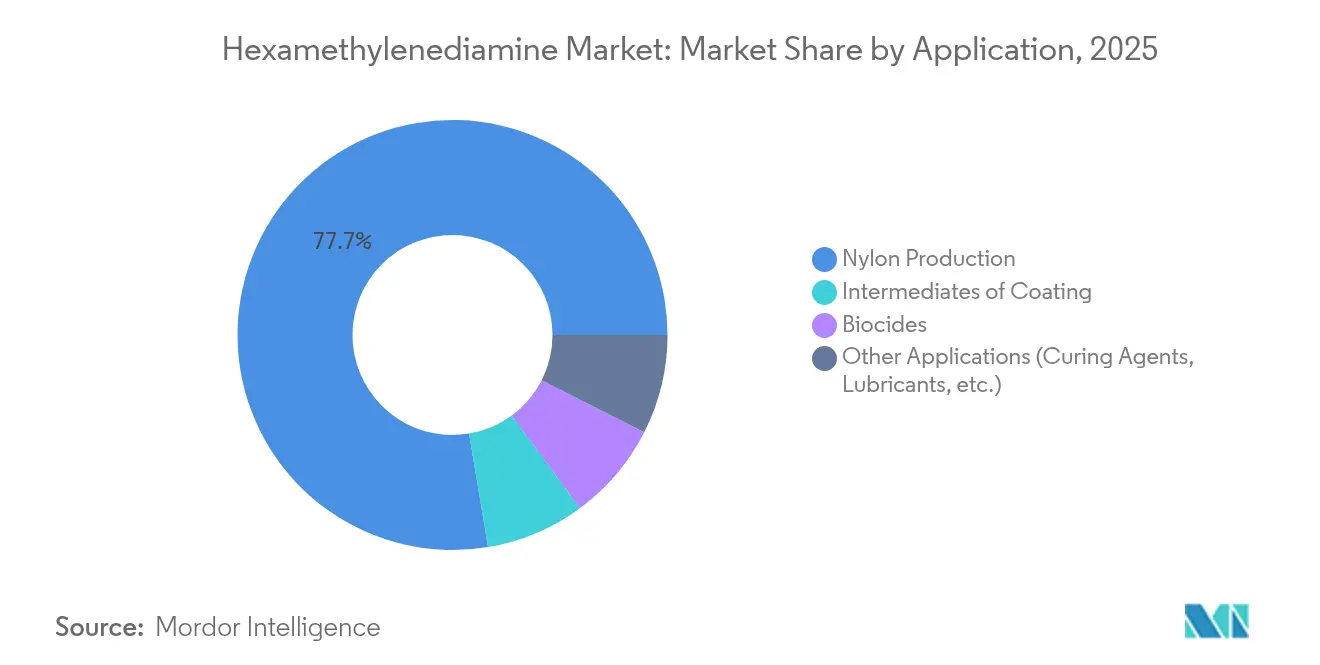

- By application, nylon production led with 77.65% of hexamethylenediamine market share in 2025; other applications are projected to grow at a 4.92% CAGR to 2031.

- By grade, standard industrial grade commanded 70.95% share of the hexamethylenediamine market size in 2025; bio-based grade is forecast to post the fastest 5.47% CAGR between 2026-2031.

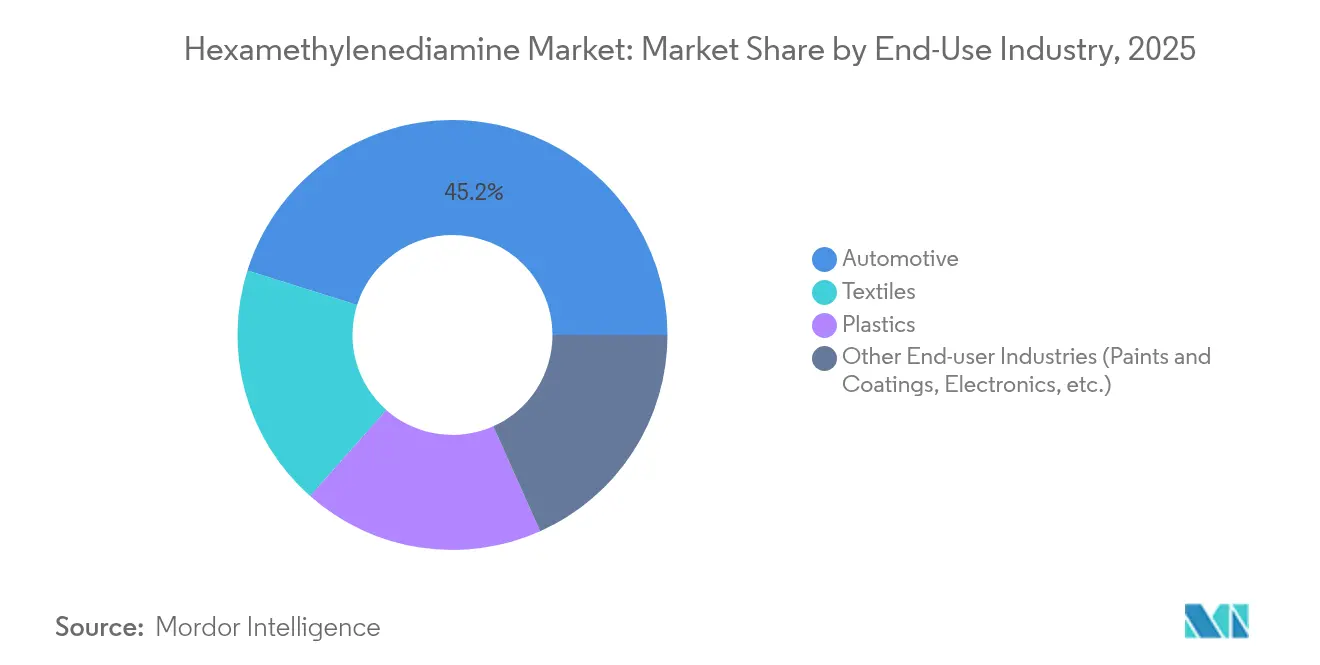

- By end-use industry, the automotive segment held 45.15% of the hexamethylenediamine market size in 2025, while other end-user industries are expected to expand at 5.33% CAGR through 2031.

- By geography, Asia-Pacific accounted for 51.74% of the hexamethylenediamine market share in 2025; the region is set to register a 4.82% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hexamethylenediamine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing consumption of Nylon 6,6 in lightweight vehicle parts | +1.2% | Global, with concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| Rapid capacity additions for adiponitrile-to-HMDA | +0.8% | Asia-Pacific core, spill-over to North America | Short term (≤ 2 years) |

| Shift towards bio-based adiponitrile feedstocks | +0.6% | Europe and North America leading, Asia-Pacific following | Long term (≥ 4 years) |

| Emergence of hexamethyldiaamine-based epoxy curing agents | +0.4% | Global, with early adoption in specialty applications | Medium term (2-4 years) |

| Growing demand for hexamethyldiaamine from textile industry | +0.7% | Asia-Pacific dominant, emerging in South America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Consumption of Nylon 6,6 in Lightweight Vehicle Parts

Automotive light-weighting targets are accelerating nylon 6,6 adoption, and the downstream pull-through is boosting the hexamethylenediamine market. Vehicle makers value polyamide’s strength-to-weight ratio, heat resistance and recyclability, particularly for battery-electric models where mass directly affects range. Asia-Pacific OEMs are ramping nylon intake manifold and structural-member usage alongside regional polyamide capacity additions, tightening regional balances and rewarding integrated suppliers. In North America, Tier-1 suppliers are redesigning engine-bay components around nylon 6,6 to cope with turbo-charging heat loads. The material substitution trend is therefore driving a structural, rather than merely cyclical, uplift in hexamethylenediamine demand.

Rapid Capacity Additions for Adiponitrile-to-HMD

Supply shocks in 2024 exposed reliance on a handful of adiponitrile units. Producers reacted by green-lighting de-bottlenecks and grass-roots lines that push integrated adiponitrile-hexamethylenediamine capacities higher in China, the Gulf Coast and Western Europe. INVISTA’s Maitland restart and Ascend’s 90 kt/y Alabama build-out epitomize the trend. While the wave will ease feedstock tightness, it also risks short-term oversupply and sharper regional price swings. Still, most operators deem the capex justified to safeguard downstream nylon economics and capture proximity advantages in Asia-centric end-use clusters.

Shift Toward Bio-Based Adiponitrile Feedstocks

Policy pressure on Scope-3 emissions is turning bio-routes from pilot curiosity into mainstream investment priority. Covestro-Genomatica’s milestone run of bio-HMD demonstrates cost parity potential against petro routes when renewable carbon credits are priced in. Europe’s decarbonization incentives shorten payback periods, prompting early-stage feasibility work in North America and, increasingly, China. Life-cycle assessments show 50-70% lower greenhouse-gas footprints, an advantage that appeals to automotive and apparel brands targeting net-zero supply chains. The competitiveness hinge remains fermentation scale-up and feedstock logistics, yet the directional shift is clear: bio-based platforms will re-shape long-term cost curves and market positioning.

Emergence of HMD-Based Epoxy Curing Agents

Beyond nylon, specialty demand is surfacing in advanced adhesives, composite resins and antimicrobial coatings. Evonik’s thermo-latent systems illustrate how HMD contributes flexibility without sacrificing glass-transition temperature, enabling crash-resistant structural bonding[1]Source: Evonik Industries, “Thermo-Latent Curing Agents for Structural Epoxy Adhesives,” evonik.com. Marine-sector coatings exploit the diamine’s chain structure to deliver long-lasting biofouling resistance, a feature attracting shipyards seeking reduced maintenance costs. Specialty volumes remain modest compared with nylon, but margin uplift exceeds 25% versus commodity grades, making this diversification a strategic hedge for producers facing nylon price cyclicality.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in crude-derived adiponitrile prices | -0.9% | Global, with acute impact in import-dependent regions | Short term (≤ 2 years) |

| Scale-up risk for bio-based hexamethyldiaamine technologies | -0.5% | Europe and North America leading adoption | Medium term (2-4 years) |

| Stringent REACH restrictions on amine emissions | -0.3% | Europe primary, with spillover to other regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Crude-Derived Adiponitrile Prices

Because adiponitrile tracks crude-naphtha spreads, upstream price shifts transmit quickly to hexamethylenediamine contract settlements, squeezing unintegrated players. The 2015 China plant accident underscored concentration risk, and subsequent refinery outages kept spot premiums wide. Import-heavy Europe feels swings most acutely, amplifying margin pressure on captive nylon spinners. Currency movement adds another layer: a weak euro inflates dollar-indexed feedstocks, further eroding competitiveness. These factors spur back-integration projects and intensify interest in bio-routes that decouple cost from oil volatility.

Scale-Up Risk for Bio-Based HMD Technologies

Fermentation yields above 99% in lab settings rarely translate seamlessly to 100 kt/y reactors. Contamination control, oxygen transfer and feedstock pre-treatment each introduce costly engineering work-arounds. Financing remains complicated by longer validation cycles and uncertain offtake commitments, slowing final investment decisions despite favorable ESG narratives. Regulatory approvals for novel enzymes add time and expense, especially in regions without harmonized biotech codes. Consequently, bio-HMD could capture single-digit share by 2030, but timelines may slip if pilot-to-commercial hurdles prove steeper than anticipated.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Nylon Dominance with Emerging Specialty Momentum

Nylon production retained a commanding 77.65% slice of the hexamethylenediamine market in 2025. The segment’s volume translates to 1.13 million tons, supported by automotive under-the-hood parts and carpet fibers. This pool underpins the largest absolute demand increment over the forecast horizon, but its CAGR trails at 3.54%. In contrast, specialty uses such as epoxy curing agents and biocide intermediates are expanding at a 4.92% pace, lifting their share of the hexamethylenediamine market size from 0.34 million tons in 2026 toward 0.43 million tons in 2031.

Diversification into higher-margin niches mitigates revenue exposure to nylon price cycles. Producers supply formulation-ready grades that shorten customer qualification time, reinforcing switching costs. The approach also leverages existing purification trains, so incremental capex stays low relative to returns. As a result, specialty penetration is expected to continue outpacing base-polymer growth across all regions.

By Grade: Standard Volume, Bio-Based Upside

Standard industrial grade remains the workhorse with 70.95% of 2025 demand, translating to about 1.04 million tons. Producers optimize this stream for balanced purity and cost, fitting nylon salt specifications. High-purity grade, at 17.72%, serves electronics and pharmaceutical uses that tolerate no trace metals. Meanwhile, bio-based grade, still niche at 11.33%, is scaling at a 5.47% CAGR on the back of brand owner sustainability goals.

The hexamethylenediamine market share shift toward bio variants accelerates once 50 kt/y fermentation lines reach nameplate throughput, a milestone anticipated in 2027. Early adopters can charge 10-15% premiums, offsetting higher initial unit costs. Long term, process learning curves and renewable-credit monetization could position bio-HMD at the low end of the global cost curve.

By End-Use Industry: Automotive Leadership, Broader Sector Uptake

Automotive accounted for 45.15% of the hexamethylenediamine market size, or roughly 0.66 million tons in 2025, anchored by nylon 6,6 structural components. Electrification reinforces this pull as every 10 kg removed from a battery-electric car can add up to 0.7% driving range. Yet, other end-user industries—encompassing electronics, healthcare and marine—are on track for a 5.33% CAGR. Their aggregate share rises from 0.28 million tons in 2026 to 0.36 million tons by 2031.

Textiles, the historic second pillar, experiences mid-single-digit growth on the back of high-tenacity industrial yarns and technical fabrics, while engineered plastics cover consumer-goods housings and small appliances. These broader avenues cushion producers from cyclical auto build rates and diversify regional revenue mixes.

Geography Analysis

Asia-Pacific’s 51.74% stake in the hexamethylenediamine market reflects China’s integrated refinery-to-nylon ecosystem and the region’s outsized automotive and textile sectors. Regional demand rises at a 4.82% CAGR, lifting volume from 0.79 million tons in 2026 to nearly 0.99 million tons by 2031. Governments promote advanced materials clusters, and proximity to adipic-acid feedstock shortens supply lines. Investments such as INVISTA’s RMB 1.75 billion capacity doubling in Shanghai anchor the local supply chain and strengthen competitiveness.

North America’s share is underpinned by shale-advantaged feedstocks and captive automotive resin demand. Yet, cost competition from imports and recent bankruptcy proceedings at a major producer underscore vulnerability to price cycles. Producers emphasize high-purity and bio-based grades to defend margins and secure offtake from electronics and medical OEMs.

Europe is focusing on sustainability and specialty niches. BASF’s new 260 kt/y French plant integrates advanced purification and energy-efficient reactors that align with tightening decarbonization directives. REACH restrictions on amine emissions are stricter than other regions, raising compliance costs yet providing a non-price competitive moat for local output.

South America plus the Middle East and Africa both regions leverage competitive gas economics and expanding downstream plastics demand. Brazil’s automotive-production rebound and Saudi Arabia’s chemicals diversification initiatives open windows for regional HMD units, albeit from a small base. Political and logistical risk keeps growth moderate compared with Asia-Pacific, but cross-border joint ventures are positioning to tap these frontier volumes.

Competitive Landscape

Global supply is consolidated around six integrated groups controlling roughly 65% of capacity. Scale economies in high-pressure nitrile hydrogenation, plus the need for captive adiponitrile, create natural entry barriers. Recent deals reinforce this structure: BASF bought Solvay’s polyamide assets then secured DOMO’s Alsachimie stake to lock in upstream intermediates, while INVISTA divested selected downstream nylon lines to focus on feedstock integration. Chinese state-backed entrants are adding capacity aggressively, intensifying margin pressure on legacy Western plants.

Competitive strategy is tilting toward process innovation and green chemistry. Patents covering low-energy hydrogenation catalysts, continuous purification and solvent recycling are climbing, offering cost and ESG advantages. Partnerships such as Covestro-Genomatica aim to commercialize bio-routes at world-scale, potentially resetting cost curves by late decade. On the specialty front, Evonik and Mitsubishi Gas Chemical tailor high-purity and latent-curing grades that fetch 25-40% price premiums over bulk material. In this evolving arena, diversified portfolios and access to bio-feedstock technology will determine long-term winners.

Hexamethylenediamine Industry Leaders

Ascend Performance Materials

INVISTA (Koch)

Henan Shenma Nylon Chemical

BASF SE

Radici Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: BASF completed the purchase of DOMO Chemicals’ 49% share in the Alsachimie joint venture, becoming sole owner of the French polyamide-6,6 precursor complex.

- June 2025: BASF started up a 260,000 t/y hexamethylenediamine plant in Chalampé, France, featuring integrated R&D facilities for advanced polyamide applications.

Global Hexamethylenediamine Market Report Scope

Hexamethylenediamine is an organic compound consisting of a hexamethylene hydrocarbon chain terminated with amine functional groups. It is used in the organic synthesis and polymerization of high molecular compounds. Hexamethylenediamine is widely used in the production of polyamides, such as nylon 66, nylon 610, etc. It is also used as a urea-formaldehyde resin, epoxy resin curing agent, and organic crosslinking agent.

The hexamethylenediamine market is segmented by application, end-user industry, and geography. By application, the market is segmented into nylon production, intermediate for coatings, biocides, and other applications (curing agents, lubricants, etc.). By end-user industry, the market is segmented into textile, plastics, automotive, and other end-user industries (paints and coatings, petrochemicals, etc.). The report also covers the market size and forecasts for hexamethylenediamine in 15 countries across major regions. Each segment's market sizing and forecasts are based on volume (tons).

| Nylon Production |

| Intermediates of Coating |

| Biocides |

| Other Applications (Curing Agents, Lubricants, etc.) |

| Standard Industrial Grade |

| High-Purity Grade |

| Bio-based Grade |

| Automotive |

| Textiles |

| Plastics |

| Other End-user Industries (Paints and Coatings, Electronics, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Malaysia | |

| Philippines | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Turkey | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Rest of Middle-East and Africa |

| By Application | Nylon Production | |

| Intermediates of Coating | ||

| Biocides | ||

| Other Applications (Curing Agents, Lubricants, etc.) | ||

| By Grade | Standard Industrial Grade | |

| High-Purity Grade | ||

| Bio-based Grade | ||

| By End-use Industry | Automotive | |

| Textiles | ||

| Plastics | ||

| Other End-user Industries (Paints and Coatings, Electronics, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Malaysia | ||

| Philippines | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Turkey | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current size of the hexamethylenediamine market

The hexamethylenediamine market stands at 1.52 million tons in 2026 and is projected to reach 1.83 million tons by 2031.

Which application dominates demand?

Nylon production accounts for 77.65% of global demand, making it the primary volume outlet for hexamethylenediamine.

Which region holds the largest share?

Asia-Pacific leads with 51.74% of global volume thanks to China’s integrated nylon supply chain and expanding automotive production.

How fast is bio-based hexamethylenediamine growing?

Bio-based grade is forecast to post a 5.47% CAGR between 2026-2031 as sustainability regulations and brand commitments drive adoption.

What are the main restraints on market growth?

Crude-linked adiponitrile price volatility and the technical scale-up risk of bio-based technologies are the two most significant headwinds.

Page last updated on: