Independent Artists Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 170.91 Billion |

| Market Size (2031) | USD 233.31 Billion |

| Growth Rate (2026 - 2031) | 6.42% CAGR |

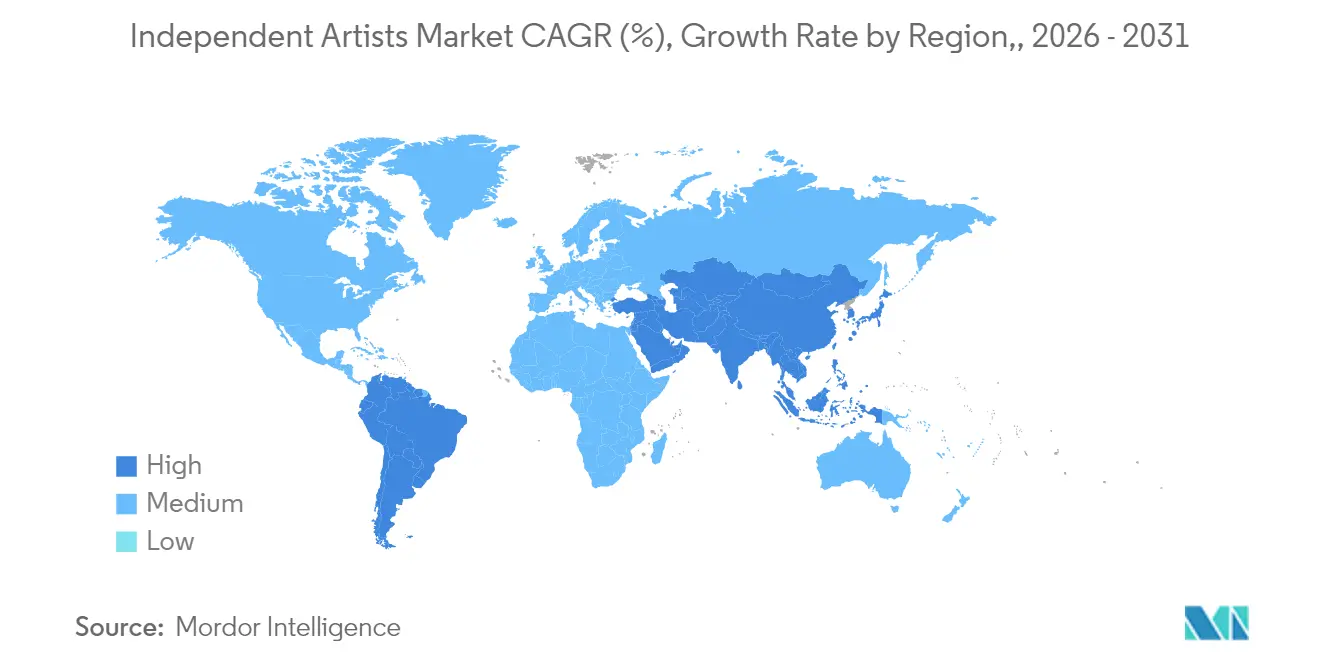

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Independent Artists Market Analysis by Mordor Intelligence

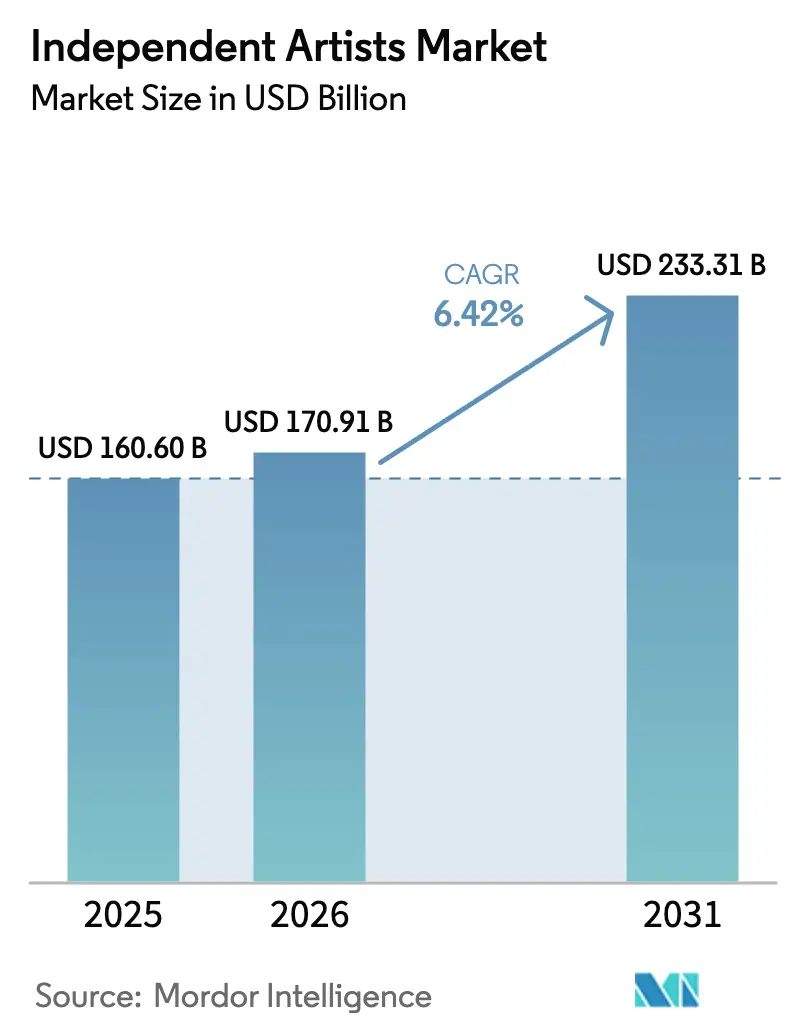

The Independent Artists market size is expected to grow from USD 160.60 billion in 2025 to USD 170.91 billion in 2026 and is forecast to reach USD 233.31 billion by 2031 at 6.42% CAGR over 2026-2031.

Independent Artists Market Steady growth reflects a structural shift in music economics as creator-centric platforms let musicians retain larger revenue shares, curbing the traditional label’s role. Streaming remains the largest income source, yet its momentum is flattening while merchandise, physical formats, and direct-to-fan products post the fastest gains. Platform consolidation around a handful of distributors raises discoverability hurdles, but new royalty rules, AI-enabled production, and subscription fan communities broaden earning options for artists willing to diversify income. Regionally, North America’s scale keeps it at the top, though Europe is expanding quicker due to supportive regulation and multilingual demand, and Asia-Pacific is the next volume frontier.

Key Report Takeaways

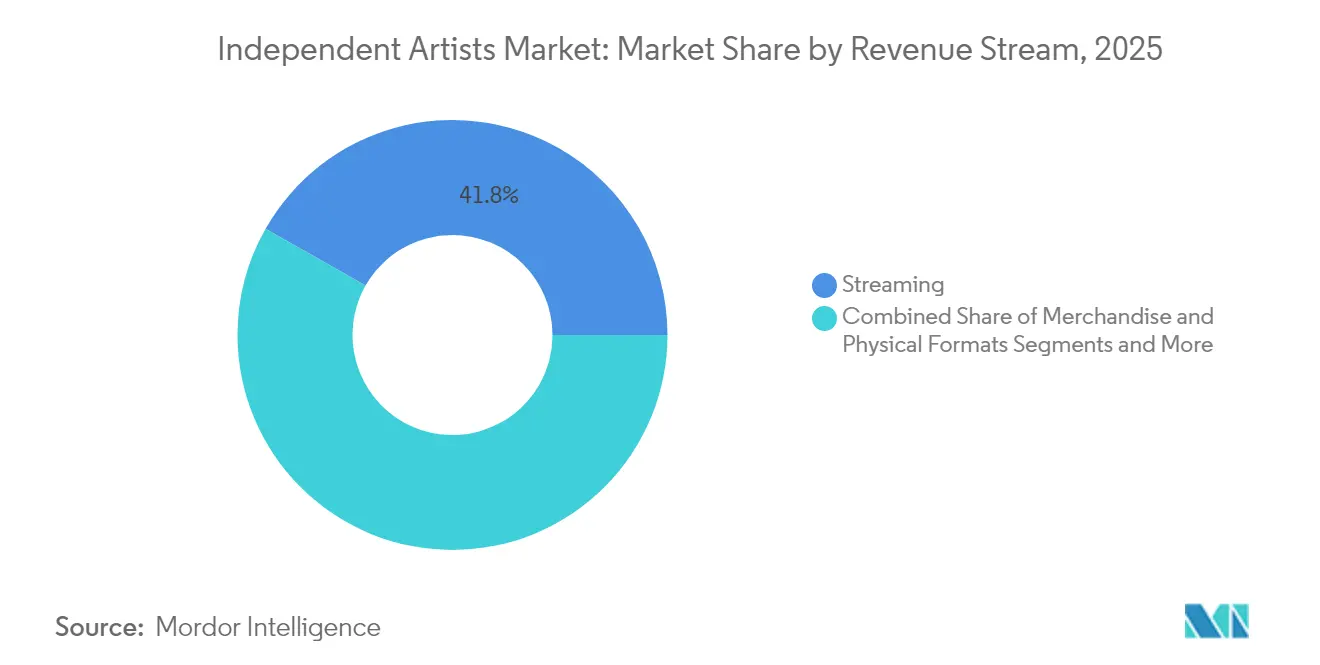

- By revenue stream, streaming captured 41.78% of independent artists market share in 2025, while merchandise and physical formats are projected to grow at an 8.45% CAGR through 2031.

- By distribution channel, digital streaming platforms held 37.74% of the independent artists market share in 2025; physical retail is expected to expand at a 8.83% CAGR to 2031.

- By genre, hip-hop and rap led with 34.02% revenue share in 2025, but electronic and dance music are set to rise at an 8.02% CAGR through 2031 in the independent artists market.

- By geography, North America accounted for 42.83% of the independent artists market share in 2025, whereas Europe is forecast to advance at a 7.21% CAGR to 2031.

- Top 5 companies, such as Believe, DistroKid, AWAL, CD Baby, and UnitedMasters, hold major independent artists' market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Independent Artists Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Creator-centric royalty reforms on DSPs | +1.2% | Global, with early adoption in North America & Europe | Medium term (2-4 years) |

| AI-enabled production and marketing tools | +0.8% | Global, concentrated in tech-advanced markets | Short term (≤ 2 years) |

| Subscription fan-clubs and superfan monetization | +1.1% | North America, Europe, expanding to APAC | Medium term (2-4 years) |

| Live-streamed concerts and virtual venues | +0.7% | Global, accelerated in APAC markets | Short term (≤ 2 years) |

| Emergence of Web3 ownership frameworks | +0.5% | North America, Europe, select APAC markets | Long term (≥ 4 years) |

| Expansion of indie-service platforms | +0.9% | Global, with strongest growth in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Creator-Centric Royalty Reforms on DSPs

User-centric payout models are replacing pooled royalty systems, letting each listener’s fee go straight to the artists they actually play. Spotify’s 2024 rule that tracks need 1,000 annual streams for payout eligibility slices low-earning titles from the pool, redistributing funds to acts that cross the threshold. Meanwhile, the US Copyright Royalty Board lifted mechanical royalties from 10.5% to 15.1%, sending roughly USD200 million in back pay to songwriters and signaling policy intent to value creator labor more fairly[1]Source: Recording Academy, “Mechanical Royalty Rate Adjustment Explained,” recordingacademy.com. These reforms reward catalog depth and loyal fan bases but also raise the technical bar for emerging acts that lack rights-management support.

AI-Enabled Production and Marketing Tools

Artificial intelligence democratizes music production by eliminating technical barriers and reducing production costs that historically favored major label artists with access to expensive studio resources. Independent artists now access professional-grade production capabilities through AI-powered tools that handle mixing, mastering, and even composition assistance at a fraction of traditional costs. The International Music Summit Business Report reveals that 60 million people used AI to create music in 2024, representing 10% of consumers and indicating mainstream adoption of generative music tools.

Subscription Fan-Clubs and Superfan Monetization

Direct memberships convert superfans into predictable annual income, cutting reliance on per-stream pennies. Patreon reports USD52 average yearly spend per fan and USD110 per paying member, figures that far outstrip ad-share returns on short-form video apps. With 67% more musicians earning from subscriptions than five years ago, the model proves especially effective for niche artists who engage small but loyal audiences.

Live-Streamed Concerts and Virtual Venues

Virtual shows trim touring costs that keep climbing; some mid-level bands reported traditional tour expenses topping GBP34,000 (USD 45529.11) in 2024. Online venues remove travel and logistics and allow tiered ticketing, merch bundling, and post-event replays. Global ticket prices have risen 20% since 2021, making affordable virtual alternatives attractive for price-sensitive fans.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising platform fees and two-tier licensing | -1.4% | Global, most severe in mature markets | Short term (≤ 2 years) |

| Algorithmic discovery bias toward majors | -0.9% | Global, concentrated on major DSPs | Medium term (2-4 years) |

| Inflation-driven touring cost spikes | -0.8% | Global, acute in developed markets | Short term (≤ 2 years) |

| Fragmented rights-administration complexity | -0.6% | Global, varying by regulatory framework | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Platform Fees and Two-Tier Licensing

DSPs have introduced minimum-stream thresholds before royalties accrue, effectively removing the smallest earners from payouts and funneling dollars to higher-volume acts. At the same time, subscription price hikes have not translated into parallel rises in songwriter payouts, squeezing margins for independent creators. These policies push musicians to scale quickly or risk disqualification, adding financial pressure in the early career phase.

Algorithmic Discovery Bias Toward Majors

Streaming platform algorithms exhibit systematic bias toward major label content through recommendation systems, playlist placement mechanisms, and promotional feature allocation that favor artists with substantial marketing budgets and data optimization capabilities. As major labels pump marketing data into the system, independents struggle for playlist slots, so popular tracks become more visible while new voices fade. Artists must now invest in social media and community channels to sidestep algorithmic gatekeeping, elevating marketing costs relative to revenue potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Revenue Stream: Streaming Dominance Faces Diversification Pressure

Streaming held 41.78% of total revenue in 2025, yet its growth dipped to 6.1% as saturation set in. Merchandise and physical releases deliver the fastest expansion at an 8.45% CAGR, showing fans will pay premium prices for tangible products and collectible editions. That pivot diversifies the independent artists market, lessening reliance on low per-stream payouts. Licensing and sync deals add evergreen income as content creators seek authentic tracks for video and gaming. Acts who balance streaming reach with high-margin merch and subscriptions better shield themselves from payment model volatility.

The independent artists market size for merchandise segments is positioned to climb alongside superfan engagement programs, while live events—notably virtual venues—offer flexible monetization without geographical limits. This blended revenue stack becomes critical as tiered royalties cap earnings on smaller catalogues, driving creators to maximize fan lifetime value elsewhere.

By Distribution Channel: DSPs Maintain Control but Alternatives Scale

Digital streaming platforms controlled 37.74% of distribution volume in 2025, but growth has slowed as artists and fans explore higher-yield channels. Physical retail, helped by vinyl resurgence, is anticipated to grow at a 8.83% CAGR, underscoring consumer appetite for premium packages. Direct-to-fan portals such as Bandcamp let musicians keep up to 82% of sales, a stark contrast to the sub-1 cent streaming payout.

A multi-channel approach is now standard: use DSPs for discovery, then migrate superfans to stores and membership hubs where take-home margins exceed 80%. Social video platforms overlay this mix, feeding algorithmic virality that funnels traffic back to merchandise drops. The independent artists market size linked to physical formats may still trail streaming in absolute dollars, yet its higher margin profile improves creator sustainability.

By Genre: Hip-Hop Leadership Challenged by Electronic Innovation

Hip-hop and rap owned 34.02% of revenue in 2025, riding evergreen demand and efficient loop-based production that favors quick releases. Electronic and dance tracks, however, will record the highest genre CAGR at 8.02% to 2031. Festival circuits, DJ culture, and remix-friendly licensing drive fresh demand. Lower entry barriers—a laptop and software—let producers scale catalogues quickly, reinforcing the independent artists market’s push toward electronic sub-genres.

Rock, pop, and alternative keep solid followings, but higher recording costs slow volume output. Jazz and classical remain niche yet command high per-ticket prices and institutional grants. As electronic producers exploit low overheads and global streaming appeal, hip-hop’s share could slip, encouraging cross-genre collaborations to retain attention spans.

Geography Analysis

North America generated 42.83% of 2025 revenue in the independent artists market, leveraging mature streaming adoption, strong ARPU, and dense live-music circuits. Government grants in Canada add financial scaffolding, while the United States hosts sophisticated marketing and rights-management ecosystems that independent acts can rent on demand. Yet operating expenses and fierce competition temper upside.

Europe is the fastest-growing region in the independent artists market at a 7.21% CAGR, buoyed by multilingual content consumption and robust copyright rules. Domestic artists top the charts in France, Germany, and Spain, suggesting cultural preference for local voices, a tailwind for regional independents. EU funding programs and cross-border touring agreements make expansion cheaper than in North America.

Asia-Pacific offers unmatched audience scale, though ARPU remains low. Japan paid independent and self-released artists over 25 billion yen in 2024, 25% higher year on year, and half of those royalties came from foreign listeners. South Korea’s creator economy surpassed KRW 1 trillion in 2022, although earnings concentrate among a small elite. India’s streamer count is soaring, but payment conversion lags, challenging monetization.

South America delivers high growth independent artists market, led by Brazil’s USD 641 million recorded music revenue in 2024, up 18.7% versus 2023. Rapid smartphone adoption and vibrant local genres attract DSP investment, yet currency volatility can erode dollar returns. The Middle East and Africa recorded 24.7% growth in 2023, albeit off a lower base, aided by telco-bundled streaming and rising middle-class spending.

Competitive Landscape

Five distributors—Believe, DistroKid, AWAL, CD Baby, and UnitedMasters—anchor the ecosystem, supplying metadata compliance, rights collection, and marketing dashboards. Believe booked USD 510 million revenue in H1 2024, up 12.3%, affirming scale advantages[3]Source: Music Business Worldwide, “Believe Posts Double-Digit Growth in H1 2024,” musicbusinessworldwide.com. Fee structures range from fixed subscriptions to revenue splits, letting artists pick cost models aligned with catalog maturity.

Competitive focus has shifted from pure distribution toward integrated SaaS, analytics, and financing. EMPIRE’s February 2025 investment in un:hurd demonstrates an appetite for AI-driven campaign tools that can replicate label-level outreach for smaller budgets. Legal friction is also visible: Universal’s 2024 suit against Believe and TuneCore over alleged mass infringement underscores rising compliance risk as catalogues balloon.

White-space remains in emerging territories, niche genre platforms, and Web3 delivery where incumbents lag. Blockchain-native portals claim 100% payout to artists minus nominal transaction fees, but limited mainstream adoption means DSPs still dictate reach. Consolidation is likely as leading players acquire niche tech to tighten ecosystems, reinforcing the need for artists to diversify both partners and channels.

Independent Artists Industry Leaders

Believe

DistroKid

AWAL

CD Baby

UnitedMasters

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Tencent Music Entertainment agreed to acquire Ximalaya for USD2.9 billion, adding 600 million users to its audio portfolio.

- April 2025: GoldState Music raised USD 500 million in new funding to scale support services for self-releasing musicians.

- February 2025: EMPIRE partnered with marketing platform un:hurd to enhance data-driven promotion for independent rosters.

Global Independent Artists Market Report Scope

An independent artist is a musician or musical group not contracted with a record label. When it comes to bands, those that release their own material on self-published CDs or those that primarily exist to perform at concerts can be considered unsigned bands. Market overview, market size estimation for key segments and emerging trends in the market segments, market dynamics, and insights are covered in the report. The report will also cover information on some major global players.

Independent artists is segmented by type, end user, and geography. By type, the market is sub-segmented into performing arts, and visual arts. By end user, the market is sub-segmented into individual users and commercial users. By geography, the market is sub-segmented into North America, Europe, Asia-Pacific, Latin America, and Middle-East and Africa. The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Streaming |

| Live Performances |

| Merchandise and Physical Formats |

| Direct Fan Subscriptions |

| Licensing and Sync |

| Digital Streaming Platforms (DSPs) |

| Direct-to-Fan Marketplaces |

| Social / UGC Platforms |

| Physical / Retail |

| Pop |

| Hip-Hop / Rap |

| Electronic / Dance |

| Rock and Alternative |

| Other Genres (Jazz, Classical, etc.) |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | |

| Rest of Asia-Pacific | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Revenue Stream | Streaming | |

| Live Performances | ||

| Merchandise and Physical Formats | ||

| Direct Fan Subscriptions | ||

| Licensing and Sync | ||

| By Distribution Channel | Digital Streaming Platforms (DSPs) | |

| Direct-to-Fan Marketplaces | ||

| Social / UGC Platforms | ||

| Physical / Retail | ||

| By Genre | Pop | |

| Hip-Hop / Rap | ||

| Electronic / Dance | ||

| Rock and Alternative | ||

| Other Genres (Jazz, Classical, etc.) | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | ||

| Rest of Asia-Pacific | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the independent artists market?

The independent artists market reached USD 170.91 billion in 2026 and is projected to hit USD233.31 billion by 2031.

What is the current Independent Artists Market size?

In 2026, the Independent Artists Market size is expected to reach USD 170.91 billion.

Why are subscription fan-clubs important?

They generate average annual spends of USD 52 per supporter, offering predictable income that exceeds per-stream payouts.

Which region leads market growth?

Europe is estimated to gr Europe shows the fastest expansion with a 7.21% CAGR forecast through 2031, supported by strong local-language demand and cultural funding owe at the highest CAGR over the forecast period (2026-2031).

Who are the key distribution players for independent artists?

Believe, DistroKid, AWAL, CD Baby, and UnitedMasters dominate, providing global digital access and added marketing services.

Page last updated on: