Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.19 Billion |

| Market Size (2026) | USD 2.41 Billion |

| Market Size (2031) | USD 3.89 Billion |

| Growth Rate (2026 - 2031) | 10.06% CAGR |

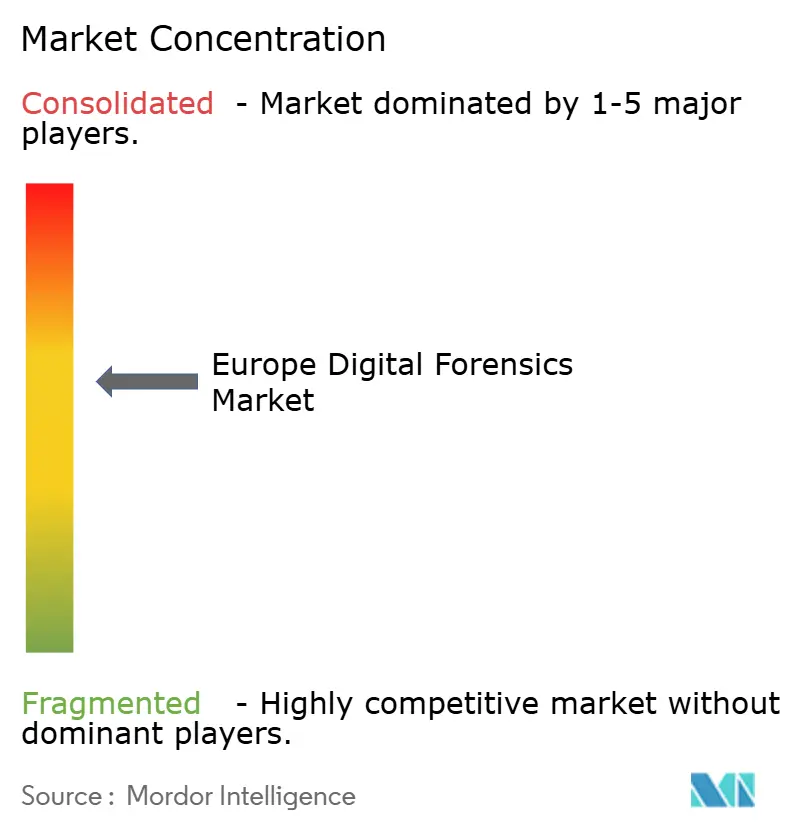

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Digital Forensics Market Analysis by Mordor Intelligence

The Europe digital forensics market size was valued at USD 2.19 billion in 2025 and estimated to grow from USD 2.41 billion in 2026 to reach USD 3.89 billion by 2031, at a CAGR of 10.06% during the forecast period (2026-2031). Consistent public-sector funding, tighter resilience rules such as the Digital Operational Resilience Act, and rising cross-border cybercrime keep spending on investigation platforms high.[1]European Parliament and Council, “Regulation 2022/2554 – DORA,” eur-lex.europa.eu Technology refresh cycles are shortening as AI analytics, cloud evidence capture, and automated case management replace legacy point tools, prompting vendors to pursue subscription models and managed offerings. Heightened ransomware activity across DACH, Benelux, and Nordic banking clusters forces enterprises to embed forensic readiness in incident-response playbooks. Venture funding for smart-vehicle and 5G security startups accelerates demand for new data-capture probes focused on in-vehicle systems and high-traffic edge nodes.

Key Report Takeaways

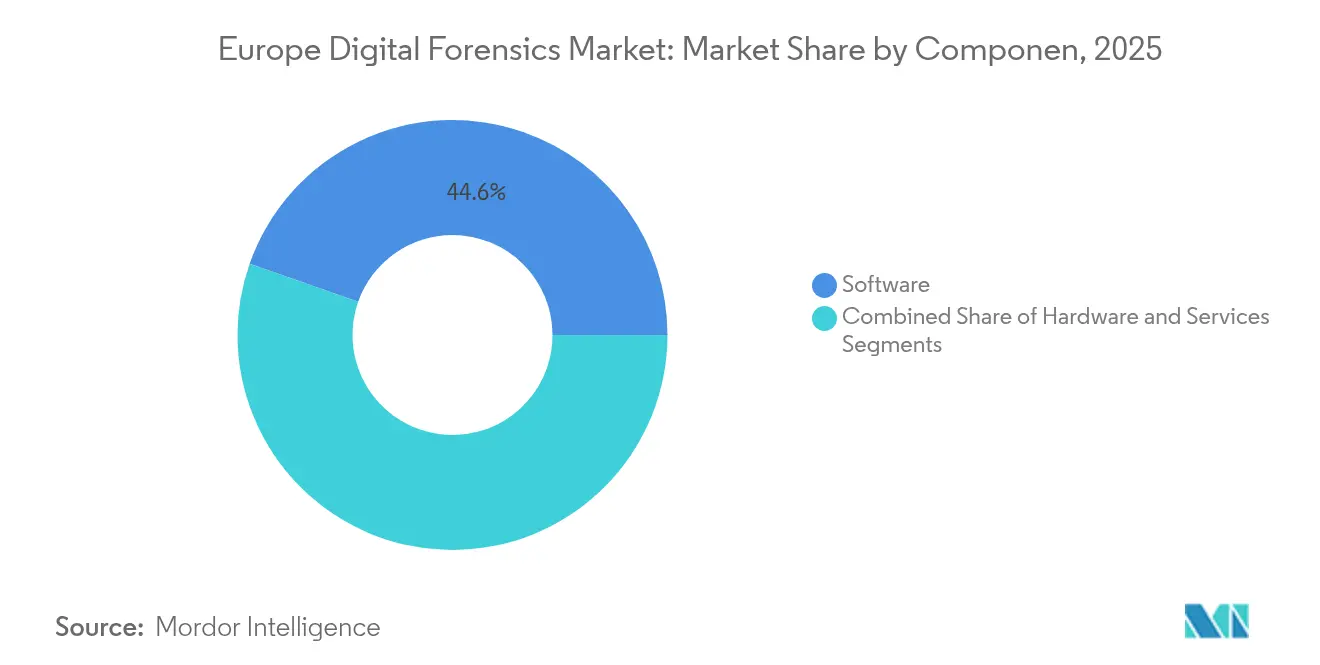

- By component, software retained 44.62% of the Europe digital forensics market share in 2025, while services are tracking the highest CAGR at 11.01% through 2031.

- By type, mobile device forensics led with 34.58% revenue share in 2025; cloud forensics is projected to expand at an 11.23% CAGR to 2031.

- By tool, data acquisition and preservation represented 31.47% of the Europe digital forensics market size in 2025, whereas forensic data analytics posts a 10.78% CAGR through 2031.

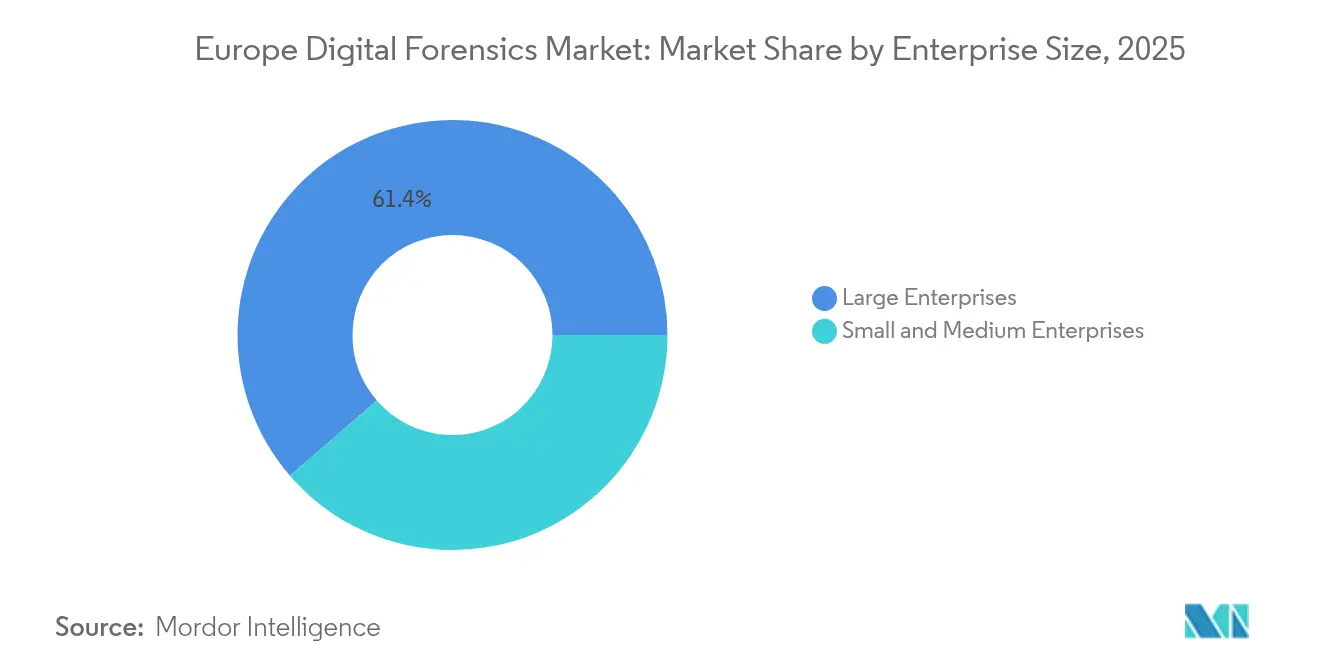

- By enterprise size, large enterprises commanded 61.35% share in 2025, but the SME segment is growing fastest at 10.55% CAGR to 2031.

- By end-user, government and law enforcement held 57.42% share in 2025; the BFSI sector records the strongest 11.33% CAGR on the back of DORA compliance.

- By geography, the United Kingdom captured 21.76% of the Europe digital forensics market in 2025, while Poland shows the quickest 10.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Digital Forensics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU DORA & NIS2 Compliance Accelerating Forensic Readiness | +2.8% | EU-wide, strongest in financial hubs | Medium term (2-4 years) |

| Proliferation of Encrypted Messaging Apps Boosting Mobile Forensics Demand | +2.1% | Global, concentrated in Western Europe | Short term (≤ 2 years) |

| Spike in Ransomware Incidents Across DACH & Benelux Elevating Incident-Response Forensics | +1.9% | DACH & Benelux, spillover to Nordic | Short term (≤ 2 years) |

| Connected-Vehicle Growth Creating New Vehicle/IoT Forensics Workloads | +1.6% | EU-wide, early adoption in Germany & Nordic | Long term (≥ 4 years) |

| 5G Roll-out Driving AI-based Network Forensics Investments | +1.4% | Advanced markets: UK, Germany, Nordic | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU DORA & NIS2 Compliance Accelerating Forensic Readiness

Since 17 January 2025, financial entities across the bloc must prove continuous monitoring, incident logging, and third-party oversight, turning forensic readiness from an optional add-on into a regulatory baseline. Supervisors now audit registers of ICT providers, so banks procure enterprise-wide evidence repositories that plug directly into SIEM stacks and automate breach notification. Harmonisation with NIS2 extends similar obligations to energy utilities and digital service providers, widening the European digital forensics market beyond core finance. Budget reallocations favour multi-tenant cloud platforms offering chain-of-custody validation, which lifts recurring revenue for software vendors.

Proliferation of Encrypted Messaging Apps Boosting Mobile Forensics Demand

End-to-end encryption in iOS 18 and disappearing-message defaults push investigators toward advanced bypass techniques that combine logical extraction, backup parsing, and AI pattern matching. Research shows 83.33% of deleted WhatsApp messages remain recoverable through notification artefacts when sophisticated tooling is used.[2]Makino. "Forensic Analysis of WhatsApp Disappearing Message on Unrooted Android Using Mobile Device Forensics Methodology NIST SP 800-101r1." tj.kyushu-u.ac.jpGreater technical complexity makes professional services indispensable, fuelling the services segment’s double-digit growth trajectory.

Spike in Ransomware Incidents Across DACH & Benelux Elevating Incident-Response Forensics

Germany logged 330,000 cybercrime cases in 2024 with EUR 178.6 billion (USD 190.8 billion) in losses, pushing insurers and regulators to request full post-event forensics within hours. [3]Protector, “Bundeslagebild Cybercrime 2024,” protector.de Municipal breaches such as Anhalt-Bitterfeld’s 2021 shutdown continue to influence the procurement of automated triage tools that shrink containment times. DDoS-for-hire services lower entry barriers, so organisations invest in cloud capture appliances capable of petabit traffic inspection to reconstruct attack timelines.

Connected-Vehicle Growth Creating New Vehicle/IoT Forensics Workloads

EU Regulation 155, mandatory for all new cars from July 2024, forces OEMs to keep tamper-resistant logs, giving rise to purpose-built probes that interface with CAN, LIN, and Automotive Ethernet buses. Academic frameworks such as CFPEA secure evidence hand-off between roadside units and cloud vaults, reducing chain-of-custody risk. Insurers and fleet operators now outsource periodic vehicle forensics audits, opening white-space for niche service boutiques.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GDPR Privacy Limits on Evidence Acquisition | -1.8% | EU-wide, strictest in Germany & Nordic | Long term (≥ 4 years) |

| End-to-End Encryption Increasing Investigation Time & Cost | -1.4% | Global, concentrated in privacy-conscious markets | Medium term (2-4 years) |

| Fragmented Police Procurement Budgets Slowing Adoption | -1.2% | National level, varying by country budget cycles | Medium term (2-4 years) |

| Shortage of ISO/IEC 17025-Accredited Labs in Europe | -0.9% | EU-wide, acute in smaller jurisdictions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

GDPR Privacy Limits on Evidence Acquisition

Privacy Impact Assessments now accompany most large-scale forensic cases, lengthening engagement cycles and pushing smaller labs to defer complex cross-border work. National differences in supervisory interpretation mean evidence gathered legally in one state may face challenge in another, adding legal-review overhead. Investment is shifting toward selective-collection software that can hash and flag personally identifiable data instead of extracting entire disk images, aligning practice with data-minimisation rules.

End-to-End Encryption Increasing Investigation Time & Cost

Policy debates over lawful access remain unresolved; meanwhile, forensic teams spend more budget on FPGA-based accelerated cracking rigs and specialist SaaS decryption platforms. Smaller providers struggle to amortise these capital costs, raising barriers to entry and reinforcing vendor consolidation dynamics. Regulators such as the UK are examining technical backdoor proposals, but uncertainty keeps procurement focused on advanced brute-force and metadata-correlation tools.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Drive Market Transformation

Software retains the dominant 44.62% slice of the European digital forensics market in 2025, thanks to scaled subscription pricing and continuous feature updates covering mobile, cloud, and SaaS artefact parsing. Hardware spend slows as acquisition tasks shift into virtual machines, yet proprietary dongles for chip-off extraction and high-speed write-blockers stay necessary for severe criminal investigations. Overall, a service-centric operating model positions providers to capture expansion budgets while protecting customers from skills shortages.

Services recorded the quickest 11.01% CAGR between 2026-2031 as corporates outsource complex evidence collection to specialised teams that operate remote labs and on-demand analytics. Large financial institutions sign multi-year managed forensics contracts that embed consultants during resilience-testing cycles mandated by DORA.Vendors differentiate through court-ready documentation workflows and API integrations with e-discovery suites, reducing hand-off friction for legal counsel

By Type: Mobile Device Forensics Leads Market Evolution

Mobile platforms captured 34.58% of the Europe digital forensics market size in 2025, reflecting smartphone ubiquity across personal and enterprise workflows. Investigators focus on encrypted chat artefacts, sensor fusion data, and artefact timeline stitching to recreate user journeys. Companion wearables add another evidence layer, further cementing handset analysis as a foundational discipline.

Cloud forensics grows at 11.23% CAGR as multi-tenant SaaS moves key evidence off-premise. Providers now supply snapshot tooling that freezes virtual instances and automates jurisdiction mapping to maintain legal validity. Computer forensics share declines, though endpoint artefacts still anchor insider-threat and fraud probes. Emergent vehicle and IoT evidence types spur integrated platforms able to stitch log data from ECUs, smart sensors, and central clouds in a single case file.

By Tool: Data Analytics Transforms Investigation Capabilities

Data acquisition and preservation solutions held 31.47% of the Europe digital forensics market share in 2025 because chain-of-custody integrity starts at the point of capture. Imaging products now trigger automatic SHA-512 hashing and evidence-locker synchronisation to support courtroom validation standards.

Forensic data analytics posts a 10.78% CAGR as machine-learning engines correlate chat, location, and financial artefacts within minutes, collapsing manual review cycles. Review-and-reporting tools evolve to enable multi-jurisdiction case teams to annotate artefacts simultaneously, embedding audit trails. Decryption tool spending rises, but growth remains niche given ongoing regulatory debate around lawful-access mandates.

By Enterprise Size: SMEs Accelerate Digital Forensics Adoption

Large enterprises still account for the bulk of spend, yet SMEs add the most new customers with a 10.55% CAGR through 2031. EU legislation assigns identical incident-reporting duties to smaller firms, compelling them to adopt affordable SaaS forensic suites that bundle automated playbooks and regulatory templates. National grant programs offset compliance costs, boosting vendor pipeline activity in manufacturing, retail, and professional services verticals.

The Europe digital forensics market sees community colleges and regional chambers launch micro-credential courses to close skill gaps exposed by SME adoption. Managed-security providers partner with boutique forensic labs to deliver tier-2 support, ensuring investigators can escalate complex artefact analysis without full-time staff. Over time, SME uptake expands addressable revenue while diversifying incident datasets used to train AI engines.

By End-user Industry: BFSI Sector Drives Rapid Growth

Government and law-enforcement agencies commanded 57.42% of 2025 revenue, yet the BFSI domain grows fastest at 11.33% CAGR as supervisors tie operational-resilience scoring to forensic maturity. Banks deploy centralised evidence lakes feeding automated risk dashboards that translate technical artefacts into monetary impact visuals for boards.

Telecom operators upgrade lawful-intercept gateways to ingest 5G slice logs, while healthcare systems invest in immutable audit chains to safeguard patient confidentiality. Energy utilities pilot forensic collectors on SCADA networks to satisfy NIS2, and e-commerce portals integrate payment-fraud evidence capture to accelerate charge-back disputes. Diversified sectoral adoption embeds the Europe digital forensics market deeply across the real economy.

Geography Analysis

The United Kingdom retained its 21.76% leadership position in 2025, supported by a cybersecurity sector that generated GBP 13.2 billion (USD 16.7 billion) in revenue and exported GBP 7.2 billion (USD 9.1 billion) in services. Active policy work on a Cyber Security and Resilience Bill and a public stance against synthetic-media abuses spur further investment in forensic deepfake-analysis tools. Capital continues to flow into safety-tech vendors, reinforcing the nation’s innovation cluster.

Germany stands as the largest single continental market after reporting EUR 178.6 billion (USD 190.8 billion) in cybercrime damages during 2024. Federal initiatives to expand ISO/IEC 17025-accredited labs and Fraunhofer training programs strengthen the professional talent pipeline. France benefits from its EUR 1 billion (USD 1.1 billion) cybersecurity fund under France 2030, with EUR 39 million (USD 41.7 million) allocated to 17 targeted projects that include next-generation forensics.

Poland records the fastest 10.74% CAGR on the back of USD 2.5 billion in governmental cyber programs and the EU’s highest 32% incident rate among firms. Nordic collaboration tightens after large-scale DDoS attacks, with Norway forecasting a USD 20.65 million market by 2029 at 10.07% growth. Denmark’s Digital Growth Strategy and Norway’s Data Economy study underscore shared recognition that digital-evidence management is critical to economic sovereignty

Competitive Landscape

The Europe digital forensics market remains moderately concentrated; the top five vendors collectively control about 48% of revenue, leaving room for specialised entrants. Cellebrite grew annual recurring revenue by 26% to USD 346 million in 2024, driven by AI modules that compress case review from months to weeks. The firm’s push for FedRAMP authorisation signals strategic alignment with sovereign-cloud mandates in defence and public-safety segments.

Emerging academic spinouts such as the University of Winchester’s “Spidernet” illustrate how research labs commercialise cloud-scale mapping algorithms that track digital “DNA” across smart-device ecosystems. Niche startups focus on IoV log harvesters and quantum-resistant evidence lockers, exploiting product gaps in incumbent suites. Established integrators partner with telco operators to insert lawful-intercept probes at the 5G edge, expanding managed-service addressable revenue.

M&A activity revolves around talent acquisition and cross-border expansion. Vendors buy boutique labs in Poland and the Baltic to secure low-cost analyst benches and local language expertise. Strategic alliances with legal-technology providers help convert forensic artefacts directly into e-discovery deliverables, positioning suppliers as end-to-end litigation-support partners. Overall, innovation velocity and regulatory complexity dictate that competitive advantage hinges on continuous R&D and compliance alignment.

Europe Digital Forensics Industry Leaders

-

MSAB AB

-

LogRhythm Inc.

-

IBM Corporation

-

PricewaterhouseCoopers LLP

-

Nuix Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: BPI France earmarked EUR 25 million (USD 26.7 million) for blockchain startups, expanding investigative tooling for crypto-asset tracing.

- March 2025: France launched PROQCIMA under France 2030, dedicating EUR 1.8 billion (USD 1.9 billion) to quantum computing prototypes with direct implications for post-quantum forensics.

- January 2025: DORA entered full application, obliging financial entities to maintain detailed ICT supplier registers and periodic resilience testing, thereby boosting forensic readiness spending.

- November 2024: ENISA’s NIS Investments report showed enterprises dedicating 9% of IT budgets to security and planning staff additions, confirming rising forensic workloads.

Europe Digital Forensics Market Report Scope

Digital forensics is identifying, preserving, analyzing, and presenting digital evidence. Digital forensics enables the extraction of evidence through the analysis and evaluation of data from digital devices and is used to recover and inspect the data while maintaining its originality.

Various digital forensics, including mobile forensics, computer forensics, network forensics, and other types (e-mail forensics, cloud forensics, social media forensics, IoT forensics, disk forensics, and database forensics), are considered under the scope.

The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

By Component

| Hardware |

| Software |

| Services |

By Type

| Computer Forensics |

| Mobile Device Forensics |

| Network Forensics |

| Cloud Forensics |

| Database Forensics |

| IoT and Embedded Device Forensics |

By Tool

| Data Acquisition and Preservation |

| Data Recovery and Reconstruction |

| Forensic Data Analysis |

| Review and Reporting |

| Forensic Decryption and Password Cracking |

By Enterprise Size

| Large Enterprises |

| Small and Medium Enterprises |

By End-user Industry

| Government and Law Enforcement Agencies |

| BFSI |

| IT and Telecom |

| Healthcare |

| Retail and E-commerce |

| Energy and Utilities |

| Manufacturing |

| Transportation and Logistics |

| Defense and Aerospace |

| Education |

By Country

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Nordics |

| Rest of Europe |

| By Component | Hardware |

| Software | |

| Services | |

| By Type | Computer Forensics |

| Mobile Device Forensics | |

| Network Forensics | |

| Cloud Forensics | |

| Database Forensics | |

| IoT and Embedded Device Forensics | |

| By Tool | Data Acquisition and Preservation |

| Data Recovery and Reconstruction | |

| Forensic Data Analysis | |

| Review and Reporting | |

| Forensic Decryption and Password Cracking | |

| By Enterprise Size | Large Enterprises |

| Small and Medium Enterprises | |

| By End-user Industry | Government and Law Enforcement Agencies |

| BFSI | |

| IT and Telecom | |

| Healthcare | |

| Retail and E-commerce | |

| Energy and Utilities | |

| Manufacturing | |

| Transportation and Logistics | |

| Defense and Aerospace | |

| Education | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Nordics | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current size of the Europe digital forensics market?

The market is valued at USD 2.41 billion in 2026 and is projected to hit USD 3.89 billion by 2031 at a 10.06% CAGR.

Which component is growing fastest?

Services grow at 11.01% CAGR as organisations outsource complex evidence collection and analysis tasks.

Why is the BFSI sector investing heavily in digital forensics?

The Digital Operational Resilience Act mandates continuous incident logging and resilience testing, driving 11.33% CAGR spending within banks and insurers.

How does GDPR affect forensic investigations?

GDPR imposes strict data-minimisation rules and mandatory privacy assessments, adding cost and time to evidence acquisition.

Which geography shows the fastest growth?

Poland leads with a 10.74% CAGR due to high incident rates and USD 2.5 billion in government cyber investments.

What emerging technology will reshape forensic tools?

AI-driven analytics that correlate multi-source artefacts in real time are reducing investigation timelines and enabling proactive threat-hunting across 5G and cloud environments.

Page last updated on: