Dimethylaminopropylamine (DMAPA) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

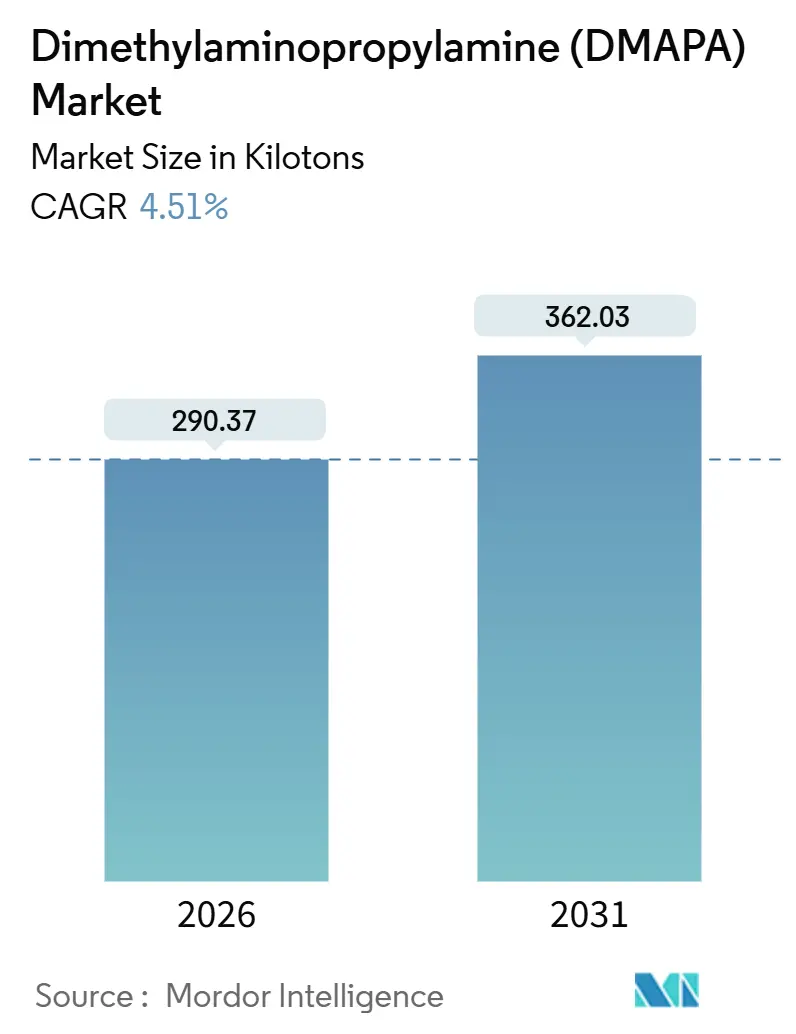

| Market Volume (2026) | 290.37 kilotons |

| Market Volume (2031) | 362.03 kilotons |

| Growth Rate (2026 - 2031) | 4.51% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dimethylaminopropylamine (DMAPA) Market Analysis by Mordor Intelligence

The Dimethylaminopropylamine Market size is estimated at 290.37 kilotons in 2026, and is expected to reach 362.03 kilotons by 2031, at a CAGR of 4.51% during the forecast period (2026-2031). The Dimethylaminopropylamine market’s short-term outlook benefits from rising demand for cocamidopropyl betaine surfactants, low-emission polyurethane catalysts, and water-treatment flocculants, even as feedstock swings and stricter cosmetic limits challenge margins. Capacity additions in China and India are lifting global nameplate output, while renewable electricity transitions in Nanjing and Jurong Island plants help suppliers defend prices against carbon-focused buyers. Downstream personal-care formulators, automotive OEMs, and epoxy-coating manufacturers are accepting modest cost increases to secure low-VOC chemistries and bio-circular grades. Regional price gaps persist: Asia-Pacific maintains the lowest ex-works cost base, whereas European buyers pay a 15-20% premium for pharmaceutical or cosmetic grade material that meets EU Annex III nitrosamine limits.

Key Report Takeaways

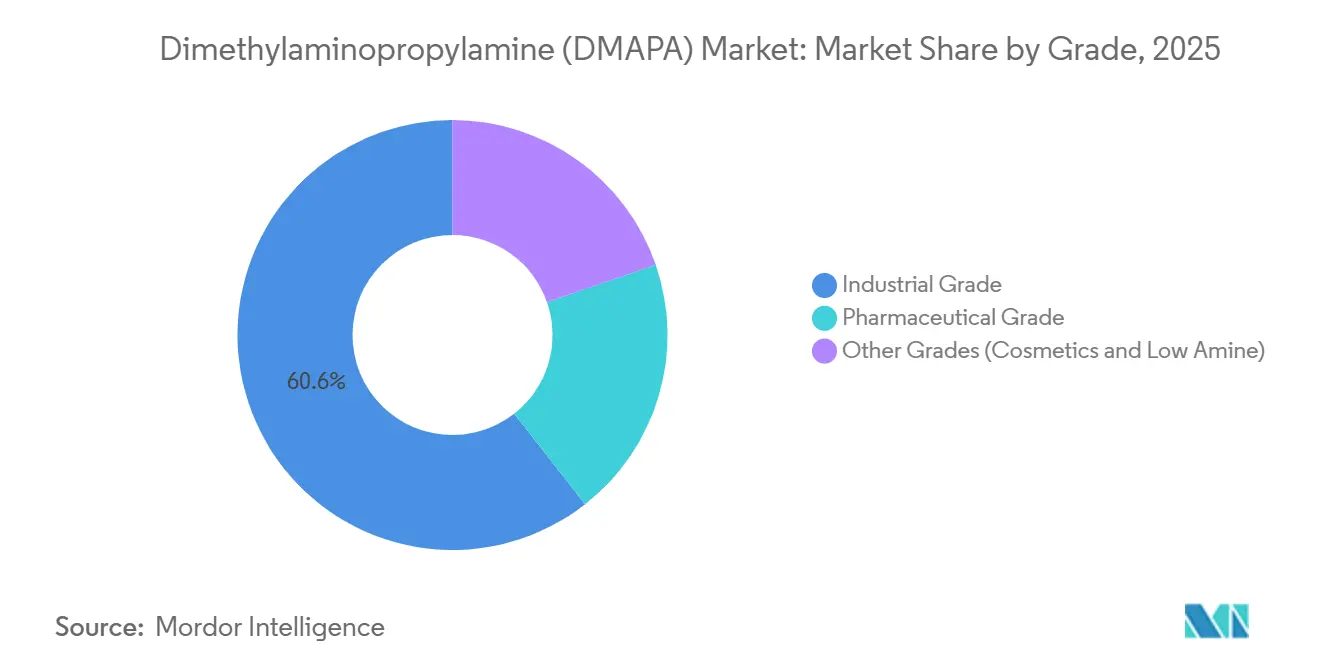

- By grade, industrial grade commanded 60.58% of the Dimethylaminopropylamine market share in 2025, while other grades that include cosmetics and low amine are projected to grow at a 4.91% CAGR.

- By application, beauty and personal care surfactants led with 49.35% share in 2025; the segment is forecast to expand at a 4.98% CAGR through 2031.

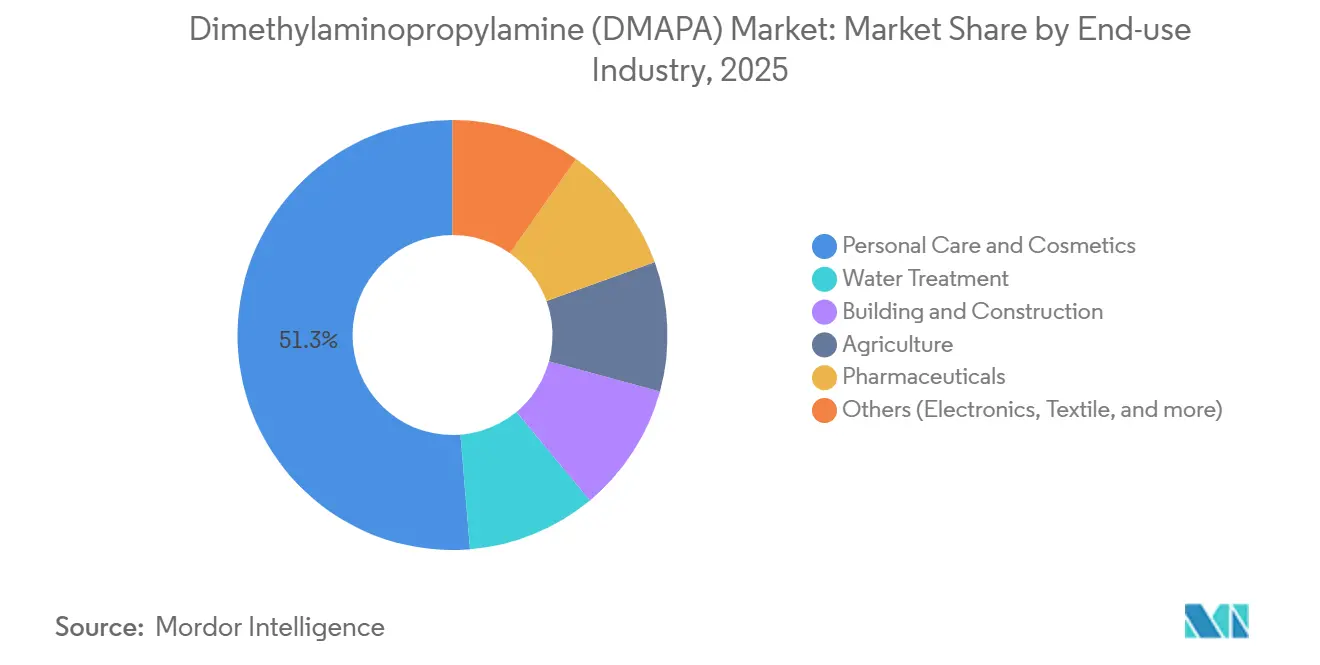

- By end-use industry, personal care and cosmetics led with 51.29% share in 2025; the segment is forecast to expand at a 5.10% CAGR through 2031.

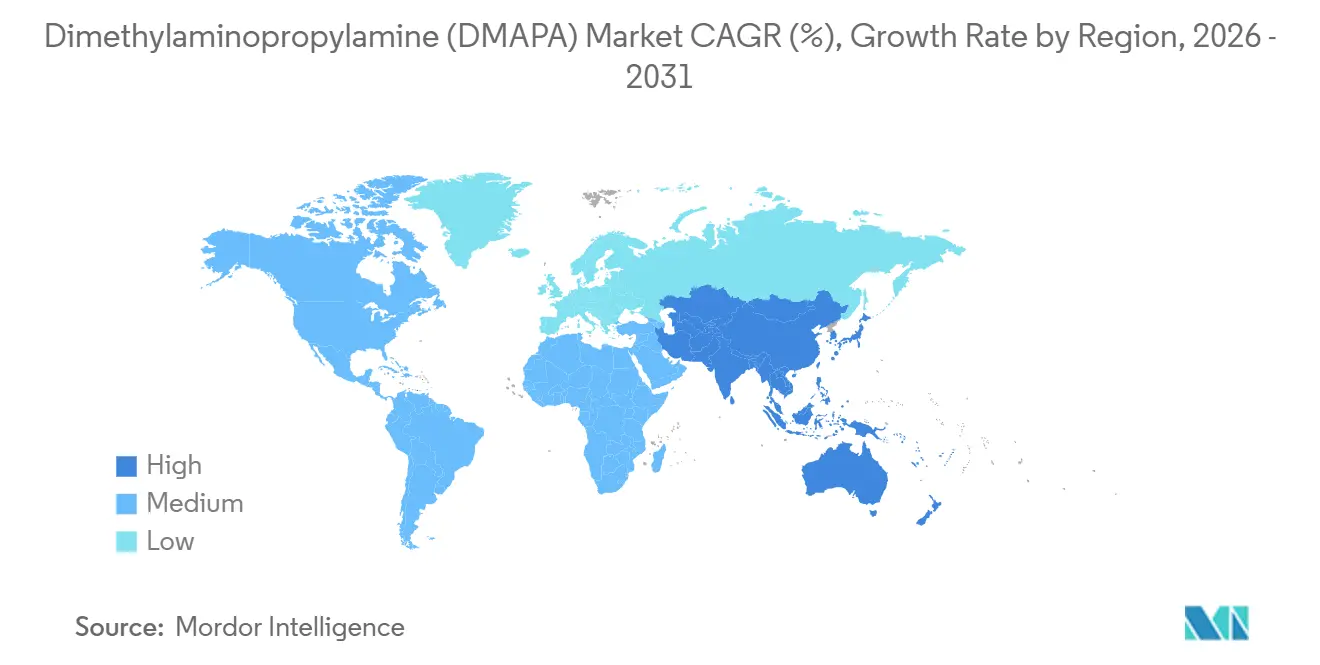

- By region, Asia-Pacific captured 42.55% of the 2025 market share and is forecast to grow at a 5.02% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Dimethylaminopropylamine (DMAPA) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid shift to mild, CAPB-based surfactants in hair- and skin-care formulations | +1.20% | Global, with highest adoption in North America, Western Europe and urban Asia-Pacific | Medium term (2-4 years) |

| Regulatory push for formaldehyde-free, low-VOC chemistries in coatings and PU foams | +0.90% | North America & EU (EPA 40 CFR Part 59, EU Directive 2004/42/EC), spillover to APAC export-oriented manufacturers | Short term (≤ 2 years) |

| Asia-Pacific capacity expansions for batch and continuous DMAPA plants | +1.00% | APAC core (China, India), spillover to MEA and South America via exports | Medium term (2-4 years) |

| Emergence of bio-circular DMAPA via ISCC-PLUS certified feedstocks | +0.60% | EU and North America (driven by Scope 3 carbon accounting), early adoption in APAC by multinational subsidiaries | Long term (≥ 4 years) |

| Growing OEM additive packages for electric-vehicle coolants and lubricants | +0.50% | Global, concentrated in automotive hubs (Germany, US, China, South Korea, Japan) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Shift to Mild, CAPB-Based Surfactants in Hair- and Skin-Care Formulations

Shampoo and body-wash brands are replacing sodium lauryl sulfate with cocamidopropyl betaine to meet irritation-free claims and regulatory guidance on chronic skin exposure. Each tonne of CAPB uses about 0.35 tonnes of DMAPA, so every reformulation cycle lifts demand for high-purity amine feedstock. Syensqo earned ISCC PLUS certification at Zhangjiagang in 2023, enabling bio-circular Dimethylaminopropylamine that lowers Scope 3 footprints by up to 30%[1]Syensqo, “Zhangjiagang Site Gains ISCC PLUS Certification,” syensqo.com. Personal-care suppliers in the United States and Germany now lock in multi-year purchase agreements for low-amine grades, while Chinese contract manufacturers ramp batch tolling to supply regional indie brands. Urban consumers in Seoul, Shanghai, and Los Angeles drive double-digit growth in premium mild cleansers, anchoring the Dimethylaminopropylamine market in value-added segments.

Regulatory Push for Formaldehyde-Free, Low-VOC Chemistries in Coatings and PU Foams

The U.S. 40 CFR Part 59 rule and EU Directive 2004/42/EC cap VOC content in decorative paints, prompting formulators to swap solvent-borne hardeners for DMAPA-derived waterborne systems[2]U.S. EPA, “40 CFR Part 59 Architectural Coatings,” epa.gov. Huntsman’s JEFFCAT LE-340 meets VDA-278 emission thresholds for automotive seating, and orders surged after German OEMs mandated low-emission catalysts in new electric-vehicle interiors. Evonik embeds DMAPA into its Ancamine line to cut drying time in high-solids primers, giving coatings producers a way to comply without sacrificing throughput. The regulatory clampdown converts compliance cost into volume upside for continuous-process producers that can guarantee residual amine below 0.2%.

Asia-Pacific Capacity Expansions for Batch and Continuous Plants

BASF doubled Nanjing output in July 2025, taking global capacity to about 85,000 MT yr and switching the site to 100% renewable electricity. Evonik broke ground on a specialty-grade line at the same hub in November 2024, reinforcing Jiangsu’s status as the epicenter of Dimethylaminopropylamine market growth. In India, Alkyl Amines approved up to USD 18 million for 4,000 MT of new specialty capacity at Dahej, targeting pharmaceutical-grade niches. Continuous hydrogenation systems lower residuals but cost USD 50-80 million per 10,000 MT, limiting adoption to large multinationals. The near-term result is an oversupply of industrial grade and a persistent shortfall of cosmetic grade, preserving the 15-20% premium.

Emergence of Bio-Circular DMAPA via ISCC PLUS Certified Feedstocks

The ISCC PLUS list now covers N, N-dimethyl-1,3-propanediamine, enabling mass-balance tracking from renewable naphtha to finished amine. Nouryon certified its green ethylene-oxide chain in June 2024, giving downstream surfactant makers an audited renewable carbon claim. BASF signed an offtake deal for 100,000 t yr of Indian green ammonia in October 2024, locking low-carbon hydrogen for European amines without major capex. Bio-circular Dimethylaminopropylamine commands a 25-35% premium, but upcoming EU CSRD rules will make product-level Scope 3 disclosures mandatory, widening adoption from prestige shampoos to mass-retail hair care.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in acrylonitrile and dimethylamine feedstock pricing | -0.7% | Global, most acute in regions without vertical integration (Europe, North America import-dependent facilities) | Short term (≤ 2 years) |

| Stricter EU cosmetic limits on residual DMAPA | -0.4% | EU, with spillover to export-oriented APAC and North American suppliers targeting EU market | Medium term (2-4 years) |

| High capex for explosion-proof continuous hydrogenation systems | -0.3% | Global, particularly constraining for mid-tier producers in India, Southeast Asia and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Acrylonitrile and Dimethylamine Feedstock Pricing

Spot acrylonitrile and dimethylamine swung by more than 20% inside 2025, eroding margins for producers without captive upstream units. Huntsman’s Performance Products EBITDA slid 24% on cost pass-through lags, highlighting exposure in merchant-purchase regions. BASF’s Verbund model at Ludwigshafen and Nanjing shelters earnings by integrating propylene oxide and ammonia on-site. Mid-tier Indian and Southeast Asian firms that buy methanol or propylene at market rates face working-capital strain when feedstocks spike, forcing some to idle reactors to avoid losses.

Stricter EU Cosmetic Limits on Residual DMAPA

Annex III of EU Regulation 1223/2009 caps secondary amines at 0.5% and nitrosamines at 50 µg kg, pushing personal-care buyers toward pharmaceutical-grade material. Continuous plants now run extra purification and real-time analytics, adding 12-18% to conversion cost. Asian batch producers risk losing access to the 260 million-unit EU shampoo market unless they retrofit columns or outsource polishing to tollers in Singapore or Germany. North American brands pre-emptively adopt EU-compliant specs to keep global SKUs harmonized, spreading the compliance premium across hemispheres.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Premium Variants Gain Momentum

Industrial grade dominated with 60.58% volume in 2025, but price discounts widened as new Chinese lines targeted water-treatment and agrochemical blenders. Pharmaceutical and Cosmetic grades, grouped as “Other Grades” in earlier audits, are expanding at a 4.91% CAGR as EU Annex III and Good Manufacturing Practice rules tighten. BASF’s Nanjing upgrade dedicated extra trays to high-purity cuts, while Evonik’s 2024 project embeds continuous hydrogenation and inline GC analytics to keep residual secondary amine below 0.2% (evonik.com). The Dimethylaminopropylamine market size for premium grades reached about 115 kilotons in 2026 and is on track to cross 150 kilotons by 2031.

Syensqo’s bio-circular cosmetic grade sells at a 25-35% premium, attracting luxury shampoo makers eager for Europe’s Green Deal labeling advantage. Huntsman leverages GMP-certified lines in Singapore to supply EDC coupling agents in peptide drug synthesis, where lot traceability outweighs price sensitivity. This three-tier structure, industrial, pharmaceutical, and bio-circular, locks in higher average selling prices even as commodity margins compress.

By Application: Personal Care Leads, PU Catalysts Accelerate

Beauty and Personal Care Surfactants absorbed 49.35% of the 2025 volume, underpinned by the pivot from SLS to DMAPA-based CAPB in mass and salon hair care. The segment moves roughly in line with premium shampoo launch velocity, translating to a 4.98% CAGR through 2031. Polyurethane Foam Catalysts trail in size but climb faster on strict in-cabin emission rules for electric cars; Huntsman’s LE-340 catalyst alone lifted DMAPA use in flexible seats by almost 9% year over year.

Water-treatment flocculants and epoxy-resin hardeners form the second application cluster, benefiting from infrastructure upgrades in Asia and repaint cycles in the EU. The Dimethylaminopropylamine market size tied to epoxy systems is catching up as wind-turbine blade makers push for rapid-cure primers. Overall, high-value downstream uses cushion the Dimethylaminopropylamine market against cyclical softness in industrial cleaning and oilfield chemicals.

By End-Use Industry: Personal Care and Cosmetics Outpace Industrial Segments

In 2025, Personal Care and Cosmetics end-users accounted for 51.29% of the volume and are projected to grow at a 5.10% CAGR through 2031, driven by clean-beauty claims and Scope 3 carbon reduction targets. Reformulations by Procter & Gamble, Unilever, and Henkel to replace SLS with CAPB are boosting DMAPA consumption. The Building and Construction sector benefits from DMAPA's use in epoxy curing agents for industrial flooring, wind turbine blade coatings, and architectural paints, supported by infrastructure investments in Asia-Pacific and green building standards in Europe. Water Treatment demand, concentrated in municipal and industrial sectors, is driven by tertiary amines improving flocculation efficiency and China's 14th Five-Year Plan.

Pharmaceuticals, though smaller in volume, represent a high-value segment where DMAPA is used in peptide coupling reagents like EDC and API intermediates, with GMP-compliant material commanding a premium. Molkem Pharmaceuticals in India highlights domestic capability for pharmaceutical-grade DMAPA derivatives. The 'Others' category, including Electronics and Textiles, remains stable, with modest growth in electronics tied to EV battery production. Huntsman’s diverse clientele spans automotive additives, industrial cleaning, coatings, and composites, reflecting broad end-use demand. The shift toward personal care and pharmaceuticals, requiring high-grade DMAPA, sustains premium pricing and drives investments in continuous hydrogenation systems.

Geography Analysis

Asia-Pacific anchored 42.55% of 2025 demand, with a 5.02% CAGR outlook as Chinese and Indian producers integrate propylene oxide, dimethylamine, and renewable power onsite. BASF’s July 2025 doubling of Nanjing capacity secured local supply for Jiangsu’s personal-care contract manufacturers, while Evonik’s adjacent build targets pharmaceutical and low-amine variants. India, buoyed by Alkyl Amines and Balaji Amines expansions, shifts from a net importer to a balanced trade, yet still relies on Chinese propylene intermediates.

In North America, Huntsman opened its Conroe E-GRADE unit in May 2025, aiming at semiconductor wet-process chemicals, an emerging high-purity pocket. US buyers absorb higher delivered costs than Asian peers but value local supply and regulatory certainty. Mexico’s near-shoring boom in autos and personal-care filling plants nudges regional uptake, though the country remains import-dependent.

In Europe, producers grapple with energy surcharges yet win on premium price points because Annex III compliance filters supply. BASF took full control of the Chalampé amine-precursor site in July 2025, increasing feedstock security for specialty amines in the bloc. Demand tilts to cosmetic and epoxy hardener grades, sustaining the Dimethylaminopropylamine market despite flat macro consumption.

In South America and Middle East and Africa, Brazil’s personal-care clusters in São Paulo and Minas Gerais drive imports, while Saudi Arabia’s Jubail site supplies oilfield service chains that value DMAPA corrosion-inhibitor precursors. Longer lead times and currency swings temper growth, but do not change the underlying upward trajectory tied to population expansion and infrastructure spend.

Competitive Landscape

The Dimethylaminopropylamine (DMAPA) market is moderately consolidated. Mid-tier Asian firms such as Alkyl Amines and Hubei Jusheng pursue industrial grade volumes at discount prices, leveraging lower labor costs. Patent filings around low-emission catalysts (CN111748068B) and reactive amine epoxy agents (EP2042534A1) show how incumbents defend their share with application know-how. Huntsman pivots to electronics amines with its Conroe upgrade, chasing higher margins amid commodity oversupply. The competitive picture thus splits between scale leaders investing in sustainability and technology, and regional challengers focusing on cash-flow plays in bulk segments.

Dimethylaminopropylamine (DMAPA) Industry Leaders

BASF SE

Eastman Chemical Company

Huntsman International LLC

Alkyl Amines Chemicals Ltd.

Syensqo

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: October 2025 - BASF marked a significant milestone, celebrating both the 10th anniversary and the expansion of its production facilities for 3-(dimethylamino)propylamine (DMAPA) and polyetheramine (PEA) at its Nanjing site.

- April 2025: Eastman Chemical Company began producing a more sustainable version of dimethylaminopropylamine (DMAPA ES) at its St. Gabriel, Louisiana, facility. By utilizing renewable raw materials, DMAPA ES can boost the global warming potential (GWP) of cocamidopropyl betaine (CAPB) surfactant producers by as much as 50%, benefiting the consumer products industry.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the dimethylaminopropylamine (DMAPA) market as the global trade and on-purpose production of neat DMAPA, a clear diamine manufactured by hydrogenating dimethylaminopropionitrile and chiefly consumed in amphoteric surfactants, polyurethane catalysts, water-treatment additives, epoxy curing agents, and crop-protection intermediates. According to Mordor Intelligence, the scope spans merchant sales and captive use across industrial, pharmaceutical, and personal-care formulations, tracked in kilotons and, where data allow, converted to revenue through region-specific average selling prices.

Scope exclusion. Our assessment leaves out downstream blends or finished toiletries that already incorporate DMAPA-based surfactants.

Segmentation Overview

- By Grade

- Industrial Grade

- Pharmaceutical Grade

- Other Grades (Cosmetics, Low Amine)

- By Application

- Beauty and Personal Care Surfactants

- Water and Waste-water Treatment Chemicals

- Polyurethane Foam Catalysts

- Epoxy Resin Hardeners and Coatings

- Crop-Protection Intermediates

- Industrial and Institutional Cleaning Agents

- Others (Oilfield, Corrosion Inhibitors, and Ion-Exchange Resins)

- By End-Use Industry

- Personal Care and Cosmetics

- Water Treatment

- Building and Construction

- Agriculture

- Pharmaceuticals

- Others (Electronics, Textile, and more)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Structured discussions with sourcing managers at surfactant formulators, procurement leads at polyurethane foam makers, and plant engineers at Asian DMAPA facilities supplied real-time utilization rates, typical contract prices, and forward views on catalyst and surfactant demand. Follow-up calls in North America and Europe balanced regional perspectives before final triangulation.

Desk Research

Our analysts gathered baseline supply figures from customs and production data sets such as UN Comtrade, Eurostat PRODCOM, and the United States International Trade Commission, which disclose HS-coded export and import flows for amines. Prices and short-term trends were reviewed in open publications from ChemAnalyst, ICIS, and national chemical associations in China, India, and Germany.

We then validated demand signals with public filings and investor decks of major producers that report segmental volumes, while D&B Hoovers furnished company-level capacity details. Patents mined through Questel, along with PubChem toxicology dossiers and U.S. EPA Skin Sensitization assessments, helped our team flag regulatory counterforces. The sources listed illustrate the breadth of the desk review and are not exhaustive; many additional data points were consulted to refine numbers and narrative.

Market-Sizing & Forecasting

We begin with a top-down reconstruction that aligns apparent consumption = domestic output + imports - exports in every major producing and consuming economy. Those totals are reconciled with sampled bottom-up indicators, including name-plate capacity roll-ups, typical operating rates, and sampled average selling prices from distributor invoices, which together ground our volume and value baseline. Key variables tracked through the model include personal-care surfactant output, polyurethane slab-stock production, municipal water-treatment chemical demand, crop-acreage treated with betaine-based herbicides, and DMAPA plant capacity utilization.

Forecasts to 2030 rely on multivariate regression that relates DMAPA uptake to shampoo and liquid-soap retail sales, residential construction square-footage (foam demand proxy), and irrigated farmland area. Expert consensus guides scenario weighting, and any data gaps in bottom-up estimates are bridged using regional consumption-to-GDP elasticities observed in nearby mature markets.

Data Validation & Update Cycle

Before sign-off, Mordor analysts compare model outputs with external trade totals, company earnings, and price trajectories, and anomalies trigger re-checks with data providers or interviewees. A second analyst reviews every formula and assumption. The report is refreshed annually, while material events such as major plant debottlenecks prompt interim updates, ensuring clients always access the freshest view.

Why Mordor's Dimethylaminopropylamine Baseline Commands Reliability

Published numbers for DMAPA often diverge because firms differ on whether they include captive usage, convert volumes to revenue with spot or contract prices, or refresh models after feedstock swings.

Key gap drivers are evident: some publishers restrict scope to personal-care surfactants and miss industrial catalysts, while others fold broader tertiary amines into totals. A few rely solely on revenue models that inflate values when prices spike yet ignore latent capacity overhangs. Mordor's blended volume and value approach, yearly refresh, and dual validation steps mitigate such distortions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 278.05 kilotons (2025) | Mordor Intelligence | - |

| USD 376.3 million (2024) | Global Consultancy A | Revenue only, excludes captive Asian volumes, limited primary checks |

| USD 7.73 billion (2024) | Trade Journal B | Combines DMAPA with broader amines, high-level top-down, opaque segmentation |

In short, the disciplined scoping and bi-layer validation followed by Mordor Intelligence give decision-makers a balanced, transparent baseline they can trace back to clear variables and repeat with confidence.

Key Questions Answered in the Report

What is the forecast growth rate for global Dimethylaminopropylamine demand through 2031?

What is the forecast growth rate for global Dimethylaminopropylamine demand through 2031?

Which end-use sector consumes the most DMAPA today?

Which end-use sector consumes the most DMAPA today?

Why are pharmaceutical and cosmetic grades gaining share?

EU Annex III nitrosamine limits and global clean-beauty claims push buyers toward low-amine material, driving a 4.91% CAGR for premium grades.

How are Chinese producers influencing global supply?

Zhanjiang lines lower production costs and add renewable-powered tonnage, keeping Asia-Pacific at 42.55% of volume.

What premium does bio-circular DMAPA command over fossil grades?

ISCC PLUS certified bio-circular material typically sells at a 25-35% premium, reflecting renewable feedstock and mass-balance audit costs.

Page last updated on: