Retinal Biologics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

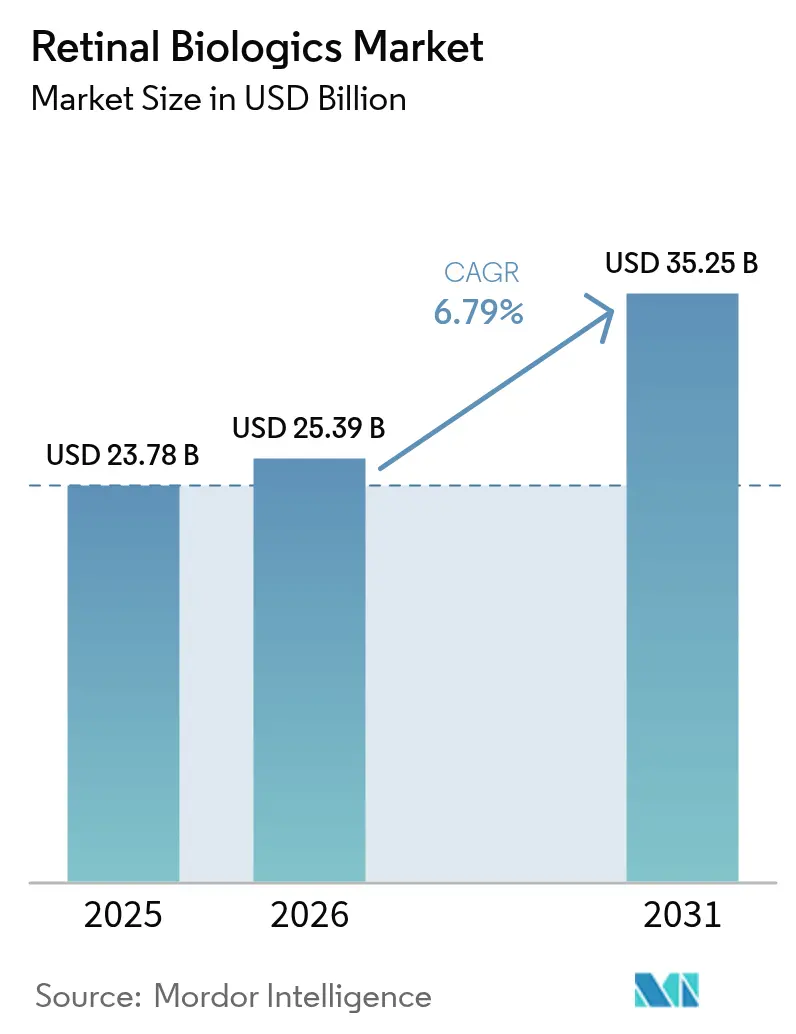

| Market Size (2026) | USD 25.39 Billion |

| Market Size (2031) | USD 35.25 Billion |

| Growth Rate (2026 - 2031) | 6.79% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Retinal Biologics Market Analysis by Mordor Intelligence

Retinal biologics market size in 2026 is estimated at USD 25.39 billion, growing from 2025 value of USD 23.78 billion with 2031 projections showing USD 35.25 billion, growing at 6.79% CAGR over 2026-2031. Expansion is anchored in an aging population that raises age-related macular degeneration (AMD) prevalence, a surge in diabetes that magnifies diabetic retinopathy cases, and breakthrough approvals for gene therapies and long-acting platforms that promise durable efficacy with fewer injections. Biosimilar launches, notably five aflibercept versions cleared by the FDA in 2024, are re-shaping competitive economics even as one-time interventions such as revakinagene taroretcel-lwey (ENCELTO) begin to arrive in clinics. Investment momentum has accelerated, illustrated by Merck’s USD 3 billion EyeBio acquisition and Cencora’s USD 4.6 billion purchase of Retina Consultants of America, underscoring confidence in the retinal biologics market. Macro factors such as payer step-therapy rules that delay access to premium agents and manufacturing bottlenecks that restrict sterile fill-finish capacity temper the growth outlook but have not derailed the retinal biologics market trajectory.

Key Report Takeaways

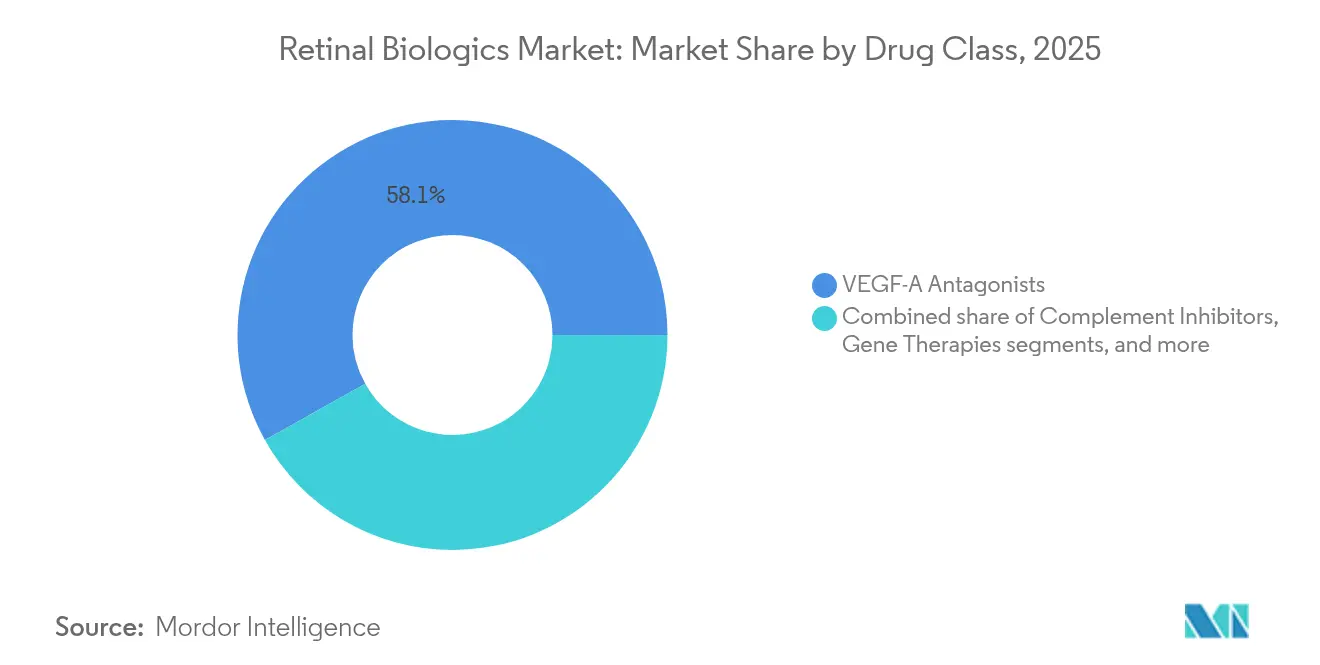

- By drug class: VEGF-A antagonists led with 58.12% of the retinal biologics market share in 2025, while gene therapies are projected to expand at a 13.09% CAGR through 2031.

- By molecule type: Monoclonal antibodies accounted for 45.74% share of the retinal biologics market size in 2025; gene vectors will grow fastest at 11.98% CAGR to 2031.

- By indication: AMD retained 52.02% share in 2025, yet diabetic retinopathy is forecast to post the highest CAGR at 8.94% during 2026-2031.

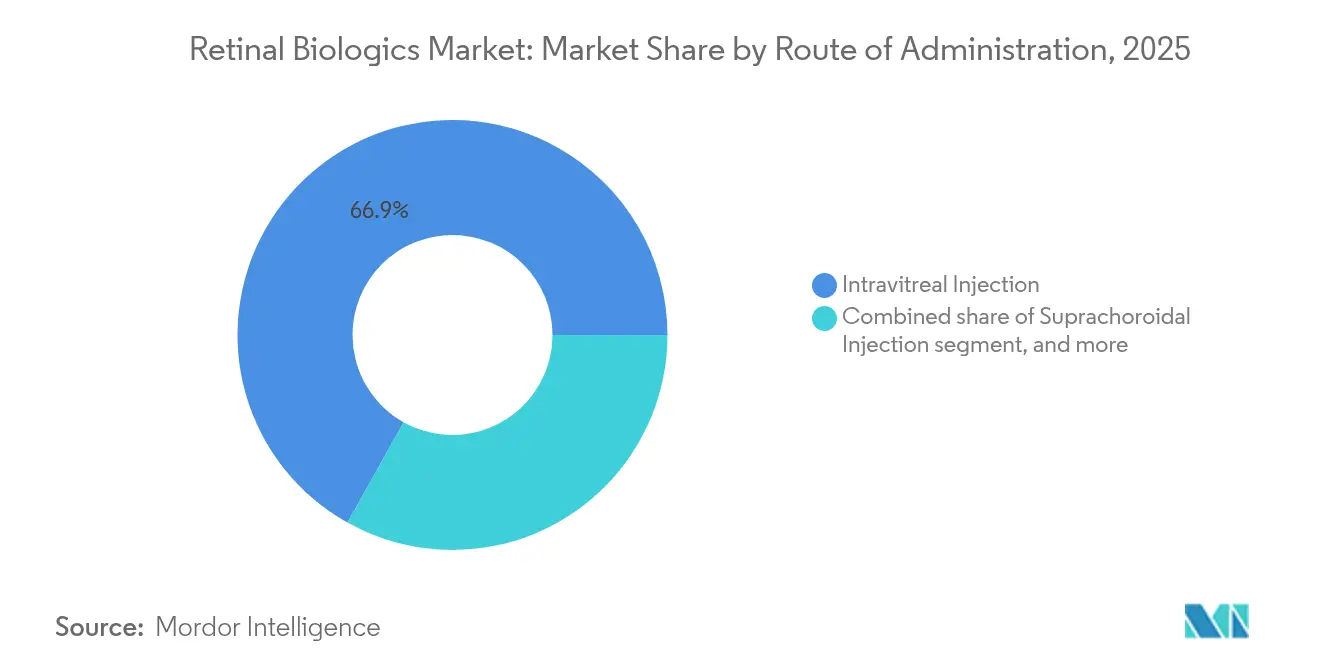

- By route of administration: Intravitreal injections dominated with 66.88% share of the retinal biologics market size in 2025, whereas suprachoroidal delivery will advance at 9.78% CAGR.

- By distribution channel: Hospital pharmacies held 52.11% share in 2025; specialty clinics will rise quickest at a 8.76% CAGR to 2031.

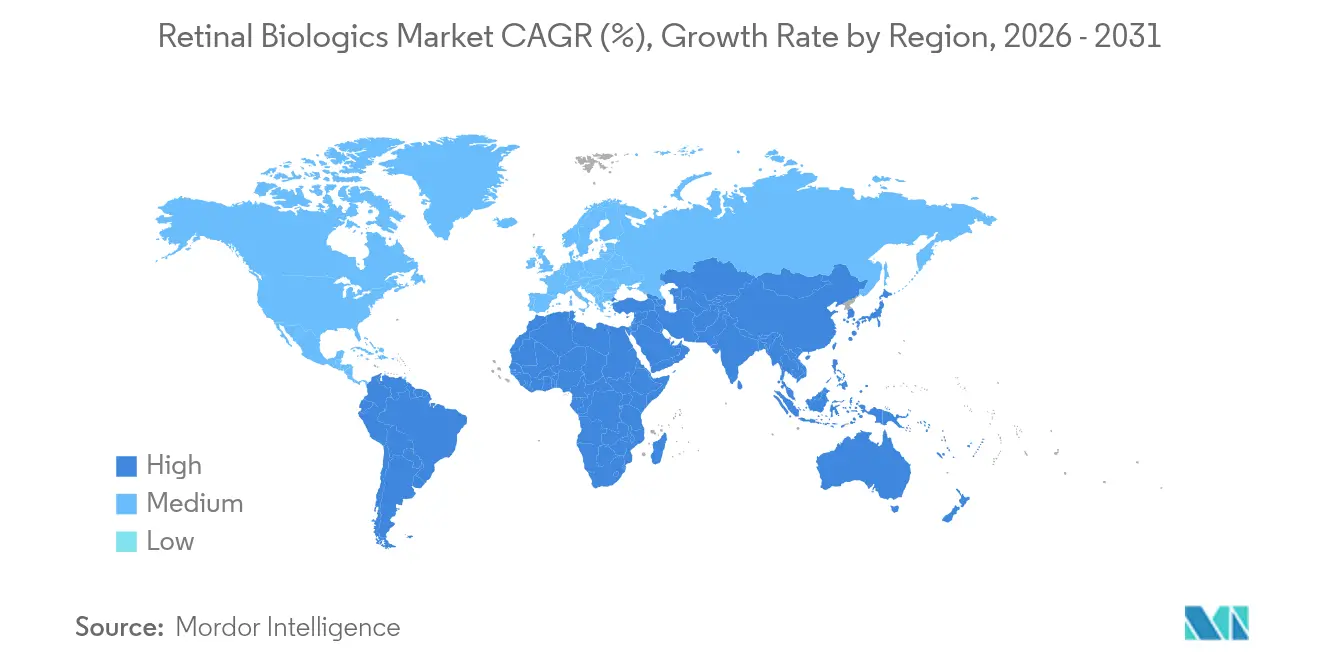

- By geography: North America captured 39.21% of the retinal biologics market size in 2025; Asia-Pacific will lead growth with an 8.12% CAGR over the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Retinal Biologics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Rise in Retinal Disease Burden & Diabetic Population | +1.8% | Global; highest in Asia-Pacific, MEA | Long term (≥ 4 years) |

| Accelerated R&D Output & FDA/EMA Approvals of Novel Biologics | +1.5% | North America, EU; spill-over to APAC | Medium term (2-4 years) |

| Ageing Demographics Driving AMD Cases | +1.2% | Global; concentrated in developed markets | Long term (≥ 4 years) |

| Strong Clinical Adoption of Anti-VEGF Injections | +0.9% | Global | Short term (≤ 2 years) |

| Long-Acting Delivery Platforms Unlocking New Patient Pools | +0.7% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Payer-Led Biosimilar Uptake in Cost-Sensitive Regions | +0.6% | Europe & emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Rise in Retinal Disease Burden & Diabetic Population

Escalating diabetes prevalence is fuelling diabetic retinopathy, which records a 9.26% CAGR and now represents the fastest-growing indication within the retinal biologics market. Emerging economies see parallel gains in diagnostic capacity that expose latent disease pools. One-time modalities such as ABBV-RGX-314 showed clinically meaningful improvements[1]Maricruz Odio-Herrera, “Gene Therapy in Diabetic Retinopathy and Diabetic Macular Edema: An Update,” Journal of Clinical Medicine, mdpi.com in diabetic retinopathy severity scores in the ALTITUDE study, reducing vision-threatening events and hinting at lower lifetime treatment costs. Payers see value, given the USD 134.2 billion economic burden tied to vision loss in the United States alone. Asia-Pacific markets face the steepest climb, combining high myopia rates with accelerating metabolic disease. The driver’s long-term trajectory supports sustained demand for biologics with durable activity.

Accelerated R&D Output & FDA/EMA Approvals of Novel Biologics

Regulatory momentum underpins a vibrant pipeline. In March 2025 the FDA cleared ENCELTO for Macular Telangiectasia type 2, establishing a gene-based precedent. EMA’s positive opinions for OCU410 and OCU410ST reinforce a harmonised European path for advanced therapies. Capital is flowing into capacity: Ritedose is investing USD 81 million in blow-fill-seal lines capable of producing 2.6 billion ophthalmic units annually. AI-driven trial design, exemplified by RetinAI collaborations with Boehringer Ingelheim, is elevating success odds. Together, these factors raise innovation velocity and broaden the retinal biologics market.

Ageing Demographics Driving AMD Cases

Global AMD cases will top 288 million by 2040, and geographic atrophy already affects about 5 million people, ensuring a large, stable addressable population. Developed nations carry the highest incidence, but emerging markets are aging rapidly. Complement inhibition has entered clinical practice, with pegcetacoplan reducing geographic atrophy progression by 25% over 3 years though vigilance for rare vasculitis events remains vital. Korean research on PROX1-neutralising antibody CLZ001 suggests regenerative possibilities extending beyond existing paradigms, as six-month vision restoration was observed in pre-clinical models. Demographic inevitability and scientific progress together sustain AMD-driven demand.

Strong Clinical Adoption of Anti-VEGF Injections

Anti-VEGF injections hold entrenched status, underpinning 67.52% of the 2024 retinal biologics market size, yet treatment fatigue is a recognised limitation. High-dose aflibercept (8 mg) lengthens retreatment intervals without new safety issues[2]Laura Hoffmann, “Aflibercept High-Dose (8 mg) Related Intraocular Inflammation (IOI) – A Case Series,” BMC Ophthalmology, biomedcentral.com, while faricimab captures share through dual VEGF-A/Ang-2 inhibition. Port delivery platforms such as Susvimo add convenience by cutting injection frequency. Entrenched clinician familiarity continues to buoy the retinal biologics market, even as next-generation modalities vie for position.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Regulatory Hurdles & Cap-Ex Intensity | -1.3% | Global; most pronounced in US, EU | Medium term (2-4 years) |

| Safety-Related Label Updates | -0.8% | Global; acute during post-marketing surveillance | Short term (≤ 2 years) |

| Sterile Fill-Finish Capacity Bottlenecks | -0.5% | Global, concentrated in specialized facilities | Medium term (2-4 years) |

| High Drop-Out Rates from Burdensome Injection Schedules | -0.4% | Global, acute in elderly populations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Hurdles & Cap-Ex Intensity

Post-marketing safety issues heighten oversight, as seen when faricimab’s label was updated to flag retinal vasculitis risk. FDA warning letters, including one issued to Regenerative Processing Plant in August 2024 for CGMP violations[3]U.S. Food and Drug Administration, “Warning Letter: Regenerative Processing Plant, LLC,” U.S. Food and Drug Administration, fda.gov, illustrate rising compliance costs. Gene therapy programmes face multi-year follow-up mandates that smaller firms find capital-intensive. Recent FDA refusals of Nesvategrast and Outlook Therapeutics’ wet AMD biologic underscore higher efficacy thresholds that elongate timelines and inflate budgets. These pressures restrain pipeline throughput despite strong investor interest.

High Drop-Out Rates from Burdensome Injection Schedules

Visual outcomes suffer when elderly patients discontinue frequent injections, a scenario exacerbated in regions with sparse specialist coverage. Opthea’s sozinibercept failed to outperform standard care in the COAST trial, highlighting difficulty in justifying added complexity without clear gains. Step-therapy rules that force bevacizumab trials before premium agents introduce delays that can trigger irreversible vision loss. Indirect economic costs of disability climb when adherence falls, reinforcing the value proposition for long-acting or one-time modalities yet hampering short-term uptake prospects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Gene Therapies Challenge VEGF Dominance

Gene therapies validated by ENCELTO’s 2025 approval herald a shift from chronic injection regimens, yet VEGF-A antagonists still commanded a 58.12% retinal biologics market share in 2025. That dominance springs from long-established safety profiles and insurance coverage pathways. However, gene therapies are projected to expand at a 13.09% CAGR, the fastest within the retinal biologics market, reflecting clinician enthusiasm for durable protein expression platforms. Bispecific VEGF/Ang-2 inhibitors such as faricimab offer a bridging technology that lengthens dosing intervals while leveraging proven VEGF biology.

Growth prospects are also buoyed by complement inhibitors like pegcetacoplan and avacincaptad pegol, which widen the mechanism spectrum beyond angiogenesis. TNF-α inhibitors stay niche, primarily treating uveitic entities where systemic inflammation drives pathology—an “Others” bucket houses tyrosine kinase inhibitors and cell-based constructs that could upend today’s hierarchy. Diversifying mechanisms and payer appetite for outcomes-based contracting reinforce the gene therapy growth curve inside the retinal biologics market.

By Molecule Type: Gene Vectors Disrupt Antibody Hegemony

Monoclonal antibodies undergirded 45.74% of the 2025 retinal biologics market size and will continue to post solid volume through brand maturity and biosimilar entry. Yet gene vectors, primarily adeno-associated viruses, will register a 11.98% CAGR, aided by sustained intraocular expression of anti-VEGF proteins in ABBV-RGX-314 trials. Fusion proteins retain relevance owing to aflibercept’s clinical ubiquity, while antibody fragments provide potential cost and penetration advantages.

RNA-based candidates, led by ProQR’s editing platform, target single-mutation diseases and attract orphan-drug incentives. Manufacturing advances such as modular vector suites accelerate lot release and reduce cost per dose. Payers weigh curative promise against upfront cost, yet outcome-based deals are emerging that could normalise one-time prices. As vectors cross regulatory hurdles, gene therapies are positioned to erode antibody hegemony in the retinal biologics market.

By Indication: Diabetic Retinopathy Acceleration Outpaces AMD Growth

AMD secured 52.02% share of the retinal biologics market size in 2025, reflecting decades of development focus and established anti-VEGF coverage. Still, diabetic retinopathy posts a 8.94% CAGR through 2031, bolstered by rising global diabetes prevalence and better screening protocols. ABBV-RGX-314’s ALTITUDE data confirm durable efficacy in both non-proliferative and proliferative forms, signalling that gene therapies could displace repeat injections.

Uveitis remains smaller but benefits from targeted biologics such as filgotinib that cut inflammation flares by over 50% compared with steroids. Rare inherited disorders fall under “Other” and carry premium reimbursement, though patient numbers are limited. Shifting disease mix toward metabolic and genetic conditions emphasizes long-acting solutions and magnifies unmet need, especially in Asia-Pacific, thus expanding the broader retinal biologics market.

By Route of Administration: Suprachoroidal Innovation Challenges Intravitreal Standard

Intravitreal injection accounted for 66.88% of the retinal biologics market share in 2025, founded on proven efficacy, predictable pharmacokinetics, and clinic workflows. Suprachoroidal delivery, advancing at a 9.78% CAGR, deposits drug closer to affected tissues while sparing anterior structures, potentially reducing endophthalmitis risk. Implants such as Susvimo sustain ranibizumab release for up to six months and may supplant monthly injections for compliant candidates.

Topical and transscleral modalities still grapple with posterior segment bioavailability, yet nanoparticle formulations show encouraging permeability gains. Device-enabled routes face reimbursement negotiations that will shape uptake. Overall, clinician confidence coupled with patient convenience considerations will steer modal shifts within the retinal biologics market.

By Distribution Channel: Specialty Clinics Gain Share from Hospital Dominance

Hospital pharmacies retained 52.11% of the retinal biologics market share in 2025 due to bulk purchasing agreements and integrated care pathways. Specialty clinics, however, will post the quickest 8.76% CAGR as injection procedures migrate to high-throughput outpatient suites that improve scheduling and lower administrative overhead. This transition is mirrored by Cencora’s acquisition of Retina Consultants of America, signalling the strategic value of vertically integrated clinical networks.

Retail and online pharmacies continue to confront cold-chain and compounding constraints that limit biologic handling. Nonetheless, home-administered long-acting implants could eventually alter distribution dynamics. For now, specialist settings that combine research participation with routine care delivery are the linchpin of access across the retinal biologics market.

Geography Analysis

North America held 39.21% of the retinal biologics market size in 2025 and will grow at a 6.45% CAGR through 2031, buoyed by reimbursement frameworks that accept premium biologics despite intensifying step-therapy protocols. FDA designations hasten regional approvals, while domestic manufacturing expansions such as Ritedose’s blow-fill-seal project position the United States as a supply hub. Biosimilar entry compresses pricing power, yet innovation cycles remain anchored in the region.

Asia-Pacific will deliver the fastest 8.12% CAGR, driven by demographic aging, diabetes growth, and government investment in ophthalmology infrastructure. Constraints include uneven specialist distribution and sporadic quality lapses; FDA citations of Indian fill-finish plants for sterility failures illustrate lingering hurdles. Multinationals such as Alcon are committing capital to local research centres and physician training programmes to build sustainable demand.

Europe enjoys 6.83% CAGR, aided by advanced therapy regulations and proactive biosimilar policies. EMA approval of Lytenava, a purpose-formulated bevacizumab, addresses off-label use and may reset price anchors. EMA designations for OCU410 variants further cement Europe’s weight in gene therapy roll-out. Middle East & Africa and South America grow from smaller bases at 7.65% and 7.12% CAGRs respectively, offering longer-term upside to early entrants.

Competitive Landscape

Competitive dynamics in the retinal biologics market remain intense yet moderately consolidated. Regeneron, Novartis, and Roche still control much of the VEGF field, but biosimilars—five aflibercept versions approved in 2024—are narrowing margins. Merck’s USD 3 billion EyeBio purchase for Restoret and Cencora’s USD 4.6 billion bid for Retina Consultants of America highlight the premium assigned to late-stage pipelines and distribution scale.

Technology strategies diverge. Incumbents pursue life-cycle extensions through high-dose or port delivery formats, while emerging firms target curative gene therapies or regenerate retinal tissue, as KAIST’s PROX1 programme illustrates. Patent activity around mucus-penetrating formulations underscores ongoing attempts to boost ocular bioavailability. White-space opportunities in rare paediatric dystrophies draw investors, helped by US rare-disease incentives such as priority review vouchers.

Digital health integration is climbing the agenda. RetinAI analytics platforms enhance endpoint sensitivity in trials and refine real-world dosing decisions, creating value-added partnerships with pharma. Overall, strategic differentiation now rests on delivering durable efficacy, easing clinic burden, and aligning price with outcomes—all vital themes for future share capture inside the retinal biologics market.

Retinal Biologics Industry Leaders

AbbVie Inc.

F. Hoffmann-La Roche Ltd

Novartis AG

Outlook Therapeutics Inc.

Regeneron Pharmaceuticals Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Korea Advanced Institute of Science & Technology (KAIST) team reported six-month vision restoration in mice using PROX1-neutralising antibody CLZ001, paving the way for first-in-human trials by 2028.

- May 2025: FDA granted rare paediatric disease designation to Ocugen’s OCU410ST gene therapy for Stargardt disease, enabling a potential priority review voucher upon approval.

- April 2025: Biocon Biologics reached settlement agreement with Regeneron to commercialize aflibercept biosimilar Yesafili in the US by second half of 2026, resolving patent litigation and enabling market entry.

- March 2025: FDA approved revakinagene taroretcel-lwey (ENCELTO) as the first therapy for Macular Telangiectasia type 2, with US launch slated for June 2025.

Global Retinal Biologics Market Report Scope

As per the report's scope, biologics are generally produced from living organisms such as microorganisms or animal or plant cells. Retinal biologics refer to bioengineered molecules implanted inside the eyes to heal chronic retinal diseases. The Retinal Biologics Market is Segmented by Drug Class (VEGF-A Antagonist, TNF-a Inhibitor), Disease Indication (Macular Degeneration, Diabetic Retinopathy, Uveitis, Others), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The report offers the value (in USD million) for the above segments. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (USD million) for the above segments.

| VEGF-A Antagonists |

| Bispecific VEGF/Ang-2 Inhibitors |

| Complement Inhibitors |

| TNF-? Inhibitors |

| Gene Therapies |

| Others |

| Monoclonal Antibodies |

| Fusion Proteins |

| Antibody Fragments |

| Gene Therapy Vectors |

| RNA-based Biologics |

| Age-Related Macular Degeneration (AMD) |

| Diabetic Retinopathy |

| Uveitis |

| Other Retinal Disorders |

| Intravitreal Injection |

| Suprachoroidal Injection |

| Sustained-Release Implant |

| Topical Delivery |

| Other Routes |

| Hospital Pharmacies |

| Specialty Clinics |

| Retail & Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | VEGF-A Antagonists | |

| Bispecific VEGF/Ang-2 Inhibitors | ||

| Complement Inhibitors | ||

| TNF-? Inhibitors | ||

| Gene Therapies | ||

| Others | ||

| By Molecule Type | Monoclonal Antibodies | |

| Fusion Proteins | ||

| Antibody Fragments | ||

| Gene Therapy Vectors | ||

| RNA-based Biologics | ||

| By Indication | Age-Related Macular Degeneration (AMD) | |

| Diabetic Retinopathy | ||

| Uveitis | ||

| Other Retinal Disorders | ||

| By Route of Administration | Intravitreal Injection | |

| Suprachoroidal Injection | ||

| Sustained-Release Implant | ||

| Topical Delivery | ||

| Other Routes | ||

| By Distribution Channel | Hospital Pharmacies | |

| Specialty Clinics | ||

| Retail & Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How are gene therapies changing long-term treatment expectations for retinal diseases?

Gene therapies offer the possibility of one-time dosing that sustains therapeutic protein expression, which could reduce the lifetime injection burden and reshape follow-up schedules for both clinicians and patients.

What impact do biosimilars have on the competitive landscape for anti-VEGF drugs?

Biosimilars introduce lower-cost alternatives that pressure brand-name pricing and encourage payers to revisit formulary placement, accelerating value-based contracting across ophthalmology.

Why are suprachoroidal injections gaining attention among retinal specialists?

Delivering drug into the suprachoroidal space can localize exposure to posterior tissues while minimizing anterior-segment complications, potentially improving safety profiles and dosing flexibility.

How do step-therapy requirements influence access to premium retinal biologics?

Many commercial plans mandate initial use of low-cost bevacizumab before covering branded agents, delaying uptake of newer biologics and affecting early visual outcomes for eligible patients.

What role do specialty clinics play in expanding access to retinal biologics?

Dedicated retinal centers streamline injection workflows, offer research participation opportunities, and provide consistent follow-up care, making them pivotal in delivering advanced therapies outside hospital settings.

Why is sterile fill-finish capacity considered a bottleneck in biologic supply chains?

Rapid Rise in Retinal Disease Burden & Diabetic Population Accelerated R&D Output & FDA/EMA Approvals of Novel Biologics Ageing Demographics Driving AMD Cases Strong Clinical Adoption of Anti-VEGF Injections Long-Acting Delivery Platforms Unlocking New Patient Pools Payer-Led Biosimilar Uptake in Cost-Sensitive Regions

Page last updated on: