Diesel Power Engine Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 12.87 Billion |

| Market Size (2031) | USD 16.69 Billion |

| Growth Rate (2026 - 2031) | 5.33% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

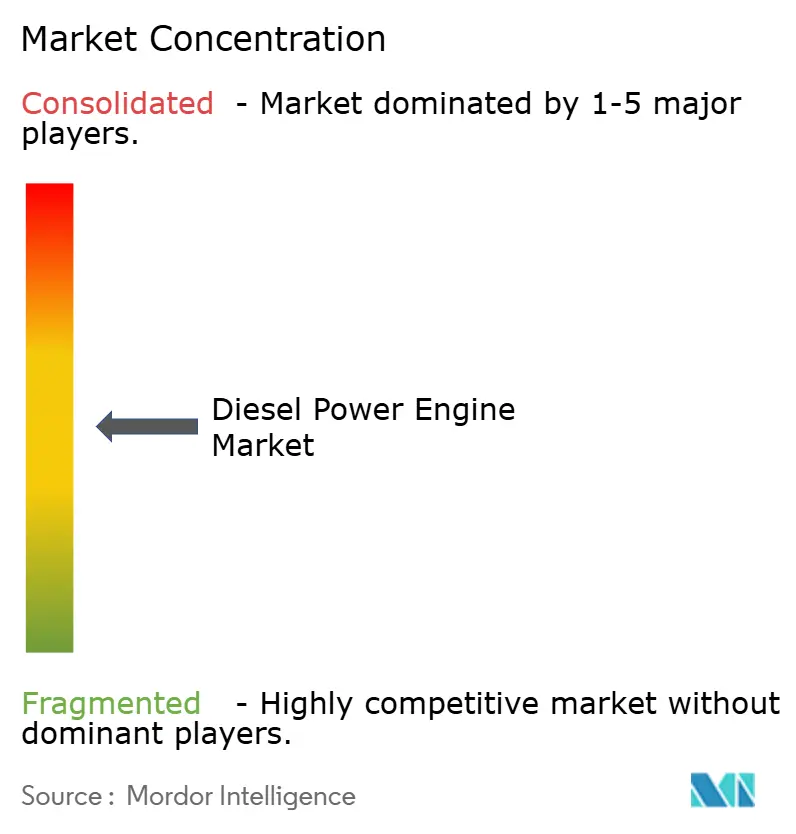

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Diesel Power Engine Market Analysis by Mordor Intelligence

The Diesel Power Engine Market size is estimated at USD 12.87 billion in 2026, and is expected to reach USD 16.69 billion by 2031, at a CAGR of 5.33% during the forecast period (2026-2031).

Declining battery-storage costs, wider scrutiny of grid resilience, and the need for multi-day autonomy continue to shape procurement decisions, even as regulatory pressures intensify across OECD regions. Data-center expansions in Asia-Pacific, military modernization in NATO and Indo-Pacific countries, and grid-hardening initiatives in Sub-Saharan Africa provide steady volume for mid- and high-capacity gensets. Simultaneously, OEMs are front-loading investment into after-treatment systems and hybrid controllers to comply with EPA Tier 4 Final and EU Stage V norms and to preserve margins in a price-sensitive environment. Larger engines are also benefiting from modular designs that allow facilities to scale standby power in smaller increments, reducing single-point failure risk and easing maintenance scheduling.

Key Report Takeaways

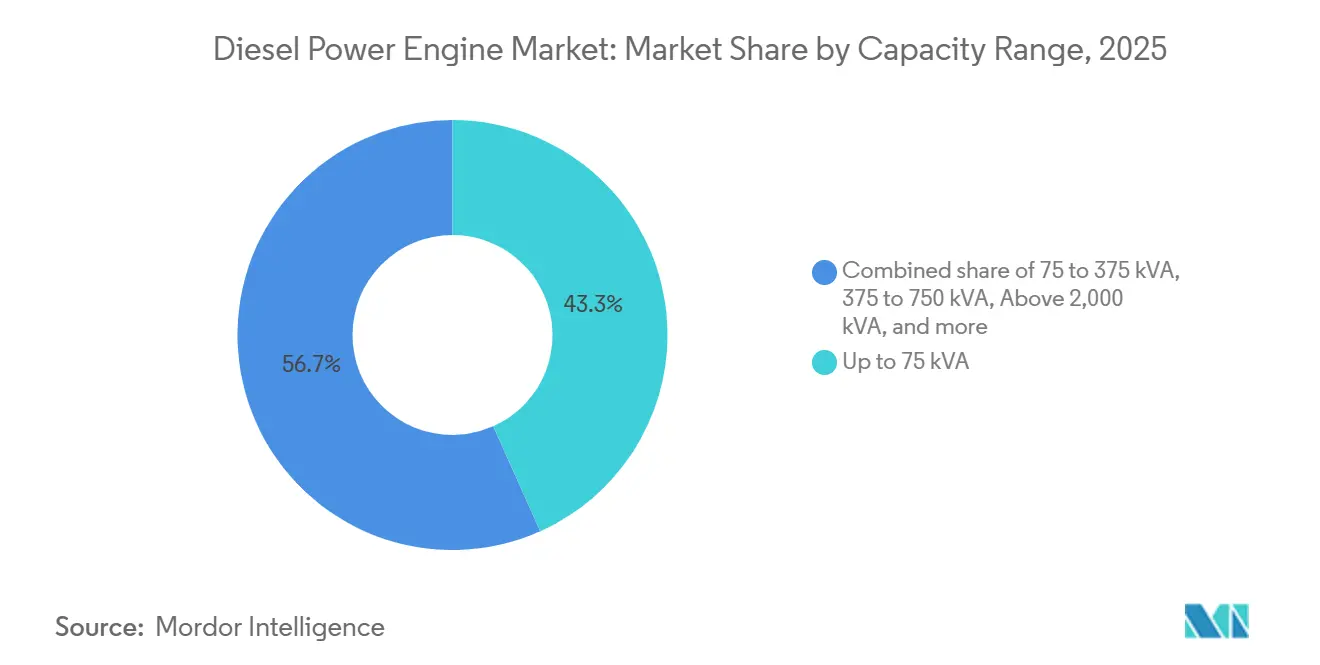

- By capacity, units up to 75 kVA held 43.3% of the diesel power engine market share in 2025, while the 375-750 kVA band is expanding at a 7.5% CAGR through 2031.

- By application, standby installations commanded 56.3% of the diesel power engine market size in 2025 and are advancing at a 6.3% CAGR through 2031.

- By end user, industrial facilities accounted for 55.7% of 2025 revenue and will grow at a 6.2% CAGR between 2026-2031.

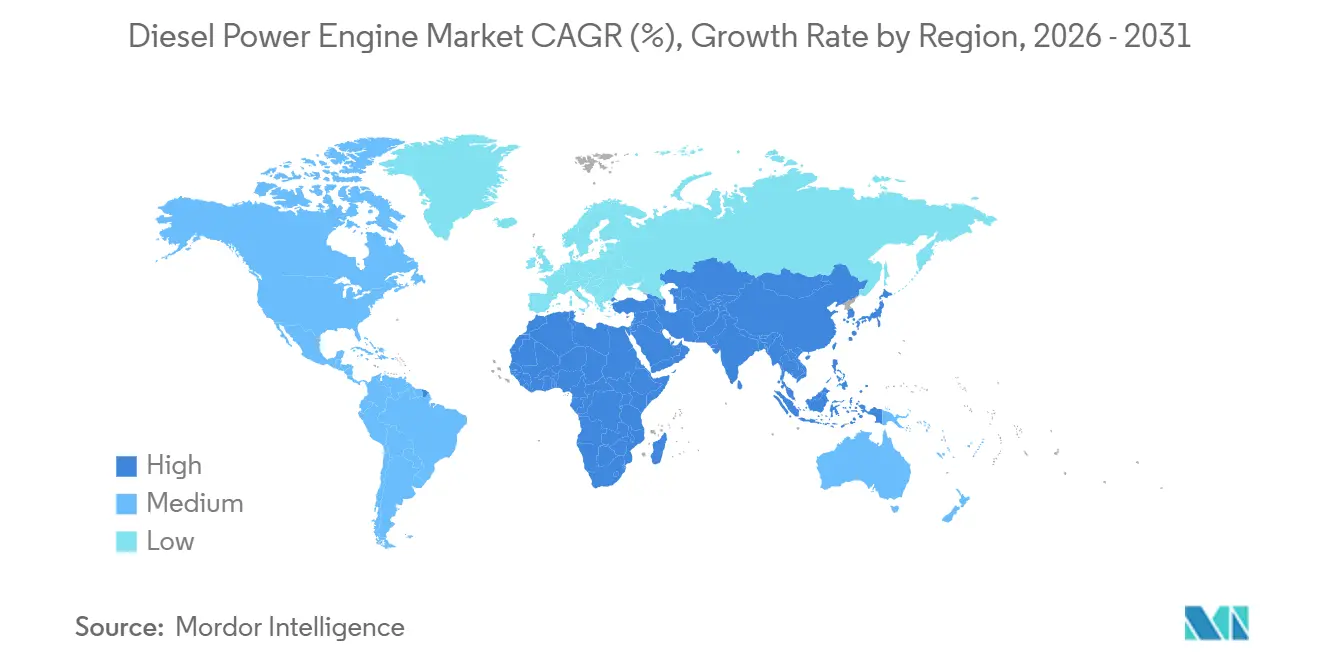

- By geography, Asia-Pacific captured a 38.1% share in 2025 and is projected to post a 6.6% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Diesel Power Engine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-hardening investments in emerging markets | +1.2% | Sub-Saharan Africa, South Asia, Southeast Asia | Medium term (2-4 years) |

| Boom in data-center construction across Asia | +1.5% | China, India, ASEAN; spill-over to Middle East | Short term (≤ 2 years) |

| Industrial automation demand for mission-critical backup | +0.9% | North America, Europe, East Asia | Medium term (2-4 years) |

| Military mobile-power modernization programs | +0.6% | North America, Europe, Indo-Pacific | Long term (≥ 4 years) |

| Micro-utility growth in rural Africa | +0.5% | Sub-Saharan Africa, South Asia | Long term (≥ 4 years) |

| Maritime IMO III retrofit wave | +0.4% | Global maritime routes, Asian shipyards | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid-Hardening Investments in Emerging Markets

Utilities in Sub-Saharan Africa and South Asia are adopting diesel-solar mini-grids as an interim solution while long-distance transmission lines and substations catch up with electrification targets. In 2025, the World Bank allocated USD 2.3 billion for rural projects pairing 50-150 kW engines with photovoltaic arrays, lowering delivered power costs to USD 0.18-0.25 per kWh in 18 African nations.[1]World Bank Group, “Mini-Grid Market Opportunities,” worldbank.org India’s Saubhagya program completed household connections yet still recorded sub-12-hour daily reliability in 40% of rural districts, prompting state utilities to order 15,000 standby gensets last year.[2]Government of India, “Saubhagya Scheme Dashboard,” gov.in These sets often run 6-10 hours per day, driving faster wear and replacement cycles. The African Development Bank confirms similar economics, noting that mini-grids can undercut regulated tariffs without direct subsidies in Kenya, Tanzania, and Nigeria.[3]African Development Bank, “Hybrid Mini-Grid Economics in Africa,” afdb.org

Boom in Data-Center Construction Across Asia

Hyperscale operators installed 1.2 GW of new diesel standby capacity in Asia-Pacific during 2025, with India and China representing 68% of the total build-out. Microsoft and AWS committed USD 6.5 billion to campuses in Hyderabad requiring N+1 diesel redundancy for 72-hour operation, while China’s Ministry of Industry and Information Technology obliges all new Tier-3 sites to store three days of fuel on-site.[4]Ministry of Industry and Information Technology, “Data Center Energy Regulations,” miit.gov.cn NREL’s latest density models suggest battery systems will not match diesel’s energy storage efficiency at the multi-megawatt scale until after 2029.

Industrial Automation Demand for Mission-Critical Backup

Semiconductor fabs, automotive lines, and pharmaceutical clean rooms have tightened voltage-sag tolerances to less than 2%. In Arizona, TSMC installed six Caterpillar 3512C gensets rated 1,825 kVA each, capable of full load within 10 seconds of grid loss. Cummins reports a 31% year-on-year surge in orders for QSK60 and QSK95 engines equipped with digital load-sharing controllers for plants in Mexico and Eastern Europe. Vaccine cold-chain hubs in Singapore and Belgium specified automatic-transfer switches rated for 100,000 cycles, highlighting how downtime avoidance justifies higher capital outlay.

Military Mobile-Power Modernization Programs

NATO identified aging 60 kVA tactical sets as a capability gap and began replacing them with 375-750 kVA modular units interoperable with JP-8, F-76, and commercial ultra-low-sulfur diesel. The U.S. Army awarded Cummins a USD 180 million contract in 2025 for 1,200 AMMPS gensets rated 450 kVA each. Australia’s Department of Defence ordered Caterpillar C18 units for forward bases, emphasizing silent-watch and encrypted controls to thwart cyber intrusion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid fall in battery-storage LCOE | -1.3% | North America & Europe (primary), Asia-Pacific (accelerating), with spillover to Middle East & Africa | Short term (≤ 2 years) |

| Tighter NOx & particulate limits in OECD markets | -0.9% | North America, Europe, Japan, South Korea (OECD core markets) | Medium term (2-4 years) |

| LNG-to-power small-scale deployments | -0.6% | Asia-Pacific, Middle East, Africa, Latin America (emerging markets with gas infrastructure development) | Medium to Long term (3-5 years) |

| OEM supply-chain exposure to Tier-1 chip shortages | -0.4% | Global (affecting all major manufacturing regions and OEMs) | Short to Medium term (1-3 years) |

| Source: Mordor Intelligence | |||

Rapid Fall in Battery-Storage LCOE

Lithium-ion battery pack prices fell to USD 139 per kWh in 2024, a 14% drop from 2023, making four-hour storage viable for commercial buildings previously reliant on diesel. California’s Self-Generation Incentive Program distributed USD 320 million in 2025, allowing hospitals and data centers to substitute battery systems for short-duration outages. Lazard’s 2025 analysis shows a 1 MW/4 h battery delivers backup at USD 0.18 per kWh over 15 years, versus USD 0.22 for a diesel set running 50 hours per year. Yet providing 72-hour autonomy for a 5 MW load still requires a 360 MWh battery system costing about USD 50 million, compared to USD 3 million for diesel hardware and fuel.

Tighter NOx & Particulate Limits in OECD Markets

EPA Tier 4 Final and EU Stage V standards cap nitrogen oxides at 0.4 g/kWh and particulate matter at 0.02 g/kWh, forcing adoption of SCR and diesel particulate filters. Caterpillar’s compliant C9.3B engine adds USD 18,000 in after-treatment components, raising the price of a 500 kVA genset by 12%. The California Air Resources Board plans to prohibit new diesel sets above 500 kW in certain air basins from 2027, potentially affecting 22% of U.S. commercial sales (arb.ca.gov). European regulators are debating real-time emissions monitoring for engines above 1 MW, adding USD 25,000-40,000 per unit.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Capacity Range: Mid-Power Surge Reshapes Demand

The diesel power engine market size for 375-750 kVA units is expanding at 7.5% per year during 2026-2031, outpacing every other band as hospitals, telecom hubs, and factories upgrade to higher reliability specifications. Sets up to 75 kVA retained 43.3% of the diesel power engine market share in 2025 by serving residential and small-commercial loads, yet growth moderates to 4.8% as affluent consumers migrate toward solar-battery solutions. Mid-range 75-375 kVA engines equip retail centers and food-processing sites where automatic transfer within 10 seconds is now a standard bid requirement. At 500-750 kVA, Caterpillar’s C18 and Rolls-Royce’s mtu 12V 2000 capture healthcare and telecom orders by coupling variable-geometry turbochargers with 6% lower fuel burn. Units above 2,000 kVA continue to serve hyperscale campuses, though operators now favor multiple 1,500-2,000 kVA modules for redundancy rather than single 4 MW blocks, tempering procurement cycles but not eliminating demand.

Telecom carriers in India and Indonesia are retiring 250 kVA gensets in favor of 500-600 kVA models to feed 5G radio units that consume 40% more power than 4G. PwC’s 2025 telecom-energy audit found that 600 kVA machines cut carbon intensity 12% on a per-subscriber basis by reducing runtime through improved efficiency. Hospital administrators similarly specify 600-750 kVA arrays to cover expanded ICU and imaging loads, and these orders are bundled with eight-hour load-bank tests to secure insurance certification. Small sets under 75 kVA will still permeate rural Africa and South Asia, aided by micro-financing programs that spread payments over five years.

By Application: Standby Installations Cement Dominance

Standby duty accounted for 56.3% of 2025 revenue and will rise at a 6.3% CAGR, underscoring diesel’s role as insurance rather than baseload generation. Regulatory frameworks tighten fuel-reserve targets: U.S. hospitals must maintain 96 hours of storage and run monthly load tests, prompting 1,800 facilities to replace or augment legacy equipment. Data-center colocation providers limit runtime to fewer than 50 hours a year yet demand 72-hour autonomy, further anchoring diesel in the architecture of digital infrastructure. Prime-duty engines running daily in off-grid mines or island utilities advance at 4.2% as LNG micro-turbines and solar hybrids capture part of the segment. Peak-shaving remains a niche play, hindered by batteries that bid into demand-response programs without emitting pollutants; California enrolled 420 MW of battery capacity for this purpose in 2025.

Across standby operations, the diesel power engine market size for healthcare alone is forecast to hit USD 3.1 billion by 2031, reflecting growth in imaging and critical-care wings. Continuous-duty applications survive where heat recovery boosts total efficiency above 70%; a Brazilian ethanol plant achieved this threshold using Cummins QSK60 units paired with heat-recovery boilers. Peak-shaving still appeals to industrial users in regions with punitive demand charges, provided local air-quality rules allow limited runtime.

By End User: Industrial Sector Anchors Growth

Industrial plants retained 55.7% revenue in 2025 and will maintain a 6.2% CAGR through 2031. Semiconductor fabs deploy multimillion-dollar backup suites. TSMC’s Arizona line invested in six synchronized 1,825 kVA units because a single power event can scrap USD 2-5 million in wafers. Automotive suppliers reshoring to Mexico and Eastern Europe replicate similar architectures, producing a wave of 500-1,500 kVA orders that extend well beyond 2029. Cold-chain logistics facilities safeguard vaccine inventories using diesel gensets with automatic transfer switches designed for 100,000 cycles, a specification now written into most pharmaceutical RFPs.

Commercial buildings occupy 38% of 2025 sales, with developers in California and New York choosing natural-gas engines backed by small diesel sets to satisfy air-quality mandates. Generac’s 350 kVA gas-diesel hybrid targets this slice, promising 15-year total cost parity with a traditional diesel-only approach. Residential demand grows at 4.5% but is bifurcated: solar-battery adoption trims sales in wealthy suburbs while micro-finance expands ownership of 10-25 kVA sets in India, Nigeria, and the Philippines. Kirloskar’s financing plan with HDFC Bank lowered the upfront cost to USD 800-1,200, capturing 62% of India’s sub-15 kVA niche.

Geography Analysis

Asia-Pacific booked 38.1% of 2025 turnover and is set to deliver a 6.6% CAGR, backed by China’s mandate for 72-hour reserves at all new Tier-3 data centers and India’s USD 1.3 trillion infrastructure roadmap. ASEAN’s telecom tower boom under unreliable grids spurred Yanmar to place 2,500 gensets in rural India and Indonesia during 2025. Middle-East-Africa clocks a robust 6.4% CAGR: Saudi Arabia’s NEOM ordered 400 MW of standby power using Wärtsilä 31 engines, and Kenya, Tanzania, and Nigeria scale mini-grid programs with World Bank backing. North America posts a mature 4.1% trajectory, limited by battery incentives and stricter emissions but buoyed by military contracts and semiconductor reshoring. Europe’s 3.8% clip reflects parallel pressures, especially with the pending Industrial Emissions Directive that may require live emissions telemetry on engines over 1 MW.

Across the diesel power engine market, Asia-Pacific’s sustained investment pipeline and looser emissions rules offset headwinds in developed economies. The Middle East leverages petro-financed megaprojects to offset rising gas-turbine adoption, while Sub-Saharan Africa relies on hybrid diesel-solar mini-grids to bridge electrification gaps through 2035.

Regulatory Landscape

Emissions compliance remains the primary regulatory constraint shaping diesel power engine specifications across stationary, non-road, and marine use cases. In the United States, the EPA Tier 4 Final framework continues to govern non-road compression-ignition engines, driving widespread use of SCR and diesel particulate filters. The report scope also captures localized tightening, including the California Air Resources Board plan to prohibit new diesel sets above 500 kW in certain air basins from 2027. These requirements increase system cost and integration complexity (after-treatment packaging, monitoring, and periodic testing), particularly in mid- and high-capacity standby installations.

For marine-linked demand (auxiliary power and harbor or shipyard applications), the International Maritime Organization (IMO) MARPOL Annex VI continues to steer engine certification and NOx controls through Tier requirements under Regulation 13. Effective March 2026, amendments designated the Canadian Arctic and the Norwegian Sea as new Emission Control Areas (ECAs), extending Tier III NOx compliance triggers for marine diesel engines above 130 kW based on ship construction dates. A grace period for SOx and PM compliance extends to February 2027. The geographic expansion of ECAs raises the compliance value of Tier III-capable engine platforms and after-treatment readiness for operators serving these routes.

Competitive Landscape

The top five OEMs, Caterpillar, Cummins, Generac, Kohler, and Wärtsilä, captured a combined 48% of global revenue in 2025, lending the diesel power engine market a moderately concentrated profile. Caterpillar and Cummins dominate mid- to high-capacity sets, plowing R&D into after-treatment and digital diagnostics; Cummins allocated USD 890 million to R&D in 2025, with 18% devoted to remote analytics and alternative fuels. Wärtsilä and Rolls-Royce focus on utility-scale microgrids, showcasing hybrid controllers that shave fuel consumption 30-40% during partial-load events. Generac and Kohler rely on extensive dealer networks to address North American home and light-commercial replacements, while Himoinsa and Kirloskar win on speed-to-market in rental and off-grid telecom niches.

Patent filings for digital load-sharing and hybrid controllers rose 22% year-on-year, underlining a pivot toward total cost-of-ownership differentiation rather than raw horsepower. Mitsubishi Heavy Industries’ S16R-PTA2 earned IMO III certification by integrating urea injection and exhaust-gas recirculation, capturing Asian yard retrofits for auxiliary power. Aggreko’s battery-diesel hybrids trimmed runtime 40% during short outages at Malaysian data centers, signaling emergent competition from rental specialists offering modular green upgrades. Successful OEMs will pair emissions-compliant hardware with financing structures that spread higher acquisition costs over long service contracts, ensuring adoption in both regulated and emerging markets.

Diesel Power Engine Industry Leaders

Caterpillar Inc.

Cummins Inc.

Generac Holdings Inc.

Kohler Co.

Mitsubishi Heavy Industries Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Named capacity expansions and critical-infrastructure procurement are widening the near-term whitespace for OEMs and packagers that can deliver emissions-compliant, high-capacity sets with shorter lead times and tighter controls integration. In May 2026, Wärtsilä announced approximately EUR 90 million to expand technical production capacity at its Sustainable Technology Hub in Vaasa, Finland, by an additional 30%, reinforcing investment momentum behind large-engine manufacturing serving both energy and marine applications. In India, Kirloskar Oil Engines disclosed board approval for approximately INR 1,400 crores for capacity enhancement at its Kagal (Kolhapur) plant, adding 20,000 engines per annum over two years to align with demand pockets in telecom, industrial backup, and distributed power.

At the same time, regulatory tightening in OECD markets creates scope for retrofit-friendly architectures, digital monitoring, and hybridization that can reduce runtime while preserving multi-day autonomy where batteries remain cost-prohibitive at scale. The report context also points to OEM front-loading investment into after-treatment systems and hybrid controllers under EPA Tier 4 Final and EU Stage V, with marine demand tied to IMO Tier III adding another compliance-driven pull for certified platforms. On the demand side, Asia-Pacific data centers installed 1.2 GW of new diesel standby capacity during 2025, and China mandates three days of on-site fuel storage for new Tier-3 sites, supporting continued preference for modular multi-unit standby designs that improve redundancy and maintenance scheduling.

Recent Industry Developments

- June 2026: Cummins Power Generation introduced additions to its high-horsepower Centum Series for 50 Hz markets using the QSK78 engine platform, extending standby ratings up to 3,500 kVA and adding PowerCommand 3400 controls. The announcement supports Cummins positioning in regions where large 50 Hz standby sets underpin hyperscale data centers and industrial backup requirements. It also reflects specification trends toward integrated digital control and load management.

- October 2025: Researchers at the Federal University of Technology, Owerri, reported a method intended to reduce diesel engine pollution without compromising performance. The work points to continued innovation pressure around NOx and particulate reduction. It also supports ongoing OEM and fleet interest in combustion and after-treatment pathways that limit runtime emissions as air-quality scrutiny tightens.

- April 2024: Weichai Power announced a diesel engine reaching 53.09% thermal efficiency, exceeding typical diesel efficiency benchmarks. The result strengthens total cost-of-ownership differentiation in prime and high-runtime applications. It also reinforces the competitive push toward advanced combustion and systems optimization alongside emissions compliance.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the diesel power engine market covers revenue generated from diesel-fueled engines used to deliver mechanical power for stationary power needs, and then sold into end users through OEM and aftermarket channels across regions.

Scope exclusions: We exclude natural gas engines, gasoline engines, and pure electric powertrains, and we do not count the full generator set package value beyond the engine and its core engine-related auxiliaries.

Segmentation Overview

- By Capacity Range

- Up to 75 kVA

- 75 to 375 kVA

- 375 to 750 kVA

- 750 to 2,000 kVA

- Above 2,000 kVA

- By Application

- Stand-by

- Prime/Continuous

- Peak-shaving

- By End User

- Industrial

- Commercial

- Residential

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Spain

- NORDIC Countries

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Australia and New Zealand

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Egypt

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was first used to set a clean demand and supply picture, before assumptions were pushed into the model. We referenced public and official sources such as US Energy Information Administration data (diesel consumption and pricing signals), International Energy Agency publications (power demand context), UN Comtrade (engine and parts trade flows), World Bank indicators (industrial activity and infrastructure trends), and US EPA and European Environment Agency materials for emission-related context that influences replacement timing.

To convert those signals into market-ready inputs, we also reviewed annual reports, 10-K style filings, investor decks, and product catalogs to map typical kVA ratings, application usage, and channel structures. A paid company financials and intelligence subscription was used selectively to normalize reported revenue lines and to avoid double counting between engine sales and packaged systems. These are illustrative sources, and many other public references were also checked to collect, validate, and clarify data points during the work.

Primary Interviews and Surveys

Primary work focused on structured expert interviews and short surveys with OEM-facing executives, distributor leaders, service partners, and large end users across industrial, commercial, and residential demand pools. Since this is a global market, viewpoints were balanced across APAC, EMEA, and the Americas so pricing, utilization, and replacement cycles could be tested under different operating conditions, and then gaps were closed through re-contacts when assumptions moved materially.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 12% | APAC: 45% |

| Mid tier: 46% | Functional/Unit leaders: 38% | EMEA: 35% |

| Smaller Players: 16% | Managers: 50% | Americas: 20% |

Market-Sizing & Forecasting

Market sizing is built using a top-down and bottom-up combination, where demand is reconstructed from power equipment deployment signals, replacement cycles, and trade and production indicators, and then filtered into diesel power engine value using observed penetration and application shares. The totals are corroborated with selective bottom-up approximations, such as sampled average selling price by kVA band multiplied by estimated unit volumes from channel checks, which are then sanity-checked with supplier and distributor feedback.

Key inputs used in the model include installed base and replacement timing for standby and prime applications, kVA rating mix shifts, regional diesel price movements that influence runtime behavior, infrastructure and industrial activity indicators that influence purchases, and import-export trends for engines and major parts that signal supply availability. Forecasting uses scenario analysis supported by simple multivariate regression on industrial output and power demand indicators, and then it is adjusted where experts expect policy or fuel-price volatility to change buying patterns. Where bottom-up visibility is weak (for example in fragmented service channels), conservative ranges are applied and then narrowed after follow-up validation.

Data Validation & Update Cycle

Outputs are validated through cross-checks that compare implied engine revenue with independent signals like generator deployments by rating band, engine trade intensity, and public commentary on orders and backlogs. When a region shows an unusual jump, the drivers are reviewed, the pricing and volume split is rechecked, and respondents are re-contacted to confirm whether a one-off event explains the change.

A multi-step analyst review is followed before sign-off, covering math checks, variance checks against prior editions, and logic checks on the most sensitive variables. Reports refresh annually, and interim updates are triggered when material events happen, such as emission rule changes, major capacity additions, or sharp diesel price swings. Before delivery, we do a final pass so clients receive the latest updated view.

Mordor Intelligence's Diesel Power Engine Market Sizing Compared With Other Published Estimates

Published market sizes for diesel power engines can vary a lot, even when the topic label looks the same, because the counted product scope and the pricing unit are not always aligned. Differences also show up when one estimate is updated more recently than another, or when demand is tied to different indicators such as engine revenue versus packaged system deployments.

Some publications appear to treat the market as a broader pool that includes complete generator sets and related equipment value. For Mordor Intelligence, the value line is limited to diesel power engines mapped by kVA ratings and applications, so generator alternators, enclosures, and balance-of-system components are not added into the engine total.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 12.87 B (2026) | |

| Industry Publisher A | USD 8.75 B (2024) | Uses an earlier base year and a longer horizon, and its scope language reads broader across end uses and power bands, which can shift the included revenue pools and the pricing assumptions used for ASP progression. |

| Global Publisher B | USD 8.78 B (2024) | Anchors the market in 2024 and may blend engine revenue with packaged equipment pricing in some applications, and this can move the total depending on how generator set components and service-related value are counted. |

The spread across sources is mainly explained by base-year choice and what is counted as engine-only revenue versus packaged systems and adjacent components. When the model is anchored to rating-band mix, application usage patterns, and regional demand signals, the result stays traceable to inputs that can be rechecked and updated in a repeatable way.

Key Questions Answered in the Report

What is the expected CAGR for diesel power engines between 2026-2031?

The diesel power engine market is projected to grow at a 5.33% CAGR during 2026-2031, driving the market from USD 12.87 billion in 2026 to USD 16.69 billion in 2031.

Which capacity range is expanding the fastest?

Engines rated 375-750 kVA are growing at 7.5% annually, driven by hospital, telecom, and manufacturing upgrades.

Why does Asia-Pacific dominate future demand?

Large data-center rollouts, infrastructure spending, and rural electrification gaps give Asia-Pacific 38.1% share and a 6.6% growth trajectory.

How are emissions regulations affecting OEM costs?

Compliance with EPA Tier 4 Final and EU Stage V adds roughly USD 18,000 per 500 kVA unit for after-treatment hardware.

Are batteries replacing diesel in standby roles?

Batteries are gaining share for four-hour autonomy needs, but diesel remains the cost-effective choice for multi-day backup where 72-hour reserves are mandated.

Which companies lead R&D on alternative fuels?

Rolls-Royce and Cummins are testing hydrogen blends and hybrid controllers, while Mitsubishi Heavy Industries focuses on marine IMO III compliance.

Page last updated on: