Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.13 Billion |

| Market Size (2031) | USD 3.49 Billion |

| Growth Rate (2026 - 2031) | 10.36% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

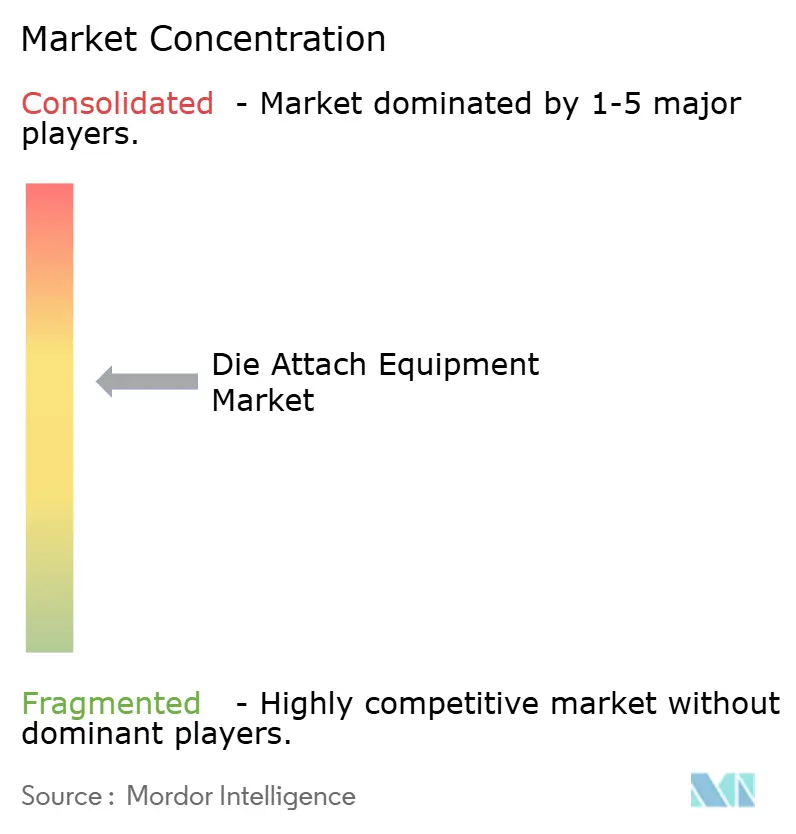

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Die Attach Equipment Market Analysis by Mordor Intelligence

Die attach equipment market size in 2026 is estimated at USD 2.13 billion, growing from 2025 value of USD 1.93 billion with 2031 projections showing USD 3.49 billion, growing at 10.36% CAGR over 2026-2031. Government incentives that localize semiconductor supply chains, rapid electrification of vehicles, and the surge of chiplet-based AI accelerators collectively keep capital spending on new bonding tools on an expansionary path. In parallel, wide-bandgap device adoption is pushing process temperatures and pressure profiles higher, while mini-LED backlights and emerging micro-display fabs demand sub-5 µm placement repeatability. Equipment suppliers are reacting with hybrid architectures that merge flip-chip, eutectic, and pressure-sintering heads on a single chassis so that contract manufacturers can tackle heterogeneous integration without line changeovers. Larger average selling prices for these configurable platforms are buffering vendors against smartphone-centric slowdowns, and process control software that captures bond-by-bond traceability is emerging as a differentiator in customer qualification audits.

Key Report Takeaways

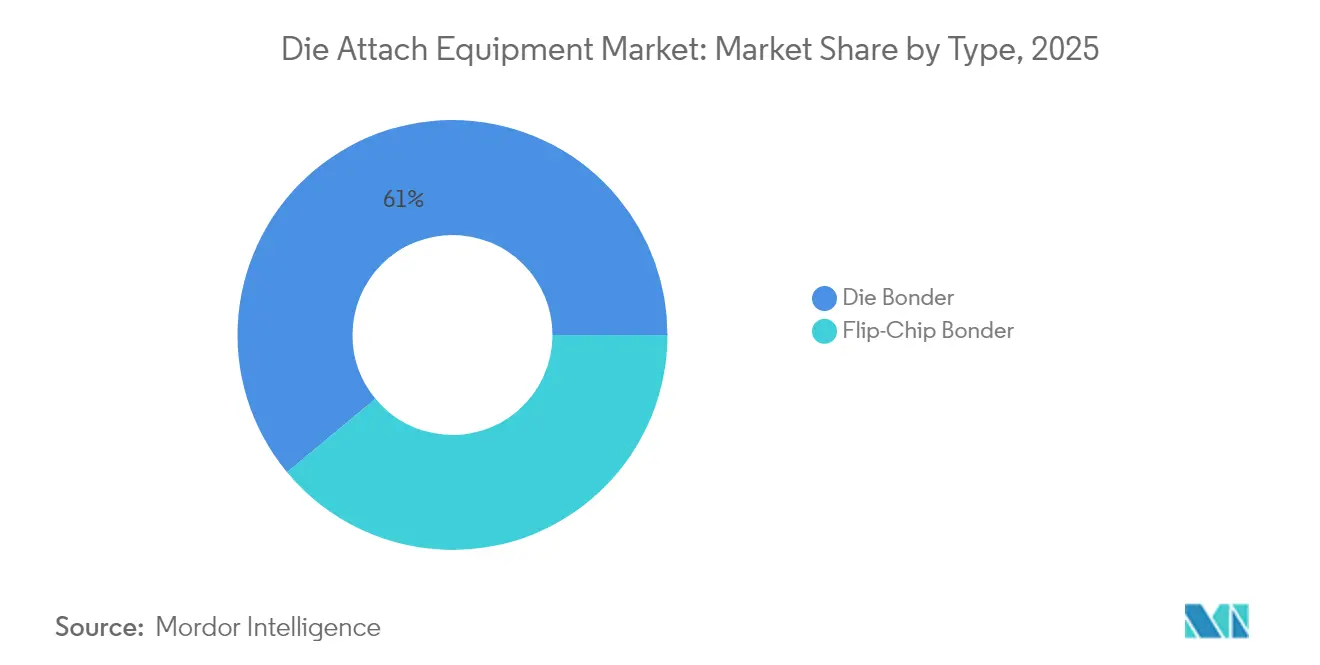

- By bonder type, die bonders led with 61.02% of die attach equipment market share in 2025, while flip-chip bonders are projected to log an 11.35% CAGR through 2031.

- By bonding technique, epoxy accounted for 37.64% of the die attach equipment market size in 2025; hybrid bonding is forecast to expand at a 11.58% CAGR to 2031.

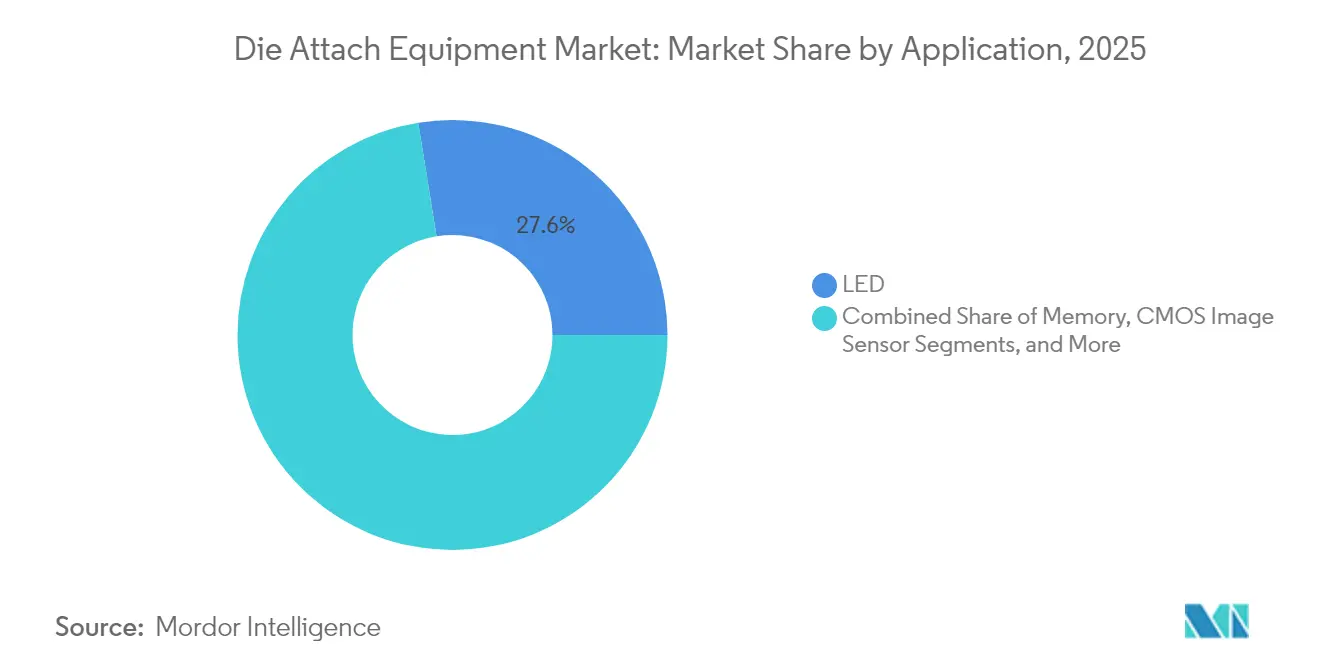

- By application, LED manufacturing contributed 27.55% of the die attach equipment market size in 2025, and optoelectronics/photonics is advancing at a 12.96% CAGR through 2031.

- By end-user industry, consumer electronics held 32.74% of the die attach equipment market share in 2025, whereas automotive and transportation record the highest projected CAGR at 14.02% between 2026 and 2031.

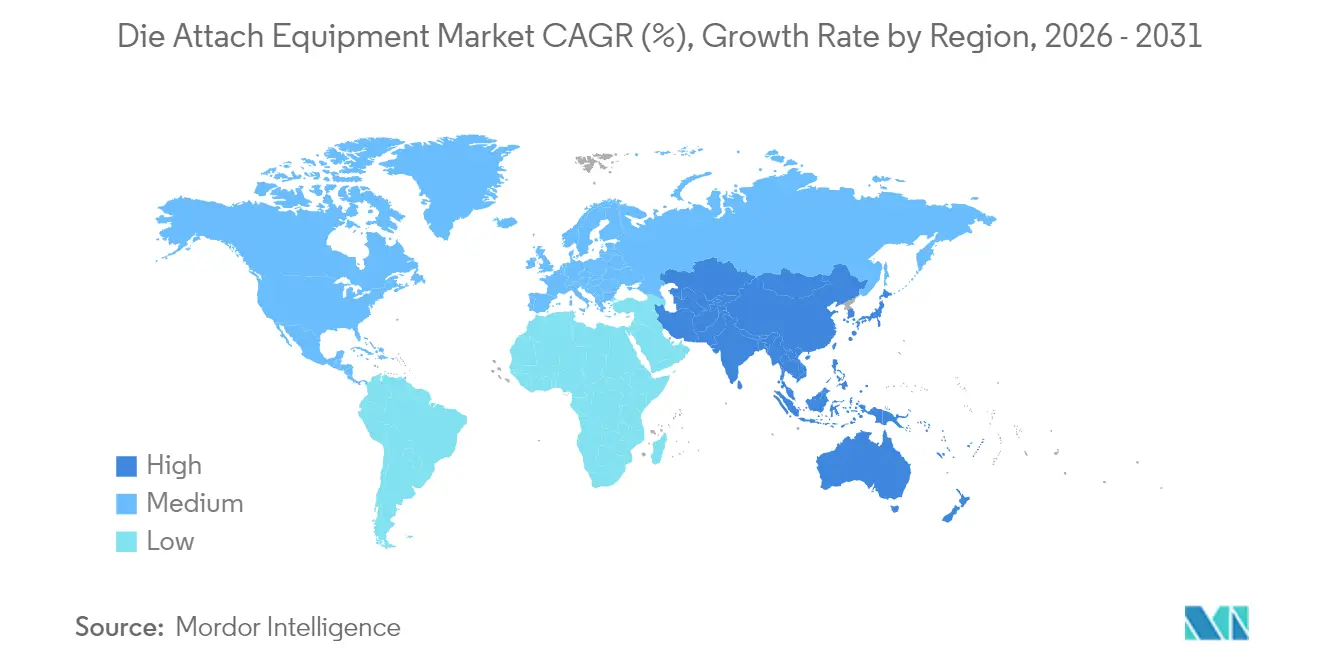

- By geography, North America captured 55.05% of the die attach equipment market size in 2025; Asia-Pacific is rising at a 13.31% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Die Attach Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of AuSn eutectic die-attach in advanced RF modules | +1.80% | Global, with early gains in North America, Europe | Medium term (2-4 years) |

| Proliferation of SiC/GaN discrete power devices in EV inverters | +2.30% | APAC core, spill-over to North America & EU | Short term (≤ 2 years) |

| LED mini-/micro-display capacity build-out in Asia | +1.50% | APAC, particularly China, Taiwan, South Korea | Short term (≤ 2 years) |

| Heterogeneous integration demand for Chiplet-based AI accelerators | +2.10% | Global, with concentration in Taiwan, North America | Medium term (2-4 years) |

| Government CHIPS-style fab equipment incentives outside the US | +1.40% | North America, EU, with expansion to India, Japan | Long term (≥ 4 years) |

| Shift toward high-mix, low-volume photonics packaging lines | +0.90% | North America & EU, niche expansion to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of AuSn eutectic die-attach in advanced RF modules

Gold–tin eutectic bonding has regained popularity because 5G millimeter-wave and satellite payloads dissipate higher heat loads than legacy epoxy joints can handle. The 80/20 alloy melts at 280 °C yet keeps thermal conductivity near 57 W/mK, enabling hermetic packages that survive thermal cycling in aerospace and defense deployments.[1]Palomar Technologies, “Technical Papers & e-Books,” palomartechnologies.com Pulsed-heat tools confine energy to the joint area and prevent substrate warpage, which historically limited AuSn adoption on larger laminated boards. Although volume remains modest, margins are attractive and justify premium equipment pricing as OEMs tighten longevity specifications for mission-critical radios.

Proliferation of SiC/GaN discrete power devices in EV inverters

Silicon carbide and gallium nitride switches sustain junction temperatures above 200 °C, so automotive Tier-1s are migrating from epoxy to pressure-sintered silver layers that lower thermal resistance and eliminate voids.[2]Bozhon Semiconductor, “FastStar Series,” bozemi.com New die attach platforms incorporate closed-loop pressure monitoring and controlled-atmosphere chambers that complete sintering in less than 3 minutes, outperforming earlier six-minute cycles. Because vehicle programs lock production tooling two years before SOP, equipment suppliers enjoy predictable bookings, yet purchasing waves remain synchronized with model-year launches, leading to revenue lumpiness.

LED mini-/micro-display capacity build-out in Asia

Display makers racing toward direct-view mini-LED backlights are specifying placement repeatability tighter than 3 µm, up from 7 µm tolerances in 2023. Throughput targets now exceed 70 kUPH for mini-LED arrays, requiring parallel pick heads and dual high-resolution vision stacks to identify dice as small as 50 × 125 µm on the fly.[3]ITEC, “Die Attach Solutions,” itecequipment.com Suppliers offering embedded optical binning are winning contracts because they eliminate post-bond inspection stages, shaving two seconds off cycle time per module and freeing floor space in high-cost cleanrooms.

Heterogeneous integration demand for chiplet-based AI accelerators

High-performance GPUs and custom inference engines are shifting to chiplet layouts to sidestep reticle-size limits. Die attach equipment must therefore place compute, HBM, and I/O tiles within 1 µm tolerance so that subsequent hybrid bonding forms low-resistance Cu–Cu interconnects. Vendors integrate machine-learning vision algorithms that classify fiducials under non-uniform lighting, while linear-motor and air-bearing stages deliver 20 nm step resolution.[4]Mycronic, “Microelectronics Die Bonding Systems,” mycronic.com Systems shipping into this niche command ASPs above USD 3 million and generate service annuities because software upgrades extend tool life across successive process nodes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dimensional changes and mechanical unbalance during thermo-compression | -1.20% | Global, particularly affecting advanced packaging | Short term (≤ 2 years) |

| Cyclical slow-down in smartphone CMOS image-sensor cap-ex | -0.80% | APAC core, with secondary impact on North America | Medium term (2-4 years) |

| Talent shortage for sub-5 µm placement accuracy assembly engineers | -0.60% | Global, most acute in North America & Europe | Long term (≥ 4 years) |

| Supply-chain exposure to indium and gold price volatility | -0.40% | Global, with higher impact on cost-sensitive applications | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Dimensional changes and mechanical unbalance during thermo-compression

Thermo-compression bonding exposes substrates to 300 °C loads that trigger differential expansion between silicon, organics, and metal pillars. Warpage exceeding 400 µm causes non-contact points and degrades yield, especially on 90 × 110 mm panels. Although inline metrology now feeds Z-axis corrections to bond heads in real time, physics still caps panel size and slows production ramp-ups. Users consequently run smaller lots while process windows stabilize, lowering overall tool utilization.

Cyclical slow-down in smartphone CMOS image-sensor cap-ex

Global smartphone shipments fell 3.2% in 2024, prompting major sensor fabs to cut capital budgets 15-20% and defer tool deliveries.[5]Semiconductor Industry Association, “CHIPS Act Implementation,” semiconductors.org Because CMOS image-sensor lines dominate die bonding volume in East Asia, equipment orders retraced for two consecutive quarters. Offsetting growth emerges from automotive ADAS cameras, but those projects use smaller wafer starts and cannot fully compensate for handset softness, introducing volatility into quarterly revenue for several toolmakers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Bonder Type: Flip-chip momentum challenges die-bonder incumbency

Die bonders commanded 61.02% of 2025 revenue and remained the workhorse for wire-bonded packaging, memory stacks, and cost-optimized consumer electronics lines, giving them the single-largest slice of the die attach equipment market size. OEMs appreciate the mature process libraries, low consumables cost, and broad operator familiarity these tools deliver. Yet flip-chip platforms are climbing at an 11.35% CAGR as 2.5D interposers and chip-on-wafer-on-substrate flows move from pilot to volume. Increasingly, contract manufacturers want one chassis that can swap feed heads so that both eutectic die and bump-first flip-chips ride the same conveyor. Tool vendors reply with modular decks whose changeover completes in under 8 minutes.

Hybrid product families blur distinctions between bonder types. Stage kinematics now borrow from lithography steppers, with air bearings and linear motors pushing placement three-sigma below 1 µm. Software orchestrates multi-tool cells, routing jobs to the die bonder or flip-chip head according to tape width and solder-mask windows. This flexibility lets customers amortize capital across broader order books, and the strategy secures stickier service contracts for OEMs pivoting toward recurring revenue. The result is tighter competition as emerging vendors court niches such as compound-semiconductor lasers while stalwarts safeguard share in the bulk commodity compute segment.

By Bonding Technique: Hybrid bonding narrows the gap

Epoxy processes held 37.64% of 2025 revenue thanks to material affordability and relaxed thermal budgets that fit legacy ovens, anchoring the largest portion of the die attach equipment market share. Dispense-then-place remains indispensable in sensor and RF-front-end modules where gap-filling counters die thickness variation. Nonetheless, equipment orders for hybrid bonding post 11.58% CAGR as copper-to-copper micro-bumpless contacts sprint ahead of interposer limits.

Hybrid-capable bonders integrate wafer-level planarization checkpoints that verify Cu pad co-planarity within 30 nm, then transition to die-level pick-and-place without breaching the Class 1 clean constraint. Applied Materials’ USD 2.8 billion equity move in Besi underscores the capital intensity required to master this overlay. For users, the step change promises signal latency drops of 35 ps per hop, translating to 5% overall inference speedup in AI accelerators. Yet first-pass yields still lag epoxy by 200 basis points, so adoption centers on premium devices where the ASP cushion absorbs yield drag.

By Application: Photonics steps into the spotlight

LED assembly secured 27.55% of 2025 demand, riding the replacement of fluorescent backlights and the rise of energy-efficient architectural lighting. High-speed carousel pick heads that bond four chips per second keep cost per lumen competitive against OLED. However, optoelectronics and photonics equipment logs a faster 12.96% CAGR, grabbing cap-ex budgets as cloud operators extend 800 G and 1.6 T fiber links and coherent pluggables migrate to shorter reaches.

Photonics packaging obliges sub-micron Z-axis coplanarity so optical axes line up within 0.2 µm, a tougher metric than electrical pad attachment. New bonders therefore embed fringe-field interferometers for in-situ alignment using live optical feedback instead of post-bond rejection. Simultaneous dispense of low-shrink epoxies curbs stress on glass-through-silicon vias, a feature that telephone modules rarely need. Vendors that pre-engineer photonic-specific nests and reflectometry options lock in tool share early because retrofitting general-purpose bonders proves cost-prohibitive after cleanroom hook-up.

By End-User Industry: Electrified mobility accelerates spend

Consumer electronics retained 32.74% of 2025 shipments, leveraging fully depreciated high-volume bonders that withstand narrow factory margins in handset and tablet production. Nevertheless, EV makers are on pace for a 14.02% CAGR in equipment purchases as traction inverters, onboard chargers, and autonomous driving sensors proliferate. Silver-sinter bonders that tolerate 200 °C junctions and 3,000 thermal cycles underpin this growth.

The lengthy automotive PPAP qualification, which spans two years, gives tool vendors visibility but imposes documentation rigor that disqualifies some smaller entrants. Industrial power segments supply baseline demand for motor drives and solar inverters, while telecom and datacom keep incremental orders alive for 5G radios and data-center switches. Aerospace programs, though niche, pay premiums for hermetic AuSn process modules that survive proton radiation in LEO constellations. Collectively, these niches help cushion suppliers over the smartphone troughs that periodically hit Asian OSAT lines.

Geography Analysis

North America controlled 55.05% of 2025 revenue, leveraging the CHIPS Act’s USD 52 billion grants that redirect tool budgets toward domestic fabs. Major tool clusters sit in California and Arizona where process engineers co-locate with design teams from Intel, Nvidia, and AMD. Coupled with strong defense contracts that favor U.S. soil assembly, these dynamics keep premium-price hybrid bonders booked through 2026. Clean-energy subsidies also encourage regional SiC module lines, adding a dependable equipment pull outside traditional microprocessor channels.

Europe follows at a steady pace, buoyed by Infineon and STMicroelectronics expanding wide-bandgap pilot fabs in Germany and Italy. Automotive OEMs anchor demand curves, especially as EU emissions mandates tighten and inverter efficiencies become buying criteria for fleet managers. Although volume manufacturing sometimes migrates to Asian OSAT partners, initial capacity ramps occur domestically so that quality teams can iterate faster. This localized prototyping preserves a portion of bonding tool orders within the bloc and ensures compliance with future carbon-audit frameworks envisioned under the Green Deal.

Asia-Pacific posts the quickest 13.31% CAGR to 2031 as Taiwan’s TSMC pours more than USD 10 billion yearly into CoWoS and SoIC lines serving AI chips. South Korea’s memory titans add flip-chip capacity to package next-gen HBM, while Chinese policy banks extend low-interest loans that finance domestically sourced bonders when export licenses stall. Despite intellectual-property headwinds, several local OEMs replicate legacy die bonder functionality and bundle aggressive service terms, expanding price competition. The region’s density of contract manufacturers lowers response time, allowing quick diffusion of process tweaks across ecosystem partners.

Competitive Landscape

Industry incumbents, ASM Pacific Technology, MicroAssembly Technologies, and Besi, still sit atop revenue tables by virtue of broad portfolios that span wire bond, flip-chip, and hybrid bonding stations. Each vendor offers unified software suites that standardize recipe management, letting contract manufacturers shuffle labor between SMT and packaging lines without extra training. Yet the die attach equipment market is not static; mid-tier innovators like Mycronic and Palomar Technologies are winning design-in slots where sub-micron accuracy trumps unit throughput. Their platforms use air bearings and closed-loop thermal expansion control borrowed from aerospace machining, moving them into higher-margin verticals.

Strategic tie-ups are reshaping share. Applied Materials 9% stake in Besi injects front-end process know-how into back-end assembly, producing an integrated flow that pulls wafers straight from CMP into die-level hybrid bonding. Chinese challengers such as Bozhon Semiconductor lure cost-sensitive buyers with 3,000-UPH mid-accuracy units that undercut foreign prices by 20%, eroding volume at the low end and pressuring incumbents to differentiate.

Niche players focus on photonics and compound semiconductors. SUSS MicroTec tunes bond heads for 2 × 3 mm InP laser chips that feed co-packaged optics, while Palomar’s 3880-II adopts pulsed-heat eutectic for defense-grade RF components. Because these applications carry high ASPs, even single-digit shipment volumes materially affect revenue mix. Supply-chain resilience also influences vendor choice; customers now scrutinize BOM origin to minimize exposure to sanctions. Toolmakers capable of multi-sourcing linear motors and vision modules earn purchasing preference, accelerating a gradual redistribution of share toward companies with diversified component pipelines.

Die Attach Equipment Industry Leaders

Palomar Technologies, Inc.

Shinkawa Ltd.

MicroAssembly Technologies, Ltd.

ASM Pacific Technology Limited

Be Semiconductor Industries N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Applied Materials acquired a 9% stake in BE Semiconductor Industries for USD 2.8 billion to accelerate hybrid bonding solutions.

- January 2025: Mycronic introduced the MRSI-LEAP high-speed die bonder with 1 µm placement accuracy aimed at AI optical modules.

- January 2025: Micross completed the acquisition of Integra Technologies, expanding U.S. OSAT capability.

Global Die Attach Equipment Market Report Scope

Die attach or die bonding is a process of attaching a semiconductor die to a package, a substrate such as a PCB board, or another die. The die attach equipment offering includes multi-chip bonders for advanced packaging through market techniques such as epoxy, soft solder bonders, etc., to various applications such as Memory, RF & MEMS, LED, etc.

The die attach equipment market is segmented by type (die bonder, flip chip bonder), bonding technique (epoxy, eutectic, soft solder, hybrid bonding), application (memory, RF & MEMS, LED, CMOS image sensor, logic, optoelectronics/photonics), and geography (North America Europe, Asia Pacific, Latin America, Middle East and Africa).

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Bonder Type

| Die Bonder |

| Flip-Chip Bonder |

By Bonding Technique

| Epoxy |

| Eutectic |

| Soft Solder |

| Hybrid Bonding |

| Other Bonding Techniques |

By Application

| Memory |

| RF and MEMS |

| LED |

| CMOS Image Sensor |

| Logic |

| Optoelectronics / Photonics |

| Other Applications |

By End-User Industry

| Consumer Electronics |

| Automotive and Transportation |

| Industrial and Power |

| Telecommunications and Datacom |

| Aerospace and Defense |

| Healthcare and Life-Sciences |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Bonder Type | Die Bonder | ||

| Flip-Chip Bonder | |||

| By Bonding Technique | Epoxy | ||

| Eutectic | |||

| Soft Solder | |||

| Hybrid Bonding | |||

| Other Bonding Techniques | |||

| By Application | Memory | ||

| RF and MEMS | |||

| LED | |||

| CMOS Image Sensor | |||

| Logic | |||

| Optoelectronics / Photonics | |||

| Other Applications | |||

| By End-User Industry | Consumer Electronics | ||

| Automotive and Transportation | |||

| Industrial and Power | |||

| Telecommunications and Datacom | |||

| Aerospace and Defense | |||

| Healthcare and Life-Sciences | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the die attach equipment market by 2031?

It is expected to climb to USD 3.49 billion, reflecting a 10.36% CAGR from 2026.

Which bonder type is growing the fastest?

Flip-chip bonders are advancing at an 11.35% CAGR thanks to rising adoption in advanced packaging.

Why is hybrid bonding gaining traction?

Chiplet-based AI accelerators need copper-to-copper connections that hybrid bonding delivers, prompting a 11.58% CAGR in equipment demand.

How big is North America's share of die attach equipment revenue?

The region accounted for 55.05% of 2025 spending, driven by CHIPS Act incentives and advanced packaging R&D.

Which end-user sector shows the highest growth?

Automotive and transportation leads with a 14.02% CAGR as EV power electronics and autonomous systems scale.

What technical challenge limits thermo-compression bonding yields?

Differential thermal expansion causes substrate warpage and micro-cracks when temperatures hit 300 °C, trimming yields in large-panel formats.

Page last updated on: