Network Forensics Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

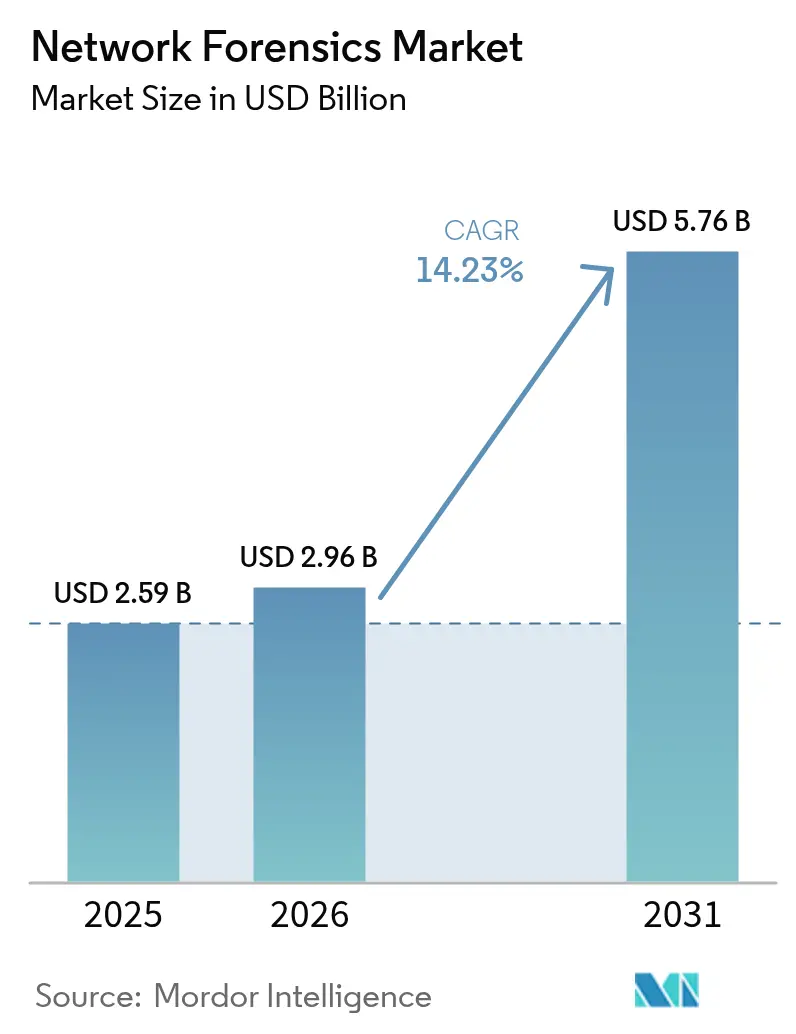

| Market Size (2026) | USD 2.96 Billion |

| Market Size (2031) | USD 5.76 Billion |

| Growth Rate (2026 - 2031) | 14.23% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Network Forensics Market Analysis by Mordor Intelligence

Network forensics market size in 2026 is estimated at USD 2.96 billion, growing from 2025 value of USD 2.59 billion with 2031 projections showing USD 5.76 billion, growing at 14.23% CAGR over 2026-2031. The adoption curve is steep because packet-level visibility has become indispensable for rapid breach diagnosis, regulatory reporting and cyber-insurance compliance. Spending momentum is especially strong where hybrid-cloud traffic, 5G roll-outs and encrypted east-west flows expose blind spots that traditional perimeter tools overlook. Vendors are therefore embedding forensic functionality into Network Detection and Response (NDR) platforms, shrinking tool sprawl and lowering mean-time-to-respond. Demand is also lifted by insurers that now require packet evidence for claims validation and by regulators such as the SEC and the EU’s Digital Operational Resilience Act, which mandate timely, well-documented incident disclosure.[1]Fortinet, "What Is The Digital Operational Resilience Act (DORA)?", www.fortinet.com

Key Report Takeaways

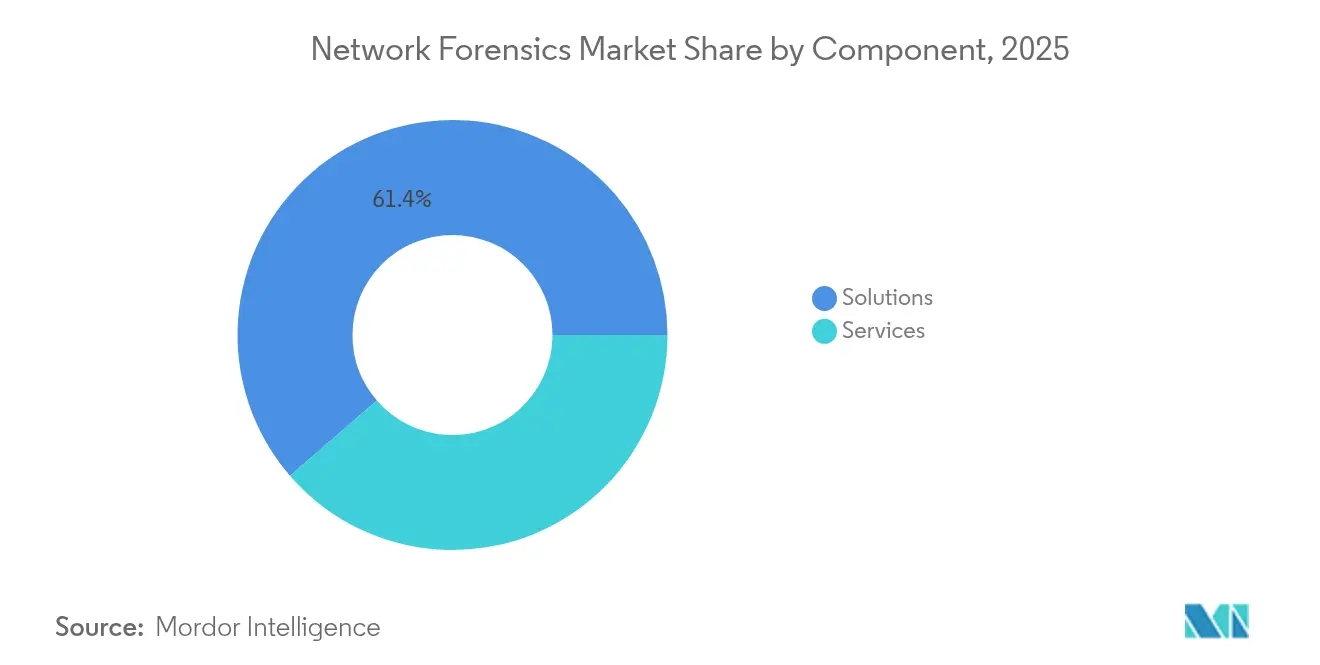

- By component, Solutions led with 61.35% of network forensics market share in 2025, while Services are set to expand at an 17.75% CAGR through 2031.

- By deployment model, on-premise installations held 52.20% of the network forensics market size in 2025; cloud-hosted options are projected to grow at a 22.05% CAGR between 2026-2031.

- By organization size, large enterprises commanded 57.30% share of the network forensics market size in 2025; small and mid-sized enterprises (SMEs) register the fastest growth at 18.95% CAGR to 2031.

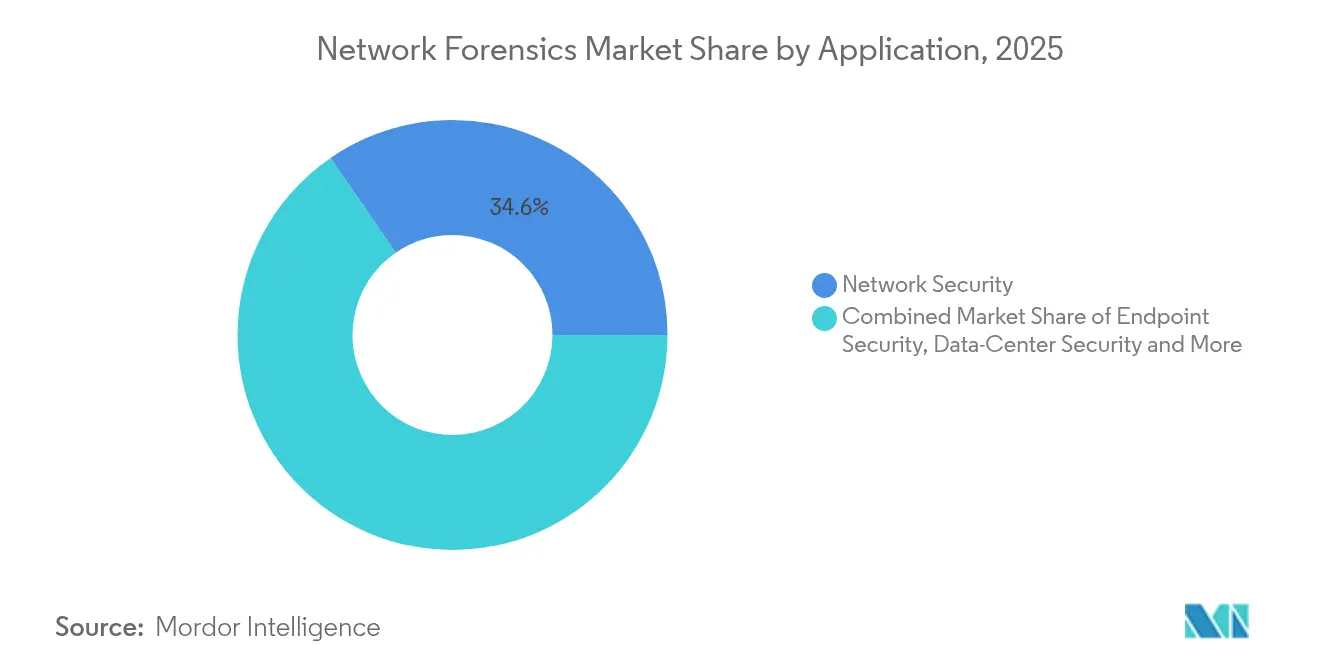

- By application, Network Security accounted for 34.60% of network forensics market share in 2025, whereas Endpoint Security is forecast to rise at a 20.6% CAGR through 2031.

- By end-user industry, BFSI led with 27.45% revenue share in 2025; Healthcare is advancing at a 17.3% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Network Forensics Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of cloud & hybrid IT traffic visibility needs | +3.2% | Global (North America & Europe core) | Medium term (2-4 years) |

| Escalating frequency & sophistication of cyber-attacks | +4.1% | Global | Short term (≤ 2 years) |

| Stringent breach-reporting mandates (GDPR, SEC, DORA) | +2.8% | North America & EU, spillover to APAC | Medium term (2-4 years) |

| Convergence of NDR & forensics reducing tool sprawl | +1.9% | Global, early adoption in North America | Medium term (2-4 years) |

| 5G standalone roll-outs expanding east-west traffic capture | +1.5% | APAC, North America, Europe | Long term (≥ 4 years) |

| Cyber-insurance policies mandating packet-level evidence | +2.3% | North America & Europe, emerging APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Proliferation of Cloud & Hybrid IT Traffic Visibility Needs

Cloud migration has outpaced traditional monitoring, leaving 73% of enterprises unable to derive actionable insight from existing toolsets. East-west traffic among ephemeral workloads often vanishes before legacy collectors capture it, prompting demand for cloud-native capture engines that automate evidence gathering across multiple IaaS and PaaS domains. Emerging offerings integrate packet capture, artifact preservation and timeline reconstruction in a single workflow, improving investigative efficiency and supporting consistent policy enforcement across on-premises, public cloud and hybrid environments. Providers have begun to embed smart storage tiering, enabling long-term retention without linear cost escalation and ensuring regulators can audit forensic evidence on demand.

Escalating Frequency & Sophistication of Cyber-Attacks

Global breach costs climbed to USD 4.88 million in 2024, while credential-theft incidents surged 84%, fueling adoption of network analytics that surface anomalous authentication spikes and lateral-movement beacons.[2]Arthur J. Gallagher, "2025 Cyber Insurance Market Conditions Outlook, www.ajg.com Healthcare institutions remain under siege as 93% encountered a breach within three years, pushing them to deploy continuous packet capture that pinpoints dwell time and attack provenance. [3] TechMagic, "Top 5 Healthcare Cyber Threats and How to Avoid Them.", www.techmagic.co Enterprises now integrate enriched network telemetry into threat-hunting routines that cross-reference endpoint, identity and cloud logs, raising the bar for adversaries and accelerating post-incident forensics for legal, regulatory and insurance stakeholders.

5G Standalone Roll-outs Expanding East-West Traffic Capture

5G’s service-based architecture segments traditional monoliths into discrete cloud-native functions, multiplying east-west session density. Manufacturing and healthcare pilots already rely on 5G slices that handle telemetry, robotics and imaging workloads, yet these carry fresh exposure points. Specialized probes decode GPRS Tunnelling Protocol (GTP), HTTP/2 and HTTP/3 headers at line rate, letting operators visualize subscriber behaviour and thwart signaling-layer abuse. Scalable, containerised capture nodes provide elastic packet buffering so carriers keep pace with quadrupling throughput expectations by 2028.

Cyber-Insurance Policies Mandating Packet-Level Evidence

Underwriters tightened terms as premiums swelled alongside ransomware severity. Policies now stipulate demonstrable packet evidence for claims adjudication, elevating network forensics from best practice to board-level requirement. Customer enquiries increasingly originate from risk-transfer conversations rather than security budgets, broadening the addressable base beyond highly regulated verticals. Insurers also recommend minimum retention windows, compelling buyers to modernize storage hierarchies and de-duplication strategies.

Restraints Impact Analysis of Network Forensics Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of skilled packet-level investigators | -1.8% | Global, severe in APAC | Medium term (2-4 years) |

| High CAPEX of >40 Gbps capture appliances | -1.6% | Emerging markets, SMEs worldwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled Packet-Level Investigators

Demand for information-security analysts is projected to expand 32% between 2022-2032, yet universities and training pipelines lag, leaving 54% of employers unable to fill packet-analysis roles.[4]Drummond, Rachel, "Computer Forensics Examiner Job Outlook & Salary Info." Forensics Colleges, www.forensicscolleges.comThe deficit inflates salary baselines beyond USD 119,000 and amplifies operational risk when alerts outstrip triage capacity. Organizations respond by shifting routine parsing to AI-assisted playbooks, outsourcing level-1 monitoring to managed service partners and prioritizing tool usability so non-specialists can navigate packet timelines with minimal ramp-up.

High CAPEX of >40 Gbps Capture Appliances

Enterprises processing tens of petabytes per month often face multi-million-dollar price tags for top-tier probes and petascale storage. The financial hurdle is acute for SMEs and public-sector agencies whose compliance mandates still dictate two-week retention. Next-generation offerings emphasize FPGA-accelerated de-duplication, smart indexing and cloud-burst tiering, trimming on-premise hardware footprints. Consumption-based licensing and appliance virtualization further democratize adoption and permit incremental scaling aligned with traffic growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Network Forensics Market Segment Analysis

By Component:

Solutions Prevail as Service Uptake AcceleratesSolutions generated 61.35% of network forensics market revenue in 2025, a position powered by demand for high-speed packet capture, behavioural analytics and encrypted-traffic visibility. Feature velocity is brisk, with vendors embedding machine-learning algorithms that establish baseline traffic profiles and surface deviations in seconds. The services segment is smaller today yet expands at an 17.75% CAGR because organizations need integration, tuning and continuous investigation support while talent remains scarce. Providers bundle assessment, incident-response retainers and managed detection to convert one-time licences into recurring revenue streams. Over the forecast horizon, joint go-to-market programs between hardware vendors and global system integrators will further amplify adoption, especially in regulated industries that require 24-hour evidence retrieval.

Investment patterns suggest that automation-ready solutions will dominate capital budgets, while advisory services grow as strategic overlays that maximize tooling value. The blended model supports life-cycle management from deployment to incident post-mortems, ensuring the network forensics market retains strong pull across diverse buyer personas.

By Deployment Mode:

Cloud Momentum ContinuesOn-premise deployments maintained 52.20% share of network forensics market size in 2025 because many financial, government and defense entities require local custody of evidence. Nevertheless, cloud-native deployments soar at a 22.05% CAGR as traffic migrates to SaaS, IaaS and containerised stacks. Cloud collectors orchestrate evidence gathering across regions, auto-scale during volumetric events and decouple storage from compute, slashing upfront expense. Hybrid architectures emerge where sensitive data stays on site, yet burst workloads and less regulated segments leverage cloud collectors.

Platform providers now ship lightweight sensors deployable in Kubernetes clusters or as side-cars, ensuring parity of telemetry between virtual networks and physical switch spans. Compliance teams value the immutable audit trails that cloud object stores enable, while finance teams appreciate opex-based consumption that aligns spend with seasonal traffic variance. Together these dynamics reinforce an enduring pivot toward distributed collection topologies within the broader network forensics market.

By Organization Size:

Large Enterprises Lead While SME Adoption QuickensLarge enterprises accounted for 57.30% of 2025 revenue thanks to expansive traffic matrices that demand multi-gigabit capture fabrics. These organizations often integrate forensics into security information and event management pipelines to create unified evidence hubs. They also pilot AI-driven investigations that accelerate root-cause discovery and support red-team validation campaigns. SMEs, although historically constrained by budgets and staffing, now adopt cloud-delivered forensics at a 18.95% CAGR, aided by simplified pricing tiers and cyber-insurance mandates.

Vendor roadmaps increasingly feature easy-to-deploy appliances with guided workflows, enabling resource-limited teams to achieve compliance benchmarks. As economies of scale lower price points, SME penetration is expected to inject new volume into the network forensics market, broadening addressable demand beyond Fortune 1000 customers and national governments.

By Application:

Network Security Dominates, Endpoint Integration SurgesNetwork Security held 34.60% of network forensics market share in 2025 because packet capture remains the bedrock for lateral-movement detection and infrastructure hygiene. Continuous full-packet capture delivers evidentiary artefacts essential for root-cause analysis and prosecution. Endpoint Security posts a 20.6% CAGR as organizations pair host telemetry with network flows to achieve layered visibility. Correlated analytics expose evasion tactics that bypass single vantage points, thereby enriching detection quality.

Data-center security also gains traction as east-west traffic within software-defined fabrics obscures attacker pathways. Operators deploy micro-segmented tap architectures coupled with high-speed indexers that replay conversations in microseconds, sustaining service-level agreements and forensic fidelity. Application-specific monitoring is now bundled into observability stacks, allowing DevSecOps teams to troubleshoot performance and security anomalies via the same data plane—a convergence that deepens market stickiness.

By End-User Industry:

BFSI Leads, Healthcare Rises QuicklyFinancial institutions represented 27.45% of 2025 sales given stringent fraud-monitoring, audit and compliance duties. Real-time packet capture facilitates dispute arbitration, protects payment rails and supports regulator examinations. Healthcare, expanding at 17.3% CAGR, pushes vendors to deliver HIPAA-aligned evidence chains and ransomware containment playbooks. Digital front-door initiatives such as telemedicine widen attack surfaces, making network telemetry indispensable for post-breach diagnosis.

Telecom operators embed forensics to safeguard 5G core functions and assure service uptime, while government and defense agencies require deep traffic reconstruction to counter espionage campaigns. Retailers capture card-holder data flows for PCI-DSS audits, and manufacturers map operational technology traffic to uncover malware that targets programmable-logic controllers. Combined, these varied requirements sustain multi-vertical growth across the network forensics market.

Geography Analysis

North America Network Forensics Market

North America held 39.60% share in 2025, driven by SEC disclosure rules that enforce four-day breach reporting and by an advanced cyber-insurance ecosystem that ties coverage to evidence quality. U.S. enterprises deploy AI-enabled analysis to overcome skills shortages and maintain comprehensive logs for potential litigation or regulatory inquiry. Canada follows a comparable trajectory, underpinned by mandatory privacy breach notifications and concentrated presence of critical infrastructure operators.

Europe Network Forensics Market

Europe captured 27.70% of network forensics market revenue in 2025, benefiting from GDPR enforcement and the January 2025 start of DORA. Banking hubs in the United Kingdom, Germany and France doubled packet-capture budgets to achieve 24-hour incident notification. Public-sector projects focused on 5G corridors channel EUR 865 million (USD 931 million) into network build-outs, prompting new security monitoring layers. Cross-border data-sharing frameworks inside the EU also stimulate demand for standardized forensic workflows that meet multi-jurisdictional evidence admissibility criteria.

APAC Network Forensics Market

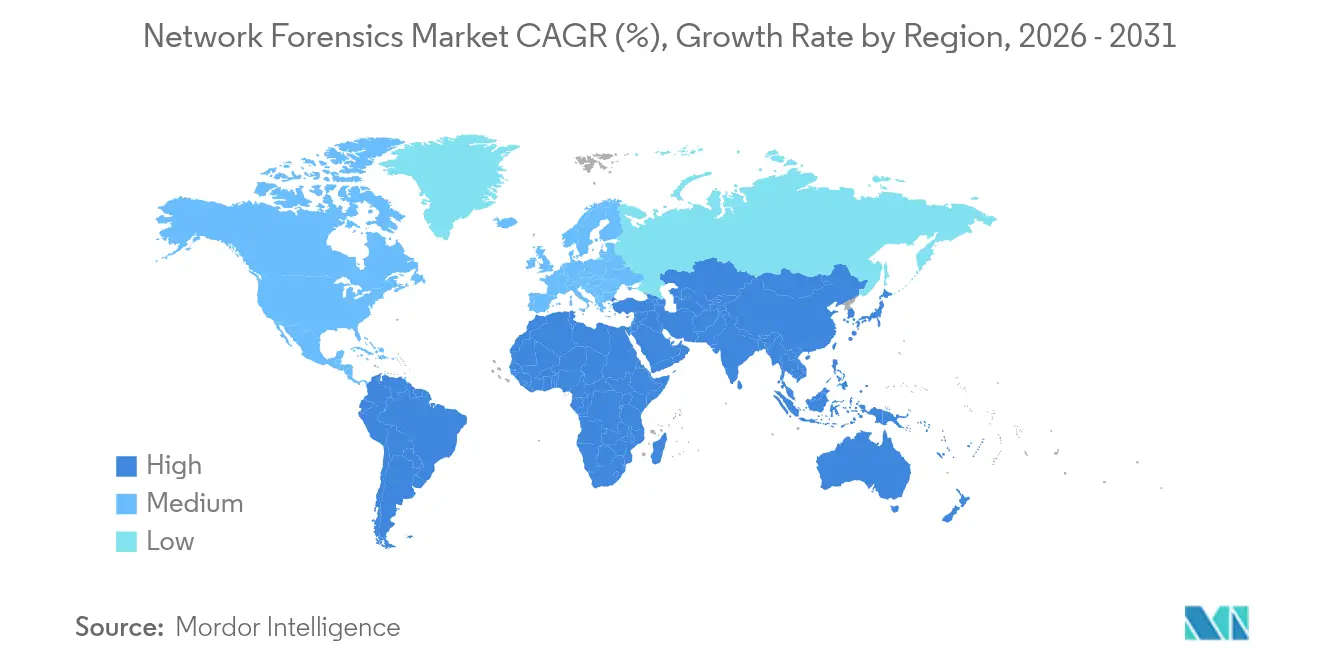

Asia-Pacific is the fastest-growing theatre with a 17.65% 2026-2031 CAGR. China’s digital-finance expansion, India’s 5G auctions and Australia’s critical-infrastructure reforms create sustained opportunities. South Korea’s digital forensics sector alone is projected at USD 3.52 billion by 2025, reflecting public-private investment in national cyber-resilience. While skills shortages remain acute, managed security services offset local gaps and accelerate uptake among medium-sized enterprises. The region’s exposure to state-sponsored campaigns further elevates the relevance of network forensics market tools that can reconstruct sophisticated, multi-stage intrusions.

Regulatory Landscape

Network forensics adoption is increasingly shaped by cyber risk management and incident-disclosure obligations that raise expectations for evidentiary logging, monitoring, and data retention. In the United States, NIST Cybersecurity Framework (CSF) 2.0 (released February 2024) formalized a stronger governance focus, while a January 2025 federal requirement driven by DHS/CISA actions pushed agencies to establish enterprise technical capability to access endpoint detection and response (EDR) data across the federal civilian environment, reinforcing centralized visibility and incident validation workflows.

In Europe, the NIS2 Directive (EU) 2022/2555 and the October 2024 Commission Implementing Regulation (EU) 2024/2690 tightened technical expectations around cybersecurity risk management measures, including monitoring, logging, and support for forensic investigation. Parallel policy actions in 2026 also reinforced monitoring rigor for critical infrastructure and national security environments, including the March 2026 approval of NERC Reliability Standard CIP-003-11 in the United States for bulk electric system cyber assets and the June 2026 White House NSPM-12 for National Security Systems cybersecurity governance and baselines, both of which lift demand for defensible packet and telemetry evidence in regulated investigations.

Value Chain Analysis

The network forensics value chain begins with visibility and collection inputs (network TAPs/SPAN access, sensors, and high-speed packet capture nodes deployed across data centers, branch sites, and cloud or virtual networks), then moves into capture and retention layers (lossless packet capture, indexing, compression, and tiered storage). Most of the value creation sits in analysis and reconstruction software that converts packets and flows into sessions, timelines, and investigation artifacts, increasingly embedded within NDR-aligned workflows to reduce manual PCAP handling and speed incident response.

Integration and consumption depend on interoperability requirements, with platforms connecting into SIEM, SOAR, and XDR ecosystems for correlation, case management, and automated playbooks. Services and channel partners (system integrators, managed security providers, and incident response retainers) operationalize deployments where packet-level investigator shortages persist, while standards and guidance (for example, NIST SP 800-86 for forensic guidance and ISO/IEC 27033-1 for network security) influence how organizations implement evidence handling, chain-of-custody practices, and audit-ready logging across hybrid estates.

Competitive Landscape

The vendor field shows moderate consolidation as large cybersecurity suites absorb specialized forensics startups, aiming to deliver end-to-end security fabrics. Cisco’s 2024 acquisition of Splunk embeds full-stack observability and packet replay into a single portfolio, enabling cross-sell synergies across its installed base. Palo Alto Networks enhanced its Prisma Access service with TLS 1.3 decryption, strengthening encrypted-traffic analysis and locking customers into its cloud security platform.

Specialists such as ExtraHop, NIKSUN and Darktrace differentiate through FPGA-accelerated capture, protocol-agnostic analytics and self-learning algorithms that adapt to dynamic baselines. They also partner with traffic-capture hardware firms to bypass high CAPEX hurdles via joint reference architectures. Axellio’s alliance with Garland Technology and Mira Security illustrates this strategy by combining tap visibility, traffic decryption and high-speed storage distribution into a bundled solution.

Strategic road maps converge on three imperatives: encrypted-traffic visibility, cloud-agnostic deployment and analyst productivity. Vendors invest in AI copilots that auto-generate incident timelines, recommend investigative next steps and surface policy gaps. Meanwhile, open API frameworks facilitate integration with Security Orchestration, Automation and Response (SOAR) systems, cementing the network forensics market as a core telemetry source for fully automated defense pipelines.

Network Forensics Industry Leaders

-

Broadcom Inc. (Symantec Corporation)

-

Cisco Systems Inc.

-

IBM Corporation

-

Netscout Systems Inc.

-

Valvi Solutions Inc.

- *Disclaimer: Major Players sorted in no particular order

Network Forensics Market Companies Covered in this Report

- Broadcom (Symantec)

- Cisco Systems

- IBM Corporation

- Netscout Systems

- Trellix (FireEye)

- RSA Security

- AccessData (OpenText)

- LogRhythm

- LiveAction

- NIKSUN

- Rapid7

- Palo Alto Networks

- Darktrace PLC

- ExtraHop Networks

- Vectra AI

- CrowdStrike Holdings

- Fortinet Inc.

- Check Point Software Tech.

- Sophos Group

- Gigamon

Market Opportunities and Future Outlook

Regulatory-driven forensic readiness creates whitespace for always-on evidence capture and faster investigation workflows that align with compressed reporting timelines and auditability needs. NIS2 (Directive (EU) 2022/2555) and the October 2024 Commission Implementing Regulation (EU) 2024/2690 explicitly connect cybersecurity risk management measures with monitoring and logging capabilities that support forensic investigations, shifting buyer preferences toward standardized, defensible telemetry pipelines rather than ad hoc packet collection.

Product and platform opportunities are concentrating in three areas: (i) encrypted traffic visibility and retrospective investigation at scale, supporting incident validation and insurance and regulatory narratives; (ii) design-time and programmable telemetry approaches (for example, telemetry architectures evaluated against MITRE ATT&CK hypotheses and programmable pipelines) that help organizations prove coverage and reduce blind spots across hybrid cloud and SDN domains; and (iii) device and network-appliance logging features aligned with government guidance such as UK NCSC recommendations on protective monitoring and digital forensics, which emphasize secure remote logging and machine-readable log formats. Vendor roadmaps that combine packet evidence with AI-ready data pipelines (as seen in communications service provider observability and security tooling) also create room for solutions that reduce analyst workload while preserving chain-of-evidence quality.

Recent Industry Developments in Network Forensics Market

- March 2026: Broadcom introduced Symantec CBX (Carbon Black XDR), combining Symantec and Carbon Black capabilities in a cloud-based platform designed for under-resourced security operations teams. The integrated approach improves correlation across endpoint, network, and data signals, supporting faster triage and more consistent incident evidence packaging in hybrid environments.

- February 2026: NETSCOUT extended Omnis AI Insights to communications service providers, focusing on transforming network data into AI-ready smart data for operational and security use cases. The move reinforces the shift toward scalable data pipelines that can feed automated threat detection and investigation across high-volume service provider networks.

- July 2025: NETSCOUT added Adaptive Threat Analytics to its Omnis Cyber Intelligence NDR offering to strengthen threat hunting and incident response. Enhanced analytics in NDR platforms increases the utility of captured network telemetry for forensic reconstruction, reducing reliance on separate point tools during investigations.

Network Forensics Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the network forensics market covers software and related services used to capture, store, and analyze network traffic so incidents can be reconstructed and investigated in enterprise and public sector environments.

Scope exclusions: We exclude general security monitoring tools that do not support packet or flow level reconstruction, along with pure consulting that is not tied to a network forensics platform.

Segments Covered in This Report

-

By Component

- Solutions

- Services

-

By Deployment Mode

- On-premise

- Cloud-based

-

By Organization Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

-

By Application

- Endpoint Security

- Data-Center Security

- Network Security

- Application Security

-

By End-user Industry

- IT and Telecom

- BFSI

- Retail and E-commerce

- Government and Defense

- Healthcare and Life Sciences

- Manufacturing

- Others (Energy, Education)

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

South America

- Brazil

- Rest of South America

-

Europe

- United Kingdom

- Germany

- France

- Rest of Europe

-

APAC

- China

- India

- Japan

- Australia

- Rest of APAC

-

Middle East and Africa

-

Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

-

Africa

- South Africa

- Rest of Africa

-

Middle East

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the factual base for the model before any assumptions were applied. We leaned on public cybersecurity and network indicators, along with official references such as NIST guidance, CISA advisories, FCC materials, and datasets from the US Bureau of Labor Statistics for wage and workforce signals that influence services delivery and pricing.

To shape the demand side and validate regional patterns, we also reviewed sources such as ITU connectivity statistics, ENISA threat landscape publications, and peer reviewed security and networking journals that discuss traffic visibility, incident response practices, and packet capture limits. On the supply side, we referenced company annual reports, earnings notes, product documentation, reputable press coverage, and patent databases for tracking product direction and feature maturity. The sources mentioned above are illustrative, and many other public references were also used for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what buyers actually deploy for investigation and what they pay for it, since public pricing rarely shows the full picture. We covered security leaders, network operations teams, incident response practitioners, and channel partners across APAC, EMEA, and the Americas so adoption assumptions, cloud migration timing, and services attachment rates could be checked against real buying cycles.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 12% | APAC: 51% |

| Mid tier: 50% | Functional/Unit leaders: 31% | EMEA: 29% |

| Smaller Players: 19% | Managers: 57% | Americas: 20% |

Market-Sizing & Forecasting

Sizing was built using a top-down demand pool approach where enterprise security spending, network traffic visibility needs, and regulatory pressure are translated into an addressable adoption base for network forensics tools and related services. Results were then checked through selective bottom-up approximations, such as sampling typical platform pricing bands, using channel feedback on deal sizes, and applying services-to-software attachment ratios to confirm totals stay realistic.

Key inputs that shaped the model included the mix of on-premise versus cloud deployments, average retention periods for captured traffic, incident investigation frequency, encrypted traffic inspection trends, and staffing intensity for network security operations. These variables influence how much capture capacity is purchased, how much storage is required, and whether buyers lean toward licenses, subscriptions, or add-on services.

For forecasting, we used scenario analysis supported by expert views on cloud migration speed, threat intensity, and budget prioritization, then converted scenarios into a single base case using the most common buyer behavior heard in interviews. Where bottom-up checks had gaps (for example, limited disclosure of services revenue splits), assumptions were tightened using multiple respondent inputs and re-tested against adoption patterns by region and organization size.

Data Validation & Update Cycle

Outputs were validated through multiple checks so the final numbers stay consistent with real market signals. We compared implied spend per customer, deployment mix, and services intensity against independent indicators, and any outliers were traced back to a specific assumption before being accepted or corrected.

A second analyst review is completed before sign-off, and sensitive assumptions are re-checked through follow-up outreach when the variance looks high. Reports are refreshed every year, and interim updates are added when major events shift budgets or deployment patterns. Before delivery, an analyst performs a fresh pass so clients receive the latest updated view.

Mordor Intelligence's Network Forensics Market Size Compared With Other Published Estimates

Published market sizes for network forensics often do not match because each publisher defines what counts as forensics revenue a bit differently, and they also select different base years and currency timing. Gaps also show up when one estimate assumes faster cloud replacement of on-premise deployments, or uses a higher services share without validating it with buyers.

Some external totals appear to include adjacent security spend such as general monitoring platforms that do not enable packet-level reconstruction. For Mordor Intelligence, revenue is counted only when the solution or service supports capture and analysis that can reconstruct network activity for investigations, which keeps the total tied to forensic use cases instead of wider security tooling.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.96 B (2026) | |

| Global Consultancy A | USD 2.20 B (2023) | Uses an earlier base year and appears to include a wider set of security analytics tools under network forensics, which can pull in spending that is closer to broader network security monitoring. |

| Trade Publisher B | USD 1.90 B (2024) | Applies a narrower capture of paid deployments and a more conservative adoption curve, and the lower figure may reflect a smaller assumed services share plus different currency conversion timing. |

Taken together, the spread is mainly explained by scope choices and by how quickly cloud deployments and services revenue are assumed to ramp. Our method keeps assumptions visible and repeatable, since totals are anchored to clear adoption drivers, deployment mix, and pricing checks that can be re-tested as the market shifts.

Key Questions Answered in the Report

What is driving the rapid growth of the network forensics market?

Growth is propelled by stricter breach-reporting laws, the surge in encrypted east-west cloud traffic, and cyber-insurance clauses that now require packet-level evidence.

Which component segment will expand the fastest through 2031?

Services are projected to grow at an 17.75% CAGR as organizations need specialized expertise to deploy, tune and operate forensic platforms amid a global talent shortage.

How does 5G adoption influence network forensics investments?

5G standalone architectures multiply east-west sessions among virtualized functions, so operators require high-speed probes and analytics that can decode new protocols at scale.

Why are SMEs increasingly adopting network forensics solutions?

Cloud-delivered capture tools with pay-as-you-go pricing, coupled with insurer requirements, allow SMEs to secure evidence without large capital expenditure.

Which region offers the highest growth potential after 2026?

Asia-Pacific leads with a forecast 17.65% CAGR, supported by accelerated digitalization in China, India and South Korea and rising investment in managed security services.

How does converging NDR and forensics benefit security teams?

Unified platforms eliminate tool switching, reduce mean-time-to-respond and maintain a single evidence repository, enhancing analyst productivity and lowering operating cost.

Page last updated on: