Diabetic Macular Edema Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

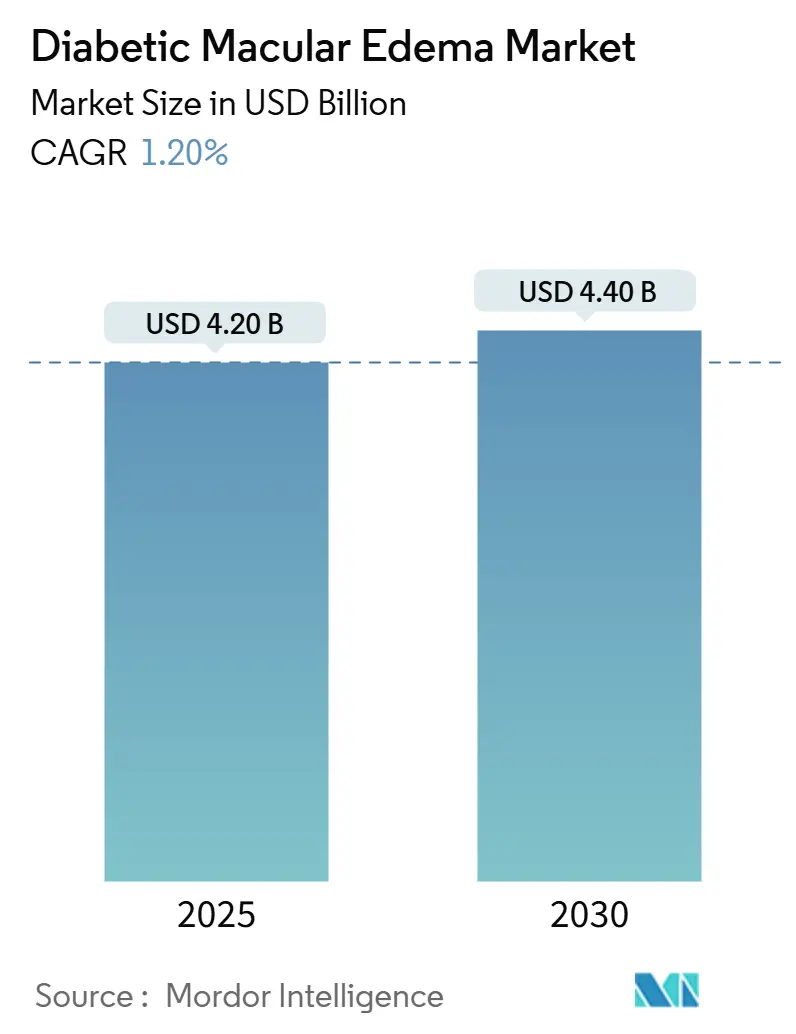

| Market Size (2025) | USD 4.20 Billion |

| Market Size (2030) | USD 4.40 Billion |

| Growth Rate (2025 - 2030) | 1.20% CAGR |

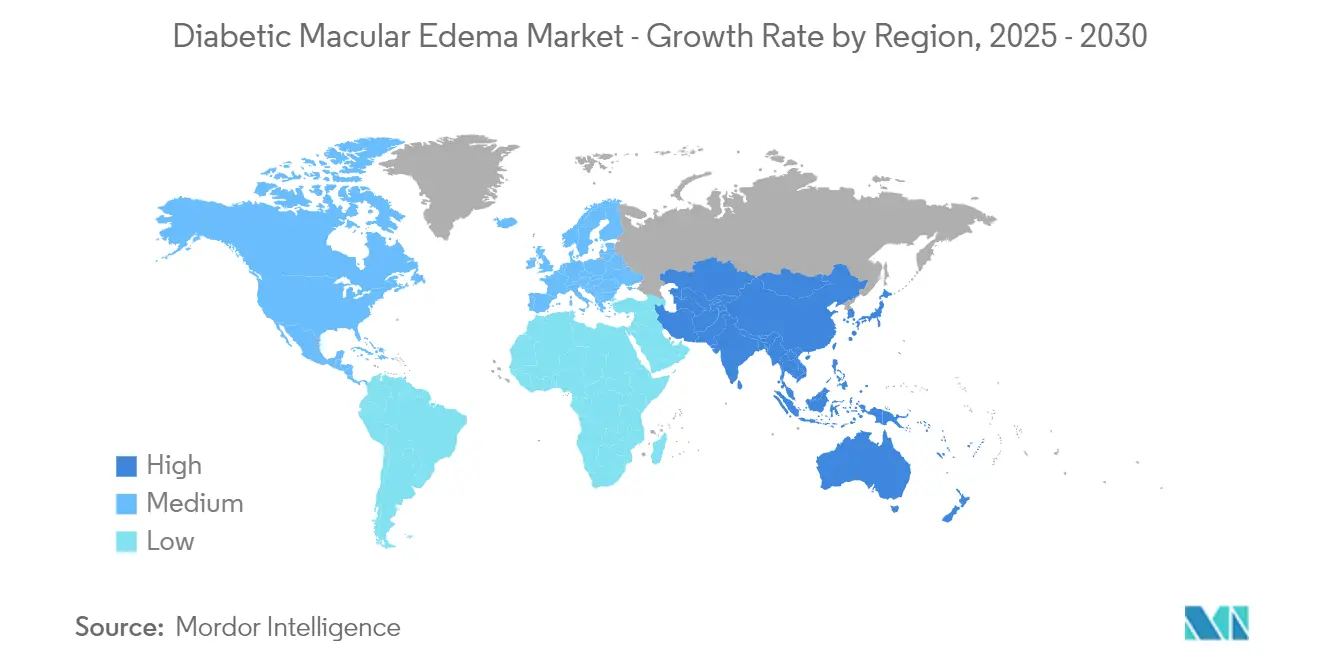

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

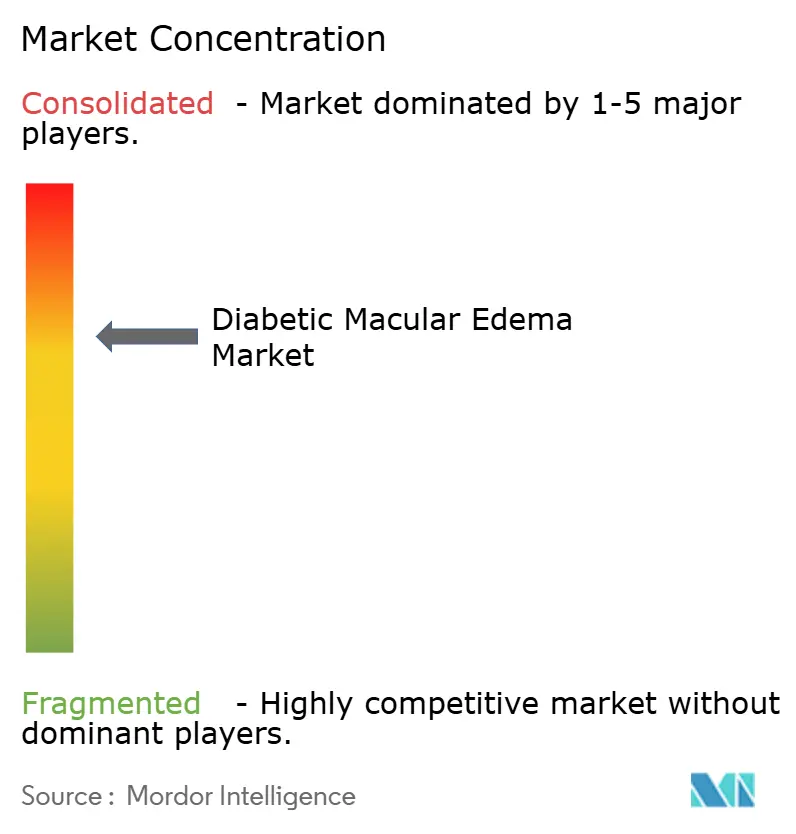

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Diabetic Macular Edema Market Analysis by Mordor Intelligence

The Diabetic Macular Edema Market size is estimated at USD 4.20 billion in 2025, and is expected to reach USD 4.40 billion by 2030, at a CAGR of 1.20% during the forecast period (2025-2030).

Diabetic Macular Edema Market Overview

The diabetic macular edema landscape is experiencing significant transformation driven by broader healthcare industry trends and improved access to specialized care. Healthcare systems worldwide are increasingly prioritizing early detection and management of retinal conditions through enhanced screening programs and referral networks. The integration of value-based care models has fundamentally altered treatment approaches, with approximately 1.55 million prevalent cases reported across major markets in 2023 according to the data published in the Journal of International Journal of Retina and Vitreous in October 2024, highlighting the substantial patient population requiring management. Insurance coverage expansions and favorable reimbursement policies have improved treatment accessibility, while healthcare providers are increasingly adopting standardized treatment protocols to ensure consistent care delivery.

The treatment paradigm has evolved considerably with the emergence of more sophisticated therapeutic approaches and delivery systems. The field has witnessed a shift from traditional laser photocoagulation to more advanced biological therapies, with sustained-release implants gaining particular attention for their potential to reduce treatment burden. Recent developments include the FDA approval of Eylea HD (aflibercept) 8 mg for the treatment of patients with diabetic macular edema (DME) in August 2023, offering extended dosing intervals while maintaining therapeutic efficacy. The introduction of biodegradable steroid implants and novel drug delivery systems has created additional options for clinicians, particularly benefiting patients who show suboptimal response to conventional treatments.

Digital transformation has revolutionized disease management and patient care coordination in the DME space. The widespread adoption of telemedicine platforms has enhanced access to specialist care, particularly beneficial for patients in remote areas or those with mobility limitations. Advanced imaging technologies coupled with artificial intelligence algorithms have improved diagnostic accuracy and treatment planning, with nearly 45% of eye care providers reporting increased utilization of digital health tools for patient monitoring in 2023. These technological advancements have enabled more precise disease progression tracking and personalized treatment adjustments.

The industry has witnessed a notable shift toward personalized medicine approaches, reflecting the heterogeneous nature of DME and varying patient responses to treatment. Demographics analysis reveals that the age group of 45-64 years represents the largest patient population suffering from DME worldwide. This understanding has led to more tailored therapeutic strategies based on individual patient characteristics, genetic markers, and response patterns. Healthcare providers are increasingly utilizing biomarker-based approaches and advanced diagnostic tools to optimize treatment selection and timing, resulting in improved patient outcomes and resource utilization.

Global Diabetic Macular Edema Market Trends and Insights

Increasing Prevalence of Diabetic Macular

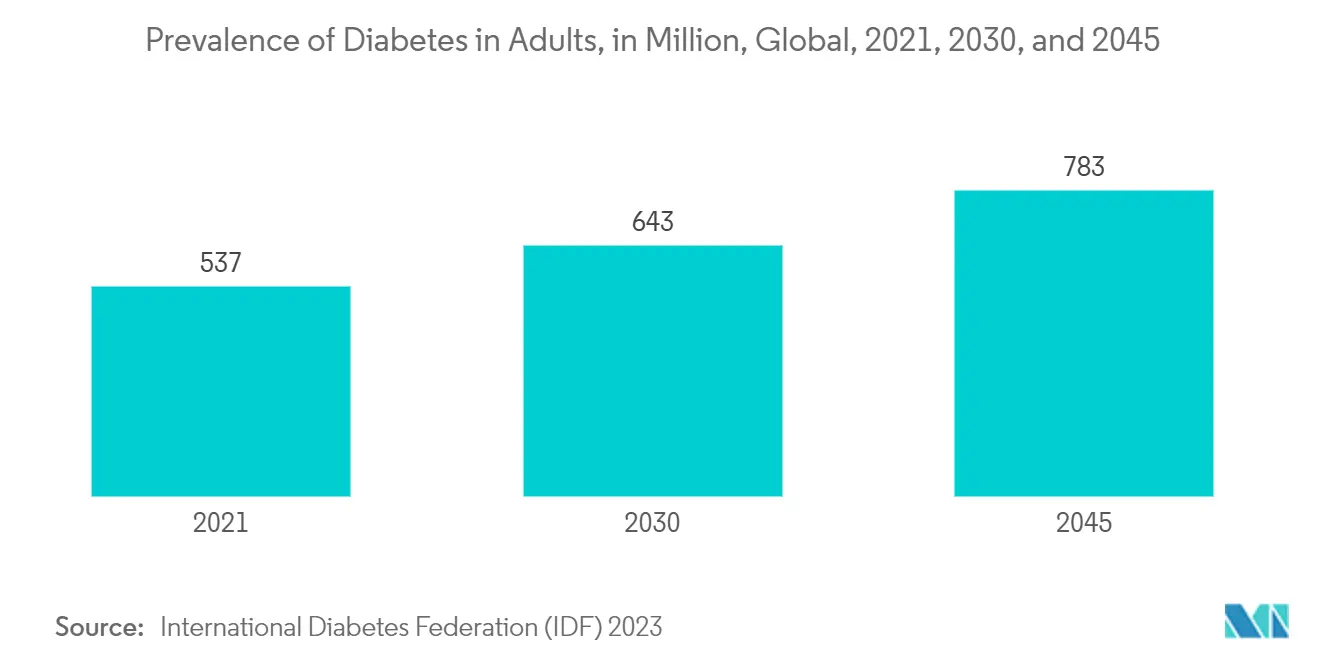

The rising prevalence of diabetic macular edema (DME) represents a significant driver for market growth, affecting 29 million adults worldwide in 2023 according to the data published in the 2024 annual report of F. Hoffmann-La Roche Ltd. The high patient population highlights a growing patient population requiring effective treatments. This surge in cases stimulates demand for innovative therapies and management options, boosting market growth. Additionally, heightened awareness and advancements in diagnostic technology are further fueling investment and development within the DME market.

The increasing awareness and improved diagnostic capabilities have led to earlier detection of DME cases, particularly in developed healthcare markets. Healthcare providers are now implementing more robust screening protocols for diabetic patients, leading to the identification of DME in its early stages when treatment outcomes are typically more favorable. The establishment of comprehensive diabetic eye care programs in many healthcare systems has enhanced the ability to track and manage potential DME cases, while improved patient education about the importance of regular eye examinations has resulted in higher presentation rates for treatment. This combination of factors has created a more conducive environment for market expansion, as more patients seek and receive appropriate care for their condition.

Technological Advancements & Treatment Innovations

The field of DME treatment has witnessed remarkable technological advancements, particularly in drug delivery systems and imaging technologies. The development of sustained-release implants represents a significant innovation, offering extended drug release periods and reducing the treatment burden on patients. These advanced delivery systems, including intravitreal implants and novel injection technologies, have improved treatment adherence and outcomes by minimizing the frequency of interventions required. Additionally, the integration of artificial intelligence algorithms in diagnostic processes has revolutionized early detection capabilities, enabling healthcare providers to identify and initiate treatment at optimal stages of disease progression. The emergence of home monitoring kits has further transformed patient care, allowing for more proactive management and timely intervention between clinic visits.

The evolution of anti-VEGF therapies continues to drive market expansion through improved formulations and delivery mechanisms. Recent innovations have focused on developing longer-acting compounds and combination therapies that address multiple pathways involved in DME pathogenesis. The introduction of advanced imaging technologies, including enhanced OCT systems and AI-powered analysis tools, has improved the precision of diagnosis and treatment monitoring. These technological developments have not only enhanced treatment efficacy but have also improved the overall patient experience by reducing treatment burden and enabling more personalized care approaches. The integration of telemedicine platforms has further expanded access to specialized care, particularly benefiting patients in remote areas who previously faced barriers to receiving regular treatment.

Growing Pipeline of Emerging Therapies

The robust pipeline of emerging therapies for DME represents a significant market driver, with numerous innovative treatments in various stages of development. Key emerging therapies including OCS-01, THR-149, EXN407, and EYP-1901 are showing promising results in clinical trials, offering potential alternatives or complementary treatments to existing options. The diversity of these pipeline candidates, targeting different aspects of DME pathogenesis, suggests a future treatment landscape that may offer more personalized therapeutic approaches. Gene therapy developments are particularly noteworthy, with several candidates being investigated for their potential to provide long-term or permanent solutions for DME patients, representing a paradigm shift from current management approaches.

The advancement of regenerative medicine approaches in DME treatment has opened new avenues for therapeutic intervention. Stem cell therapies and tissue engineering techniques are being explored for their potential to reverse DME-related damage and restore lost vision, rather than merely managing symptoms. The development of combination therapies that target multiple pathways simultaneously has shown promise in clinical trials, potentially offering more effective treatment options for patients who don't respond adequately to current monotherapies. This expanding pipeline is characterized by innovative approaches such as novel drug delivery systems, targeted molecular therapies, and biotechnology-based solutions, all of which contribute to the potential transformation of DME treatment paradigms. The focus on developing treatments with improved efficacy, longer duration of action, and better safety profiles continues to drive research and development investments in this field.

Diabetic Macular Edema Market Drug Segment Analysis

Anti-VEGF Therapies Segment in Diabetic Macular Edema Market

The Anti-VEGF Therapies segment dominates the diabetic macular edema market, commanding approximately 65% of the market share in 2024. This substantial market position is primarily driven by the proven efficacy of key drugs like Ranibizumab and Aflibercept in treating DME patients. The segment's leadership is reinforced by strong clinical evidence supporting these therapies' ability to reduce retinal thickness and improve visual acuity. Major pharmaceutical companies have invested heavily in developing and marketing these treatments, leading to widespread adoption among healthcare providers. The segment's prominence is further supported by favorable reimbursement policies and inclusion in treatment guidelines across major healthcare markets. Additionally, the continuous development of new formulations and delivery methods has helped maintain the segment's dominant position in the market.

Corticosteroid Therapies Segment in Diabetic Macular Edema Market

The corticosteroid therapies segment is emerging as the fastest-growing segment in the DME market, with a projected CAGR of 2.0% from 2025 to 2030. This remarkable growth is attributed to the increasing adoption of long-acting steroid implants and innovative delivery systems for drugs like Dexamethasone and Fluocinolone Acetonide. The segment's expansion is particularly driven by its effectiveness in treating patients who show insufficient response to Anti-VEGF therapies. Recent technological advancements in drug delivery systems have significantly improved the safety profile and duration of action for these treatments. The segment is also benefiting from growing physician confidence in using corticosteroids as both primary and secondary treatment options. Furthermore, ongoing clinical trials and research initiatives are expected to strengthen the evidence base for these therapies, potentially expanding their application in specific patient populations.

Diabetic Macular Edema Market Form Segment Analysis

Intravitreal Injections Segment in Diabetic Macular Edema Market

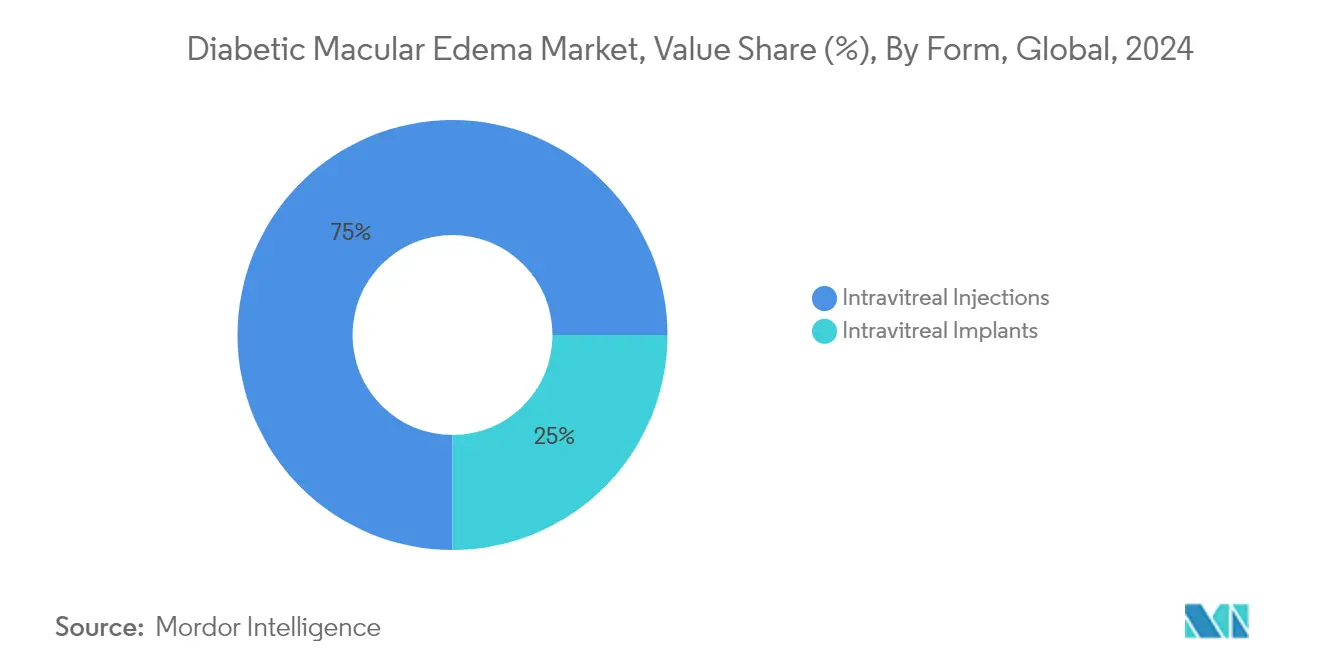

The intravitreal injections segment maintains its dominant position in the diabetic macular edema market, commanding approximately 75% of the market share in 2024. This substantial market presence is primarily attributed to the widespread adoption of anti-VEGF therapies and corticosteroids administered through intravitreal injections. The segment's leadership is reinforced by established treatment protocols, extensive clinical evidence supporting their efficacy, and physician familiarity with administration techniques. Healthcare providers' confidence in intravitreal injections is further strengthened by their ability to deliver precise drug quantities directly to the affected area, ensuring optimal therapeutic outcomes. The segment's robust performance is also supported by the availability of multiple FDA-approved injectable treatments and ongoing research initiatives focusing on improving injection techniques and patient comfort. Additionally, the relatively lower cost compared to implants and the flexibility to adjust treatment regimens contribute to the segment's market dominance.

Intravitreal Implants Segment in Diabetic Macular Edema Market

The intravitreal implants segment is emerging as the fastest-growing segment in the diabetic macular edema market, projected to expand at an impressive CAGR of 2.0% from 2025 to 2030. This remarkable growth trajectory is driven by increasing patient preference for longer-acting treatment options that reduce the frequency of clinical visits. The segment's expansion is further accelerated by technological advancements in implant design, improving both durability and drug release profiles. Pharmaceutical companies are actively investing in research and development to create innovative sustained-release platforms, addressing the need for extended therapeutic coverage. The growing adoption of intravitreal implants is also supported by emerging clinical evidence demonstrating their effectiveness in maintaining stable vision improvements over extended periods. Healthcare providers are increasingly recognizing the potential benefits of implants in improving patient compliance and reducing the overall treatment burden, particularly for chronic DME cases.

Diabetic Macular Edema Market Geography Segment Analysis

Diabetic Macular Edema Market in United States

The United States continues to dominate the global diabetic macular edema market, commanding approximately 42% of the market share in 2024. The market is projected to grow at nearly 1.0% CAGR through 2030, driven by the country's robust healthcare infrastructure and high adoption of advanced treatment options. The presence of sophisticated diagnostic capabilities, including cutting-edge imaging technologies and early detection protocols, has established the US as a pioneer in DME management. The market is further strengthened by favorable reimbursement policies and extensive insurance coverage for DME treatments, particularly for anti-VEGF therapies and novel drug delivery systems. The country's leadership in clinical research and development of innovative therapies, coupled with a strong network of specialized retinal care centers, continues to attract significant investment in DME treatment solutions. Additionally, increasing awareness among healthcare providers and patients about early intervention and treatment options has contributed to better disease management outcomes.

Diabetic Macular Edema Market in Germany

Germany has established itself as a crucial market for diabetic macular edema treatments, characterized by its systematic approach to disease management and strong focus on preventive care. The country's healthcare system emphasizes early diagnosis and intervention, supported by a comprehensive network of ophthalmology centers and specialized clinics. German healthcare providers have been particularly proactive in adopting innovative treatment protocols and participating in clinical trials for new DME therapies. The market benefits from the country's robust healthcare infrastructure and strong emphasis on quality care delivery. The presence of well-established research institutions and academic medical centers has facilitated the development and evaluation of novel treatment approaches. Furthermore, Germany's strategic position within the European Union has made it a key hub for pharmaceutical companies and medical device manufacturers focusing on DME treatments.

Diabetic Macular Edema Market in United Kingdom

The United Kingdom maintains a significant position in the diabetic macular edema market, distinguished by its comprehensive National Health Service (NHS) framework and systematic approach to eye care delivery. The country has implemented robust screening programs and treatment protocols, ensuring widespread access to DME treatments across its population. British healthcare providers have been particularly successful in integrating telemedicine solutions for DME management, especially in remote areas. The market is characterized by strong collaboration between academic institutions, healthcare providers, and industry partners in advancing DME research and treatment options. The UK's commitment to evidence-based medicine has resulted in well-structured treatment guidelines and pathways for DME management. Additionally, the country's focus on patient education and support services has contributed to improved treatment adherence and outcomes.

Diabetic Macular Edema Market in Other Countries

The diabetic macular edema market in other regions, including Japan, France, Spain, and Italy, demonstrates diverse healthcare approaches and market dynamics. These countries have shown significant progress in adopting advanced DME treatments and establishing comprehensive care pathways. Each market is characterized by its unique healthcare delivery system and reimbursement policies, influencing treatment accessibility and adoption patterns. The integration of artificial intelligence and digital health solutions in DME management varies across these regions, with some countries taking leading roles in technological innovation. These markets also demonstrate varying levels of participation in global clinical trials and research initiatives, contributing to the overall advancement of DME treatments. The collective impact of these markets continues to shape global trends in DME management and treatment approaches.

Competitive Landscape

Top Companies in Diabetic Macular Edema Market

The diabetic macular edema market is led by key players including Oculis, Oxurion, Novartis AG, Exonate Limited, Ripple Therapeutics, EyePoint Pharmaceuticals, RemeGen Co., Ltd., Alimera Sciences, Curacle Co., Ltd., and F. Hoffmann-La Roche AG. These companies are actively pursuing product innovation through extensive R&D investments, particularly in developing novel anti-VEGF therapies and sustained-release drug delivery systems. The competitive landscape is characterized by strategic collaborations between pharmaceutical companies and research institutions to accelerate drug development and clinical trials. Companies are expanding their geographical presence through partnerships with regional players and investing in manufacturing capabilities to ensure reliable supply chains. Additionally, there is an increasing focus on developing combination therapies and exploring gene therapy solutions to provide more effective treatment options for patients with diabetic macular edema.

Market Consolidation Drives Industry Evolution Pattern

The diabetic macular edema market exhibits a moderately consolidated structure, dominated by large pharmaceutical conglomerates with established ophthalmology portfolios. These major players leverage their extensive research capabilities, global distribution networks, and strong financial positions to maintain market leadership. The market is witnessing increased merger and acquisition activities, particularly involving smaller biotech companies with promising pipeline products or innovative drug delivery technologies. Regional players are gaining prominence in emerging markets by offering cost-effective alternatives and building strong relationships with local healthcare providers.

The competitive dynamics are evolving with the entry of specialized biotechnology firms focusing exclusively on ophthalmic conditions. These companies are bringing fresh perspectives and innovative approaches to treatment, challenging the traditional market structure. The industry is seeing a trend toward strategic partnerships between established players and emerging companies, combining the resource strength of large pharmaceuticals with the innovation capabilities of smaller firms. This collaborative approach is reshaping the competitive landscape and accelerating the pace of innovation in diabetic macular edema treatments.

Innovation and Accessibility Drive Future Growth

Success in the diabetic macular edema market increasingly depends on developing treatments that offer improved efficacy while reducing the treatment burden on patients. Incumbent companies need to focus on expanding their product portfolios through internal development and strategic acquisitions, while simultaneously investing in real-world evidence generation to demonstrate long-term treatment benefits. Market leaders must also prioritize patient access programs and work closely with healthcare providers to optimize treatment protocols. Additionally, companies need to strengthen their manufacturing capabilities and supply chain resilience to ensure consistent product availability across markets.

For emerging players and contenders, differentiation through innovative drug delivery systems and novel therapeutic approaches presents a significant opportunity. Companies must focus on developing cost-effective solutions that address the growing demand for less frequent dosing regimens. Building strong relationships with key opinion leaders and healthcare providers is crucial for market penetration. The regulatory landscape is becoming more supportive of innovative therapies, but companies must maintain robust compliance programs and actively engage with regulatory authorities. Success also depends on establishing effective pricing strategies that balance accessibility with sustainable business operations, particularly in markets with diverse reimbursement systems.

Diabetic Macular Edema Industry Leaders

Oculis

Oxurion

Novartis AG

Exonate Limited

Ripple Therapeutics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: F. Hoffmann-La Roche Ltd received US Food and Drug Administration (FDA) approval of Susvimo (ranibizumab injection) 100 mg/mL for the treatment of diabetic macular edema (DME). This approval marks a significant advance in managing this condition.

- January 2025: Ashvattha Therapeutics, a clinical-stage company specializing in nanomedicine therapeutics, secured USD 50 million in financing to advance clinical trials for their DME treatment pipeline.

- January 2025: 4DMT reported promising interim results from its 4D-150 SPECTRA clinical trial for diabetic macular edema (DME). The company also announced its alignment with the FDA on the registrational path for the therapy.

- January 2025: Clearside Biomedical's Asia-Pacific Partner, Arctic Vision, received regulatory approval for suprachoroidal treatment for macular edema in Australia and Singapore, expanding geographic reach.

- July 2024: F. Hoffmann-La Roche Ltd.’s Vabysmo demonstrated sustained efficacy over four years in DME treatment, with many patients extending dosing intervals to 3-4 months.

- April 2024: UNITY Biotechnology Inc. extended its Phase 2b ASPIRE clinical study, which evaluates UBX1325 for the treatment of diabetic macular edema (DME). This extension aims to further assess the efficacy and safety of UBX1325 in addressing this condition.

Global Diabetic Macular Edema Market Report Scope

As per the scope of the report, diabetic macular edema (DME) is a complication of diabetes characterized by the swelling of the macula, the central part of the retina, due to leakage of fluid from damaged blood vessels. This condition can lead to vision impairment and is a major cause of vision loss in individuals with diabetes.

The diabetic macular edema market is segmented into drug, form, distribution channel, and geography. By drug, the market is segmented into Anti-VEGF therapies, corticosteroid therapies, and other drugs. By form, the market is segmented into intravitreal injections and intravitreal implants. By distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies. By geography the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. The report also offers the market size and forecasts for 17 countries across the region. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Anti-VEGF Therapies |

| Corticosteroid Therapies |

| Other Drugs |

| Intravitreal Injections |

| Intravitreal Implants |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug | Anti-VEGF Therapies | |

| Corticosteroid Therapies | ||

| Other Drugs | ||

| By Form | Intravitreal Injections | |

| Intravitreal Implants | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the Diabetic Macular Edema Market?

The Diabetic Macular Edema Market size is expected to reach USD 4.20 billion in 2025 and grow at a CAGR of 1.20% to reach USD 4.40 billion by 2030.

What is the current Diabetic Macular Edema Market size?

In 2025, the Diabetic Macular Edema Market size is expected to reach USD 4.20 billion.

Which is the fastest growing region in Diabetic Macular Edema Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Diabetic Macular Edema Market?

In 2025, the North America accounts for the largest market share in Diabetic Macular Edema Market.

What years does this Diabetic Macular Edema Market cover, and what was the market size in 2024?

In 2024, the Diabetic Macular Edema Market size was estimated at USD 4.15 billion. The report covers the Diabetic Macular Edema Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Diabetic Macular Edema Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: