Incident Response Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

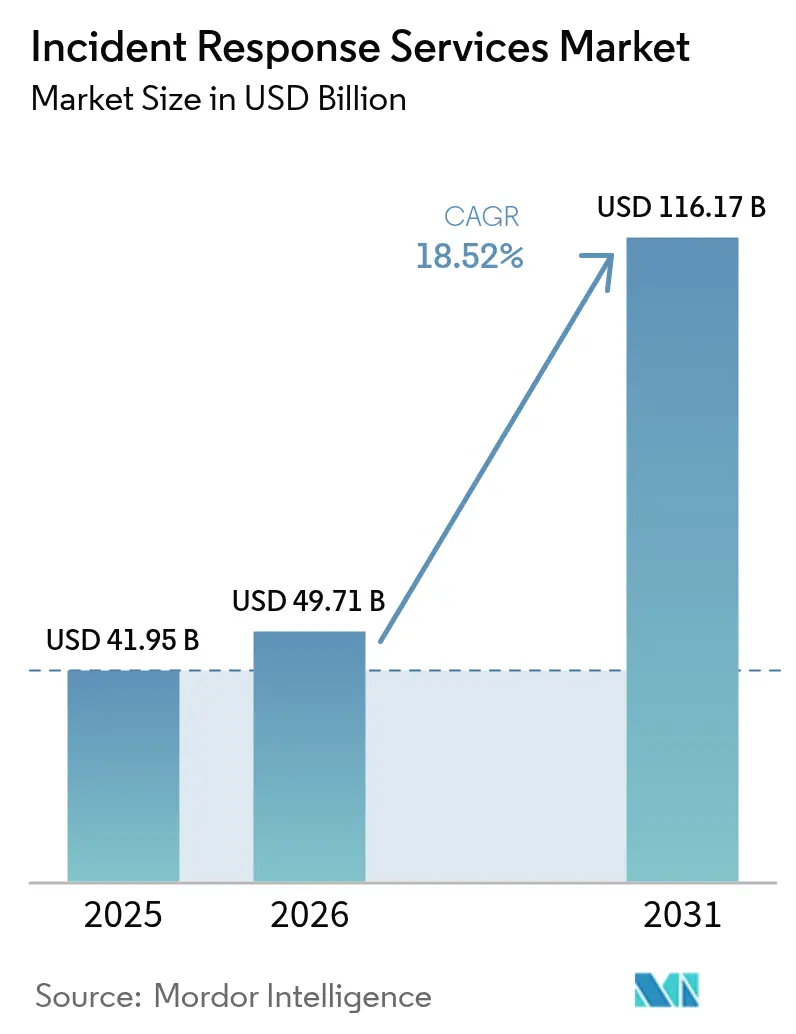

| Market Size (2026) | USD 49.71 Billion |

| Market Size (2031) | USD 116.17 Billion |

| Growth Rate (2026 - 2031) | 18.52% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Incident Response Services Market Analysis by Mordor Intelligence

incident response services market size in 2026 is estimated at USD 49.71 billion, growing from 2025 value of USD 41.95 billion with 2031 projections showing USD 116.17 billion, growing at 18.52% CAGR over 2026-2031. Rising attack sophistication, stricter data-protection mandates, and cloud-first architectures are redefining service expectations in ways that favor automation, artificial intelligence, and cross-border response expertise. Vendor consolidation is underway as platform providers acquire managed detection and response (MDR) specialists to integrate threat hunting and containment under one operating model. Cloud workload migration continues to expand the incident response services market, yet on-premises tooling still dominates highly regulated environments that must meet local data-sovereignty rules. Meanwhile, cyber-insurance underwriters are tightening policy language and rewarding buyers that can show signed response retainers, incentivizing organizations of every size to reassess coverage gaps.

Key Report Takeaways

- By service type, Containment and Mitigation led with 32.75% incident response services market share in 2025, while Managed Detection and Response is projected to grow at a 20.6% CAGR through 2031.

- By deployment mode, On-Premises solutions held 56.45% of the incident response services market size in 2025; cloud-based services are advancing at a 19.85% CAGR to 2031.

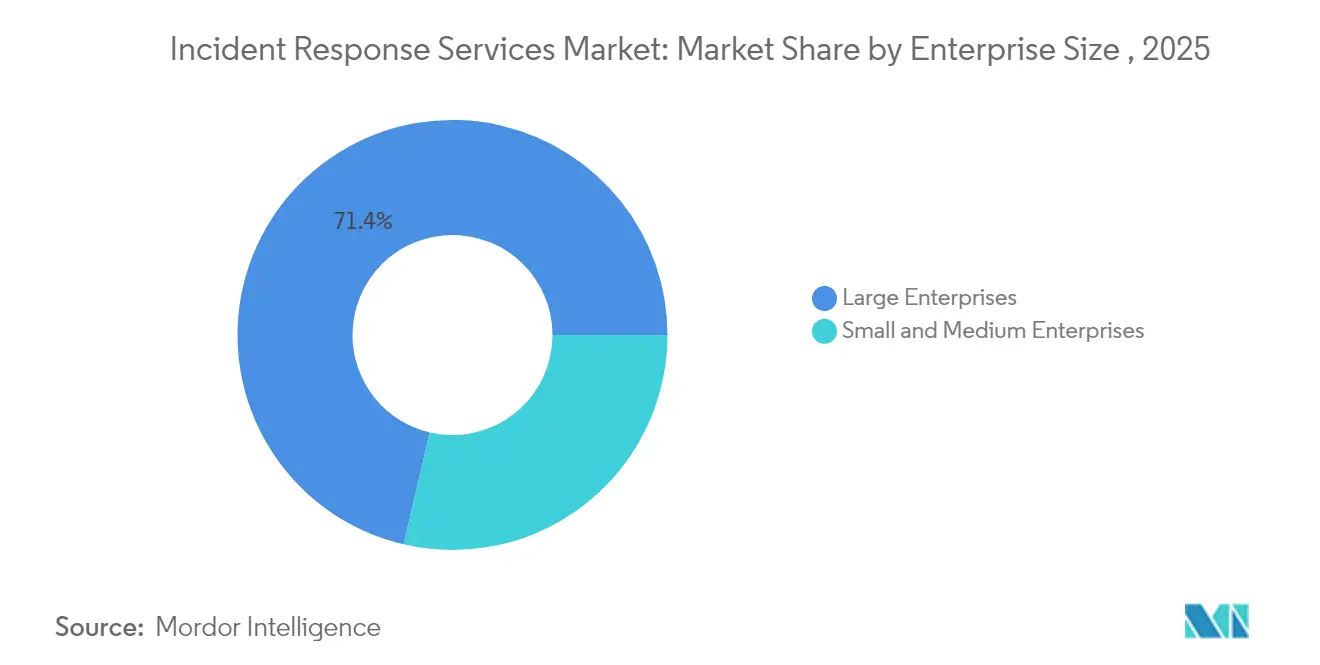

- By enterprise size, Large Enterprises controlled 71.35% revenue share in 2025; Small and Medium Enterprises are expanding at a 18.74% CAGR as cyber-insurance clauses push pre-approved retainers.

- By end-user industry, Banking, Financial Services, and Insurance accounted for 23.15% of the incident response services market size in 2025, while Healthcare and Life Sciences is rising at a 19.24% CAGR.

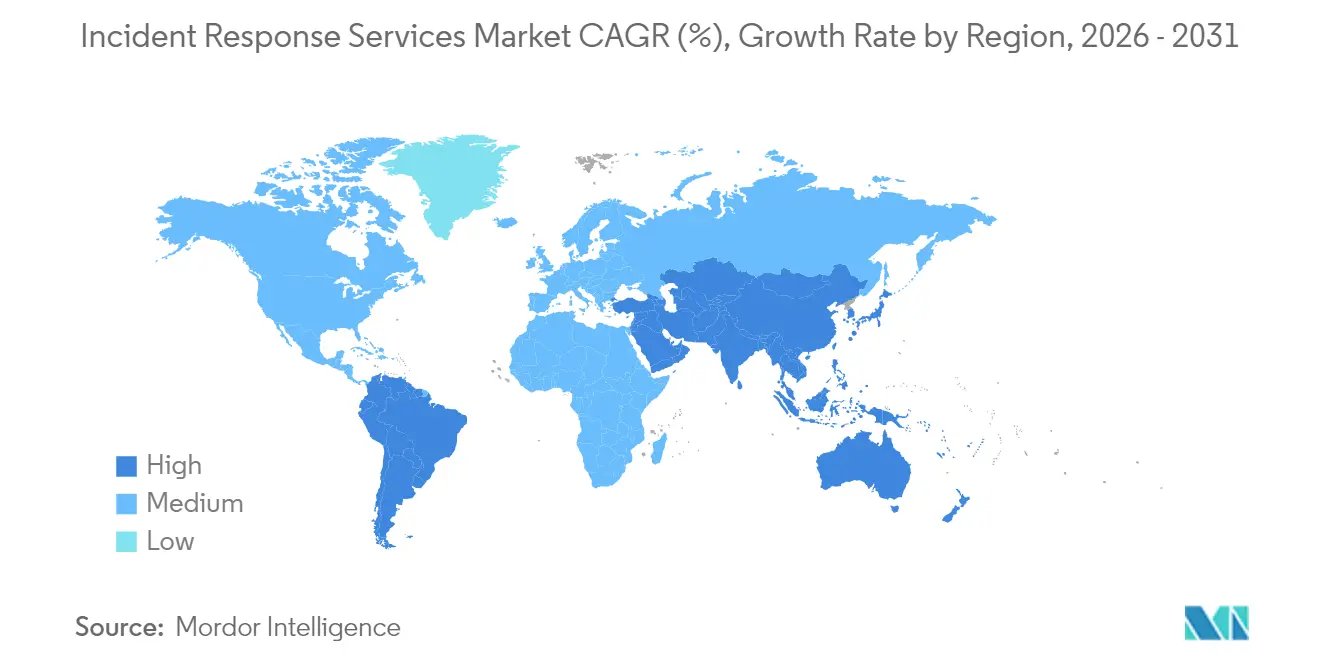

- By geography, North America led with 37.85% incident response services market share in 2025; Asia-Pacific is the fastest-growing region at a 20.12% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Incident Response Services Market Trends and Insights

Surge in Frequency and Sophistication of Cyber-Attacks in BFSI and Critical Infrastructure

Financial institutions and utility operators now contend with attack dwell times measured in minutes rather than days, forcing a pivot to containment-first playbooks that emphasize rapid isolation of endpoints and network segments. The Unit 42 Global Incident Response Report recorded that 86% of 2024 breaches disrupted business operations, while adversaries exfiltrated data inside the first hour of compromise. Legacy system convergence with open banking APIs compounds risk in BFSI, whereas operational technology (OT) environments in energy and transport require response teams to preserve uptime even while eradicating malware. Government guidance, such as the Texas Department of Banking’s 2025 notice that basic cyber hygiene blocks 98% of threats, reinforces the view that specialized responders are essential for the remaining high-grade incidents. [1]Texas Department of Banking, “Industry Notice 2025-01,” dob.texas.gov

Stricter Data-Protection Regulations Driving Compliance-Mandated Investments

The European Union’s NIS2 directive obliges essential entities to report significant incidents within 24 hours and faces violators with fines up to EUR 10 million (USD 11.3 million). [2]European Commission, “Directive (EU) 2022/2555 on Measures for a High Common Level of Cybersecurity,” secureframe.com Similar momentum exists in North America, where PCI-DSS 4.0 and evolving state privacy laws demand verifiable incident response programs that extend beyond technical logs to downstream reporting and stakeholder communication. Compliance overlap across regions has spurred multinational firms to seek global response partners that can align evidence collection, legal holds, and public disclosure standards in one coordinated workflow.

Cloud-First Adoption Expanding Attack Surface

Organizations shifting to multi-cloud infrastructures discover that perimeter-centric response plans break down when serverless functions, APIs, and container workloads disappear within seconds. The Cloud Security Alliance warns that ineffective playbooks delay cloud breach detection and amplify downstream losses. Shared responsibility models further complicate forensic chain-of-custody, motivating providers to embed automated snapshots and tamper-proof logging. Early adopters report that cloud-native MDR contracts shorten detection windows, though some financial services clients still require on-premises analysis for regulated data sets.

Rise of Ransom-Cloud and BEC 3.0 Exploiting OAuth Tokens

Threat actors now leverage legitimate OAuth applications to tunnel operations that appear whitelisted to security monitors. Microsoft observed Storm-1283 using cloud virtual machines for lateral movement, with incident losses ranging from USD 10,000 to USD 1.5 million securityaffairs. Attack schemes classed as BEC 3.0 combine token theft and social engineering to redirect wire transfers and payroll files, raising the stakes for rapid token revocation and account restoration. The FBI attributes USD 17.3 billion in global business email compromise losses between 2013 and 2022, with a sharp rise in 2023 linked to cloud collaboration platforms guycarpenter.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global shortage of skilled incident responders | -2.8% | Global, acute in North America and Europe | Long term (≥ 4 years) |

| High cost of premium IR retainers limiting SME uptake | -1.9% | Global, especially emerging markets | Medium term (2-4 years) |

| Overlap with XDR/SOAR platforms causing buyer confusion | -1.4% | North America and Europe | Short term (≤ 2 years) |

| Zero-trust architectures shortening dwell time, reducing full-scale IR engagements | -1.1% | Global, led by mature markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Global Shortage of Skilled Incident Responders Constraining Growth

The worldwide cybersecurity workforce gap climbed significantly in 2025, with incident responders among the scarcest skill sets. Staffing deficits raise time-to-contain metrics and inflate breach liabilities; IBM estimates an average USD 1.76 million premium for firms lacking dedicated incident response resources. Outsourcing partners benefit, yet capacity bottlenecks persist during multi-client surge events, spurring investments in AI-driven triage to extend human expertise

High Cost of Premium IR Retainers Limiting SME Adoption

Monthly retainers can range between USD 500 and USD 5,000, a barrier for small enterprises that nonetheless account for nearly half of reported cyber breaches strongdm. Median impact costs of USD 3 million including operational downtime and reputational damage outstrip many SME balance sheets, creating a protection gap where reactive, pay-as-you-go clean-ups remain the only option. Managed security providers are responding with tiered offerings and community-based response models to broaden access without undermining profitability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Containment Now, MDR Next

Containment and Mitigation captured 32.75% of the incident response services market in 2025, reflecting the urgency to isolate compromised assets before attackers pivot or exfiltrate data. Rapid isolation of endpoints and privileged credentials has become standard practice as median attacker dwell time shrinks. Over the forecast horizon, Managed Detection and Response will expand at a 20.6% CAGR, elevating continuous threat-hunting and proactive remediation from optional add-ons to core contract deliverables.

MDR momentum is powered by AI-assisted analytics that surface anomalies human analysts might miss. Vendors infuse large-language-model copilots that accelerate root-cause discovery and automated playbook execution, slashing response hours. Remediation and Recovery maintain relevance, particularly when regulatory reporting or litigation requires certified evidence handling. Digital Forensics and Analytics is evolving through machine-learning-based pattern recognition, enabling incident responders to reconstruct attacker timelines faster while satisfying evidentiary standards for court proceedings.

By Deployment Mode: Balancing Control and Flexibility

On-Premises installations still held 56.45% share of the incident response services market size in 2025 due to sovereignty mandates and board-level preferences for local custody of sensitive logs. Financial institutions and public agencies continue to limit external data transfers, especially in jurisdictions that prohibit customer information from leaving national borders. Yet cloud-based response tooling will outpace overall growth at a 19.85% CAGR as security teams embrace plug-and-play scalability.

Hybrid deployment models now fuse local log retention with cloud analytics engines, giving organizations the forensic visibility they require without sacrificing elastic compute capacity. Zero-trust philosophies reinforce the shift by de-emphasizing network location as a security boundary and normalizing remote examination of forensic artifacts. Providers differentiate by offering “bring-your-own-key” encryption and in-region data storage to satisfy compliance audits.

By Enterprise Size: Large Budgets, Small-Business Volume

Large Enterprises commanded 71.35% revenue in 2025, having the budget to fund end-to-end response teams that integrate threat intelligence, playbook automation, and crisis communications. Meanwhile, SMEs represent the fastest-growing opportunity at a 18.74% CAGR. The value proposition for smaller firms hinges on pooled SOC resources and cyber-insurance incentives that now require pre-negotiated retainer agreements.

SMEs turn to subscription-based platforms that bundle MDR, incident response, and regulatory reporting in one license. Large enterprises remain innovation drivers, validating advanced use cases such as OT forensics and AI-guided threat prioritization. The incident response services market continues to mature toward outcome-based pricing, where service-level agreements tie fees to containment time or compliance benchmarks.

By End-User Industry: BFSI Leads, Healthcare Surges

Banking, Financial Services, and Insurance retained 23.15% of the incident response services market size in 2025 owing to strict supervisory requirements and the sector’s outsized exposure to financial crime. However, Healthcare and Life Sciences will advance at 19.24% CAGR as patient-safety imperatives and soaring ransomware frequency heighten urgency. Hospital downtime directly threatens clinical care, pushing boards to prioritize guaranteed response SLAs.

Government and Defense agencies accelerate adoption to counter nation-state espionage, while Industrial Manufacturing, Energy, and Utilities seek OT-specific response capabilities that preserve safety and uptime across critical infrastructure. Retail and E-commerce players emphasize customer trust and continuity during peak shopping periods, integrating incident response playbooks with payment system redundancies.

Geography Analysis

North America retained the regional lead with 37.85% incident response services market share in 2025, propelled by mature breach-notification laws and robust security ecosystems. United States financial regulators, such as the New York Department of Financial Services, require formalized incident response plans, reinforcing demand across large banks and fintechs. Canada’s critical-infrastructure directives and Mexico’s expanding fintech rules extend regional volume.

Asia-Pacific is on track for a 20.12% CAGR to 2031. Regulatory harmonization in Japan, Singapore, and Australia now mandates 24-hour breach disclosure and certified response processes, encouraging organizations to secure retainers before incidents occur. The region recorded 34% of global attacks in 2024, intensifying demand for bilingual, cross-jurisdictional responders who can navigate local rules and diverse cloud stacks.

Europe’s compliance-driven adoption accelerates under NIS2, which broadens the scope of “essential entities” and elevates fines for insufficient preparedness. Organizations must harmonize GDPR data-breach reporting with NIS2 security-incident disclosure, fueling bundled privacy-plus-security response engagements. Eastern European members look to consultancies for playbook localization, while larger economies deepen contracts to cover supply-chain and OT threats.

Latin America, the Middle East, and Africa remain nascent but rising. Digital-commerce expansion and new data-protection statutes open opportunities, though budgetary and talent constraints temper immediate growth. International providers partner with local MSSPs to bridge language, culture, and compliance gaps, a model expected to scale as regional investment in cyber resilience continues.

Mordor Intelligence provides coverage of the incident response services market across other key regional markets, including Latin America, each with their regulatory frameworks and demand patterns.

Regulatory Landscape

Mandatory cyber-incident reporting timelines are tightening across major jurisdictions, increasing demand for incident response services that can produce regulator-ready evidence and disclosures on compressed deadlines. In the European Union, NIS2 requires reporting significant incidents within 24 hours, with fines up to EUR 10 million for non-compliance. DORA is also reinforced by Commission Delegated Regulation (EU) 2025/301 (dated 23 October 2024), which specifies technical standards for the content and time limits of major ICT-incident reporting by financial entities.

Outside Europe, the United States reporting regime under 6 U.S.C. Section 681b requires covered entities to report covered cyber incidents to CISA within 72 hours and ransomware payments within 24 hours, which increases the need for coordinated DFIR and communications workflows. In March 2026, the Nigerian Communications Commission released the Cyber Resilience Framework for the Nigerian Communication Sector (CRF-NCS), requiring Tier 1 telecom operators to report significant threats and incidents within four hours of detection. Alongside EU-wide response coordination under the Cyber Solidarity Act (Regulation (EU) 2025/38), these requirements are pushing buyers toward retained services, automated triage, and cross-border playbooks that align technical containment with legal reporting obligations.

Competitive Landscape

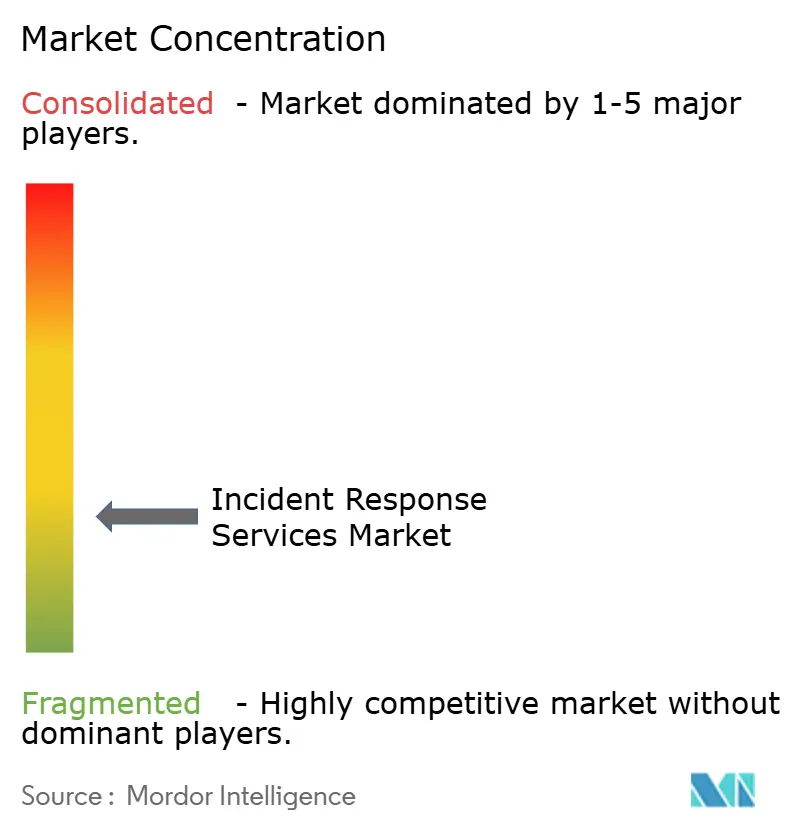

The incident response services market is moderately fragmented. Established vendors such as IBM, CrowdStrike, and Rapid7 integrate AI-driven correlators with broad service portfolios, while niche consultancies focus on vertical specialties like OT or legal-grade forensics. Strategic acquisitions highlight convergence: Zscaler acquired Red Canary in May 2025 to embed MDR into its zero-trust stack, adding USD 140 million in recurring revenue and bolstering 24/7 monitoring.

Platform consolidation favors buyers seeking unified dashboards, streamlined invoicing, and preconfigured workflow integrations. Technology differentiation is shifting to large-language-model copilots that automate evidence triage and draft regulator-ready reports. Disruptors compete on cost-effective retainers for SMEs, offering chat-based incident portals and automated response orchestration.

White-space opportunities lie in supply-chain investigation and OT-centric services. Providers that can validate vendor-risk exposures or run forensics in air-gapped networks will gain share, especially as industrial firms adopt digital twins that require specialized analytic tooling. Alliances between cloud hyperscalers and response boutiques are also emerging, delivering regionally hosted evidence lockers that meet sovereignty conditions while leveraging hyperscale compute for rapid analysis.

Incident Response Services Industry Leaders

CrowdStrike Holdings Inc.

NCC Group plc

Rapid7 Inc.

IBM Corporation

Check Point Software Technologies Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Compressed reporting windows and standards-driven risk management create whitespace for providers that can operationalize end-to-end response, from containment through disclosure, across hybrid and multi-cloud environments. Under DORA-linked rules, including Commission Delegated Regulation (EU) 2025/301, and broader EU cybersecurity requirements, including Regulation (EU) 2024/2690 referencing standards such as ISO/IEC 27001 and ISO/IEC 27002, multinational firms increasingly need incident response partners that can harmonize evidence handling, chain-of-custody, and regulator-ready reporting across jurisdictions. This supports demand for engagements that bundle digital forensics, breach assessment, and crisis communications into a single operating model.

Commercial packaging and technology are also shifting toward outcomes and scalability, creating opportunities for flexible retainers, AI-assisted triage, and integrated MDR-to-IR workflows. In November 2025, LevelBlue completed its acquisition of Cybereason to combine XDR with DFIR and incident response capabilities, reflecting buyer interest in fewer, more integrated operating models. In March 2026, LevelBlue launched a funds-based Resilience Retainer to provide prioritized access to a large incident response bench while allowing budget to be used for preparedness activities, and Allens introduced RADAR to speed compromised-data assessment using AI. These actions point to continued focus on rapid data scoping, cloud identity incident handling, and standardized reporting artifacts that match regulator timelines and cyber-insurance retainer requirements.

Recent Industry Developments

- March 2026: CrowdStrike and IBM expanded their strategic collaboration to integrate CrowdStrike Charlotte AI with IBM Autonomous Threat Operations Machine (ATOM) for agentic SOC transformation and coordinated incident response. The combined approach targets faster triage and containment by connecting AI-driven analytics with automated response operations, aligning incident response services with machine-speed workflows demanded by large enterprises.

- December 2025: CrowdStrike entered into a multi-year partnership with Kroll to elevate managed detection and response (MDR) services, including migrating more than 500,000 endpoints to the CrowdStrike Falcon platform. The deal strengthens an MDR-to-incident-response pipeline by combining a large endpoint footprint with established incident response and advisory capabilities.

- January 2024: Commission Delegated Regulation (EU) 2025/301 (dated 23 October 2024) formalized technical standards for the content and time limits of major ICT-related incident reporting under the EU Digital Operational Resilience Act (DORA). More prescriptive reporting requirements increase the value of incident response providers that can deliver audit-ready documentation, timelines, and stakeholder communications alongside technical remediation.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers paid services that help an organization prepare for, respond to, investigate, and recover from cybersecurity incidents, including retainer based readiness support and post-incident advisory delivered by external providers.

Scope exclusions: The sizing does not count software license revenue, in-house security operations labor cost, or broader physical emergency management services.

Segmentation Overview

- By Service Type

- Containment and Mitigation

- Remediation and Recovery

- Digital Forensics and Analytics

- Managed Detection and Response (MDR)

- Others

- By Deployment Mode

- On-Premises

- Cloud-based

- Hybrid

- By Enterprise Size

- Small and Medium Enterprises

- Large Enterprises

- By End-User Industry

- BFSI

- Government and Defense

- IT and Telecom

- Healthcare and Life Sciences

- Industrial Manufacturing

- Energy and Utilities

- Retail and E-commerce

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with building a fact base on cyber incident volumes and risk drivers, then converting those signals into a service demand view. We relied on public sources such as CISA advisories, NIST publications, FBI IC3 reports, and OECD digital security documents to understand incident types, reporting behavior, and response practices that are commonly followed.

To anchor the commercial side, we reviewed provider websites and service catalogs, annual reports and investor presentations, and trusted press coverage on breach events and regulatory actions. In some cases, paid subscriptions for company financials and news intelligence helped confirm revenue splits and the timing of major service expansions, and patent databases were used to check how automation features were being positioned in response workflows. These examples are illustrative only, and many other public references were consulted to collect, cross-check, and clarify data points.

Primary Interviews and Surveys

Primary inputs were taken from interviews and surveys with incident response service providers, channel partners, and enterprise security leaders who buy or manage these engagements. Respondent input was used to confirm service scope definitions, typical response timelines, retainer utilization patterns, and how pricing changes with severity, industry sensitivity, and cloud workload share across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 18% | APAC: 46% |

| Mid tier: 43% | Functional/Unit leaders: 23% | EMEA: 29% |

| Smaller Players: 20% | Managers: 59% | Americas: 25% |

Market-Sizing & Forecasting

Sizing began with a top-down reconstruction of addressable demand using security incident frequency signals, outsourcing propensity, and average engagement value by incident class, which were then mapped to regional enterprise IT and cyber risk indicators. Only after the demand pool was formed were service categories allocated based on how retainers, emergency response, forensics, and post-incident advisory typically split in real projects.

To keep results realistic, selective bottom-up approximations were used as a check, such as rolling up sampled provider revenues, validating utilization assumptions for incident handlers, and cross-checking implied deal volumes against common response lead times. Key model inputs included breach notification intensity, regulated-industry share, cloud workload penetration, average response hours by severity, and pricing shifts tied to ransomware and data exfiltration patterns.

Forecasts were built using scenario analysis supported by trend lines for incident frequency and compliance pressure, then adjusted through expert views on staffing constraints and automation adoption. When bottom-up information was incomplete for smaller regions or newer service types, gaps were handled by using proxy ratios from comparable markets and then re-tested in interviews before finalizing totals.

Data Validation & Update Cycle

Outputs were checked against independent signals like security spending growth, reported breach volumes, and regional enforcement activity, and then variances were reviewed in a separate analyst pass. If a region showed an unusual jump, assumptions on engagement frequency, average pricing, and retainer conversion were revisited and, when needed, respondents were re-contacted for clarification.

Each report is refreshed annually, and interim updates are triggered when major regulatory changes, large-scale attack waves, or material pricing shifts are observed. Before delivery, a final sweep is completed so clients receive the latest updated view.

Mordor Intelligence's Incident Response Services Market Sizing Compared With Other Published Estimates

Published estimates for incident response often do not match because the scope line is drawn differently, and because pricing and deal volume assumptions get updated at different times. Differences also come from whether a study counts only outsourced services or also includes adjacent software and internal staffing costs.

Some sources bundle incident response with broader security solutions and platform revenue, or they use aggressive expansion assumptions for cloud security categories and long forecast windows. The spread also shows up when pricing is modeled as a flat uplift instead of being tied to incident severity mix and retainer utilization, and when currency conversion uses different reference periods and refresh cadences. Some estimates fold incident response into combined solution plus service totals, and then apply generalized security spending ratios. For Mordor Intelligence, only externally delivered incident response service revenue is counted, and software licenses and internal SOC labor costs are excluded.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 49.71 B (2026) | |

| Global Consultancy A | USD 29.46 B (2024) | Uses an earlier base year and a broader incident response market framing that blends service activity with solution-led spending patterns, which can depress the services-only total when mapped to 2024 pricing. |

| Industry Publisher B | USD 41.50 B (2025) | Includes solution and service components together and applies a longer forecast frame with different category splits (such as threat hunting and planning packaged under mixed security types), which changes what is counted as services revenue in the base year. |

Looking across the three figures, the main driver of the gap is not one single assumption but a combination of base year choice, whether software and services are mixed, and how engagement pricing is linked to incident mix. By keeping inclusions tied to paid response engagements and by cross-checking volumes and pricing with practitioners, the final value stays traceable to clear demand drivers and repeatable steps.

Key Questions Answered in the Report

What is the current size of the incident response services market?

The incident response services market is valued at USD 49.71 billion in 2026 and is forecast to reach USD 116.17 billion by 2031.

How fast is the market expected to grow?

The market is projected to expand at an 18.52% compound annual growth rate (CAGR) between 2026 and 2031.

Which service category will grow the fastest through 2031?

Managed Detection and Response (MDR) is projected to log the highest growth at a 20.6% CAGR over the forecast period.

Which region is expected to record the strongest growth?

Asia-Pacific leads growth momentum with a 20.12% CAGR through 2031, driven by new cybersecurity regulations in Japan, Singapore, and Australia.

What industry vertical currently dominates spending on incident response services?

Banking, Financial Services, and Insurance holds the largest share at 23.15% of global revenue in 2025, reflecting stringent regulatory requirements.

Why are small and medium enterprises (SMEs) accelerating adoption?

Cyber-insurance policies now require signed response retainers, prompting SMEs to adopt managed services and fueling a 18.74% CAGR in this segment.

Page last updated on: