Diaphragm Pump Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

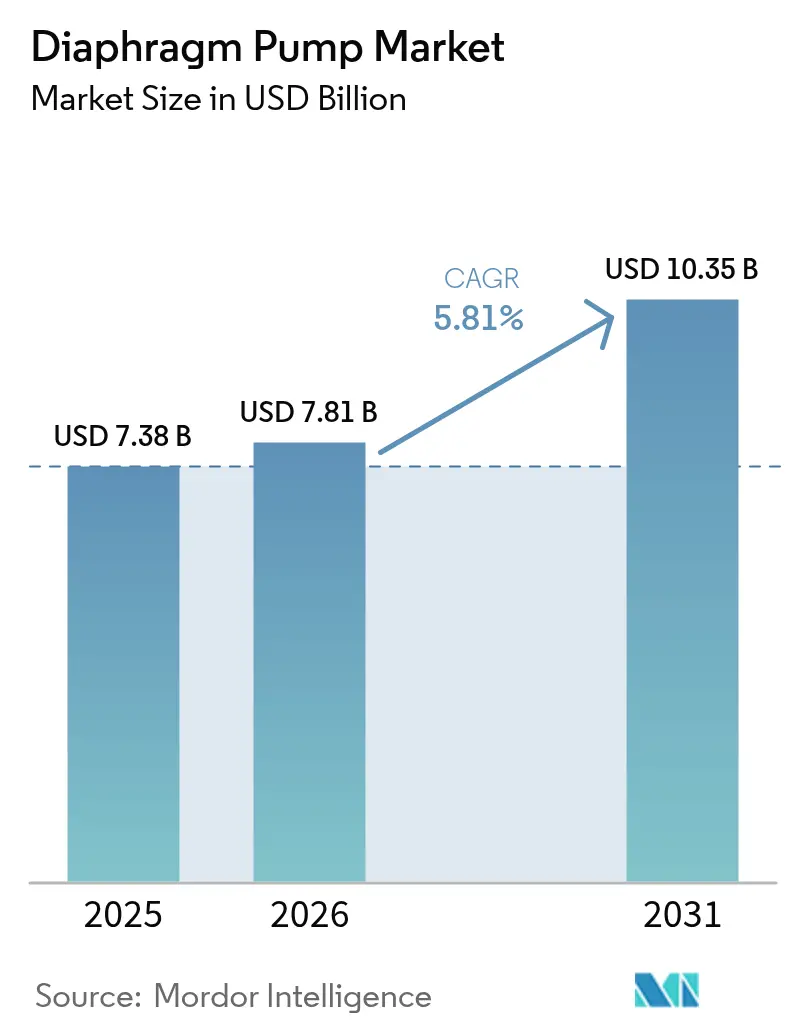

| Market Size (2026) | USD 7.81 Billion |

| Market Size (2031) | USD 10.35 Billion |

| Growth Rate (2026 - 2031) | 5.81% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Diaphragm Pump Market Analysis by Mordor Intelligence

Diaphragm Pump market size in 2026 is estimated at USD 7.81 billion, growing from 2025 value of USD 7.38 billion with 2031 projections showing USD 10.35 billion, growing at 5.81% CAGR over 2026-2031.

Moderate growth is supported by rising industrial automation, tightening environmental regulations that favor leak-free pumping solutions, and a progressive shift toward electrically driven designs that reduce energy use. Rising project activity in water and wastewater treatment, capacity additions in chemicals and battery materials, and demand for shear-sensitive transfer in advanced manufacturing are widening the application base. Technology upgrades around IoT-enabled condition monitoring and predictive maintenance are shortening replacement cycles. Mid-sized players continue to enter niche segments, yet strategic acquisitions by global incumbents are consolidating product portfolios. Collectively, these forces signal a resilient outlook for the diaphragm pump market.

Key Report Takeaways

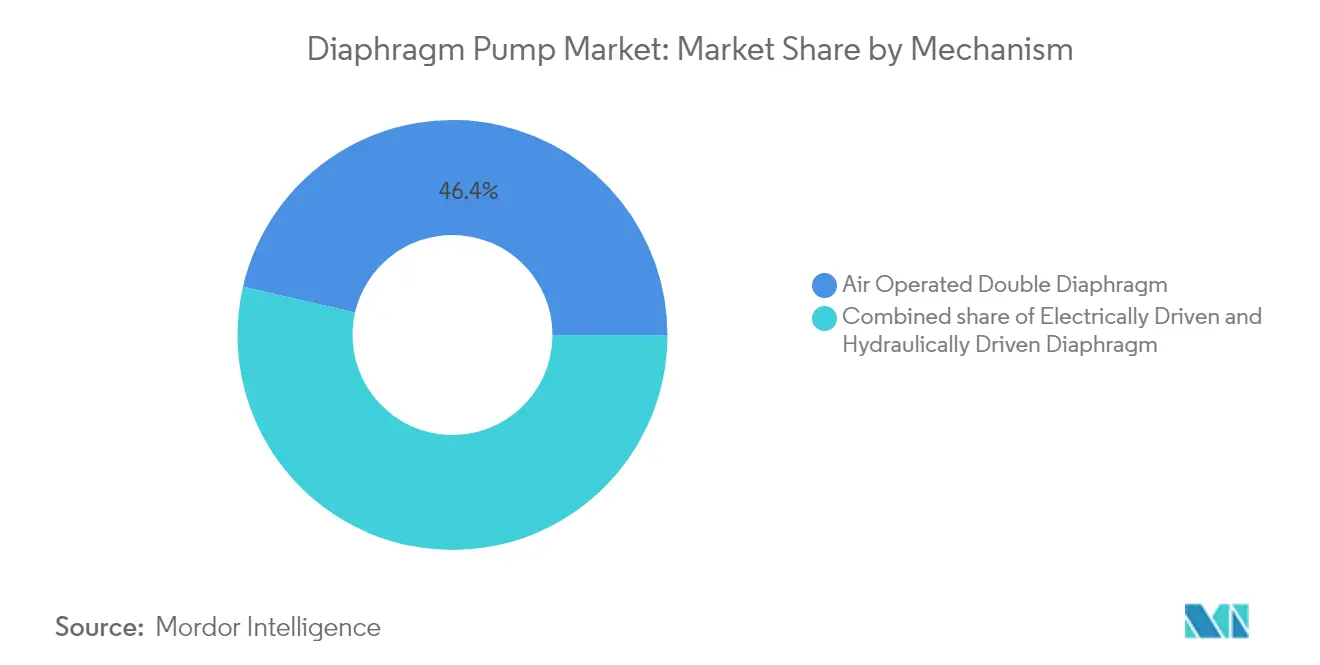

- By mechanism, air-operated double diaphragm pumps led with 46.40% revenue share in 2025; electrically driven diaphragm pumps are projected to expand at a 6.89% CAGR to 2031.

- By body material, metal housings held 52.30% of the diaphragm pump market share in 2025, while plastic and composite constructions are advancing at a 7.12% CAGR through 2031.

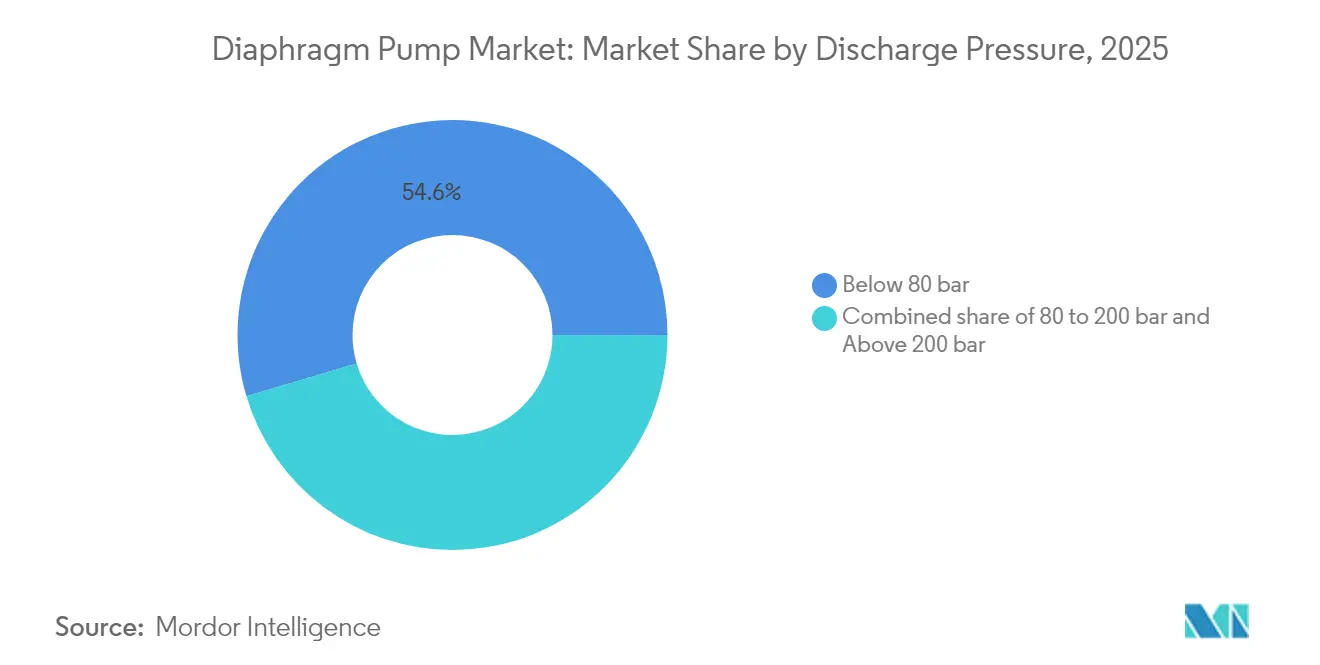

- By discharge pressure, applications below 80 bar captured 54.60% of the diaphragm pump market size in 2025; duties above 200 bar are forecast to grow at a 6.65% CAGR over the forecast period.

- By end-user, chemical and petrochemical processes accounted for a 22.60% share of the diaphragm pump market size in 2025, whereas water and wastewater treatment is expanding at a 6.78% CAGR between 2026-2031.

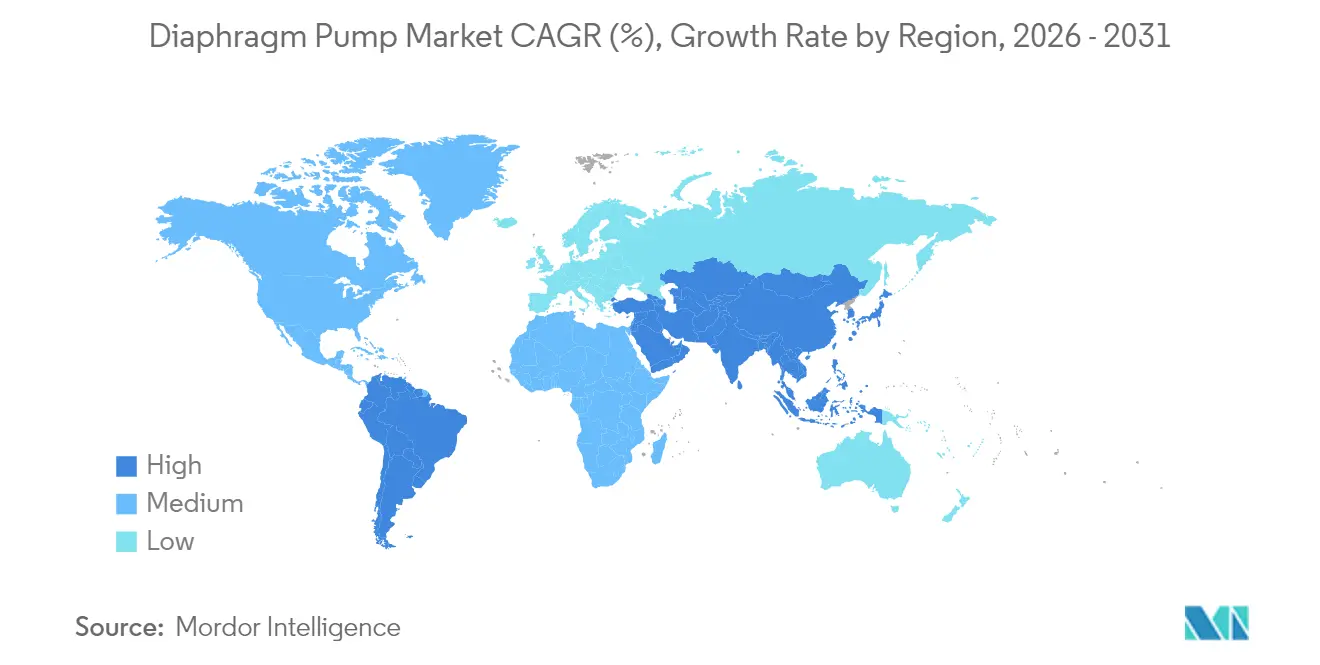

- By geography, Asia-Pacific commanded 36.70% of the diaphragm pump market size in 2025 and is progressing at a 5.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Diaphragm Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Water and wastewater build-outs in emerging economies | +1.20% | Asia-Pacific core, spill-over to Middle East & Africa | Medium term (2-4 years) |

| Expansion of chemical and petrochemical capacity | +1.00% | Global, with focus in Asia-Pacific and Middle East | Long term (≥ 4 years) |

| Tightening fugitive-emission rules that favor leak-free pumps | +0.80% | North America and EU, expanding into Asia-Pacific | Short term (≤ 2 years) |

| Battery-grade electrolyte plants requiring shear-sensitive transfer | +0.60% | Early adoption in China, South Korea, Germany | Medium term (2-4 years) |

| IoT-enabled predictive-maintenance retrofits | +0.50% | North America and EU, selective uptake in Asia-Pacific | Long term (≥ 4 years) |

| Craft-beverage boom driving sanitary AODD installations | +0.30% | North America and EU, emerging in urban Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Water & Wastewater Build-outs in Emerging Economies

Large-scale infrastructure programs across Asia-Pacific and parts of the Middle East are boosting demand for robust fluid-transfer equipment in municipal and industrial treatment plants. The Asian Development Bank approved a USD 41.6 million project in the Philippines that includes a 30 million L per day surface-water facility relying heavily on diaphragm pumps for varied fluid viscosities and leak-free operation(1)Asian Development Bank, “Philippines Water District Development Project,” adb.org. Government funding and stricter discharge guidelines accelerate specification of diaphragm pumps because they offer dry-running capability, clog resistance, and chemical compatibility. Cities upgrading legacy plants treat diaphragm pumps as a life-cycle cost hedge against fines that stem from effluent leaks.

Expansion of Chemical & Petrochemical Capacity

New olefins, polymers, and specialty-chemical complexes continue to surface across China, India, Saudi Arabia, and the United Arab Emirates. LEWA reports rising installations of hydraulically actuated diaphragm metering pumps for hydrocracking, polymerization, and catalyst injection, where precise flow control safeguards product yield(2)LEWA GmbH, “Petrochemical Pump Solutions,” lewa.com. Operators also value hermetic separation between drive and process chambers that prevents hazardous spills. The trend aligns with broader investments in high-purity intermediates and value-added derivatives, ensuring long-run pull for the diaphragm pump market.

Tightening Fugitive-Emission Rules Favoring Leak-Free Pumps

The U.S. Environmental Protection Agency’s methane and VOC regulations now require closed-vent routing and 95% emission reduction from pump stations(3)Environmental Protection Agency, “Standards of Performance for Crude Oil and Natural Gas Facilities,” epa.gov. European regulators mirror these limits under the Industrial Emissions Directive. Compressed-air models remain compliant, yet many operators transition to electric diaphragm pumps that eliminate pneumatic exhaust. Viking Pump’s GB-410 series meets zero-emission provisions, giving early movers an advantage in securing regulatory approval. Compliance costs bolster demand for diaphragm pumps over packed-shaft centrifugal alternatives.

Battery-Grade Electrolyte Plants Demanding Shear-Sensitive Transfer

Lithium-ion cell makers increasingly adopt shear-sensitive diaphragm pumps for cathode-slurry and electrolyte transfer. SANDPIPER notes that AODD designs avoid metal-to-fluid contact, protect slurry particle size, and resist aggressive solvents used in nickel-rich chemistries(4)SANDPIPER Pump, “Battery Production White Paper,” sandpiperpump.com. As plants scale beyond 100 GWh per year, operators standardize on PTFE-lined wetted paths to preserve electrolyte purity. Corresponding capital outlays widen the addressable diaphragm pump market.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility impacting ASPs | -0.70% | Global, acute where steel costs spike | Short term (≤ 2 years) |

| Substitution by centrifugal or peristaltic pumps in low-viscosity duties | -0.50% | Global, focused on cost-sensitive industries | Medium term (2-4 years) |

| Compressed-air energy penalties for AODD units | -0.40% | Global, highest in high-power-cost regions | Long term (≥ 4 years) |

| Urban noise-vibration ordinances hindering plant siting | -0.20% | Densely populated manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility Impacting ASPs

Stainless steel, aluminum, and high-grade elastomer prices have moved erratically since 2024, compressing margins for smaller manufacturers that lack hedging mechanisms. Quarterly list-price adjustments propagate into capital budget uncertainty, delaying customer orders for projects not under schedule pressure. Regions with thin specialty alloy supply chains, including parts of Latin America and Africa, feel cost spikes more acutely because freight surcharges compound volatility.

Substitution by Centrifugal / Peristaltic Pumps in Low-Viscosity Duties

For water-thin fluids that do not require leak-free containment, centrifugal or low-maintenance peristaltic solutions can outcompete diaphragm pumps on upfront cost. Operators in paints, resins, or agricultural chemicals sometimes switch technologies when performance differences are negligible. This competitive pressure is strongest in markets with limited regulatory oversight on fugitive emissions, causing occasional share attrition in the diaphragm pump market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mechanism: Electric Drives Challenge AODD Dominance

The diaphragm pump market size for air-operated double diaphragm units stood at USD 3.42 billion in 2025, or 46.40 % of global revenue, largely due to intrinsic safety and ease of start-up. Electrically driven diaphragm pumps, though smaller in base, are forecast to post a 6.89 % CAGR, outpacing all other mechanisms. Energy-audit data show these models cut operating costs by as much as 80 % and curb compressor-related CO₂ emissions, aligning with corporate net-zero pledges. Integration with variable-frequency drives allows finer dosing accuracy, especially in chemical injection and bioprocess fermenters. Against this backdrop, the diaphragm pump market share of electric models is expected to cross 27.60 % by 2031, supported by grid-connected plants where hazardous-location certification is feasible. AODD designs still dominate in solvent recovery, paint circulation, and explosion-prone zones because they run on shop air and stall without overheating.

A similar pattern emerges in hydraulically driven diaphragm pumps, which retain pockets of demand in high-pressure transfer above 200 bar, such as offshore injection skids and testing rigs. Despite slower growth, vendors enhance hydraulic frames with leak-detection sensors and magnetites to capture metal debris. Tier-two producers differentiate through integrated accumulator dampening that steadies pulsation, offering users an alternative when compressed air is scarce and high voltage is impractical.

By Body Material: Plastic Composites Gain Ground

Metal casings—stainless steel, cast iron, and aluminum—represented USD 3.86 billion of diaphragm pump market size in 2025, equal to a 52.30 % revenue share. They remain dominant for abrasion resistance, thermal stability, and high-pressure integrity in mining leachate and refinery units. Yet plastic and composite pumps are expanding at 7.12 % CAGR. Polypropylene housings coupled with PTFE heads mitigate corrosion in acid-transfer circuits, notably in battery-grade phosphate lines. Lightweight builds ease installation on elevated pipe racks and reduce freight bills for export-oriented chemical plants. Some pharmaceutical users prefer PVDF constructions that meet ASME-BPE electropolish criteria, shrinking validation time.

Metal users respond by upgrading surface treatments, such as duplex stainless alloys and ceramic coatings, to fend off corrosive sludge and extend mean time between failures. Additive manufacturing also gains traction for complex valve plates, slashing lead time on custom low-volume orders. This dual track keeps both material categories viable, yet the shift underscores how application-specific corrosion resistance shapes procurement.

By Discharge Pressure: High-Pressure Applications Accelerate

Below 80 bar duties generated 54.60 % of 2025 global revenue, serving potable-water dosing, paint recirculation, and dairy CIP circuits. However, above-200 bar applications, while less than 14.90 % of current diaphragm pump market size, are projected to rise at 6.65 % CAGR because chemical plants push toward intensified reactions and higher solid concentrations. Operators gravitate to triplex and quintuplex pump heads with PTFE composites to endure cyclical stress. Battery-recycling hydrometallurgy plants and supercritical CO₂ extraction systems exemplify niche pockets driving the high-pressure uptick.

Design innovations such as floating diaphragms with fiber reinforcement curtail compression set, boosting service life from 8,000 to 14,000 hours. Vendors widen aftermarket kits that bundle valves, gaskets, and diaphragms, minimizing downtime when operating above 200 bar. The 80-to-200 bar cohort maintains steady uptake in tailings transfer, metal finishing, and brine desalting, aided by regulatory pushes for zero-liquid discharge infrastructure.

By End-User: Water Treatment Outpaces Chemicals

The chemical and petrochemical sector consumed USD 1.67 billion worth of pumps in 2025, equal to a 22.60 % slice of diaphragm pump market size. Precise metering of catalysts and caustics preserves margin amid volatile feedstock prices. Nonetheless, the water and wastewater segment is on track for a 6.78 % CAGR to 2031, underpinned by UN Sustainable Development Goal investments targeting safe water access. Municipal utilities retrofit diaphragm pumps for lime slurry dosing, polymer flocculant injection, and high-solids sludge transfer. The sector further benefits as desalination plants adopt leak-free hermetic designs to protect downstream membranes.

Oil and gas retains mid-single-digit growth, buoyed by produced-water reinjection, well-stimulation chemical blends, and vapor-recovery mandates for leak-free equipment. Pharmaceutical and biotechnology users prefer compact hygienic pumps that pass validation audits and minimize cross-batch cleaning labor. Food and beverage processors install sanitary AODD units to transfer viscous syrups and brewer’s mash without shear, supporting flavor consistency. Mining and metals depend on diaphragm pumps for solvent-extraction electrowinning; their cyclical expansions translate to lumpy but significant volumes. Pulp and paper mills deploy chemical feed systems for bleaching and pH control, delivering stable replacement demand.

Geography Analysis

Asia-Pacific held USD 2.71 billion of diaphragm pump market size in 2025 and is expected to reach USD 3.83 billion by 2031, equivalent to a 5.95 % CAGR [1]. China’s rising battery and petrochemical complexes, India’s Smart Cities Mission, and Southeast Asia’s wastewater programs reinforce momentum. Provincial subsidies for pollution-control equipment amplify uptake of leak-free units. Mature producers in Japan and South Korea focus on compact electric designs compatible with heavily automated factories.

North America contributed USD 1.89 billion in 2025. The EPA’s ban on methane-venting pneumatic pumps prompts midstream operators to adopt electric ranges, while the craft-beverage surge, mainly in the United States, elevates 3-A sanitary demand. Canada benefits from brownfield oil sands retrofits where low-temperature reliability steers users toward PTFE diaphragm constructions.

Europe generated USD 1.46 billion in 2025. Germany’s specialty-chemicals growth sustains high-pressure metering projects, whereas EU Industrial Emissions Directive upgrades in Italy, Spain, and the Netherlands encourage replacement of packed-gland centrifugal units with diaphragm technology. Regional grants linked to energy-efficiency drive adoption of smart electric pumps integrated with factory analytics.

The Middle East and Africa surpassed USD 0.73 billion in 2025 fueled by water reclamation and oil-field injection. Saudi Arabia’s seawater cooling mega-plants and the United Arab Emirates’ battery-precursor ventures stimulate demand for duplex-stainless and alloy-20 pumps capable of high chloride resistance. Sub-Saharan Africa’s mining sector remains intermittent but promising.

South America reached USD 0.59 billion, led by Brazil’s petrochemical restart initiatives and Argentina’s lithium brine extraction. Local OEM assemblers partner with global licensors to shorten lead times, but currency volatility restrains capex schedules, tempering near-term expansion.

Competitive Landscape

The diaphragm pump industry hosts a mix of diversified conglomerates and focused specialists, resulting in moderate fragmentation. Dover Corporation deepened its portfolio by adding Cryogenic Machinery Corp. and Marshall Excelsior Company for a combined USD 690 million, expanding vertical reach in liquefied gas and clean-energy components. Graco’s QUANTM line leverages XTREME TORQUE motors that cut weight and enable 480 V compatibility, widening addressable retrofits. IDEX Corporation booked record orders of USD 872 million in Q1 2025 and acquired Mott Corporation for USD 1 billion, introducing micro-porous filtration synergies to Warren Rupp diaphragm offerings.

Flowserve reached USD 816.4 million in Q4 2024 pump bookings, highlighting resilient utility and power-generation demand. Meanwhile, mid-tier regional players emphasize localized service centers and faster lead times to stay competitive. Internet-of-Pumps connectivity, life-cycle contract models, and material science improvements remain the central battlegrounds as customers evaluate total ownership costs over upfront price.

Diaphragm Pump Industry Leaders

Idex Corporation

Graco Inc.

Tapflo Group

Dover Corporation

Ingersoll-Rand PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Graco Inc. has upgraded its QUANTM Electric Diaphragm Pumps with XTREME TORQUE motors and 480V compatibility. These enhancements are designed to improve efficiency, reduce costs, and simplify maintenance.

- February 2025: IDEX Corporation bought Mott Corporation for USD 1 billion to expand into micro-precision filtration for semiconductors and water purification.

- January 2025: Dover Corporation announced that it has acquired Cryogenic Machinery Corp. ("Cryo-Mach"). The acquisition will become part of the PSG business within Dover's Pumps & Process Solutions segment.

- May 2024: The Asian Development Bank (ADB) has approved a $41.6 million loan for a water district development project in the Philippines that will utilize diaphragm pumping equipment.

Global Diaphragm Pump Market Report Scope

The diaphragm pump market report includes:

| Air-Operated Double Diaphragm (AODD) |

| Electrically Driven Diaphragm |

| Hydraulically Driven Diaphragm |

| Metal (Al, SS, CI) |

| Plastic and Composite |

| Below 80 bar |

| 80 to 200 bar |

| Above 200 bar |

| Water and Wastewater |

| Oil and Gas |

| Chemical and Petrochemical |

| Pharmaceutical and Biotechnology |

| Food and Beverage |

| Mining and Metals |

| Pulp and Paper |

| Others (Paints, Electronics, etc.) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Mechanism | Air-Operated Double Diaphragm (AODD) | |

| Electrically Driven Diaphragm | ||

| Hydraulically Driven Diaphragm | ||

| By Body Material | Metal (Al, SS, CI) | |

| Plastic and Composite | ||

| By Discharge Pressure | Below 80 bar | |

| 80 to 200 bar | ||

| Above 200 bar | ||

| By End-User | Water and Wastewater | |

| Oil and Gas | ||

| Chemical and Petrochemical | ||

| Pharmaceutical and Biotechnology | ||

| Food and Beverage | ||

| Mining and Metals | ||

| Pulp and Paper | ||

| Others (Paints, Electronics, etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current diaphragm pump market size?

The diaphragm pump market size stands at USD 7.81 billion in 2026, with expectations to reach USD 10.35 billion by 2031 at a 5.81 % CAGR.

Which mechanism segment is growing fastest?

Electrically driven diaphragm pumps are the fastest-expanding mechanism, projected to advance at 6.89 % CAGR through 2031 on the back of energy-efficiency gains and IoT readiness.

Why is Asia-Pacific the largest regional market?

Asia-Pacific commands 36.70 % of global revenue because of large-scale investments in water treatment, chemical capacity expansions, and battery manufacturing that all specify diaphragm pumps.

How do environmental regulations influence adoption?

Tightening fugitive-emission rules in the United States and EU encourage leak-free diaphragm pump installations, particularly electric models that eliminate methane or VOC venting.

Which end-user application is expanding fastest?

Water and wastewater treatment registers the highest growth at 6.78 % CAGR thanks to infrastructure modernization and strict effluent-quality targets worldwide.

What technologies enhance pump reliability?

IoT-enabled predictive maintenance, advanced motor drives in electric pumps, and composite diaphragms with fiber reinforcement collectively extend service life and cut downtime.

Page last updated on: